1. Introduction

In the Internet of Things era, human life is intimately interconnected with digital technologies, such as thin-film transistor liquid-crystal displays (TFT-LCDs). Consumers rely on display panels to monitor their electrical devices, and growing demand has motivated the development of the TFT-LCD industry in the world. Although TFT-LCD manufacturing processes yield highly desirable products, such processes create undesirable byproducts in addition to producing pollution that can endanger the environment. Alarmed by climate change and roused to action by environmental education efforts, communities are calling for environmental protection. The common consensus is that a balance must be established among the environment, society, and governance (ESG) [

1]. This environmental consciousness guides consumers’ opinions when they make purchasing decisions. Numerous advanced countries have started to redefine economic development and growth from a different perspective. However, almost all electronic products still rely on display panels for monitoring and/or control, which are manufactured by TFT-LCD factories. Even though a particular industry might produce notable quantities of pollution, that industry can commit to a constant process of improvement to become sustainable. Hence, manufacturers can embed concepts of clean production, also called green production, in their governance plans for sustainable improvement to achieve an aura of eco-friendliness in response to corporate social responsibility (CSR). Furthermore, balanced development satisfies customers’ needs while protecting the environment; this market trend will continue to be necessary in the future [

2,

3,

4]. Therefore, the aim of this study was to develop the most effective sustainable improvement strategies for enhancing competitive advantages in real-world situations.

Before environmental awareness became widespread, the business term “competitive advantage” often referred to the pursuit of business goals, which usually meant profitability as a means to pay returns to investors and stakeholders. Stakeholders in different periods have sought different types of competitive advantage; the concept has evolved from the simple pursuit of economic growth to the maximization of ethical business. Financial performance has dominated the measurement of competitive advantage, but unsustainable growth at any cost causes short-sighted, short-term profits for corporations. Currently, companies have begun to pursue long-term and sustainable competitive advantage on the basis of the balanced scorecard (BSC) involving four dimensions: (1) Learning and Growth; (2) Internal Business Processes; (3) Customer; and (4) Financial. However, the interactions among the BSC dimensions necessitate seeking reasonable real-world solutions that are relevant to a manufacturer’s industrial characteristics [

5]. Because high-tech industries have numerous attributes that can be configured in various manners, grueling competition and complicated operational processes engender resource differentials and adequacy challenges; this is especially true in the TFT-LCD panel industry in Taiwan. This study integrated sustainability and competitive advantage concepts to develop the most effective solutions for enterprises that use natural resources.

Simon received the Nobel Prize in Economics in 1978 [

6] for ideas relating to sustainable competitive advantage and aspiration levels. A visionary TFT-LCD company must implement a systematic plan of sustainable improvement; this plan must grow into a comprehensive development map that combines the characteristics of the TFT-LCD panel industry with the BSC concepts of ecological responsibility. Comprehensive development maps (referred to as the influential network relation map (INRM)) and influential weights of DEMATEL-based ANP (DANP) may benefit from the DEMATEL (decision making trial and evaluation laboratory) technique, and modified VIKOR (VlseKriterijumska Optimizacija I Kompromisno Resenje, in Serbian) method challenges by integrating the BSC and the influential weights of DANP with a modified VIKOR (DANP-V). DANP-V has two main characteristics: (1) it can be analyzed under the guidelines of the appraisal program; and (2) it systematically approaches continuous improvement of its proposals. The modified VIKOR method in DANP-V can be used for bridging the performance gap by setting an “aspired-worst” benchmark to replace the “max–min” benchmark used in the conventional VIKOR approach (to avoid “picking only the best apple from a barrel of rotten apples”); this thus prevents the application of “piecemeal, stop-gap tactics” and enables achieving aspiration levels through systematic improvements based on INRM.

Since 1999, Taiwanese enterprises and the government have provided a considerable amount of talent, training, and finances to enable the TFT-LCD panel industry to obtain competitive advantage cutting-edge specialized field technology and patents because of their wide range and application in many types of electronic merchandise. The key players within the TFT-LCD manufacturing field are clustered in Taiwan and South Korea, constituting approximately 83% of the total worldwide TFT-LCD sales [

7]. The industrial structures of these two countries are quite different. Compared to the Korean TFT-LCD industry, which is built up by consortium support by National Plan, the Taiwanese TFT-LCD industry consists of small and medium firms that are merged into a group [

8]. Hence, the TFT-LCD panel industry business success of note, which affects the survival on a wide level, has become an indicator of Taiwanese industry. Within the past decades, numerous Taiwanese TFT-LCD panel companies have implemented cost reduction strategies and reduced the costs of production, and intense price competition was generated in the industry as an empirical real case. Taiwanese TFT-LCD firms were gradually losing ground to the competition in the global market. A resource integration strategy was executed by merging five major panel companies into two groups, Companies A and I; each group was assisted by the government and accounted for the formation of a duopoly market in Taiwan. However, these two companies still cannot effectively enhance their sustainable competitive advantage over competitors with the same technology level. TFT-LCD technology has to take into consideration the intense competition in the industry. These corporations are facing the pressure of upgrade sustainability capacity from advanced countries and the challenge to employ technology or raw materials to manufacture products in an environmentally friendly manner. If corporations do not have a standardized environmental protection policy, they cannot provide module or semi-finished products, particularly in electronic merchandise, to downstream manufacturers for produce and/or import to those advanced countries [

9,

10]. Therefore, the concept of sustainability has driven electronics firms to develop continuous improvement strategies intended to achieve an environmentally relevant aspiration level in Taiwan. Strategies of sustained competitive advantage for achieving the desired aspiration level are explained in terms of continuous improvement and sustainable development in the context of existing interrelationships. Through the analysis of the two companies’ architectures of performance, the problem is explained and solutions that create sustainable competitive advantage are discussed.

The research topic of this study is as follows: two major Taiwanese TFT-LCD companies are gaining consumers in advanced countries with the rise and spread of environmental awareness and face the early implementation of a cleaner production program towards the approach of sustainable development of enterprises to maintain a business competitive advantage. Sustainable development is a continuous improvement progress, thus companies will need to continue investing resources for improving ability to achieve the expectation goal in the future. However, understanding how to invest and improve in the right path for systematically sustainable development is an urgent and important issue.

The main contribution of this study is the comprehensive solution for two major TFT-LCD companies to deal with the fundamental problem (gap) of clearly understanding how to implement the company operations for sustainable development in real-world situations. Furthermore, this study also found the requirement to keep investing in the continuously improving path (INRM) with a resource integration relationship to bridge the gap, in order to make the cooperation plan of these two TFT-LCD companies toward achieving aspiration levels in the future.

The remainder of this paper is organized as follows.

Section 2 presents a literature review to establish the indicator framework, and

Section 3 presents the DANP-V method.

Section 4 reviews the empirical facts regarding TFT-LCD companies in Taiwan, and

Section 5 presents conclusions.

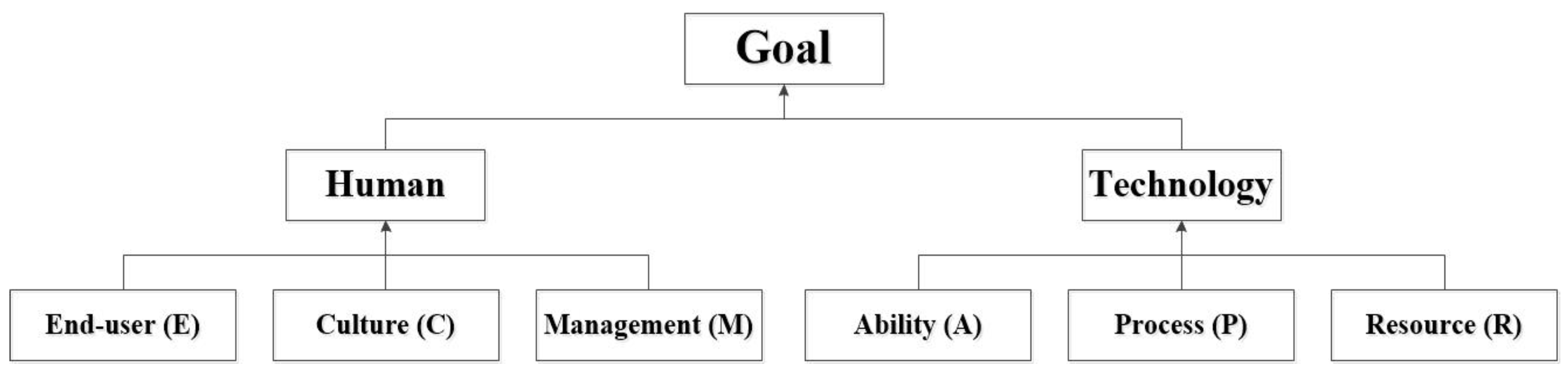

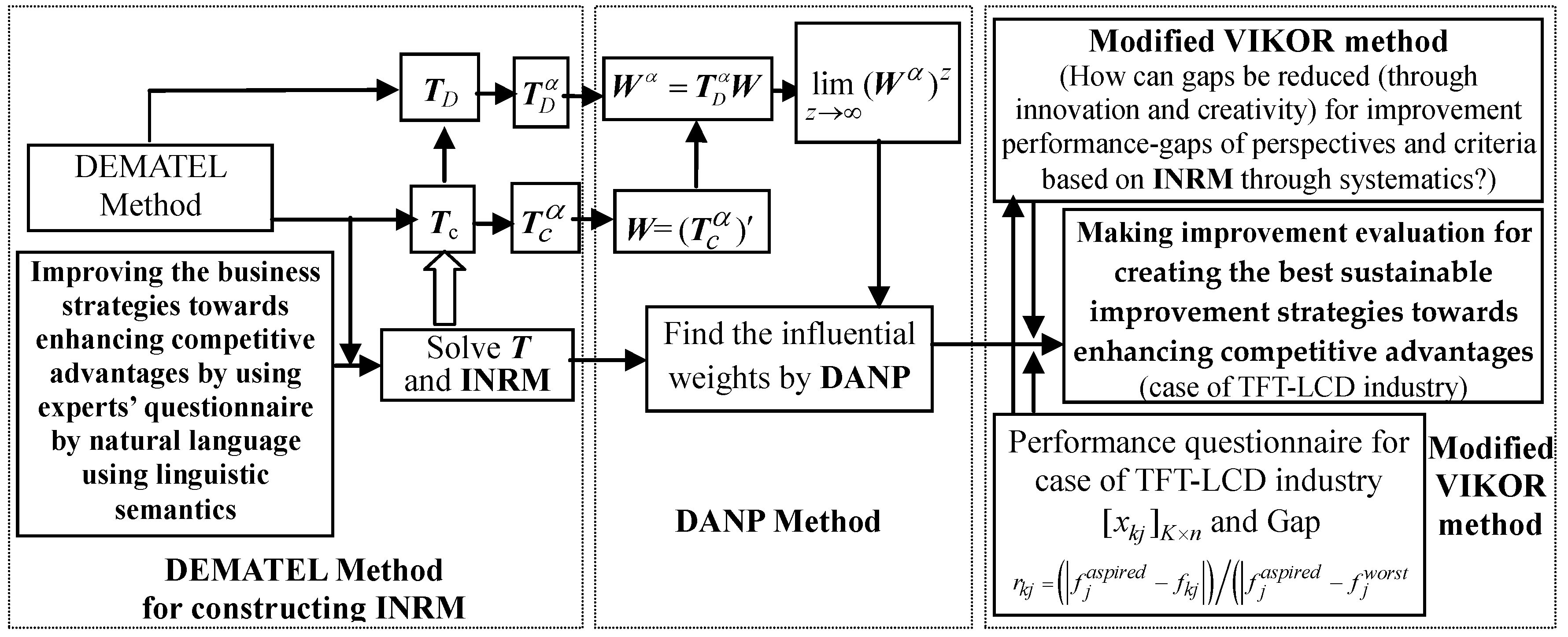

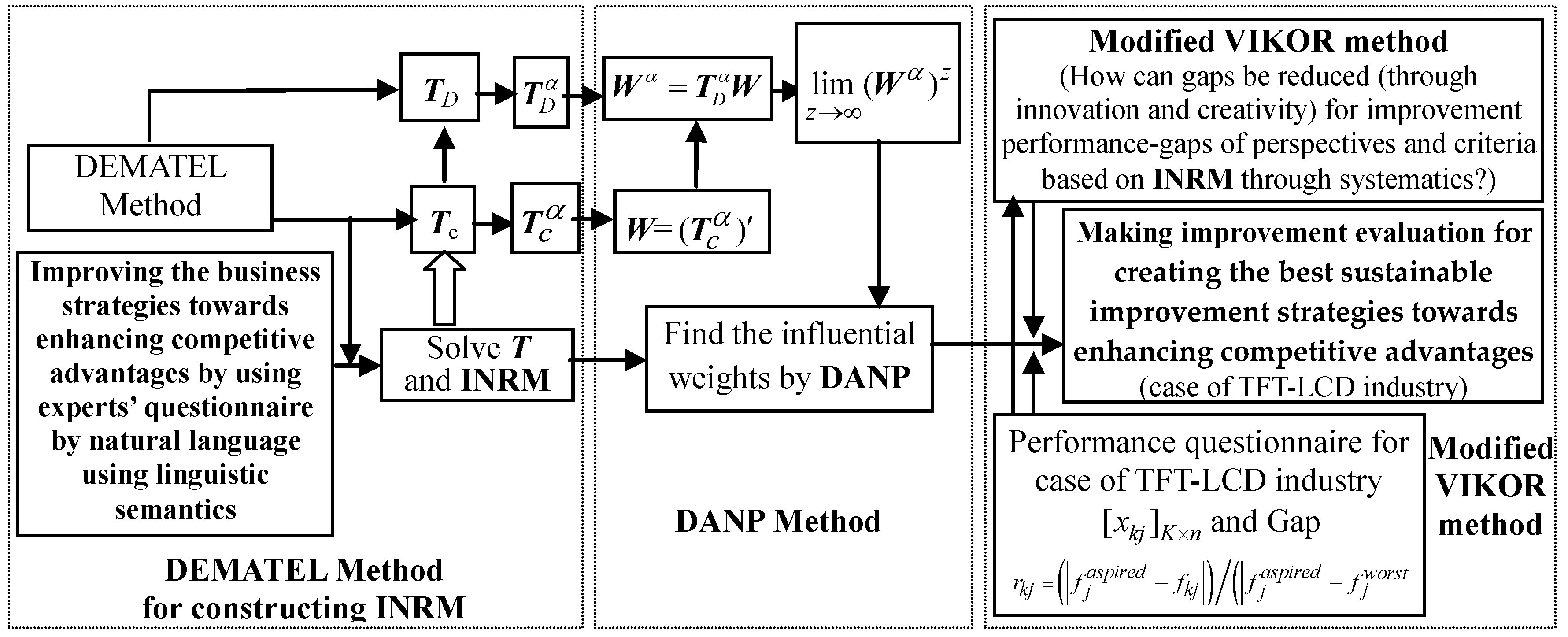

3. Method: DANP-V Model

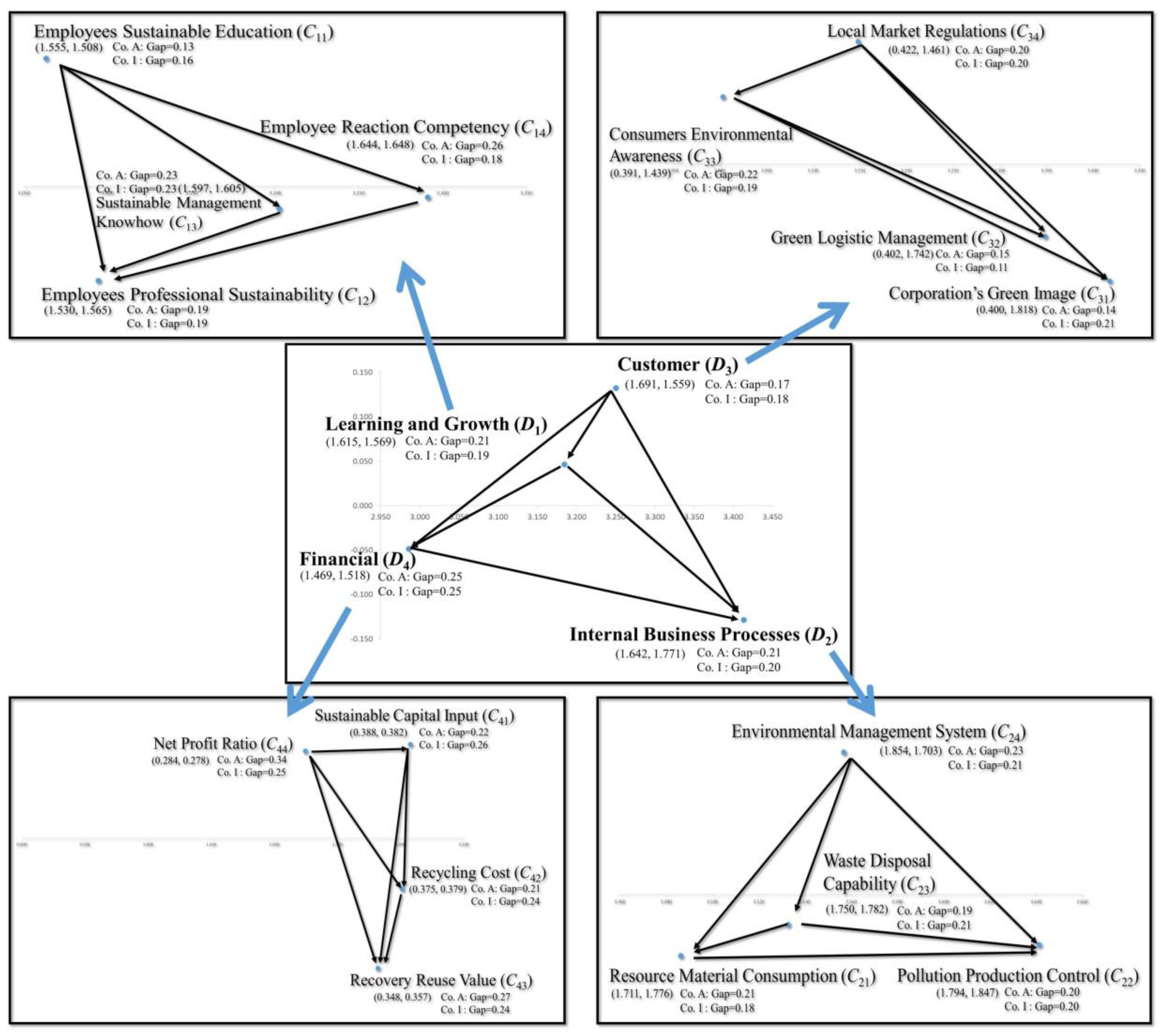

This study used a hybrid modified MADM model combined with the DEMATEL technique to construct the INRM (

Figure 2,

Figure 3 and

Figure 4). The influential weights (IWs) of the DANP were calculated to confirm the causes and effects associated with each perspective and criterion in the existing relationships and to measure and evaluate the importance of each factor. The DANP-V model is a hybrid modified MADM model, also called the modified VIKOR-DANP model [

27], developed on the basis of the aforementioned studies, and it is appropriate for assessing and improving business competitiveness [

91] and bridging the performance gaps in each criterion. The dimensions and criteria were generated using the DEMATEL technique to construct the INRM and determine the IWs through a procedure of the DANP, which is a hybrid adopting the basic ANP concept by Saaty [

84] and using the DEMATEL technique (Equations (7)–(12)). The global weights can also be obtained using the influence relation matrix through these hybrid methods [

28]. Because the influence level is a characteristic of the weights, this study referred to these as the IWs of DANP [

28,

29,

30,

31,

32,

33,

92,

93,

94,

95]. The modified VIKOR method was then used to calculate the ratio of the gap between the real performance

and the aspiration level

in the alternative

k of criterion

j ; that is

such that the calculations of the IWs are integrated among various programs. Finally, the problems of each program were determined through the modified VIKOR method (If the gap value of a criterion is larger, the problems are more acute and should receive priority for improvement). The INRM was applied to determine the crux criterion through path analysis of influential directions among criteria to identify the cause of the problem and to determine how to formulate improvement strategies through systematics [

29] to avoid the “stop-gap piecemeal practice” [

30,

31,

33,

92,

93,

94,

95].

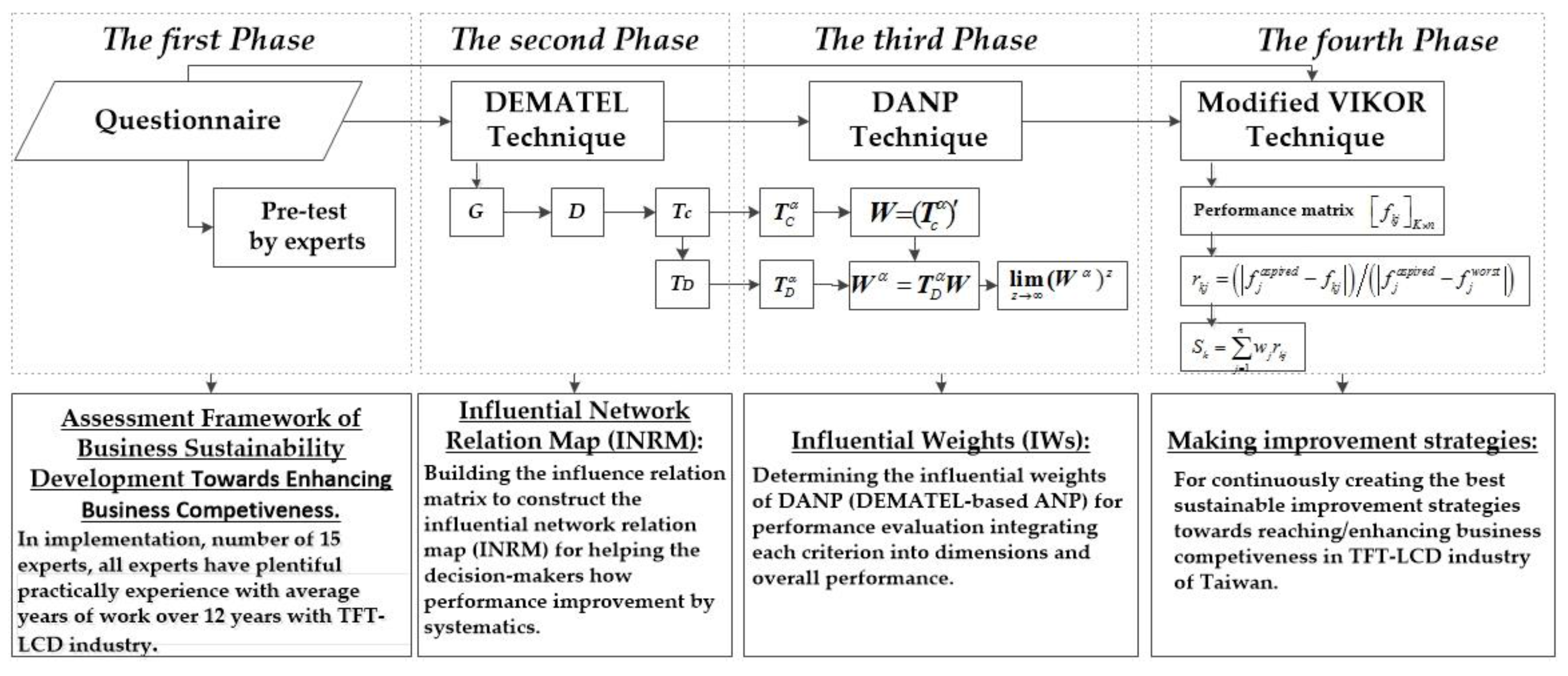

In this study, the DANP-V model was executed in four phases [

31]: the first phase was a pretest of the measures in the framework, the second phase established the comprehensive, influential network diagram, the third phase entailed determining the correct training value of IWs, and the fourth phase involved programs for developing improvement strategies, as shown in

Figure 2.

The main purpose of the first phase was to determine the degree of influence of each criterion on the research goal on the basis of experience of experts to ensure the reliability of the overall study. A questionnaire was designed and divided into two parts: the first part applied a 5-point Likert scale on which some of the experts evaluated the importance of each criterion; the second part of the questionnaire comprised open-answer items for enhancing the quality of the questionnaire through experts’ sharing of their experience and modified the criteria and connotations. The expert questionnaires were used to survey senior practitioners of sustainable development in the TFT-LCD industry. The selected criteria were identified by experts in fields relevant to the TFT-LCD industry. An appointment was made in advance, and the experts were asked when they could complete the expert questionnaires; the survey was then conducted. The personal information of the experts interviewed was kept confidential in accordance with the principles of research ethics. Only the relevant basic information required for this survey was disclosed. All experts had considerable practical experience, with average years of work of over 12 years within the TFT-LCD industry; they were serving as persons in charge of sustainable development duties. The experts had received Ph.D. and Master’s degrees relevant to the field as academia, industry, and government representatives.

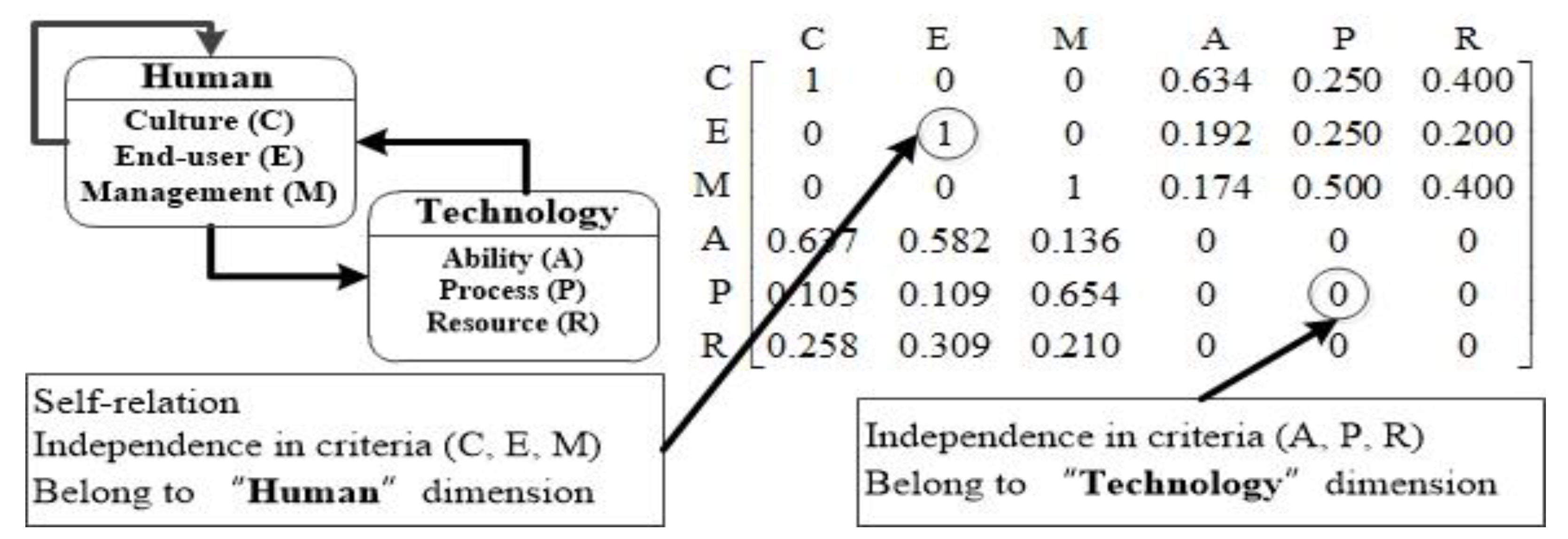

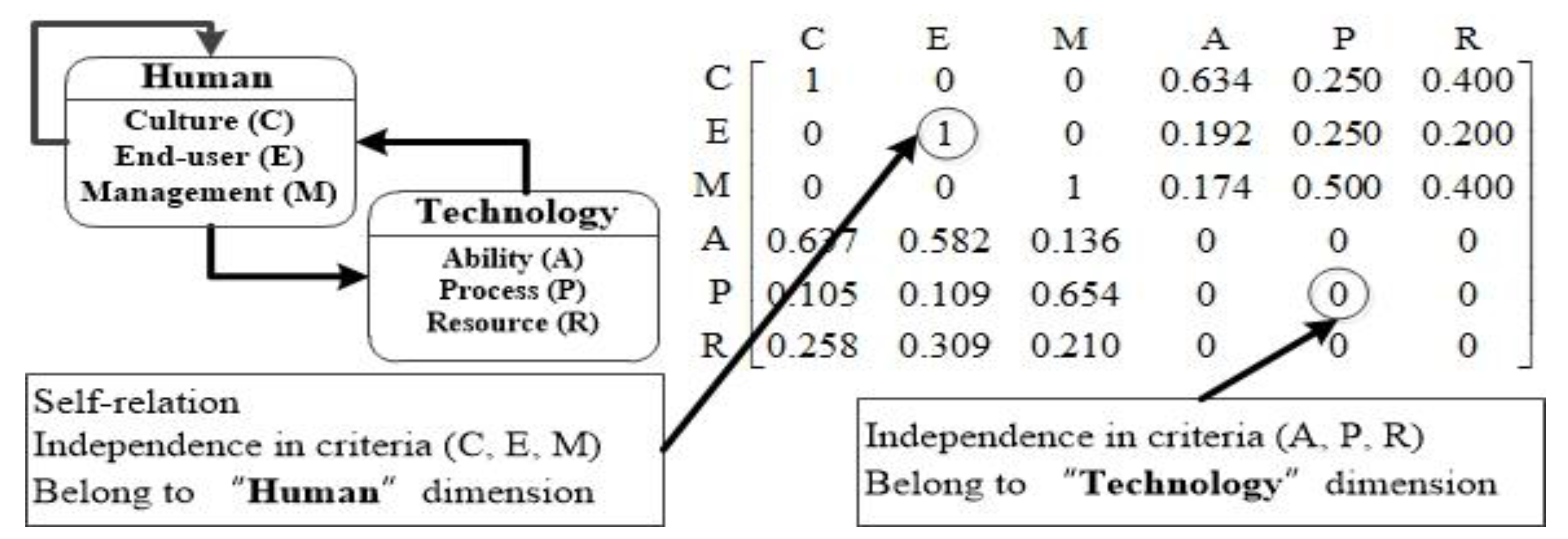

The second phase entailed establishing a comprehensive INRM through a systematic thought process. This phase of the survey involved a pair of experts who compared the degree of influence between the criterion value, aggregated it into a matrix that was initialized, and then by using the DEMATEL technique calculated the dimensions (

) and criteria (

) of the total influence relation matrix [

83]. The INRM was constructed on the basis of the influence intensity among dimensions (

) and criteria (

) and then overlapped it; the overall effect diagram (see INRM in

Figure 4) was then completed.

The third phase involved the DEMATEL technique, which is detailed as follows:

Step 1: Calculate the direct influence relation average matrix . Assume the number of experts to be H and number of criteria to be n. The pairwise comparisons between any two criteria are assigned and denoted by an integer score of 0, 1, 2, 3, or 4, representing the range from “absolutely no influence (0)” to “very high influence (4)” according to natural language (e.g., semantics) and denoting the degree to which each criterion

i affects each criterion

j. The answers by each expert form a

nonnegative matrix

where

are the answer matrices of the

H experts with practical experience, and the elements of

are denoted by

from expert

H (

h = 1, 2,‖,

H). Therefore, an

average matrix

of all experts given can be constructed using Equation (1).

The average score of the H experts is . The average matrix is called the initial direct relation matrix and represents the degree of influence that one criterion exerts on another criterion as well as the degree of influence it receives from other criteria.

Step 2: Normalize the initial direct influence relation matrix. The normalized initial direct influence relation matrix

is acquired by normalizing the average matrix G. The matrix

is easily derived from Equations (2) and (3), in which all principal diagonal criteria are equal to 0:

Step 3: Obtain the total influence-relation matrix . A continual decrease in the indirect effects of problems was observed with the increasing powers of the matrix

, for example,

and

for

, where

is an

unit matrix. The total influence relation matrix

is an

matrix, and is defined by

as shown in Equation (4).

where

,

,

(when

),

,

and

, and at least one row or column of the summation, but not all, equals one; then,

can be guaranteed.

Using the total influence relation matrix

, (

by criteria and

by dimensions), the INRM can be acquired according to Equation (4). Equations (5) and (6) are used to generate each row sum and column sum in the matrix

, respectively.

where

is the row sum in the total influence relation matrix

, which represents the total effects (both direct and indirect) of a criterion or perspective

i on all other criteria or perspectives

. Similarly,

is the column sum in the total influence relation matrix

, which represents the total effects (both direct and indirect) that a criterion or perspective

j receives from all other criteria or perspectives

. Therefore, when

i =

j,

offers an index of the strength of the total influences given and received; that is,

indicates the degree of importance of the criterion or perspective

i in the system. In addition,

provides an index of the degree of the cause of total influence. If

is positive, then the criterion or perspective

i is a net causer, and if

is negative, then the criterion or perspective

i is a net receiver.

The third phase involved assigning weights to training data. The total influence relation matrix (

and

) of the second phase was determined using the basic ANP concept [

79,

84], and the proposed training processes affected the accuracy of the values; this method is called the DANP.

The IWs can be obtained through the DANP as follows (see

Appendix B.3 DEMATEL-based technique to determine the IWs in DANP (DEMATEL-based ANP):

Step 1: Total influence relation matrix . The DEMATEL technique is used to construct the total influence relation matrix

from each perspective (dimension or cluster), with different degrees of influence relation for the criteria, as shown in Equation (7), where

,

, and

as an

matrix.

where

is the

mth cluster,

is the

mth criterion in the

mth dimension, and

is a submatrix of the influence relation obtained from a comparison of the criteria of the

ith and

jth dimensions. In addition, if the

ith dimension has no influence on the

jth dimension, then submatrix

shows independence (no influence relation) in every other criterion.

Step 2: Form an un-weighted super-matrix . Normalize the total influence relation matrix

as shown in Equation (8).

where

denotes the normalized total influence relation matrix. Similarly,

can be obtained.

According to pairwise comparisons with the criteria and the basic concept of the ANP, the un-weighted super-matrix

can be obtained by transposing the normalized influence-relation matrix

(basic ANP concept in the form of un-weighted supermatrix; see

Appendix B.1 AHP and

Appendix B.2. ANP) by dimensions (clusters); that is,

, as shown in Equation (9).

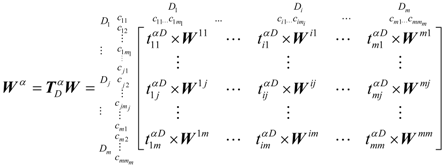

Step 3: Obtain the weighted super-matrix . The total influence-relation matrix of dimensions is derived according to the DEMATEL technique, as presented as following matrix.

The normalized total influence-relation matrix of dimensions can be obtained through the total influence-relation matrix divided by , , as shown in Equation (10).

The normalized , unweighted super-matrix (shown as Equation (9)), and weighted super-matrix (normalized super-matrix) can be easily obtained through Equation (11), where is a scalar and .

Step 4: Calculate the limit of the super-matrix . Limit the weighted super-matrix by raising it to the zth power until it has converged and become a stable super-matrix. The global priority vectors are obtained, which are called the IWs of the DANP, such as , where z represents any number.

In brief, according to the aforementioned process, the INRM and IWs can be obtained and can be used in resolving the problem of interdependence and feedback to develop the most effective systematic improvement strategies for reducing the gaps in criterion performance, such that all criteria facilitate achievement of the aspiration level.

The fourth phase entailed developing the most effective sustainable improvement strategies for enhancing competitive advantages in the TFT-LCD industry. The gaps can be calculated using the modified VIKOR method, which entails considering each absolute distance between performance values and adopting the aspiration level and worst value, called “aspired-worst”, as benchmarks [

80,

81,

82,

83,

85,

93,

94,

95,

96], rather than using the relative distance and adopting positive and negative ideal points, called “max-min”, as the benchmarks as in the conventional VIKOR method [

86,

87,

88,

93,

94,

95,

96]. Accordingly, the phase involved solving problems through the modified VIKOR programs in the problem criteria; the INRM was then used to identify the crux of the criteria (the criteria on the impact of the problem criteria). The conventional and modified VIKOR methods are compared to demonstrate the concept of continual improvement in sustainability. Finally, the reasons for the impact of the criteria through the crux are elucidated for developing the most effective improvement strategies for reaching the aspiration level.

The fourth phase: The modified VIKOR method is described as follows:

Step 1: Derive the positive and negative-ideal solutions for replacing the aspiration levels and worst value to fit the current real-world situation. Define the aspiration level in the j criterion and worst value for all criteria , which can be converted from the conventional form into the modified form.

- (1)

The conventional approach for deriving the positive- and negative-ideal solutions as the benchmarks (max-min) is illustrated as follows.

Positive-ideal solution: where ;

Negative-ideal solution: where

- (2)

The modified approach for replacing the aspiration level and worst value as the benchmark (“aspired-worst”) is shown as follows.

Aspiration level: , where is an aspiration level, called the most effective value;

Worst values: , where is a worst value.

In this study, performance scores ranging from 0 to 100 (very bad ← 0, 10, 20, ..., 90, 100 very good) were used according to natural language (e.g., linguistic/semantic) in the questionnaire, therefore, the aspiration level takes the highest score of 100, and the worst value takes the value of 0. Hence, is defined as the aspiration level and as the worst value; this can prevent “choosing the most effective option from a set of substandard options”. In other words, it can prevent “picking the most effective apple from a barrel of rotten apples”.

Step 2: Determine the mean group utility for the gap. can be calculated using Equation (12):

where

is defined as the normalized ratio of the distance to the aspiration level, which implies the synthesized gaps for the criteria;

indicates the IWs of the criteria obtained from the DANP (called DANP-V, see

Appendix B.4 Modified VIKOR; and

indicates the normalized gap (shown as

) of the distance to the aspiration level.

The modified VIKOR method can be used for ranking and selecting alternatives and bridging performance gaps by evaluating all criteria, based on the INRM acquired through systematics, to avoid the “stop-gap piecemeal practice” and “pick the most effective apple from a barrel of rotten apples”. Moreover, it can be used to solve any daily or single problem (i.e., only one problem, no other alternatives) for bridging the performance-gap by considering all perspectives (dimensions) and criteria [

81].

5. Conclusions

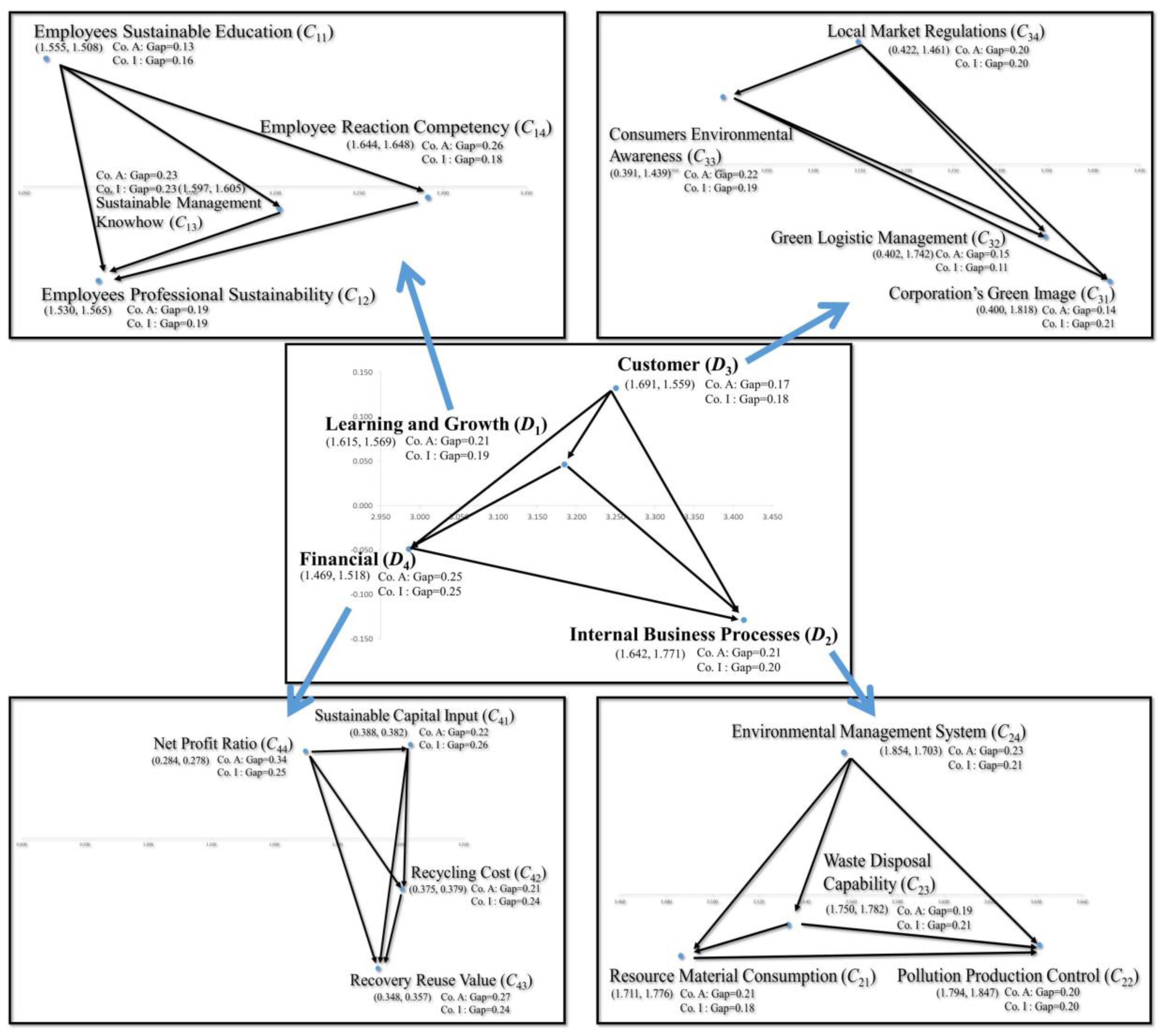

This study successfully integrates sustainability and competitive advantage concepts to formulate the most effective allocation strategies for natural resources. This study considers sustainable competitive advantage as an aspiration level. The transmission characteristics of the TFT-LCD panel industry development guidelines are thus integrated with BSC concepts of environmental responsibility to establish an assessment framework. Through the integration of sustainability, competitive advantage, and BSC, the original four BSC dimensions and characteristics of the TFT-LCD panel industry are consolidated with environmental concepts and condensed into the 16 indicators of the DANP-V model of sustainable competitive advantage. The DANP-V model is refined and debugged and then used to conduct a case study on two Taiwanese TFT-LCD manufacturers, namely Companies A and I.

The findings of the case study are outlined as follows:

(1) Companies A and I show only a small performance gap; the overall performance of Company I (79.66) is higher than that of Company A (79.05), and the performance of Company I is superior to that of Company A in three of four dimensions, namely Learning and Growth (D1), Internal Business Processes (D2), and Financial (D4). However, in the Customer (D3) dimension, Company A is superior to Company I. Furthermore, for both companies, the performance levels on each dimension demonstrate slight advantages and disadvantages. Even though programs do not have easily distinguishable characteristics, the DANP-V method avoids the need to “pick the most effective apple from a barrel of rotten apples”.

(2) The proposed method can identify performance gaps, explain those gaps according to the INRM, and achieve lasting solutions that are not limited by “stop-gap piecemeal practices”. Currently, both companies must improve their performance in the financial dimension to achieve sustainable development and sustainable competitive advantages; cooperation is thus proposed to improve both companies. Nevertheless, the two companies present different criteria gaps. Hence, different strategies are required to improve these two companies; the heterogeneity of the backgrounds and current states of the companies are detailed in

Section 4.3.1,

Section 4.3.2,

Section 4.3.3 and

Section 4.3.4, respectively.

Because the TFT-LCD industry has complex processes, a duopoly market, and special technology patterns that induce environmental effects in Taiwan, this and follow-up studies must conform to the limitations of the industry. Follow-up studies may be designed to address loosely defined questions. Because the small- and medium-sized firms of the TFT-LCD panel industry are crucial to Taiwan, future research may focus on challenges specific to Taiwan. However, international manufacturers may use the DANP-V method to examine TFT-LCD manufacturing outside Taiwan. The present research establishes a set of indicators of sustainable competitive advantage for Taiwan. Multinational manufacturers may find that the present indicators are not suitable for other countries.

The special characteristics of Taiwan’s TFT-LCD industry include its complex processes, special environmental effects, and domestic and overseas duopoly markets. Future research may propose a newly modified hybrid of multi-attribute decision making (MADM) and multi-objective decision making (MODM); such research may propose novel improvement strategies to reach aspiration levels. Classical MODM is based on a fixed set of conditions or resources, called the “decision space”, and seeks a Pareto-optimal solution in a fixed feasible region, called the “objective space”. Moreover, future research may propose models with changeable decision spaces and objective spaces to implement and enforce sustainable improvement without being limited to Pareto optimality. Achieving an aspiration level is more useful than achieving Pareto optimality; new MADM solutions may enhance manufacturers’ performance levels for aspiration levels in criteria, dimensions, innovation, and creativity. This new thinking in changeable space programming may help decision makers to achieve win–win planning and to achieve desired aspiration levels that are preferable to Pareto-optimal solutions and ideal points [

96,

99,

100,

101,

102].

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}