The case of wine producers presents a typical example of contract incompleteness under asymmetric positions of power. Information asymmetry is expected to benefit the distributor as the “stronger” party. The reason is that the distributor possesses a more powerful bargaining position, considering that he/she has superior market insights, a broader range of professional personnel, more knowledge and experience in negotiation techniques, knowledge of business processes, and (most importantly) the “entry ticket” to retail chains and restaurants. The negotiation process between the mentioned actors affects the distribution of profits and the price paid by the end customer.

Contracts signed between wine producers and distributors are typically standard and simple, leaving out many important contingencies that eventually reflect on the financial performance of wine producers. Such contracts are not “relation-specific”; from the distributor’s viewpoint, logistics, warehousing, and sales comprise a standardized process. The standardization of contracts serves to lower the administration costs borne by distributors and to give them more maneuver space when providing services to wine-producers. The fact that the form of the contract is designed to serve the interests of the distributor reinforces the assumption of power asymmetry in the relationship between the wine-producers and the distributor.

In contrast to the distributor’s “standardized” approach, the perspective of the wine producer may be quite different. On the market, wine is not a homogeneous good because there are numerous opportunities for a strategic differentiation among wine producers [

34]. Moreover, wine is perceived as an experience product rather than a commodity [

35]. Wine prices on end-markets are rather elastic, depending on multiple factors such as wine origin, category, producers’ reputation, point of sale (location), occasion, presentation, and currently dominating tastes. Therefore, the possibility to manage contract conditions could grant producers access to better business performance.

By signing the contract with a distributor, the control over strategically important issues, such as the choice of the target market (in geographic or sociodemographic terms), the selling price, the extent and form of advertisement, and the type/attractiveness of sales establishment(s), will be implicitly transferred to the distributor. This observation justifies our approach in treating the relationship between wine-producers and distributors as being an agency relationship. Thus, seen from the perspective of the agricultural producer, the distributor assumes the role of an agent in a principal-agent relationship and the deployment of price and non-price market strategies of the agricultural producer will be mediated by the decision taken by the distributor. Accordingly, since the small agricultural producer engages an “agent” to act as an intermediary in accessing final consumption markets, our expectations were that agency costs will act as a mediating factor between the wine producers’ attributes and its financial performance.

3.1. Variables and Hypotheses

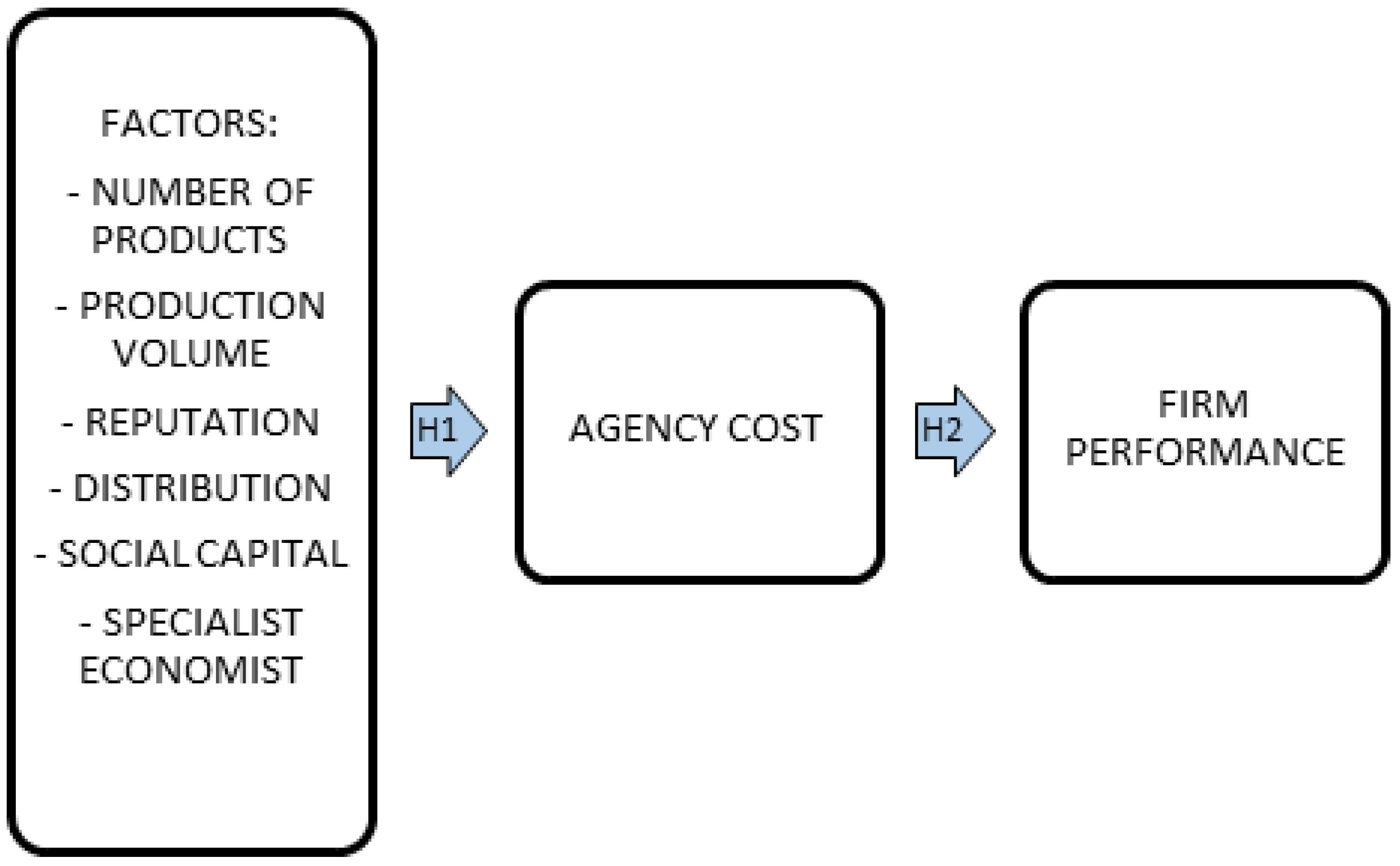

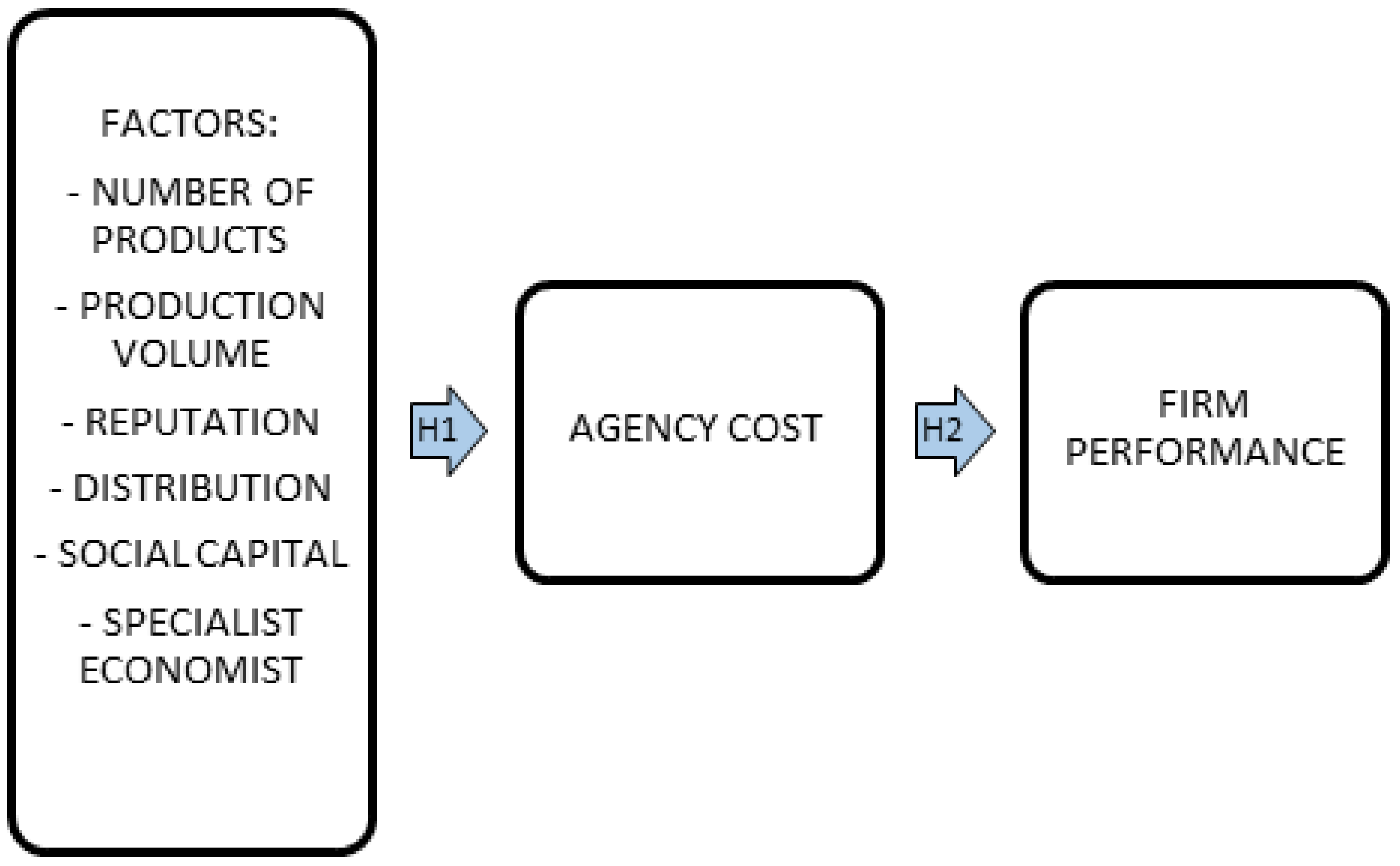

There are two main hypotheses implied by this model:

Hypothesis 1 (H1). Specific factors attributed to producers affect agency costs.

Hypothesis 2 (H2). Agency costs reflect on the wine producer’s performance.

These hypotheses were established to explain whether factors attributed to bargaining power (in market transactions) can be associated with a higher degree of agency costs. With our first hypothesis (H1), we examined the influence of factors related to the wine producer’s bargaining position on agency costs. The independent variables whose impact were as follows: number of products, production volume, reputation, number of distribution channels, social capital, and employment of a specialized economist. The choice of independent variables was intended, at least when starting this research, as an attempt to establish and measure factors that could be traced to some basic forms of agency costs. As a result, the act of hiring a specialized economist by the wine-producer may be interpreted, at least partly, as a cost undertaken in order to have better control or rather to create some awareness of how well the distributor is tending to the wine-producer’s interests. Therefore, hiring a specialist could be considered a monitoring cost. However, as our research (the interviews) proceeded, it became more apparent that there was no possibility of classifying agency costs due to the small scale of wine producers and the standard form of contract agreements. Such reasoning led us to assume that the interests served by the distributor would be primarily his own. The “level of service” that favors the interests of wine-producers eventually depends on the particular attributes of the wine-producer himself/herself. The attributes representing factors to be tested are explained in more detail bellow. Consequently, all agency costs—monitoring, bonding, and residual costs—were assumed to be included in the distributor’s margin.

Therefore, in order to measure the impact of agency costs on performance in the regression model, the difference in dealer and retail price increased by monitoring costs was treated as a reflection of agency costs, which leads to our second hypothesis (H2).

The main hypotheses were followed by sub-hypotheses:

Hypothesis 1.1 (H1.1). The number of products (labels) influences agency costs.

Hypothesis 1.2 (H1.2). The volume of production influences agency costs.

The first two variables—the number of products (measured though the number of labels offered by the wine producer; H1.1.) and production volume (expressed as the annual production in liters; H1.2.), taken from the perspective of the distributor—were expected to produce the equivalent of scale economies; it can be expected that the distributor will have higher earnings per unit as a result of efforts made in administering a relationship with a specific wine producer while the volume and variety of products increases. Therefore, the expectation is that these two factors provide a negative impact on wine-producers’ agency costs, which transforms into a positive influence on their performance. It should be noted that the previous research we consulted mostly dealt with bargaining positions and not agency costs, although Ang et al. [

36] controlled for firm sales, which, given the specifics of wine industry, is comparable with the volume of production variable that we chose. The previous studies of the impact of firm size on firm performance showed inconsistencies. Though Becker-Blease [

37] proved a negative relationship between the observed variables, Pervan and Višić [

38], Akinlo [

39], Dogan [

40], and Babalola [

41] proved a positive impact of firm size on financial performance.

Hypothesis 1.3 (H1.3). Reputation influences agency costs.

Reputation, as a factor, is expected to facilitate sales’ volume and lower the costs of advertising borne by the distributor. Although reputation is not easy to quantify because it is determined by perception and interpretation of the observer, many scientific studies have addressed the impact of reputation on product price [

42,

43] and firm financial performance [

44,

45,

46,

47,

48]. Reputation also plays an essential role in solving the problems arising from information asymmetry [

49] and reduces the incentives of opportunistic behavior, thus reducing the costs of monitoring and bonding [

50]. Moreover, Meuleman at el. [

49] tested the role of reputation in alleviating agency costs.

Hypothesis 1.4 (H1.4). Distribution influence agency costs.

The variable distribution, used by H1.4. is a factor assumed to have a different effect compared to the previous three factors. Reliance on the distributor was chosen as an indication of the level of the wine producers’ dependency. Our supposition was that the possibility to access alternative distribution channels would grant the wine producer more bargaining power, making the distributor more concerned with maintaining the contract relationship. The impact of distribution channels on firm performance was studied by Lassar and Kerr [

29], who concluded that the greater the number of distributors in a geographic area, the greater the loss of control for the produce, and the higher the possibility of opportunistic behavior by distributors. On the other hand, Coelho et al. [

51] proved a positive relationship between the number of distribution channels and sales performance.

The last two factors, social capital (H1.5.), and internalized professional advice addressed though the question on whether the wine-producer employed an economist (H1.6.), were as indicators of the wine producer’s negotiating capacity. As with distribution, these two variables were intended to measure the bargaining power of the wine-producer.

Hypothesis 1.5 (H1.5). Social capital influences agency costs.

The relationship between social capital and agency theory was examined in the work of Beccera and Gupta [

52], who concluded that the lower the social capital (measured by trust), the higher the agency costs. According to Pospech and Spešna [

53], social capital, especially informal personal ties, has a positive influence on the economic performance of firms in the agricultural sector. In addition to these, there have been a number of other studies analyzing the relationship between social capital and firm performance [

54,

55,

56].

Hypothesis 1.6 (H1.6). Employing a specialist (economist) influences agency costs.

In the reviewed literature, we found that studies of human capital on firm development have been mainly conducted on samples including large companies (due to data availability), while Storey [

57] concluded that investing in specialized workforce in small firms is riskier and has a significantly lower expected return.

Our main hypothesis states that agency costs influence the performance of wine producers.

It was assumed that agency costs are borne by the wine producer. For previously mentioned reasons and because there was no available data estimation of their monetary value, we treated agency costs as a single entity. Their expected impact on performance was negative. The sub-hypotheses assumed that financial performance is measured through revenue per employee (H2.1.) and non-financial performance is measured through prizes won (H2.2.).

Hypothesis 2.1 (H2.1). Agency costs influence financial performance (revenue per employee).

Hypothesis 2.2 (H2.2). Agency costs influence non-financial performance (number of prizes won).

The literature connected to these hypothesis (primarily with H2.1.) includes the work of Wang [

30], who investigated the impact of agency costs on firm performance (that is, on stock return) and that of Cadot [

58], who investigated the impact of agency costs on the financial performance of firms, namely revenues.

{kind=link}