Power Muirhead Mean Operators for Interval-Valued Linear Diophantine Fuzzy Sets and Their Application in Decision-Making Strategies

,

,

and

and

Abstract

:1. Introduction

- The pair includes interval-valued MG and NMG. The IV-IFS approach delivers the following result: . Hence, the technique of IV-IFS creates in this case a problem for experts.

- Similarly, the pair includes interval-valued MG and NMG. The IV-PFS approach gives the result: . Hence, the technique of IV-PFS creates a problem for experts.

- The pair includes the interval-valued MG and NMG, and the IV-QROFS approach delivers the following result: for any value of . In this case, the result by the IV-QROFS technique is problematic for experts.

- As already seen, the data cannot be resolved by the IV-IFS technique, while the IV-PFS technique delivers the result: . It means that IV-PFS is preferable over IV-IFS.

- The data cannot be resolved by IV-PFS, but the IV-QROFS technique gives the result: . Hence, the IV-QROFS technique is preferable over IV-IFS and IV-PFS.

- The data , could not be resolved by means of the IV-QROFS technique, while the IV-LDFS technique delivers by fixing the value of the reference parameter in the form . It means that the technique of IV-LDFS is preferable over IV-IFS, IV-PFS, and IV-QROFS.

- Analysis of the IV-LDF settings and use of their algebraic laws.

- Introduction of the IV-LDFPMM and IV-LDFWPMM operators, and discussion of some special properties and results.

- Demonstration of the beneficial optimum by using the MADM approach through examples.

- Demonstration of the advantages through a comparative analysis and geometrical interpretations.

2. Preliminaries

- 1.

- ;

- 2.

- ;

- 3.

- , if.

3. Interval-Valued Linear Diophantine Fuzzy Sets

- 1.

- If, then;

- 2.

- If, then;

- (i)

- If, then;

- (ii)

- If, then;

4. Power Muirhead Mean (MM) Operators under the IV-LDFSs

- 1.

- ;

- 2.

- ;

- 3.

- , if.

5. Multi-Attribute Decision-Making (MADM) Procedure under the Power MM Based on IV-LDFNs

5.1. An Illustrative Example

5.1.1. Start with the Chief Executive Officer

5.1.2. Review the Company Business Model

5.1.3. Consider the Competitive Advantages of a Company

5.1.4. Examine Revenue Trends and Price History

5.1.5. Assess Net Income Growth Year to Year

5.1.6. Examine the Profit Margin

5.1.7. Compare Debt-to-Equity Ratio

5.1.8. Analyze Price-to-Earnings (P/E) Ratio

- : Car Enterprise.

- : Computer Enterprise.

- : TV Enterprise.

- : Food Enterprise.

- : Laptop Enterprise.

- : Growth Analysis.

- : Social Impact Analysis.

- : Political Impact Analysis.

- : Environmental Impact Analysis.

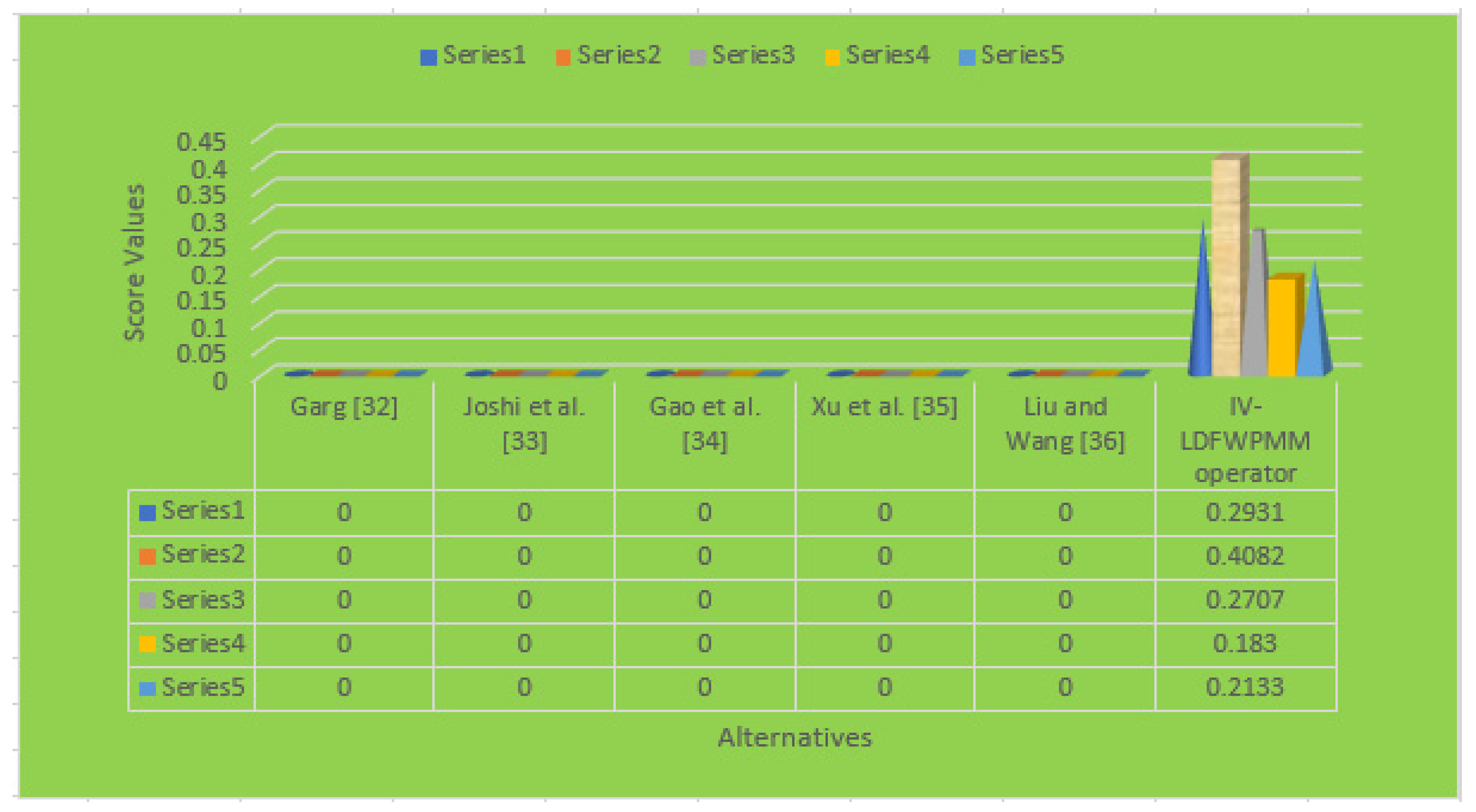

5.2. Comparative Analysis

6. Conclusions

- The principle of IV-LDFS and its algebraic laws were introduced.

- The IV-LDFPMM and IV-LDFWPMM operators were introduced and their properties discussed to determine the strength and consistency of the operators.

- A MADM technique is presented in combination with the introduced operators, and the numerical examples demonstrated its advantages.

- Finally, a comparative analysis of the presented and other operators was discussed.

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Zadeh, L.A. Fuzzy sets. Infor. Control 1965, 8, 338–353. [Google Scholar] [CrossRef] [Green Version]

- Atanassov, K. Intuitionistic fuzzy sets. Fuzzy Sets Syst. 1986, 20, 87–96. [Google Scholar] [CrossRef]

- Bloch, I. Lattices of fuzzy sets and bipolar fuzzy sets, and mathematical morphology. Inf. Sci. 2011, 181, 2002–2015. [Google Scholar] [CrossRef]

- Muhammad, L.J.; Badi, I.; Haruna, A.A.; Mohammed, I.A. Selecting the Best Municipal Solid Waste Management Techniques in Nigeria Using Multi Criteria Decision Making Techniques. Rep. Mech. Eng. 2021, 2, 180–189. [Google Scholar] [CrossRef]

- Karamaşa, Ç.; Karabasevic, D.; Stanujkic, D.; Kookhdan, A.; Mishra, A.; Ertürk, M. An extended single-valued neutrosophic AHP and MULTIMOORA method to evaluate the optimal training aircraft for flight training organizations. Facta Univ. Ser. Mech. Eng. 2021, 19, 555–578. [Google Scholar] [CrossRef]

- Ramakrishnan, K.R.; Chakraborty, S. A cloud TOPSIS model for green supplier selection. Facta Univ. Ser. Mech. Eng. 2020, 18, 375–397. [Google Scholar] [CrossRef]

- Milosevic, T.; Pamucar, D.; Chatterjee, P. Model for selecting a route for the transport of hazardous materials using a fuzzy logic system. Mil. Tech. Cour. 2021, 69, 355–390. [Google Scholar]

- Milovanovic, V.R.; Aleksic, A.V.; Sokolovic, V.S.; Milenkov, M.A. Uncertainty modeling using intuitionistic fuzzy numbers. Mil. Tech. Cour. 2021, 69, 905–929. [Google Scholar]

- Yang, J.; Yao, Y. A three-way decision-based construction of shadowed sets from Atanassov intuitionistic fuzzy sets. Inf. Sci. 2021, 577, 1–21. [Google Scholar] [CrossRef]

- Jana, C.; Pal, M. Application of bipolar intuitionistic fuzzy soft sets in decision-making problem. Int. J. Fuzzy Syst. Appl. IJFSA 2018, 7, 32–55. [Google Scholar] [CrossRef]

- Yager, R.R. Pythagorean membership grades in multicriteria decision making. IEEE Trans. Fuzzy Syst. 2013, 22, 958–965. [Google Scholar] [CrossRef]

- Garg, H. A novel improved accuracy function for interval-valued Pythagorean fuzzy sets and their applications in the decision-making process. Int. J. Intell. Syst. 2017, 32, 1247–1260. [Google Scholar] [CrossRef]

- Peng, X.; Yang, Y. Fundamental properties of interval-valued Pythagorean fuzzy aggregation operators. Int. J. Intell. Syst. 2016, 31, 444–487. [Google Scholar] [CrossRef]

- Naeem, K.; Riaz, M.; Afzal, D. Pythagorean m-polar Fuzzy Sets and TOPSIS method for the Selection of Advertisement Mode. J. Intell. Fuzzy Syst. 2019, 37, 8441–8458. [Google Scholar] [CrossRef]

- Riaz, M.; Naeem, K.; Afzal, D. Pythagorean m-polar fuzzy soft sets with TOPSIS method for MCGDM. Punjab Univ. J. Math. 2020, 52, 21–46. [Google Scholar]

- Chen, T.Y. New Chebyshev distance measures for Pythagorean fuzzy sets with applications to multiple criteria decision analysis using an extended ELECTRE approach. Expert Syst. Appl. 2020, 147, 113164–113178. [Google Scholar] [CrossRef]

- Yager, R.R. Generalized orthopair fuzzy sets. IEEE Trans. Fuzzy Syst. 2016, 25, 1222–1230. [Google Scholar] [CrossRef]

- Garg, H. A new possibility degree measure for interval-valued q-rung orthopair fuzzy sets in decision-making. Int. J. Intell. Syst. 2021, 36, 526–557. [Google Scholar] [CrossRef]

- Liu, Z.; Wang, X.; Li, L.; Zhao, X.; Liu, P. Q-rung orthopair fuzzy multiple attribute group decision-making method based on normalized bidirectional projection model and generalized knowledge-based entropy measure. J. Ambient Intell. Humaniz. Comput. 2021, 12, 2715–2730. [Google Scholar] [CrossRef]

- Khan, M.J.; Kumam, P.; Shutaywi, M. Knowledge measure for the q-rung orthopair fuzzy sets. Int. J. Intell. Syst. 2021, 36, 628–655. [Google Scholar] [CrossRef]

- Papadakis, V.M.; Lioukas, S.; Chambers, D. Strategic decision-making processes: The role of management and context. Strateg. Manag. J. 1998, 19, 115–147. [Google Scholar] [CrossRef]

- Kushwaha, D.K.; Panchal, D.; Sachdeva, A. Risk analysis of cutting system under intuitionistic fuzzy environment. Rep. Mech. Eng. 2020, 1, 162–173. [Google Scholar] [CrossRef]

- Garg, H. CN-q-ROFS: Connection number-based q-rung orthopair fuzzy set and their application to the decision-making process. Int. J. Intell. Syst. 2021, 36, 3106–3143. [Google Scholar] [CrossRef]

- Sarkar, A.; Biswas, A. Dual hesitant q-rung orthopair fuzzy Dombi t-conorm and t-norm based Bonferroni mean operators for solving multicriteria group decision-making problems. Int. J. Intell. Syst. 2021, 36, 3293–3338. [Google Scholar] [CrossRef]

- Liu, D.; Huang, A. Consensus reaching process for fuzzy behavioral TOPSIS method with probabilistic linguistic q-rung orthopair fuzzy set based on correlation measure. Int. J. Intell. Syst. 2020, 35, 494–528. [Google Scholar] [CrossRef]

- Ali, M.I. Another view on q-rung orthopair fuzzy sets. Int. J. Intell. Syst. 2018, 33, 2139–2153. [Google Scholar] [CrossRef]

- Riaz, M.; Hashmi, M.R. Linear Diophantine fuzzy set and its applications towards multi-attribute decision-making problems. J. Intell. Fuzzy Syst. 2019, 37, 5417–5439. [Google Scholar] [CrossRef]

- Almagrabi, A.O.; Abdullah, S.; Shams, M.; Al-Otaibi, Y.D.; Ashraf, S. A new approach to q-linear Diophantine fuzzy emergency decision support system for COVID19. J. Ambient. Intell. Humaniz. Comput. 2021, 1–27. [Google Scholar] [CrossRef]

- Ayub, S.; Shabir, M.; Riaz, M.; Aslam, M.; Chinram, R. Linear Diophantine Fuzzy Relations and Their Algebraic Properties with Decision Making. Symmetry 2021, 13, 945. [Google Scholar] [CrossRef]

- Parimala, M.; Jafari, S.; Riaz, M.; Aslam, M. Applying the Dijkstra Algorithm to Solve a Linear Diophantine Fuzzy Environment. Symmetry 2021, 13, 1616. [Google Scholar] [CrossRef]

- Atanassov, K.T.; Gargov, G. Interval-valued intuitionistic fuzzy sets. Fuzzy Sets Syst. 1989, 31, 343–349. [Google Scholar] [CrossRef]

- Garg, H. A novel accuracy function under interval-valued Pythagorean fuzzy environment for solving multicriteria decision-making problems. J. Intell. Fuzzy Syst. 2016, 31, 529–540. [Google Scholar] [CrossRef]

- Joshi, B.P.; Singh, A.; Bhatt, P.K.; Vaisla, K.S. Interval-valued q-rung orthopair fuzzy sets and their properties. J. Intell. Fuzzy Syst. 2018, 35, 5225–5230. [Google Scholar] [CrossRef]

- Gao, H.; Ju, Y.; Zhang, W.; Ju, D. Multi-Attribute Decision-Making Method Based on Interval-Valued q-Rung Orthopair Fuzzy Archimedean Muirhead Mean Operators. IEEE Access 2019, 7, 74300–74315. [Google Scholar] [CrossRef]

- Xu, W.; Shang, X.; Wang, J.; Li, W. A novel approach to multi-attribute group decision-making based on interval-valued intuitionistic fuzzy power Muirhead mean. Symmetry 2019, 11, 441. [Google Scholar] [CrossRef] [Green Version]

- Liu, P.; Wang, P. Some improved linguistic intuitionistic fuzzy aggregation operators and their applications to multiple attribute decision making. Int. J. Inf. Technol. Decis. Mak. 2017, 16, 817–850. [Google Scholar] [CrossRef]

- Riaz, M.; Hashmi, M.R. Soft rough Pythagorean m-polar fuzzy sets and Pythagorean m-polar fuzzy soft rough sets with application to decision-making. Comput. Appl. Math. 2020, 39, 1–36. [Google Scholar] [CrossRef]

- Naeem, K.; Riaz, M.; Karaaslan, F. Some novel features of Pythagorean m-polar fuzzy sets with applications. Complex Intell. Syst. 2021, 7, 459–475. [Google Scholar] [CrossRef]

- Mahmoodzadeh, S.; Shahrabi, J.; Pariazar, M.; Zaeri, M.S. Project selection by using fuzzy AHP and TOPSIS technique. World Acad. Sci. Eng. Technol. 2007, 30, 333–338. [Google Scholar]

- Liu, P.; Zhu, B.; Wang, P. A multi-attribute decision-making approach based on spherical fuzzy sets for Yunnan Baiyao’s R&D project selection problem. Int. J. Fuzzy Syst. 2019, 21, 2168–2191. [Google Scholar]

- Karaaslan, F.; Dawood, M.A.D. Complex T-spherical fuzzy Dombi aggregation operators and their applications in multiple-criteria decision-making. Complex Intell. Syst. 2021, 7, 2711–2734. [Google Scholar] [CrossRef] [PubMed]

- Nasir, A.; Jan, N.; Yang, M.S.; Khan, S.U. Complex T-spherical fuzzy relations with their applications in economic relationships and international trades. IEEE Access 2021, 9, 66115–66131. [Google Scholar] [CrossRef]

- Ali, M.; Smarandache, F. Complex neutrosophic set. Neural Comput. Appl. 2017, 28, 1817–1834. [Google Scholar] [CrossRef] [Green Version]

- Dat, L.Q.; Thong, N.T.; Ali, M.; Smarandache, F.; Abdel-Basset, M.; Long, H.V. Linguistic approaches to interval complex neutrosophic sets in decision making. IEEE Access 2019, 7, 38902–38917. [Google Scholar] [CrossRef]

- Quek, S.G.; Broumi, S.; Selvachandran, G.; Bakali, A.; Talea, M.; Smarandache, F. Some results on the graph theory for complex neutrosophic sets. Symmetry 2018, 10, 190. [Google Scholar] [CrossRef] [Green Version]

- Singh, P.K. Complex neutrosophic concept lattice and its applications to air quality analysis. Chaos Solitons Fractals 2018, 109, 206–213. [Google Scholar] [CrossRef] [Green Version]

- Gao, Y.; Zhang, Z. Consensus reaching with non-cooperative behavior management for personalized individual semantics-based social network group decision making. J. Oper. Res. Soc. 2021, 1–18. [Google Scholar] [CrossRef]

- Zhang, Z.; Li, Z.; Gao, Y. Consensus reaching for group decision making with multi-granular unbalanced linguistic information: A bounded confidence and minimum adjustment-based approach. Inf. Fusion 2021, 74, 96–110. [Google Scholar] [CrossRef]

- Zhang, Z.; Guo, C.; Martínez, L. Managing multi granular linguistic distribution assessments in large-scale multiattribute group decision making. IEEE Trans. Syst. Man Cybern. Syst. 2016, 47, 3063–3076. [Google Scholar] [CrossRef] [Green Version]

- Zhang, Z.; Kou, X.; Yu, W.; Gao, Y. Consistency improvement for fuzzy preference relations with self-confidence: An application in two-sided matching decision making. J. Oper. Res. Soc. 2021, 72, 1914–1927. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Symbol | Name | Symbol | Name | Symbol | Name |

|---|---|---|---|---|---|

| Universal set | Element of | Truth Grade | |||

| Falsity grade | Reference Parameter for Truth grade | Reference Parameter for Falsity grade | |||

| Scaler element | Accuracy value | Score value |

| AR− 1 | AR− 2 | |

|---|---|---|

| AT− 1 | (([0.6,0.7], [0.5,0.6]), ([0.3,0.4], [0.4,0.5])) | (([0.61,0.71], [0.51,0.61]), ([0.31,0.41], [0.41,0.51])) |

| AT− 2 | (([0.7,0.8], [0.4,0.5]), ([0.4,0.4], [0.5,0.5])) | (([0.71,0.81], [0.41,0.51]), ([0.41,0.41], [0.51,0.51])) |

| AT− 3 | (([0.1,0.9], [0.1,0.3]), ([0.2,0.3], [0.2,0.6])) | (([0.11,0.91], [0.11,0.31]), ([0.21,0.31], [0.21,0.61])) |

| AT− 4 | (([0.4,0.8], [0.6,0.8]), ([0.1,0.2], [0.3,0.4])) | (([0.41,0.81], [0.61,0.81]), ([0.11,0.21], [0.31,0.41])) |

| AT− 5 | (([0.1,0.6], [0.3,0.4]), ([0.4,0.5], [0.1,0.2])) | (([0.11,0.61], [0.31,0.41]), ([0.41,0.51], [0.11,0.21])) |

| AR− 3 | AR− 4 | |

| AT− 1 | (([0.62,0.72], [0.52,0.62]), ([0.32,0.42], [0.42,0.52])) | (([0.63,0.73], [0.53,0.63]), ([0.33,0.43], [0.43,0.53])) |

| AT− 2 | (([0.72,0.82], [0.42,0.52]), ([0.42,0.42], [0.52,0.52])) | (([0.73,0.83], [0.43,0.53]), ([0.43,0.43], [0.5,0.53])) |

| AT− 3 | (([0.12,0.92], [0.12,0.32]), ([0.22,0.32], [0.22,0.62])) | (([0.13,0.93], [0.13,0.33]), ([0.23,0.33], [0.23,0.63])) |

| AT− 4 | (([0.42,0.82], [0.62,0.82]), ([0.12,0.22], [0.32,0.42])) | (([0.43,0.83], [0.63,0.83]), ([0.13,0.23], [0.33,0.43])) |

| AT− 5 | (([0.12,0.62], [0.32,0.42]), ([0.42,0.52], [0.12,0.22])) | (([0.13,0.63], [0.33,0.43]), ([0.43,0.53], [0.13,0.23])) |

| IV–LDFWPMM | |

|---|---|

| AT− 1 | (([0.6119,0.7119], [0.5579,0.6494]), ([0.3118,0.4118], [0.4661,0.5579])) |

| AT− 2 | (([0.7137,0.8132], [0.4698,0.5612]), ([0.4144,0.4143], [0.5612,0.5522])) |

| AT− 3 | (([0.1142,0.9130], [0.1871,0.3792]), ([0.2152,0.3156], [0.2852,0.5440])) |

| AT− 4 | (([0.4142,0.8131], [0.6520,0.8333]), ([0.1132,0.2138], [0.3770,0.4694])) |

| AT− 5 | (([0.1136,0.6144], [0.3780,0.4704]), ([0.4148,0.5147], [0.1860,0.2840])) |

| Methods | Score Values | Ranking Values |

|---|---|---|

| Garg [32] | Cannot be Formulated | Cannot be Formulated |

| Joshi et al. [33] | Cannot be Formulated | Cannot be Formulated |

| Gao et al. [34] | Cannot be Formulated | Cannot be Formulated |

| Xu et al. [35] | Cannot be Formulated | Cannot be Formulated |

| Liu and Wang [36] | Cannot be Formulated | Cannot be Formulated |

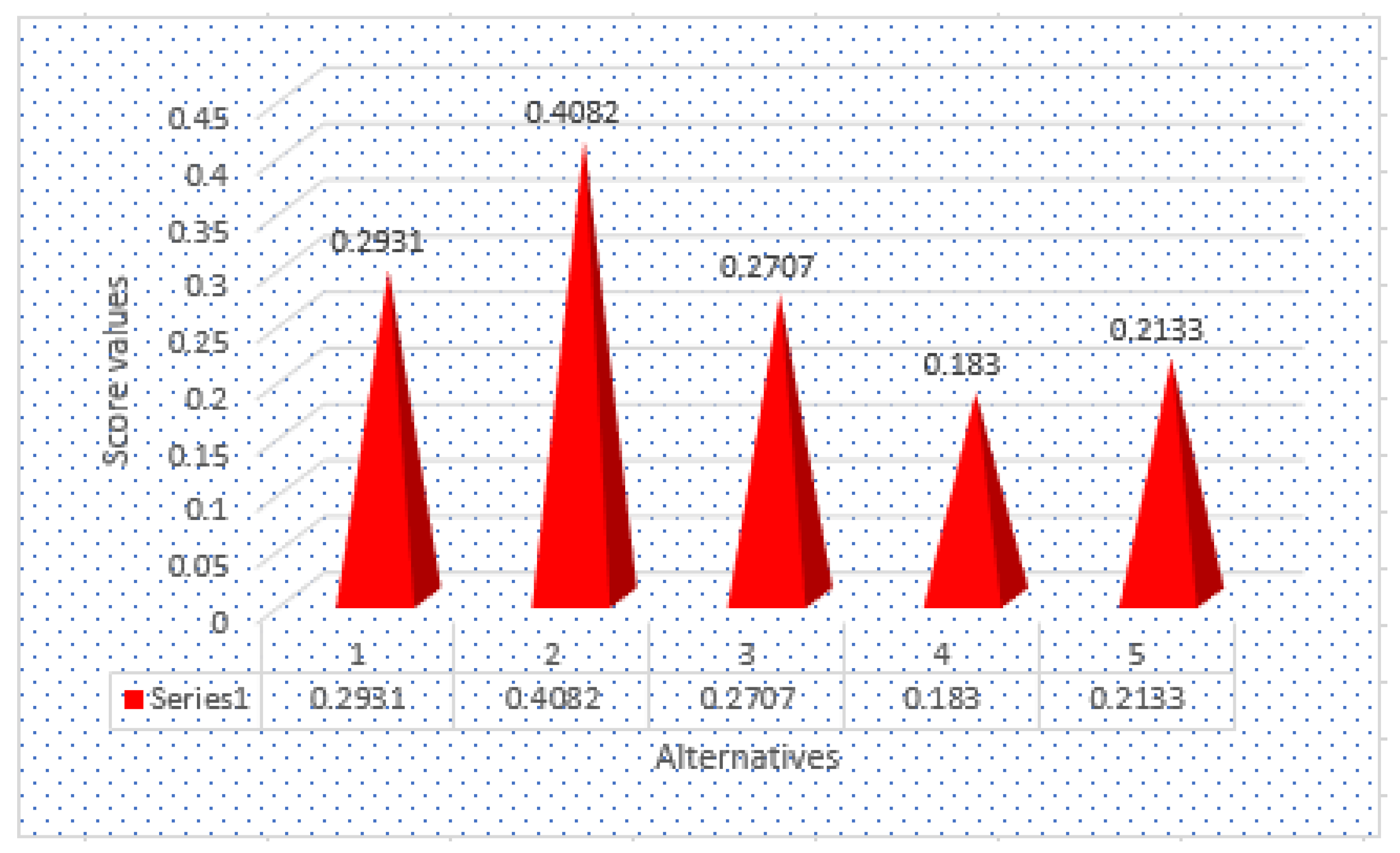

| IV-LDFWPMM Operator | 0.2931, 0.4082, 0.2707, 0.1830, 0.2133 | AT− 2 > AT − 1 > AT − 3 > AT − 5 > AT − 4 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Mahmood, T.; Haleemzai, I.; Ali, Z.; Pamucar, D.; Marinkovic, D. Power Muirhead Mean Operators for Interval-Valued Linear Diophantine Fuzzy Sets and Their Application in Decision-Making Strategies. Mathematics 2022, 10, 70. https://doi.org/10.3390/math10010070

Mahmood T, Haleemzai I, Ali Z, Pamucar D, Marinkovic D. Power Muirhead Mean Operators for Interval-Valued Linear Diophantine Fuzzy Sets and Their Application in Decision-Making Strategies. Mathematics. 2022; 10(1):70. https://doi.org/10.3390/math10010070

Chicago/Turabian StyleMahmood, Tahir, Izatmand Haleemzai, Zeeshan Ali, Dragan Pamucar, and Dragan Marinkovic. 2022. "Power Muirhead Mean Operators for Interval-Valued Linear Diophantine Fuzzy Sets and Their Application in Decision-Making Strategies" Mathematics 10, no. 1: 70. https://doi.org/10.3390/math10010070