Towards Sustainable Private Labels—What is the Consumer Behavior Relating to Private Labels in the UK and Poland?

Abstract

1. Introduction

2. Materials and Methods

2.1. Ethics Approval Statement

2.2. Data Collection

2.3. Questionnaire Design

2.4. Statistical Analysis

2.5. Sample Characteristics

3. Results

3.1. The Period of Buying PLs

3.2. Frequency of Purchasing PL Products

3.3. Main Factors of PL Purchase

3.4. Opinions of PL Development

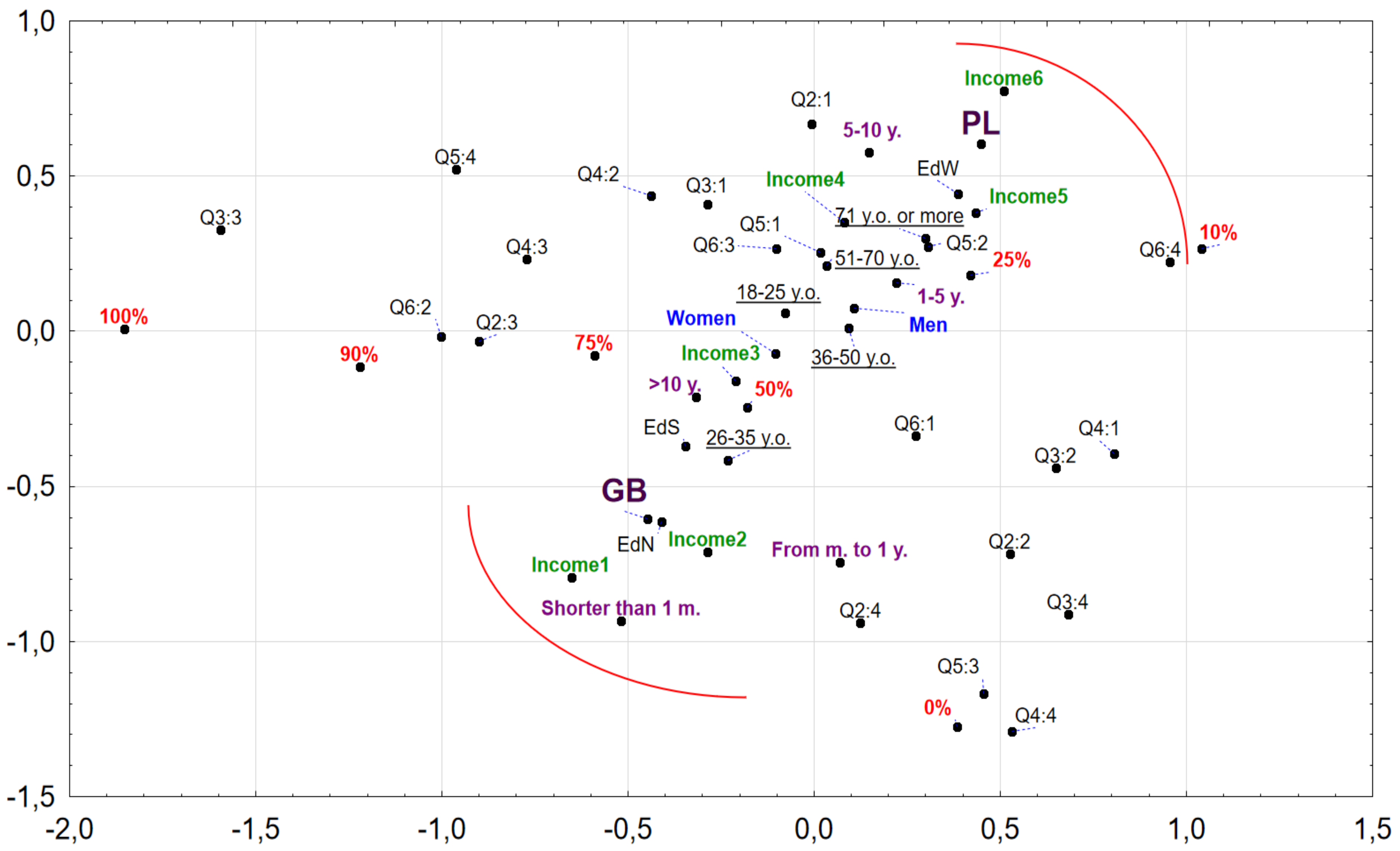

3.5. Purchase Behavior of PL Products—The Correspondence Analysis

4. Discussion

5. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Steenkamp, J.B.E.M.; Dekimpe, M.G. The Increasing Power of Store Brands: Building Loyalty and Market Share. Long Range Plann. 1997, 30, 917–930. [Google Scholar] [CrossRef]

- Shukla, P.; Banerjee, M.; Adidam, P.T. The moderating influence of socio-demographic factors on the relationship between consumer psychographics and the attitude towards private label brands. J. Consum. Behav. 2013, 1–13. [Google Scholar] [CrossRef]

- Ailawadi, K.L.; Pauwels, K.; Steenkamp, J.-B.E. Private Label Use and Store Loyalty. J. Mark. 2008, 1–31. [Google Scholar] [CrossRef]

- Wang, J.J.; Torelli, C.J.; Lalwan, A.K. The interactive effect of power distance belief and consumers’ status on preference for national (vs. private-label) brands. J. Bus. Res. 2020, 107, 1–12. [Google Scholar] [CrossRef]

- Dekimpe, M.G.; Deleersnyder, B. Business cycle research in marketing: A review and research agenda. J. Acad. Mark. Sci. 2018, 46, 31–58. [Google Scholar] [CrossRef]

- Martos-Partal, M.; González-Benito, O.; Fustinoni-Venturini, M. Motivational profiling of store brand shoppers: Differences across quality tiers. Mark. Lett. 2015, 26, 187–200. [Google Scholar] [CrossRef]

- Gómez-Suárez, M.; Martínez-Ruiz, M.P. Handbook of Research on Strategic Retailing of Private Label Products in a Recovering Economy; IGI Global: Hershey, PA, USA, 2016. [Google Scholar]

- Kumar, N.; Steenkamp, J.-B.E.M. Private Label Strategy How to Meet the Store Brand Challenge; Harvard Business School Press: Brighton, MA, USA, 2007; ISBN 9781422101674. [Google Scholar]

- Lincoln, K.; Thomassen, L. Private Label. Turning the Retail. Brand Threat into Your Biggest Opportunity; Kogan Page: London, UK, 2008; ISBN 0749455934. [Google Scholar]

- De, D.; Singh, A. Consumer’s Perspective and Retailer’s Consideration Towards Purchase of Private Label Brands. Procedia Comput. Sci. 2017, 122, 587–594. [Google Scholar] [CrossRef]

- Górska-Warsewicz, H.; Zakowska-Biemans, S.; Czeczotko, M.; Swiatkowska, M.; Stangierska, D.; Swistak, E.; Bobola, A.; Szlachciuk, J.; Krajewski, K. Organic private labels as sources of competitive advantage-The case of international retailers operating on the Polish market. Sustainability 2018, 10, 2338. [Google Scholar] [CrossRef]

- Geyskens, I.; Keller, K.O.; Dekimpe, M.G.; de Jong, K. How to brand your private labels. Bus. Horiz. 2018, 61, 487–496. [Google Scholar] [CrossRef]

- Liderzy I Trendy W Handlu. Available online: https://retail360.pl/wp-content/uploads/2012/08/RTP_liderzy2017_calosc.pdf (accessed on 8 January 2020).

- Chan Choi, S. Defensive strategy against a private label: Building brand premium for retailer cooperation. J. Retail. Consum. Serv. 2017, 34, 335–339. [Google Scholar] [CrossRef]

- Collins-Dodd, C.; Lindley, T. Store brands and retail differentiation: The influence of store image and store brand attitude on store own brand perceptions. J. Retail. Consum. Serv. 2003, 10, 345–352. [Google Scholar] [CrossRef]

- Grewal, D.; Krishnan, R.; Baker, J.; Borin, N. The Effect of Store Name, Brand Name and Price Discounts on Consumers’ Evaluations and Purchase Intentions. J. Retail. 1998, 74, 331–352. [Google Scholar] [CrossRef]

- Laaksonen, H.; Reynolds, J. Own brands in food retailing across Europe. J. Brand Manag. 1994, 2, 37–46. [Google Scholar] [CrossRef]

- Nielsen Company The Rise and Rise again of Private Label. Available online: http://www.nielsen.com/us/en/insights/%20reports/2018/the-rise-and-rise-again-of-private-label.html (accessed on 9 June 2019).

- Private Label Market (PLMA) Private Label gains across Europe, climbing to all- time highs in seven countries. Available online: https://www.plmainternational.com/industry-news/private-label (accessed on 26 June 2018).

- Private Label Market (PLMA) Private Label’S Market Share Reaches All-Time High sin 9 European Countries. Available online: https://www.plmainternational.com/industry-news/private-label-today, (accessed on 22 June 2017).

- Private Label Market (PLMA) Market Shares Climbing to All-Time Highs in Five Countries. Available online: https://www.plmainternational.com/industry-news/ (accessed on 3 February 2020).

- Sogn-Grundvåg, G.; Larsen, T.A.; Young, J.A. Product Differentiation with Credence Attributes and Private Labels: The Case of Whitefish in UK Supermarkets. J. Agric. Econ. 2014, 65, 368–382. [Google Scholar] [CrossRef]

- Burt, S. The strategic role of retail brands in British grocery retailing. Eur. J. Mark. 2000, 34, 875–890. [Google Scholar] [CrossRef]

- Peter, J. Boyle and E. Scott Lathrop the value of private label brands to U.S. consumers: An objective and subjective assessment. J. Retail. Consum. Serv. 2007, 20, 80–86. [Google Scholar]

- IRi. Share of Private-Label-Price-Level-in-Europe-2018-by-Country. Available online: https://www.statista.com/statistics/383455/private-label-price-level-by-european-countries/ (accessed on 22 May 2020).

- Cotterill, R.W. The food distribution system of the future: Convergence towards the US or UK model. Agribusiness 1997, 13, 123–135. [Google Scholar] [CrossRef]

- Hokelekli, G.; Track, L.; Co-author, R.; Hokelekli, G.; Leuven, K.U.; Verboven, F.; Leuven, K.U. Private-Label Proliferation A New Dimension of Competition Between Private Labels and National Brands. J. Retail. Consum. Serv. 2015, 36, 38–52. [Google Scholar]

- Tarzijan, J.M. Private Labels and ratail market concentration. Abande 2003, 6, 1–20. [Google Scholar]

- Nielsen the State of Private Label around the World. Available online: https://www.nielsen.com/ssa/en/insights/report/2014/the-state-of-private-label-around-the-world/ (accessed on 12 April 2020).

- PWC The Private Labels Revolution. Available online: https://www.pwc.pl/en.html (accessed on 9 May 2020).

- Górska-Warsewicz, H. Zachowania konsumentów wobec marek w sytuacjach kryzysowych. Probl. Zarz. 2013, 11, 143–156. [Google Scholar] [CrossRef]

- Górska-Warsewicz, H.; Czeczotko, M. Analysis of Product Strategies of Dairy Trade Brands in Biedronka and Lidl Discounters. Probl. Zarz. 2016, 57, 138–151. [Google Scholar] [CrossRef]

- PMR Market Experts Private Label Retail Market in Poland 2019. Market. Analysis and Development Forecasts for 2019–2024. Available online: https://mypmr.pro/products/private-label-retail-market-in-poland-2019 (accessed on 14 May 2020).

- Geyskens, I.; Gielens, K.; Gijsbrechts, E. Proliferating Private-Label Portfolios: How Introducing Economy and Premium Private Labels Influences Brand Choice. J. Mark. Res. 2010, 47, 791–807. [Google Scholar] [CrossRef]

- Vroegrijk, M.; Gijsbrechts, E.; Campo, K. Battling for the Household’s Category Buck: Can Economy Private Labels Defend Supermarkets Against the Hard-Discounter Threat. J. Retail. 2016, 92, 300–318. [Google Scholar] [CrossRef]

- Górska-Warsewicz, H.; Czeczotko, M.; Kudlińska-Chylak, A. Consumer Behaviours towards Private Labels. Handel Wewnętrzny 2018, 2, 54–64. [Google Scholar]

- Czeczotko, M.; Górska-Warsewicz, H. Consumers’ knowledge of own brands in Poland. In Nauki Społeczno-Ekonomiczne. Nieprzetarte Ścieżki, Czy Utarte Szlaki; Misiuna, J., Dworakowska, M., Wosiek, R., Eds.; SGH: Warsaw, Poland, 2018; pp. 149–159. ISBN 978-83-8030-256-3. [Google Scholar]

- Czeczotko, M.; Kulykovets, O.; Kudlińska-Chylak, A.; Górska-Warsewicz, H. Perception of Private Labels of the Makro Cash & Carry Wholesale Network by Professional Customers from the Sector of Catering Services. Handel Wewnętrzny 2017, 3, 265–274. [Google Scholar]

- Czeczotko, M.; Popławski, D. Private labels of retail chains- comparative analysis of purchase portfolio 2017–2018. In Przedsiębiorczość W Nauce I Praktyce: Zarządzanie-Finanse-Rynek; Górska-Warsewicz, H., Czeczotko, M., Eds.; SGGW: Warsaw, Poland, 2019; pp. 160–167. ISBN 9788375838473. [Google Scholar]

- Górska-Warsewicz, H.; Czeczotko, M. Perception of Private Labels in Poland. In Internal Trade in Poland; Kłosiewicz-Górecka, U., Klonowska, U., Śmigielska, G., Radziukiewicz, M., Kasperec, S., Eds.; GUS Central Statistical Office: Warsaw, Poland, 2017; pp. 167–187. [Google Scholar]

- Czeczotko, M.; Kosicka-Gębska, M.; Górska-Warsewicz, H.; Kudlińska-Chylak, A.; Kulykovets, O. The Retail Trade Characteristics as a Part of a Distribution System in Poland. Przedsiębiorczość i Zarządzanie 2018, XIX, 169–182. [Google Scholar]

- Kong, H.; West, S. Wma Declaration of Helsinki—Ethical Principles for Scientific Requirements and Research Protocols. World Med. Assoc. 2013, 79, 29–32. [Google Scholar]

- Scherpenzeel, A.C.; Bethlehem, J.G. How Representative Are Online Panels. In Social and Behavioral Research and the Internet: Advances in Applied Methods and Research Strategies; Das, M., Ester, P., Kaczmirek, L., Eds.; Taylor & Francis Group: New York, NY, USA, 2011; pp. 105–132. [Google Scholar]

- Lubsky, A. Methodology of Social Research; Laxmi Publications: New Delhi, India, 2017. [Google Scholar]

- Wójcicki, T. Application of the CAWI method for the holistic support of innovation. Maint. Probl. 2012, 4, 175–186. [Google Scholar]

- C.S.O. Statistical Yearbook of the Republic of Poland 2018; Central Statistical Office: Warsaw, Poland, 2019.

- Gov.UK National MinimumWage and National Living Wage Rates. Available online: https://www.gov.uk/national-minimum-wage-rates (accessed on 26 May 2020).

- Statistics Poland Methodological Report. In Household Budget Survey; Statistics Poland: Warsaw, Poland, 2001. Available online: https://www.ilo.org/ilostat-files/SSM/SSM6/E/455A.html (accessed on 10 June 2020).

- Garczarek-Bąk, U. Retailers’ private label review in Poland and worldwide. Mark. Rynek 2016, 8, 2–14. [Google Scholar]

- Matysik-Pejas, R.; Sowula, M. Perception of private labels by purchasers. Eur. Policies Financ. Mark. 2013, 10, 475–483. [Google Scholar]

- Cyran, K. The perception of private labels of food products vs. the prospects for their development. Res. Pap. Wrocław Univ. Econ. 2016, 450, 114–124. [Google Scholar]

- Kot, Z.; Kaczorowska, J. Perception of Private Labels in Poland among Young Consumers. Eur. POLICIES, Financ. Mark. 2013, 10, 371–380. [Google Scholar]

- Rybowska, A. Consumer opinion to the products of its private label trade network operating on the polish market. Rocz. Nauk. Stowarzyszenia Ekon. Rol. Agrobiznesu 2014, 16, 3–258. [Google Scholar]

- Urbanek, P.; Walińska, E. Private label image branding—onditions, directions and good practices. In Ekonomia I Zarządzanie W Teorii I Praktyce; University of Łódź: Łodź, Poland, 2016; pp. 201–213. [Google Scholar]

- Wanjiku, M. Consumer Perception Towards Private Label. Brands of Four Key Supermarkets in Kenya. Ph.D. Thesis, University of Nairobi, Nairobi, Kenya, 2015; pp. 1–55. [Google Scholar]

- Veloutsou, C.; Gioulistanis, E.; Moutinho, L. Own labels choice criteria and perceived characteristics in Greece and Scotland: Factors influencing the willingness to buy. J. Prod. Brand Manag. 2004, 13, 228–241. [Google Scholar] [CrossRef]

- Bao, Y.; Bao, Y.; Sheng, S. Motivating purchase of private brands: Effects of store image, product signatureness, and quality variation. J. Bus. Res. 2011, 64, 220–226. [Google Scholar] [CrossRef]

- Joshi, A.; Kale, S.; Chandel, S.; Pal, D. Likert Scale: Explored and Explained. Br. J. Appl. Sci. Technol. 2015, 7, 396–403. [Google Scholar] [CrossRef]

- Awang, Z.; Afthanorhan, A.; Mamat, M.; Sultan, U.; Abidin, Z. The Likert scale analysis using parametric based Structural Equation Modeling (SEM). Comput. Methods Soc. Sci. 2016, 4, 13–21. [Google Scholar]

- Roopa, S.; Rani, M. Questionnaire Designing for a Survey. J. Indian Orthod. Soc. 2012, 46, 273–277. [Google Scholar] [CrossRef]

- Sansone, M.; Bruni, R.; Colamatteo, A. Selecting Factors Affecting the Purchase of Private Label Products. In Advances in National Brand and Private Label Marketing; Martínez-López, F., Gázquez-Abad, J., Ailawadi, K., Yagüe-Guillén, M., Eds.; Springer: Berlin/Heidelberg, Germany, 2017; pp. 117–129. ISBN 9783319597010. [Google Scholar]

- Opportunities in the Value-Added Private Label. Market. Available online: https://www.iplc-europe.com/wp-content/uploads/2020/01/IPLC-Research-Report-2018.pdf (accessed on 18 March 2020).

- Godderidge, P.; Johansson, N.; Larsson, L. Private Labels and Generation Dislo(Y)al–The Impact of Private Labels on Store Loyalty within the Swedish Grocery Retail. Industry; Cerne, A., Ed.; Lund University, School of Economics and Management: Lund, Sweden, 2016. [Google Scholar]

- Danziger, S.; Hadar, L.; Morwitz, V.G. Retailer Pricing Strategy and Consumer Choice under Price Uncertainty. J. Consum. Res. 2014, 41, 761–774. [Google Scholar] [CrossRef]

- Gangwani, S.; Mathur, M.; Shahab, S. Influence of consumer perceptions of private label brands on store loyalty–evidence from Indian retailing. Cogent Bus. Manag. 2020, 7. [Google Scholar] [CrossRef]

- Dobson, P.; Chakraborty, R. Private labels and branded goods: Consumers’ “horrors” and “heroes.”. In Labels, Brands and Competition Policy: The Changing Landscape of Retail. Competition; Ezrachi, A., Bernitz, U., Eds.; Oxford University Press: Oxford, UK, 2009; pp. 100–124. ISBN 0199559376. [Google Scholar]

- Smith, R. Employee earnings in the UK. 2018. Available online: https://www.ons.gov.uk/employmentandlabourmarket/peopleinwork/earningsandworkinghours/bulletins/annualsurveyofhoursandearnings/2018 (accessed on 15 June 2020).

- Kohonen, T. Self-Organizing Maps, 3th ed.; Springer: Berlin/Heidelberg, Germany, 2001; ISBN 9783540679219. [Google Scholar]

- Clarke, K.R.; Warwick, R. Change in Marine Communities an Approach to Statistical Analysis and Interpretation, 2nd ed.; Primer-E: Plymouth, UK, 2001. [Google Scholar]

- Greenacre, M.; Blasius, J. Multiple Correspondence Analysis and Related Methods. (Statistics in the Social and Behavioral Sciences Series); Taylor & Francis Group: Boca Raton, FL, USA; CRC: New York, NY, USA, 2006; ISBN 9781584886280. [Google Scholar]

- Ibarra Consuegra, O.; Kitchen, P. Own labels in the United Kingdom: A source of competitive advantage in retail business. Pensamiento & Gestión 2006, 21, 114–161. [Google Scholar]

- Eales, T. Private Label in Western Economies. Available online: https://www.iriworldwide.com/en-GB/News/Media-Coverage/Private-label-in-Europe-Tailor-your-growth-strategy-per-country,-says-IRI (accessed on 20 May 2019).

- Statistica.com Sales share of private labels food in USA in 2019, by category. Available online: https://www.statista.com/statistics/1100038/sales-share-of-private-label-food-us-by-category/ (accessed on 29 March 2020).

- Valaskova, K.; Kliestikova, J.; Krizanova, A. Consumer Perception of Private Label Products: An Empirical Study. J. Compet. 2018, 10, 149–163. [Google Scholar]

- Abotorabi, O. Private Label in Western Economies IRI Special Report. Available online: https://www.statista.com/statistics/1100038/sales-share-of-private-label-food-us-by-category/ (accessed on 29 March 2020).

- Beristain, J.J.; Zorrilla, P. The relationship between store image and store brand equity: A conceptual framework and evidence from hypermarkets. J. Retail. Consum. Serv. 2011, 18, 562–574. [Google Scholar] [CrossRef]

- Retnawati, B.B.; Ardyan, E.; Farida, N. The important role of consumer conviction value in improving intention to buy private label product in Indonesia. Asia Pacific Manag. Rev. 2018, 23, 193–200. [Google Scholar] [CrossRef]

- Kowalska, M. Development and Significance of Private Label in Poland. Stud. I Pr. Wydz. Nauk. Ekon. I Zarządzania 2015, 39, 365. [Google Scholar]

- Majewska, M. How Do We Perceive Private Labels. Prospects for the Development of Private Label. Market. in Poland; Private Label in Poland: Warsaw, Poland, 2014. [Google Scholar]

- The Rise of Premium Private Label and it’s Impact on Discount Retailers—Nielsen. Available online: https://www.nielsen.com/us/en/insights/article/2019/the-rise-of-premium-private-label-and-its-impact-on-discount-retailers/?utm_source=sfmc&utm_medium=email&utm_campaign=newswire&utm_content=9-4-19 (accessed on 1 June 2020).

- Roosen, J. Marketing of safe food through labeling. J. Food Distrib. Res. 2003, 34, 77–82. [Google Scholar]

- Calvo-Porral, C.; Lévy-Mangin, J.P. Private label brands: Major perspective of two customer-based brand equity models. Int. Rev. Retail. Distrib. Consum. Res. 2014, 24, 431–452. [Google Scholar] [CrossRef]

- Agyekum, C.K.; Haifeng, H.; Agyeiwaa, A. Consumer Perception of Product Quality. Microeconomics Macroecon. 2015, 3, 25–29. [Google Scholar]

- Koshy, A., A. Quality Perceptions of Private Label Brands. Indian Inst. Manag. 2008, 1–22. [Google Scholar]

- Yee, C.J.; San, N.C. Consumers’ Perceived Quality, Perceived Value and Perceived Risk Towards Purchase Decision on Automobile. Am. J. Econ. Bus. Adm. 2011, 3, 47–57. [Google Scholar]

- DelVecchio, D. Consumer perceptions of private label quality: The role of product category characteristics and consumer use of heuristics. J. Retail. Consum. Serv. 2001, 8, 239–249. [Google Scholar] [CrossRef]

- Aaker, D.A. Managing Brand Equity Capitalizing on the Value of a Brand Name; Free Press: Toronto, ON, Canada; New York, NY, USA, 1991. [Google Scholar]

- Umar, T.; Mat, N.K.N.; Tahir, F.A.; Alekam, J.M.E. The Practicality and Application of Aaker’s Customer Based Brand Equity Model in the Nigerian Banking Sector. Am. J. Econ. 2012, 2, 149–152. [Google Scholar] [CrossRef]

- Jaafar, S.N. Consumers’ Perceptions, Attitudes and Purchase Intention towards Private Label Food Products in Malaysia. Asian J. Bus. Manag. Sci. 2018, 2, 73–90. [Google Scholar]

- Lewis, M. Understanding the Value of Private Label Store Brands—Reasons to Buy. Available online: https://www.moneycrashers.com/private-label-store-brands/ (accessed on 14 July 2020).

- Bauer, H.H.; Heinrich, D.; Schäfer, D.B. The effects of organic labels on global, local, and private brands. More hype than substance. J. Bus. Res. 2013, 66, 1035–1043. [Google Scholar] [CrossRef]

{kind=link}

| Question | Cited Literature | Variants of Answers | |

|---|---|---|---|

| 1. | Period of purchase of PL products | - | choose the right answer |

| less than 1 month | - | ||

| 1 month to 1year | - | ||

| 1 to 5 years | - | ||

| 5 to 10 years | - | ||

| more than 10 years | - | ||

| 2. | Opinions of PLs regarding retail chains | not analyzed in this paper | |

| 3. | Factors for purchasing PL products: | - | 1—totally disagree 2—disagree; 3—neither agree nor disagree; 4—agree; 5—totally agree |

| wide product range | [29,36,49,50,51] | ||

| lower price compared to leading brands | [29,49,52,53,54] | ||

| high product quality | [29,36,50,52,53,54,55,56] | ||

| ability to buy the same products repeatedly | [36,57] | ||

| availability of PL products in every store of a particular chain | [36,49,50,51,55] | ||

| attachment to a given chain | [36,55,56,57] | ||

| feeling of safety and trust to PL products | [51,52,55,57] | ||

| recognisability of PLs among consumers | [40,54,55,57] | ||

| 4. | Opinions on currently offered PL products | not analyzed in this paper | |

| 5. | Opinions on the current development of the PL product range | - | |

| improvement in the quality of PL products | [29,36,52,61] | 1—unimportant | |

| increase in the range of products offered under PL | [61,62] | 2—fairly unimportant | |

| improved visual presentation of PL products | [52,61,63] | 3—neither important nor unimportant | |

| lower price of PL products while retaining quality | [3,61,63,64] | ||

| greater availability of PL products | [36,49,50,51,55] | 4—fairly important | |

| improved image/perception of PL products | [61,63,65] | 5—very important | |

| 6. | Frequency of purchasing particular categories of products sold under the PLs of retail chains: | [49,53,55,66] | scale: 1—I don’t buy at all; 2—I buy rarely; 3—I buy sometimes; 4—I buy often; 5—buy very often. |

| dairy products, grain products, sweets &biscuits, bread and bakery products, meat and meat products, fruits &vegetables, fruit &vegetable products, frozen food, non-alcoholic beverages & water, alcohol | - | ||

| 7. | Indicative share of PL products in relation to total food purchases: | - | scale: 0%; 10%;25%; 50%;75%; 90%; 100% |

| 8. | Retail chains most frequently chosen for PLs purchase (appropriate list of stores for the country) | - | not analyzed in this paper |

| United Kingdom: Aldi; Asda; Iceland; Lidl; Mark and Spencer; Morrison’s; Sainsbury’s; Symbols & Independent; Tesco; The Co-operative; Waitrose; Ocado; Other Outlets | - | choose the right answer (max. 3) | |

| Poland: Tesco; Auchan; Carrefour; Netto; Kaufland; Biedronka; Lidl; Aldi; E. Leclerc; Delikatesy Centrum; Żabka; Stokrotka; Intermarche; Polomarket, Lewiatan; Makro; Selgros | - | choose the right answer (max. 3) | |

| 9. | Sociodemographic data: | - | choose the right answer |

| Gender: women, men | - | ||

| Age (years): 18–25; 26–35; 36–50; 51–70;71+ | - | ||

| Education: primary and vocational, secondary, higher | - | ||

| Place of residence: rural area; cities up to 19,999; cities above 20,000 to 99,999; cities above 100,000 to 499,999; cities above 500,000 | - | ||

| Household income (per person; status on January 1, 2018) United Kingdom: under £1200; £1201–£1800; £1801–£2500; £2501–£3500; £3500 or more Poland: under 1000 PLN; 1001 PLN-1500 PLN; 1501 PLN-2500 PLN; 2501 PLN-4000 PLN; 4001 PLN or more | [46,48,67] | ||

| Group | Poland | United Kingdom | ||

|---|---|---|---|---|

| Number of Respondents | Percentage | Number of Respondents | Percentage | |

| Total | ||||

| - | 500 | 100.0 | 500 | 100.0 |

| Gender | ||||

| Women | 261 | 52.2 | 246 | 49.2 |

| Men | 239 | 47.8 | 254 | 50.8 |

| Age | ||||

| 18–25 | 55 | 11.0 | 31 | 6.2 |

| 26–35 | 91 | 18.2 | 156 | 31.2 |

| 36–50 | 133 | 26.6 | 126 | 25.2 |

| 51–70 | 161 | 32.2 | 149 | 29.8 |

| 71+ | 60 | 12.0 | 38 | 7.6 |

| Education | ||||

| Primary and vocational | 16 | 3.2 | 56 | 11.2 |

| Secondary | 187 | 37.4 | 283 | 56.6 |

| Higher | 297 | 59.4 | 161 | 32.2 |

| Place of Residence | ||||

| Rural area | 150 | 30.0 | 119 | 23.8 |

| Cities up to 19,999 | 85 | 17.0 | 76 | 15.2 |

| Cities above20,000 to 99,999 | 95 | 19.0 | 86 | 17.2 |

| Cities above100,000 to 499,999 | 87 | 17.4 | 112 | 22.4 |

| Cities above 500.000 | 83 | 16.6 | 107 | 21.4 |

| Household Income; Poland | ||||

| Under 1000 PLN | 46 | 9.2 | - | - |

| 1001 PLN–1500 PLN | 67 | 13.4 | - | - |

| 1501 PLN–2500 PLN | 146 | 29.2 | - | - |

| 2501 PLN–4000 PLN | 164 | 32.8 | - | - |

| 4001 PLN or more | 77 | 15.4 | - | - |

| Household Income; UK | ||||

| Under £1200 | - | - | 110 | 22.0 |

| £1201–£1800 | - | - | 130 | 26.0 |

| £1801–£2500 | - | - | 101 | 20.2 |

| £2501–£3500 | - | - | 92 | 18.4 |

| £3500 or more | - | - | 67 | 13.4 |

| Period | Poland (n = 500) | UK (n = 500) | p-Value * |

|---|---|---|---|

| less than 1 month | 4 (0.8%) | 33 (6.6%) | <0.01 |

| from month to 1 year | 43 (8.6%) | 61 (12.2%) | |

| 1 to 5 years | 229 (45.8%) | 120 (24.0%) | |

| 5 to 10 years | 154 (30.8%) | 55 (11.0%) | |

| more than 10 years | 70 (14.0%) | 231 (46.2%) |

| Products | Average 1/ | p Value | Average for Polish and British Population | |

|---|---|---|---|---|

| A | dairy products | 3.63 | 0.0029 |  |

| B | cereal products | 3.12 | 0.0685 | |

| C | sweets and biscuits | 3.24 | <0.01 | |

| D | Bakery | 3.42 | <0.01 | |

| E | meat and cold meat | 3.24 | <0.01 | |

| F | fruits and vegetables | 3.48 | <0.01 | |

| G | fruit and vegetable products | 3.06 | 0.0730 | |

| H | non-alcoholic beverages | 3.34 | 0.1109 | |

| I | Alcohol | 2.33 | <0.01 | |

| J | frozen food | 3.29 | <0.01 |

| Factors for Purchasing PL Products | Average 1/ | p-Value | Correlation | Average for Clusters | |||

|---|---|---|---|---|---|---|---|

| UK | Poland | Whole Population | |||||

| A | wide product range | 3.56 | 3.31 | 3.44 | 0.0000 |  | |

| B | lower price compared to leading brands | 3.83 | 4.02 | 3.92 | 0.0003 | ||

| C | high product quality | 3.57 | 3.27 | 3.42 | 0.0000 | ||

| D | ability to buy the same products repeatedly | 3.71 | 3.72 | 3.71 | 0.9036 | ||

| E | availability of PL products in every store of a particular chain | 3.67 | 3.73 | 3.70 | 0.2393 | ||

| F | attachment to a given chain | 3.50 | 3.62 | 3.56 | 0.0241 | ||

| G | feeling of safety and trust to PL products | 3.57 | 3.47 | 3.52 | 0.0518 | ||

| H | recognisability of PLs among consumers | 3.55 | 3.37 | 3.46 | 0.0011 | ||

| Specification | Cluster 1 | Cluster 2 | Cluster 3 | Cluster 4 | Chi Square (χ2) | p-Value | Cramer Correlations |

|---|---|---|---|---|---|---|---|

| Poland (n = 500) | 241 (48.2%) | 198 (39.6%) | 33 (6.6%) | 28 (5.6%) | 12.46 | 0.0049 | 0.112 |

| UK (n = 500) | 202 (40.4%) | 201 (40.2%) | 66 (13.2%) | 31 (6.2%) | |||

| Total (n = 1000) | 443 (44.3%) | 399 (39.9%) | 99 (9.9%) | 59 (5.9%) |

| Opinions on the Current Development of the PL Product Range | Average 1/ | p-Value | Correlation | Average for Clusters | |||

|---|---|---|---|---|---|---|---|

| UK | Poland | Whole Population | |||||

| A | improvement in the quality of PL products | 3.81 | 4.07 | 3.94 | 0.0000 |  | |

| B | increase in the range of products offered under PL | 3.73 | 3.90 | 3.81 | 0.0007 | ||

| C | improved visual presentation of PL products | 3.52 | 3.70 | 3.61 | 0.0007 | ||

| D | lower price of PL products while retaining quality | 3.92 | 4.19 | 4.05 | 0.0000 | ||

| E | greater availability of PL products | 3.72 | 3.87 | 3.80 | 0.0036 | ||

| F | improved image/perception of PL products | 3.67 | 3.87 | 3.77 | 0.0002 | ||

| Specification | Cluster 1 | Cluster 2 | Cluster 3 | Cluster 4 | Chi Square (χ2) | p-Value | Cramer Correlations |

|---|---|---|---|---|---|---|---|

| Poland (n = 500) | 218 (43.6%) | 118 (23.6%) | 67 (13.4%) | 97 (19.4%) | 42.56 | 0.0001 | 0.2063 |

| UK (n = 500) | 156 (31.2%) | 111 (22.2%) | 149 (29.8%) | 84 (16.8%) | |||

| Total (n = 1000) | 374 (37.4%) | 229 (22.9%) | 216 (21.6%) | 181 (18.1%) |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Czeczotko, M.; Górska-Warsewicz, H.; Laskowski, W. Towards Sustainable Private Labels—What is the Consumer Behavior Relating to Private Labels in the UK and Poland? Sustainability 2020, 12, 6035. https://doi.org/10.3390/su12156035

Czeczotko M, Górska-Warsewicz H, Laskowski W. Towards Sustainable Private Labels—What is the Consumer Behavior Relating to Private Labels in the UK and Poland? Sustainability. 2020; 12(15):6035. https://doi.org/10.3390/su12156035

Chicago/Turabian StyleCzeczotko, Maksymilian, Hanna Górska-Warsewicz, and Wacław Laskowski. 2020. "Towards Sustainable Private Labels—What is the Consumer Behavior Relating to Private Labels in the UK and Poland?" Sustainability 12, no. 15: 6035. https://doi.org/10.3390/su12156035

APA StyleCzeczotko, M., Górska-Warsewicz, H., & Laskowski, W. (2020). Towards Sustainable Private Labels—What is the Consumer Behavior Relating to Private Labels in the UK and Poland? Sustainability, 12(15), 6035. https://doi.org/10.3390/su12156035