Residential Wind Loss Mitigation Case Study: An Analysis of Insurance Claim Data for Hurricane Michael

1

Department of Mechanical Engineering, University of West Florida, 11000 University Parkway, Pensacola, FL 32514, USA

2

Public Administration Program, Department of Business Administration, University of West Florida, Pensacola, FL 32514, USA

3

College of Health Sciences and Public Policy, Walden University, Minneapolis, MN 55401, USA

*

Author to whom correspondence should be addressed.

Climate 2023, 11(12), 237; https://doi.org/10.3390/cli11120237

Submission received: 27 September 2023

/

Revised: 24 November 2023

/

Accepted: 29 November 2023

/

Published: 4 December 2023

(This article belongs to the Special Issue Analysis of Hurricane Extremes)

Abstract

:This study analyzes insurance claim data from an 11-county area in the Florida Panhandle following the landfall of Hurricane Michael. The data includes 1467 non-mobile home structures, with 902 (61.5%) storm-damaged structures in Bay County. The analysis focuses on Wind Mitigation form 1802. Specifically, building design variables were analyzed via linear regression as to their influence on the percent claim loss. The building design variables included total square footage, dwelling construction type, age of the building, roof type, roof cover type, roof deck attachment type, roof to wall attachment, the presence of secondary water resistance (or sealed roof deck), opening protection type, and roof shape. Results show that building design variables for insurance claims have a high predictive value relative to a Category 5 hurricane event. However, the predictive values of building design variables are also dependent on the dwelling’s proximity to the coast, its location relative to the strong or weak side of the storm, the diameter of the storm, and other wind field variables.

1. Introduction

Warm waters in the Western Atlantic Ocean, Caribbean Sea, and Gulf of Mexico provide ideal conditions for tropical cyclone development during the summer and fall months. Officially, hurricane season starts on 1 June and runs through 30 November. Although mean sea surface temperatures are increasing, research has suggested a prolonged season in future years, more intense storms, and potential landfalls in areas outside of the norm [1]. Loss prediction models are beginning to take climate change into consideration [2]. Thus, wind maps and associated building codes (see Chapter 16) from state to state may prove inadequate as climate and conditions change [3,4,5].

According to the National Centers for Environmental Information and the National Oceanic and Atmospheric Administration (NOAA), the United States experienced 310 so-called “billion dollar” weather events between 1980 and 2021. Fifty-six of these events were tropical cyclones, with a total cost of 1148 billion dollars [6]. In 2019, the Congressional Budget Office (CBO) predicted losses from hurricanes at 54 billion dollars per year [7].

Historically, several storms have provided the impetus for more stringent and consistent building design. On 24 August 1992, Hurricane Andrew made landfall near Homestead, Florida, 25 miles south of downtown Miami. Due to the storm’s proximity to such a densely populated urban area, Andrew remains one of the most costly and devastating storms in history and one of only five Category 5 hurricanes to hit the U.S. mainland. Andrew is also associated with the State of Florida’s adoption of the International Building Code with the express purpose of providing consistency from jurisdiction to jurisdiction and more easily enforceable standards for wind loads and structural design.

After striking South Florida, Hurricane Katrina made a second landfall on 29 August 2005 over Southeast Louisiana and Mississippi before moving on to inundate the City of New Orleans. Due to the failure of various levees and the catastrophic flooding that ensued, Katrina remains the costliest hurricane in U.S. history. Lessons learned from the storm point to an egregious lack of planning, preparation, and governmental response [8,9]

The changing environment makes losses and damage harder to predict. The insurance industry has adapted, with many private insurers refusing to cover properties in the highest-risk areas. In some cases, public entities have had to step in and provide insurance where private companies will not. Examples include the Texas Windstorm Insurance Association (TWIA), the Citizens Property Insurance Corporation (Florida), and the Louisiana Citizens Property Insurance Corporation. These insurers operate as state-affiliated, non-profit organizations and are often referred to as “insurers of last resort.” In Louisiana, Citizens is “state-mandated to be more costly than private property insurance companies,” ostensibly as a deterrent to high-risk coastal development.

Meteorological models have attempted to assess the probability of tropical cyclone severity and the location of landfall. Following the highly active storm seasons of 2004 and 2005, the Florida Department of Financial Services (FDFS) commissioned the Florida Public Hurricane Loss Model (FPHLM). As stated on the Wind & Hurricane Impact Research Laboratory (WHIRL) website, “the basic objective of the model is to produce good estimates of hurricane losses and therefore help determine actuarially sound pricing for homeowner insurance that is fair to both homeowners and to the insurance companies” [10], as described in Tao et al. [11]. By extension, hurricane claim losses from insurance data will validate and further calibrate the WHIRL model [12,13]. In the Florida panhandle, Hurricanes Opal (1995) and Ivan (2004) are within the memory of many residents. A broader awareness of risk exists for most long-term residents of the area. However, awareness does not always result in meaningful action and concerted community efforts toward resilience. Certainly, there will be other storms.

This article covers Hurricane Michael, a catastrophic storm with 160 mph winds that came ashore near Mexico Beach, Bay County, Florida, on 10 October 2018 [14]. The storm essentially wiped the city from the earth [15], as evidenced in Figure 1, as follows:

The following questions are of particular interest to this study: Will claims data from Hurricane Michael support existing insurance models for predicted losses? What can be learned about building design variables in the context of a catastrophic hurricane? Is the influence of building design variables dependent on wind speed, location, or other variations in the wind field? According to this study, building design variables make a difference in modeling percentage loss in a major hurricane event, and this is generally true in a variety of areas of storm impact.

2. Literature Review

“Hurricane Michael made landfall as an unprecedented Category 5 Hurricane in the Florida Panhandle region, with maximum sustained wind speeds of 140 knots (161 mph) and a minimum pressure of 919 mb. The storm caused catastrophic damage from wind and storm surge, particularly in the Panama City Beach to Mexico Beach to Cape San Blas areas” [16]. The devastation from the storm was, in some cases, total, and recovery continues in the area even four years after the storm’s landfall (Figure 1 and Figure 2).

Bay County, Florida, provides an important case study; wind load requirements and housing inventory are different than in other parts of the state. Thus, the landfall of a catastrophic hurricane (see Figure 1) allows for the examination of vulnerability in the county’s structures, specifically in single-family homes.

- i.

- Vulnerability

Much has been said about the vulnerability of communities and how various factors can contribute to a greater difficulty for some individuals and families to return to normal after the shock of a hazard event. The post-disaster period is chaotic; curfews are often enacted to maintain basic law and order, and resources may be extremely scarce or unavailable. As such, it is often easier to prepare for an eventual disaster than it is to react to one. Theoretically, it is also cheaper to encourage resilience than it is to rebuild whole communities, trying desperately to make people whole again [17]. More broadly, it is difficult to reconcile any kind of coastal development with the risk of mega-disasters [18], which regularly push demand far beyond governments’ ability to respond. Building in coastal areas invariably increases vulnerability, and the cost is borne by us all.

While there has been a focus on various types of infrastructure in the literature [19], relatively less research has been completed on areas that are tourist-driven. Cities are vulnerable for a variety of reasons, notably the incidence of natural disasters, terrorism, and technological disasters [20], but cities that are tourist hotspots have additional concerns with which to contend, which make them particularly vulnerable; the prosperity of the community is dependent on maximizing coastal development and beach access, which in turn increases vulnerability.

Bakkensen et al. [21] suggested that “vulnerability is a component of the risk formula: risk = hazard × vulnerability × consequence” (p. 983), or alternatively, sensitivity to stress and exposure, or potential for loss. Efforts to quantify danger and the potential for devastation are numerous and varied. The potential for hazard-related deaths was described by Zhang and Huang as a product of population density multiplied by danger, where danger is a function of the severity of events and their incidence [22]. Vulnerability indices have been suggested to help communities understand potential risks. For example, Bay County, Florida—one of the two counties most impacted by Hurricane Michael—has a score in the Baseline Resilience Index for Communities (BRIC) index of between 2.57 and 3.08, indicating relatively higher resilience [21]. Other metrics include the concept of Exceedence Probability Loss (EPL), which identifies the most vulnerable parts of Florida [23]. Additional Bayesian and probablistic models have been developed to estimate the hurricane fragility and vulnerability of wood-frame housing [24,25]. Another model predicts disruption to critical infrastructure, such as roadways [26].

In this study, special consideration is given to older buildings built prior to the adoption of a single statewide code. Prior to 1 March 2002, the state permitted construction under a variety of local codes, which were inconsistently enforced and proved inadequate in the face of a major storm such as Hurricane Andrew. Buildings under the new code were expected to be “safe, sustainable, affordable, and resilient.” The application of the constantly evolving code to new structures has been described as akin to dealing with other regulations for land use [27]. The cost of retrofitting old structures to meet new standards is often exorbitant, especially when housing is considered on a larger, collective scale. As such, there is little incentive to upgrade the structure of older buildings.

- ii.

- Resilience

Kontokosta and Malik wrote that “the process of identifying vulnerable communities and quantifying their resilience capacity [is] critical to effective emergency management and long-term resilience investments” [28]. The concept of resilience is not well defined and is compounded by uncertainties about what it is, how to reach it, and whom it ultimately benefits [29]. In a critical review of resilience, Meerow et al. proposed the following definition: “Urban resilience refers to the ability of an urban system-and all its constituent socio-ecological and socio-technical networks across temporal and spatial scales-to maintain or rapidly return to desired functions in the face of a disturbance, to adapt to change, and to quickly transform systems that limit current or future adaptive capacity.” With regard to buildings and infrastructure, resilience is often interpreted as a general “hardening,” with more stringent codes and design standards [30].

Independent of a specific definition, resilience is routinely tested in the response and recovery to major storm events. For example, since Hurricane Michael, even with the inflow of federal assistance, the storm proved highly disruptive, and economic and infrastructure resilience was not immediately obvious in the areas most affected by the storm, even though an argument can be made for the dogged determination and individual and community ‘human spirit’ of the county as a normative matter [31], with observed “cultural differences” [32]. Ultimately, resilience is a measure of the efficacy and synergy between many different systems, including infrastructure (road networks and spatial characteristics), buildings (structural components and configuration), and the community (people and organizations) [33]. Even the potential for FEMA aid presents some potential for vulnerability, as local governments pay for disaster-related expenses and then request reimbursement; this process can be arduous and complex.

- iii.

- Building Design and Hardening

Coastal construction has long been understood to be risky. In 1981, the Federal Emergency Management Administration (FEMA) authored the first edition of the Coastal Construction Manual with the intent of providing guidance on the unique characteristics of coastal construction and the specific building techniques that would prove to be more “successful” [34].

In 2001, the American Wood Council (AWC) published the first edition of the Special Design Provisions for Wind and Seismic (SDPWS) standard, which contains specific provisions for materials, design, and construction of wood members, fasteners, and assemblies to resist wind forces [35]. The American Society of Civil Engineers (ASCE) has been publishing the Minimum Design Loads and Associated Criteria for Buildings and Other Structures—commonly referred to as ASCE 7—since 1988, when it assumed responsibility for the standard from the American National Standards Institute (ANSI). ASCE 7 is incorporated by reference in the International Building Code (IBC) and thus serves as the primary basis for the structural design of buildings throughout the United States, including states along the Atlantic seaboard and the Gulf Coast, where hurricane landfall is most likely. Chapter 16 of the Code covers structural design. Herein, State Codes, such as the Florida Building Code, provide specific considerations for regional weather patterns, including wind and flood maps and structural loading (such as wind), with more specific criteria for design incorporated by reference in ASCE 7 [36].

The compound effects of climate change present a tremendously complex design challenge, especially in coastal areas along the Atlantic and Gulf coasts. Rising sea levels are steadily removing the natural protections of barrier islands and wetlands; increases in hydrostatic pressure exacerbate conditions of saltwater intrusion; drainage fails to keep pace with the additional volume of water; and flooding occurs on a much more regular basis. In South Beach, Miami, evidence of “nuisance flooding” regularly occurs during summertime afternoon thunderstorms.

It is important to note that all building codes, including the Florida Building Code, provide minimum standards for construction. There are, of course, many ways to go above and beyond the Code, and make buildings more resilient. In effect, enhanced building techniques, means, and methods have been largely embraced by the insurance industry. However, it has been noted that the insurance industry funds a large amount of the scientific research in this area with the sole aim of lowering insurance premiums, to the detriment of a broader discussion, the so-called “Governor’s Dilemma” [37].

In this regard, roof coverings provide a logical starting point. Roofs are subjected to the full brunt of the elements and often fail in unexpected ways. However, it has been noted that tests are often performed in wind tunnels, and test methods may not always capture the different profiles of roofing material [38], and may not adequately measure a roof covering’s ability to resist uplift and suction [39]. On a more technical level, wind-induced pressure loading on the surface of the standing seam metal roofs is highly non-uniform and dependent on the wind direction, and rib spacing, roof geometrical profile, and eave details significantly affect the nature of wind pressures on standing seam roofs [40]. Asphalt shingles, which comprise upward of 89% of the residential roofing market [41], have been found to fail due to “unsealed portions of the shingle, where the adhesive front end of the shingle has failed or detached from the roof deck, or previous row of shingles. It has been observed that the quantity and percentage of shingles in “unsealed” conditions increase with age. Further, unsealed shingles affected the performance of adjacent sealed shingles; wind blowing under the surface edge of an unsealed shingle produces uplift, which increases the surface area exposed to uplift and ultimately leads to the shingles breaking or detaching from the substrate [42]. These conclusions are consistent with previous studies on the effects of wind on asphalt shingles [43]. Additional studies have observed the degradation of structural components over time, specifically in roof-to-wall connections [44]. Other in situ studies have observed that clay tile roofs on larger homes incur relatively little damage, even when located near the point of landfall, e.g., Punta Gorda, Florida, and Hurricane Charley [45].

On a broader scale, Pita et al. (2015) have recognized five disparate methods for estimating hurricane losses: past-loss data, enhanced damage data, heuristics, physics, and simulation [46]. Various studies have attempted to model or predict hurricane losses [47,48,49,50], with noted emphasis on wind-driven rain and water intrusion as the principle causes of loss [51]. Logically, the importance of window protection and shutters is consistent from model to model [52].

Many factors are known to influence the structural integrity of a residential building, and some prove consequential in the outcome of a building when subjected to hurricane force winds. For instance, building age, or “year built,” has been shown to affect the structural integrity of a home. In 1994, Fronstin and Holtmann posited that older homes incurred less damage during Hurricane Andrew because of a perceived “erosion” of building codes [53]. More recent publications have pointed in the opposite direction, i.e., the age of the structure has been shown to be a statistically significant variable in hurricane loss prediction [54,55]. Both perspectives have logical explanations; a study prepared for the Florida Office of Insurance Regulation notes a perceptible peak in hurricane losses relevant to the “year built” or age of the structure, with provisions for high wind standards in 1993 and the adoption of the Florida Building Code on 1 March 2002. In effect, there was an increase in hurricane losses associated with building age prior to Hurricane Andrew, with precipitous drops following the adoption of the 1993 high wind standards and the 2002 Florida Building Code [56].

- iv.

- The Insurance Industry

Insurance rates for homeowners in Florida are assessed based on a variety of conditions, including the age of the structure, assessed value, and location, the latter of which often proves decisive. Rodriguez-Gaviria et al. (2019) have noted that household income, area of building, year building constructed, and ‘state of preservation of the structure’ have been suggested as potential vulnerability variables [57].

Structural components for hurricane coverage are assessed using the Uniform Mitigation Verification Inspection Form, also known as the Florida Wind Mitigation Form, or Form OIR-B1-1802 (hereinafter referred to as Form 1802). Form 1802 provides for a documented inspection of the property and evaluates the quality of different components, including roof geometry and covering, wall construction type, roof-to-deck attachment, roof-to-wall attachment, secondary water resistance, and opening protection (e.g., hurricane shutters). All wind mitigation inspections must be performed by a licensed home inspector. A full copy of Form 1802 is provided in Supplementary Materials.

- v.

- Bay County Housing Profile

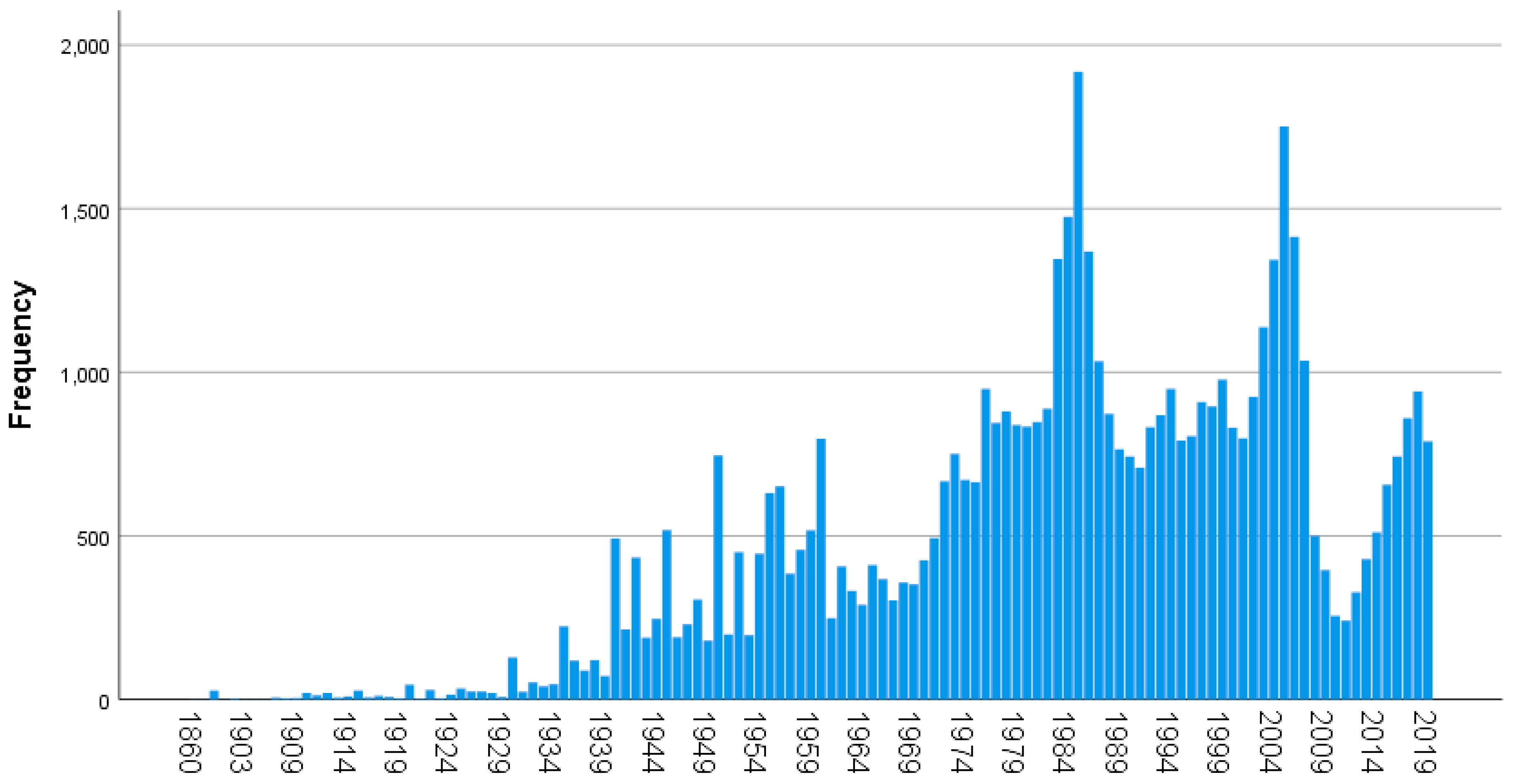

Homes in Bay County, Florida, are skewed toward the low end of the range of property values and were built mostly before the building code improvements that occurred after Hurricane Andrew. Based on a population of 55,767 homes, the median year built for single-family homes in Bay County is 1984, and even with extensive renovation, 1989 is the mean. A distribution by age of Bay County, Florida, housing is shown in Figure 3.

In terms of housing values, single-family homes had an average value of USD 157,049, with a median value of USD 125,134. For the top 10% of housing, values range from USD 276,315 to near 5 million dollars. Based on a population of 55,798 single-family homes, cumulative assessed property values total USD 8.763 billion (see Table 1).

3. Materials and Methods

This study utilizes data obtained from Citizens Property Insurance Corporation (CPIC, hereinafter referred to as “Citizens”). Citizens was established in 2002 as a “not-for-profit, tax-exempt, government entity to provide property insurance to eligible Florida property owners unable to find insurance coverage in the private market” [58]. Citizens is a non-profit ‘insurer of last resort,’ created from two previous entities—the Florida Windstorm Underwriting Association (FWUA), founded in 1972 to insure against wind damage in Monroe County (Florida Keys area), and the Florida Residential Property and Casualty Joint Underwriting Association (FRPCJUA), founded in 1992 after Hurricane Andrew to cover parts of the state not already covered by the FWUA. The public purpose of Citizens is to “provide property insurance coverage to those unable to find coverage in the voluntary admitted market or if coverage in the voluntary admitted market is more than 15% higher than coverage with Citizens” [59]. Rates charged by Citizens for insurance are “required to be actuarily sound, but not to exceed 10% increase annually per policy.” CPIC is one of the largest home property insurers in the state; “as of March 2021, Citizens provided coverage to approximately 570,000 policyholders and had exposure of USD 157 billion” [60], making its database an ideal source of information for connecting insurance-industry practices with the realities of building construction in a scenario involving extreme weather.

While the database is of great interest to research, few if any academic studies have employed it or used it to consider risk analysis and building construction in a catastrophic storm event. For its part, Hurricane Michael is understudied in the academic literature. Access to these data was made through a request to Citizens. Citizens was proactive in responding to the request, providing a wealth of understanding to the authors about the database and its interpretation. This information supplemented previous understanding given the literature and allowed the authors to explore the database for its insight as a purpose-built tool for assessing risk. This paper does not report property-specific information, as it is protected by Citizens and Florida Statute, with an agreement on the part of the researchers that our exploratory analysis will only consider these data in aggregate.

The database utilized for this study is a subset of Citizens data specifically related to the damage caused by Hurricane Michael, which made landfall as a category five storm on 10 October 2018 near Mexico Beach in Bay County, Florida. While all cases are included in an initial analysis, houses located in Bay County were also examined on their own, given the landfall of the storm and its especially dire impacts on homes in that specific area.

For non-mobile home structures, the population for this study is 1467 structures, with 902 (61.5%) of storm-damaged structures in Bay County, as shown in Table 2.

For the 1467 structures analyzed in this study, the mean square footage was 1522, with a standard deviation of 620 square feet. The oldest building was built in 1907, and as expected, perhaps the newest structure was built in 2018. The mean for “year built” was 1983, with a standard deviation of 18.95. The mean value for Distance To Coast (DTC) was approximately 7 miles.

Most of the houses (roughly 62%) in this dataset had asphalt singles as a roof covering (including composition shingles). An additional 21% of the houses had metal roofs. The remaining 17% of roofs were split between clay, built-up, slate, and “other” types of roof covering.

In addition, 64.7% of the houses in this study had gable roofs, 20.1% had hip roofs, and 2.3% had flat roofs, with the remaining 12.9% of roof shapes identified as “other” or “unknown.”

Furthermore, 55.7% of dwellings had no secondary water resistance, such as storm shutters. Only 4.8 of the structures had some form of secondary water resistance. Since 39.1 of the houses were reported as “unknown” in this category, the number of houses with secondary water resistance could be substantially higher. Further, this metric does not include houses with impact-resistant glass, which fulfills many of the same purposes as secondary water resistance.

The primary research question for this project is: What can be learned about the influence of building design variables on the percentage of loss in a catastrophic hurricane from an insurance company database?

A number of hypotheses are appropriate for examining the research question:

H1.

Building design variables, operationalized as total square footage, dwelling construction type, age of the building, roof type, roof cover type, roof deck attachment type, roof to wall attachment, the presence of secondary water resistance (or sealed roof deck), opening protection type, and roof shape, make a difference in modeling percentage loss in a major hurricane event.

The dependent variable for this study is percent loss (defined as claim paid divided by coverage total). Consistent with the Uniform Mitigation Verification Inspection Form, the database includes a variety of building design variables that are appropriate for explanatory purposes as independent variables. Specifically, total square footage, dwelling construction type, age of the building, roof type, roof cover type, roof deck attachment type, roof to wall attachment, the presence of secondary water resistance (or sealed roof deck), opening protection type, and roof shape were all considered as potential indicators of percent loss experienced in the storm. A complete list of the variables tested in this study is shown in the Supplementary Materials.

H2.

The influence of hurricane risk variables (form 1802) is greatest in areas of extreme devastation.

H3.

Age of dwelling predicts percentage loss in a Category 5 hurricane.

H3a.

Buildings constructed since the adoption of the International Building Code (“post Andrew”) fair best in extreme storm events. According to the NAHB in 2019, it has been noted that the Southern U.S. is primarily where non-wood frame techniques are utilized as a result of resilience standards [61].

The study design for this project involves the use of linear regression. For some aspects, such as the impact of roof shape, means comparisons were also examined.

4. Results

4.1. Area Impacted by Hurricane Michael

First, the model was examined given all non-mobile home properties insured by Citizens that experienced damage in Hurricane Michael. It should be noted that these dates include properties from Bay, Calhoun, Franklin, Gadsden, Gulf, Homes, Jackson, Leon, Liberty, Wakulla, and Washington counties, some of which are located inland and relatively far away from the storm’s landfall. Additionally, the characteristics of the wind field during a major hurricane event are highly variable, subject to rapid change, and depend upon a multitude of variables, including the structure’s distance from landfall.

For percent loss across all cases included in the analysis, the regression model is statistically significant: F(9,1130) = 3.587, p < 0.0005. Independent variables in the model accounted for just 2.8% of the variation in percent loss across the whole area, with an adjusted R2 of 2%, a small effect according to Cohen [62]. It is worth noting that only roof shape type and roof type rank are statistically significant in this case when applied to all structures across the storm-impacted area. More specifically, these data show that hip roofs are the preferred “roof shape” with regard to wind loading, overall performance, and percent loss during a major storm event across all 11 counties. Regression statistics for the 11-county study are shown in Table 3.

4.2. Bay County

Next, Bay County was examined with the model. The sub-analysis is relevant because Bay County experienced the highest number of claims and the greatest extent of damage in this dataset.

In this “sub-analysis,” the regression model is statistically significant: F(10,684) = 3.868, p < 0.0005. The R2 for this subset is slightly larger than the whole, at 0.054, with an adjusted R2 of 4%. For Bay County, total square footage, roof shape type, and roof type rank were all statistically significant indicators for percent loss, as shown in Table 4.

It was apparent that additional analysis was needed on a microlevel. Bay County cases were separated by zip code to pinpoint more localized effects, as well as the closeness-of-fit for the model in specific instances. The model was thus run with the database separated by zip codes, as shown in Table 5.

Evidently, some zip codes experienced impacts that more closely approximated the model. In particular, zip codes 32407 and 32456 showed moderately strong explanatory power from the model. The strongest run, zip code 32409, was unfortunately informed by a low number of cases. Further, the zip code with the greatest devastation, 32410 (Mexico Beach area), had too few cases in this database to suggest closeness of fit. The regression model was statistically significant in five zip codes. In 32405, F(8,94) = 2.672, p < 0.1; 32407, F(9,41) = 2.691, p < 0.1; 32408, F(9,153) = 1.784, p < 0.1; 32409, F(7,3) = 6.787, p < 0.1; and 32456, F(9,17) = 2.582, p < 0.1.

Additional analyses were conducted on the full dataset. In examining roof types, hip roofs fair better than other types of roofs (i.e., gable roofs) in this case. The mean percent loss for non-hip roofs was 22%, compared with 13% for hip roofs. Given the coverage of this dataset, this indicates that roof choice is always relevant in this area to mitigate wind-based risk, echoing previously existing literature on the subject, as shown in Table 6.

Given hypothesis one, which suggested that building design variables make a difference in modeling percentage loss in a major hurricane event, there is reason to conclude that this is the case, particularly in areas where the full impact of storms is seen. However, the model provides a reasonably close fit to impacts in a variety of areas of impact, not just in areas of extreme impact, so hypothesis two is generally not supported.

H3.

Age of dwelling predicts percentage loss in a major hurricane event.

For the areas impacted by Hurricane Michael and a subset with just Bay County properties, age of property was examined as a potentially explanatory factor for percent loss.

As a general matter, the correlation between the age of a building (year built) and percent loss is statistically significant (all areas, Pearson correlation = 0.097, p < 0.0005; Bay County, Pearson = 0.139, p < 0.0005). Hypothesis three is thus supported.

H3a.

Buildings constructed since the change in building code as a result of Andrew’s best extreme storm events.

As 1995 is a key date for the implementation of building code revisions following Hurricane Andrew, the dataset was coded for pre-1995 and post-1995 building dates, as shown in Table 7.

The results show that in both the whole dataset and Bay County specifically, the mean percent loss was higher for structures built in 1995 and before. Even though Bay County saw more impact from Hurricane Michael, year built (and building code in place at the time) matters for predicting percent loss. The difference is notable across the dataset. Hypothesis 3a is thus supported.

Additionally, as a broader point of discussion, the Code, writ large, is often discussed as the primary driver of losses from natural disasters, particularly those emanating from tropical cyclones. Thus, this finding (H3a) corroborates the notion that losses can be regulated and minimized according to the standards of code.

- i.

- Limitations

Michael spent only 30 min at category-five intensity. As a result, it would not be appropriate to generalize to other storms or events, especially when the events have a longer duration. This analysis is limited to those properties insured by Citizens. In certain areas devastated by the storm, many structures are not covered by Citizens. For future research, the lack of coverage in this particular exploratory study does present an opportunity to consider other insurers’ wind mitigation models with regard to building construction choices, as well as the real-world impact of these choices when it comes to the percent loss seen in hazard events. Another limitation is the low sample size in certain zip codes, particularly those that were exposed to the greatest impacts from the storm. We know that Mexico Beach, for example, was heavily damaged by the storm, but cases from the zip code in this dataset are few, possibly because Citizens may not be the primary insurer for this location. This analysis does not consider the impact of Hurricane Michael on mobile homes, which present far greater risks for homeowners given their construction quality.

- ii.

- Threats to Validity

One major threat to validity with these data is the potential for vagueness in the collection instrument, Form 1802. The form mentions a variety of aspects of building construction that may be relevant in mitigating loss due to the wind of a tropical system, but the way the questions are posed may present some problems. The selection of responses does not eliminate ambiguity. An example of this is roof-to-wall attachment. The selection of an option like ‘toe nail’ is subject to far more variation than would be suggested by the choice being one of four overly simplified options. Approaches to installation may vary, yielding a wider array of possible outcomes.

Ranks were used in the case of some variables, like dwelling construction type and roof type, because the options given basically yield only a few levels of real difference. Masonry receives a higher rating than a stick frame structure, but a masonry veneer is rated for the underlying structure rather than for the veneer. The valuing system employed by insurers values clay roof tiles over asphalt shingles, without consideration of the variety of specifications. As such, the relative value of various roof coverings may be uncertain.

Ultimately, Form 1802 is completed by a licensed home inspector. While the credential assures some level of quality, home inspections can be, and often are, subjective. Two independent licensed home inspectors may draw different conclusions about the same residence. Since the form can be vague at times and open to interpretation, the results of Form 1802 may be biased. Additionally, some components are not readily visible without a more invasive form of exploratory inspection.

5. Discussion

In the search for more resilient homes and communities, hurricane claim data offers unique insight into statewide construction practices, housing inventory, and the insurance policies that cover real property. Such was the case in this study. In the analysis of claim data relevant to Hurricane Michael, a storm that tracked over 11 counties, several patterns emerged. Although it should be noted that, due to the size and geographic spread of the initial dataset, said patterns were not immediately visible. Rather, the model began to come into focus as the dataset was broken into subsets and focused on specific locations. Over the 11-county area, our model produced a minimal number of tangible results, and many of the variables had little to no explanatory power. When the data were limited to Bay County and to specific locations relative to the eye of the storm (e.g., the eastern side), the model began to come into focus, and higher R2 values were observed.

As mentioned previously, Hurricane Michael spent only 30 min as a Category 5 hurricane. The storm was approximately 350 miles in diameter and moved north at an average speed of 13 miles per hour. After four hours over the Florida panhandle, Michael moved into Southern Georgia and further dissipated. Certainly, Michael was a unique storm; its intensity, movement, and diameter all affected the frequency and severity of hurricane losses. As such, the model used in this study would, in all probability, experience variations from storm to storm. Data on losses may be widespread, but the predictive capacity of wind mitigation, structural hardness, and building design variables will vary in accordance with other storm metrics.

Roof shape (geometry) was observed as statistically significant across all models in this study, with hip roofs fairing the best. This is consistent with the literature and what is known about wind pressures across different roof structures. Opening protection also presented some interesting results as a minimizing factor in the scale of hurricane claim losses. This is also consistent with the body of knowledge and further supports “opening protection’ as a consideration on Form 1802. It is also believed that opening protection is influential for two reasons in particular. First, if a window opening becomes compromised during a windstorm, tornado, or hurricane event, the opening will allow the entire structure to become pressurized in a way that may further compromise its integrity. Second, wind is not the only consideration in post-disaster investigations. Storm surge, flooding, wind-driven rain, and any manner of water intrusion are responsible for a substantial percentage and large number of insurance claims. When reporting claims, many inspectors cite “hurricane” as the chief cause of the loss. While, in a general sense, this may be true, the inexactitude of the so-called chief cause does little to identify the root cause of the claim, nor does it identify the mechanisms of failure from structure to structure. Form 1802 is accurately termed a “wind mitigation” form. However, only one variable on Form 1802 considers water intrusion. i.e., Secondary Water Resistance (SWR). Practically speaking, the installation of an “ice and water shield” applied directly to the roof deck satisfies this requirement and affords the homeowners a small decrease in their insurance rates. More broadly, water intrusion is not directly considered on the wind mitigation form, nor are inspections required for the quality of installations, including flashing, weather-stripping, sealants, and all other forms of water and moisture protection. Future research should examine the prevalence and severity of water intrusion losses and recommend construction practices that align with better outcomes for water damage.

The rationale for Form 1802 is widely understood and supported by a general consensus. For example, there are fundamental differences between “Roof to Wall” attachments. In order of best to worst, double wraps are preferred to single wraps, clips, and toe nails. Although, as discussed previously, not all nails are created equal. Even among 6d nails, there are fundamental differences between those that are delivered via nail gun, hammer, or the ring shank variety. In the context of a home inspection, these nuances may be hard to detect or simply unobservable. As such, it should be noted that the basis of measurement (form 1802) should be refined to better explain the dynamic between hurricane and structure.

Several variables were excluded from this analysis, as they were excluded from Form 1802 and must be produced via geospatial analysis. Two variables are of particular interest for future research. Surface rugosity (roughness) is known to disrupt wind patterns, as is urban density. Effectively, these are colinear variables and present two different ways of measuring the same conceptual variable. Chapter 16 of the Florida Building Code, Section 1609.4, refers to an “exposure category that adequately reflects the characteristics of ground surface irregularities for the site at which the building or structure is to be constructed”. No such variables were available in the Citizens dataset. However, through geospatial analysis and the use of Geographic Information Systems (GIS) software, future research will be able to test for correlations between exposure categories and hurricane claim losses. Similarly, it is believed that tree cover (approximated by the Normalized Difference Vegetation Index—NDVI) will further clarify the potential benefits—and hazards—of adjacent tree cover.

Ultimately, Citizens’ insurance claim data for Hurricane Michael has not been widely analyzed. To the authors’ knowledge, no academic publications have resulted from the analysis of these data. Thus, this study presents a unique contribution to the scientific literature on this topic.

In terms of the validation of the model, Citizens Property Insurance Corporation uses exactly the same variables that are discussed in this paper as part of their proprietary actuarial algorithm used to determine homeowner insurance premiums from dwelling to dwelling. The findings presented in this paper are consistent with those of Citizens’ actuarial model, with some unique differences, perhaps attributable to the specific nature and dynamics of Hurricane Michael. As it is with the Citizens model, with each successive storm and additional data, the model is refined.

It should also be noted that these data were collected in the field by human subjects using imperfect methods. Thus, these data exhibit several limitations, as described above. In this manner, these data are perhaps dissimilar to those that might be generated by controlled experiments. By itself, this does not disqualify the analysis herein. Rather, as these data were handled in accordance with all academic and scientific protocols, the various acknowledgements of the data’s limitations simply provide more context and speak to the study’s authenticity.

6. Conclusions

Hurricane claim data provide excellent insight into local housing inventory. Additionally, models of hurricane loss prediction, while providing statistically acceptable predictive capabilities, are very much a work in progress. Some of the refinements and suggestions for improvement are detailed in this paper. Perhaps more importantly, from the standpoint of consumer advocacy and the responsible use of public funds, more accurate methods would benefit us all.

The results reported in this paper are only useful insofar as they are unique to Hurricane Michael and represent a first round of what is planned to be a replicable analysis. Other disasters may identify unknown variability in the model or reveal new insights altogether. However, with reasonable predictive capability, the model used in this paper provides a relatively high level of explanation for the variables influencing the losses identified in Citizens hurricane claims.

Finally, the data used in this paper came from a unique provider. Citizens is identified as an insurer of last resort, and thus, it is possible that private insurance companies’ data would provide different outcomes. Thus, future research is certainly warranted.

Supplementary Materials

The following supporting information can be downloaded at: https://www.mdpi.com/article/10.3390/cli11120237/s1.

Author Contributions

Conceptualization, A.G. and C.L.A.; methodology, A.G. and C.L.A.; validation, A.G. and C.L.A.; formal analysis, A.G. and C.L.A.; writing—original draft preparation, A.G. and C.L.A.; writing—review and editing, A.G. and C.L.A.; All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Data Availability Statement

Restrictions apply to the availability of these data. Data was obtained from Citizens Property Insurance Corporation. These data are not publicly available because they involve individual homeowner information, including claims and coverage.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Li, Y.; Stewart, M. Cyclone Damage Risks Caused by Enhanced Greenhouse Conditions and Economic Viability of Strengthened Residential Construction. Nat. Hazards Rev. 2011, 12, 9–18. [Google Scholar] [CrossRef]

- Walker, G.R.; Mason, M.S.; Crompton, R.P.; Musulin, R.T. Application of insurance modelling tools to climate change adaptation decision-making relating to the built environment. Struct. Infrastruct. Eng. 2016, 12, 450–462. [Google Scholar] [CrossRef]

- International Code Council. International Building Code, 7th ed.; Building; International Code Council: Murrieta, CA, USA, 2018. [Google Scholar]

- Florida Building Code. 2020. Building, 7th Edition. International Code Council. Available online: https://codes.iccsafe.org/codes/florida (accessed on 30 November 2023).

- Building Code of New York State. 2020. International Code Council. Available online: https://up.codes/viewer/new_york/ibc-2018 (accessed on 30 November 2023).

- National Oceanic and Atmospheric Administration. Climate Monitoring, Billion Dollar Climate and Weather Disasters, Summary Data. 2022. Available online: https://www.ncdc.noaa.gov/billions/summary-stats (accessed on 4 February 2022).

- Congressional Budget Office. Expected Costs of Damage from Hurricane Winds and Storm-Related Flooding; United States Congress: Washington, DC, USA, 2019.

- Select Bipartisan Committee to Investigate the Preparation for and Response to Hurricane Katrina. A Failure of Initiative: Final Report. 2006. Available online: https://www.govinfo.gov/content/pkg/CRPT-109hrpt377/pdf/CRPT-109hrpt377.pdf (accessed on 30 November 2023).

- Nicholls, K.; Picou, J.S. The Impact of Hurricane Katrina on Trust in Government. Soc. Sci. Q. 2013, 94, 344–361. [Google Scholar] [CrossRef]

- Wind and Hurricane Impact Research Laboratory (WHIRL). Florida Public Hurricane Loss Model (FPHLM), Objective. 2022. Available online: https://research.fit.edu/whirl/projects/florida-public-hurricane-loss-model-fphlm/ (accessed on 4 March 2022).

- Tao, Y.; Wang, T.; Sun, A.; Hamid, S.S.; Chen, S.C.; Shyu, M.L. Florida public hurricane loss model: Software system for insurance loss projection. Softw. Pract. Exp. 2022, 52, 1736–1755. [Google Scholar] [CrossRef]

- Pinelli, J.P.; Gurley, K.R.; Subramanian, C.S.; Hamid, S.S.; Pita, G.L. Validation of a probabilistic model for hurricane insurance loss projections in Florida. Reliab. Eng. Syst. Saf. 2008, 93, 1896–1905. [Google Scholar] [CrossRef]

- Pinelli, J.P.; Pita, G.; Gurley, K.; Torkian, B.; Hamid, S.; Subramanian, C. Damage Characterization: Application to Florida Public Hurricane Loss Model. Nat. Hazards Rev. 2011, 12, 190–195. [Google Scholar] [CrossRef]

- Beven, J.L., II; Berg, R.; Hagen, A. National Hurricane Center Tropical Cyclone Report, Hurricane Michael. NHC Report AL142018. 2019. Available online: https://www.nhc.noaa.gov/data/tcr/AL142018_Michael.pdf (accessed on 15 April 2023).

- Banerjee, N. The Common Language of Loss. Inside Climate News. 2019. Available online: https://insideclimatenews.org/american-climate/essay/loss (accessed on 15 April 2023).

- National Weather Service. Catastrophic Hurricane Michael Strikes Florida Panhandle. 2018. Available online: https://www.weather.gov/tae/HurricaneMichael2018 (accessed on 15 April 2023).

- Atkinson, C.L. Toward Resilient Communities: Examining the Impacts of Local Governments in Disasters; Routledge: New York, NY, USA, 2014. [Google Scholar]

- Coutaz, G. Coping with Disaster Risk Management in Northeast Asia: Economic and Financial Preparedness in China, Taiwan, Japan and South Korea; Emerald Publishing: Bingley, UK, 2018. [Google Scholar]

- Sherly, M.A.; Karmakar, S.; Parthasarathy, D.; Chan, T.; Rau, C. Disaster vulnerability mapping for a densely populated coastal urban area: An application to Mumbai, India. Ann. Assoc. Am. Geogr. 2015, 105, 1198–1220. [Google Scholar] [CrossRef]

- Fischer, K.; Hiermaier, S.; Riedel, W.; Haring, I. Morphology dependent assessment of resilience for urban areas. Sustainability 2018, 10, 1800. [Google Scholar] [CrossRef]

- Bakkensen, L.A.; Fox-Lent, C.; Read, L.K.; Linkov, I. Validating resilience and vulnerability indices in the context of natural disasters. Risk Anal. 2017, 37, 982–1004. [Google Scholar] [CrossRef] [PubMed]

- Zhang, N.; Huang, H. Resilience analysis of countries under disasters based on multisource data. Risk Anal. 2018, 38, 31–42. [Google Scholar] [CrossRef]

- Kakareko, G.; Jung, S.; Vanli, O.A. Hurricane risk analysis of the residential structures located in Florida. Sustain. Resilient Infrastruct. 2020, 5, 395–409. [Google Scholar] [CrossRef]

- Kakareko, G.; Jung, S.; Mishra, S.; Vanli, O.A. Bayesian capacity model for hurricane vulnerability estimation. Struct. Infrastruct. Eng. 2020, 17, 638–648. [Google Scholar] [CrossRef]

- Abdelhady, A.U.; Spence, S.M.J.; McCormick, J. Risk and fragility assessment of residential wooden buildings subject to hurricane winds. Struct. Saf. 2022, 94, 102137. [Google Scholar] [CrossRef]

- Kocatepe, A.; Ulak, M.B.; Kakareko, G.; Ozguven, E.E.; Jung, S.; Arghandeh, R. Measuring the accessibility of critical facilities in the presence of hurricane-related roadway closures and an approach for predicting future roadway disruptions. Nat. Hazards 2018, 95, 615–635. [Google Scholar] [CrossRef]

- Florida Housing Finance Corporation. Overview of the Florida Building Code. 2017. Available online: https://www.floridahousing.org/docs/default-source/aboutflorida/august2017/august2017/tab4.pdf (accessed on 15 April 2023).

- Kontokosta, C.E.; Malik, A. The resilience to emergencies and disasters index: Applying big data to benchmark and validate neighborhood resilience capacity. Sustain. Cities Soc. 2018, 36, 272–285. [Google Scholar] [CrossRef]

- Cutter, S.L. Resilience to what? Resilience for whom? Geogr. J. 2016, 182, 110–113. [Google Scholar] [CrossRef]

- Meerow, S.; Newell, J.P.; Stults, M. Defining urban resilience: A review. Landsc. Urban Plan. 2016, 147, 38–49. [Google Scholar] [CrossRef]

- Schweers, J. ‘Collectively We’ve Forgotten Them’: Hurricane Michael Survivors Hanging on One Year Later. Tallahassee Democrat. 2019. Available online: https://www.tallahassee.com/story/news/local/state/2019/10/04/hurricane-michael-survivors-hanging-one-year-later/3774446002/ (accessed on 15 April 2023).

- Morss, R.E.; Lazrus, H.; Bostrom, A.; Demuth, J.L. The influence of cultural worldviews on people’s responses to hurricane risks and threat information. J. Risk Res. 2020, 23, 1620–1649. [Google Scholar] [CrossRef]

- Rus, K.; Kilar, V.; Koren, D. Resilience assessment of complex urban systems to natural disasters: A new literature review. Int. J. Disaster Risk Reduct. 2018, 31, 311–330. [Google Scholar] [CrossRef]

- Federal Emergency Management Administration (FEMA). Coastal Construction Manual: Principles and Practices of Planning, Siting, Designing, Constructing, and Maintaining Residential Buildings in Coastal Areas, 4th ed.; FEMA P-55; FEMA: Washington, DC, USA, 2011.

- American Wood Council (AWC). Special Design Provisions for Wind and Seismic (SDPWS); 2021 Edition; AWC: Kansas City, MO, USA, 2021. [Google Scholar]

- American Society of Civil Engineers (ASCE). Minimum Design Loads and Associated Criteria for Buildings and Other Structures; ASCE/SEI 7; ASCE: Reston, VA, USA, 2021. [Google Scholar]

- Weinkle, J. Experts, regulatory capture, and the “governor’s dilemma”: The politics of hurricane risk science and insurance. Regul. Gov. 2020, 14, 637–652. [Google Scholar] [CrossRef]

- Smith, D.J.; Master, F.J.; Chowdhury, A.G. Investigating a wind tunnel method for determining wind-induced loads on roofing tiles. J. Wind. Eng. Ind. Aerodyn. 2016, 155, 47–59. [Google Scholar] [CrossRef]

- Mooeghi, M.A.; Irwin, P.; Chowdhury, A.G. Large-scale testing on wind uplift of roof pavers. J. Wind. Eng. Ind. Aerodyn. 2014, 28, 22–36. [Google Scholar]

- Habte, P.; Mooneghi, M.A.; Chowdhury, A.G.; Irwin, P. Full-scale testing to evaluate the performance of standing seam metal roofs under simulated wind loading. Eng. Struct. 2015, 105, 231–248. [Google Scholar] [CrossRef]

- Asphalt Roofing Manufacturers Association (ARMA). The Bitumen Roofing Industry—A Global Perspective; ARMA: Washington, DC, USA, 2011. [Google Scholar]

- Dixon, C.R. The Wind Resistance of Asphalt Roofing Shingles. Ph.D. Thesis, University of Florida, Gainesville, FL, USA, 2013. [Google Scholar]

- Marshall, T.P.; Morrison, S.J.; Herzog, R.F.; Green, J.R. Wind Effects on Asphalt Shingles. In Proceedings of the 29th Conference on Hurricanes and Tropical Meteorology, Tucson, AZ, USA, 10–14 May 2010; p. 2.17. [Google Scholar]

- Mishra, S.; Vanli, O.A.; Kakareko, G.; Jung, S. Preventative maintenance of wood-framed buildings for hurricane preparedness. Struct. Saf. 2019, 76, 28–39. [Google Scholar] [CrossRef]

- Meloy, N.; Sen, R.; Pai, N.; Mullins, G. Roof Damage in New Homes Caused by Hurricane Charley. J. Perform. Constr. Facil. 2007, 21, 97–107. [Google Scholar] [CrossRef]

- Pita, G.; Pinelli, J.P.; Gurley, K.; Mitrani-Reiser, J. State of the Art of Hurricane Vulnerability Estimation Methods: A Review. Nat. Hazards Rev. 2015, 16, 04014022. [Google Scholar] [CrossRef]

- Pinelli, J.P.; Simiu, E.; Gurley, K.; Subramanian, C.; Zhang, L.; Cope, A.; Filliben, J.J.; Hamid, S. Hurricane Damage Prediction Model for Residential Structures. J. Struct. Eng. 2004, 130, 1685–1691. [Google Scholar] [CrossRef]

- Vickery, P.J.; Lin, J.; Skerlj, P.F.; Twisdale, L.A., Jr.; Huang, K. HAZUS-MH hurricane model methodology. I: Hurricane hazard, terrain, and wind load modeling. Nat. Hazards Rev. 2006, 7, 82–93. [Google Scholar] [CrossRef]

- Vickery, P.J.; Skerlj, P.F.; Twisdale, L.A. Simulation of hurricane risk in the U.S. using empirical track model. J. Struct. Eng. 2006, 126, 1222–1237. [Google Scholar] [CrossRef]

- Simmons, K.M.; Kruse, J.B.; Smith, D.A. Valuing Mitigation: Real Estate Market Response to Hurricane Loss Reduction Measures. S. Econ. J. 2002, 68, 660–671. [Google Scholar]

- Van de lindt, J.A.; Dao, T.N. Loss Analysis for Wood Frame Buildings during Hurricanes. II: Loss Estimation. J. Perform. Constr. Facil. 2012, 26, 739–747. [Google Scholar] [CrossRef]

- Gurley, K.R.; Masters, F.J. Post-2004 Hurricane Field Survey of Residential Building Performance. Nat. Hazards Rev. 2011, 12, 177–183. [Google Scholar] [CrossRef]

- Fronstin, P.; Holtmann, A.G. The Determinants of Residential Property Damage Caused by Hurricane Andrew. South. Econ. J. 1994, 61, 387–397. [Google Scholar] [CrossRef]

- Kim, J.M.; Woods, P.K.; Park, Y.J.; Kim, T.; Son, K. Predicting hurricane wind damage by claim payout based on Hurricane Ike in Texas. Geomat. Nat. Hazards Risk 2016, 7, 1513–1525. [Google Scholar] [CrossRef]

- Dehring, C.; Halek, M. Coastal Building Codes and Hurricane Damage. Land Econ. 2013, 89, 597–613. [Google Scholar] [CrossRef]

- Applied Research Associates, Inc. 2008 Florida Residential Wind Loss Mitigation Study. Prepared for Florida Office of Insurance Regulation, ARA Final Report 18401 Version 1.11. 2008. Available online: https://www.floir.com/sitedocuments/aralossmitigationstudy.pdf (accessed on 15 April 2023).

- Rodriguez-Gaviria, E.M.; Ochoa-Osorio, S.; Builes-Jaramillo, A.; Botero Fernandez, V. Computational bottom-up vulnerability indicator for low-income flood-prone urban areas. Sustainability 2019, 11, 4341. [Google Scholar] [CrossRef]

- Citizens Property Insurance Corporation (CPIC). Who We Are. 2022. Available online: https://www.citizensfla.com/who-we-are (accessed on 15 April 2023).

- Ashburn, C. Citizens Property Insurance Corporation Overview. 2019. Available online: https://www.citizensfla.com/documents/20702/9063551/20190110+House+Insurance+and+Banking+Subcommittee+Citizens+Property+Insurance+Corporation+Overview/ae856970-a807-4b7e-af32-5f6e9fe1790c (accessed on 15 April 2023).

- Florida Office of Insurance Regulation. OPPAGA Government Program Summary. 2022. Available online: https://oppaga.fl.gov/ProgramSummary/ProgramDetailPrint?programNumber=4102 (accessed on 15 April 2023).

- NAHB. Framing Methods for Single-Family Homes. 2019. Available online: https://eyeonhousing.org/2019/10/framing-methods-for-single-family-homes-2018/ (accessed on 30 November 2023).

- Cohen, J. Statistical Power Analysis for the Behavioral Sciences, 2nd ed.; Lawrence Erlbaum Associates: Mahwah, NJ, USA, 1988. [Google Scholar]

Figure 1.

Before and After Photos of Mexico Beach—Hurricane Michael, October 2018. (Source: United States Geological Survey, Hurricane Michael Pre- and Post-Storm Photo Comparisons—Mexico Beach. Arrow identifies unimpacted structure for reference. Electronic Resource: https://www.usgs.gov/media/images/hurricane-michael-pre-and-post-storm-photo-comparisons-mexico-beach-0, accessed on 21 November 2023.

Figure 1.

Before and After Photos of Mexico Beach—Hurricane Michael, October 2018. (Source: United States Geological Survey, Hurricane Michael Pre- and Post-Storm Photo Comparisons—Mexico Beach. Arrow identifies unimpacted structure for reference. Electronic Resource: https://www.usgs.gov/media/images/hurricane-michael-pre-and-post-storm-photo-comparisons-mexico-beach-0, accessed on 21 November 2023.

Figure 2.

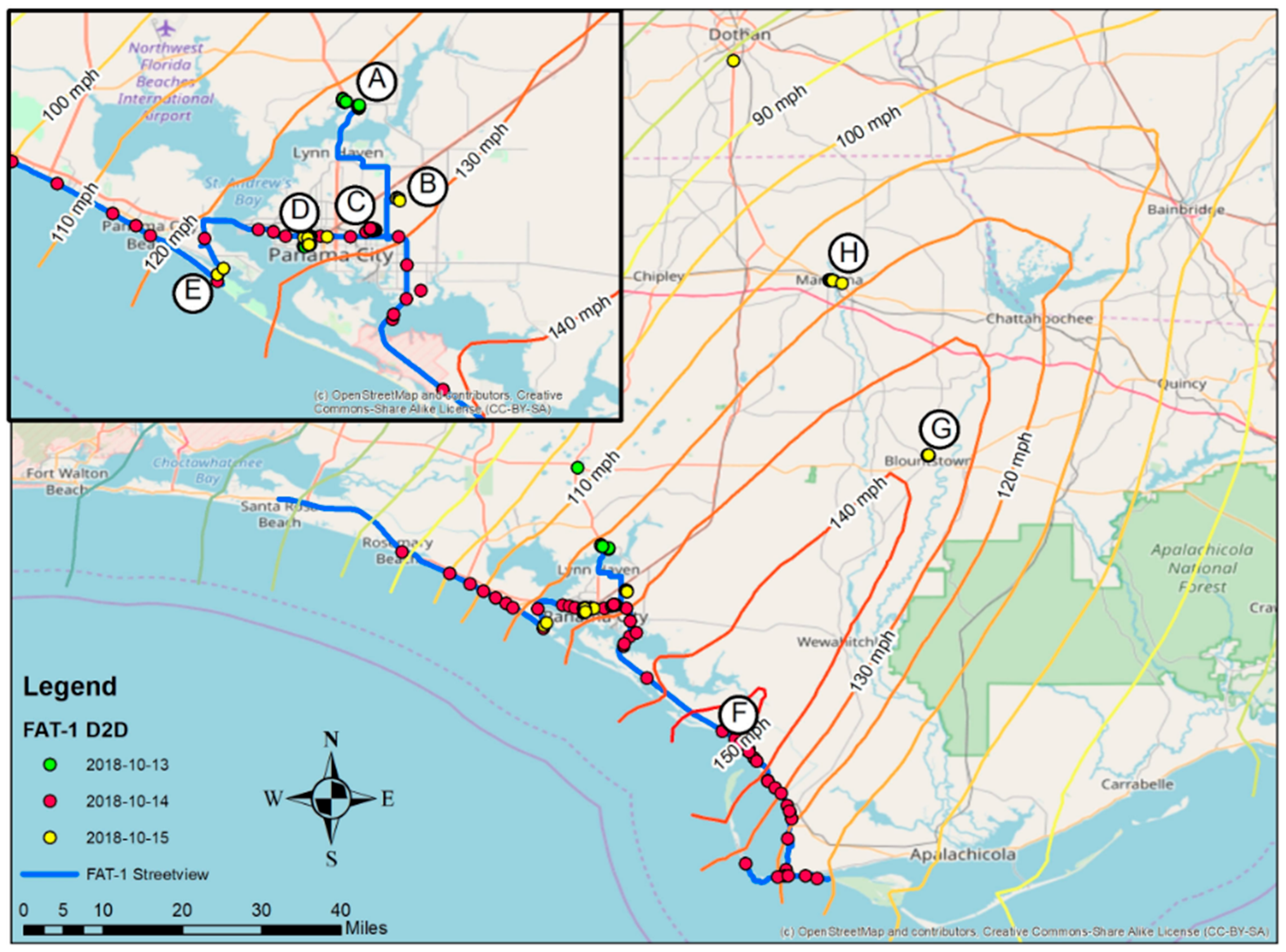

Peak gust wind speeds as estimated by Applied Research Associates (Source: Structural Extreme Event Reconnaissance (StEER) Network, Hurricane Michael: Field Assessment Team 1 (FAT-1), Early Access Reconnaissance Report (EARR), 2018 [17]) Letters A-H indicate the locations of measurement sites.

Figure 2.

Peak gust wind speeds as estimated by Applied Research Associates (Source: Structural Extreme Event Reconnaissance (StEER) Network, Hurricane Michael: Field Assessment Team 1 (FAT-1), Early Access Reconnaissance Report (EARR), 2018 [17]) Letters A-H indicate the locations of measurement sites.

Figure 3.

Year built, single-family homes in Bay County, Florida, frequency by year.

{kind=link}

{kind=link}

{kind=link}

Table 1.

Year built, year of effective building (renovation), and parcel value, Bay County, Florida.

Table 1.

Year built, year of effective building (renovation), and parcel value, Bay County, Florida.

| Variable | N | Range | Min. | Max. | Sum | Mean |

|---|---|---|---|---|---|---|

| First building actual year built | 55767 | 159 | 1860 | 2019 | - | 1984 |

| First building effective year built (extensive renovation) | 55767 | 159 | 1860 | 2019 | - | 1990 |

| Parcel total appraised value | 55798 | USD 4496191 | USD 3712 | USD 4499903 | USD 8763042790 | USD 157049 |

Table 2.

Non-mobile-home structures in the 11-county study area.

| County | Frequency | Percent | Valid Percent | Cumulative Percent |

|---|---|---|---|---|

| Bay | 902 | 61.5 | 61.5 | 61.5 |

| Gulf | 197 | 13.4 | 13.4 | 92 |

| Franklin | 162 | 11 | 11 | 73.3 |

| Gadsden | 77 | 5.2 | 5.2 | 78.6 |

| Jackson | 54 | 3.7 | 3.7 | 95.8 |

| Leon | 29 | 2 | 2 | 97.8 |

| Wakulla | 22 | 1.5 | 1.5 | 99.5 |

| Calhoun | 12 | 0.8 | 0.8 | 62.3 |

| Washington | 8 | 0.5 | 0.5 | 100 |

| Liberty | 3 | 0.2 | 0.2 | 98 |

| Holmes | 1 | 0.1 | 0.1 | 92.1 |

| Total | 1467 | 100 | 100 |

Table 3.

Regression analysis of the 11-county study area.

| Unstandardized Coefficients | Standardized Coefficients | ||

|---|---|---|---|

| B | Std. Error | Beta | |

| (Constant) | 21.495 | 5.212 | |

| Dwelling Total Sq Ft | 0.001 | 0.002 | 0.01 |

| Dwelling Years Old | 0.044 | 0.055 | 0.026 |

| Roof Shape Type | −9.767 *** | 2.314 | −0.13 |

| Roof-to-Wall Rank | 2.456 | 1.586 | 0.075 |

| Roof Deck Attachment | −1.413 | 1.091 | −0.057 |

| Roof Cover Type | 1.347 | 1.259 | 0.035 |

| Roof Type Rank | −3.94 * | 1.669 | −0.07 |

| Secondary Water Resist | 6.543 | 5.139 | 0.039 |

| Opening Protection Type | −0.625 | 1.34 | −0.014 |

* p < 0.1, *** p < 0.001.

Table 4.

Regression Analysis of claims data for Bay County, Florida.

| Unstandardized Coefficients | Standardized Coefficients | ||

|---|---|---|---|

| B | Std. Error | Beta | |

| (Constant) | 17.678 | 7.487 | |

| Dwelling Total Sq Ft | 0.006 ** | 0.002 | 0.103 |

| Dwelling Years Old | 0.116 | 0.078 | 0.063 |

| Roof Shape Type | −12.669 *** | 3.295 | −0.15 |

| Roof-to-Wall Rank | 0.979 | 2.307 | 0.026 |

| Roof Deck Attachment | −1.984 | 1.433 | −0.075 |

| Roof Cover Type | 2.021 | 1.9 | 0.047 |

| Roof Type Rank | −5.736 * | 2.48 | −0.089 |

| Construction Type | 1.115 | 1.608 | 0.028 |

| Secondary Water Resist | 7.753 | 7.533 | 0.039 |

| Opening Protection Type | 0.448 | 2.284 | 0.007 |

* p < 0.1, ** p < 0.01, *** p < 0.001.

Table 5.

Regression analysis of Citizens data by selected zip code.

| Zip Code | R Square | Adjusted R Square | N | Sig. | Location |

|---|---|---|---|---|---|

| 32401 | 0.068 | −0.013 | 113 | 0.581 | On coast, center of track |

| 32403 | 1 | 1 | . | On coast, to the right of track | |

| 32404 | 0.077 | −0.03 | 87 | 0.689 | Inland, to the right of track |

| 32405 | 0.185 | 0.116 | 102 | 0.011 * | Inland near coast, center of track |

| 32407 | 0.371 | 0.233 | 50 | 0.015 * | On coast, left of track |

| 32408 | 0.095 | 0.042 | 162 | 0.076 * | On coast, left of track |

| 32409 | 0.941 | 0.802 | 10 | 0.072 * | Inland, left of track |

| 32413 | 0.096 | −0.052 | 64 | 0.749 | On coast, left of track |

| 32444 | 0.153 | 0.032 | 64 | 0.282 | Inland, center of track |

| 32456 | 0.577 | 0.354 | 26 | 0.044 * | On coast, right of track |

| 32466 | 1 | 5 | . | Inland, center of track |

* p < 0.1.

Table 6.

Comparison of means by roof shape.

| Percent Loss by Roof Shape Type—Means Comparison. | Mean | Median | N | Std. Deviation |

|---|---|---|---|---|

| All other roof types | 22.3259 | 8.3724 | 1172 | 30.1381 |

| Hip roofs | 13.7542 | 6.0737 | 295 | 20.4406 |

| Total | 20.6022 | 7.7445 | 1467 | 28.6554 |

Table 7.

Comparison of pre- and post-1995 construction.

| All Areas Impacted by Hurricane Michael | Mean | Median | N | Std. Deviation |

|---|---|---|---|---|

| pre-1995 | 22.8294 | 9.0556 | 1054 | 30.47203 |

| post-1995 | 14.9184 | 5.7146 | 413 | 22.43946 |

| Total | 20.6022 | 7.7445 | 1467 | 28.65543 |

| Bay County | Mean | Median | N | Std. Deviation |

| pre-1995 | 27.3005 | 12.7314 | 668 | 32.52479 |

| post-1995 | 16.576 | 6.8002 | 234 | 24.08371 |

| Total | 24.5183 | 10.7472 | 902 | 30.90696 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Grant, A.; Atkinson, C.L. Residential Wind Loss Mitigation Case Study: An Analysis of Insurance Claim Data for Hurricane Michael. Climate 2023, 11, 237. https://doi.org/10.3390/cli11120237

AMA Style

Grant A, Atkinson CL. Residential Wind Loss Mitigation Case Study: An Analysis of Insurance Claim Data for Hurricane Michael. Climate. 2023; 11(12):237. https://doi.org/10.3390/cli11120237

Chicago/Turabian StyleGrant, Aneurin, and Christopher L. Atkinson. 2023. "Residential Wind Loss Mitigation Case Study: An Analysis of Insurance Claim Data for Hurricane Michael" Climate 11, no. 12: 237. https://doi.org/10.3390/cli11120237

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.