Do Natural Disasters Reduce Loans to the More CO2-Emitting Sectors?

1

CER-Roma, Dipartimento di Scienze Economiche e Statistiche, Università di Salerno, 84084 Fisciano, Italy

2

Central Bank of the Republic of Turkey, 34435 Istanbul, Turkey

3

Dipartimento di Economia, Statistica e Finanza, Università della Calabria, 87036 Rende, Italy

*

Author to whom correspondence should be addressed.

Sustainability 2024, 16(10), 3943; https://doi.org/10.3390/su16103943

Submission received: 24 February 2024

/

Revised: 26 April 2024

/

Accepted: 1 May 2024

/

Published: 8 May 2024

(This article belongs to the Special Issue Barriers to Green Investments and Circular Economy Businesses Models in Small and Medium-Sized Enterprises)

Abstract

:We studied the impact of major floods occurring in Turkey between 2005 and 2020 on lending and the allocation of loans between sectors that differ in their CO2 emissions. Our evidence shows that the floods are not significant determinants of lending or the allocation of loans between sectors, even though CO2 emissions contribute to the reallocation of loans from the more polluting to the less polluting sectors. Indeed, risks and returns of the sector remain the main determinants of lending and of the allocation of loans among sectors. The results are robust to alternative estimation methods and specifications of the econometric models. Since in the period of investigation no environmental regulations were implemented in Turkey, and the Paris Agreement was ratified only at end-2021, the evidence suggests that more stringent regulations and green policies are required to accelerate the green transition in Turkey.

JEL Classification:

G21; Q51; Q581. Introduction

Emissions of CO2 greenhouse gases are the main cause of climate change, which causes natural disasters in the form of floods, storms, and desertification. Reducing CO2 emissions has been paramount for the survival of the human kind and other species. Furthermore, the green transition relies on the incentives of governments, firms, financial institutions, and the public to reduce CO2 emissions, as well as on regulatory requirements, which impose change in their behavior. Natural disasters generated by climate change may increase and incentives and public awareness of the necessity to reduce CO2 emission activities, and to accelerate the transition to a greener economy. Among the consequences of the increased awareness of the transition to a greener economy, there may be a switching in the allocation of loans from higher to lower CO2-emitting sectors. Indeed, after a natural disaster, banks are under more pressure to support firms’ transition to a more sustainable business model. On the other hand, banks may face risks as a result of the transition to a lower carbon economy. This occurs when a bank funds or has stakes in companies that emit greenhouse gases (GHGs). The higher the current profits from polluting sectors, the greater the banks’ opportunity costs of supporting the green transition of the economy. Thus, the pace and direction of the green transition is the outcome of these countervailing effects.

However, it is difficult to assess the relevance of public awareness on the effects of global warming in banking behavior, since very often it is impossible to disentangle public awareness from other factors (e.g., environmental regulation) that may increase the incentives to promote the green transition. Turkey provides a good example to disentangle these effects. On one hand, Turkey is a developing country in the process of industrialization. Before the last decade, CO2 per capita emission levels were quite moderate in Turkey when compared to USA, EU27, and global averages. Although per capita CO2 emission levels are moderate, when it comes to total greenhouse gas emissions, the picture is different. Since the mid-2010s, annual per person emissions increased to more than the global average, and Turkey is among the top 20 polluting countries, with 1% share of global greenhouse gas emissions (See EDGAR (Emissions Database for Global Atmospheric Research of European Commission). EDGAR provides independent emission estimates based on data reported by European Member States or by Parties under the United Nations Framework Convention on Climate Change (UNFCCC), using international statistics and a consistent IPCC methodology.) On the other hand, Turkey ratified the Paris Agreement only at end-2021, despite taking steps afterwards. Thus, we can study the impact of public awareness on lending independently of regulatory aspects that can affect banking behavior. In addition, between 2005 and 2020, Turkey was affected by three major floods, and natural disasters are external shocks which can spur public awareness and incentives to speed up the green transition. The first occurred in 2009, affecting more than 35,000 people, the second in 2015, which affected 6500 people, and the third was in 2019, affecting about 15,000 people. Finally, and most importantly, Turkey has a bank-based financial system, and in this country, banks may play a big role in the green transition (see [1]).

Hence, we studied the impact of the major floods occurring in Turkey between 2005 and 2020 on the allocation of loans across sectors that differ in terms of their CO2 emissions. We examined the concurrence of the floods, which increase incentives and awareness to spur green transition, with countervailing effects related to the existence of high returns from polluting sectors. Indeed, the evidence shows that in the period under investigation, most of the more polluting sectors in Turkey were among those with higher value added, preventing banks from reallocating loans from the more polluting to the less polluting sectors.

The clear result is that lending is determined by risk and return of the sector but not by the CO2 emissions of the sector. However, the latter are a significant determinant of the allocation of loans between sectors. On the other hand, the main floods occurring in Turkey did not affect the impact of CO2 emissions on lending and on the allocation of loans among sectors. One possible reason for this is the fact that most of the sectors with high CO2 emissions are also more efficient, determining a high transition risk for Turkish banks and firms. These results are robust to alternative estimation methods and specifications of the econometric models, and they suggest that a more stringent regulation is necessary to speed up the green transition in Turkey.

The contribution of this paper to the literature is twofold. First, we study the main conflicting factors that affect lending in Turkey. In addition, we estimate the impact of the floods on the allocation of the loans between sectors in a context in which green regulation is ineffective. We take a holistic approach, by investigating how CO2 emissions affect bank lending behavior after controlling for sectoral loan demand and bank characteristics.

2. Related Literature

Natural disasters may have several effects on banking. First, they increase the riskiness of the loans, and this may lead banks to cut lending, not only in the areas affected by the disasters but also elsewhere. The authors of [2] find that, after natural disasters, credit in unaffected but connected markets declines by almost 50 per cent of additional lending in shocked areas. The authors of [3] show that, following a hurricane strike, banks face deposit withdrawals to which they respond by reducing lending and by drawing on liquid assets. The authors of [4] study the impact of natural disasters on credit allocation. They show that natural disasters lead to an increase in corporate credit demand in affected regions, which banks meet in part by reducing credit to distant regions that are unaffected by disasters. This evidence indicates that natural disasters in some part of the country affects lending all through the country. In addition, the impact of natural disasters on lending and the allocation of loans between sectors depend on their impact on the supply and the demand for loans. References [5,6] show that banks respond to climate risks such as abnormally high temperatures and floods by reducing credit amounts and credit approval rates. Additionally, refs. [7,8,9] find that banks reduce their asset-side liquidity creation by reducing their lending activities. The authors of [10] suggest that in the presence of shocks from extreme weather hazards, banks may shy away from lending under the impact of an extreme weather disaster, resulting in illiquidity in the financing market. In addition, ref. [11] suggests that bank lending shyness is pronounced in developing countries after a climate disaster. There is contrasting evidence on the effects of natural disasters on the demand for loans. Some authors show that natural disasters increase the demand for loans, due to the necessity to repair the damages, and because firms emitting higher CO2 may become more aware that their activities face a higher risk of regulation. For example, ref. [12] find that loan demand would increase following natural disasters, but the proportion of applicants who manage to access funding would decrease due to the higher risks involved. By contrast, ref. [13] show that firms exposed to climate risk-driven liquidity shocks use less trade credit, and [14] show that in developing countries, even ten years after the natural disasters, the private credit to GDP ratio remains approximately 30% below its counterfactual, due to a shock to collateral value.

Third, natural disasters may lead to the reallocation of loans from more polluting to less polluting industries. The authors of [15] study loan allocation around the world, and they show that natural disasters have a significant negative effect on the credit supply to the private sector and a positive effect on that to the public sector. In addition, natural disasters caused by global warming increase the direct costs faced by banks due to climate change relative to transition risks, and they lead to increased lending that accelerates the transition to a greener economy. Furthermore, [16] show that climate risk spur banks to launch more green credit projects, and makes credit resources flow more to low-carbon industries. Additionally, refs. [17,18] show that refusing to lend to highly polluting industries can reduce risk and improve banks’ reputation. The authors of [19] provide evidence that banks making commitments to carbon neutrality affect carbon emissions via credit reallocation (from brown to green firms), rather than via providing loans to brown firms for the investment necessary to reduce carbon emission. Similarly, ref. [20] investigates whether banks that claim to be green decrease their loans by relatively more to the most carbon-intensive sectors, and finds that climate commitments by banks are associated with less lending to large corporates in the five brownest industries. However, ref. [21] find that syndicated loan spreads offered by international banks do not reflect any concern for stranded assets of firms heavily invested in fossil fuel reserves, and [22] find that banks with more extensive environmental disclosures are also those specialized in extending loans to brown industries.

This paper contributes to the existing literature by highlighting the role of natural disasters in the incentive to reallocate loans from the most polluting to the less polluting sectors, in a context in which banks face a trade-off between promoting the green transition at the cost of giving up the high profits generated by the most polluting sectors.

3. Data and Empirical Design

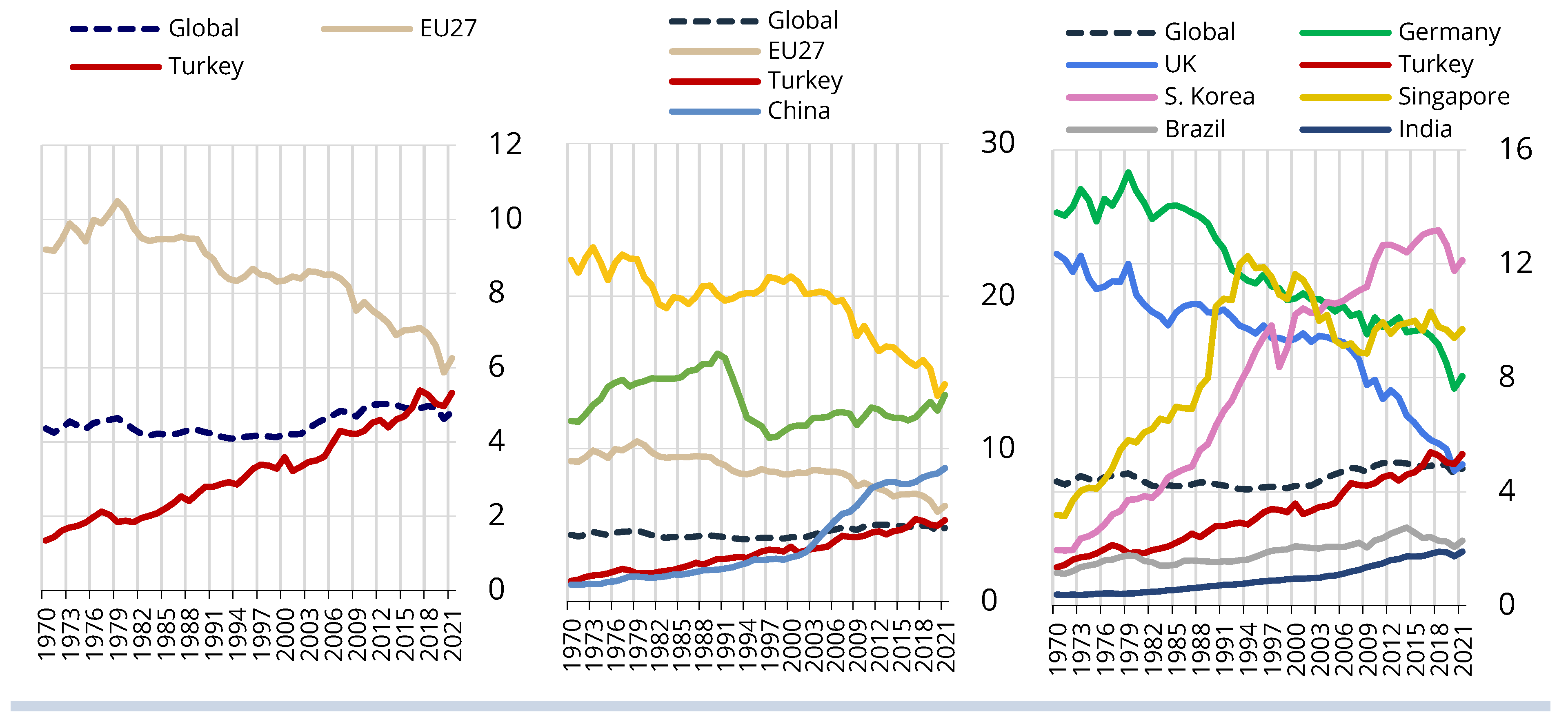

Turkey is a country with per capita CO2 emissions below the global average between 1970 and 2016, and emissions slightly above the global average after 2016. With increasing industrialization since 1970, per capita CO2 emissions in Turkey have exhibited a steady increasing trend and reached the global average level (Figure 1). Comparisons with selected countries show that Turkey’s CO2 emission level is well below that of selected countries such as EU27, USA, Russia, China, and South Korea; however, similar to China, Russia, and South Korea, in the last decade CO2 emissions increased, although at a lower speed than in these countries. By contrast, in EU27 and USA, CO2 emissions steadily decreased in the same period.

We employed several datasets covering the period 2007–2021. The first set of data was collected from the Banking Regulation and Supervision Agency (BRSA) and contains the corporate loans and non-performing loans data at sectoral level provided by resident banks in Turkey. (Sectoral data covers: B—Mining and quarrying, C—Manufacturing, D—Electricity, gas, steam and air conditioning supply, E—Water supply; sewerage, waste management and remediation activities, F—Construction, G—Wholesale and retail trade; repair of motor vehicles and motorcycles, H—Transportation and storage, I—Accommodation and food service activities, J—Information and communication, L—Real estate activities, M—Professional, scientific and technical activities, N—Administrative and support service activities, P—Education, Q—Human health and social work activities, R—Arts, entertainment and recreation, S—Other service activities (see Appendix A Table A1 for a detailed list).) Sectoral data cover 36 economic sectors. While all sectoral datasets use the Statistical Classification of Economic Activities in the European Community NACE Rev.2 codes in the sectoral classification, the first set of data on loans is on a different coding classification called “financing subject codes”, developed and most prevalently used by the Risk Centre, CBRT, and BRSA in Turkey. Thus, in order to combine the datasets, we mapped the financing subject codes into NACE codes, resulting in a total of 36 sectors for the analysis. The list of NACE sectors is presented in Appendix A Table A1.

The second set of data provides the value added of sectors, obtained from Turkish Statistical Institute (TURKSTAT), and shows the gross income from operating activities after adjusting for operating subsidies and indirect taxes. Thirdly, we used the data of air emission of one of the greenhouse gases, carbon dioxide (CO2), on a sectoral basis in Turkey, which is published by Eurostat every year. Air emission of CO2 accounts record the flows of CO2 emitted by sectors and flowing into the atmosphere, regardless of where these emissions actually occur geographically. (Natural flows of residual gaseous are excluded, e.g., volcanos and forest fires. Also excluded are air emissions arising from land use, land use changes, and forestry as well as any indirect emissions. Table A2 in the Appendix A lists the CO2 emissions of the industries by year.) Fourth, we used a firm-level dataset from TURKSTAT to calculate investments, which are computed as the absolute change in tangible fixed assets of firms at sectoral level. Finally, we used the records of EM-DAT, an international platform that provides information on the occurrence and impacts of mass disasters worldwide. This database is compiled from various sources such as UN agencies, non-governmental organizations, reinsurance companies, research institutes, and press agencies. There are over 100 disaster records for Turkey in the data, not only natural disasters caused by climate change, but also traffic accidents, mining accidents, and earthquakes. Below in Table 1, we present the full list of climate-related flood disasters according to EM-DAT records during 2007–2020. According to EM-DAT records, the listed disasters affected more than 60 thousand people and the cost of total damage was USD 1.8 billion, whereas the insured damage was USD 0.7 billion. (Disasters that cause medium or minor damage are not recorded by EM-DAT. In order for a disaster event to be recorded in the EM-DAT database, at least one of the four criteria given below must hold: (1) at least 10 people lose their lives, (2) at least 100 people are affected, (3) a state of emergency is declared, (4) an international call for help is made. As a result, it turns out that, in order for a disaster to be entered into the EM-DAT database, its damage must be great due to the criteria in question.).

For this study, we concentrated on climate-related flood disasters that have a widespread impact, dated 2009, 2015, and 2019. The list of the main variables used in the paper is presented in Table 2.

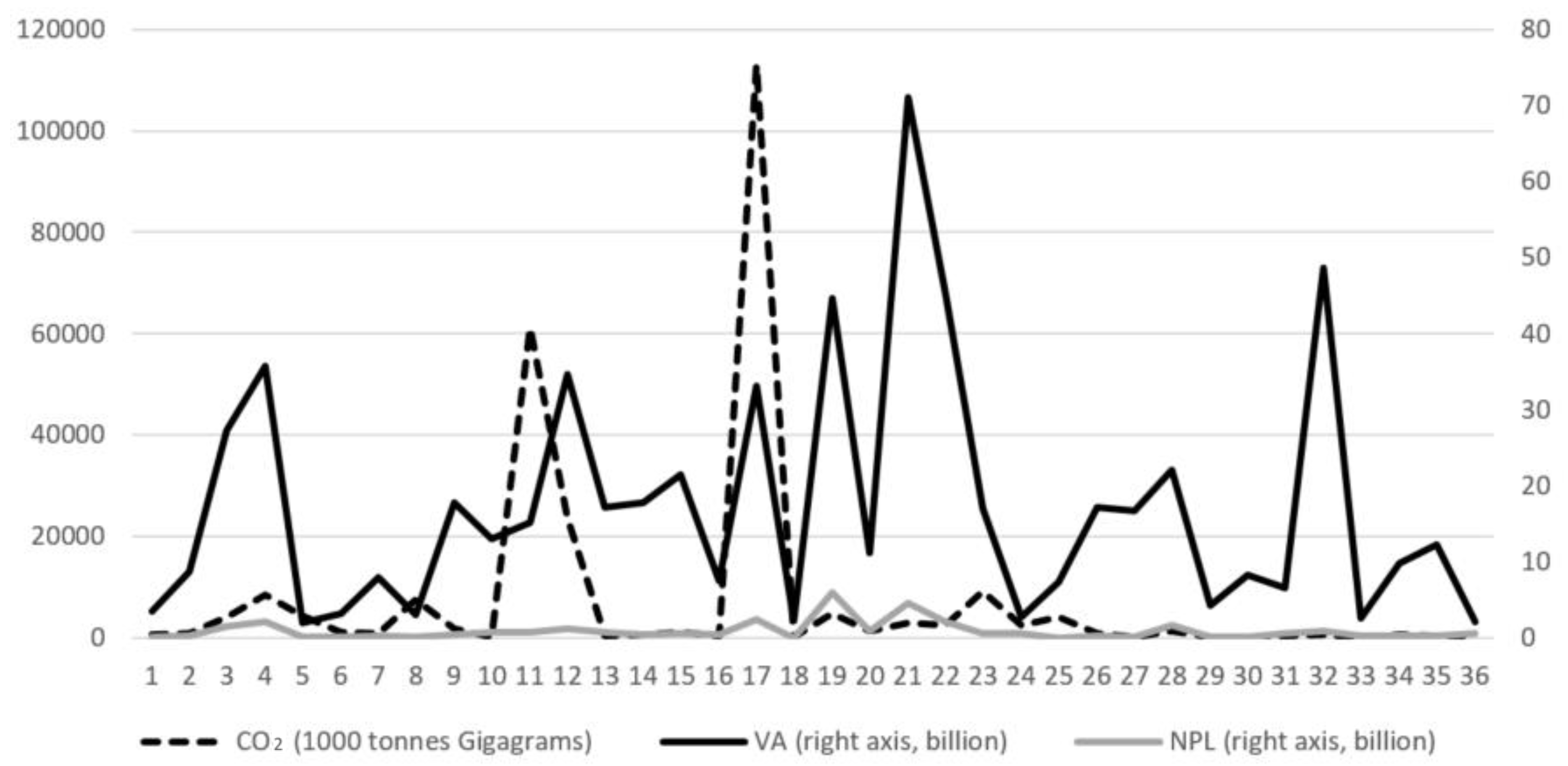

Figure 2 above shows the CO2 emissions, value-added (VA), and non-performing loans of 36 sectors throughout 2005–2020. Overall, the figure suggests that CO2 emissions and VA show a similar pattern on a sectoral basis. When the correlation between CO2 emissions and VA is calculated across 36 sectors, it is found that, while for 11 sectors the correlation is negative, for 25 sectors the correlation is positive. The 25 sectors with a positive correlation between VA and CO2 emissions constitute 72% of the total VA throughout the years and the average correlation of these 25 is again +72%. The remaining 11 sectors with a negative correlation between VA and CO2 emissions comprise 28% of the total VA throughout the years and the average correlation of these 11 sectors is—49%. These figures suggest that CO2 emissions are created by the sectors with higher VA.

With the first model below (1), we study how risk and return, as well as CO2 emissions of the sector, affect lending, and whether the main floods that occurred between 2007 and 2020 in Turkey changed the relationship between CO2 emissions and lending. In addition, we use cross-section and time fixed effects models to consider other potential determinants of lending. (The redundancy tests show that when we estimate Equation (1), both cross-section and time fixed effects models are appropriate.).

where Loans is total loans to the industry, NPLRATIO is non-performing loans over total loans in the industry, and VA denotes the value added of the industry. CO2 is greenhouse gas emissions in the industry, and is investment in the sector calculated from the firm-level data showing the change in tangible fixed assets, special costs, exploration expenses, preparation and development expenses, and financial leasing. Following ref. [23], this variable is used as a proxy for the demand for loans. DFlood is the dummy taking the value of 1 after the year in which the main flood occurred (2009, 2015, 2019) and 0 before. denotes absolute change, δ and ρ are, respectively, the sector and time fixed effects, and ε is the error term. All variables were deflated using the CPI index. We assume that Turkish banks consider both change in risk and return as well as the CO2 emissions of the sector while lending, and we test whether this assumption is supported by the empirical evidence. In addition, we assume that the floods that occurred in Turkey between 2005 and 2020 reduce lending to more polluting industries. In order to capture the prevailing effects, the data used in the regressions cover the period 2005–2021. Although the relationship between lending and pollution reflects the economic structure of the country, an unexpected natural event such as a flood may increase bank manager awareness of the detrimental effects of climate change, and it may lead to reduce lending to the more polluting industries (i.e., we assume that the sign of the coefficient above is negative).

Equation (1) above assumes that lending to one sector is independent of lending to the other sectors. In Equation (2), we estimate whether the main floods that occurred in Turkey affect the allocation of the loans between sectors.

where TOTLOANS denotes total loans, the total CO2 emissions, TOTNPL the total non-performing loans, the total value added, and TOTINV the total investments in the 36 industries. The other variables are defined above. We expect that if floods increase banks’ awareness of the effects of climate change, banks reallocate loans from increasing CO2-emitting industries to the other industries (the sign of the coefficient in (2) is negative).

4. Results

In the first set of results, we provide evidence for the main determinants of lending, and the impact of the three major floods that occurred in Turkey between 2005 and 2020 on the relationship between CO2 emissions and lending. (The authors of [14,24], among others, find evidence of a direct link between emission intensity and lending in a few salient industries.).

The most evident results on the determinants of lending are that banks take account of risk and return of the sector but not of the CO2 emissions of the sector (Table 3). Specifically, they increase loans to the sector as the value added of the sector increases and the ratio of non-performing loans over total loans decreases. In addition, the main floods that occurred in Turkey after 2007 did not seem to have a significant impact on the relationship between CO2 emissions and lending of the sector; instead, they increased the impact of investments on lending after the 2019 flood (We cannot estimate the impact of the 2009 major flood on investment since data on investment start in 2010.) (see Table 3).

We estimated Equation (1) using additional variables and alternative methodologies. Specifically, we added the interbank rate and bank capital to take account of bank’s constraints on lending [25]. In addition, we included among the regressors an indicator of macroeconomic performance (change in real gross domestic product [26]). To include these additional variables, we need to estimate the model without time fixed effects. In addition, we estimated the model with and without cross-section fixed effects. The results (reported in Appendix A) show a positive impact of the capital on lending, and a reduction in lending to the more polluting sectors only as a consequence of the 2019 flood. However, the main results reported in Table 3 are also confirmed with these alternative specifications (see Table A6).

To obtain more insight into the role of CO2 emissions in lending, we estimated the impact of CO2 emissions relative to value added (a proxy of the productive efficiency of the sector) on loans/value added.

The results reported in Table 4 indicate that only non-performing loans relative to value added is a significant determinant of lending, confirming that banks in lending do not take account of the CO2 emissions of the sector. Indeed, the following graph also supports this conclusion.

Figure 3 suggests that in the period of the greater increase in lending (2005–2014), there was a slight reduction in CO2 emissions in Turkey relative to value added. By contrast, in the period of the greatest reduction in CO2/VA (2015–2021), LOAN/VA had a stable or decreasing trend. Indeed, between 2005 and 2021, Turkey increased both CO2 emissions and value added, but the former increased less than the latter (see Figure A2b in Appendix A), mainly due to replacement of coal with alternative sources (natural gas, electric heating, solar energy, and wind energy) [27]. In addition, in the same period, Turkish banks increased loans to the most polluting sectors (17—Electric, Gas and Water Resources, 19—Retail Sale of Motor Vehicles and Its Fuel Oil, 21–26—Transportations) relative to the other sectors (Figure A1).

While Equation (1) and the foregoing results are based on the assumption that lending to a sector is independent of that to other sectors, Equation (2) assumes that banks have a portfolio approach in the allocation of the loans between sectors, and lending to a sector depends on the relative risk and return of the sector as well as on the relative CO2 emissions of the sector. We assume that floods reduce loans to the sectors with higher relative CO2 emissions. Table 5 summarizes the results of the estimation of Equation (2). (Redundancy tests show that in this case, only cross-section fixed effects are relevant, while in the estimations reported in Table 5 below, both cross-section and time fixed effects are appropriate (see Appendix A)).

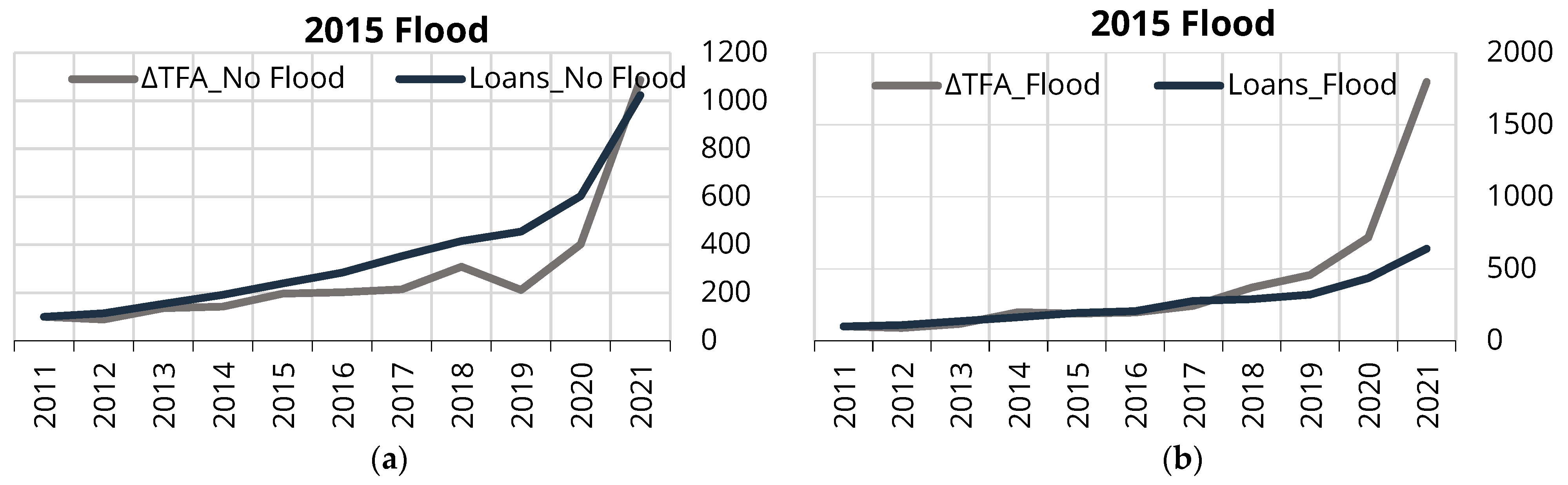

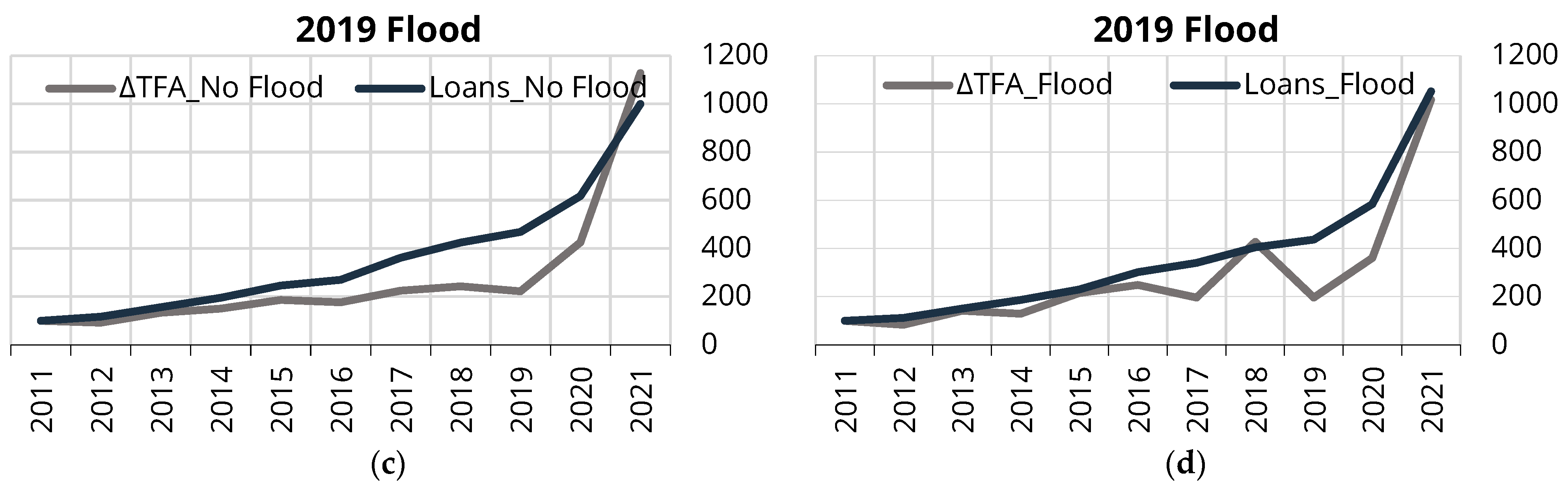

First, in the allocation of loans between sectors, banks take account of the relative risk and relative value added of the sector. In addition, they reduce the allocation of the loans to those sectors with higher relative CO2 emissions. However, the main floods that occurred in Turkey did not have a significant impact on the allocation of loans to the more polluting sectors. Note that the main results reported in Table 5 also hold when we estimate Equation (2) including additional variables and using alternative estimation methods (see Table A8 in Appendix A). Thus, the results reported in Table 5 extend previous conclusions on the impact of the floods on lending to the allocation of the loans between sectors, but, differently from lending, banks also take account of the relative pollution in the allocation of loans between sectors. Finally, after the floods of 2015 and 2019, there was a smaller impact of investments on lending. To understand whether this result is due to the floods or other factors that affected the Turkish economy in the same period, we compared changes in investments and loans in provinces affected and not affected by the floods. The results reported in Figure A3 indicate that investments increased more in the provinces affected by the floods than in the rest of the country.

Overall, while risk and return of the sector are always determinants of lending and of the allocation of loans between sectors, CO2 emissions affect only the latter. The major floods that occurred in Turkey did not have a significant impact on lending or on the allocation of the loans among sectors.

5. Robustness Checks

In this section we provide some robustness checks on the previous results. In the first robustness check, we use the number of people affected by the floods as an alternative indicator of the relevance of the natural disasters. The results reported in Table 6 show that the number of people affected by the floods does not have a significant impact on lending or on the allocation of loans among sectors. All the other previous results remain valid, including the role of CO2 emissions in determining the allocation of the loans among sectors.

In the second set of robustness checks, we again performed the main regressions reported in Table 3, Table 4 and Table 5, using only the subsample of the sectors with an amount of CO2 emissions above average all through the period of investigation. We expect that, if banks take account of the floods in the allocation of the loans among sectors, the effect of CO2 emissions on the lending and the allocation of the loans will be stronger than in the case using the overall sample.

Indeed, the results do not support this assumption (Table 7). Similar to previous results (see Table 3), the main floods do not have a significant effect on the relationship between CO2 and lending. The fact that floods do not affect lending is also supported by the determinants of LOANS/VA in the subsample of the more polluting sectors (see Table 8).

We have shown above that in the allocation of loans between sectors, banks take account of the risk and value added of the sector. In addition, there is a significant impact of CO2 emissions on the allocation of loans among sectors. The results for the subsample of the more polluted sectors (see Table 9) indicate that relative risk of the sector is no longer a significant determinant of the allocation of the loans to the sector, while it increases the relevance of the value added in the allocation of loans among sectors. In addition, the impact of the CO2 emissions on the allocation of the loans to the sector is weaker for the more polluting sectors than in the full sample. However, the evidence reported in Table 9 indicates that the floods also did not affect the allocation of the loans for the subsample of the more polluted sectors.

These results can be justified by the fact that the most polluting sectors in Turkey are also those with the highest value added. However, the results reported in this section strengthen the conclusion that in lending as well as in the allocation of loans between sectors, factors other than public awareness about the effects of climate change are relevant in determining Turkish banks’ behavior.

6. Concluding Remarks

Climate change, among other factors, leads to an increase in the occurrence of natural disasters. Natural disasters are not only seen as a threat to human life and the environment due to the damage created, but they may also shift the public awareness towards a faster transition to a green economy. We studied the impact of one type of natural disaster (i.e., floods) in Turkey on the allocation of loans among the more polluting industries. We claim that the occurrence of major natural disasters leads banks to spur the green transition if they do not have a stake in the more polluting sectors. Indeed, the evidence shows that banks in Turkey have a great stake in more polluting industries. Indeed, the more efficient and profitable sectors in Turkey are also the more polluting ones. Thus, the results of the econometric analysis indicate that floods did not reduce loans to the more polluting sectors. Indeed, risk and return are the main determinants of lending and of the allocation of loans among sectors. Several robustness checks confirm these findings, including the results of the analysis of the subsample of the more polluting industries.

Very recently, ref. [1] examined how Turkish banks adjust credit supply in provinces with higher air pollution, and they show that banks, following the 2015 Paris Agreement, limited their credit extension to more polluted provinces, implying that Turkish banks were affected by this agreement, despite the fact that Turkey did not ratify it until October 2021. Our analysis provides a different narrative. Even though Turkish banks take account of the proportion of the CO2 emissions in the allocation of loans among sectors, the major floods that occurred in Turkey in 2015 and 2019 did not spur the transition to a greener economy. However, a deeper analysis involving more dynamic models is necessary to better understand the relevance of the determinants of the allocation of loans in Turkey. Banks in Turkey differ according to their business model and ownership structure. Therefore, a natural extension of this work is to investigate whether there is one type of bank that reacts more to natural disasters and provides greater encouragement for the green transition. However, our evidence suggests that countries relying more on polluting industries face more difficulties in switching to a greener economy, even though the Turkish government has taken several actions after signing the Paris Agreement. On 29 October 2021, the Directorate of Climate Change was established to carry out the duties of “determining policies, strategies and actions at national and international levels within the scope of Turkey’s climate change combat and adaptation efforts, carrying out negotiation processes, and ensuring coordination with institutions and organizations”. In addition, climate change topics have started being introduced into various government plans and programs announced to the public (see: “2024–2030 Climate Change Mitigation Strategy and Action Plan”, Directorate of Climate Change, Ministry of Environment, Urbanization and Climate Change, 2024, Turkey). Although Turkey has been taking rapid steps with the contribution of all stakeholders since end-2021, it seems that it will take time for this to be reflected in both the corporate sector’s transition to green energy sources and banks’ loan allocation across sectors. However, more effective regulations and green policies may speed up the green transition process.

Author Contributions

Conceptualization, D.B.S.; Methodology, A.F.; Investigation, A.F., S.S. and D.B.S.; Data curation, S.S.; Writing—original draft, D.B.S. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Informed consent was obtained from all subjects involved in the study.

Data Availability Statement

Data are contained within the article.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table A1.

List of productive sectors with corresponding NACE codes.

| No | Name | NACE Codes |

|---|---|---|

| 1 | Extracting of Mines Product Energy | 05 + 06 |

| 2 | Extracting of Mines Not Product Energy | 07 + 08 + 09 |

| 3 | Food, Beverage and Tobacco Industry. | 10 + 11 + 12 |

| 4 | Textile and Textile Products Industry | 13 + 14 |

| 5 | Leather and Leather Products Industry | 15 |

| 6 | Wood and Wood Products Industry | 16 |

| 7 | Paper Raw Materials and Paper Products Industry | 17 + 18 |

| 8 | Nuclear Fuel and Refined Petroleum and Coke Coal Industry | 19 |

| 9 | Chemical Products Industry | 20 + 21 |

| 10 | Rubber and Plastic Products Industry | 22 |

| 11 | Other Mines Excluding Metal Industry | 23 |

| 12 | Main Metal Industry | 24 + 25 |

| 13 | Machine and Equipment Industry | 28 + 33 |

| 14 | Electrical and Optical Devices Industry | 26 + 27 |

| 15 | Transportation Vehicles Industry | 29 + 30 |

| 16 | Manufacturing Industry Not Classified in Other Places | 31 + 32 |

| 17 | Electric, Gas and Water Resources | 35 + 36 |

| 18 | Construction | 41 + 42 + 43 |

| 19 | Retail Sale of Motor Vehicles and Its Fuel Oil | 45 |

| 20 | Wholesale Trade and Brokerage | 46 |

| 21 | Retail Trade and Personal Products | 47 |

| 22 | Hotels + Restaurants + Other Tourism | 55 + 56 |

| 23 | Railroad Transportation + Road Transportation + Road Haulage | 49 |

| 24 | Maritime Transportation | 50 |

| 25 | Air Transportation | 51 |

| 26 | Other Transportation Activities | 52 + 79 |

| 27 | Communication | 53 + 61 |

| 28 | Real Estate Brokerage | 68 |

| 29 | Rent (Vehicle, Machine, Device) | 77 |

| 30 | Computer and Related Activities | 62 + 63 |

| 31 | Research, Consulting, Advertising and Other Activities | 69 + 70 + 71 + 72 + 73 + 74 + 75 + 78 + 80 + 81 + 82 |

| 32 | Education | 85 |

| 33 | Health and Social Services | 86 + 87 + 88 |

| 34 | Arranging of Drainage and Waste | 37 + 38 + 39 |

| 35 | Cultural, Entertainment and Sporting Activities | 58 + 59 + 60 + 90 + 91 + 92 + 93 |

| 36 | Other Personal Services | 95 + 96 |

Figure A1.

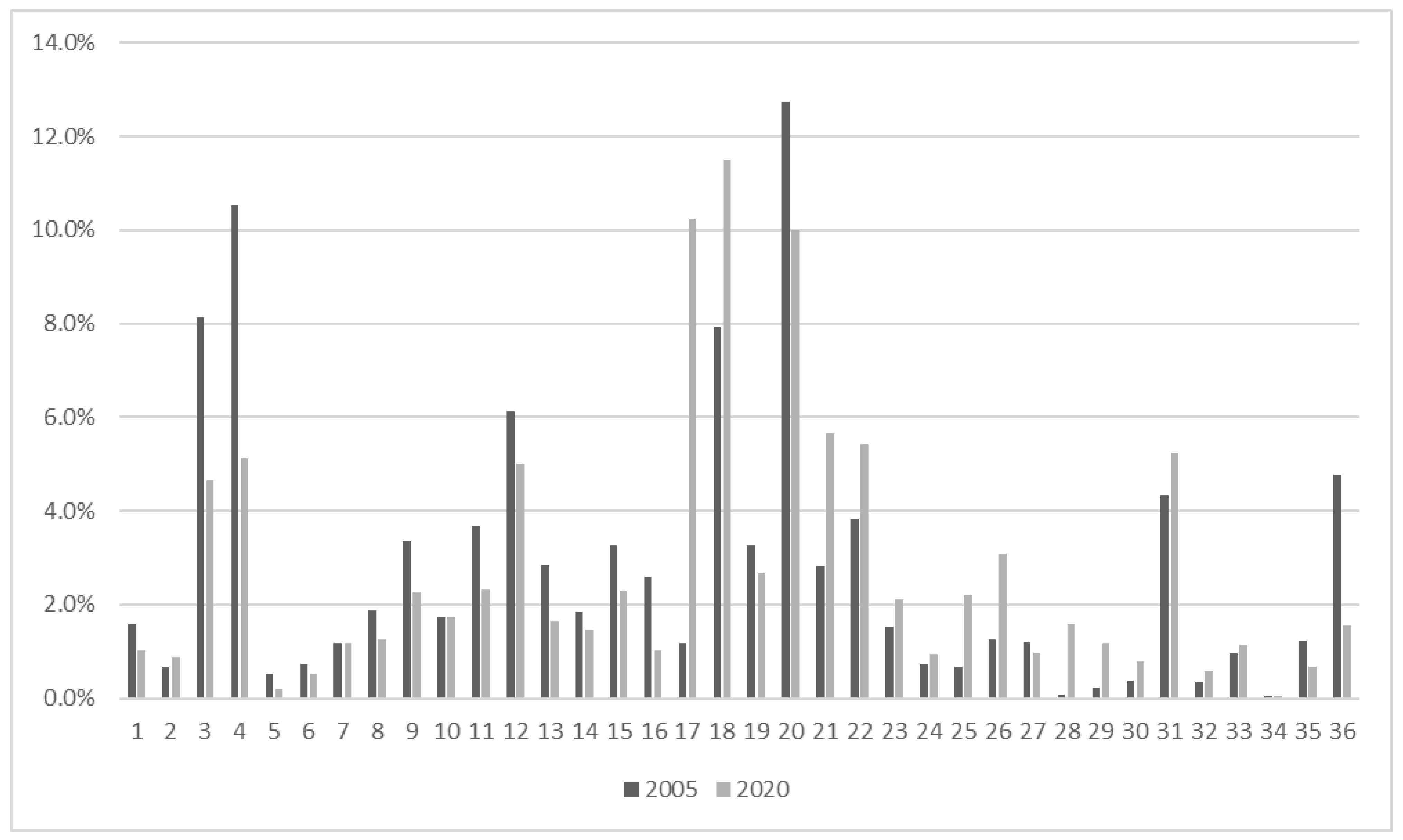

The allocation of loans by sector in Turkey in 2005 and 2020, sectoral loans to total loans. The allocation of the loans among sectors in 2020 relative to 2005 shows a sharp increase in lending to highly polluting sectors (17 Electric, Gas and Water Resources, 18 Construction, 21 Retail Trade and Personnel Products, 22 Hotels, Restaurants, Other Tourism, 25 Air Transportation, 26 Other Transportation Activities, 31 Education).

Figure A1.

The allocation of loans by sector in Turkey in 2005 and 2020, sectoral loans to total loans. The allocation of the loans among sectors in 2020 relative to 2005 shows a sharp increase in lending to highly polluting sectors (17 Electric, Gas and Water Resources, 18 Construction, 21 Retail Trade and Personnel Products, 22 Hotels, Restaurants, Other Tourism, 25 Air Transportation, 26 Other Transportation Activities, 31 Education).

Figure A2.

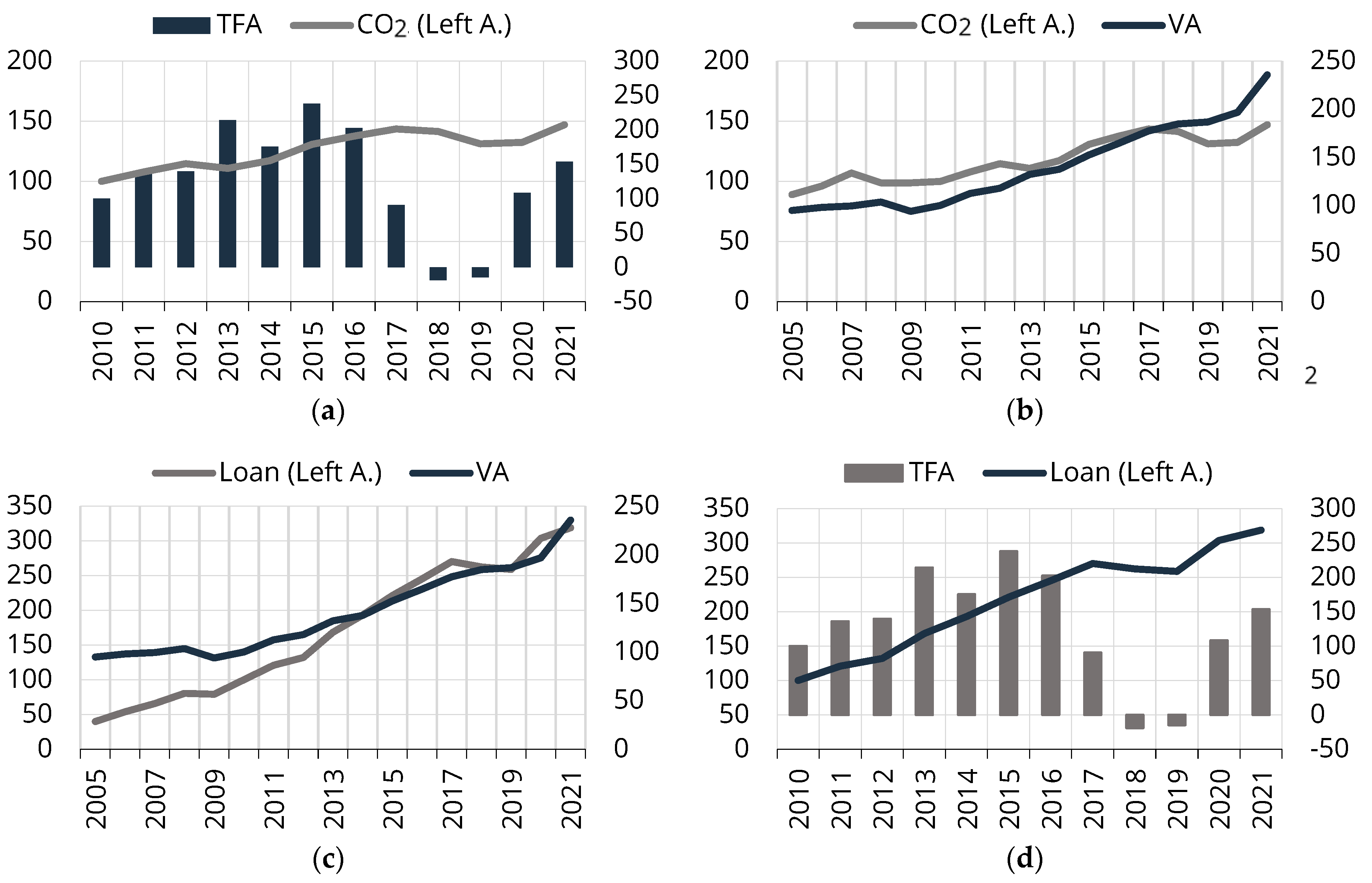

Comparisons of CO2 emissions- change in tangible fixed assets (a), CO2 emissions - value-added (b), loans-value added (c), and loans-change in tangible fixed assets (d) in Turkey from 2005 to 2021. The graphs show CO2 emissions, investment, value-added, and performing loan development during 2005–2021. Due to availability of data, for tangible fixed asset (proxy for investment) comparisons, the coverage period is 2010–2021, where 2010 is taken as the base year (=100) for indexing. Tangible fixed assets were generated using micro-level firm data. The calculation is based on the change in balance sheet items such as tangible fixed assets, special costs, exploration expenses, preparation and development expenses, and financial leasing compared to the previous year. Loans include performing firm loans both in domestic currency and FX. The series are deflated. The figures show that TFA increase with CO2 emission and loans. In years when there is not addition to TFA, CO2 emission declines. Also, both CO2 and loans move with the value-added.

Figure A2.

Comparisons of CO2 emissions- change in tangible fixed assets (a), CO2 emissions - value-added (b), loans-value added (c), and loans-change in tangible fixed assets (d) in Turkey from 2005 to 2021. The graphs show CO2 emissions, investment, value-added, and performing loan development during 2005–2021. Due to availability of data, for tangible fixed asset (proxy for investment) comparisons, the coverage period is 2010–2021, where 2010 is taken as the base year (=100) for indexing. Tangible fixed assets were generated using micro-level firm data. The calculation is based on the change in balance sheet items such as tangible fixed assets, special costs, exploration expenses, preparation and development expenses, and financial leasing compared to the previous year. Loans include performing firm loans both in domestic currency and FX. The series are deflated. The figures show that TFA increase with CO2 emission and loans. In years when there is not addition to TFA, CO2 emission declines. Also, both CO2 and loans move with the value-added.

Figure A3.

Comparisons of change in tangible fixed assets -loans in provinces affected by flood (b,d) versus provinces not affected by flood (a,c). The graphs show the total tangible fixed assets and loan development in the provinces affected and unaffected by the 2015 and 2019 floods as an index, where 2011 is taken as the base year (=100) in indexing. Tangible fixed assets were generated using micro-level firm data. The calculation is based on the change in balance sheet items such as tangible fixed assets, special costs, exploration expenses, preparation and development expenses, and financial leasing compared to the previous year. Loans include performing firm loans both in domestic currency and FX. The series are not adjusted for inflation or exchange rate effects. The figures show that in regions where there is no flood, loans continued increasing the change in total fixed assets. On the other hand, in regions hit by the flood of 2019, while loans increase with the change in total fixed assets, it is less likely to be the case in 2015.

Figure A3.

Comparisons of change in tangible fixed assets -loans in provinces affected by flood (b,d) versus provinces not affected by flood (a,c). The graphs show the total tangible fixed assets and loan development in the provinces affected and unaffected by the 2015 and 2019 floods as an index, where 2011 is taken as the base year (=100) in indexing. Tangible fixed assets were generated using micro-level firm data. The calculation is based on the change in balance sheet items such as tangible fixed assets, special costs, exploration expenses, preparation and development expenses, and financial leasing compared to the previous year. Loans include performing firm loans both in domestic currency and FX. The series are not adjusted for inflation or exchange rate effects. The figures show that in regions where there is no flood, loans continued increasing the change in total fixed assets. On the other hand, in regions hit by the flood of 2019, while loans increase with the change in total fixed assets, it is less likely to be the case in 2015.

Table A2.

Redundancy fixed effects tests on Table 3 estimations.

Table A2.

Redundancy fixed effects tests on Table 3 estimations.

| Test Cross-Section and Period Fixed Effects | |||

|---|---|---|---|

| Effects Test | Statistic | d.f. | Prob. |

| Cross-section F | 4.320293 | (35,485) | 0.0000 |

| Cross-section Chi-square | 146.545302 | 35 | 0.0000 |

| Period F | 3.197548 | (14,485) | 0.0001 |

| Period Chi-square | 47.674382 | 14 | 0.0000 |

| Cross-Section/Period F | 3.984000 | (49,485) | 0.0000 |

| Cross-Section/Period Chi-square | 182.661206 | 49 | 0.0000 |

Table A3.

Redundancy fixed effects tests on Table 4 estimations.

Table A3.

Redundancy fixed effects tests on Table 4 estimations.

| Test Cross-Section and Period Fixed Effects | |||

|---|---|---|---|

| Effects Test | Statistic | d.f. | Prob. |

| Cross-section F | 0.252735 | (35,486) | 1.0000 |

| Cross-section Chi-square | 9.740217 | 35 | 1.0000 |

| Period F | 3.233234 | (14,486) | 0.0001 |

| Period Chi-square | 48.088536 | 14 | 0.0000 |

| Cross-Section/Period F | 1.104600 | (49,486) | 0.2971 |

| Cross-Section/Period Chi-square | 57.020053 | 49 | 0.2015 |

Table A4.

Redundancy fixed effects tests on Table 5 estimations.

Table A4.

Redundancy fixed effects tests on Table 5 estimations.

| Test Cross-Section and Period Fixed Effects | |||

|---|---|---|---|

| Effects Test | Statistic | d.f. | Prob. |

| Cross-section F | 1.700013 | (35,485) | 0.0086 |

| Cross-section Chi-square | 62.488746 | 35 | 0.0029 |

| Period F | −0.000000 | (14,485) | 1.0000 |

| Period Chi-square | 0.000000 | 14 | 1.0000 |

| Cross-Section/Period F | 1.214295 | (49,485) | 0.1595 |

| Cross-Section/Period Chi-square | 62.488746 | 49 | 0.0933 |

Table A5.

Carbon dioxide emissions (without emissions from biomass used as a fuel) (1000 tonnes Gigagrams), parts 1 and 2.

Table A5.

Carbon dioxide emissions (without emissions from biomass used as a fuel) (1000 tonnes Gigagrams), parts 1 and 2.

| Part 1 | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| Sector (NACE2) | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | |

| 05 + 06 | 684 | 827 | 956 | 574 | 603 | 572 | 485 | 555 | |

| 07 + 08 + 09 | 1026 | 1240 | 1434 | 862 | 905 | 858 | 728 | 833 | |

| 10 + 11 + 12 | 2595 | 2522 | 1987 | 1973 | 1068 | 1467 | 3999 | 4239 | |

| 13 + 14 | 13,813 | 17,402 | 20,013 | 9416 | 10,148 | 9570 | 6654 | 8112 | |

| 15 | 6907 | 8701 | 10,006 | 4708 | 5074 | 4785 | 3327 | 4056 | |

| 16 | 1691 | 2113 | 2433 | 1206 | 1292 | 1220 | 891 | 1073 | |

| 17 + 18 | 189 | 202 | 239 | 245 | 247 | 235 | 1031 | 1014 | |

| 19 | 5821 | 5954 | 6065 | 6704 | 4797 | 5594 | 6606 | 6570 | |

| 20 + 21 | 1272 | 871 | 885 | 1022 | 911 | 1082 | 1931 | 2166 | |

| 22 | 125 | 135 | 157 | 155 | 156 | 151 | 162 | 188 | |

| 23 | 38,410 | 40,506 | 41,404 | 48,061 | 47,630 | 55,771 | 61,920 | 65,640 | |

| 24 + 25 | 23,288 | 22,546 | 21,361 | 17,032 | 17,157 | 20,093 | 21,338 | 24,394 | |

| 26 + 27 | 615 | 767 | 882 | 437 | 468 | 443 | 323 | 398 | |

| 28 + 33 | 863 | 1065 | 1224 | 648 | 687 | 654 | 504 | 630 | |

| 29 + 30 | 1761 | 2216 | 2548 | 1206 | 1299 | 1226 | 857 | 1053 | |

| 31 + 32 | 381 | 433 | 479 | 265 | 279 | 267 | 222 | 277 | |

| 35 + 36 | 79,816 | 84,995 | 101,325 | 106,013 | 107,365 | 101,542 | 111,975 | 112,906 | |

| 37 + 38 + 39 | 104 | 113 | 132 | 131 | 129 | 122 | 132 | 153 | |

| 41 + 42 + 43 | 6178 | 7618 | 8760 | 4666 | 4942 | 4703 | 3644 | 4507 | |

| 45 | 681 | 732 | 829 | 771 | 766 | 766 | 790 | 1065 | |

| 46 | 1025 | 1108 | 1262 | 1174 | 1166 | 1158 | 1200 | 1625 | |

| 47 | 1028 | 1112 | 1265 | 1173 | 1164 | 1157 | 1198 | 1634 | |

| 49 | 5944 | 6289 | 6767 | 6371 | 6407 | 6368 | 6548 | 8572 | |

| 50 | 1299 | 1462 | 1597 | 1541 | 1630 | 1678 | 2233 | 1618 | |

| 51 | 4077 | 4497 | 5996 | 5203 | 5134 | 2868 | 3347 | 3728 | |

| 52 + 79 | 291 | 313 | 357 | 339 | 338 | 334 | 349 | 449 | |

| 53 + 61 | 42 | 45 | 51 | 48 | 47 | 47 | 49 | 66 | |

| 55 + 56 | 419 | 452 | 518 | 490 | 488 | 481 | 503 | 654 | |

| 58 + 59 + 60 + 90 + 91 + 92 + 93 | 31 | 33 | 38 | 35 | 35 | 34 | 36 | 48 | |

| 62 + 63 | 26 | 28 | 32 | 30 | 30 | 30 | 31 | 42 | |

| 68 | 230 | 247 | 286 | 278 | 278 | 271 | 288 | 350 | |

| 69 + 70 + 71 + 72 + 73 + 74 + 75 + 78 + 80+ 81 + 82 | 270 | 291 | 333 | 311 | 309 | 306 | 318 | 426 | |

| 77 | 27 | 30 | 34 | 32 | 31 | 31 | 32 | 44 | |

| 85 | 67 | 72 | 83 | 79 | 79 | 77 | 81 | 104 | |

| 86 + 87 + 88 | 122 | 131 | 152 | 152 | 152 | 147 | 158 | 182 | |

| 95 + 96 | 80 | 86 | 98 | 91 | 90 | 90 | 93 | 127 | |

| part 2 | |||||||||

| Sector (NACE2) | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 |

| 05 + 06 | 468 | 482 | 469 | 483 | 508 | 521 | 497 | 471 | 522 |

| 07 + 08 + 09 | 701 | 723 | 703 | 724 | 762 | 781 | 745 | 707 | 784 |

| 10 + 11 + 12 | 4337 | 4114 | 5163 | 5824 | 5836 | 5996 | 6057 | 6713 | 7288 |

| 13 + 14 | 5756 | 5544 | 5078 | 4950 | 5078 | 5209 | 5103 | 4732 | 5074 |

| 15 | 2878 | 2772 | 2539 | 2475 | 2539 | 2604 | 2552 | 2366 | 2537 |

| 16 | 801 | 787 | 736 | 731 | 756 | 775 | 753 | 704 | 764 |

| 17 + 18 | 1034 | 1178 | 1258 | 1389 | 1279 | 1325 | 1345 | 1577 | 1628 |

| 19 | 5836 | 5798 | 8214 | 10,889 | 11,590 | 9017 | 10,957 | 10,636 | 10,570 |

| 20 + 21 | 1789 | 2026 | 2373 | 2037 | 1940 | 2733 | 2244 | 2148 | 3299 |

| 22 | 195 | 210 | 215 | 231 | 244 | 248 | 236 | 230 | 260 |

| 23 | 67,287 | 69,586 | 70,734 | 75,973 | 79,591 | 76,978 | 64,536 | 77,199 | 83,897 |

| 24 + 25 | 23,384 | 23,803 | 27,837 | 27,527 | 27,185 | 28,690 | 26,678 | 27,516 | 31,625 |

| 26 + 27 | 306 | 301 | 284 | 285 | 294 | 300 | 292 | 276 | 301 |

| 28 + 33 | 524 | 526 | 509 | 522 | 540 | 549 | 534 | 513 | 565 |

| 29 + 30 | 760 | 735 | 678 | 665 | 682 | 699 | 685 | 639 | 687 |

| 31 + 32 | 235 | 245 | 239 | 248 | 253 | 260 | 255 | 249 | 266 |

| 35 + 36 | 108,349 | 118,537 | 119,578 | 126,667 | 136,600 | 140,540 | 130,433 | 123,361 | 139,520 |

| 37 + 38 + 39 | 153 | 158 | 162 | 175 | 185 | 187 | 179 | 176 | 199 |

| 41 + 42 + 43 | 3728 | 3751 | 3620 | 3712 | 3847 | 3911 | 3801 | 3640 | 4008 |

| 45 | 1185 | 1257 | 1762 | 1851 | 1878 | 1746 | 1729 | 1708 | 1898 |

| 46 | 1807 | 1920 | 6511 | 6449 | 6253 | 4885 | 5040 | 4832 | 5175 |

| 47 | 1822 | 1935 | 4658 | 4696 | 4618 | 3817 | 3881 | 3759 | 4080 |

| 49 | 9648 | 10,261 | 12,015 | 12,644 | 13,252 | 12,658 | 12,321 | 11,925 | 13,353 |

| 50 | 1164 | 1357 | 5223 | 4838 | 3594 | 2694 | 3210 | 3761 | 3709 |

| 51 | 3754 | 4090 | 4227 | 4304 | 4921 | 4905 | 4371 | 1651 | 2098 |

| 52 + 79 | 489 | 521 | 1565 | 1556 | 1517 | 1210 | 1240 | 1190 | 1279 |

| 53 + 61 | 74 | 79 | 268 | 266 | 258 | 201 | 208 | 199 | 213 |

| 55 + 56 | 715 | 762 | 3350 | 3282 | 3159 | 2386 | 2480 | 2359 | 2504 |

| 58 + 59 + 60 + 90 + 91 + 92 + 93 | 54 | 57 | 238 | 234 | 225 | 171 | 178 | 170 | 181 |

| 62 + 63 | 47 | 49 | 78 | 81 | 82 | 74 | 73 | 72 | 80 |

| 68 | 371 | 398 | 408 | 440 | 464 | 469 | 449 | 441 | 498 |

| 69 + 70 + 71 + 72 + 73 + 74 + 75 + 78 + 80+ 81 + 82 | 472 | 502 | 1146 | 1158 | 1142 | 954 | 967 | 936 | 1019 |

| 77 | 48 | 51 | 74 | 77 | 78 | 72 | 72 | 71 | 78 |

| 85 | 114 | 121 | 1803 | 1726 | 1627 | 1117 | 1195 | 1118 | 1158 |

| 86 + 87 + 88 | 188 | 202 | 1345 | 1300 | 1242 | 900 | 943 | 886 | 930 |

| 95 + 96 | 141 | 150 | 815 | 794 | 759 | 559 | 587 | 557 | 587 |

Table A6.

The impact of the main floods on lending in Turkey with additional variables.

| Dependent Variable: ∂(LOANS)st Estimation Method: Panel Least Squares | ||||

|---|---|---|---|---|

| 1 | 2 | 3 | 4 | |

| C | −41,463,726 *** (13,721,062) | −16,497,319 * (9,209,414) | −38,423,098 *** (14,648,789) | −11,491,869 (9,801,190) |

| ∂(LOANS)st−1 | 0.010111 (0.054857) | 0.016993 (0.053439) | 0.211454 *** (0.054000) | 0.225946 *** (0.051767) |

| ∂(NPLRATIOst) | −34,652,631 *** (6,660,165) | −32,452,880 *** (6,466,236) | −30,232,937 *** (6,956,792) | −28,174,752 *** (6,761,418) |

| ∂(VAst) | −0.000161 * (8.95 × 10−5) | −0.000246 *** (8.90 × 10−5) | −5.14 × 10−5 (9.17 × 10−5) | −0.000116 (9.12 × 10−5) |

| ∂(CO2)st−1 | −35.75991 (125.7362) | 41.36008 (93.01380) | 48.24618 (126.9419) | 155.6697 * (87.35823) |

| ∂(CO2)st−1*D2015 | −39.27358 (144.2516) | −87.87949 (149.9677) | ||

| ∂(CO2)st−1*D2019 | −39.62631 (143.0178) | −255.0271 * (139.1890) | ||

| ∂(INVSETst) | 5323.494 (18,710.76) | 27,662.49 *** (9011.493) | 82,076.65 *** (16,530.13) | 52,748.22 *** (8349.350) |

| ∂(INVSETst)*D2015 | 45,044.03 ** (19,336.54) | −18,205.09 (18,518.94) | ||

| ∂(INVSETst)*D2019 | 122,649.0 *** (23,063.40) | 103,114.8 *** (23,421.08) | ||

| D2015 | −1,014,612 ** (510,482.8) | −445,570.6 (539,281.5) | ||

| D2019 | −254,285.7 (404,927.4) | 158,201.6 (427,720.5) | ||

| ∂(GDP)t−1 | −2.029624 (3.662386) | −0.666831 (3.913548) | −7.146751 * (3.867557) | −3.707346 (4.160369) |

| ∂(Real Interb Rate)t−1 | −24,234.40 (20,961.12) | −16,771.28 (21,989.76) | −34,846.14 (22,369.49) | −35,458.57 (23,361.85) |

| Log(TotEquity)t−1 | 3,721,902 *** (1,204,335) | 1,516,435 (803,081.2) | 3,403,082 *** (1,285,616) | 1,049,656 (854,422.0) |

| Sample | 2010–2021 | 2010–2021 | 2010–2021 | 2010–2021 |

| Total Observations | 432 | 432 | 432 | 432 |

| Adjusted R-squared | 0.36 | 0.39 | 0.26 | 0.31 |

| F-statistic | 6.18 *** | 7.07 *** | 15.07 *** | 18.44 *** |

| DW | 2.25 | 2.30 | 2.20 | 2.29 |

| Cross-section fixed effects | Yes | Yes | No | No |

| Period fixed effects | No | No | No | No |

* significant at 10%, ** significant at 5%, *** significant at 1%. Standard error in brackets.

Table A7.

Lending relative to value added of the sector without period fixed effects.

| Dependent Variable: ∂ (LOANSst/VAst) Estimation Method: Panel Least Squares | ||||

|---|---|---|---|---|

| 1 | 2 | 3 | 4 | |

| C | −0.003872 (0.003780) | 0.005587 ** (0.002602) | −0.003694 (0.003637) | 0.005493 ** (0.002507) |

| ∂(LOANSst−1/VAst−1) | −0.504135 *** (0.072589) | −0.499060 *** (0.071241) | −0.478311 *** (0.067748) | −0.473509 *** (0.066053) |

| ∂(CO2st−1/VAst−1) | 31.11498 (79.53593) | 52.08928 (62.17235) | 28.87092 (73.53356) | 38.85587 (57.60055) |

| ∂(CO2st−1/VAst−1)*D2015 | 43.48320 (107.9941) | 31.57589 (102.5113) | ||

| ∂(CO2st−1/VAst−1)*D2019 | 7.508978 (121.9143) | 5.730307 (109.3602) | ||

| ∂(NPLst/VAst) | 4.758286 *** (0.815275) | 4.658038 *** (0.806216) | 4.888359 *** (0.766911) | 4.795813 *** (0.758947) |

| ∂(INVSETst) | 5.38 × 10−6 (5.21 × 10−6) | 3.52 × 10−6 (2.56 × 10−6) | 6.72 × 10−6 * (4.04 × 10−6) | 4.31 × 10−6 ** (2.08 × 10−6) |

| ∂(INVSETst)*D2015 | −3.84 × 10−6 (5.41 × 10−6) | −7.62 × 10−6 (6.23 × 10−6) | −4.92 × 10−6 (4.64 × 10−6) | −7.95 × 10−6 (5.70 × 10−6) |

| ∂(INVSETst)*D2019 | ||||

| D2015 | −0.000193 (0.000141) | −0.000177 (0.000134) | ||

| D2019 | 0.000284 ** (0.000114) | 0.000284 *** (0.000109) | ||

| ∂(GDP)t−1 | −1.62 × 10−9 * (9.52× 10−10) | 1.95× 10−10 (1.10 × 10−9) | −1.63 × 10−9 * (9.17 × 10−10) | 1.76× 10−10 (1.06 × 10−9) |

| ∂(Real Interb Rate)t−1 | −1.41 × 10−5 ** (5.77 × 10−6) | −2.08 × 10−5 *** (6.14 × 10−6) | −1.43 × 10−5 ** (5.56 × 10−6) | −2.10 × 10−5 *** (5.91 × 10−6) |

| Log(TotEquity)t−1 | 0.000352 (0.000332) | −0.000483 ** (0.000227) | 0.000335 (0.000319) | −0.000475 ** (0.000218) |

| Sample | 2010–2021 | 2010–2021 | 2010–2021 | 2010–2021 |

| Total Observations | 432 | 432 | 432 | 432 |

| Adjusted R-squared | 0.22 | 0.23 | 0.28 | 0.28 |

| F-statistic | 3.73 *** | 3.82 *** | 17.53 *** | 17.92 *** |

| DW | 2.07 | 2.07 | 2.07 | 2.06 |

| Cross-section fixed effects | Yes | Yes | No | No |

| Period fixed effects | No | No | No | No |

* significant at 10%, ** significant at 5%, *** significant at 1%. Standard error in brackets.

Table A8.

CO2 emissions and the allocation of loans between sectors without period fixed effects.

| Dependent Variable: ∂ (LOANSst/TOTLOANSst) Estimation Method: Panel Least Squares | ||||

|---|---|---|---|---|

| 1 | 2 | 3 | 4 | |

| C | −0.015573 (0.012601) | −0.002837 (0.011065) | −0.020570 * (0.012170) | −0.002113 (0.011239) |

| ∂(LOANSst−1/TOTLOANSst−1) | −0.209425 *** (0.047336) | −0.203547 *** (0.047232) | −0.134295 *** (0.045599) | −0.099946 ** (0.045284) |

| ∂(NPLst/TOTNPLt) | 0.073013 *** (0.020396) | 0.076663 *** (0.020875) | 0.088379 *** (0.018991) | 0.103292 *** (0.019516) |

| ∂(VAst/VASUMt) | 0.165689 *** (0.051201) | 0.157052 *** (0.050820) | 0.153404 *** (0.049317) | 0.137420 *** (0.049625) |

| ∂(CO2st−1/CO2TOTt−1) | −0.158698 ** (0.062298) | −0.158176 *** (0.044900) | −0.179905 *** (0.058853) | −0.198917 *** (0.043629) |

| ∂(CO2st−1/CO2TOTt−1)*D2015 | 0.061692 (0.074892) | 0.061078 (0.072416) | ||

| ∂(CO2st−1/CO2TOTt−1)*D2019 | 0.098271 (0.076753) | 0.114919 (0.077133) | ||

| ∂(INVSETst/INVTOTt) | 0.020870 ** (0.008541) | −0.000539 ** (0.000254) | 0.027712 *** (0.007150) | −0.000524 ** (0.000247) |

| ∂(INVSETst/INVTOTt)*D2015 | −0.021427 ** (0.008526) | −0.028296 *** (0.007151) | ||

| ∂(INVSETst/INVTOTt)*D2019 | −0.006173 ** (0.002898) | −0.004603 (0.002830) | ||

| ∂(GDP)t−1 | −9.97× 10−10 (5.48 × 10−9 ) | −9.14× 10−10 (5.49 × 10−9 ) | −1.32× 10−9 (5.49 × 10−9 ) | −6.81× 10−10 (5.58 × 10−9 ) |

| ∂(Real Interb Rate)t−1 | 2.37 × 10−6 (3.40 × 10−5) | 3.22 × 10−6 (3.41 × 10−5) | 3.14 × 10−6 (3.41 × 10−5) | 2.40 × 10−6 (3.46 × 10−5) |

| Log(TotEquity)t−1 | 0.001322 (0.001080) | 0.000252 (0.000952) | 0.001746 * (0.001044) | 0.000188 (0.000967) |

| Sample | 2010–2021 | 2010–2021 | 2010–2021 | 2010–2021 |

| Total Observations | 432 | 432 | 432 | 432 |

| Adjusted R-squared | 0.13 | 0.13 | 0.13 | 0.10 |

| F-statistic | 2.44 *** | 2.41 *** | 7.16 *** | 5.76 *** |

| DW | 1.95 | 1.93 | 1.93 | 1.94 |

| Cross-section fixed effects | Yes | Yes | No | No |

| Period fixed effects | No | No | No | No |

* significant at 10%, ** significant at 5%, *** significant at 1%. Standard error in brackets.

References

- Aslan, C.; Bulut, E.; Cepni, O.; Yilmaz, M.H. Does climate change affect bank lending behavior? Econ. Lett. 2022, 220, 110859. [Google Scholar] [CrossRef]

- Cortés, K.R.; Strahan, P.E. Tracing out capital flows: How financially integrated banks respond to natural disasters. J. Financ. Econ. 2017, 125, 182–199. [Google Scholar] [CrossRef]

- Brei, M.; Mohanb, P.; Strobl, E. The impact of natural disasters on the banking sector: Evidence from hurricane strikes in the Caribbean. Q. Rev. Econ. Financ. 2019, 72, 232–239. [Google Scholar] [CrossRef]

- Ivanov, I.T.; Macchiavelli, M.; Santos, J. Bank lending networks and the propagation of natural disasters. Financ. Manag. 2020, 51, 903–927. [Google Scholar] [CrossRef]

- Faiella, I.; Natoli, F. Natural Catastrophes and Bank Lending: The Case of Food Risk in Italy; Bank of Italy Occasional Paper; Bank of Italy: Rome, Italy, 2018; Volume 457. [Google Scholar]

- Li, S.; Wu, X. How does climate risk affect bank loan supply? Empirical evidence from China. Econ. Chang. Restruct. 2023, 56, 2169–2204. [Google Scholar] [CrossRef]

- Berger, A.N.; Guedhami, O.; Kim, H.H.; Li, X. Economic Policy Uncertainty and Bank Liquidity Hoarding. J. Financ. Intermediation Forthcom. 2022, 49, 100893. [Google Scholar] [CrossRef]

- Lee, C.-C.; Wang, C.-W.; Thinh, B.-T.; Xu, Z.-T. Climate risk and bank liquidity creation: International evidence. Int. Rev. Financ. Anal. 2022, 82, 102198. [Google Scholar] [CrossRef]

- Do, Q.A.; Phan, V.; Nguyen, D.T. How do local banks respond to natural disasters? Eur. J. Financ. 2023, 29, 754–779. [Google Scholar] [CrossRef]

- Hosono, K.; Miyakawa, D.; Uchino, T.; Hazama, M.; Ono, A.; Uchida, H.; Uesugi, I. Natural Disasters, Damage to Banks, and Firm Investment. Int. Econ. Rev. 2016, 57, 1335–1370. [Google Scholar] [CrossRef]

- David, M.A. How do international financial flows to developing countries respond to natural disasters? Int. Monet. Fund 2010, 11, 1850243. [Google Scholar] [CrossRef]

- Berg, G.; Schrader, J. Access to credit, natural disasters, and relationship lending. J. Financ. Intermediat. 2012, 21, 549–568. [Google Scholar] [CrossRef]

- Islam, M.N.; Wheatley, C.M. Impact of Climate Risk on Firms’ Use of Trade Credit: International Evidence. Int. Trade J. 2020, 35, 40–59. [Google Scholar] [CrossRef]

- Horvath, G. Natural catastrophes and financial depth: An empirical analysis. J. Financ. Stab. 2021, 53, 100842. [Google Scholar] [CrossRef]

- Li, S.; Li, Q.; Lu, S. The impact of climate risk on credit supply to private and public sectors: An empirical analysis of 174 countries. Environ. Dev. Sustain. 2022, 26, 2443–2465. [Google Scholar] [CrossRef] [PubMed]

- Sun, H.; Bless, K.E.; Sun, C.; Kporsu, A.K. Institutional quality, green innovation and energy efficiency. Energy Policy 2019, 135, 111002. [Google Scholar] [CrossRef]

- Fatica, S.; Panzica, R.; Rancan, M. The pricing of green bonds: Are financial institutions special? J. Financ. Stab. 2021, 54, 100873. [Google Scholar] [CrossRef]

- Gangi, F.; Meles, A.; D’Angelo, E.; Daniele, L.M. Sustainable development and corporate governance in the financial system: Are environmentally friendly banks less risky? Corp. Soc. Responsib. Environ. Manag. 2019, 26, 529–547. [Google Scholar] [CrossRef]

- Kacperczyk, M.; Peydró, J. Carbon Emissions and the Bank-Lending Channel. 2022. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3915486 (accessed on 20 December 2023).

- Mésonnier, J. Banks’ Climate Commitments and Credit to Brown Industries: New Evidence for France. Banque de France Working Paper 743. 2019. Available online: https://ssrn.com/abstract=3502681 (accessed on 12 November 2023).

- Delis, M.D.; de Greiff, K.; Ongena, S. Being Stranded on the Carbon Bubble? Climate Policy Risk and the Pricing of Bank Loans; Swiss Finance Institute Research Paper Series 18-10; Swiss Finance Institute: Zürich, Switzerland, 2018. [Google Scholar]

- Giannetti, M.; Jasova, M.; Lomiouti, M.; Mendicino, C. “Glossy Green” Banks: The Disconnect between Environmental Disclosures and Lending Activities. ECB Working Paper. 2023. Available online: https://ssrn.com/abstract=4668588 (accessed on 30 December 2023).

- Verga, G.; Soana, M.G. Supply and demand in the European credit market during the recent crisis. Appl. Financ. Econ. 2012, 22, 1355–1366. [Google Scholar] [CrossRef]

- Mueller, I.; Sfrappini, S. Climate Change-Related Regulatory Risks and Bank Lending. ECB Working Paper No. 2022/2670. 2022. Available online: https://ssrn.com/abstract=4144358 (accessed on 2 October 2023).

- Loayza, N.V.; Olaberria, E.; Rigolini, J.; Christiaensen, L. Natural Disasters and Growth: Going beyond the Averages. World Dev. 2012, 40, 1317–1336. [Google Scholar] [CrossRef]

- Gan, J. Collateral, debt capacity, and corporate investment: Evidence from a natural experiment. J. Financ. Econ. 2007, 85, 709–734. [Google Scholar] [CrossRef]

- Kasap, Y.; Şensöğüt, C.; Ören, Ö. Efficiency change of coal used for energy production in Turkey. Resour. Policy 2020, 65, 101577. [Google Scholar] [CrossRef]

Figure 1.

CO2 emissions per capita by country 1970–2021 (tonnes CO2/capita/year). Source: EDGAR. Latest observation: 2021.

Figure 1.

CO2 emissions per capita by country 1970–2021 (tonnes CO2/capita/year). Source: EDGAR. Latest observation: 2021.

Figure 2.

CO2 emissions, value added, and non-performing loans by sector (average values 2005–2020).

Figure 2.

CO2 emissions, value added, and non-performing loans by sector (average values 2005–2020).

Figure 3.

CO2 emissions/real value added and loans/real value added in Turkey from 2005 to 2021.

Table 1.

Floods in Turkey between 2007 and 2020.

| Year | Start Date | End Date | Total Affected | Total Deaths | Disaster Description (Group-Subgroup-Type-Subtype) | Origin | Provinces |

|---|---|---|---|---|---|---|---|

| 2009 | 7 September 2009 | 10 September 2009 | 35.060 | 40 | Natural–Hydrological–Flood–Flash flood | Heavy rains | Istanbul, Tekirdag |

| 2019 | 17 August 2019 | 17 August 2019 | 15.001 | 1 | Natural–Hydrological–Flood–Flash flood | Istanbul | |

| 2015 | 30 January 2015 | 2 February 2015 | 6.508 | 8 | Natural–Hydrological–Flood–Riverine flood | Edirne | |

| 2007 | 16 November 2007 | 21 November 2007 | 2.251 | 1 | Natural–Hydrological–Flood–Riverine flood | Heavy rains | Mugla, Tekirdag, Edirne |

| 2007 | 27 May 2007 | 1 June 2007 | 763 | 13 | Natural–Hydrological–Flood–Riverine flood | Heavy rain | Agri, Van, Bitlis, Gaziantep |

| 2020 | 11 June 2020 | 12 June 2020 | 751 | 1 | Natural–Hydrological–Flood–Flash flood | Ankara | |

| 2020 | 7 January 2020 | 9 January 2020 | 302 | 2 | Natural–Meteorological–Storm–Convective storm | Mersin, Antalya | |

| 2008 | 1 August 2008 | 5 August 2008 | 302 | 2 | Natural–Climatological–Wildfire–Forest fire | Drought, high winds, heat waves, human factors | Antalya |

| 2017 | 27 July 2017 | 27 July 2017 | 270 | 0 | Natural–Meteorological–Storm–Convective storm | Istanbul | |

| 2019 | 17 July 2019 | 18 July 2019 | 227 | 7 | Natural–Hydrological–Flood–Flash flood | Duzce | |

| 2010 | 27 August 2010 | 27 August 2010 | 219 | 13 | Natural–Hydrological–Landslide–Landslide | Torrential rains | Rize |

| 2007 | 3 August 2007 | 3 August 2007 | 188 | 2 | Natural–Hydrological–Flood–Riverine flood | Heavy rain | Erzurum |

| 2020 | 4 February 2020 | 5 February 2020 | 125 | 41 | Natural–Hydrological–Landslide–Avalanche | Van | |

| 2018 | 8 July 2018 | 8 July 2018 | 124 | 24 | Natural–Hydrological–Landslide–Landslide | Heavy rains | Tekirdag |

| 2009 | 10 July 2009 | 16 July 2009 | 118 | 7 | Natural–Hydrological–Flood–Riverine flood | Heavy rains | Artvin, Sinop, Ordu, Bartin |

| 2019 | 18 June 2019 | 20 June 2019 | 80 | 10 | Natural–Hydrological–Flood–Flash flood | Heavy rains | Trabzon |

| 2020 | 21 June 2020 | 23 June 2020 | 79 | 7 | Natural–Hydrological–Flood–Flash flood | Bursa | |

| 2009 | 25 January 2009 | 25 January 2009 | 17 | 11 | Natural–Hydrological–Landslide–Avalanche | High temperatures | Gumushane |

| 2011 | 8 October 2011 | 11 October 2011 | 11 | 8 | Natural–Hydrological–Flood–Riverine flood | Heavy rains | Antalya, Denizli, Manisa |

| 2020 | 22 August 2020 | 23 August 2020 | 16 | 16 | Natural–Hydrological–Flood | Samsun, Rize, Trabzon, Giresun | |

| 2015 | 25 August 2015 | 25 August 2015 | 9 | 9 | Natural–Hydrological–Flood–Flash flood | Pouring rainfall | Artvin |

| 2013 | 28 January 2013 | 28 January 2013 | 7 | 7 | Natural–Hydrological–Landslide–Landslide | Heavy rains | Sirnak |

| 2012 | 4 July 2012 | 4 July 2012 | 13 | 13 | Natural–Hydrological–Flood–Riverine flood | Heavy rains | Samsun |

| 2009 | 21 November 2009 | 22 November 2009 | 4 | 4 | Natural–Hydrological–Landslide–Landslide | Torrential rain | Trabzon, Giresun |

| 2007 | 31 May 2007 | 31 May 2007 | 3 | 3 | Natural–Meteorological–Extreme temperature–Heat wave | Burdur, Sinop |

Note: Total affected column shows the number of people affected from the flood (including deaths). Disaster type is named “natural”. The data is sorted from highest to lowest according to the “Total Affected” column. Source: EM-DAT (International Disaster Database).

Table 2.

Descriptive statistics.

| Main Variable | Unit | Definition | Mean | Median | Std. Dev. | Min. | Max. |

|---|---|---|---|---|---|---|---|

| Sector Loan | Billion TL | Change in stock loan amount on sectoral basis | 5.77 | 1.78 | 12.82 | −31.85 | 133.61 |

| Total Loans | Billion TL | Change in total loan amount of the banks | 207.67 | 152.41 | 251.23 | 9.68 | 1019.12 |

| Sector NPL | Billion TL | Change in non-performing loan amount on sectoral basis | 0.21 | 0.03 | 0.84 | −1.20 | 11.66 |

| Total NPL | Billion TL | Change in non-performing loan amount of the banks | 7.55 | 2.84 | 12.66 | −0.84 | 48.43 |

| Interest Rate | % | Interbank rate | 10.3 | 7.5 | 5.6 | 1.6 | 22.5 |

| Sector CO2 | Gigagram | CO2 emissions on a sectoral basis | 7407 | 949 | 21,480 | 26 | 140,540 |

| Total CO2 | Gigagram | CO2 emissions of all sectors | 266,665 | 259,496 | 41,317 | 201,198 | 332,638 |

| Sector Value Added | Billion TL | Value added at factor costs at sectoral basis | 20.6 | 9.7 | 30.2 | 0.2 | 300.8 |

| Total Value Added | Billion TL | Total value added at factor costs | 743.0 | 499.1 | 641.0 | 191.7 | 2670.6 |

| Sector Investment | Million TL | Change in tangible fixed assets on sectoral basis | 6 | 3 | 15 | −77 | 157 |

| Total Investment | Million TL | Change in tangible fixed assets on sectoral basis | 231 | 243 | 134 | −28 | 425 |

| NPL Ratio | % | Non-Performing Loans/(Performing Loans + Non-Performing Loans) | 3.5 | 2.8 | 2.8 | 0.1 | 20.3 |

Table 3.

The impact of the main floods on lending in Turkey.

| Dependent Variable: ∂(LOANS)st Estimation Method: Panel Least Squares | |||||

|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 | |

| C | 1,005,112 *** (100,785.4) | 991,454.6 *** (100,132.7) | 965,255.3 *** (101,005.5) | 1,066,647 *** (139,911.3) | 976,731.0 *** (132,534.1) |

| ∂(LOANS)st−1 | −0.091259 * (0.049359) | −0.087288 * (0.049578) | −0.075999 (0.049346) | −0.119598 ** (0.055060) | −0.101683 * (0.054946) |

| ∂(NPLRATIOst) | −17,718,942 *** (525,708) | −17,854,382 *** (5,262,147) | −17,933,414 *** (5,248,747) | −21,906,659 *** (6,810,829) | −22,097,838 *** (6,755,282) |

| ∂(VAst) | 0.000335 *** (5.56 × 10−5) | 0.000340 *** (5.57 × 10−5) | 0.000332 *** (5.55 × 10−5) | 0.000292 *** (6.84 × 10−5) | 0.000247 *** (7.07 × 10−5) |

| ∂(CO2)st−1 | −216.0735 * (117.7448) | −110.0905 (70.42866) | −29.11581 (64.38706) | −68.02901 (121.2411) | 44.26970 (91.21884) |

| ∂(CO2)st−1*D2009 | 145.5409 (128.1418) | ||||

| ∂(CO2)st−1*D2015 | 29.11072 (95.41738) | −5.165647 (139.5781) | |||

| ∂(CO2)st−1*D2019 | −183.1634 (113.4169) | −133.2022 (139.1307) | |||

| ∂(INVSETst) | 843.9425 (18,111.17) | 18,437.52 ** (9088.077) | |||

| ∂(INVSETst)*D2015 | 27,911.93 (18,755.62) | ||||

| ∂(INVSETst)*D2019 | 58,867.41 ** (24,444.92) | ||||

| Sample | 2007–2021 | 2007–2021 | 2007–2021 | 2010–2021 | 2010–2021 |

| Total Observations | 540 | 540 | 540 | 432 | 432 |

| Adjusted R-squared | 0.41 | 0.41 | 0.41 | 0.42 | 0.43 |

| F-statistic | 7.87 *** | 7.83 *** | 7.91 *** | 6.88 *** | 7.09 *** |

| DW | 2.01 | 2.00 | 2.03 | 2.12 | 2.15 |

| Cross-section fixed effects | Yes | Yes | Yes | Yes | Yes |

| Period fixed effects | Yes | Yes | Yes | Yes | Yes |

* significant at 10%, ** significant at 5%, *** significant at 1%. Standard error in brackets.

Table 4.

Lending relative to value added of the sector.

| Dependent Variable: ∂ (LOANSst/VAst) Estimation Method: Panel Least Squares | |||||

|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 | |

| C | 8.53 × 10−5 *** (2.46 × 10−5) | 8.56 × 10−5 *** (2.45 × 10−5) | 8.51 × 10−5 *** (2.44 × 10−5) | 4.23 × 10−5 (3.24 × 10−5) | 5.26 × 10−5 * (3.16 × 10−5) |

| ∂(LOANSst−1/VAst−1) | −0.451685 *** (0.053234) | −0.459013 *** (0.059666) | −0.454011 *** (0.057582) | −0.475886 *** (0.067968) | −0.475805 *** (0.066809) |

| ∂(CO2st−1/VAst−1) | 12.43697 (72.93898) | 15.32679 (39.46820) | 19.52034 (36.04436) | 32.74124 (73.91078) | 33.82579 (57.93156) |

| ∂(CO2st−1/VAst−1)*D2009 | 10.94941 (82.41471) | ||||

| ∂(CO2st−1/VAst−1)*D2015 | 23.24363 (77.48787) | 18.28062 (102.4731) | |||

| ∂(CO2st−1/VAst−1)*D2019 | 14.16365 (95.37290) | 2.758186 (109.1711) | |||

| ∂(NPLst/VAst) | 4.737733 *** (0.718856) | 4.711741 *** (0.725115) | 4.739007 *** (0.718443) | 4.794958 *** (0.802638) | 4.824973 *** (0.795534) |

| ∂(INVSETst) | 6.36 × 10−6 (4.06 × 10−6) | 3.25 × 10−6 (2.12 × 10−6) | |||

| ∂(INVSETst)*D2015 | −5.48 × 10−6 (4.65 × 10−6) | ||||

| ∂(INVSETst)*D2019 | −8.01 × 10−6 (5.94 × 10−6) | ||||

| Sample | 2007–2021 | 2007–2021 | 2007–2021 | 2010–2021 | 2010–2021 |

| Total Observations | 540 | 540 | 540 | 432 | 432 |

| Adjusted R-squared | 0.27 | 0.27 | 0.27 | 0.29 | 0.29 |

| F-statistic | 12.24 *** | 12.25 *** | 12.24 *** | 11.22 *** | 11.26 *** |

| DW | 2.01 | 2.00 | 2.00 | 2.07 | 2.07 |

| Cross-section fixed effects | No | No | No | No | No |

| Period fixed effects | Yes | Yes | Yes | Yes | Yes |

* significant at 10%, *** significant at 1%. Standard error in brackets.

Table 5.

CO2 emissions and the allocation of loans between sectors.

| Dependent Variable: ∂ (LOANSst/TOTLOANSst) Estimation Method: Panel Least Squares | |||||

|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 | |

| C | 6.85 × 10−17 (0.000169) | 6.14 × 10−17 (0.000169) | 6.42 × 10−17 (0.000170) | −0.000170 (0.000196) | 5.69 × 10−5 (0.000178) |

| ∂(LOANSst−1/TOTLOANSst−1) | −0.042625 (0.040316) | −0.046170 (0.040253) | −0.045051 (0.040466) | −0.204685 *** (0.047102) | −0.203399 *** (0.047053) |

| ∂(NPLst/TOTNPLt) | 0.035152 ** (0.015715) | 0.034309 ** (0.015701) | 0.032515 ** (0.015779) | 0.072634 *** (0.020357) | 0.076668 *** (0.020797) |

| ∂(VAst/VASUMt) | 0.164782 *** (0.044940) | 0.147882 *** (0.044866) | 0.154642 *** (0.044674) | 0.165827 *** (0.051108) | 0.157072 *** (0.050630) |

| ∂(CO2st−1/CO2TOTt−1) | 0.126020 (0.101152) | −0.002633 (0.035753) | −0.026245 (0.031419) | −0.163950 *** (0.062048) | −0.158202 *** (0.044733) |

| ∂(CO2st−1/CO2TOTt−1)*D2009 | −0.177371 * (0.107436) | ||||

| ∂(CO2st−1/CO2TOTt−1)*D2015 | −0.085170 (0.058408) | 0.067780 (0.074602) | |||

| ∂(CO2st−1/CO2TOTt−1)*D2019 | −0.044083 (0.073076) | 0.098526 (0.076463) | |||

| ∂(INVSETst/INVTOTt) | 0.015440 ** (0.007369) | −0.000540 ** (0.000253) | |||

| ∂(INVSETst/INVTOTt)*D2015 | −0.016004 ** (0.007356) | ||||

| ∂(INVSETst/INVTOTt)*D2019 | −0.006031 ** (0.002854) | ||||

| Sample | 2007–2021 | 2007–2021 | 2007–2021 | 2010–2021 | 2010–2021 |

| Total Observations | 540 | 540 | 540 | 432 | 432 |

| Adjusted R-squared | 0.09 | 0.09 | 0.09 | 0.13 | 0.13 |

| F-statistic | 2.36 *** | 2.34 *** | 2.29 *** | 2.58 *** | 2.60 *** |

| DW | 2.12 | 2.11 | 2.12 | 1.95 | 1.93 |

| Cross-section fixed effects | Yes | Yes | Yes | Yes | Yes |

| Period fixed effects | No | No | No | No | No |

* significant at 10%, ** significant at 5%, *** significant at 1%. Standard error in brackets.

Table 6.

Allocation of the loans and number of people affected by natural disasters in Turkey.

| Estimation Method: Panel Least Squares | |||||

|---|---|---|---|---|---|

| 1 | 2 | 3 | |||

| Dependent Variable: | ∂ (LOANSst) | ∂(LOANSst/VAst) | ∂(LOANSst/ TOTLOANSt) | ||

| C | 898,103.8 *** (145,082.7) | C | 1.37 × 10−5 (3.80 × 10−5) | C | 1.61 × 10−5 (0.000198) |

| ∂(LOANSst−1) | −0.117976 ** (0.053186) | ∂(LOANSst−1/VAst−1) | −0.496480 *** (0.067319) | ∂(LOANSst−1/TOTLOANSt−1) | −0.188929 *** (0.046938) |

| ∂(CO2st−1) | −77.75375 (63.80037) | ∂(CO2st−1/VAst−1) | 52.64141 (59.30989) | ∂(NPLst/TOTNPLt) | 0.070529 *** (0.020464) |

| ∂(NPLRATIOst) | −33,554,090 *** (6,287,561) | ∂(NPLst/VAst) | 4.729198 *** (0.815984) | ∂(VAst/VASUMt) | 0.158392 *** (0.050984) |

| ∂(VAst) | 0.000393 *** (5.89 × 10−5) | ∂(INVSETst) | 2.51 × 10−6 (2.43 × 10−6) | ∂(CO2st−1/CO2TOTt−1) | −0.121864 *** (0.036567) |

| ∂(INVSETst) | 28,248.57 *** (8601.873) | TOTAFFNATt−1 | 7.66 × 10−9 ** (2.99× 10−9 ) | ∂(INVSETst/INVTOTt) | −0.000580 ** (0.000254) |

| TOTAFFNATt−1 | −2.722095 (10.88668) | TOTAFFNATt−1 | −1.65 × 10−20 (1.76 × 10−8 ) | ||

| Sample | 2010–2021 | 2010–2021 | 2010–2021 | ||

| Total Observations | 432 | 432 | 432 | ||

| Adjusted R-squared | 0.39 | 0.20 | 0.12 | ||

| F-statistic | 7.84 *** | 3.72 *** | 2.47 *** | ||

| DW | 2.14 | 2.09 | 1.95 | ||

| Cross-section fixed effects | Yes | Yes | Yes | ||

| Period fixed effects | No | No | No | ||

** significant at 5%, *** significant at 1%. Standard error in brackets.

Table 7.

Lending and CO2 emissions in the more polluting sectors.

| Dependent Variable: ∂ (LOANSst) Estimation Method: Panel Least Squares | |||||

|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 | |

| C | 1,092,092 *** (140,590.8) | 1,068,805 *** (138,616.2) | 1,015,951 *** (140,072.9) | 1,149,411 *** (187,123.8) | 908,797.3 *** (181,217.5) |

| ∂(LOANS)st−1 | 0.003449 (0.073509) | 0.012864 (0.073652) | 0.031653 (0.072868) | −0.027864 (0.080772) | 0.025108 (0.080575) |

| ∂(NPLRATIOst) | −34,802,255 *** (9,037,145) | −34,920,261 *** (9,052,856) | −34,805,955 *** (8,985,677) | −40,894,632 *** (11,521,580) | −42,803,859 *** (11,256,562) |

| ∂(VAst) | 0.000303 *** (6.76 × 10−5) | 0.000309 *** (6.77 × 10−5) | 0.000299 *** (6.72 × 10−5) | 0.000216 ** (8.39 × 10−5) | 0.000125 (8.91 × 10−5) |

| ∂(CO2)st−1 | −208.8401 * (113.7210) | −120.0343 * (67.53861) | −42.76500 (62.26676) | −83.50744 (113.3827) | 37.63014 (86.16163) |

| ∂(CO2)st−1*D2009 | 110.3091 (123.9884) | ||||

| ∂(CO2)st−1*D2015 | 5.678624 (91.78015) | −21.99148 (130.5297) | |||

| ∂(CO2)st−1*D2019 | −200.0598 * (107.8083) | −101.4600 (130.8603) | |||

| ∂(INVSETst) | −2825.639 (18,865.37) | 23,917.77 ** (11,782.84) | |||

| ∂(INVSETst)*D2015 | 43,432.39 ** (19,928.26) | ||||

| ∂(INVSETst)*D2019 | 96,716.82 *** (30,686.03) | ||||

| Sample | 2007–2021 | 2007–2021 | 2007–2021 | 2010–2021 | 2010–2021 |

| Total Observations | 270 | 270 | 270 | 216 | 216 |

| Adjusted R-squared | 0.52 | 0.52 | 0.53 | 0.55 | 0.57 |

| F-statistic | 9.17 *** | 9.11 *** | 9.34 *** | 8.49 *** | 9.08 *** |

| DW | 1.93 | 1.91 | 1.95 | 2.15 | 2.22 |

| Cross-section fixed effects | Yes | Yes | Yes | Yes | Yes |

| Period fixed effects | Yes | Yes | Yes | Yes | Yes |

* significant at 10%, ** significant at 5%, *** significant at 1%. Standard error in brackets.

Table 8.

The relationship between LOANS/VA and CO2/VA in the more polluting sectors.

| Dependent Variable: ∂ (LOANSst/VAst) Estimation Method: Panel Least Squares | |||||

|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 | |

| C | 0.000108 ** (4.73 × 10−5) | 0.000108 ** (4.68 × 10−5) | 0.000106 ** (4.66 × 10−5) | 6.06 × 10−5 (6.29 × 10−5) | 7.52 × 10−5 (6.27 × 10−5) |

| ∂(LOANSst−1/VAst−1) | −0.482353 *** (0.077711) | −0.499834 *** (0.088875) | −0.489796 *** (0.084620) | −0.517171 *** (0.102294) | −0.507906 *** (0.099394) |

| ∂(CO2st−1/VAst−1) | 0.034946 (101.3000) | 17.01365 (54.20721) | 25.07819 (49.66097) | 27.33130 (102.4462) | 42.38499 (80.96355) |

| ∂(CO2st−1/VAst−1)*D2009 | 37.65671 (114.5524) | ||||

| ∂(CO2st−1/VAst−1)*D2015 | 53.10270 (108.4535) | 53.81078 (143.8399) | |||

| ∂(CO2st−1/VAst−1)*D2019 | 43.97011 (130.8802) | 6.109926 (153.6854) | |||

| ∂(NPLst/VAst) | 5.249556 *** (1.108305) | 5.179697 *** (1.121878) | 5.256845 *** (1.107102) | 5.062516 *** (1.242459) | 5.185369 *** (1.223347) |

| ∂(INVSETst) | 4.60 × 10−6 (6.22 × 10−6) | 3.10 × 10−6 (3.90 × 10−6) | |||

| ∂(INVSETst)*D2015 | −4.92 × 10−6 (7.68 × 10−6) | ||||

| ∂(INVSETst)*D2019 | −1.24 × 10−5 (1.08 × 10−5) | ||||

| Sample | 2007–2021 | 2007–2021 | 2007–2021 | 2010–2021 | 2010–2021 |

| Total Observations | 270 | 270 | 270 | 216 | 216 |

| Adjusted R-squared | 0.29 | 0.29 | 0.29 | 0.29 | 0.29 |

| F-statistic | 7.10 *** | 7.11 *** | 7.10 *** | 6.20 *** | 6.27 *** |

| DW | 2.02 | 2.00 | 2.01 | 2.06 | 2.07 |

| Cross-section fixed effects | No | No | No | No | No |

| Period fixed effects | Yes | Yes | Yes | Yes | Yes |

** significant at 5%, *** significant at 1%. Standard error in brackets.

Table 9.

CO2 emissions and the allocation of loans among sectors in the more polluting sectors.

| Dependent Variable: ∂ (LOANSst/TOTLOANSt) Panel Least Squares | |||||

|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 | |

| C | −7.27 × 10−5 (0.000230) | −7.60 × 10−5 (0.000231) | −6.88 × 10−5 (0.000231) | −0.000193 (0.000267) | −2.75 × 10−5 (0.000237) |

| ∂(LOANSst−1/TOTLOANSst−1) | 0.037549 (0.057682) | 0.028030 (0.057683) | 0.032655 (0.057911) | −0.102445 (0.071716) | −0.109850 (0.068636) |

| ∂(NPLst/TOTNPLt) | −0.005619 (0.023577) | −0.008645 (0.023576) | −0.013111 (0.023787) | −0.008070 (0.029148) | −0.000803 (0.029555) |

| ∂(VAst/VASUMt) | 0.211107 *** (0.053668) | 0.188687 *** (0.053622) | 0.195376 *** (0.053291) | 0.193403 *** (0.059897) | 0.179784 *** (0.058161) |

| ∂(CO2st−1/CO2TOTt−1) | 0.138469 (0.097496) | −0.007488 (0.034973) | −0.018523 (0.031271) | −0.140547 ** (0.060907) | −0.110679 ** (0.04489) |

| ∂(CO2st−1/CO2TOTt−1)*D2009 | −0.189784 (0.104224) | ||||

| ∂(CO2st−1/CO2TOTt−1)*D2015 | −0.066906 (0.057572) | 0.065822 (0.072479) | |||

| ∂(CO2st−1/CO2TOTt−1)*D2019 | −0.068727 (0.071192) | 0.019273 (0.073653) | |||

| ∂(INVSETst/INVTOTt) | 0.005097 (0.008220) | −0.000203 (0.000275) | |||

| ∂(INVSETst/INVTOTt)*D2015 | −0.005304 (0.008195) | ||||

| ∂(INVSETst/INVTOTt)*D2019 | −0.010148 *** (0.003597) | ||||

| Sample | 2007–2021 | 2007–2021 | 2007–2021 | 2010–2021 | 2010–2021 |

| Total Observations | 270 | 270 | 270 | 216 | 216 |

| Adjusted R-squared | 0.20 | 0.19 | 0.19 | 0.15 | 0.17 |

| F-statistic | 4.01 *** | 3.90 *** | 3.87 *** | 2.53 *** | 2.90 *** |

| DW | 2.09 | 2.09 | 2.10 | 1.88 | 1.90 |

| Cross-section fixed effects | Yes | Yes | Yes | Yes | Yes |

| Period fixed effects | No | No | No | No | No |

** significant at 5%, *** significant at 1%. Standard error in brackets.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |