1. Introduction

The stock market plays an important role in economic prosperity, fostering capital formation and sustaining the economic growth of an economy [

1,

2,

3,

4]. The current and the future economic growth of the economy depend on country’s stock market performance up to some extent and the stock market performance depends on the country’s fiscal budget. This is partly due to the notion that a large budget deficit could affect the current and future economic growth of the nation through its effects on the stock markets. Theoretically, it is true that when the budget of the country is in deficit, it will depress the stock prices and undermine the investor’s confidence. Hence, the firm’s ability to get capital on favorable terms will be diminished to a large extent. Large budget deficits could lead to a stock market crash [

5]. Budget deficits also affect stock prices through anticipated future taxes, particularly if tax rates are below their revenue-maximizing levels [

6]. In contrast, however, Friedman [

7] claims that budget deficits have little effect on stock prices.

Essentially, large deficits entail additional risks to the economy which include a loss in investor’s confidence (domestic and foreign) and adverse effects on the volume of transactions. Specifically, a loss in investor’s confidence would cause a shift of portfolio away from home currency assets into foreign currency assets which would limit the ability of the country to finance its liabilities and increase the country’s exposure to exchange rate fluctuations. This situation could weaken capital spending and ignite a drop in asset prices which would further restrain real economic activity. Besides fiscal deficit, there are some other macroeconomic variables which are expected to affect stock prices directly or indirectly. Hardouvelis [

8] argues that a higher real interest rate adversely affects stock returns because it raises the real discount rate at which cash flows are capitalized, hence increasing the cost of capital, which leads to decrease in real output affecting the profitability and productivity of the industries and hence future cash flows. Sellin [

9] lays out competing theories on how money supply affects the stock market prices, namely, those of the Keynesian economists and the real activity theorists. Keynesian economists argue that there is a negative relationship between stock prices and money supply, whereas real activity theorists argue that the relationship between the two variables is positive. The real activity theorist’s argument is based on the fact that the increase in the money supply means that money demands are increasing in anticipation of an increase in economic activity. Higher economic activity implies higher expected profitability, which causes stock prices to rise. The inflation rate is one macroeconomic variable that determines the stock price behavior. One way to view the transmission mechanism between these two variables is via the budget deficit. Following the Monetization perspective, a sustained increase in the budget deficit leads to anticipated inflation and an increase in inflation uncertainty. As the budget deficit persists, real rates are pushed up; and the central bank may ease money to reduce these rates, resulting in a rise in inflation and nominal rates. The demand for long-term securities may decrease because financial market participants anticipate a higher rate of inflation or because uncertainty about such an inflationary policy makes long term securities riskier than short-term ones [

10].

In India, the average percentage growth rate of inflation was 12.56 in the year 1988–1989 which rose up to 19.30 in the year 1991–1992 and in the 2000–2001 the average percentage annual growth rate of inflation was negative (−0.33). It turned positive in the consecutive year, and in the last few years, the percentage annual growth rate of inflation increased rapidly. Significantly, in 2008–2009 it crossed the level of double digits. Money supply in India has increased considerably over the past decades, from Rs. 44.77 billion in 1988–1989 to Rs. 53.92 billion in the year 2000–2001 and to Rs. 76.33 billion in the year 2012–2013, showing an upward trend. Given India’s long history of running huge fiscal deficits, the sharp increase in its fiscal deficit over the last few years is a major concern for both academicians and policy makers in India [

11,

12]. The fiscal deficit of India stood at 7.08% of GDP in 1988. There was a clear improvement till 1990. After 1991 it started to fall with minor fluctuations till 2007–2008, when it was at its minimum of 2.54% of GDP in the year 2007–2008. After falling to 2.54% in 2007–2008, the fiscal deficit to GDP ratio started rising again and was around 5.7% in 2012.

The above discussion indicates that there are several factors that affect or are affected by the budget deficit which will then affect stock prices. Therefore, the main objective of this study is to provide some empirical evidence regarding budget deficits and their effects on stock prices and to examine the long run relationship between Fiscal Deficit, Broad Money Supply, Inflation, Real Interest Rate and Stock Market Index by annual time series data from the period of 1988–2012. This study mainly investigates whether changes in deficits cause changes in stock prices and if so, in what direction. For this purpose, the study uses the Autoregressive Distributed Lag (ARDL) method of co-integration. The ARDL approach has several advantages upon other co-integration methods

1. VECM technique has been used in the study to determine the short run Granger causality between budget deficit and stock prices and the variance decomposition (VDC) is used to predict exogenous shocks of the variables.

This study differs from previous studies in several aspects.

- ➢

First of all, only a few attempts are made to study the effects of fiscal deficit on Stock Prices for India.

- ➢

Further, in earlier research most of the related studies examine the developed economies, only a few studies are concentrated on emerging markets.

- ➢

Besides all these, the research on the topic includes bivariate analysis with conventional econometric techniques. Hence, to know the effect of other macroeconomic variables along with fiscal deficit, on stock prices, the study includes three macroeconomic variables (Inflation, Interest Rates and Money supply) by using the modern ARDL technique.

- ➢

The current study also uses a VECM technique to test the short and the long run causal relationship and the VDC to predict exogenous shocks of the variable.

The remainder of this paper is organized as follows.

Section 2 discusses the literature review,

Section 3 discusses the data and methodology used for the study,

Section 4 analyses empirical results and

Section 5 presentsa summary and conclusions of the study.

2. Literature Review

The majority of the studies that have been conducted by researchers on the effects of persistent rising fiscal deficits on stock prices have yielded contradictory results. Some researchers, particularly from developed economies, are of the view that large and persistent fiscal deficits can significantly depress stock prices [

5,

14,

15,

16,

17,

18]. Geske and Roll [

14] used a simple linear regression model and found that the expected directional impact of budget deficits on stock return should be negative. This is because a government budget deficit exerts upward pressure on the nominal interest rate which, in turn, lowers expected returns on stocks. The increase in risk premia, due to fiscal deficits, exposes investors to an uncertainty surrounding the reaction of the Central Bank and thus further confounds the equity market. Similarly, Laopodis [

17], by using vector autoregression (VAR) and Granger causality test, found that large budget deficits adversely impact stock prices. Asaolu and Ogunmuyiwa [

19] observed an inverse relationship between budget deficits and the average share prices for the period 1986–2007, by using vector autoregression (VAR) model for co-integration. Quayes [

4] studied the association between budget deficit and stock prices by integrating the effects of inflation and the demographic structure by using vector autoregression (VAR) model for co-integration. The model incorporates demand and supply functions to capture the impact of real GDP, inflation, demographic transition, and the budget deficit, on the stock prices. The results from co-integration analysis show that both budget deficits and inflation have a negative impact on stock prices. Osahon and Oriakhi [

20], by utilizing vector auto-regression and error-correction mechanisms (ECM) techniques with annual time series data spanning 1984–2010 found that fiscal deficit is negatively related to stock prices. Saleem and Yasir

et al. [

21], by using the Johansen Cointegration Technique and Granger Causality Test and utilizing annual data from 1990–2010 for Pakistan and India, found that there exists a long run positive causal relationship between budget deficit and stock prices for Pakistan and, on the contrary, in India a long run negative relationship is observed.

In contrast, Van Aarle

et al. [

22] used a structural vector auto-regression (SVAR) approach and provide evidence supporting the positive relationship between fiscal policy and stock prices using structural VAR analysis. Udegbunam and Oaikhenan [

23] found that money-financed deficits have an ambiguously positive effect on stock prices in the short run. Ardagna [

24] reports that adjustments based on expenditure reduction are related to increases in stock market prices. Darrat [

25] in his examination of the effect of monetary and fiscal policies on shares in Canada by using multivariate Granger-causality modeling technique concludes that budget deficits determine share returns, but did not ascertain whether it is positive, negative or ambiguous.

Fama and Schwert [

26], Schwert [

27], Fama [

28], Quayes and Jamal [

29], Gallagher and Taylor [

30,

31], Rapach [

32], and Feldstein [

33] have shown that inflation can have a negative impact on stock prices in industrialized countries, but Al-Khazali and Pyun [

34] and Spyrou [

35] showed that such a negative relationship may not hold true for emerging economies. However, some studies from Pearce and Roley [

36] and Hardouvelis [

37] found no significant relationship between the two variables. Since the relationship between inflation and stock prices is not clear, it is important for researchers to find out the behavior of the variables.

Maysami and Koh [

38] found a positive relationship between money supply changes and stock returns in Singapore. Bailey [

39] also stated that innovation to the monetary variable had a large positive impact on the index. Similar results were found by Maskay [

40], Bernanke and Kuttner [

41] and Alatiqi and Fazel [

42] who asserted that a change in the money supply positively affects stock prices. On the contrary, Osahon and Oriakhi [

20] found that money supply is negatively related to stock prices. Gan, Lee, Yong, and Zhang [

43] found a negative impact of a shock to the money supply on the stock index. This was explained by the fact that the money supply in New Zealand is influenced mainly by foreign investors. They argue that if the interest rate is high relative to other countries, the investors are likely to leave their money in the bank rather than to invest in the risky stock market. If the interest rate is too low, then the investors may want to invest in other markets.

Hsing [

44] using the VAR model and Arango [

45] found an inverse relationship between the share prices on the Bogota stock market and the interest rate which was measured by the inter bank loan interest rate. Uddin and Alam [

46] found that Interest Rate has a significant negative relationship with Share Price and Changes of Interest Rate has a significant negative relationship with Changes of Share Price. Similar results were found by Alam and Uddin [

47]. Osahon and Oriakhi [

20] found that interest rates are negatively related to stock prices. Besides all these studies Rizalito [

48] found no significant relationship between 91-day interest rates and the composite sectoral indices of the Makati Stock Exchange using data from January 1987 to August 1993.

5. Conclusions and Policy Implications

An effort has been made in this paper to investigate whether fiscal deficit and other macroeconomic variables affect the stock price in India or not. Towards this effort, we have used annual data from 1988–2012 for all the variables included in the estimation. The present paper used ARDL bounds testing co-integration and error correction model (ECM) for short run dynamics. The study makes use of Ng-Perron unit root tests to check the non-stationarity property of the series. The test statistics of the unit root suggest that none of the variables included in the study are I(2). The bounds test confirms that the estimated equation and the series are co-integrated. The ARDL results suggest a long run negative and significant relationship exists between budget deficit and stock prices. However, the relationship does not show any significant results in the short run. The findings imply that, in a country when the budget is in deficit, it will depress the stock prices and undermine the investor’s confidence, so the firm’s ability to get capital on favorable terms will be diminished in the long run.

Further, as the deficit increases, future tax burden, interest rates, and the dollar value increases, leading to decrease in corporate profits because of weak domestic as well as export revenues. So, sales decrease which ultimately lowers net earnings, thus decreasing equity prices. These findings are analogous with the work of Adrangi and Allender [

67]; Salem and Yasir

et al. [

21]. However, investors are indifferent to the short run fluctuations in the fiscal deficits. The money supply and inflation in India influence stock prices positively both in the long run as well as in the short run. The findings suggest that the increase in money supply leads to increase in money demand in anticipation of an increase in economic activity. Higher economic activity implies higher expected profitability, which causes stock prices to rise. The error correction term is negative and significant and full convergence process between stock prices and macroeconomic variables takes about two years in India.

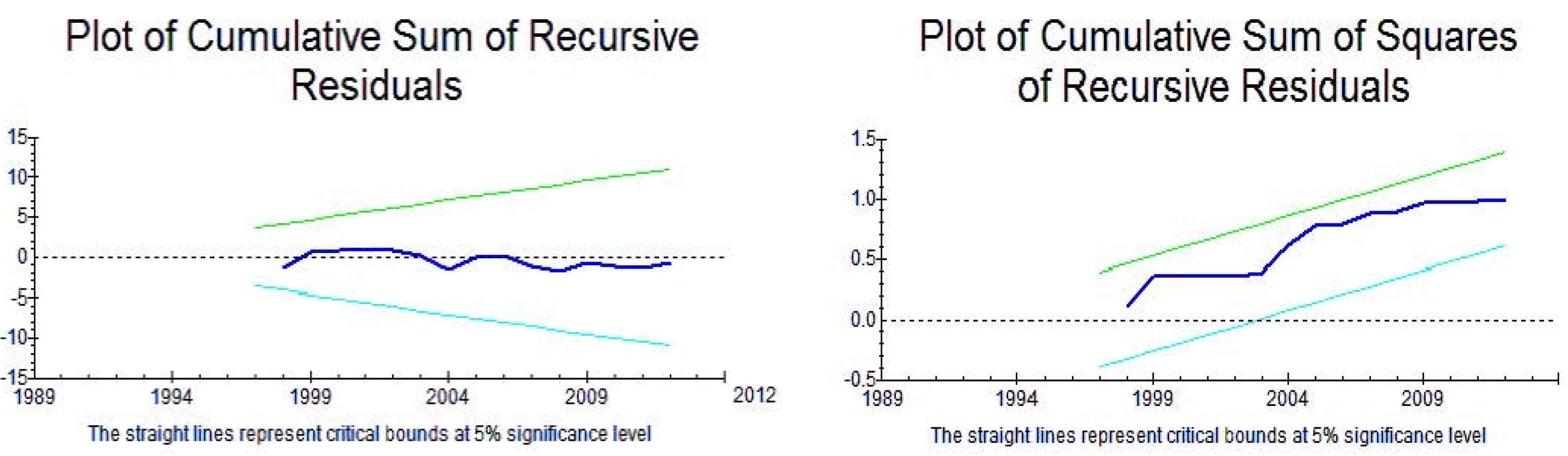

To determine the direction of causality, VECM is used in the study and the result shows that there exists a short runGranger causality running from fiscal deficit to stock price. Further, the result indicates the presence of long run Granger causality for the equation with the stock price as the dependent variable. The CUSUM and CUSUMSQ test results suggest the policy changes considering the explanatory variables of the stock price equation will not cause major distortions in India. To predict the long run and short run shocks variance decomposition technique has been used and the results of the VDC analysis show that the fiscal deficit plays an important role in explaining the variation in stock prices in India.

The implications of the present study are multifaceted. The result suggests a negative impact of fiscal deficit on the stock prices in India. Hence, the government must adopt appropriate policies to improve budget deficit. A stable government with stable policies can help in achieving confidence among foreign and domestic investors. If the government seriously targets these variables, the stock market will develop resulting in the financial development of the country.

{kind=link}