Influence of Perceived Risk of Blockchain Art Trading on User Attitude and Behavioral Intention

Department of Management Information System, National Chengchi University, Taipei 116302, Taiwan

*

Author to whom correspondence should be addressed.

Sustainability 2021, 13(23), 13470; https://doi.org/10.3390/su132313470

Submission received: 30 September 2021

/

Revised: 30 October 2021

/

Accepted: 2 December 2021

/

Published: 6 December 2021

(This article belongs to the Collection Digital Supply Chain and Sustainability)

Abstract

:In the first half of 2020, the average sales volume of gallery operators declined due to the COVID-19 pandemic and art galleries faced a crisis relating to their sustainable operation. However, crypto art finance, which combines online sales with blockchain, is attracting a considerable amount of attention. Can the use of blockchain solve the problems encountered in today’s art trading market? Is it considered acceptable by participants in the art trading market? What factors affect the behavioral intentions of blockchain technology users? In this study, we discussed the relationship between perceived risks and the three external variables of trust, government support, and auction house initiative, as well as their impacts on user attitudes and behavioral intentions regarding blockchain. The results of this study verified key factors that will help to increase the use of blockchain and solve existing market issues. It will also promote the sustainable operation and development of art enterprises and the market.

1. Introduction

Due to the COVID-19 pandemic, galleries were closed and art exhibitions were postponed or closed due to people going out less as a consequence of the pandemic, resulting in great losses. Nearly one third of museums in the United States may close permanently or face a financial crisis [1]. According to an Art Basel report [2], the average sales volume of gallery operators declined by 36% in the first half of 2020, but online sales rose significantly. Online sales have gradually become an important sales channel in the art market. In particular, the report pointed out that the use of the Bullish cryptocurrency has spread to the field of art. Blockchain technology opens up an innovative transaction model for the art market, helping art businesses to find means for sustainable growth during the pandemic.

Cryptocurrency originated with the invention of Bitcoin [3] at the end of 2008, and is now highly valued and widely applied by the market. Research and Markets [4] predicted that the global blockchain market will grow to be worth USD 39.7 billion by 2025, indicating that the application of blockchain is gradually expanding globally. According to the United Nations news [5], cryptocurrency and blockchain technology can help to combat climate change and promote a sustainable economy. Blockchain could accelerate efforts to address the climate crisis in three areas—namely, in terms of transparency, climate finance, and the clean energy market. Similarly, in the art market, the distributed ledger and smart contracts of blockchain can save paper consumed for the transaction of about 468,000 artworks per year [6]. As artworks in the traditional art market are generally screened through paper documents and receipts, the lack of appropriate record retention methods and verification standards makes it difficult to trace their sources, making auction fraud the biggest threat to the future development of the traditional business model [7]. Recent studies carried out based on the latest verified transaction methods for the Ethereum cryptocurrency show that the use of different methods for proof of stake can prevent forgery, reduce fraud, and reduce the energy cost of each transaction by 99.95% [5]. Wang et al. [1] proposed that the use of blockchain smart contracts and cryptography, together with digital watermarking technology and cloud services, can improve the digital copyright management of artworks. This combination will provide innovative, transparent, and secure transaction modes for the traditional art market and contribute to the sustainable development of the future art market.

In this study, the method of perceived risk (Jacoby and Kaplan [8]) was adopted to explore the user attitudes and behavioral intentions of participants using blockchain technology in Taiwan’s commercial art industry. This paper first collected articles from the literature related to blockchain technology and its perceived risks, including articles focusing on the online art market and the empirical browsing of how blockchain solves the pain points of the existing online art market. Then, the main research models were established, using perceived risk, user attitude, and behavioral intention, as well as the three external variables of trust, government support, and auction house initiative, to discuss the establishment of the hypotheses.

Taiwan’s art business participants and potential consumers were interviewed through a questionnaire survey, and the results regarding whether the research hypotheses and the structural model were valid were verified. This study summarizes the literature in related fields and creates a conceptual framework to identify important factors that are influenced by the perceived risk of blockchain art trading with regard to user attitude and behavioral intention. It is expected that the research results will lead to the enhancement of the use of blockchain in the art market and solve issues such as difficulties in traceability, authentication, and information opacity in the current market by utilizing the characteristics of this technology. This can help enterprises to transform to combat the impact of the pandemic, make artworks more valuable, and expand the scale of market participation. This technology could be beneficial to all participants in the art business industry and promote the sustainable development of art enterprises and the market.

2. Literature Review

2.1. Art Market

Griswold’s cultural diamond uses four endpoints to express the relationship between art and society: social world, producer, receiver, and cultural subject [9]. Alexander [10] further took dealers into account and found that entities with intermediary roles, such as galleries, art brokers, auction companies, and art critics, have a certain influence on the art market. Mark Lurie, the CEO of Codex, a blockchain startup in the art market, said in CoinCentral in 2018 that as the source information about art products has a low level of transparency, it is difficult to distinguish between real information and falsehoods when conducting research and investigation before entering the trading market. Over the years, it has proven hard to check the trading history records of global auction institutions, and sellers cannot easily share physical data such as documents about previous trading. At present, information integrity cannot be achieved in the art market [11]. Therefore, in the traditional trading market, it is extremely important to rely on the relevant information shared by auction companies and galleries.

In recent years, the art market has begun to adapt to the digital world. A huge online art trading forum has been developed. According to Hiscox’s 2019 Online Art Trading Report [12], as of 2018, the online art trading market had grown positively for five consecutive years. In 2020, the world was affected by the COVID-19 pandemic, causing the proportion of online sales to increase significantly. Among online buyers, frequent customers and new buyers each accounted for half. It can be seen from this that the collectors and buyers of artworks have gradually become accustomed to buying artworks online due to the pandemic. Gallery operators, who are limited by the constraints of physical store shopping, have had to change their business strategies and actively engage in online selling [2].

2.2. Blockchain

2.2.1. The Definition of Blockchain

The concept of blockchain originated from the research of Satoshi Nakamoto [3]. Blockchain is a public database based on the Internet and encryption technology; it has the characteristics of decentralization and distrust. Internet users are connected to each other as nodes, and each node continuously packages encrypted data into blocks, publishes the blocks to the network, and connects them in chronological order to generate permanent and irreversible data links [13]. Since the emergence of Bitcoin, the development of blockchain has gone through several different stages. The common points of division in this development [14] are the opening of the blockchain 1.0 era by the public chain Bitcoin, and the opening of the 2.0 era by the public chain Ethereum. In the 3.0 era, the application field of blockchain has extended beyond the financial industry to cover all levels of human social life.

2.2.2. Blockchain and Pain Points of the Art Market

According to the Hiscox report from 2020 [15], because of the pandemic, more than 72% of art lovers visited online sales platforms every week and millennial collectors (those born between 1982 and 2000) represented the largest consumer group in 2020. This generation tends to be more active online; millennials’ presence is growing rapidly and they invest more emotionally. Therefore, blockchain can provide services and reduce risks for this growing group of young artists [16]. These risks are reflected in the six common issues faced in today’s art market: (1) auction fraud; (2) difficulty in proving the origin and traceability of artworks; (3) difficulty in determining valuation; (4) privacy disclosure information; (5) the reluctance of artists to share the added value of artworks; and (6) intermediary and intermediate costs. The transparency, trust, and immutable ledger from blockchain can help this unsustainable industry to develop its business practices and drive social influencers to motivate consumers to engage in sustainable consumerism [17]. Therefore, in the following paragraphs we will describe in detail how blockchain can help art buyers to deal with the abovementioned issues and realize the sustainable operation and development of the market under the impact of the pandemic.

Yan Walther, chief of the Fine Arts Expert Institute (FAEI), said that more than 79% of the works of art examined by him were forged or not attributed to the correct artists, and speculated that the percentage of forged works of art in circulation in the market might reach as high as 50% [18]. The lack of proper record retention methods for art traceability causes issues 1 to 3. A blockchain cannot be deleted or modified, which allows it to be used as an ownership registration system. As a security layer implemented to prevent fraud, every verified digital trade has to be permanently viewed and protected [19]. Blockchain has been applied in the digital rights management of museums, and a combination of the Elliptic Curve Digital Signature Algorithm (ECDSA), blockchain, and smart contracts has been used to establish a sustainable mechanism for traceable cultural relic exhibition [1]. Another example of the practical application of this method includes the world’s first encryption art exhibition held by the State Russian Museum using the Verisart digital certificate [20]. The proof of ownership and transfer of Ascribe’s digital artwork were provided [21]. Additionally, Codex cooperated with LiveAuctioneers, which is a coalition of 5000 auction houses, to store trading-related documents in blockchain [22].

A total of 89% of online art consumers expect to search for or obtain comparable past trading price record information [23]. Regarding issue 3 (difficulty in determining valuation), consumers can easily obtain valuations from complete records left in the blockchain [22]. When trading in the existing encryption verification blockchain, traders do not have to disclose sensitive information such as their financial details [19], thus solving the problem of issue 4. Existing applications include Codex’s application of Biddable through blockchain technology, which allows sellers to prove the ownership of artworks without affecting their privacy. Regarding issue 5, artists cannot benefit from resale royalties. Whitaker and Kraussel [24] found that if artists could retain a 10% equity in their works during resale, the performance of this retained equity portfolio would be 986.8 times higher than that of the Standard & Poor’s 500 Index in the same period. As blockchain can record the price and number of artworks sold and provide accounting systems and automated provenance certification systems, artists can directly collect royalties after their works are sold [25].

Blockchain technology can create an interconnected platform for artists, and its information transparency enables buyers and sellers to independently verify the history of works of art, reduces the cost of intermediary expenses, and solves the problem of the intermediary costs referenced in issue 6 [26]. However, at present, large-scale art galleries, auction houses, and other intermediaries occupy a dominant position in the art business, and the blockchain infrastructure has not yet been completed, so there are still difficulties in implementation. In the future, when the infrastructure of blockchain is in place, a brand-new art service ecosystem will be built [11]. At present, the number of blockchain users is gradually increasing. Based on the research of Joo and Han [27] from 2021, the distributed trust of blockchain can enhance users’ trust and satisfaction in the area of the food supply chain for sustainable business. The smart contract supported by blockchain will contribute to the development of sustainability in the art market [28].

2.3. Perceived Risk and Influencing Factors

Dowling and Staelin [29] defined perceived risk as the possibility of perceived uncertainty and adverse results when consumers purchase products or services, which can also be said to be a subjective expected loss [30]. Perceived risk theory was first extended from the psychological concept of Bauer [31], who held that consumers may experience uncertainty before purchasing a product because they cannot predict whether the result is correct or not. In 1972, Jacoby and Kaplan [8] put forward five risk dimensions: financial risk, performance risk, physical risk, psychological risk, and social risk. These dimensions can explain 61.5% of the variance of overall risk. Kotler [32] argued that perceived risk significantly affects consumers’ purchasing decisions. Today, perceived risk is widely used as one of the indexes for measuring consumers’ purchasing intentions when enterprises formulate marketing strategies.

According to the 2018 Online Art Consumption Trend Report [23], 76% of buyers are hesitant to make online purchases and 70% are worried that the works of art they receive will differ from their description, as they cannot inspect the artworks in person. Vinhal Nepomuceno et al. [33] stated that intangible services usually cause customers to perceive higher levels of risk. The creation of new technologies can bring benefits, but also may create privacy problems and confidential data protection problems, causing the potential adopters of innovative technologies to feel at risk. Ram [34] proposed the concept of innovation resistance, in which consumers may refuse to adopt new technologies because they are worried that their existing habits or levels of satisfaction will be changed. Later, scholars proposed that perceived risk is the main reason why consumers resist adopting new technologies [35]. From the above, we can see the importance of perceived risk in the online trading market. Therefore, this section will further discuss the literature relating to the factors influenced by the perceived risk of blockchain art trading with regard to user attitude and behavioral intention.

2.3.1. Trust

Zand [36] pointed out that when social exchange behavior is uncertain, trust will reduce the participants’ fear of exploitation. Perceived integrity refers to the bidder’s honesty and their trust in the seller (and intermediary) to abide by mutually agreed-upon rules [37]. Trust can be driven by the functional [38], hedonic [39], and social [40] attributes of a technology. Van Pinxteren et al. [41] considered that the level of anthropomorphism is also an important driver of trust. Shi et al. [42] divided trust into cognitive trust and emotional trust, and suggested that emotional trust has a greater impact on technology adoption than cognitive trust. From this, we can see the relationships among perceived risk, trust, and technology adoption intentions.

2.3.2. Intermediary

In addition, it is not easy to guarantee whether there are forgeries of art in the existing art market; as the appraisal of works of art depends on professional knowledge and experience, almost all auctioneers and art clients declare that they will not bear the responsibility of forgeries before auction. The honest brand effect of an intermediary can strengthen consumers’ trust in sellers (known as institutional trust), which will reduce the level of risk consumers perceive to be associated with Internet trading [43]. Therefore, the auction house initiative is also included in the influencing factor of perceived risk.

Antwi et al. [44] noted that trust is divided into intermediary trust and seller trust in online shopping. Intermediary trust means that a person believes that a third party will act loyally in accordance with the agreed-upon terms [45]. There have been many studies on the influence of intermediaries [46,47]. Al-Swidi et al. [48] confirmed that social influence, e-government awareness, and trust in intermediary institutions are the key factors that affect users’ intention to use e-government services, and that the trust placed in intermediary institutions moderates the influence of society on the intention to use e-government services.

2.3.3. Government Support

The structural assurances proposed by Gefen et al. [49] show that people are made to feel safe by governments’ security policies or measures. For consumers, structural assurance is a safety system that includes assurance, stipulation, promises, and legal recourse [50]. Structural assurance can improve the credibility of suppliers or new technologies [51], and it is also an important indicator that can be used to predict the perceived credibility of network suppliers [49]. Therefore, it can be determined that the government’s security policy in its structural guarantee can influence consumers’ decisions. The National Legislative Council reduced the equity risk caused by consumers’ use of new technologies and then increased their willingness to use innovative technologies.

Although it has been found that political connections have a positive effect on the number of enterprise innovations taking place, they have a negative effect on the quality of innovation and can even reduce the research and development (R&D) intensity of enterprises. However, the government can make up for this partly through implementing measures to stimulate the quality of enterprise innovation, such as intellectual property protection, and anti-corruption policies [52]. Another study by Liu et al. [53] concerning government R&D subsidies indicated that ex-ante grants have a greater effect on innovation performance than ex-post rewards. Tina et al. [54] pointed out that venture capital (VC) plays an important role in promoting enterprise technological innovation. Chatterjee et al. [55] further found that government support can enhance users’ intention to apply the technology of education during a vocation. Based on the above research, it can be seen that conditional government support is able to increase enterprises’ level of technological innovation and the intentions of individuals to use technology.

3. Research Method

3.1. Research Process Design

This study was designed according to the procedure of Sekaran and Bougie [56] and included the following nine points: (1) purpose; (2) research and analysis unit; (3) types of questions and observation methods; (4) sampling design; (5) study interference; (6) time range; (7) research setting; (8) data analysis methods; and (9) analysis of research data. The purpose of this study was to design a first-stage research model with the definitions of perceived risk and external variables so as to test the factors that affect the attitudes and behavioral intentions of blockchain technology users in the art market and their relationships, with a view to providing a strategic benefit reference for the decision support of participants in Taiwan’s commercial art industry in the future. Individual participants in Taiwan’s commercial art industry were taken as the research and analysis subjects. This study mainly adopted narrative and causal research methods, and observed whether they could contribute to the decision support of senior executives in Taiwanese enterprises. A questionnaire survey was conducted with potential community members who preferred blockchain use in online shopping as the sample matrix. Before filling out each questionnaire, a presentation lasting fifteen minutes was given to explain the purpose of the questionnaire in detail. This study adopted a horizontal dimension time range. Before the formal implementation of the research, a pre-test was conducted in the first stage to collect the research questionnaire topics related to competitive intelligence published by famous journal scholars. In the second stage, a pilot test was carried out to test for problems concerning various aspects of the questionnaire, which helped us to improve the reliability of the questionnaire design. The research data analysis included reliability and validity analyses, a confirmatory factor analysis, a questionnaire narrative analysis, and a demographic survey analysis, as well as a structural equation model path analysis and hypothesis testing.

3.2. Definition of Dimensions

Through the above literature discussion, we found that perceived risk has an impact on the use of blockchain technology. Therefore, this study intended to explore the attitudes and behavioral intentions of participants in Taiwan’s commercial art industry to apply blockchain technology with perceived risk. According to the previous points mentioned in Section 2.3.2 above, in the development process of innovative technologies, the trust of users and the support of the government have impacts on the adoption of new technologies, including blockchain technologies. On the other hand, in the abovementioned literature and practice, auction house initiatives also have a certain influence on the art market. Based on the above factors, this study added three external variables—trust, government support, and auction house initiative—to the model of perceived risk affecting user attitudes and behavioral intentions. The variables discussed in this study are listed in Table 1 and are defined one by one according to the previous literature.

3.3. Research Hypotheses and Structures

In the previous section, the variables of each dimension of this study were proposed, the relationship between the dimensions was discussed, and reasonable hypotheses were put forward to construct the research model.

As mentioned above, some scholars have found that when fakes appear in the market, the owners of genuine products are more likely to seek well-known and credible auction houses to sell their artworks [62]. Bajari and Hortaçsu [63] also observed that the same goods are more likely to encounter fraud online than offline; therefore, online consumers are more willing to seek a reliable auction platform, which could then launch an evaluation and feedback mechanism to help increase its trading volume. Kambil and Van Heck [57] introduced innovative technology to the Dutch flower auction market, which solved the problem of the risk of sellers and buyers not having enough information to make real-time and correct decisions, and increased the sales volume in the auction market. Based on the above, this study aimed to further understand the relationship between perceived risk and auction house initiative to use blockchain in art trading; therefore, the following hypothesis was put forward:

Hypothesis 1 (H1).

Perceived risk has a positive impact on auction house initiatives.

The information asymmetry in online auctions is more serious and can cause stakeholders to bear higher levels of risk [63]. If people lack the necessary knowledge to assess dangerous risks, trust can become an important clue about who to trust. At this point, people will seek to rely on experts, government agencies, or other sources to interpret information for them [64]. Therefore, perceived risk is an important driving factor in people accepting the control measures implemented by the government and taking more preventive actions [65]. In the research of Gerber and Neeley [66] on perceived risk and citizens’ preference for the governmental management of daily hazards, it was found that citizens will use perceived risk rationally—the greater the perceived risk is, the more active citizens will be in supporting the governmental management of potential hazards. This coping relationship holds even if the policy options that respondents are asked to consider burden the public with significant costs. Based on this study, the following hypothesis was proposed:

Hypothesis 2 (H2).

Perceived risk has a positive impact on government support.

The COVID-19 pandemic spread across the world in 2020. As many offline activities almost stopped during this period, Christie’s and Sotheby’s online sales greatly increased. Since this time, the openness, transparency, and security of auction trading have received increasing attention. Blockchain is a technology that can improve the transparency, traceability, and security of product trading [67]. Clohessy et al. [68] asserted that blockchain will be widely used in finance, health, and even government industries in the future. It seems to be a solution to the risks brought about by auction digitalization. In addition, when users use information systems to transfer the ownership of money, goods, and information, if they can pass through an impartial third party, they can enhance their willingness to perform a transfer [69]. However, the mechanism, platform, and technology established by the third party can be supported by the government, which may affect the user’s willingness to accept it [70]. Therefore, this study puts forward the following hypothesis:

Hypothesis 3 (H3).

Auction house initiatives have a positive impact on government support.

In the world of the virtual network, it is quite difficult to gain mutual trust between people. Shneiderman [71] stated that making privacy and security enforcement policies easy to find and read through third-party certification can enhance consumer trust. Gefen et al. [49] proposed that people will gain a sense of security from guarantees and security measures, and that such security measures may come from government laws. There are also studies on factors concerning the application of blockchain technology to the logistics industry, and it is considered that government policies and support have an impact on technology development and users’ trust in technology [58]. In terms of financial technology, the regulatory sandbox established by the Financial Conduct Authority in 2015 [72] has achieved remarkable results. The UK Government Chief Science Adviser mentioned in a report [73] that the government must play the roles of leader and catalyst in order to establish a clear vision, coupled with implementing stable policies concerning the environment, to encourage the private sector to invest in financial technology. Based on the above literature, this study put forward the following hypothesis:

Hypothesis 4 (H4).

Government support has a positive impact on trust.

In the past, it was pointed out that the perceived security of users comes from personal subjective feelings, which will affect trust and satisfaction. The authors of [74] found that perceived risk is negatively correlated with consumer trust. The research of Kambil and Van Heck [57] showed that the introduction of information systems by auction houses can quickly provide information to relevant stakeholders (such as sellers and buyers), enable them to take appropriate responses in real time, reduce the uncertainty of trading, and increase trust. In addition, Shin [75] suggested that trust is one of the important factors in using blockchain services. Therefore, this study deemed it necessary to test the influence of perceived risk on trust when using blockchain technology and put forward the following hypothesis:

Hypothesis 5 (H5).

Perceived risk has a negative relationship with trust.

Salam et al. [43] indicated that the buyer and the intermediary will influence each other, and that the brand strength of the intermediary will also affect the buyer’s trust in the seller. Buyers believe that intermediaries will protect users, offer a secure and stable environment, and guarantee problem-free trading [76]. Zucker [77] held that the independent activities of buyers and sellers can be combined by trusted third parties, which is called institutional trust. Hong and Cho [78] found that consumers’ trust in intermediaries will affect their loyalty and purchase intention, and that trust can even be transferred to sellers through intermediaries, which means that the credibility of intermediaries plays a key role in determining the degree of consumer trust and the acceptance of sellers in electronic markets. Therefore, this study inferred that the ability, behavior, reputation, and rules of auction houses and auction platforms, as third parties in the trading process, will affect the intentions of sellers and buyers to participate in the auction. The following hypothesis was put forward:

Hypothesis 6 (H6).

Auction house initiatives have a positive impact on user attitudes.

As for online reverse auctions, Kuo et al. [79] indicated that there are two kinds of auction methods: open bidding and sealed bidding. When the seller recognizes the security of the bidding process, they will not create difficulties for the auction process and results, making the auction trading process smoother. However, the development of a network is not a panacea. When privacy issues are involved, the information that websites can collect may be limited, and it may be impossible to provide users with more complete information [80]. For example, a price comparison website may only provide the prices of operators who put advertisements on their website. When users find this, it is possible to change their attitude towards the website, as user attitudes change with the level of trust in IT systems [81]. Therefore, this study inferred that when users use blockchain in art trading, their trust has an impact on their attitudes. The following hypothesis was put forward:

Hypothesis 7 (H7).

Trust has a positive impact on user attitudes.

Trust is a subjective belief and its influence on behavioral intention is positive [82]. Trust can reduce the fear of buyers and sellers when trading behavior is highly uncertain [36]. Beltrametti and Marrone [83] found that the auction market for ancient cultural relics is highly complex, and that when cultural relics are judged or certified by the court, buyers will be willing to pay a higher price. Studies on online auctions have also suggested that if the auction platform can hide and protect the information of bidders, their willingness to bid will increase and the bidding will become more intense [79]. Moreover, Latif and Zakaria’s [84] research on the use of blockchain technology by public institutions showed that trust has a significant positive impact on use intentions. However, Wong et al. [85] explored the application of blockchain technology in supply chain management and found that trust has no significant effect on intention of use behavior. This study attempted to understand the relationship between trust and behavioral intention when applying blockchain technology in art trading. Therefore, the following hypothesis was put forward:

Hypothesis 8 (H8).

Trust has a positive impact on behavioral intention.

Moon and Kim [86] found that in a study of users’ acceptance of a network in the network context, users’ attitudes will affect their intention to engage in continuous use. Users’ intention to adopt a technology is mainly determined by their satisfaction with the previous experience of the system [87,88]. According to the above related research, this study put forward the following hypothesis:

Hypothesis 9 (H9).

User attitude has a positive impact on behavioral intention.

Through a literature discussion, this study identified various dimension variables, put forward research hypotheses, and constructed a research model, as Figure 1 shows.

3.4. Data Collection and Questionnaire Design

The purpose of this paper was to explore the practical application of blockchain in art trading and to explore the measurement of the intention of applying blockchain technology in Taiwan’s commercial art industry. In addition to the literature review, a questionnaire was presented to interview 15 art trading practitioners in Taiwan. The original questionnaire items were divided into three parts. The first part was a survey of the participants’ basic data and had a total of 10 items, including gender, age, occupation, education level, familiarity with e-commerce, familiarity with blockchain, experience in purchasing art, and acceptable prices. The second part measured user attitude and behavioral intention and included two subsections with nine items. Items 1 to 7 focused on user attitude, and items 8 and 9 focused on behavioral intention. The third part was a survey of the external variables and included 4 subsections with 10 items. The first to third items focused on trust, the fourth to fifth items focused on trust in the auction house initiative, the sixth to seventh items focused on perceived risk, and the eighth to tenth items focused on government support. At the same time, Rickett’s five-point scale was used to represent the degree of agreement with the questions, with answers rated from “Strongly Agree” to “Agree”, “Neutral”, “Disagree”, and “Strongly Disagree”.

The original questionnaire was modified from the standard scale, then the original 15 experts engaged in art trading in this field were invited to conduct a pilot test to verify whether the content of the test questionnaire met the research purpose and whether the suitability of the auction house initiative, government support, and trust was related to perceived risks. Next, a pretest was conducted to verify whether the words used in the test questionnaire items were appropriate and whether any items should be added or deleted.

3.5. Data Analysis Methods

In this study, SPSS 18.0 and AMOS 18.0 were used to analyze the data of the questionnaires. After the questionnaires were collected and invalid responses were deleted, a statistical analysis was carried out, followed by basic narrative statistics, item analysis, confirmatory factor analysis, reliability and validity, and the verification of the structural equation modeling (SEM). The basic data analysis was divided into two parts: questionnaire collection and basic narrative statistics. The questionnaire recovery included the number of questionnaires after recovery, as well as descriptions of the valid samples in order to understand the questionnaire distribution and recovery situation. The basic narrative statistics included items on gender, educational background, age, and occupation, and were used to understand the basic information of the subjects.

4. Results and Discussion

4.1. Basic Narrative Statistics

The main subjects of this study were the potential users of blockchain, so this study distributed questionnaires to these individuals. From 1 March to 10 June 2020, a total of 946 questionnaires were collected; however, 274 questionnaires were deleted after removing unqualified responses (such as those from individuals who were completely unfamiliar with blockchain), responses with repeated answers (such as checking the same answer for the whole questionnaire), and outliers. Finally, the actual valid sample was 672 and the valid questionnaire rate was 71%.

In terms of the gender distribution of the subjects, there were 366 males (54.5%) and 306 females (45.5%). Regarding educational background, 277 (41.2%) had a Bachelor’s degree, 150 (22.3%) had a Master’s degree or above, 150 (22.3%) had a baccalaureate degree, and 95 (14.1%) had a diploma from schools below a college. Regarding the age distribution, 225 people were aged 47–56 (33.5%), followed by 165 people aged 36–46 (24.6%). For the occupational distribution, because the questionnaire was distributed to the general public, the occupational distribution was quite scattered, showing that the sampling was uniform and without concentration. As for the occupational categories, the number of subjects engaged in the service industry was 157 (23.4%), followed by 90 subjects in financial insurance (14.4%) and 60 subjects in traditional manufacturing (8.9%).

Regarding the familiarity of the subjects with the application of blockchain, because the application of blockchain has not been fully popularized, only 78 (11.6%) of the respondents had been exposed to the use of blockchain, followed by 459 (68.3%) who knew a little about it but had never used it, and 135 (20.1%) who knew about it but had never used it. The subjects’ self-admission of their familiarity with e-commerce networks (online shopping) showed that, because the use of blockchain is highly related to the network environment, potential users need experience in network use. In this study, online shopping was used as an alternative variable for familiarity with the network environment. According to the interview sample, only 24 subjects (3.6%) had no online shopping experience, while 450 subjects (66.9%) had moderate participation (buying once a month, on average) or high participation (buying more than once every two weeks, on average). There were 182 people (27.1%) who browsed online shopping (but did not buy anything) and 16 people (2.4%) who did not buy items regularly.

4.2. Hypothesis and Model Validation

4.2.1. Dimension Reliability

In this study, Cronbach’s α coefficient [89], which is the most commonly used reliability test, was used to test whether the internal consistency of each part of the questionnaire was achieved. Generally speaking, a Cronbach’s α higher than 0.7 is considered to have high reliability, while a value of 0.6 is accepted in exploratory studies. If Cronbach’s α is lower than 0.35, it is regarded as low reliability and should be rejected [90]. After the expert pilot test, in order to modify the original questionnaire and make the test scale consistent, 50 financial practitioners conducted pre-test and reliability analyses. The results of the reliability analysis are listed in Table 2. The Cronbach’s α values for each dimension and the whole model were all greater than 0.7, showing a high reliability. The content of this questionnaire was based on theory combined with the characteristics of Taiwanese online shopping, and the expert test and pre-test revealed it to have considerable content validity.

4.2.2. Correlation Analysis to Verify Construction Validity

Fornell and Larcker [91] suggested that construction validity should be measured using the composite reliability (CR) and average variance extracted (AVE). In general, the composite reliability must be greater than 0.6, and the higher this value is, the higher the internal consistency is. Hair et al. [92] stated that the CR must be greater than 0.7. The AVE is used to calculate the variable interpretation ability of potential variables for each measurement item. The higher the AVE, the higher the reliability and convergence efficiency of the potential variables. Generally speaking, an AVE value greater than 0.5 is preferred.

After analysis and verification, all of the items were between 0.7914 and 0.934, which was higher than that of Hair et al. [92]. The reliability of composition was 0.863–0.939 and higher than 0.7, indicating a high level of internal consistency. The AVE value was 0.675–0.838, which was higher than 0.5, and the explanatory power and convergence validity were both acceptable. X2/d.f. was 3.646 and within the standard value of 5. GFI and AGFI were 0.921 and 0.891, which were greater than the standard value of 0.8. CFI and RFI were also in line with the standard value, at 0.968 and 0.946, respectively, and were greater than 0.9. The results of the abovementioned mode adaptability pointer showed a good goodness of fit.

According to the two criteria proposed by Gaski and Nevin [93], the correlation coefficient between the two dimensions should be less than 1 and should be smaller than the Cronbach’s α reliability coefficient, which indicates that the two dimensions have distinguishing validity. According to Fornell and Larcker [91], if the correlation coefficient of two dimensions is less than the square root of AVE, this means that these two dimensions have distinguishing validity. In this study, SPSS was used to analyze the correlation coefficient matrix of each measurement variable. The dimensions all met the above three criteria for testing the differential validity, indicating that the differential validity of the dimensions was good (Table 3).

4.2.3. Model Path Analysis

In this study, structural equation modeling was used to measure the research framework and test the research hypothesis, and the measurement model mainly established the relationship between the measurement pointers and the potential variables. After the data reliability and validity tests and the statistical basic hypothesis tests, this study used AMOS 18.0 to examine the path relationships among perceived risk, trust, government support, auction house initiative, user attitude, and behavioral intention.

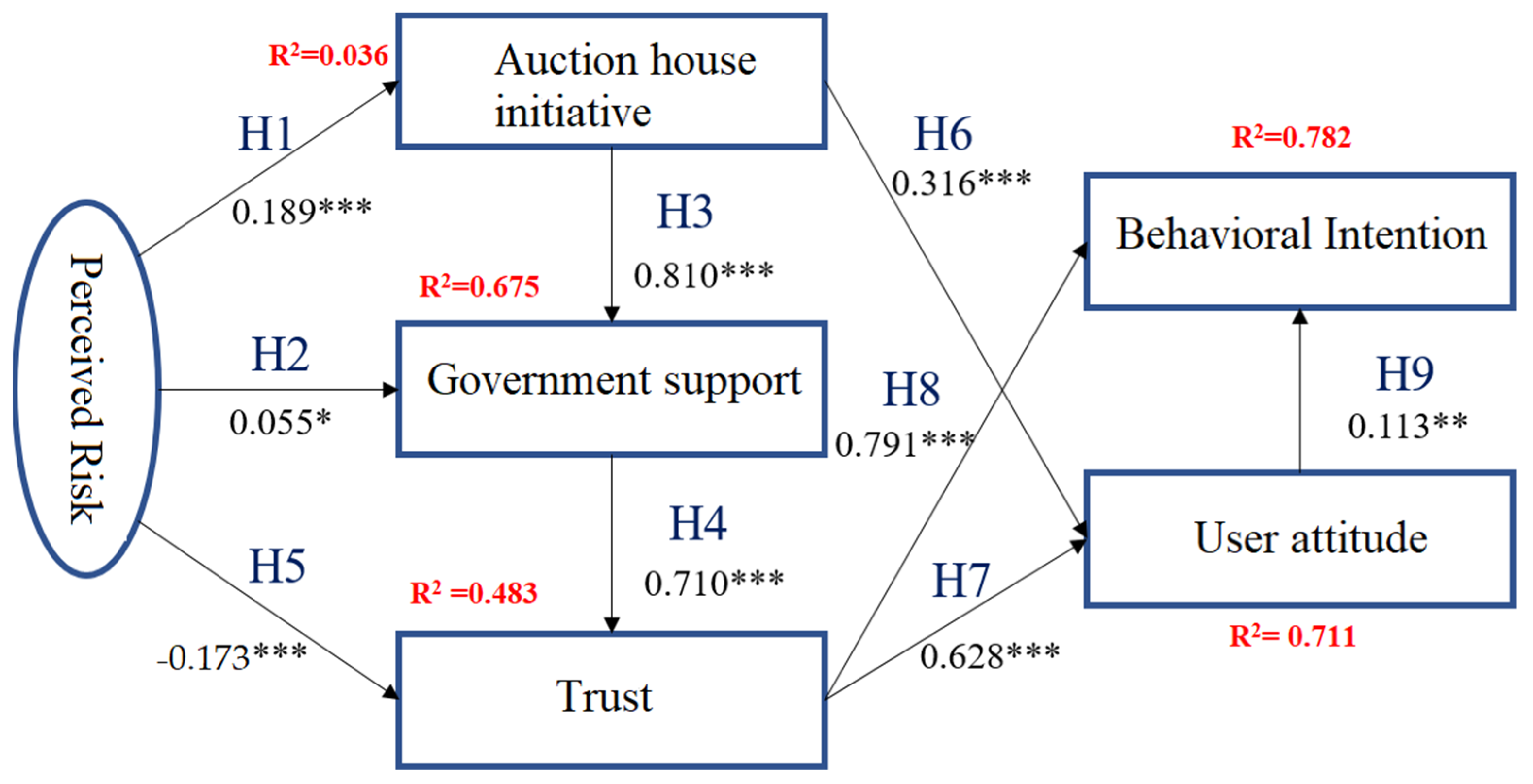

In this study pattern, all pathways from H1 to H9 reached significant levels (as shown in Figure 2 and Table 4). The auction house showed a moderate R2 of 0.036, indicating that the perceived risk could be promoted by the auction house with a moderate variance of 3.6%. The R2 of GSM was 0.675, showing that perceived risk and auction house initiative could explain 67.5% of the variance of GSM. The R2 of trust was 0.483, showing that government support and perceived risk could explain 48.3% of the variance of trust matching. The R2 of user attitude was 0.711, indicating that auction house initiative and trust could explain 71.1% of the variance of trust. The R2 of behavioral intention was 0.782, showing that user attitude and trust could explain behavioral intention with a variance of 78.2%.

Table 4 lists the value of each path coefficient estimated using the maximum likelihood method. It can be seen that the direct effect path of perceived risk on the auction house initiative reached a significance level of p < 0.001. The non-standardized coefficient was 4.659 and the estimated standard error was 0.045. The direct effect path of perceived risk on government support reached a significance level of p < 0.05, with a non-standardization coefficient of 2.038 and an estimated standard error of 0.039. The direct effect path of auction house initiative to government support reached a significance level of p < 0.001, with a non-standardization coefficient of 21.548 and an estimated standard error of 0.031. The direct effect path of government support on trust reached a significance level of p < 0.001, with a non-standardization coefficient of 18.770 and an estimated standard error of 0.038. The direct effect path of perceived risk on government support reached a significance level of p < 0.001. The non-standardization coefficient was −5.486, and the estimated standard error was 0.036. The direct effect path of auction house initiative on user attitude reached a significance level of p < 0.001, with a non-standardization coefficient of 9.067 and an estimated standard error of 0.036. The direct effect path of trust on user attitude reached a significance level of p < 0.001. The non-standardization coefficient was 15.873 and the estimated standard error was 0.039. The direct effect path of user attitude on behavioral intention reached a significance level of p < 0.001. The non-standardization coefficient was 14.656 and the estimated standard error was 0.059. The direct effect path of behavioral intention on trust reached a significance level of p < 0.05. The non-standardization coefficient was 2.421 and the estimated standard error was 0.051, which also met the standard, indicating that this model met the adaptive standard.

There were nine hypotheses in this study, as summarized in Table 5 according to the verification results gained from the above statistical analysis.

4.2.4. Results and Discussion

After analyzing the model path through the structural equation model, this study explained and put forward a discussion and views on the model path. The analysis results and discussions of each path are shown below.

1. Perceived risk has a positive impact on the auction house’s desire to use blockchain technology in art trading.

According to H1, the results of this study held true (a path standardization coefficient of 0.189, p < 0.001), indicating that the higher the users perceive the level of risk of using blockchain technology in art trading to be, the more auction houses need to advocate for the use of blockchain technology in art trading. Auction houses advocate that blockchain technology should be applied to art trading to reduce the risk of personal information abuse and financial money loss that consumers may face through blockchain, which can then affect user attitudes and behavioral intentions.

2. Perceived risk has a positive impact on the government-supported use of blockchain in art trading.

According to H2, the results of this study held true (a path standardization coefficient of 0.055, p < 0.05), indicating that the higher the users perceive the level of risk of using blockchain technology in art trading to be, the more government support for the use of blockchain technology in art trading is needed. The results of this study were the same as those found in previous research [49,50,51,70]. Government-supported security policy measures, guarantees, regulations, commitments, and legal recourse are important means to increase the perceived credibility of new technologies.

3. Auction house initiative has a positive impact on the government’s support for the use of blockchain technology in art trading.

According to H3, the results of this study held true (a path standardization coefficient of 0.810, p < 0.001), indicating that when auction houses propose the use of blockchain technology in art trading, the government is more likely to support the wide application of this technology in art trading. This result shows that auction houses have a great influence in the art market and that auction house initiatives can prompt government units to show their support for the use of blockchain technology in art trading.

4. The government’s support for the use of blockchain technology in art trading has a positive impact on consumer trust.

According to H4, the results of this study held true (a path standardization coefficient of 0.710, p < 0.001). This result was the same as that found in previous research [58]. The government’s support of the application of blockchain technology can significantly improve users’ perceptions of the trustworthiness of this technology, increase the trust of art traders in blockchain technology, and positively affect users’ attitudes and buyers’ (consumers’) behavioral intentions.

5. Perceived risk has a negative relationship with consumers’ trust in the use of blockchain technology in art trading.

According to H5, the results of this study held true (a path standardization coefficient of −0.713, p < 0.001), showing that when participants use blockchain technology in art trading, the degree of perceived risk will affect their trust in blockchain technology as well as affecting user attitudes and behavioral intentions. This result was consistent with that of previous research [75].

6. Auction house initiative has a positive impact on consumers’ attitudes towards the use of blockchain technology in art trading.

According to H6, the results of this study held true (a path standardization coefficient of 0.316, p < 0.001). This study also found that auction house initiatives play a key role in consumers’ acceptance of blockchain technology and have a positive impact on consumers’ behavioral intentions by enhancing the impact on user attitudes.

7. Consumers’ trust in the application of blockchain technology in art trading has a positive impact on user attitudes.

According to H7, the results of this study held true (a path standardization coefficient of 0.628, p < 0.001). This result also pointed out that users’ trust in blockchain technology will not only affect users’ attitudes, but will also directly affect users’ behavioral intentions. The privacy protection of blockchain technology can reduce perceived risks, directly affect user attitudes on the basis of trust, and increase consumers’ continuous use of blockchain technology for art trading.

8. Consumers’ trust in the use of blockchain technology in art trading has a positive impact on consumers’ behavioral intentions.

According to H8, the results of this study held true (a path standardization coefficient of 0.113, p < 0.05). These results were the same as the results of previous research [82,84].

9. User attitudes towards the application of blockchain technology in art trading have a positive impact on consumers’ behavioral intentions.

5. Conclusions

According to the literature collection and analysis carried out in this study, blockchain technology has been widely used in the supply chain management of many industries and can improve its efficiency. The data traceability and transparency of blockchain technology are helpful to art trading management, and can help to solve the issue of distinguishing authenticity or quality defects in today’s online art trading market. Based on perceived risk, which affects consumers’ acceptance of new technologies, this study took perceived risk as its theoretical framework and added the three variables of auction house initiative, government support, and trust to deduce nine hypotheses.

This study further distributed questionnaires to potential users of blockchain technology, gaining 672 valid responses. AMOS 18.0 was used to test the path relationships among perceived risk, trust, government support, auction house initiative, user attitude, and behavioral intention. The results showed that H1–H9 were valid. The only negative relationship found was H5 (perceived risk has a negative relationship with consumers’ trust in the use of blockchain technology in art trading), which was consistent with the results of previous research. The rest had positive relationships, including H3 (auction house initiative has a positive impact on the government’s support for the use of blockchain technology for art trading) and H6 (auction house initiative has a positive impact on consumers’ attitudes toward the use of blockchain technology in art trading). According to the past literature, the use of auction houses and the government as an intermediary third party can enhance consumers’ trust and reduce their perception of risks. Therefore, when people are dealing with high-risk artwork, they will actively seek to obtain guarantees from auction houses and the government; meanwhile, their willingness to seek auction house initiatives is higher than government support, which shows that in today’s online art market, as carrying out art appraisals relies on professional knowledge and prior experience, users still rely on and trust honest and reliable auction houses. Consistent with the results of previous studies, we found that trust has a positive impact on user attitudes and behavioral intentions. It was particularly noteworthy that the auction house initiative has a positive impact on user attitudes and government support. This result verified the research of Salam et al. [43]. The brand effect of the intermediary will directly strengthen consumers’ trust in sellers, help to develop institutional trust, and reduce consumers’ perceived risk level. This study found that auction houses will play a key role in the promotion of the use of blockchain, user attitudes, and behavioral intentions in the future.

5.1. Implications and Contribution

The above research results contribute to the literature as follows. (1) Operators can be enabled to master the key factors of blockchain introduction, reduce risks and losses during adaptation, and accelerate the integration of blockchain technology. (2) The issues that need to be solved in the existing art market need to be mitigated in order to assist enterprises in undergoing transformations and achieving sustainable operations during the pandemic. (3) The constructed research model could help to make art market trading more transparent and secure, thus expanding the scale of market participation, increasing the value of art, and accelerating market circulation and sustainable development. (4) These findings could facilitate the permanent preservation of artwork ownership certification, reduce the consumption of paper in art market transactions, and reduce environmental pollution. (5) There is no explanatory power regarding the previously stated perceived risk concerning users’ willingness to accept blockchain technology [94,95]. This study pointed out that the initiative of auction houses and governmental support are the key pre-factors affecting consumers’ trust in blockchain technology, and have a significant impact on reducing consumers’ perceptions of risk. These factors not only successfully make up for the deficiencies of previous studies, but also enable the more complete application of blockchain technology in art transactions.

5.2. Research Limitations and Future Studies

One limitation of this study is that, except for 15 art trading experts, the questionnaire was distributed to the general public, as potential users of blockchain technology. Therefore, the distribution of the occupations of our subjects was quite scattered. Not all of the respondents had experience in art trading or in real blockchain use. Additionally, the questionnaires were distributed in Taiwan, and the ecological environment of the art market varies from country to country. Future studies should consider different countries and age groups, or use a population with actual experience in blockchain as subjects in order to increase the breadth and depth of our knowledge in this field and make it more comprehensive.

In terms of variables, since this study mainly discussed the variables affecting the use of blockchain technology from the perspective of society and enterprises, it is suggested that future models should include the two variables of perceived ease of use and perceived usefulness outlined in the Technology Acceptance Model (TAM), as well as exploring the topic from the perspective of individuals. In addition, the COVID-19 pandemic has led to uncertainty concerning economic policies (GEPU) in many countries, and enterprises are thus facing higher business risks [96]. Whether this will prompt enterprises to become conservative in their budgets allocated to technology investment or try to invest in cost-saving new technologies is another topic that is worthy of further study in the future. In addition to gold capital increasing with hedging risk [97], Bitcoin investment has also climbed. Due to the complementary relationship between Bitcoin and gold [98] and the tendency toward safe investment during the pandemic period [99], Bitcoin, which is owned in a digital wallet, has become a popular choice among diversified asset portfolios, thereby greatly enhancing the willingness of consumers to use blockchain technology. Therefore, economic policy uncertainties caused by the pandemic may also be one of the variables influencing the use of blockchain technology. Further research should aim to explore this topic in the future.

Author Contributions

Conceptualization, P.-H.L. and Y.-P.C.; methodology, P.-H.L. and Y.-P.C.; validation, P.-H.L.; formal analysis, P.-H.L.; investigation, P.-H.L.; resources, P.-H.L.; data correction, P.-H.L. and Y.-P.C.; writing—original draft preparation, P.-H.L. and Y.-P.C.; writing—review and editing, P.-H.L. and Y.-P.C.; visualization, P.-H.L.; supervision, Y.-P.C. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Not applicable.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Wang, Y.C.; Chen, C.L.; Deng, Y.-Y. Museum-authorization of digital rights: A sustainable and traceable cultural relics exhibition mechanism. Sustainability 2021, 13, 2046. [Google Scholar] [CrossRef]

- Art/Basel. The Impact of Covid-19 on the Gallery Sector. Press Release Basel 2020. Available online: https://d2u3kfwd92fzu7.cloudfront.net/The%20Impact%20of%20COVID-19%20Survey_Press%20Release-2.pdf (accessed on 14 July 2021).

- Nakamoto, S. Bitcoin: A Peer-to-Peer Electronic Cash System. Bitcoin Org. 2008. Available online: https://bitcoin.org/bitcoin.pdf (accessed on 13 July 2021).

- Research and Markets. Blockchain Market (Global Forecast to 2025) 2020. Available online: https://www.researchandmarkets.com/reports/5025113/blockchain-market-by-component-platform-and?w=4&utm_source=BW&utm_medium=PressRelease&utm_code=zgncsk (accessed on 13 July 2021).

- Sustainability Solution or Climate Calamity? The Dangers and Promise of Cryptocurrency Technology, United Nations News. Available online: https://news.un.org/en/story/2021/06/1094362 (accessed on 26 October 2021).

- Artprice. The Art Market in 2020. Available online: https://imgpublic.artprice.com/pdf/zh-the-art-market-in-2020.pdf (accessed on 13 October 2021).

- Grazioli, S.; Jarvenpaa, S.L. Perils of internet fraud: An empirical investigation of deception and trust with experienced Internet consumers. IEEE Trans. Syst. Man Cybern. A Syst. Hum. 2000, 30, 395–410. [Google Scholar] [CrossRef] [Green Version]

- Jacoby, J.; Kaplan, L.B. The components of perceived risk. In Proceedings of the Third Annual Conference of the Association for Consumer Research, Chicago, IL, USA, 3–5 November 1972. [Google Scholar]

- Griswold, W. Cultures and Societies in a Changing World, 2nd ed.; Sage Publications: California, CA, USA, 2004; pp. 154–196. [Google Scholar]

- Alexander, V.D. Sociology of the Arts Exploring Fine and Popular Forms; Wiley-Blackwell: New Jersey, NJ, USA, 2020; pp. 1–388. [Google Scholar]

- Buchko, C. Codex CEO Mark Lurie Talks Ethereal and the Future of Blockchain Art. Conin Central. 2018. Available online: https://coincentral.com/codex-ceo-mark-lurie-interview/ (accessed on 24 July 2021).

- Hiscox. Hiscox Online Art Trading Report 2019. Available online: https://www.hiscox.co.uk/sites/uk/files/documents/2019-04/hiscox-online-art-trading-report-2019.pdf (accessed on 14 July 2021).

- Kandaswamy, R.; Furlonger, D. Hype Cycle for Blockchain Technologies. Gartner. 2018. Available online: https://www.gartner.com/en/documents/3883991/hype-cycle-for-blockchain-technologies-2018 (accessed on 25 July 2020).

- Swan, M. Blockchain: Blueprint for a New Economy; O’Reilly Media, Inc.: Newton, MA, USA, 2015. [Google Scholar]

- Hiscox. Hiscox Online Art Trading Report 2020. Available online: https://www.hiscox.co.uk/sites/uk/files/documents/2019-04/hiscox-online-art-trading-report-2020.pdf (accessed on 14 July 2021).

- The Art Market. The Art Basel and UBS Global Art Market Report 2019. Art Basel Press Release. 2019. Available online: https://d2u3kfwd92fzu7.cloudfront.net/The%20Art%20Market%202019_Press%20Release-2.pdf (accessed on 30 July 2021).

- Navas, R.; Chang, H.J.; Khan, S.; Chong, J.W. Sustainability Transparency and Trustworthiness of Traditional and Blockchain Ecolabels: A Comparison of Generations X and Y Consumers. Sustainability 2021, 13, 8469. [Google Scholar] [CrossRef]

- Salisbury, L. Art forgers—Criminals or heroes? In the post-truth era, it’s time for an unequivocal answer. Soc. Res. Int. Q. 2018, 85, 827–836. [Google Scholar]

- Dekking, N. Blockchain, The Holy Grail? Industry Voice. Art Dealer Finance. 2008. Available online: https://2018.amr.tefaf.com/voices/blockchain-technology-a-start-of-an-art-market-revolution (accessed on 23 July 2021).

- Lee, Y.S. Analysis on trends of artworks blockchain platform. Int. J. Adv. Cult. Technol. 2019, 7, 149–157. [Google Scholar]

- Golosova, J.; Romanovs, A. Overview of the blockchain technology cases. In Proceedings of the 2018 59th International Scientific Conference, Information Technology and Management Science of Riga Technical University (ITMS), Riga, Latvia, 10–12 October 2018; pp. 1–6. [Google Scholar]

- Whitaker, A. Art and Blockchain: A Primer, History, and Taxonomy of Blockchain Use Cases in the Arts. Artivate 2019, 8, 21–46. [Google Scholar] [CrossRef] [Green Version]

- Hiscox. Hiscox Online Art Trading Report 2018. Available online: https://arttactic.com/product/hiscox-online-art-trading-report-2018 (accessed on 15 July 2021).

- Whitaker, A.; Kraussl, R. Democratizing Art Markets: Fractional Ownership and The Securitization of Art. Semantic Scholar. 2018. Available online: https://www.semanticscholar.org/paper/Democratizing-Art-Markets%3A-Fractional-Ownership-and-Whitaker-Kr%C3%A4ussl/bf26cac648cd38b550fb616295d00fa6dce7b10a (accessed on 30 July 2021).

- Wang, S.; Archer, N. Strategic choice of electronic marketplace functionalities: A buyer-supplier relationship perspective. J. Comput. Mediat. Commun. 2017, 10, JCMC1016. [Google Scholar] [CrossRef]

- Zheng, Y. Blockchain, Privacy, and Artwork Registries: Consensus between Constraints. SSRN 2021. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3857241 (accessed on 27 September 2021).

- Joo, J.; Han, Y. An Evidence of Distributed Trust in Blockchain-Based Sustainable Food Supply Chain. Sustainability 2021, 13, 10980. [Google Scholar] [CrossRef]

- Salmerón-Manzano, E.; Manzano-Agugliaro, F. The role of Smart contracts in sustainability: Worldwide research trends. Sustainability 2019, 11, 3049. [Google Scholar] [CrossRef] [Green Version]

- Dowling, G.R.; Staelin, R. A model of perceived risk and intended risk-handling activity. J. Consum. Res. 1994, 20, 119–134. [Google Scholar] [CrossRef]

- Sweeney, J.C.; Soutar, G.N.; Johnson, L.W. The role of perceived risk in the quality-value relationship: A study in a retail environment. J. Retail. 1999, 75, 77–105. [Google Scholar] [CrossRef]

- Bauer, R.A. Consumer Behavior as Risk Taking; Hancock, R.S., Ed.; American Marketing Association: Chicago, IL, USA, 1960; Volume 6, pp. 389–398. [Google Scholar]

- Kotler, P. Marketing Management: Analysis, Planning, Implementation, and Control, 9th ed.; Prentice Hall: Upper Saddle River, NJ, USA, 1997. [Google Scholar]

- Vinhal Nepomuceno, M.; Laroche, M.; Richard, M.; Eggert, A. Relationship between intangibility and perceived risk: Moderating effect of privacy, system security and general security concerns. J. Consum. Mark. 2012, 29, 176–189. [Google Scholar] [CrossRef]

- Ram, S. A Model of Innovation Resistance in NA—Advances in Consumer Research; Wallendorf, M., Anderson, P., Eds.; Association for Consumer Research: Provo, UT, USA, 1987; Volume 14, pp. 208–212. [Google Scholar]

- Ram, S.; Sheth, J.N. Consumer resistance to innovations: The marketing problem and its solutions. J. Consum. Mark. 1989, 6, 5–14. [Google Scholar] [CrossRef]

- Zand, D.E. Trust and managerial problem solving. Adm. Sci. Q. 1972, 17, 229–239. [Google Scholar] [CrossRef]

- Cheung, C.; Lee, M.K.O. Trust in internet shopping: A proposed model and measurement instrument. In Proceedings of the America’s Conference on Information Systems (AMCIS’2000), Long Beach, CA, USA, 10–13 August 2020; p. 406. Available online: http://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.860.3707&rep=rep1&type=pdf (accessed on 27 September 2021).

- Lu, B.; Fan, W.; Zhou, M. Social presence, trust, and social commerce purchase intention: An empirical research. Comput. Hum. Behav. 2016, 56, 225–237. [Google Scholar] [CrossRef] [Green Version]

- Hwang, Y.; Kim, D.J. Customer self-service systems: The effects of perceived Web quality with service contents on enjoyment, anxiety, and e-trust. Decis. Support Syst. 2007, 43, 746–760. [Google Scholar] [CrossRef]

- Ye, S.; Ying, T.; Zhou, L.; Wang, T. Enhancing customer trust in peer-to-peer accommodation: A “soft” strategy via social presence. Int. J. Hosp. Manag. 2019, 79, 1–10. [Google Scholar] [CrossRef]

- van Pinxteren, M.M.; Wetzels, R.W.; Rüger, J.; Pluymaekers, M.; Wetzels, M. Trust in humanoid robots: Implications for services marketing. J. Serv. Mark. 2019, 33, 507–518. [Google Scholar] [CrossRef] [Green Version]

- Shi, S.; Gong, Y.; Gursoy, D. Antecedents of trust and adoption intention toward artificially intelligent tecommendation dystems in travel planning: A heuristic-systematic model. J. Travel Res. 2021, 60, 1714–1734. [Google Scholar] [CrossRef]

- Salam, A.F.; Rao, H.R.; Pegels, C.C. An Investigation of Consumer-Perceived Risk on Electronic Commerce Trading: The role of Institutional Trust and Economic Incentive in a Social Exchange Framework. In Proceedings of the AMCIS, Baltimore, MD, USA, 14–16 August 1998; pp. 335–337. Available online: https://aisel.aisnet.org/cgi/viewcontent.cgi?article=1541&context=amcis1998 (accessed on 28 July 2021).

- Antwi, S.; Bei, W.; Ameyaw, M.A. Investigating the moderating role of social support in online shopping intentions. J. Mark. Consum. Res. 2021, 78, 27–34. Available online: https://www.researchgate.net/profile/Samuel-Antwi-3/publication/351436209_Investigating_the_Moderating_Role_of_Social_Suport_in_Online_Shopping_Intentions/links/60978463458515d31507f6df/Investigating-the-Moderating-Role-of-Social-Support-in-Online-Shopping-Intentions.pdf (accessed on 22 October 2021).

- Kim, H.W.; Xu, Y.; Koh, J. A comparison of online trust building factors between potential customers and repeat customers. J. Assoc. Inf. Syst. 2004, 5, 392–420. [Google Scholar] [CrossRef]

- Lin, C.P.; Huang, H.Y. Modeling investment intention in online P2P lending: An elaboration likelihood perspective. Int. J. Bank Mark. 2021, 39, 1134–1149. [Google Scholar] [CrossRef]

- Lockl, J.; Stoetzer, J.C. Trust-free banking missed the point: The effect of distrust in banks on the adoption of decentralized finance. In Proceedings of the 29th European Conference on Information Systems (ECIS), Marrakech, Morocco, 14–16 June 2021; Available online: https://www.researchgate.net/profile/Jens-Christian-Stoetzer/publication/351082259_Trust-free_Banking_Missed_the_Point_-_The_Effect_of_Distrust_in_Banks_on_the_Adoption_of_Decentralized_Finance/links/6083de44881fa114b4242c65/Trust-free-Banking-Missed-the-Point-The-Effect-of-Distrust-in-Banks-on-the-Adoption-of-Decentralized-Finance.pdf (accessed on 22 October 2021).

- Al-Swidi, A.K.; Enazi, M.A. The trust in the intermediaries and the intention to use electronic government services: A case of a developing country Electronic Government. Int. J. 2020, 17, 27–54. Available online: https://www.inderscienceonline.com/doi/abs/10.1504/EG.2021.112942 (accessed on 22 October 2021). [CrossRef]

- Gefen, D.; Karahanna, E.; Straub, D.W. Trust and TAM in online shopping: An integrated model. MIS Q. 2003, 27, 51–90. Available online: https://www.researchgate.net/publication/220260204_Trust_and_TAM_in_Online_Shopping_An_Integrated_Model (accessed on 27 September 2021). [CrossRef]

- McKnight, D.H.; Choudhury, V.; Kacmar, C. The impact of initial consumer trust on intentions to transact with a web site: A trust building model. J. Strateg. Inf. Syst. 2002, 11, 297–323. [Google Scholar] [CrossRef]

- Wingreen, S.C.; Baglione, S.L. Untangling the antecedents and covariates of e-commerce trust: Institutional trust vs. knowledge-based trust. Electron. Mark. 2005, 15, 246–260. [Google Scholar] [CrossRef]

- Liu, S.; Du, J.; Zhang, W.; Tian, X.; Kou, G. Innovation quantity or quality? The role of political connections. Emerg. Mark. Rev. 2021, 48. [Google Scholar] [CrossRef]

- Liu, S.; Du, J.; Zhang, W. Opening the box of subsidies: Which is more effective for innovation? Eurasian Bus. Rev. 2021, 11, 421–449. [Google Scholar] [CrossRef]

- Tian, X.; Kou, G.; Zhang, W. Geographic Distance, Venture Capital and Technological Performance: Evidence from Chinese Enterprises; Elsevier: Amsterdam, The Netherlands, 2020; Volume 158, Available online: https://www.sciencedirect.com/science/article/abs/pii/S0040162520309811?via%3Dihub (accessed on 21 October 2021).

- Chatterjee, S.; Bhattacharjee, K.K.; Tsai, C.W. Impact of peer influence and government support for successful adoption of technology for vocational education: A quantitative study using PLS-SEM technique. Qual. Quant. 2021, 55, 2041–2064. [Google Scholar] [CrossRef]

- Sekaran, U.; Bougie, R. Research Methods for Business: A Skill Building Approach, 5th ed.; John Wiley and Sons: Chichester, UK, 2009. [Google Scholar]

- Kambil, A.; Van Heck, E. Reengineering the Dutch flower auctions: A framework for analyzing exchange organizations. Inf. Syst. Res. 1998, 9, 1–19. [Google Scholar] [CrossRef] [Green Version]

- Orji, I.J.; Kusi-Sarpong, S.; Huang, S.; Vazquez-Brust, D. Evaluating the factors that influence blockchain adoption in the freight logistics industry. Transp. Res. E Logist. Transp. Rev. 2020, 141, 102025. Available online: https://www.sciencedirect.com/science/article/abs/pii/S1366554520306761 (accessed on 27 September 2021). [CrossRef]

- Polatoglu, V.N.; Ekin, S. An empirical investigation of the Turkish consumers’ acceptance of Internet banking services. Int. J. bank Mark. 2021, 19, 156–165. [Google Scholar] [CrossRef]

- Ajzen, I. Attitude Structure and Behavior. Attitude Structure and Function; Pratkanis, A.R., Breckler, S.J., Greenwald, A.G., Eds.; Lawrence Erlbaum Associates, Inc.: Mahwah, NJ, USA, 1989; pp. 241–274. [Google Scholar]

- Ajzen, I.; Fishbein, M. A Bayesian analysis of attribution processes. Psychol. Bull. 1975, 82, 261. [Google Scholar] [CrossRef]

- Bocart, F.; Oosterlinck, K. Discoveries of fakes: Their impact on the art market. Econ. Lett. 2011, 113, 124–126. [Google Scholar] [CrossRef] [Green Version]

- Bajari, P.; Hortaçsu, A. Economic insights from internet auctions. J. Econ. Lit. 2004, 42, 457–486. [Google Scholar] [CrossRef]

- Siegrist, M.; Zingg, A. The role of public trust during pandemics implications for crisis communication. Eur. Psychol. 2014, 19, 23–32. [Google Scholar] [CrossRef]

- Siegrist, M.; Luchsinger, L.; Bearth, A. The impact of trust and risk perception on the acceptance of measures to reduce COVID-19 Cases. Risk Anal. 2021, 41, 787–800. [Google Scholar] [CrossRef]

- Gerber, B.; Neeley, G.W. Perceived risk and citizen preferences for government management of routine hazards. Policy Stud. J. 2005, 33, 395–418. [Google Scholar] [CrossRef]

- Saberi, S.; Kouhizadeh, M.; Sarkis, J.; Shen, L. Blockchain technology and its relationships to sustainable supply chain management. Int. J. Prod. Res. 2019, 57, 2117–2135. [Google Scholar] [CrossRef] [Green Version]

- Clohessy, T.; Acton, T.; Rogers, N. Blockchain adoption: Technological, organisational and environmental considerations. In Business Transformation Through Blockchain; Treiblmaier, H., Beck, R., Eds.; Palgrave Macmillan: Cham, Switzerland, 2019; pp. 47–76. [Google Scholar]

- Strub, P.J.; Priest, T.B. Two patterns of establishing trust: The marijuana user. Sociol. Focus 1976, 9, 399–411. [Google Scholar] [CrossRef]

- Jarvenpaa, S.L.; Tractinsky, N.; Vitale, M. Consumer trust in an Internet store. Inf. Technol. Manag. 2000, 1, 45–71. [Google Scholar] [CrossRef]

- Shneiderman, B. Designing trust into online experiences. Commun. ACM 2000, 43, 57–59. [Google Scholar] [CrossRef]

- Financial Conduct Authority. Regulatory Sandbox. London: Financial Conduct Authority 2015. Available online: https://www.fca.org.uk/publication/research/regulatory-sandbox.pdf (accessed on 28 September 2021).

- UK Government Chief Science Adviser. FinTech Futures: The UK as A World Leader in Financial Technologies. London: Government Office for Science 2015. Available online: https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/413095/gs-15-3-fintech-futures.pdf (accessed on 27 September 2021).

- Mou, J.; Shin, D.; Cohen, J. Trust and risk in consumer acceptance of e-services. Electron. Commer. Res. 2017, 17, 255–288. [Google Scholar] [CrossRef]

- Shin, D. Blockchain: The emerging technology of digital trust. Telemat. Inform. 2019, 45, 1–11. [Google Scholar] [CrossRef]

- Geyskens, I.; Steenkamp, J.B.E.M.; Scheer, L.K.; Kumar, N. The effects of trust and interdependence on relationship commitment: A trans-Atlantic study. Int. J. Res. Mark. 1996, 13, 303–317. [Google Scholar] [CrossRef]

- Zucker, L. Production of trust: Institutional sources of economic structure, 1840–1920. Res. Organ. Behav. 1986, 8, 53–111. [Google Scholar]

- Hong, I.B.; Cho, H. The impact of consumer trust on attitudinal loyalty and purchase intentions in B2C e-marketplaces: Intermediary trust vs. seller trust. Int. J. Inf. Manag. 2011, 31, 467–479. [Google Scholar] [CrossRef]

- Kuo, C.C.; Rogers, P.; White, R.E. Online reverse auctions: An overview. J. Int. Technol. Inf. Manag. 2004, 13, 5. [Google Scholar]

- Herschlag, M.; Zwick, R. Internet Auctions-Popular and Professional Literature Review. ResearchGate 2000. Available online: https://www.researchgate.net/publication/2459222_Internet_Auctions_--_Popular_and_Professional_Literature_Review (accessed on 29 September 2021).

- Gefen, D. Building Users’ Trust in Freeware Providers and the Effects of this Trust on Users’ Perceptions of Usefulness, Ease of Use and Intended Use of Freeware; Georgia State University: Atlanta, GA, USA, 1997. [Google Scholar]

- Slade, E.L.; Dwivedi, Y.K.; Piercy, N.C.; Williams, M.D. Modeling consumers’ adoption intentions of remote mobile payments in the United Kingdom: Extending UTAUT with innovativeness, risk, and trust. Psychol. Mark. 2015, 32, 860–873. [Google Scholar] [CrossRef]

- Beltrametti, S.; Marrone, J.V. Market responses to court rulings: Evidence from antiquities auctions. J. Law Econ. 2016, 59, 913–944. [Google Scholar] [CrossRef]

- Latif, M.I.; Zakaria, Z. Factors determine the behavioural intention in adopting the blockchain technology by Malaysian Public Sector Officers. J. Adv. Res. Bus. Manag. Stud. 2020, 20, 34–43. [Google Scholar] [CrossRef]

- Wong, L.W.; Tan, G.W.H.; Lee, V.H.; Ooi, K.B.; Sohal, A. unearthing the determinants of blockchain adoption in supply chain management. Int. J. Prod. Res. 2020, 58, 2100–2123. [Google Scholar] [CrossRef] [Green Version]

- Moon, J.W.; Kim, Y.G. Extending the TAM for World-Wide-Web context. Inf. Manag. 2001, 38, 217–230. [Google Scholar] [CrossRef]

- Bhattacherjee, A. Understanding information systems continuance: An expectation-confirmation model. MIS Q. 2001, 25, 351–370. [Google Scholar] [CrossRef]

- Lin, C.S.; Wu, S.; Tsai, R.J. Integrating perceived playfulness into expectation-confirmation model for web portal context. Inf. Manag. 2005, 42, 683–693. [Google Scholar] [CrossRef]

- Cronbach, L.J. Coefficient alpha and the internal structure of tests. Psychometrika 1951, 16, 297–334. [Google Scholar] [CrossRef] [Green Version]

- Hair, J.F.; Black, W.C.; Babin, B.J.; Anderson, R.E.; Tatham, R.L. Multivariate Data Analysis, 6th ed.; Pearson Prentice Hall: Upper Saddle River, NJ, USA, 2006; Volume 6. [Google Scholar]

- Fornell, C.; Larcker, D.F. Evaluating structural equation models with unobservable variables and measurement error. J. Mark. Res. 1981, 18, 39–50. [Google Scholar] [CrossRef]

- Hair, J.F.; Anderson, R.E.; Tatham, R.L.; Black, W.C. Multivariate Data Analysis, 5th ed.; Prentice Hall College Div: Hoboken, NJ, USA, 1998. [Google Scholar]

- Gaski, J.F.; Nevin, J.R. The differential effects of exercised and unexercised power sources in a marketing channel. J. Mark. Res. 1985, 22, 130–142. [Google Scholar] [CrossRef]

- Albayati, H.; Kim, S.K.; Rho, J.J. Accepting financial transactions using blockchain technology and cryptocurrency: A customer perspective approach. Technol. Soc. 2020, 62. [Google Scholar] [CrossRef]

- Mario, A.O.; Jorge, P.B.; Matías-Clavero Gustavo, M.C. Variables influencing cryptocurrency use: A technology acceptance model in Spain. Front. Psychol. 2019, 10, 475. Available online: https://www.frontiersin.org/article/10.3389/fpsyg.2019.00475 (accessed on 29 October 2021).

- Zhang, W.; Zhang, X.; Tian, X.; Sun, F. Economic policy uncertainty nexus with corporate risk-taking: The role of state ownership and corruption expenditure. Pac. Basin Financ. J. 2021, 65, 101496. [Google Scholar] [CrossRef]

- Qin, M.; Su, C.W.; Xiao, Y.D.; Zhang, S. Should gold be held under global economic policy uncertainty? J. Bus. Econ. Manag. 2020, 21, 725–742. [Google Scholar] [CrossRef] [Green Version]

- Su, C.W.; Qin, M.; Tao, R.; Zhang, X. Is the status of gold threatened by Bitcoin? Econ. Res. Ekon. Istraživanja 2020, 33, 420–437. [Google Scholar] [CrossRef]

- Tao, R.; Su, C.W.; Yaqoob, T.; Hammal, M. Do Financial and Non-Financial Stocks Hedge Against Lockdown in Covid-19? An Event Study Analysis. Taylor Fr. Online 2021. [Google Scholar] [CrossRef]

Figure 1.

Research model.

Figure 2.

Path coefficient analysis results. Note: * p < 0.05, ** p < 0.01, *** p < 0.005, R2 is coefficient of determination.

Figure 2.

Path coefficient analysis results. Note: * p < 0.05, ** p < 0.01, *** p < 0.005, R2 is coefficient of determination.

{kind=link}

{kind=link}

Table 1.