The Effect of Corporate Governance Elements on Corporate Social Responsibility (CSR) Disclosure: An Empirical Evidence from Listed Companies at KSE Pakistan

Abstract

:1. Introduction

1.1. Why do Firms Engage in CSR?

1.2. CSR Reporting in Pakistan

2. Literature Review

2.1. Theoretical Framework

2.2. Corporate Governance Elements and CSR Disclosure

2.2.1. Board Size

2.2.2. Independent Directors

2.2.3. Women Directors

2.2.4. Foreign Nationals

2.2.5. Ownership Concentration

2.2.6. Institutional Ownership

2.3. Control Variables

2.3.1. Company Size

2.3.2. Profitability

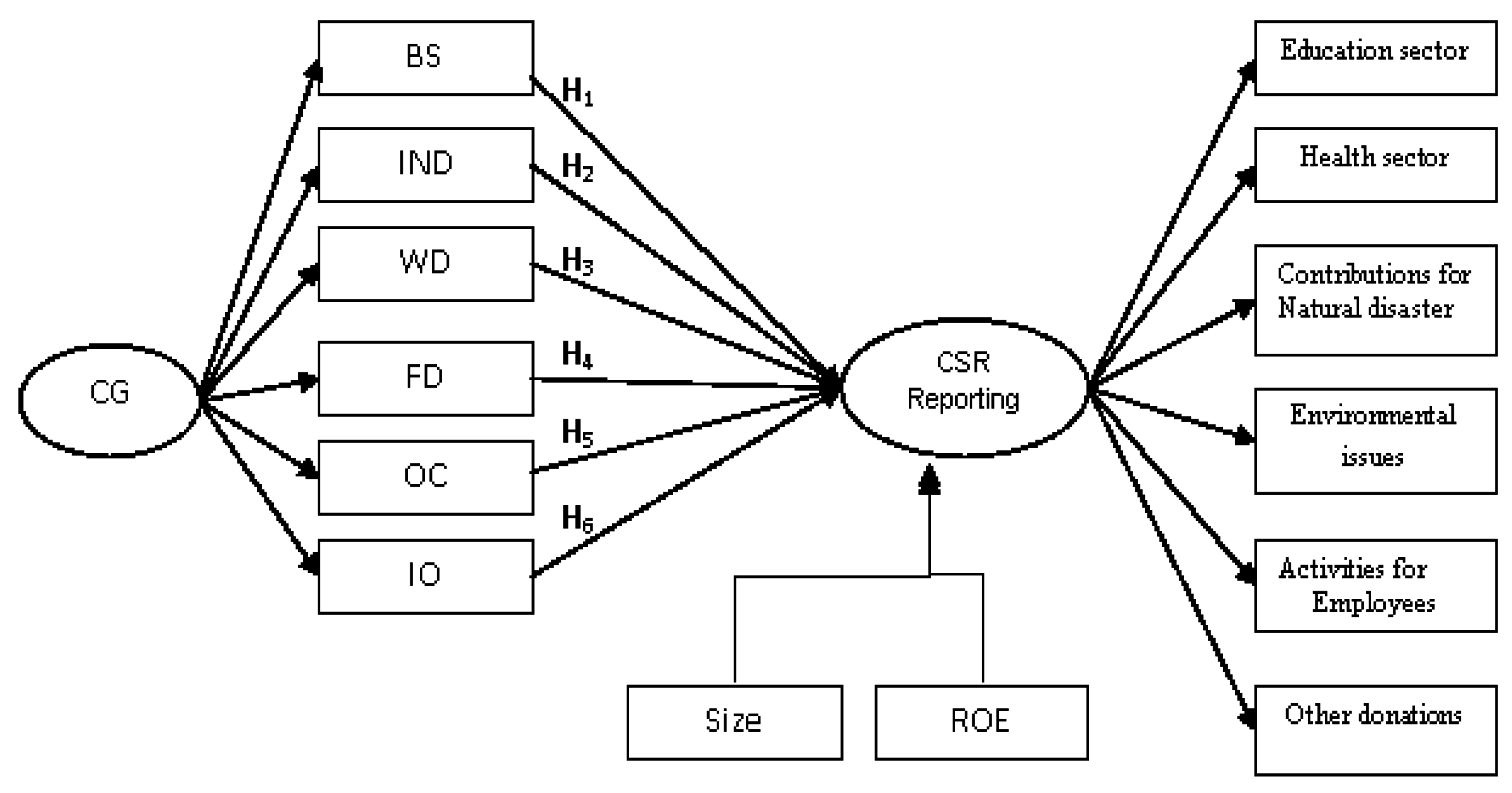

3. Research Design and Methodology

3.1. Sample Size and Data

3.2. Measurement of Variables

3.2.1. Dependent Variable—CSR Disclosure

3.2.2. Independent Variables

{kind=link}

| Sr. # | Variable | Description | Symbol | Measurement |

|---|---|---|---|---|

| 1 | X1 | Board size | BS | Total directors |

| 2 | X2 | Composition of independent directors | IND | Percentage of independent directors to total directors on the board |

| 3 | X3 | Composition of women directors | WD | Percentage of women directors to total directors on the board |

| 4 | X4 | Composition of foreign directors | FD | Percentage of non-Pakistani directors to total directors on the board |

| 5 | X5 | Ownership concentration | OC | Sum of squares of highest five shareholdings’ percentages |

| 6 | X6 | Institution ownership | IO | Sum of percentages of institutions’ ownership |

3.2.3. Control Variables

| Sr. # | Variables | Description | Symbol | Measurement |

|---|---|---|---|---|

| 1 | X7 | Size | Sales | Size based on total Sales |

| 2 | X8 | Profitability | ROE | Return on equity = Net profit after tax/total equity |

3.3. Regression Model Equation

3.4. CSR Disclosure Index (CSRDI)

4. Data Analysis and Results

4.1. Descriptive Analysis

| Variables | N | 2011 | 2010 | 2009 | 2008 | 2007 | |||||

| Mean | Std. Deviation | Mean | Std. Deviation | Mean | Std. Deviation | Mean | Std. Deviation | Mean | Std. Deviation | ||

| BS | 100 | 8.79 | 1.986 | 8.78 | 2.082 | 8.72 | 1.918 | 8.72 | 1.918 | 8.77 | 1.916 |

| IND | 100 | 44.15 | 32.996 | 46.72 | 32.461 | 44.8 | 32.196 | 44.8 | 32.196 | 44.64 | 32.696 |

| FD | 100 | 14.34 | 18.239 | 13.35 | 18.049 | 13.96 | 19.041 | 13.96 | 19.041 | 15.43 | 22.763 |

| WD | 100 | 5.46 | 11.154 | 4.69 | 10.626 | 5.76 | 11.118 | 5.76 | 11.118 | 5.46 | 10.916 |

| OC | 100 | 3138.15 | 2587.096 | 2844.63 | 2245.467 | 2950.86 | 2268.515 | 2950.86 | 2268.515 | 2940.22 | 2319.934 |

| IO | 100 | 71.41 | 28.155 | 70.6 | 28.89 | 70.54 | 27.069 | 70.54 | 27.069 | 69.51 | 27.853 |

| Size | 100 | 41,966,846,875 | 90,791,374,024 | 35,281,800,996 | 81,302,729,747 | 30,689,433,583 | 68,200,418,806 | 30,689,433,583 | 68,200,418,806 | 21,322,422,293 | 41,697,873,392 |

| ROE | 100 | 21.82 | 45.14047 | 43.2718 | 279.09081 | 15.6496 | 220.45856 | 15.6496 | 220.45856 | −1.179 | 275.2021 |

| CSRDI | 100 | 30.07 | 15.002 | 30.2 | 15.024 | 27.62 | 14.219 | 27.62 | 14.219 | 23.52 | 13.985 |

4.2. Multivariate Analysis

4.2.1. Correlation Matrix

| Variables | 2011 | 2010 | 2009 | 2008 | 2007 |

|---|---|---|---|---|---|

| CSRDI | CSRDI | CSRDI | CSRDI | CSRDI | |

| CSRDI | 1 | 1 | 1 | 1 | 1 |

| Sig (2 Tailed) | |||||

| BS | 0.384 *** | 0.374 *** | 0.383 *** | 0.357 *** | 0.370 *** |

| Sig (2 Tailed) | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| IND | −0.211 ** | −0.278 ** | −0.177 * | −0.157 | −0.162 |

| Sig (2 Tailed) | 0.035 | 0.005 | 0.078 | 0.119 | 0.109 |

| FD | 0.103 | 0.102 | 0.068 | 0.032 | −0.003 |

| Sig (2 Tailed) | 0.308 | 0.311 | 0.499 | 0.755 | 0.980 |

| WD | −0.271 *** | −0.244 ** | −0.196 * | −0.159 | −0.246 ** |

| Sig (2 Tailed) | 0.006 | 0.014 | 0.051 | 0.114 | 0.014 |

| OC | 0.244 ** | 0.246 ** | 0.360 *** | 0.331 *** | 0.360 *** |

| Sig (2 Tailed) | 0.015 | 0.014 | 0.000 | 0.001 | 0.000 |

| IO | 0.373 *** | 0.452 *** | 0.461 *** | 0.390 *** | 0.469 *** |

| Sig (2 Tailed) | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| Size | 0.323 *** | 0.301 *** | 0.321 *** | 0.288 *** | 0.412 *** |

| Sig (2 Tailed) | 0.001 | 0.002 | 0.001 | 0.004 | 0.000 |

| ROE | 0.235 ** | 0.177 * | 0.002 | 0.167* | 0.104 |

| Sig (2 Tailed) | 0.018 | 0.079 | 0.986 | 0.096 | 0.307 |

4.2.2. Regression Analysis

| Variables | 2011 | 2010 | 2009 | 2008 | 2007 | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Beta Coef | t-Value | p-Value | Beta Coef | t-Value | p-Value | Beta Coef | t-Value | p-Value | Beta Coef | t-Value | p-Value | Beta Coef | t-Value | p-Value | |

| Constant | 8.397 | 1.154 | 0.250 | 6.952 | 1.024 | 0.310 | 3.899 | 0.579 | 0.560 | 2.485 | 0.346 | 0.730 | 3.311 | 0.502 | 0.620 |

| BS | 1.427 | 1.899 * | 0.060 | 1.541 | 2.342 ** | 0.020 | 1.323 | 1.899 * | 0.060 | 1.450 | 1.885 * | 0.060 | 1.137 | 1.716 * | 0.090 |

| IND | −0.031 | −0.730 | 0.470 | −0.070 | −1.590 | 0.120 | −0.040 | −0.940 | 0.350 | −0.060 | −1.530 | 0.130 | −0.040 | −1.180 | 0.240 |

| FD | 0.006 | 0.071 | 0.940 | −0.010 | −0.130 | 0.900 | −0.070 | −1.010 | 0.320 | −0.050 | −0.640 | 0.520 | −0.040 | −0.770 | 0.450 |

| WD | −0.225 | −1.747 * | 0.080 | −0.210 | −1.689 * | 0.100 | −0.190 | −1.550 | 0.120 | −0.050 | −0.430 | 0.670 | −0.080 | −0.750 | 0.460 |

| OC | 0.000 | 0.590 | 0.560 | 0.001 | 0.789 | 0.430 | 0.001 | 1.847 * | 0.070 | 0.001 | 1.781 * | 0.080 | 0.001 | 2.012 ** | 0.050 |

| IO | 0.123 | 2.151 ** | 0.030 | 0.163 | 3.050 *** | 0.000 | 0.162 | 2.778 *** | 0.010 | 0.122 | 2.151 ** | 0.030 | 0.119 | 2.251 ** | 0.030 |

| Size | 2.601 | 1.657 * | 0.100 | 2.208 | 1.319 | 0.190 | 3.164 | 1.663 * | 0.100 | 3.350 | 1.392 | 0.170 | 8.052 | 2.678 *** | 0.010 |

| ROE | 0.030 | 0.961 | 0.340 | 0.002 | 0.509 | 0.610 | 0.006 | 1.060 | 0.290 | 0.028 | 0.855 | 0.400 | 0.001 | 0.319 | 0.750 |

| Durbin Watson | 1.921 | 1.837 | 1.904 | 1.852 | 2.176 | ||||||||||

| R2 (%) | 30.6 | 36 | 36.3 | 29.5 | 37.9 | ||||||||||

| Adjusted R2 (%) | 24.5 | 30.3 | 30.7 | 23.3 | 32.4 | ||||||||||

| F Statistics | 5.021 | 6.389 | 6.488 | 4.752 | 6.863 | ||||||||||

| Significance | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | ||||||||||

5. Conclusions

5.1. Discussion

| Hypotdesis | 2011 | 2010 | 2009 | 2008 | 2007 |

| H1 | Accept | Accept | Accept | Accept | Accept |

| H2 | Reject | Reject | Reject | Reject | Reject |

| H3 | Reject | Reject | Reject | Reject | Reject |

| H4 | Reject | Reject | Reject | Reject | Reject |

| H5 | Reject | Reject | Accept | Accept | Accept |

| H6 | Accept | Accept | Accept | Accept | Accept |

| H7 | Accept | Accept | Accept | Reject | Accept |

| H8 | Reject | Reject | Reject | Reject | Reject |

5.2. Practical Implications, Limitations and Suggestions for Further Research

Author Contributions

Conflicts of Interest

Appendix A

| A: Contribution to health sector |

| 1 Health, safety & environment policy/measures |

| 2 HIV/AIDS assistance program |

| 3 Support to acid and dowry victims |

| 4 Donation of medical equipment in different medical hospitals |

| 5 Donation/work for cancer hospital |

| 6 Donation/facility of medical hospital (government/private) |

| B: Contribution to education sector |

| 7 Donation to the universities for constructing research center |

| 8 Scholarships to the research students of different universities |

| 9 Scholarship to employee’s children |

| 10 Granted fund for special education and rehabilitation |

| 11 Work for physical disabled students/employee |

| 12 Fund raising/supporting school/college/university education programs |

| 13 Donation/charity to trusts for the widows/orphans |

| 14 Internship/apprenticeship facilities for students |

| C: Activities for natural disaster |

| 15 Part time job facilities |

| 16 Efforts for reducing child labor |

| 17 Donation/work for any relief fund for the victims of natural disasters (river erosions/flood/earthquake) |

| 18 Donation/work for rehabilitation of homeless people due to natural disasters (river erosions/flood/earthquake) |

| D: Other donations |

| 19 Establishment of health care center for rural people/underprivileged |

| 20 Financial supports to the natural affected victims of neighboring countries |

| 21 Sponsoring of different national and international games and events |

| 22 Donation to different sports organizations |

| 23 Assistance to different Trusts who works for poor people of the society/social work |

| E: Activities for employees |

| 24 Employee training programs/expenses |

| 25 Career developments |

| 26 Employee benefits |

| 27 Compensation plan for employees |

| 28 Facilities to employee’s children/employee facilities |

| 29 Amount of budget allocation on employees training |

| 30 Cost of employees safety measures |

| 31 Information about support for day-care, maternity and paternity leave/family accommodation/mother health care center |

| F: Environmental issues |

| 32 Environmental protection measures |

| 33 Planting of trees to make the country green |

| 34 Support for public/private actions designed to protect the environment (e.g. CNG station establishment)/civil work |

| 35 Promoting environmental awareness to the community through promotional tools |

| G: Product/services statements |

| 36 Explanation of major products/services/segments/projects |

| 37 Product/service quality policy/improvement/assurance |

| 38 Improvement of customer service/focus |

| 39 Receipt of awards (local or international) for CSR activities |

| 40 Information for conducting research/development on the company’s products |

Appendix B

| Sr. # | Company Names | No. of Items Disclosed (2011) | No. of Items Disclosed (2010) | No. of Items Disclosed (2009) | No. of Items Disclosed (2008) | No. of Items Disclosed (2007) |

|---|---|---|---|---|---|---|

| 1 | Oil & Gas Development Co. | 15 | 17 | 15 | 15 | 18 |

| 2 | Pak Petroleum | 24 | 25 | 26 | 24 | 25 |

| 3 | Nestle Pakistan Ltd. | 20 | 21 | 21 | 21 | 20 |

| 4 | MCB Bank | 20 | 19 | 20 | 20 | 5 |

| 5 | Fauji Fertilizer | 22 | 20 | 20 | 17 | 17 |

| 6 | Habib Bank Limited | 10 | 10 | 9 | 7 | 6 |

| 7 | UniLever Pak | 13 | 14 | 14 | 15 | 14 |

| 8 | United Bank | 15 | 13 | 12 | 5 | 5 |

| 9 | Pak Oilfields | 15 | 17 | 16 | 16 | 17 |

| 10 | National Bank Pak | 14 | 13 | 13 | 12 | 12 |

| 11 | Allied Bank Ltd. | 16 | 16 | 16 | 15 | 15 |

| 12 | P.T.C.L.A | 18 | 18 | 13 | 12 | 11 |

| 13 | Engro Corporation | 15 | 18 | 15 | 15 | 16 |

| 14 | National Foods | 14 | 17 | 18 | 10 | 9 |

| 15 | Fatima Fertilizer | 18 | 17 | 13 | ||

| 16 | Hub Power Co. | 13 | 14 | 5 | 5 | 9 |

| 17 | P.S.O | 22 | 20 | 19 | 18 | 23 |

| 18 | Standard Charter Bank | 11 | 11 | 11 | 11 | 11 |

| 19 | Lucky Cement | 22 | 20 | 19 | 3 | 3 |

| 20 | KotAddu Power | 7 | 6 | 9 | 5 | 8 |

| 21 | Fauji Fertilizer Bin | 10 | 12 | 14 | 4 | 4 |

| 22 | Colgate Palmolive | 4 | 4 | 4 | 4 | 4 |

| 23 | Attock Petroleum | 9 | 8 | 8 | 6 | 7 |

| 24 | Bank AL-Habib | 10 | 11 | 7 | 8 | 8 |

| 25 | Rafhan Maize | 18 | 13 | 13 | 9 | 10 |

| 26 | Meezan Bank Ltd. | 12 | 12 | 10 | 2 | 5 |

| 27 | Bank Al-Falah | 7 | 10 | 6 | 5 | 5 |

| 28 | Indus Motor Company | 20 | 19 | 19 | 17 | 17 |

| 29 | NIB Bank Limited | 6 | 6 | 6 | 6 | 6 |

| 30 | National Refinery | 11 | 7 | 8 | 9 | 10 |

| 31 | D.G.K. Cement | 6 | 10 | 3 | 3 | 3 |

| 32 | ICI Pakistan Ltd. | 19 | 21 | 16 | 19 | 16 |

| 33 | Habib Metropolitan | 10 | 14 | 10 | 10 | 10 |

| 34 | Sui South Gas | 21 | 16 | 13 | 17 | 17 |

| 35 | Unilever Food | 11 | 10 | 8 | 10 | 10 |

| 36 | Nishat Mills Limited | 9 | 7 | 7 | 7 | 7 |

| 37 | Ibrahim Fibers | 8 | 8 | 8 | 8 | 8 |

| 38 | Dawood Hercules | 3 | 14 | 18 | 16 | 18 |

| 39 | Millat Tractors | 12 | 9 | 8 | 9 | 9 |

| 40 | Pakistan International Container Terminal Ltd. | 16 | 16 | 16 | 12 | 10 |

| 41 | GlaxoSmithKline Pakistan | 18 | 19 | 15 | 15 | 15 |

| 42 | Bestway Cement | 16 | 17 | 16 | 16 | 16 |

| 43 | Dream world | 4 | 4 | 4 | 4 | 4 |

| 44 | Arif Habib Co. | 10 | 9 | 7 | 7 | 7 |

| 45 | Pak Tobacco | 12 | 15 | 16 | 15 | 14 |

| 46 | Lotte Pak PTA | 19 | 15 | 19 | 12 | 12 |

| 47 | Jahangir Siddiqiue and Company Limited | 2 | 3 | 11 | 8 | 3 |

| 48 | Askari Bank | 14 | 14 | 12 | 13 | 13 |

| 49 | Shell Pakistan Ltd. | 19 | 21 | 21 | 15 | 16 |

| 50 | Abbott Laboratories | 19 | 20 | 17 | 16 | 16 |

| 51 | Sui North Gas | 12 | 13 | 15 | 10 | 10 |

| 52 | EFU General Ins. | 12 | 11 | 11 | 4 | 4 |

| 53 | Atlas Honda Ltd. | 21 | 22 | 16 | 14 | 13 |

| 54 | Attock Refinery Ltd. | 22 | 21 | 23 | 21 | 19 |

| 55 | Faysal Bank | 11 | 14 | 8 | 5 | 5 |

| 56 | Byco Petroleum | 4 | 12 | 14 | 14 | 12 |

| 57 | Philip Morris Pak | 2 | 2 | 2 | 2 | 2 |

| 58 | AL-Ghazi Tractor | 12 | 17 | 12 | 15 | 15 |

| 59 | Tandlianwala Sugar | 2 | 2 | 2 | 2 | 2 |

| 60 | Adamjee Ins | 8 | 11 | 9 | 11 | 11 |

| 61 | Fauji Cement | 12 | 9 | 7 | 8 | 5 |

| 62 | Mari Gas Company | 25 | 24 | 18 | 17 | 17 |

| 63 | Packages Ltd. | 20 | 21 | 16 | 7 | 7 |

| 64 | K.E.S.C | 17 | 21 | 19 | 17 | 17 |

| 65 | Engro Polymer | 21 | 18 | 17 | 17 | 16 |

| 66 | Pak Suzuki Motor | 15 | 17 | 9 | 9 | 7 |

| 67 | Soneri Bank Ltd. | 8 | 8 | 8 | 6 | 5 |

| 68 | Indus Dyeing | 1 | 1 | 1 | 1 | 1 |

| 69 | Thal Limited | 18 | 17 | 13 | 14 | 15 |

| 70 | IGI Insurance Ltd. | 14 | 10 | 10 | 7 | 6 |

| 71 | Attock Cement | 12 | 14 | 17 | 15 | 15 |

| 72 | Universal Insurance Co. | 3 | 3 | 3 | 3 | 3 |

| 73 | Jubilee General Ins. | 14 | 14 | 13 | 13 | 13 |

| 74 | Ghani Glass Ltd. | 6 | 6 | 5 | 5 | 5 |

| 75 | Tri-Pack Films | 11 | 10 | 10 | 9 | 9 |

| 76 | P.I.A | 12 | 15 | 14 | 9 | 8 |

| 77 | Bawany Air Products | 4 | 3 | 2 | 2 | 2 |

| 78 | EFU Life Assurance Ltd. | 8 | 10 | 7 | 9 | 5 |

| 79 | Silk Bank Limited | 13 | 18 | 8 | 5 | 5 |

| 80 | Siemens Pakistan Ltd. | 17 | 18 | 12 | 12 | 14 |

| 81 | Nishat Chun Power | 1 | 1 | 1 | 1 | 1 |

| 82 | Clariant Pak | 10 | 9 | 14 | 14 | 13 |

| 83 | J.D.W.Sugar Mills | 11 | 10 | 10 | 19 | 3 |

| 84 | Nishat Power Ltd. | 7 | 3 | 3 | 3 | 3 |

| 85 | Pak Services | 13 | 12 | 11 | 11 | 11 |

| 86 | Siddiqsons Tin Plate Ltd. | 7 | 7 | 7 | 7 | 7 |

| 87 | Pak Reinsurance | 10 | 11 | 12 | 19 | 6 |

| 88 | Bata (Pak) Limited | 6 | 4 | 4 | 1 | 1 |

| 89 | Feroze 1888 Mills | 7 | 8 | 4 | 4 | 4 |

| 90 | PICIC Gro Fund | 2 | 2 | 2 | 2 | 2 |

| 91 | Murree Brewery | 6 | 4 | 4 | 4 | 6 |

| 92 | Security Paper | 14 | 14 | 15 | 16 | 15 |

| 93 | Media Times Ltd. | 3 | 3 | 3 | 3 | 3 |

| 94 | Al Abbas Cement | 5 | 2 | 2 | 2 | 3 |

| 95 | ShifaInt.Hospitals | 11 | 11 | 14 | 14 | 14 |

| 96 | Pakistan Cables | 11 | 10 | 9 | 10 | 12 |

| 97 | Netsol Technologies | 19 | 10 | 10 | 10 | 10 |

| 98 | Pace (Pak) Ltd. | 5 | 5 | 5 | 5 | 5 |

| 99 | Grays of Cambridge | 5 | 5 | 5 | 4 | 5 |

| 100 | Pak Telephone | 5 | 5 | 5 | 5 | 5 |

Appendix C

| Categories | 2011 | 2010 | 2009 | 2008 | 2007 | |||||

|---|---|---|---|---|---|---|---|---|---|---|

| Reporting Co. at least two items | No. of Words Reported | Reporting Co. at least two items | No. of Words Reported | Reporting Co. at least two items | No. of Words Reported | Reporting Co. at least two items | No. of Words Reported | Reporting Co. at least two items | No. of Words Reported | |

| A: Contribution to health sector | 57 | 668 | 57 | 652 | 48 | 504 | 42 | 425 | 42 | 408 |

| B: Contribution to education sector | 39 | 344 | 38 | 267 | 37 | 249 | 29 | 239 | 15 | 130 |

| C: Activities for natural disaster | 24 | 181 | 33 | 210 | 15 | 84 | 7 | 46 | 2 | 5 |

| D: Other donations | 36 | 249 | 35 | 231 | 33 | 229 | 28 | 161 | 28 | 68 |

| E: Activities for employees | 85 | 2069 | 60 | 1716 | 57 | 1517 | 79 | 1703 | 79 | 1560 |

| F: Environmental issues | 31 | 394 | 31 | 319 | 36 | 339 | 29 | 288 | 23 | 196 |

| G: Product/services statements | 78 | 417 | 77 | 390 | 77 | 338 | 76 | 326 | 72 | 285 |

| Total | 4322 | 3785 | 3260 | 3188 | 2652 | |||||

References

- L. Webb, J. Cohen, L. Nath, and D. Wood. “The Supply of Corporate Social Responsibility Disclosure among US Firms.” J. Bus. Ethics 84 (2009): 497–527. [Google Scholar] [CrossRef]

- J.I. Pearce, and J. Doh. “The High Impact of Collaborative Social Initiatives.” MIT Sloan Manag. Rev. 46 (2005): 30–38. [Google Scholar]

- C.A. Tilt. “The Content and Disclosure of Australian Corporate Environmental Policies.” Account. Audit. Accountable. J. 14 (2001): 190–212. [Google Scholar] [CrossRef]

- M. Newson, and C. Deegan. “Global Expectations and their Association with Corporate Social Disclosure Practices in Australia, Singapore and South Korea.” Int. J. Account. 37 (2002): 183–213. [Google Scholar] [CrossRef]

- R. Haniffa, and T. Cooke. “The Impact of Culture and Governance on Corporate Social Reporting.” J. Account. Public Policy 24 (2005): 391–430. [Google Scholar] [CrossRef]

- Y. Lim, M. Talha, J. Mohamaed, and A. Sallehuddin. “International Journal of Behavioral Accounting and Finance.” Corp. Soc. Responsib. Discl. Corp. Gov. Malays. 1 (2008): 67–89. [Google Scholar]

- C. Deegan, and B. Gordon. “A Study of the Environmental Disclosure Policies of Australian Corporation.” Account. Bus. Res. 26 (1996): 187–199. [Google Scholar] [CrossRef]

- D. Jamali, A. Safieddine, and M. Rabbath. “Corporate Governance and Corporate Social Responsibility Synergies and Interrelationships.” Corp. Gov. Int. Rev. 16 (2008): 443–459. [Google Scholar] [CrossRef]

- S. Mitra, S. Dhar, and K.M. Agrawal. “Assessment of Corporate Environmental Proactiveness.” South Asian J.Manag. 15 (2008): 99–135. [Google Scholar]

- M. Porter, and M. Kramer. “Strategy and Society: The Link between Competitive Advantage and Corporate Social Responsibility.” Harv. Bus. Rev. 84 (2006): 78–89. [Google Scholar] [PubMed]

- A. Mcwilliams, D. Siegel, and P. Wright. “Corporate Social Responsibility: Strategic Implications.” J. Manag. Stud. 43 (2006): 1–18. [Google Scholar] [CrossRef]

- G. Lantos. “The Boundaries of Strategic Corporate Social Responsibility.” J. Consum. Mark. 18 (2001): 595–630. [Google Scholar] [CrossRef]

- P. Hawken. The Ecology of Commerce: A Declaration of Sustainability. New York, NY, USA: Harper Collins Publishers, 1993. [Google Scholar]

- A. Beltratti. “The Complementarily between Corporate Governance and Corporate Social Responsibility.” Geneva Pap. Risk Insurance 30 (2005): 373–386. [Google Scholar] [CrossRef]

- D. Whetten, G. Rands, and P. Godfrey. “What Are the Responsibilities of Business to Society? ” In Hand Book of Strategy and Management. Edited by A. Pettigrew, H. Thomas and R. Whittington. London, UK: Sage, 2002, pp. 373–408. [Google Scholar]

- M. Jensen, and W. Meckling. “Theory of Firm: Managerial Behavior, Agency Costs, and Capital Structure.” J. Financ. Econ. 3 (1976): 305–360. [Google Scholar] [CrossRef]

- A. Barnea, and A. Rubin. “Corporate Social Responsibility as a Conflict between Shareholders.” J. Bus. Ethics 97 (2010): 71–86. [Google Scholar] [CrossRef]

- M. Jensen. “Value Maximization, Stakeholder Theory and the Corporate Objective Function.” Bus. Ethics Quart. 12 (2002): 235–256. [Google Scholar] [CrossRef]

- J. Hoje, and M.A. Harjoto. “Corporate Governance and Firm Value: The Impact of Corporate Social Responsibility.” J. Bus. Ethics 103 (2011): 351–383. [Google Scholar]

- S.M. Nazir. “Corporate Social Disclosure in Pakistan: A Case Study of Fertilizers Industry.” J. Commer. 2 (2011): 1–11. [Google Scholar]

- A. Waheed. Evaluation of the State of Corporate Social Responsibility in Pakistan and a Strategy for Implementation. Lahore, Pakistan: Responsible Business Initiative, 2007, pp. 1–75. [Google Scholar]

- M.A.M. Makki, and S.A. Lodhi. “Determinants of corporate philanthropy in Pakistan.” Pak. J. Commer. Soc. Sci. 1 (2008): 17–24. [Google Scholar]

- S. Ehsan, and D.A. Kaleem. “An Empirical investigation of the relationship between Corporate Social Responsibility and Financial Performance: Evidence from Manufacturing Sector of Pakistan.” J. Basic Appl. Sci. Res. 2 (2012): 2909–2922. [Google Scholar]

- M. Tilling. “Corporate Social Reporting: A Cook’s Tour.” In Proceedings of the Governance and Social Responsibility Conference, Deakin University, Melbourne, Australia, 18 May 2001.

- M.A. Islam, and C. Deegan. “Motivations for an Organisation within a Developing Country to Report Social Responsibility Information: Evidence from Bangladesh.” Account. Audit. Account. J. 21 (2007): 850–874. [Google Scholar] [CrossRef] [Green Version]

- V. Murthy, and I. Abeysekera. “Corporate Social Reporting Practices of Top Indian Software Firms.” Australas. Account. Bus. Financ. J. 2 (2008): 36–50. [Google Scholar]

- C. Deegan, M. Rankin, and J. Tobin. “An Examination of the Corporate Social and Environmental Disclosures of BHP from 1983–1997: A Test of Legitimacy Theory.” Account. Audit. Account. J. 15 (2002): 312–343. [Google Scholar] [CrossRef]

- C. Deegan, and M. Rankin. “Do Australian Companies Report Environmental News Objectively? An Analysis of Environmental Disclosures by Firms Prosecuted Successfully by the Environmental Protection Authority.” Account. Audit. Account. J. 9 (1996): 52–69. [Google Scholar] [CrossRef]

- R.L. Watts, and J.L. Zimmerman. “Towards a Positive Theory of the Determination of Accounting Standards.” Account. Rev. 53 (1978): 112–143. [Google Scholar]

- S.H. Hussain, and C. Mallin. “The Dynamics of Corporate Governance in Bahrain: Structure, Responsibilities and Operation of Corporate Boards.” Corp. Gov. Int. Rev. 11 (2003): 249–261. [Google Scholar] [CrossRef]

- M. Aktaruddin, M.A. Hossain, and L. Yao. “Corporate Governance and Voluntary Disclosure in Corporate Annual Reports of Malaysian Listed Firms.” J. Appl. Manag. Account. Res. 7 (2009): 1–20. [Google Scholar]

- R. Said, H.Z. Yuserrie, and H. Hasnah. “The Relationship between Corporate Social Responsibility Disclosure and Corporate Governance Characteristics in Malaysia Public Listed Companies.” Soc. Responsib. J. 5 (2009): 212–226. [Google Scholar] [CrossRef]

- Y. Chen. “Corporate Governance and Cash Holdings: Listed New Economy Versus old Economy Firms.” Corp. Gov. Int. Rev. 16 (2008): 430–442. [Google Scholar] [CrossRef]

- E.C. Cheng, and S.M. Courtenay. “Board Composition, Regulatory Regime and Voluntary Disclosure.” Int. J. Account. 41 (2006): 262–289. [Google Scholar] [CrossRef]

- R. Donnelly, and M. Mulcany. “Board Structure, Ownership and Voluntary Disclosure in Ireland.” Corp. Gov. Int. Rev. 16 (2008): 416–429. [Google Scholar] [CrossRef]

- L.L. Eng, and Y.T. Mak. “Corporate Governance and Voluntary Disclosure.” J. Account. Public Policy 22 (2003): 325–345. [Google Scholar] [CrossRef]

- D.G. Barako, P. Hancock, and H.Y. Izan. “Factors Influencing Voluntary Corporate Disclosure by Kenyan Companies.” Corp. Gov. Int. Rev. 14 (2006): 107–125. [Google Scholar] [CrossRef]

- J.I. Sicilian. “The Relationship of Board Member Diversity and Organization Performance.” J. Bus. Ethics 15 (1996): 1313–1320. [Google Scholar] [CrossRef]

- D. Carter, B. Simkins, and W. Simpson. “Corporate Governance, Board Diversity and Firm Value.” Financ. Rev. 38 (2003): 33–53. [Google Scholar] [CrossRef]

- M.A. Fields, and P.Y. Keys. “The Emergence of Corporate Governance From Wall St to Main St: Outside Directors, Board Diversity, Earnings Management and Managerial Incentives to Bear Risk.” Financ. Rev. 38 (2003): 1–24. [Google Scholar] [CrossRef]

- B.S. Coffey, and G.E. Fryxell. “Institutional Ownership of Stock and Dimensions of Corporate Social Performance: An Empirical Examination.” J. Bus. Ethics 10 (1991): 437–444. [Google Scholar] [CrossRef]

- P. Cox, S. Brammer, and A. Millington. “An Empirical Examination of Institutional Investor Preferences for Corporate Social Performance.” J. Bus. Ethics 52 (2004): 27–42. [Google Scholar] [CrossRef]

- S.S. Cowen, L.B. Ferreri, and L.D. Parker. “The Impact of Corporate Characteristics on Social Responsibility Disclosure: A Typology and Frequency-Based Analysis.” Account. Organ. Soc. 12 (1987): 111–122. [Google Scholar] [CrossRef]

- A. Nazli, and M. Ghazali. “Ownership Structure and corporate Social Responsibility Disclosure: Some Malaysian Evidence.” Corp. Gov. 7 (2007): 251–266. [Google Scholar]

- P. Arora, and R. Dharwadkar. “Corporate Governance and Corporate Social Responsibility (CSR): The Moderating Roles of Attainment Discrepancy and Organization Slack.” Corp.Gov. Int. Rev. 19 (2011): 136–152. [Google Scholar] [CrossRef]

- A. Belkaoui, and P. Karpik. “Determinants of the Corporate Decision to Disclose Social Information.” Account. Audit. Account. J. 2 (1989): 36–51. [Google Scholar] [CrossRef]

- C. Deegan, and M. Rankin. “The Materiality of Environmental Information to Users of Annual Reports.” Account. Audit. Account. J. 10 (1997): 562–583. [Google Scholar] [CrossRef]

- A. Belal. “Environmental Reporting in Developing Countries: Empirical Evidence from Bangladesh.” Eco-Manag. Audit. (UK) 7 (2000): 114–121. [Google Scholar] [CrossRef]

- J. Guthrie, and L. Parker. “Corporate Social Disclosure Practice: A Comparative International Analysis.” Adv. Public Interest Account. 3 (1990): 159–175. [Google Scholar]

- R.P. Weber. “Basic Content Analysis.” In Sage University Paper Series on Quantitative Applications in the Social Sciences. Beverly Hills, CA, USA; London, UK: Sage, 1988. [Google Scholar]

- D. Hackston, and M.J. Milne. “Some Determinants of Social and Environmental Disclosures in New Zealand Companies.” Account. Audit. Account. J. 9 (1996): 77–108. [Google Scholar] [CrossRef]

- D.M. Patten. “Intra-Industry Environmental Disclosures in Response to the Alaskan Oil Spill: A Note on Legitimacy Theory.” Account. Organ. Soc. 17 (1992): 471–475. [Google Scholar] [CrossRef]

- S.A. Al-Tuwaijri, T.E. Christensen, and K.I. Hughes. “The Relations among Environmental Disclosure, Environmental Performance and Economic Performance: A Simultaneous Equations Approach.” Account. Organ. Soc. 29 (2004): 447–471. [Google Scholar] [CrossRef]

- M. Suttipun, and P. Stanton. “Determinants of Environmental Disclosure in Thai Corporate Annual Reports.” Int. J. Account. Financ. Rep. 2 (2012). [Google Scholar] [CrossRef]

- J. Neter, and M. Kutner. Applied Linear Regression Models. Illinois, IL, USA: Irwin, 1989, pp. 1–220. [Google Scholar]

- J. Neter, M.H. Kutner, C.J. Nachtsheim, and W. Wasserman. Applied Statistical Models, 4th ed. Homewood, IL, USA: Irwin, 1996. [Google Scholar]

- E. Elinda, and N.A. Mohd Ghazali. “Corporate Social Responsibility and Corporate Governance in Malaysian Government-linked Companies.” Corp. Gov. 12 (2012): 292–305. [Google Scholar]

- K.S. Bukhari, H.M. Awan, and F. Ahmed. “An Evaluation of Corporate Governance Practices of Islamic Banks vs. Islamic Bank Windows of Conventional Banks: A Case of Pakistan.” Manag. Res. Rev. 36 (2013): 400–416. [Google Scholar]

- K.M. Habib-Uz-Zaman. “The Effect of Corporate Governance Elements on Corporate Social Responsibility (CSR) Reporting: Empirical Evidence from Private Commercial Banks of Bangladesh.” Int. J. Law Manag. 52 (2010): 82–109. [Google Scholar]

- S. Mustaruddin, Z. Norhayah, and M. Rusnah. “Corporate Social Responsibility Disclosure and its Relation on Institutional Ownership: Evidence from Public Listed Companies in Malaysia.” Manag. Audit. J. 25 (2010): 591–613. [Google Scholar]

- J. Neter, W. Wasserman, and M. Kutner. Applied Linear Regression Models. Edited by D. Richard. Homewood, IL, USA: Irwin, 1983. [Google Scholar]

- D. Gujarati. Basic Econometrics, 3rd ed. New York, NY, USA: McGraw-Hill, 1995. [Google Scholar]

- M.A. Sufian, and M. Zahan. “Ownership Structure and Corporate Social Responsibility Disclosure in Bangladesh.” Int. J. Econ. Financ. Issues 3 (2013): 901–909. [Google Scholar]

© 2015 by the authors; licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Majeed, S.; Aziz, T.; Saleem, S. The Effect of Corporate Governance Elements on Corporate Social Responsibility (CSR) Disclosure: An Empirical Evidence from Listed Companies at KSE Pakistan. Int. J. Financial Stud. 2015, 3, 530-556. https://doi.org/10.3390/ijfs3040530

Majeed S, Aziz T, Saleem S. The Effect of Corporate Governance Elements on Corporate Social Responsibility (CSR) Disclosure: An Empirical Evidence from Listed Companies at KSE Pakistan. International Journal of Financial Studies. 2015; 3(4):530-556. https://doi.org/10.3390/ijfs3040530

Chicago/Turabian StyleMajeed, Sadia, Tariq Aziz, and Saba Saleem. 2015. "The Effect of Corporate Governance Elements on Corporate Social Responsibility (CSR) Disclosure: An Empirical Evidence from Listed Companies at KSE Pakistan" International Journal of Financial Studies 3, no. 4: 530-556. https://doi.org/10.3390/ijfs3040530