Understanding Global Supply Chains and Seafood Markets for the Rebuilding Prospects of Northern Gulf Cod Fisheries

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

:1. Introduction

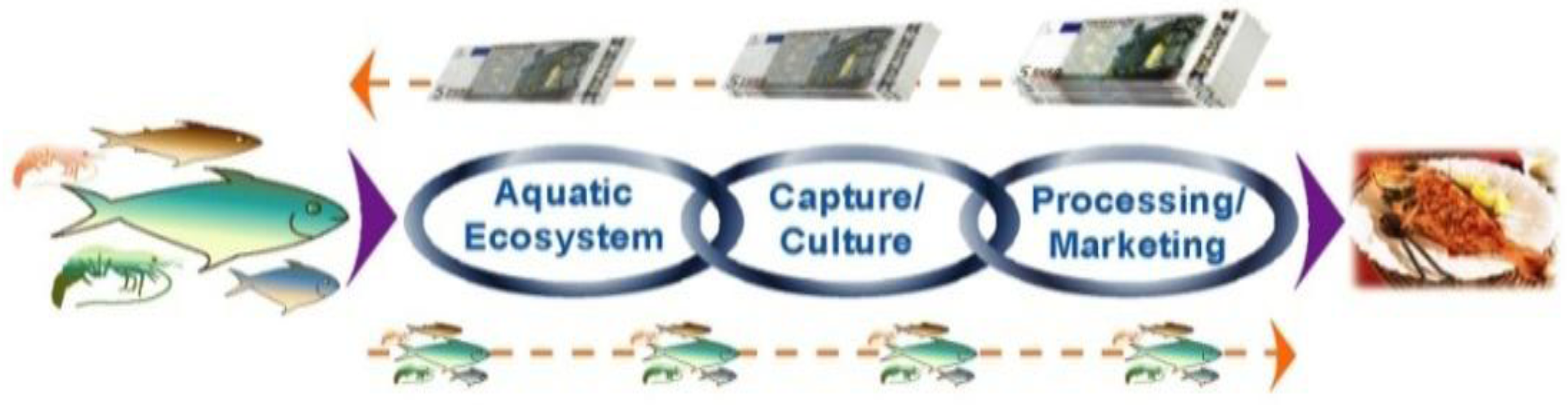

2. Conceptual and Analytical Approach

- The analysis of seafood production goes beyond the firm level and considers contributions from community small-scale fisheries and their spill-over and multiplier effects in regional and national economic development [24];

- The meaningful contributions and role of various fisheries institutions (the state, the private sector and civil society organizations) can be negotiated in terms of who pays for management cost and who benefits in the long term bearing in mind demographic changes and future access rights [25];

3. Methods

4. Results and Analyses

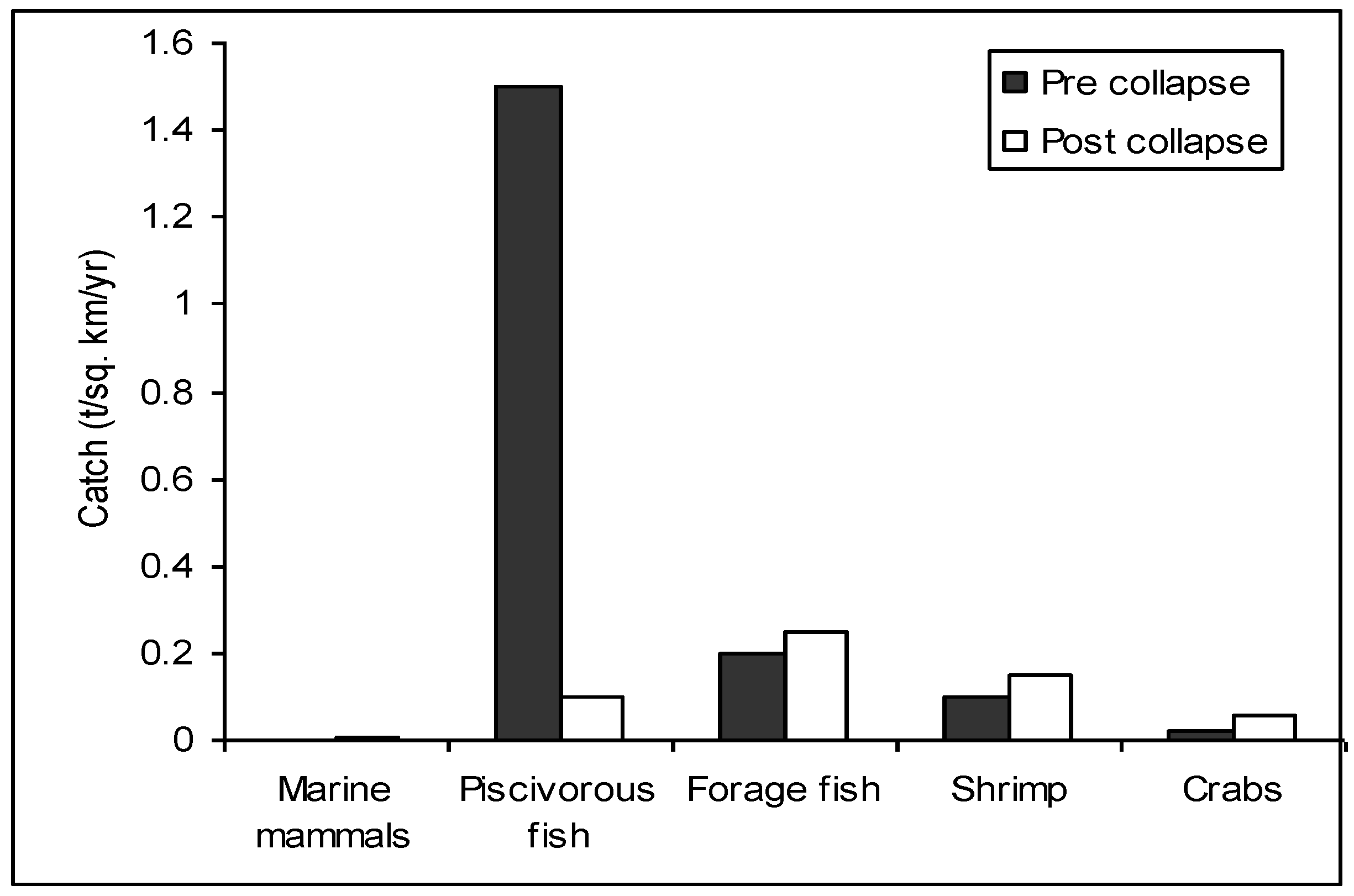

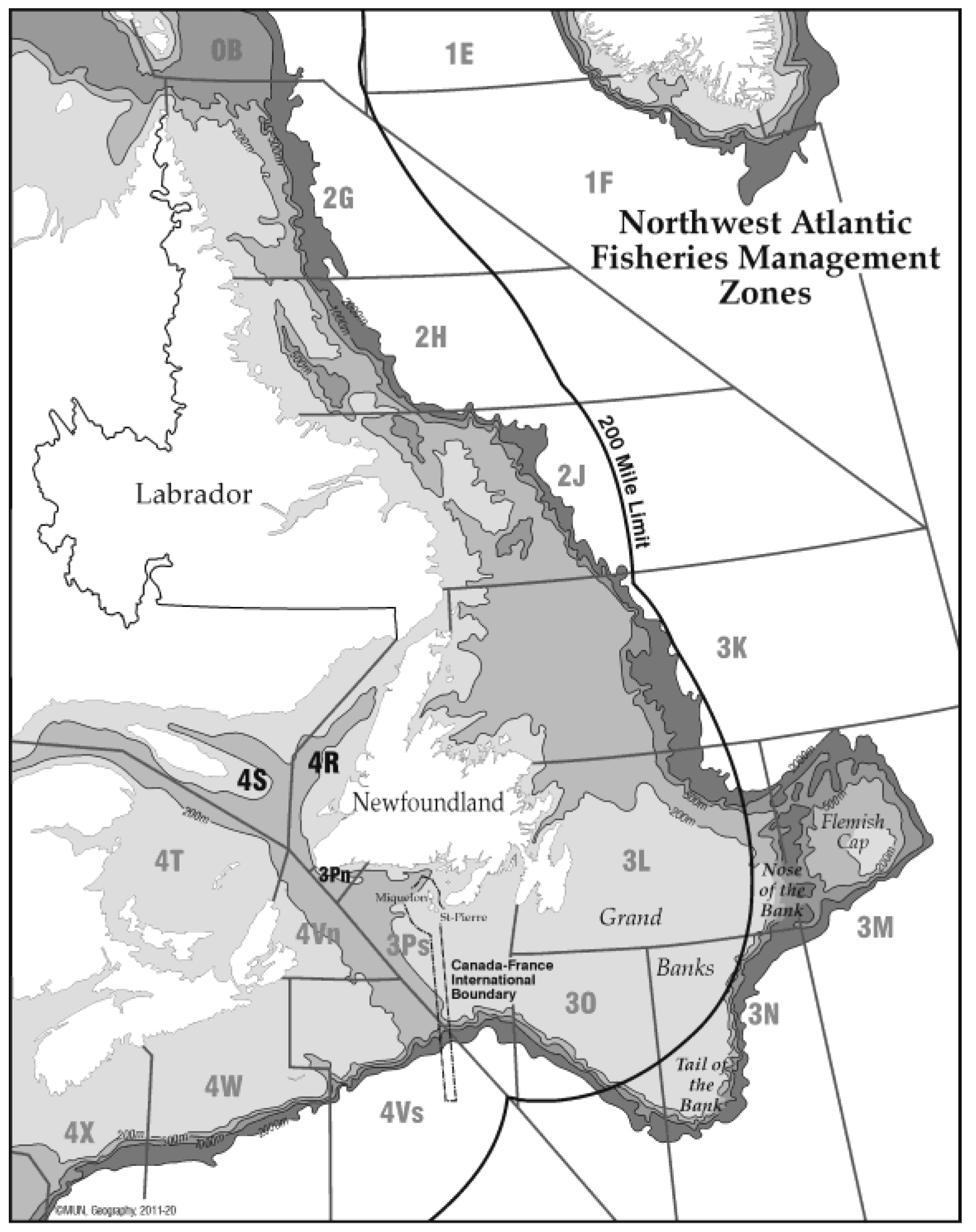

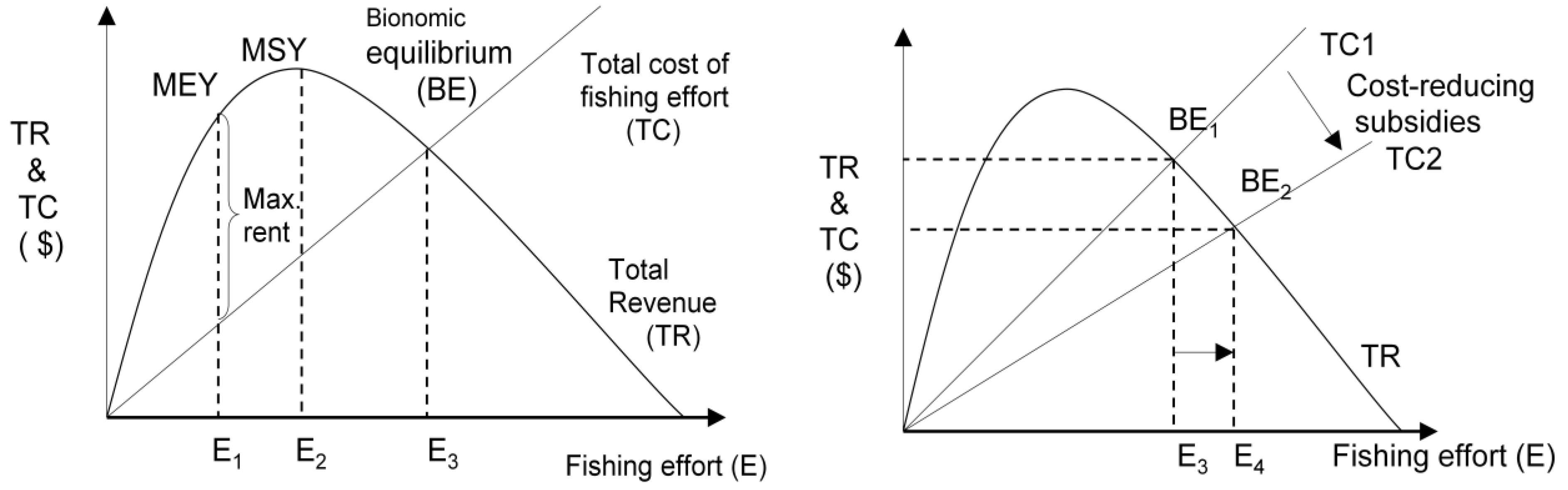

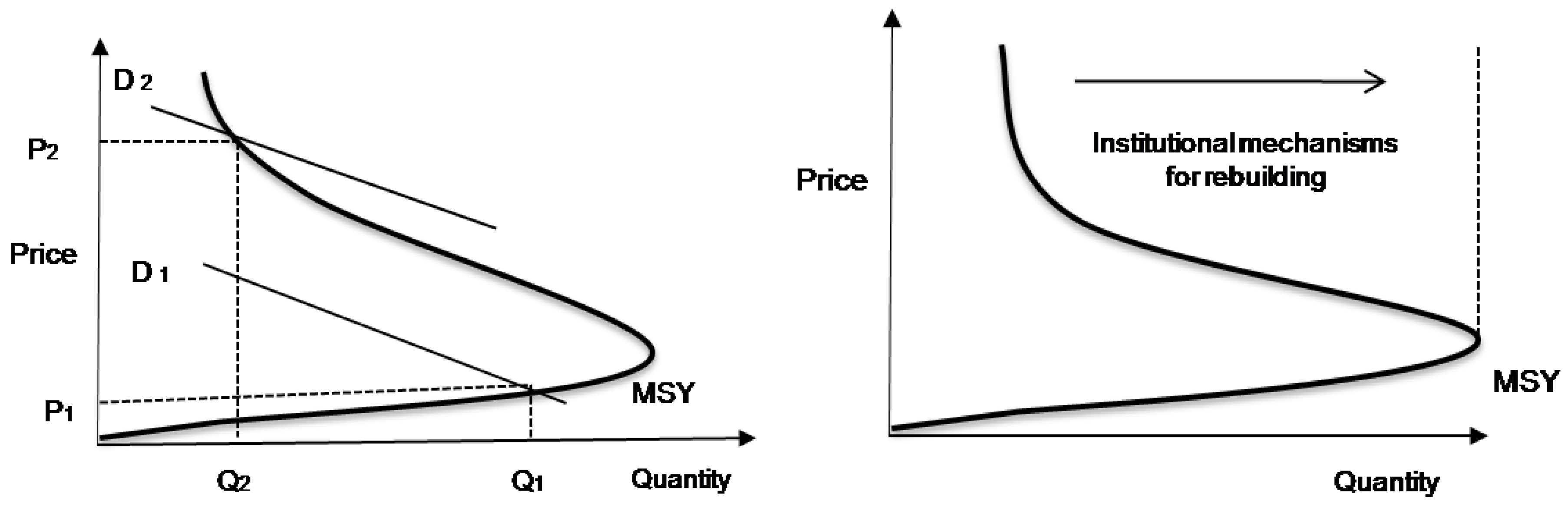

4.1 Raw Material Supply and Resource Sustainability

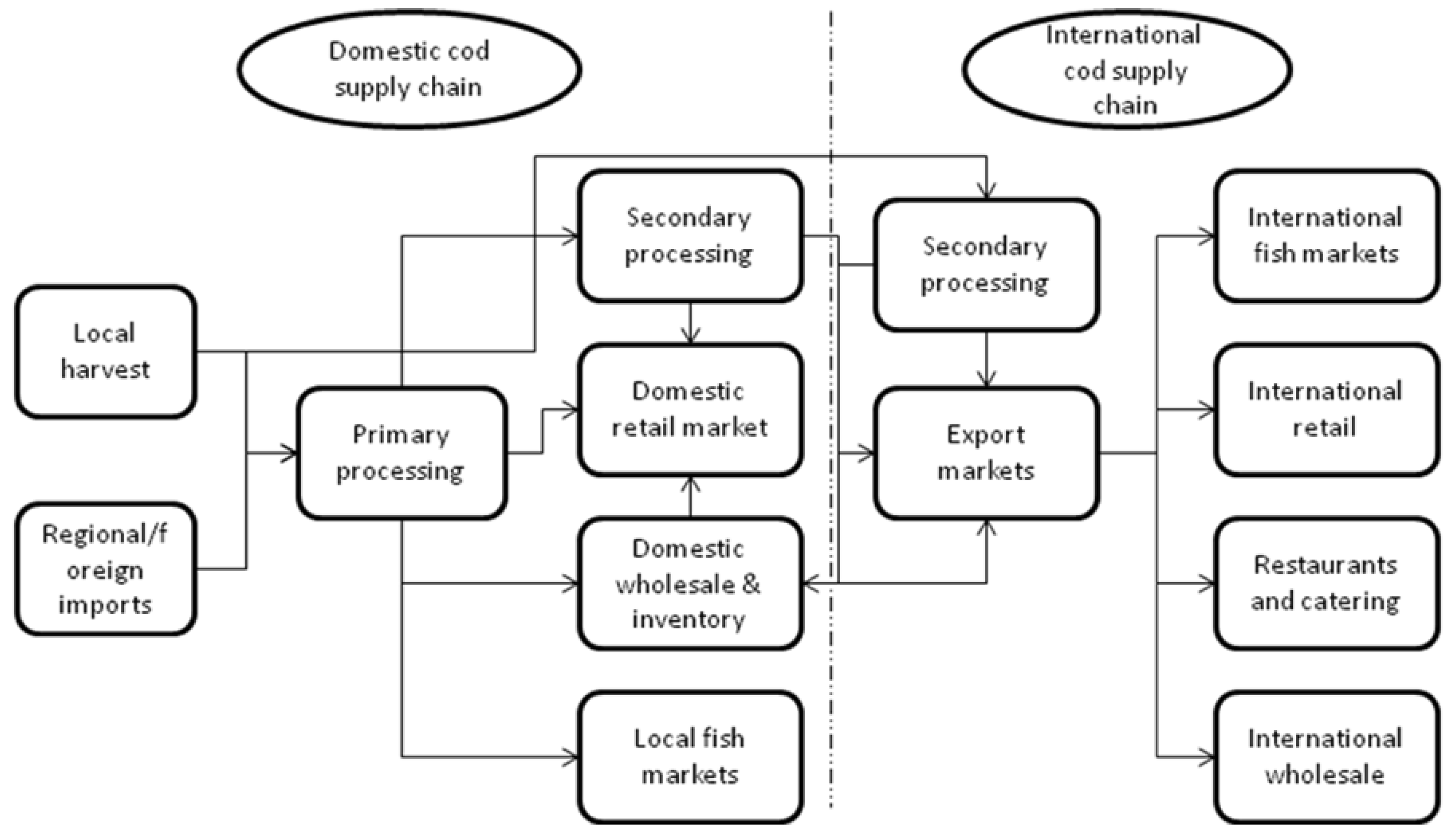

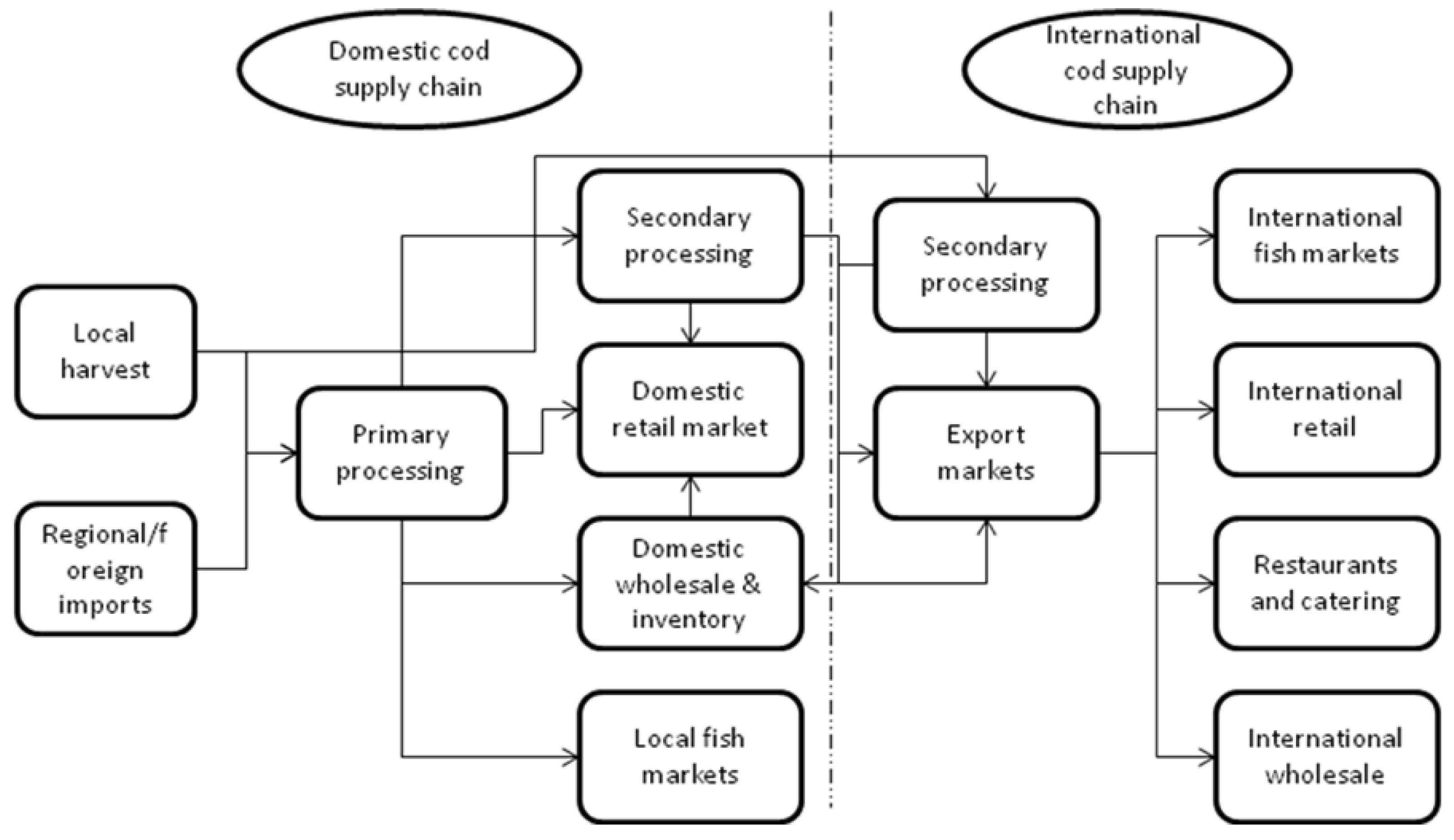

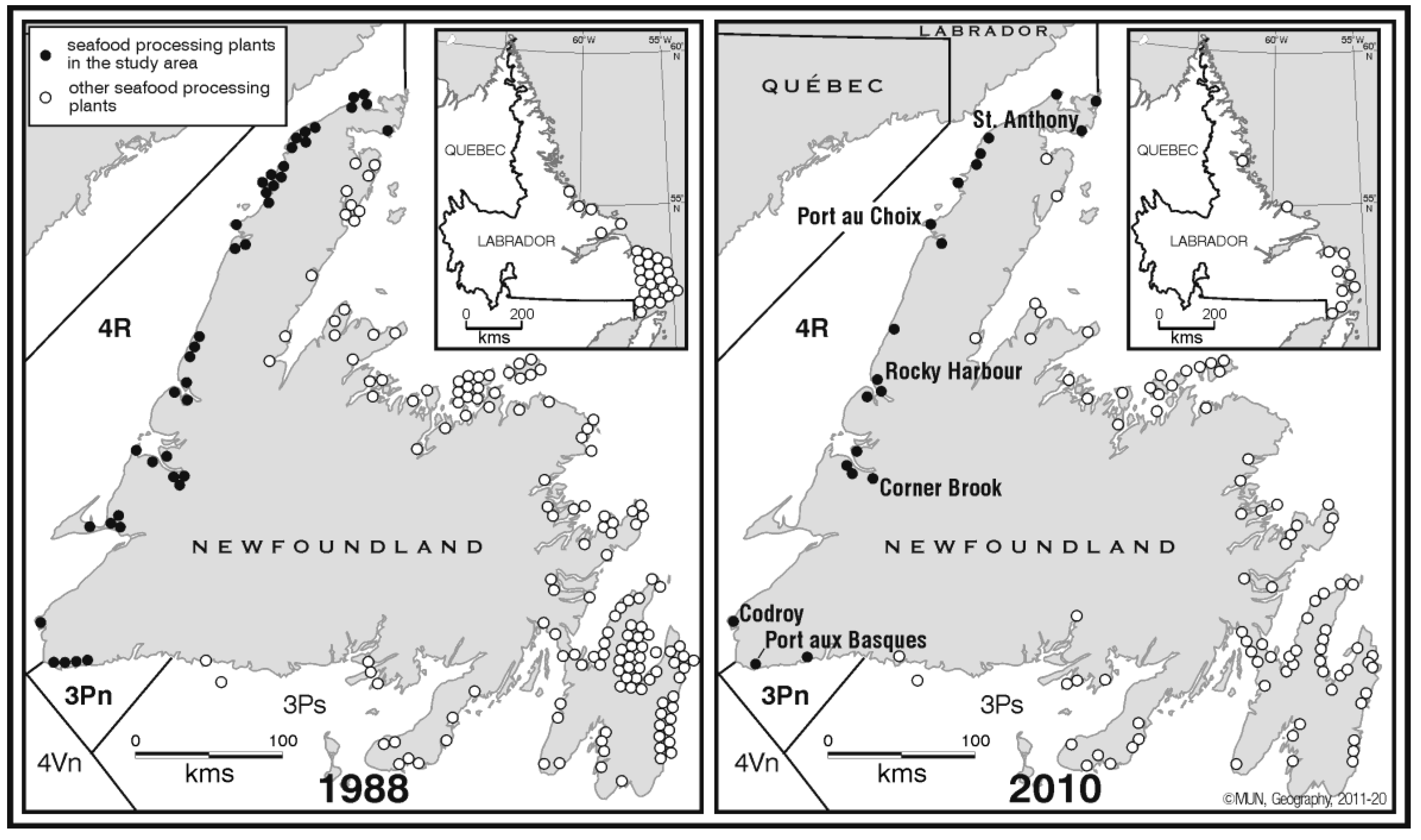

4.2 Restructuring and Organizational Changes in Seafood Production

“…you are going to have to manage it in a very different way than we used to. We have to come up with a new concept…The cod right now is a nuisance, because it’s a nuisance in by-catch. This guy is fishing turbot, but he can’t fish it because of all the [juvenile] cod. The other thing is, he is looking at cod as a predator of small shrimp and crab, and right now they’ve spent tens of thousands in changing from cod to shrimp and crab fishery. They don’t want to go back to cod; right now cod is a nuisance” (emphasis added).

4.3 Economic Viability and Coastal Community Sustainability

“The fishery is going belly up for the small [scale] man. I think if you can afford to be there, you are going to be there. And if you can’t afford to be there, if you can’t afford to spend thirty, forty thousand dollars a year, you aren’t going to stay into the fishery. I’ll be paying off credit card payments until fishing next spring to pay off what I spent in to it this year…I haven’t broke even in the last four or five years…”

“…the Canadian dollar is up now. That got a reflection in the market place and that got a reflection on the price you pay to the fishermen. I went back about two weeks ago and looked at what the exchange rate was last year; it was 21 cents. Right now we’re less than five. That’s a big difference. You’re looking at probably 18 cents difference on a pound of filets. That’s a lot of money. Every hundred thousand pounds of filets is 18,000 dollars.”

“We were getting in 1986; we got close to a dollar a pound. That was a good price. Here we are today, 24 years later, we got 37 cents this year…You can’t do that right [?]…We got to look at our expenses and that…we got to have at least 60 cents a pound to survive. Cod should be close to a dollar a pound.”

4.4 Institutional Capacity and Legislative Changes

“…we’ve learned next to nothing since the collapse….all I know is that our existing legislation is inadequate…The Americans have had success, and what I like about it, everybody knows what the objectives and timelines are. It has to be taken out of the political hands. Our current system is terrible with the amount of input the industry has…It will never go away unless we have some kind of legislation…”

5. Summary and Conclusion

Acknowledgements

Conflict of Interests

References

- DFO, Assessment of Cod in the Northern Gulf of St. Lawrence; DFO Canadian Science Advisory Secretariat: Ottawa, Ontario, Canada, 2010.

- DFO, Canadian Fisheries Statistics 2006; Department of Fisheries and Oceans, Economics Analysis and Statistics Policy Sector: Ottawa, ON, Canada, 2008.

- FAO, The State of World Fisheries and Aquaculture in 2008; Food and Agricultural Organization: Rome, Italy, 2010.

- Government of Newfoundland and Labrador, Department of Fisheries and Aquaculture. Seafood Industry Year in Review 2010. Available online: http://www.fishaq.gov.nl.ca/publications/yir_2009.pdf (accessed on 1 June 2010).

- GNPFT, Final Report on the Fishing Industry of the Great Northern Peninsula; Nordic Economic Development Corporation and Red Ochre Regional Board Inc: St. Barbe, Parsons Pond, NL, Canada, 2006.

- Khan, A.; Neis, B. The rebuilding imperative in fisheries: Clumsy solutions for wicked problems? Progr. Oceanogr. 2010, 87, 347–356. [Google Scholar] [CrossRef]

- Gordon, H.S. The economic theory of common property resource: The fishery. J. Polit. Econ. 1954, 62, 124–143. [Google Scholar]

- Schaefer, M.A. Some aspects of the dynamics of populations important to the management of the commercial marine fisheries. Bulletin of the Inter American Tropical Tuna Commission 1954, 1, 25–26. [Google Scholar]

- Clark, C.W. The Worldwide Crisis in Fisheries: Economic Models and Human Behavior; Cambridge University Press: Cambridge, MA, USA, 2006. [Google Scholar]

- Munro, G.; Sumaila, U.R. Subsidies and their potential impact on the management of the ecosystems of the North Atlantic. Fish Fish. 2002, 3, 233–250. [Google Scholar]

- Khan, A.S.; Sumaila, U.R.; Watson, R.; Munro, G.; Pauly, D. The Nature and Magnitude of Global Non-Fuel Fisheries Subsidies. In Catching More Bait: A Bottom-Up Re-Estimation of Global Fisheries Subsidies; Sumaila, U.R., Pauly, D., Eds.; Fisheries Centre Research: Vancouver, BC, Canada, 2006. [Google Scholar]

- Worm, B.; Hilborn, R.; Baum, J.K.; Branch, T.A.; Collie, J.S.; Costello, C.; Fogarty, M.J.; Fulton, E.A.; Hutchings, J.A.; Jennings, S.; et al. Rebuilding global fisheries. Science 2009, 325, 578–585. [Google Scholar] [CrossRef]

- OECD, Workshop Proceedings on the Economics of Rebuilding Fisheries: Challenges for Sustaining Fisheries; OECD: Paris, France, 2010.

- Thorpe, A.; Bennett, E. Market-driven international fish supply chains: The case of Nile Perch from Africa’s Lake Victoria. Int. Food Agribus. Manag. Rev. 2004, 7, 40–57. [Google Scholar]

- Thorpe, A.; Johnson, D.; Bavinck, M. Introduction: The Systems to Be Governed. In Fish for Life: Interactive Governance for Fisheries; Kooiman, J., Bavinck, M., Jentoft, S., Pullin, R., Eds.; Amsterdam University Press: Amsterdam, The Netherlands, 2005; pp. 41–44. [Google Scholar]

- Gudmundsson, E.; Asche, F.; Nielsen, M. Revenue Distribution through the Seafood Value Chain; FAO Fisheries Circular No. 1019; FAO: Rome, Italy, 2006. [Google Scholar]

- Nielsen, M. Modeling fish trade liberalization: Does fish trade liberalization result in welfare gains or losses. Marine Pol. 2009, 33, 1–7. [Google Scholar] [CrossRef]

- Copes, P. The backward bending supply of the fishing industry. Scottish J. Pol. Econ. 1970, 17, 69–77. [Google Scholar] [CrossRef]

- Smith, M.D.; Roheim, C.A.; Crowder, L.; Halpern, B.; Turnipseed, M.; Anderson, J.L.; Asche, F.; Bourillon, L.; Guttormsen, A.; Khan, A.; et al. Sustainability and global seafood. Science 2010, 327, 784–786. [Google Scholar] [CrossRef]

- Asche, F. Farming the Sea. Mar. Resource Econ. 2008, 23, 527–547. [Google Scholar]

- Asche, F.; Flaaten, O.; Isaksen, J.R.; Vassdal, T. Derived demand and relationships between prices at different levels in the value chain: A note. J. Agr. Econ. 2002, 53, 101–107. [Google Scholar] [CrossRef]

- Valderrama, D.; Anderson, J.L. Market interactions between aquaculture and common-property fisheries: Recent evidence from the Bristol Bay sockeye salmon fishery in Alaska. J. Environ. Econ. Manag. 2010, 59, 115–128. [Google Scholar] [CrossRef]

- Mackinson, S.; Sumaila, U.R.; Pitcher, T.J. Bioeconomics and catchability: Fish and fishers behavior during stock collapse. Fish. Res. 1997, 31, 11–17. [Google Scholar] [CrossRef]

- Dyck, A.J.; Sumaila, U.R. Economic impact of ocean fish populations in the global fishery. J. Bioeconomics 2010, 12, 227–243. [Google Scholar] [CrossRef]

- Ommer, E.R. Research Project Team, Coasts under Stress: Restructuring and Social-Ecological Health; McGill-Queens University Press: Kingston, ON, Canada, 2007. [Google Scholar]

- Sutinen, J.G. Major Challenges for Fishery Policy Reform: A Political Economy Perspective; OECD Food, Agriculture and Fisheries Working Papers, No. 8; OECD Publishing: Paris, France, 2008. [Google Scholar]

- Foley, P. The political economy of Marine Stewardship Council certification: Processors and access in Newfoundland and Labrador's inshore shrimp industry. J. Agrar. Change 2012, 12, 436–457. [Google Scholar] [CrossRef]

- Ludwig, D.; Mangel, M.; Haddad, B. Ecology, conservation and public policy. Annu. Rev. Ecol. Systemat. 2001, 32, 481–517. [Google Scholar] [CrossRef]

- Jentoft, S.; Chuenpagdee, R. Fisheries and coastal governance as wicked problems. Mar. Pol. 2009, 33, 553–560. [Google Scholar] [CrossRef]

- 30. Fish for Life: Interactive Governance for Fisheries; Kooiman, J.; Bavinck, M.; Jentoft, S.; Pullin, R. (Eds.) Amsterdam University Press: Amsterdam, The Netherlands, 2005.

- Hammer, C.; Kjesbu, O.S.; Kruse, G.H.; Shelton, P.A. Rebuilding depleted fish stocks: Biology, ecology, social science, and management strategies. ICES J. Mar. Sci. 2010, 67, 1825–1829. [Google Scholar] [CrossRef]

- Gereffi, G. The Organization of Buyer-Driven Global Commodity Chains: How U.S. Retailers Shape Overseas Production Networks. In Commodity Chains and Global Capitalism; Gereffi, G., Korzeniewicz, M., Eds.; Greenwood Press: Westport, Connecticut, USA, 1994; pp. 95–122. [Google Scholar]

- Kaplinsky, R.; Morris, M. A Handbook for Value Chain Research; Institute of Development Studies: Brighton, UK, 2001. [Google Scholar]

- Bernstein, H.; Campling, L. Review article: Commodity studies and commodity fetishism I-Trading down. J. Agrar. Change 2006, 6, 239–264. [Google Scholar] [CrossRef]

- Bavinck, M.; Chuenpagdee, R.; Diallo, M.; Heijden, P.; Kooiman, J.; Mahon, R.; Williams, S. Interactive Fisheries Governance: A Guide to Better Practice; Centre for Maritime Research, Eburon Academic Publishers: Delft, The Netherlands, 2005. [Google Scholar]

- Berkes, F.; Hughes, T.P.; Steneck, R.S.; Wilson, J.A.; Bellwood, D.R.; Crona, B.; Folke, C.; Gunderson, L.H.; Leslie, H.M.; Norberg, J.; Nystrom, M.; Olsson, P.; Osterblom, H.; Scheffer, M.; Worm, B. Globalization, roving bandits, and marine resources. Science 2006, 311, 1557–1558. [Google Scholar]

- 37. Agri-food Commodity Chains and Globalizing Networks; Stringer, C.; Le Heron, R. (Eds.) Ashgate: Aldershot, UK, 2008.

- Nielsen, M. Supply regimes in fisheries. Mar. Pol. 2006, 30, 596–603. [Google Scholar] [CrossRef]

- Moore, W.; Wash, D.; Worden, I.; Macdonald, J. The Fish Processing Sector in Atlantic Canada. Financial Performance and Sustainable Core; Task Force on Incomes and Adjustment in the Atlantic Fishery, Coopers and Lybrand; Ministry of Supply and Services Canada: Ottawa, ON, 1993. [Google Scholar]

- KPMG, Seafood Industry Value Chain Analysis: Cod, Haddock and Nephrops; Centre for Aquaculture and Fisheries, and Seafish Industry Authority: Edinburg, UK, 2004.

- DFO, Cost and Earnings Survey 2004; Department of Fisheries and Oceans, Economic Analysis and Statistics Policy Sector: Ottawa, ON, Canada, 2007.

- Roy, N.; Arnasson, R.; Schrank, W.E. The identification of economic base industries, with an application to the Newfoundland fishing industry. Land Econ. 2009, 85, 675–691. [Google Scholar]

- Rojas, A.; Valley, W.; Mansfield, B.; Orrego, E.; Chapman, G.E.; Harlap, Y. Towards food system sustainability through school food system change: Think&EatGreen@Green and the making of a community university research alliance. Sustainability 2011, 3, 763–788. [Google Scholar] [CrossRef]

- Morissette, L.; Catonguay, M.; Savenkoff, C.; Swaine, D.; Bourdages, H.; Hammill, M.; Hanson, J.M. Contrasting changes between the Northern and Southern Gulf of St. Lawrence ecosystems associated with the collapse of groundfish stocks. Deep Sea Research II 2009, 56, 2117–2131. [Google Scholar] [CrossRef]

- DFO, Recovery Potential Assessment for Laurentian North Designated Units (3Pn, 4RS and 3Ps) of Atlantic Cod (Gadua morhua); Science Advisory Report 2011/026; DFO Canadian Science Advisory Secretariat: Ottawa, ON, Canada, 2011.

- Sinclair, P. State policy and the dragger fleet in north-west Newfoundland. Mar. Pol. 1986, 1, 111–118. [Google Scholar] [CrossRef]

- Palmer, C.; Sinclair, P. When the Fish Are Gone: Ecological Disaster and Fishers in Northwest Newfoundland; Fernwood Publishing: Halifax, Nova Scotia, Canada, 1997. [Google Scholar]

- Rice, J.C.; Shelton, P.A.; Rivard, D.; Chouinard, G.A.; Frechet, A. Recovering Canadian Atlantic Cod Stocks: The Shape of Things to Come? The Scope and Effectiveness of Stock Recovery Plans in Fishery Management; CM 2003/U:06; ICES: Copenhagen, Denmark, 2003. [Google Scholar]

- Savenkoff, C.; Castonguay, M.; Chabot, D.; Hammill, M.; Bourdages, H.; Morissette, L. Changes in the Northern Gulf of St. Lawrence ecosystem estimated by inverse modeling: Evidence of a fishery induced regime shift. Est. Coast. Shelf Sci. 2007, 73, 711–724. [Google Scholar] [CrossRef]

- O’Reilly, A. Market Perspectives: Canadian Seafood Products. Task Force on Incomes and Adjustment in the Atlantic Fishery; Ministry of Supply and Services Canada: Ottawa, ON, Canada, 1993. [Google Scholar]

- Schrank, W.E. The Newfoundland fishery: Ten years after the moratorium. Mar. Pol. 2005, 29, 407–420. [Google Scholar] [CrossRef]

- Asche, A.; Smith, M. Trade and Fisheries: Key Issues for the World Trade Organization; Staff Working Paper ERSD-2010-03; World Trade Organization: Geneva, Switzerland, 2010. [Google Scholar]

- Clift, T. Working Group Team, Report of the Independent Chair: MOU Steering Committee; NL Fishing Industry Rationalization and Restructuring: St. John’s, NL, Canada, 2011. [Google Scholar]

- Asche, F. Capacity measurement in fisheries: What can we learn? Mar. Resource Econ. 2008, 22, 105–108. [Google Scholar]

- Kirby, M.J.L. Navigating Troubled Waters: A New Policy for the Atlantic Provinces; Report of the Task Force on Atlantic Fisheries; Ministry of Supply and Services Canada: Ottawa, ON, Canada, 1982. [Google Scholar]

- Lowitt, K. A community Food Security Assessment of the Bonne Bay Region; Report prepared for the Community University Research for Recovery Alliance; Memorial University of Newfoundland: Norris Point, Canada, 2009. [Google Scholar]

- Tveterås, S.; Asche, F.; Bellemare, M.F.; Smith, M.D.; Guttormsen, A.G.; Lem, A.; Lien, K.; Vannuccini, S. Fish is Food-The FAO’s fish price index. PLoS ONE 2012, 7, e36731. [Google Scholar] [CrossRef]

- Jacquet, J.; Pauly, D.; Ainley, D.; Holt, S.; Dayton, P.; Jackson, J. Seafood stewardship in crisis. Nature 2010, 467, 28–29. [Google Scholar]

- Swartz, W.; Sumaila, U.R.; Watson, R.; Pauly, D. Sourcing seafood to three major markets: The EU, Japan, and the USA. Mar. Pol. 2010, 34, 1366–1373. [Google Scholar] [CrossRef]

- Gulbrandsen, L.H. The emergence and effectiveness of Marine Stewardship Council. Mar. Pol. 2009, 33, 654–660. [Google Scholar] [CrossRef]

- Ponte, S. Greener than thou: The political economy of fish ecolabeling and its local manifestations in South Africa. World Dev. 2007, 36, 159–175. [Google Scholar] [CrossRef]

- OAG, A Study of Managing Fisheries for Sustainability; Report of the Commissioner of the Environment and Sustainable Development; Office of the Auditor General of Canada: Ottawa, Canada, 2011.

- Schrank, W.E.; Skoda, B.; Parson, P.; Roy, N. The cost to government of maintaining a commercially unviable fishery: The case for Newfoundland 1981/82 to 1990/91. Ocean Dev. Intl. Law 1995, 26, 357–390. [Google Scholar] [CrossRef]

- Dean, L. Report on the Special Panel of Corporate Concentration in the NL Fishing Industry; Government of Newfoundland and Labrador: St. John’s, NL, Canada, 2001. [Google Scholar]

- McManus, G.E. Atlas of Newfoundland and Labrador; Breakwater: St. John’s, NL, Canada, 1991. [Google Scholar]

- Schelling, T. The Strategy of Conflict; Harvard University Press: Cambridge, USA, 1960. [Google Scholar]

- ardy, D.A. Team, New Beginnings: Bringing Stability and Structure to Price Determination in the Fishing Industry; Taskforce on Fish/Crab Price Settlement Mechanisms in the Fishing Industry Collective Bargaining Act; Government of Newfoundland and Labrador: St. John’s, Canada, 1998. [Google Scholar]

- Hamilton, L.C.; Butler, M.J. Outport adaptations: Social indicators through Newfoundland’s cod crisis. Hum. Ecol. Rev. 2001, 8, 1–11. [Google Scholar]

- North, D.C. Institutions,Institutional Change and Economic Performance; Cambridge University Press: New York, USA, 1990. [Google Scholar]

- DFO, Socioeconomic Considerations to Inform a Decision Whether or Not to List Three Populations of Atlantic Cod under Species of Risk Act; Department of Fisheries and Oceans, Economic Analysis and Statistics Policy Sector: Ottawa, ON, Canada, 2005.

- DFO, Assessing Recovery Potential: Long-Term Projections and their Implications for Socio-economic Analysis; Science Advisory Report 2007/045; DFO Canadian Science Advisory Secretariat: Ottawa, ON, Canada, 2007.

- Sumaila, U.R. Intergenerational cost-benefit analysis and marine ecosystem restoration. Fish Fish. 2004, 5, 329–343. [Google Scholar] [CrossRef]

- Hutchings, J.A.; Festa-Bianchet, M. Canadian species at risk (2006-2008) with particular emphasis on fishes. Environ. Rev. 2009, 17, 53–65. [Google Scholar] [CrossRef]

- Sumaila, U.R.; Dominguez-Torreiro, D. Discount factors and the performance of alternative fisheries governance systems. Fish Fish. 2010, 11, 278–287. [Google Scholar]

- Malakoff, D. Environmental science feels pinch in Canada’s budget. Science 2012, 336, 1627. [Google Scholar] [CrossRef]

- UNEP, The Role of Supply Chains in Addressing the Global Seafood Crisis; UNEP: Nairobi, Kenya, 2009.

- Campling, L.; Havice, E.; Howard, P.M. The political economy and ecology of capture fisheries: Market dynamics, resource access and relations of exploitation and resistance. J. Agrar. Change 2012, 12, 177–203. [Google Scholar] [CrossRef]

- Stockstad, E. Floundering? Hardly. U.S. Fisheries continue to flourish. Science 2012, 337. [Google Scholar]

- Wakeford, R.; Agnew, D.; Mees, C. Review of institutional arrangements and evaluation of factors associated with successful stock recovery plans. Rev. Fish. Science 2009, 17, 190–222. [Google Scholar] [CrossRef]

- OECD, Rebuilding Fisheries: The Way Forward; OECD: Paris, France, 2012.

© 2012 by the authors; licensee MDPI, Basel, Switzerland. This article is an open-access article distributed under the terms and conditions of the Creative Commons Attribution license (http://creativecommons.org/licenses/by/3.0/).

Share and Cite

Khan, A.S. Understanding Global Supply Chains and Seafood Markets for the Rebuilding Prospects of Northern Gulf Cod Fisheries. Sustainability 2012, 4, 2946-2969. https://doi.org/10.3390/su4112946

Khan AS. Understanding Global Supply Chains and Seafood Markets for the Rebuilding Prospects of Northern Gulf Cod Fisheries. Sustainability. 2012; 4(11):2946-2969. https://doi.org/10.3390/su4112946

Chicago/Turabian StyleKhan, Ahmed S. 2012. "Understanding Global Supply Chains and Seafood Markets for the Rebuilding Prospects of Northern Gulf Cod Fisheries" Sustainability 4, no. 11: 2946-2969. https://doi.org/10.3390/su4112946

APA StyleKhan, A. S. (2012). Understanding Global Supply Chains and Seafood Markets for the Rebuilding Prospects of Northern Gulf Cod Fisheries. Sustainability, 4(11), 2946-2969. https://doi.org/10.3390/su4112946