The EU Food Label ‘Protected Geographical Indication’: Economic Implications and Their Spatial Dimension

Abstract

1. Introduction

- It originates in a specific place, region, or country;

- the quality, reputation, or other characteristic of the product are essentially attributable to that geographical origin; and

- at least one of the production steps takes place in the defined geographical area (Article 5 (2) of EU Regulation 1151/2012).

- Beer: Bayerisches Bier PGI;

- asparagus: Franken-Spargel PGI, Schrobenhausener Spargel PGI;

- carp: Aischgründer Karpfen PGI, Oberpfälzer Karpfen PGI.

2. Market Success of Products of Protected Origin

2.1. Price-Related Arguments

2.2. Sales-Related Arguments

2.3. Geographical Origin as ‘Key Information’ for the Consumer

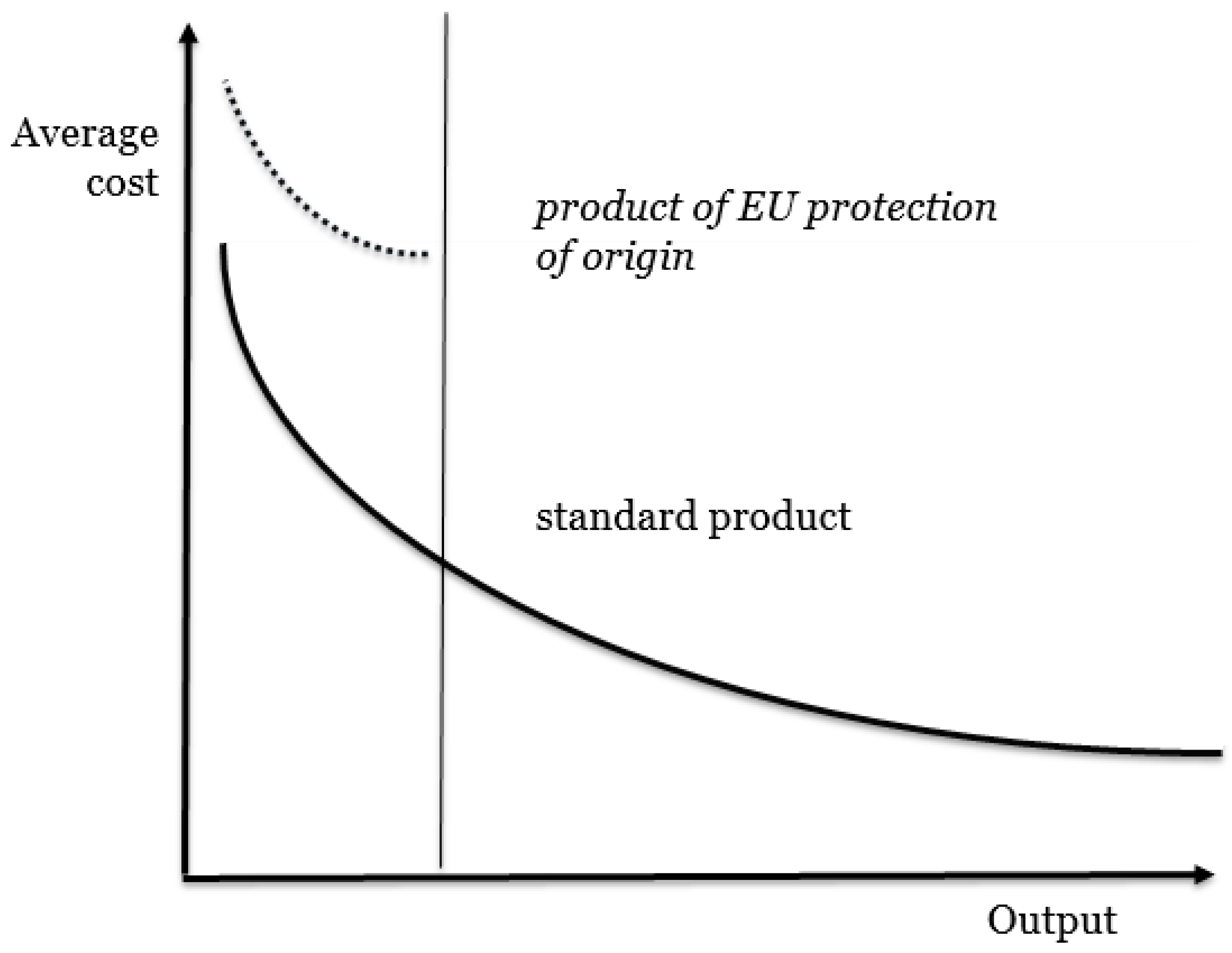

2.4. Economies of Scale

- Firstly, the possible quantity of production is limited due to product-specific and geographical definitions. To give a concrete example, Allgäuer Sennalpkäse PDO can be produced in significantly smaller quantities than ‘Bergkäse’ (mountain cheese) in general, due to its small reference area and the few cheese producers located in the area. ‘Bergkäse’, on the other hand, can also be produced entirely outside of the mountains (Allgäu and others).

- Secondly, higher average costs per produced unit is a potential result. More specific and complex production methods can come with a greater appreciation of these products by consumers and thus higher prices.

2.5. Research Focus

3. Methodology

- To what extent do the experts confirm the secondary statistical analyses as presented (in the graphics shown during the interviews)?

- What motives are most important for implementing geographical indication?

- To what extent is the economic performance of the products linked to the European protection policy? Which other factors also have an impact, and to what extent?

- What price differences can be instated between a protected product and an unprotected product with similar product characteristics?

- How have sales volume, turnover, and price of the protected product developed since its registration?

4. Results

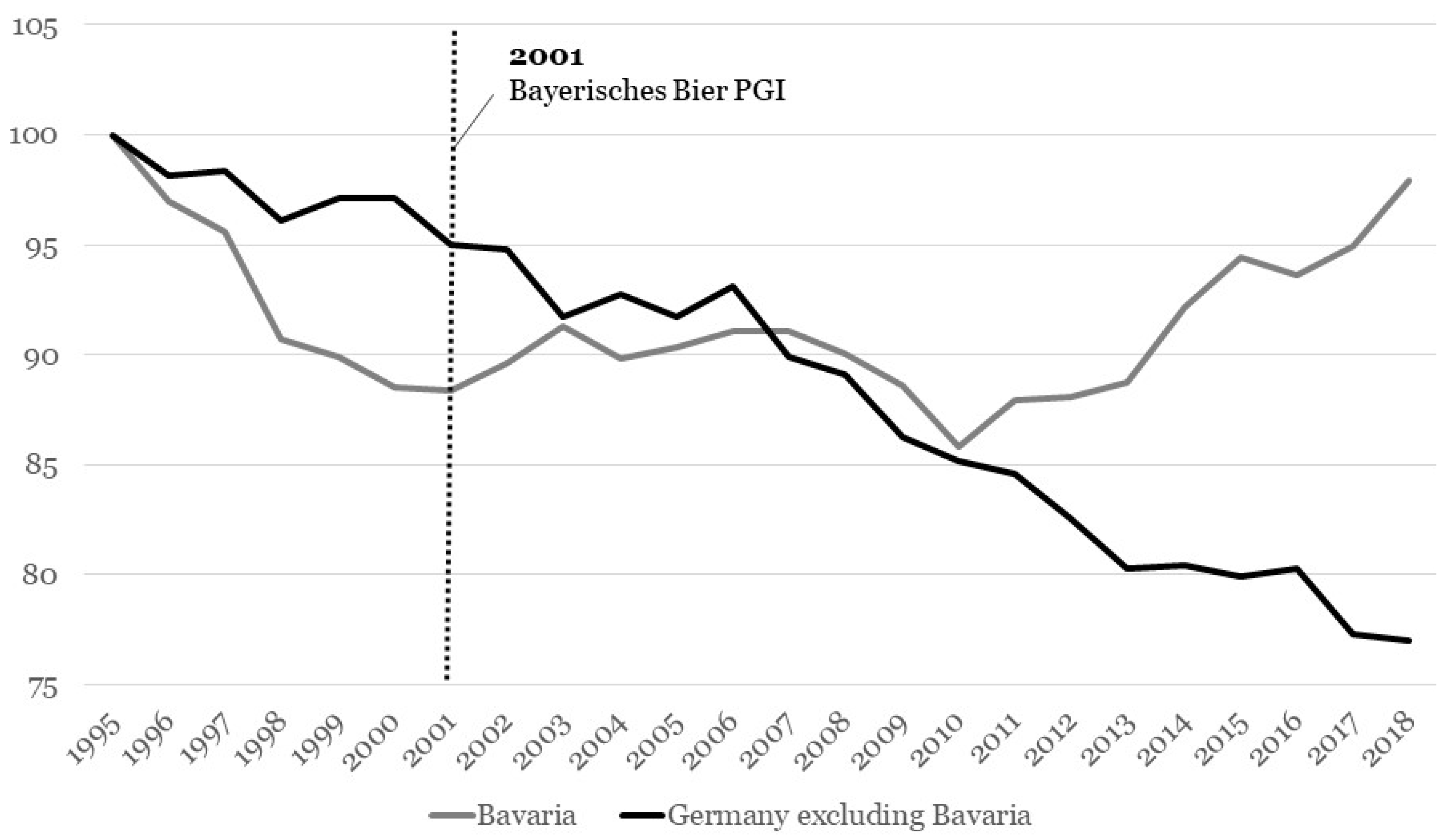

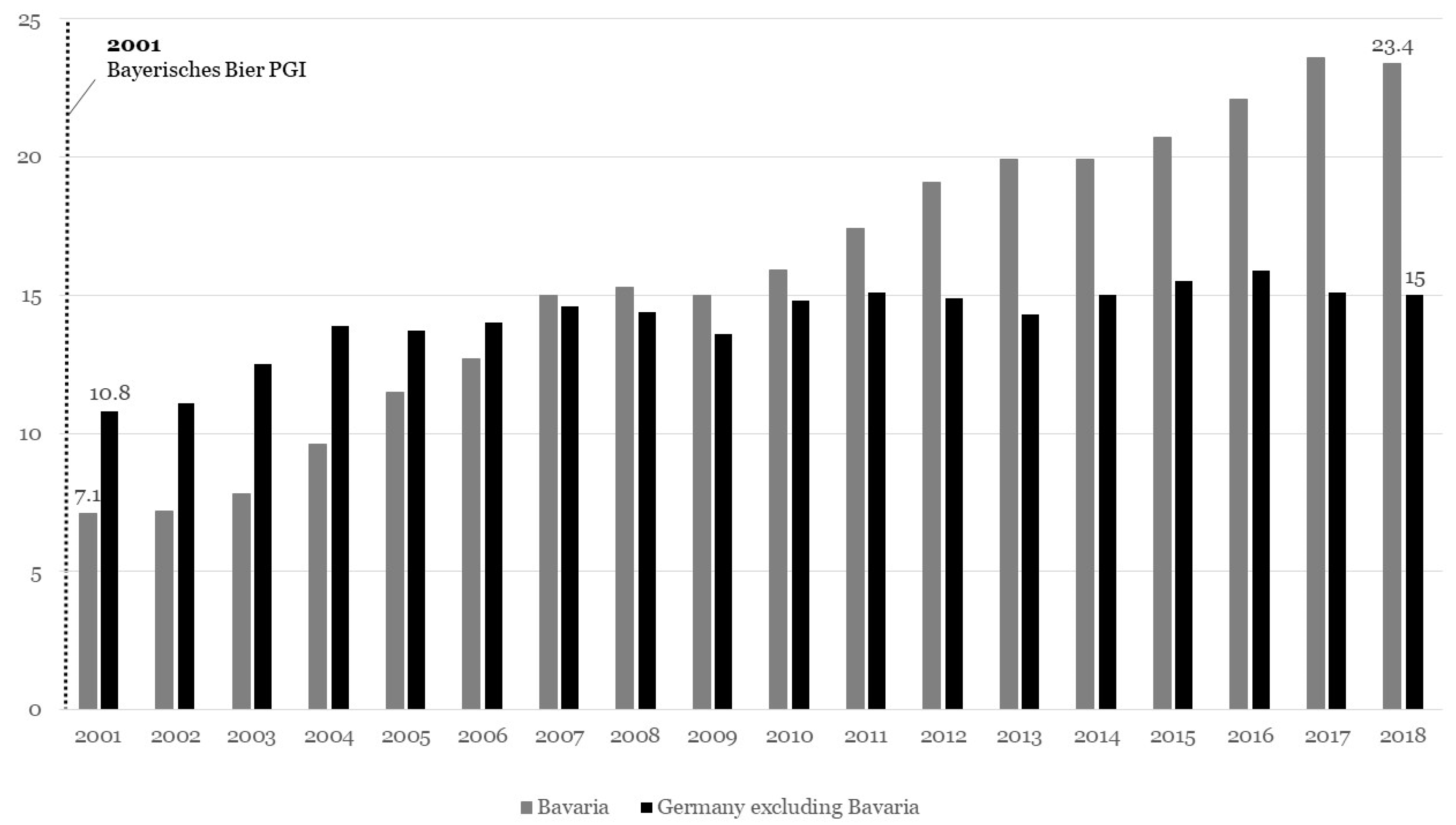

4.1. Beer

4.1.1. Market Context and Protection of Origin

4.1.2. Economic Effects

Sales Development

Price Development

The Role of Consumer Information

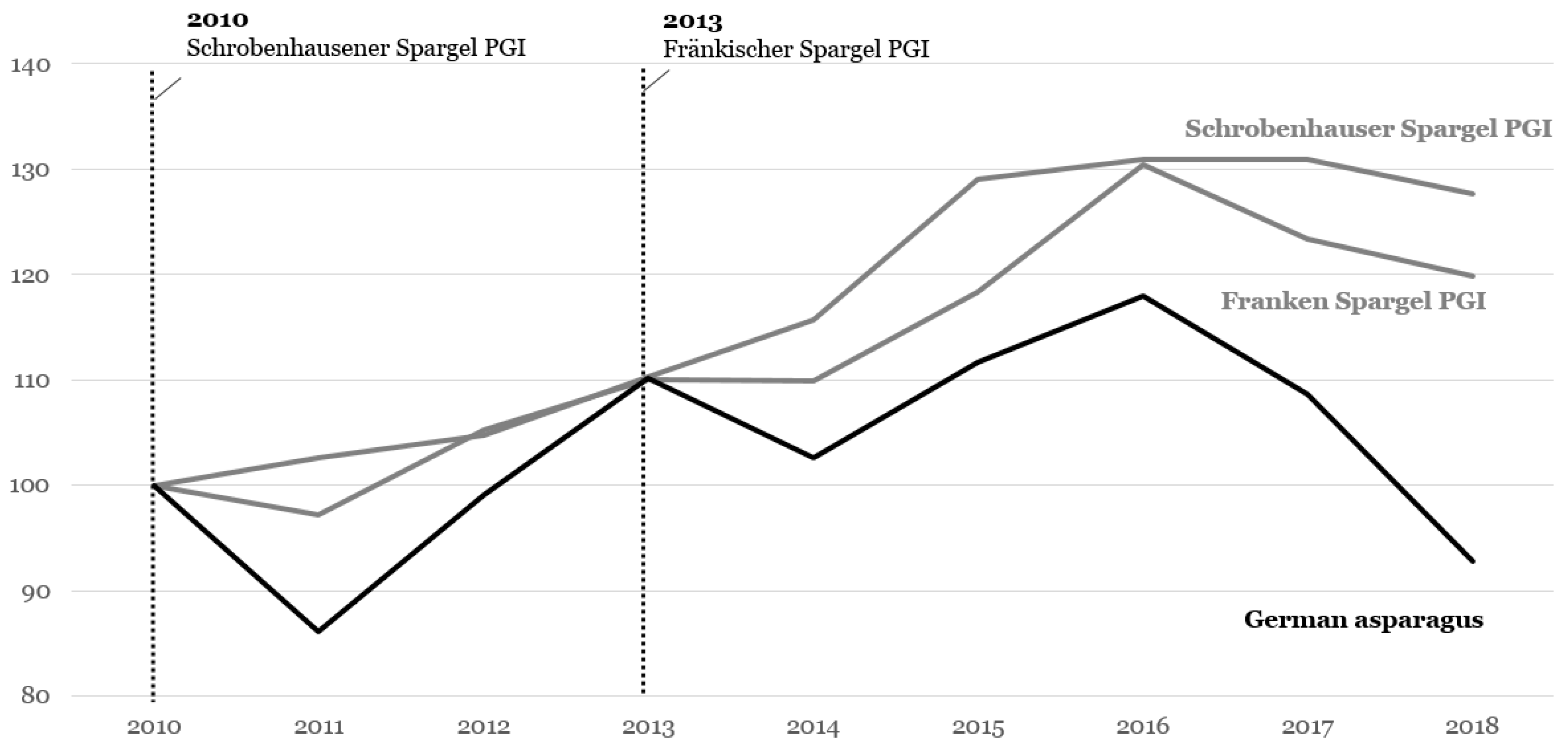

4.2. Asparagus

4.2.1. Market Context and Protection of Origin

4.2.2. Economic Effects

Sales Development

Price Development

The Role of Consumer Information

4.3. Carp

4.3.1. Market Context and Protection of Origin

4.3.2. Economic Effects

Sales Development

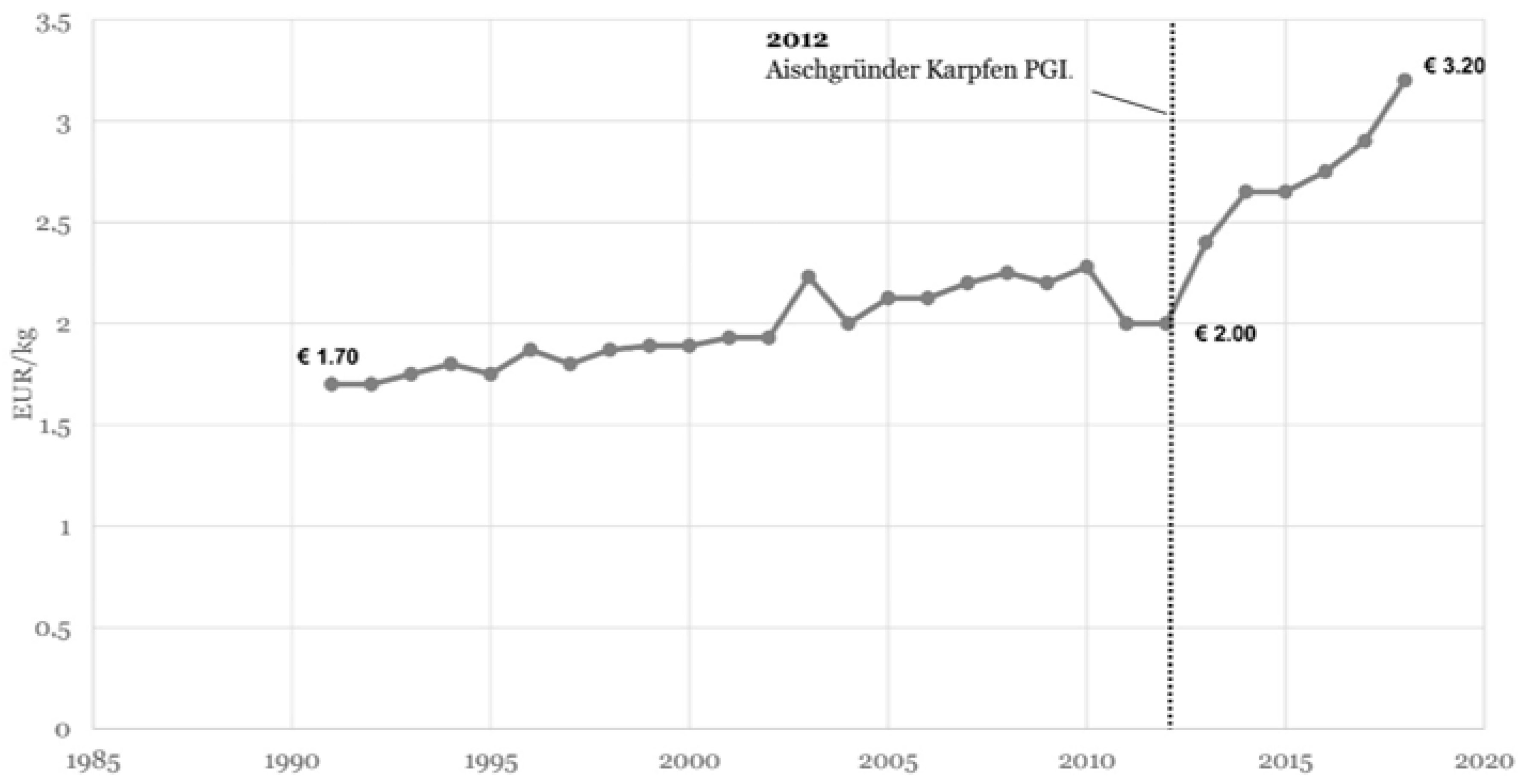

Price Development

The Role of Consumer Information

5. Discussion and Conclusion

5.1. Comparative Perspective

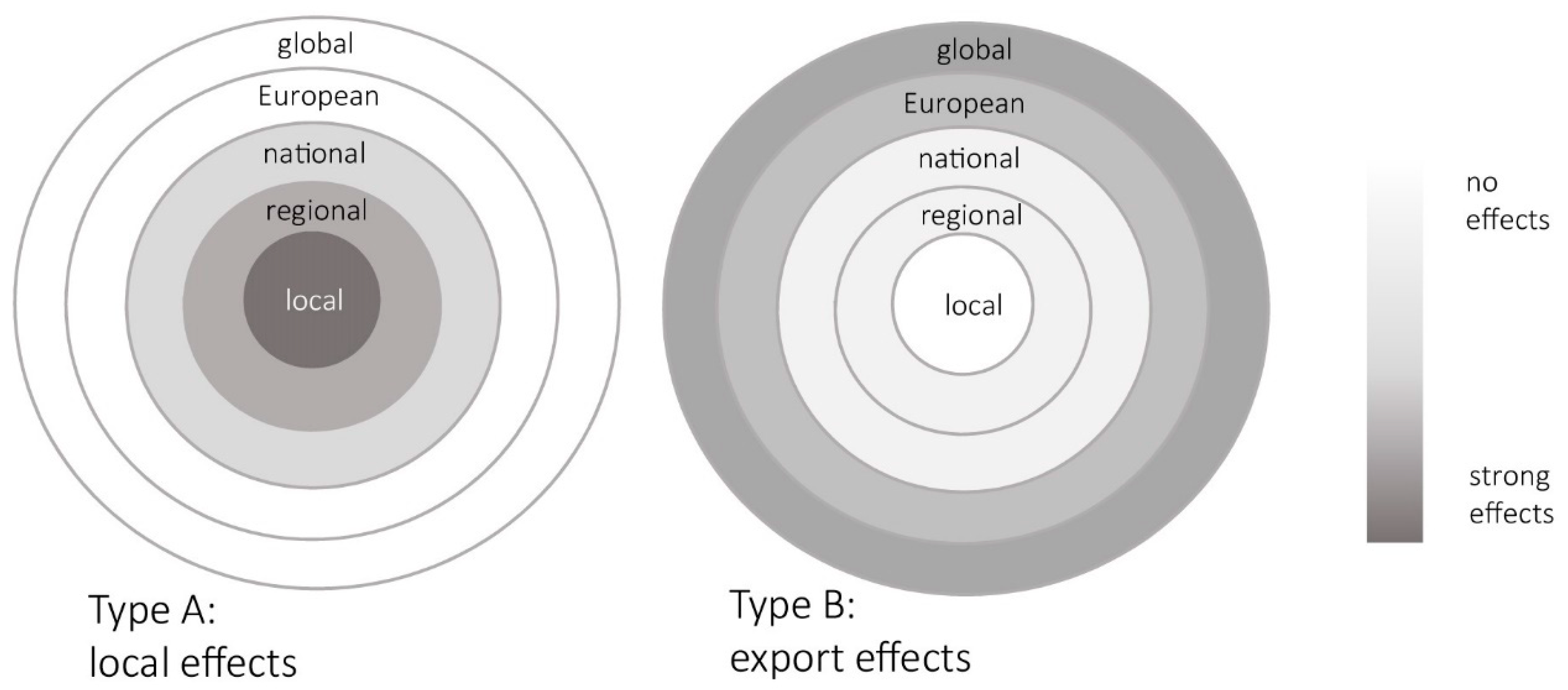

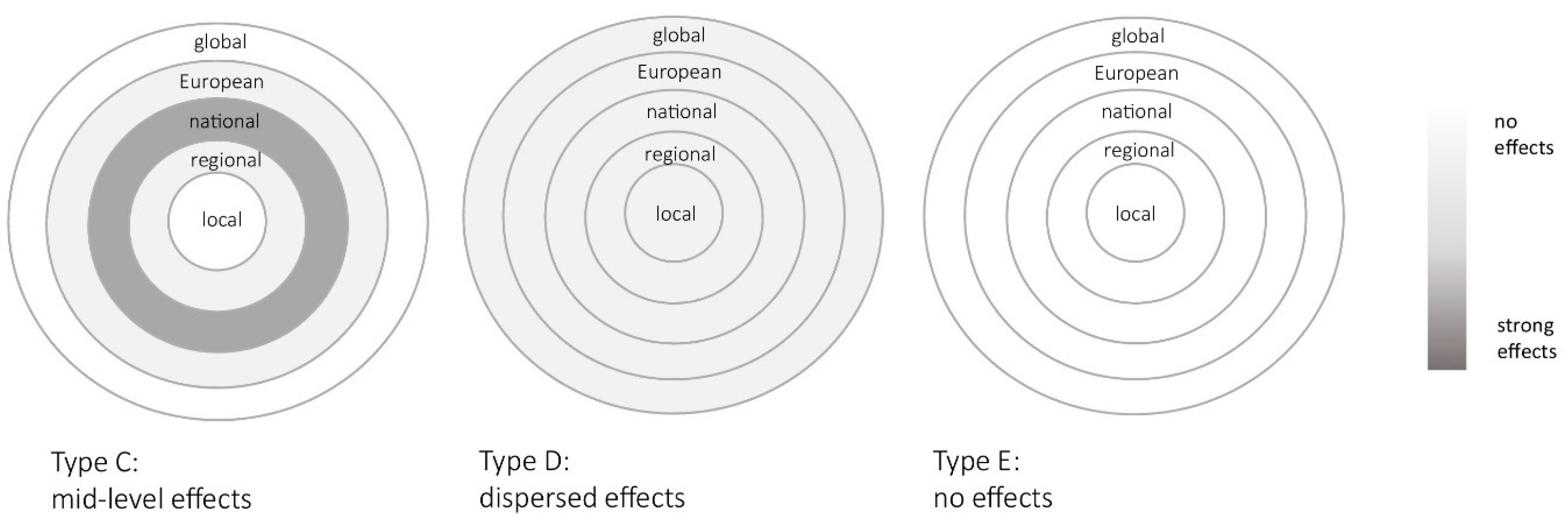

5.2. ‘Price and Sales Geography’: Spatial Characteristics of Economic Effects

5.3. Conclusion and Outlook

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- AND-International. Study on Economic Value of EU Quality Schemes, Geographical Indications (GIs) and Traditional Specialities Guaranteed (TSGs), Final Report. Available online: https://op.europa.eu/en/publication-detail/-/publication/a7281794-7ebe-11ea-aea8-01aa75ed71a1 (accessed on 22 June 2020).

- Török, Á.; Moir, H.V.J. The market size for GI food products—Evidence from the empirical economic literature. Stud. Agric. Econ. 2018, 120, 134–142. [Google Scholar] [CrossRef]

- Consors Finanz. Konsumbarometer—Global Denken, Regional Handeln, Study. Available online: https://www.consorsfinanz.de/unternehmen/studien/Konsumbarometer/Studien/PDF_Konsumbarometer/Konsumbarometer_2019.pdf (accessed on 22 June 2020).

- European Food Safety Authority. Food safety in the EU, Special Eurobarometer 2019. Available online: https://www.efsa.europa.eu/sites/default/files/corporate_publications/files/Eurobarometer2019_Food-safety-in-the-EU_Full-report.pdf (accessed on 21 June 2020).

- Arfini, F.; Capelli, M.G. The resilient character of PDO/PGI products in dynamic food markets. In Proceedings of the 113th Seminar, Chania, Crete, Greece, 3–6 September 2009. [Google Scholar]

- Tiberio, L.; Francisco, D. Agri-food traditional products: From certification to the market—Portuguese recent evolution. Reg. Sci. Inq. 2012, 4, 57–86. [Google Scholar]

- Profeta, A.; Balling, R.; Schoene, V.; Wirsig, A. Protected Geographical Indications and Designations of Origin: An Overview of the Status Quo and the Development of the Use of Regulation (EC) 510/06 in Europe, With Special Consideration of the German Situation. J. Int. Food Agribus. Mark. 2010, 22, 179–198. [Google Scholar] [CrossRef]

- Schober, K. Das Herkunftsschutzsystem für Agrarprodukte und Lebensmittel der Europäischen Union. Ein Instrument der nachhaltigen Regionalentwicklung. Unpublished Master’s Thesis, University of Erlangen-Nürnberg, Erlangen, Germany, 2015. [Google Scholar]

- Drivas, K.; Iliopoulos, C. An Empirical Investigation in the Relationship Between PDOs/PGIs and Trademarks. J. Knowl. Econ. 2017, 8, 585–595. [Google Scholar] [CrossRef]

- London Economics. Evaluation of the CAP Policy on Protected Designations of Origin (PDO) and Protected Geographical Indications (PGI); Final Report; Study financed by the European Commission; London Ecomomics: London, England, 2008. [Google Scholar]

- Voss, J.; Spiller, A. Der EU-Herkunftsschutz—Eine Perspektive für Wurst und Fleischspezialitäten? In Zukunftsperspektiven der Fleischwirtschaft. Verbraucher, Märkte, Geschäftsbeziehungen; Spiller, A., Schulze, B., Eds.; Niedersächsische Staats- und Universitätsbibliothek, Univ.-Verl. Göttingen: Göttingen, Germany, 2008. [Google Scholar]

- Menapace, L.; Moschini, G. Quality certification by geographical indications, trademarks and firm reputation. Eur. Rev. Agric. Econ. 2012, 39, 539–566. [Google Scholar] [CrossRef]

- Belletti, G.; Burgassi, T.; Manco, E.; Marescotti, A.; Pacciani, A.; Scaramuzzi, S. The roles of geographical indications (PDO and PGI) on the internationalisation process of agro-food products. In Proceedings of the 105th Seminar, Bologna, Italy, 8–10 March 2007. [Google Scholar]

- Cei, L.; Defrancesco, E.; Stefani, G. From Geographical Indications to Rural Development: A Review of the Economic Effects of European Union Policy. Sustainability 2018, 10, 3745. [Google Scholar] [CrossRef]

- Biénabe, E.; Marie-Vivien, D. Institutionalizing Geographical Indications in Southern Countries: Lessons Learned from Basmati and Rooibos. World Dev. 2017, 98, 58–67. [Google Scholar] [CrossRef]

- Albert, J. Innovations in Food Labelling; Food and Agriculture Organization of the United Nations: Rome, Italy; Cambridge, UK; Boca Raton, FL, USA, 2010. [Google Scholar]

- Vandecandelaere, E.; Teyssier, C.; Barjolle, D.; Jeanneaux, P.; Fournier, S.; Beucherie, O. Strengthening Sustainable Food Systems Through Geographical Indications: An Analysis of Economic Impacts; FAO: Rome, Italy, 2018. [Google Scholar]

- Vandecandelaere, E.; Arfini, F.; Belletti, G.; Marescotti, A. Linking People, Places and Products: A Guide for Promoting Quality Linked to Geographical Origin and Sustainable Geographical Indications; FAO: Rome, Italy, 2009. [Google Scholar]

- Marescotti, A.; Quiñones-Ruiz, X.F.; Edelmann, H.; Belletti, G.; Broscha, K.; Altenbuchner, C.; Penker, M.; Scaramuzzi, S. Are Protected Geographical Indications Evolving Due to Environmentally Related Justifications? An Analysis of Amendments in the Fruit and Vegetable Sector in the European Union. Sustainability 2020, 12, 3571. [Google Scholar] [CrossRef]

- European Commission. eAmbrosia—The EU Geographical Indications Register. 2020. Available online: https://ec.europa.eu/info/food-farming-fisheries/food-safety-and-quality/certification/quality-labels/geographical-indications-register/ (accessed on 19 June 2019).

- Thiedig, F. Spezialitäten Mit Geographischer Herkunftsangabe: Marketing, Rechtlicher Rahmen Und Fallstudien; Zugl.: Munich, Germany, 2003; reprinted by Lang: Frankfurt am Main, Germany in 2004. [Google Scholar]

- Barjolle, D.; Sylvander, B. Some factors of success for origin labelled products in agri-food supply chains in Europe; market, internal resources and institutions. In Proceedings of the 67th EAAE Seminar, Le Mans, France, 28–30 October 1999. [Google Scholar]

- Deutsches Institut für Wirtschaftsforschung. Höhere Qualität von Lebensmitteln durch gesetzlich geschützte Herkunftsangaben. DIW Wochenber. 2007, 74, 377–382. [Google Scholar]

- Torok, A.; Jambor, A. Determinants of the revealed comparative advantages: The case of the European ham trade. Agric. Econ. Czech 2016, 62, 471–482. [Google Scholar]

- Profeta, A.; Wirsig, A. Mehr Dynamik im Regal Durch Herkunftsschutz. Available online: http://www.terra-fusca.de/fileadmin/user_upload/2009_Profeta_SG_Interview.pdf (accessed on 21 June 2020).

- May, S. Geografische Herkunftsangaben Als Kulturelles Eigentum: Praktiken Der Propertisierung und Inwertsetzung von Europäischen Käsespezialitäten. Ph.D. Thesis, University of Tübingen, Tübingen, Germany, 2017. [Google Scholar]

- Carbone, A.; Caswell, J.; Galli, F.; Sorrentino, A. The Performance of Protected Designations of Origin: An Ex Post Multi-Criteria Assessment of the Italian Cheese and Olive Oil Sectors. J. Agric. Food Ind. Organ. 2014, 12, 121–140. [Google Scholar] [CrossRef]

- Agostino, M.; Trivieri, F. Geographical indication and wine exports. An empirical investigation considering the major European producers. Food Policy 2014, 46, 22–36. [Google Scholar] [CrossRef]

- Agostino, M.; Trivieri, F. European Wines Exports Towards Emerging Markets. The Role of Geographical Identity. J. Ind. Compet. Trade 2016, 16, 233–256. [Google Scholar] [CrossRef]

- AND-International. Value of Production of Agricultural Products and Foodstuffs, Wines, Aromatised Wines and Spirits Protected by a Geographical Indication (GI). Commissioned by the European Commission. 2012. Available online: https://op.europa.eu/en/publication-detail/-/publication/32b62342-b151-4bf3-8ba8-18568f37f43b (accessed on 22 June 2020).

- Huber, F. Relevanz bayerischer Produkte mit europäischem Herkunftsschutz. Unpublished Master’s (Master of Science) Thesis, Technical University of Munich, Munich, Germany, 2018. [Google Scholar]

- Hassan, D.; Monier-Dilhan, S.; Orozco, V. Measuring Consumers’ Attachment to Geographical Indications. J. Agric. Food Ind. Organ. 2011, 9, 1–28. [Google Scholar] [CrossRef]

- Strecker, O.; Strecker, O.A.; Elles, A.; Weschke, H.-D.; Kliebisch, C.; Enneking, U. Marketing Für Lebensmittel Und Agrarprodukte, 4th ed.; DLG-Verl.: Frankfurt am Main, Germany, 2010. [Google Scholar]

- Ferrer-Pérez, H.; Abdelradi, F.; Gil, J.M. Geographical Indications and Price Volatility Dynamics of Lamb Prices in Spain. Sustainability 2020, 12, 3048. [Google Scholar] [CrossRef]

- Lence, S.H.; Marette, S.; Hayes, D.J.; Foster, W. Collective Marketing Arrangements for Geographically Differentiated Agricultural Products: Welfare Impacts and Policy Implications. Am. J. Agric. Econ. 2007, 89, 947–963. [Google Scholar] [CrossRef]

- Moschini, G.; Menapace, L.; Pick, D. Geographical Indications and the Competitive Provision of Quality in Agricultural Markets. Am. J. Agric. Econ. 2008, 90, 794–812. [Google Scholar] [CrossRef]

- Deconinck, K.; Huysmans, M.; Swinnen, J.F.M. The Political Economy of Geographical Indications. SSRN Scholarly Paper ID 2671764: Rochester, NY, USA. 2015. Available online: https://econpapers.repec.org/paper/liclicosd/37215.htm (accessed on 7 July 2020).

- Yu, J.; Bouamra-Mechemache, Z. Production standards, competition and vertical relationship. Eur. Rev. Agric. Econ. 2016, 43, 79–111. [Google Scholar] [CrossRef]

- Marette, S.; Crespi, J.M. Can Quality Certification Lead to Stable Cartels? Rev. Ind. Organ. 2003, 23, 43–64. [Google Scholar] [CrossRef]

- Teuber, R. Consumers’ and producers’ expectations towards geographical indications. Br. Food J. 2011, 113, 900–918. [Google Scholar] [CrossRef]

- Wirsig, A.; Profeta, A.; Häring, A.; Lenz, A. Indigenous species, traditional and local knowledge and intellectual property rights. In Proceedings of the 9th European IFSA Symposium, Vienna, Austria, 4–7 July 2010; pp. 1721–1730. [Google Scholar]

- Balogh, J.M.; Jámbor, A. Determinants of revealed comparative advantages: The case of cheese trade in the European Union. Acta Aliment. 2017, 46, 305–311. [Google Scholar] [CrossRef]

- Kizos, T.; Vakoufaris, H. Valorisation of a local asset: The case of olive oil on Lesvos Island, Greece. Food Policy 2011, 36, 705–714. [Google Scholar] [CrossRef]

- Tregear, A.; Török, Á.; Gorton, M. Geographical indications and upgrading of small-scale producers in global agro-food chains: A case study of the Makó Onion Protected Designation of Origin. Environ. Plan A 2016, 48, 433–451. [Google Scholar] [CrossRef]

- Galli, F.; Carbone, A.; Caswell, J.A.; Sorrentino, A. A Multi-Criteria Approach to Assessing PDOs/PGIs: An Italian Pilot Study. Special issue on sustainability in the food sector. Int. J. Food Syst. Dyn. 2011, 2, 219–236. [Google Scholar]

- Török, Á.; Jámbor, A. Competitiveness and Geographical Indications: The case of fruit spirits in Central and Eastern European countries. Stud. Agric. Econ. 2013, 115, 25–32. [Google Scholar] [CrossRef]

- Raimondi, V.; Falco, C.; Curzi, D.; Olper, A. Trade effects of geographical indication policy: The EU case. J. Agric. Econ. 2020, 71, 330–356. [Google Scholar] [CrossRef]

- Huysmans, M.; Curzi, D. The impact of protecting EU Geographical Indications in trade agreements. In Proceedings of the 94th Annual Conference, Leuven, Belgium, 15–17 April 2020. [Google Scholar]

- Schirrmann, E.; Holzmüller, H.H. Lokale Produktherkunft Und Konsumentenverhalten: Der Einfluss Der City-of-Origin Auf Die Kaufentscheidung, 1st ed.; Dt. Univ.-Verl.: Wiesbaden, Germany, 2005. [Google Scholar]

- Bardají, I.; Iráizoz, B.; Rapún, M. Protected geographical indications and integration into the agribusiness system. Agribusiness 2009, 25, 198–214. [Google Scholar] [CrossRef]

- Profeta, A.; Enneking, U.; Balling, R. Wahrnehmung von regionalen Lebensmittelspezialitäten in Deutschland—Eine repräsentative Konsumentenbefragung. Ber. über Landwirtsch. 2007, 85, 238–251. [Google Scholar]

- European Commission. Under preparation. A Farm to Fork Strategy. For a fair, healthy and environmentally-friendly food system. Communication from the Commission. Unpublished work. 2020. [Google Scholar]

- Dentoni, D.; Menozzi, D.; Capelli, M.G. Heterogeneity of Members’ Characteristics and Cooperation within Producer Groups Regulating Geographical Indications: The Case of the “Prosciutto di Parma” Consortium. In Proceedings of the 116th Seminar, Parma, Italy, 27–30 October 2010. [Google Scholar]

- Dentoni, D.; Menozzi, D.; Capelli, M.G. Group heterogeneity and cooperation on the geographical indication regulation: The case of the “Prosciutto di Parma” Consortium. Food Policy 2012, 37, 207–216. [Google Scholar] [CrossRef]

- Chilla, T. Maßnahmen und Strategien zur Etablierung von ‚Nischenprodukten‘. Eine vergleichende Analyse von Allgäuer Sennalpkäse, Aischgründer Karpfen, Bamberger Hörnla, Fränkischem Gelbvieh, Laufener Landweizen und Rhönschaf, Erlangen, Germany. Unpublished Study. 2019. [Google Scholar]

- Bayerische Staatskanzlei. Bericht aus der Kabinettssitzung vom 02. Juli 2019 | Bayerisches Landesportal. 2019. Available online: https://www.bayern.de/bericht-aus-der-kabinettssitzung-vom-02-juli-2019/ (accessed on 10 June 2020).

- Balling, R. Genuss Schätze. Besondere Produkte in Bayern. In Proceedings of the Fachtagung Treffen der Kulinarischen Schatzbewahrer Bayerns, Regensburg, Germany, 29 May 2019. [Google Scholar]

- Agentur für Lebensmittel Produkte aus Bayern. Spezialitaetenland Bayern—EU-Herkunftszeichen. 2019. Available online: https://www.spezialitaetenland-bayern.de/schutz/eu-herkunftszeichen/ (accessed on 10 June 2020).

- Statistisches Bundesamt. Finanzen und Steuern. Brauwirtschaft. 2018. 2019. Available online: https://www.destatis.de/DE/Themen/Staat/Steuern/Verbrauchsteuern/Publikationen/Downloads-Verbrauchsteuern/brauwirtschaft-2140922187005.xlsx?__blob=publicationFile (accessed on 19 June 2020).

- Bayerische Landesanstalt für Landwirtschaft (LfL). Agrarmärkte 2016, Fisch; Bayerische Landesanstalt für Landwirtschaft: Freising-Weihenstephan, Germany, 2017; pp. 349–360. [Google Scholar]

- Agrarmarkt Informations-Gesellschaft. AMI Markt Bilanz Gemüse 2016. Anbau, Produktion, Absatz und Preise von Spargel in Deutschland; Agrarmarkt Informations-Gesellschaft mbH: Bonn, Germany, 2016; p. 129. [Google Scholar]

- Spargelerzeugerverband Franken e.V. 2019. Entwicklung des Spargelanbaus in Bayern. 2019. Available online: https://www.spargel-franken.de/docs/Spargelanbau_Entwicklung_und_Preise_Stand_Juni_2019.pdf (accessed on 19 June 2020).

- Jakob, W. Risiken der Regionalvermarktung. Available online: https://www.fischjakob.de/userfiles/downloads/Fisch_Jakob_seafood_2019.pdf (accessed on 19 June 2020).

- Barth-Haas Group. Barth-Bericht Hopfen 2018/2019. Available online: https://www.barthhaas.com/aktuelles/der-neue-barth-bericht-hopfen-2018-2019-ist-veroeffentlicht (accessed on 22 June 2020).

- Statistisches Bundesamt. Biersteuerstatistik. Absatz von Bier, Betriebe Braustätten, Verbrauch von Bier. Deutschland., Zeitraum 1993–2018. 2019. Available online: https://www-genesis.destatis.de/genesis/online?language=de&sequenz=tabelleErgebnis&selectionname=73421-0001 (accessed on 19 June 2020).

- Deutscher Brauer-Bund. Die deutsche Brauwirtschaft in Zahlen 2008. 2009. Available online: http://dev.brauerbund.de/download/Archiv/PDF/statistiken/Die%20deutsche%20Brauwirtschaft%20in%20Zahlen%202008.pdf (accessed on 11 March 2020).

- Statistisches Bundesamt. Finanzen und Steuern. Brauwirtschaft. 2014. 2015. Available online: https://www.destatis.de/GPStatistik/servlets/MCRFileNodeServlet/DEHeft_derivate_00022166/2140922157005.xlsx;jsessionid=1F1D8237F8717BFDC3927F5046B9EE3E (accessed on 19 June 2020).

- Bayerischer Brauerbund. Der Biermarkt. Die Struktur der Bayerischen Brauwirtschaft; Bayerischer Brauerbund e.V.: Munich, Germany, 2017. [Google Scholar]

- The Brewers of Europe. Beer Statistics—2018 and Previous Years; The Brewers of Europe: Brussels, Belgium, 2018. [Google Scholar]

- Ermann, U. Brauereien in Deutschland: Vom lokalen zum globalen Bier—Und wieder zurück? Nationalatlas aktuell. 2019. Available online: http://aktuell.nationalatlas.de/Brauereien.3_04-2019.0.html/ (accessed on 10 June 2020).

- Interview 2. Empirical Research, Interviewer Benedikt Fink, Munich, Germany. 29 April 2019.

- Bayerische Landesanstalt für Landwirtschaft (LfL); Institut für Ernährung und Markt. Liste der Hersteller, die die geschützte geographische Angabe „Bayerisches Bier g.g.A.“nutzen und in das Kontrollsystem aufgenommen sind. 2018. Available online: https://www.lfl.bayern.de/mam/cms07/iem/dateien/2019_03_13_herstellerliste_bayerisches_bier.pdf (accessed on 19 June 2020).

- Interview 1. Empirical Research, Interviewer Benedikt Fink, Munich, Germany. 21 May 2019.

- Interview 4. Empirical Research, Interviewer Benedikt Fink, interview by phone, Erlangen, Germany. 10 April 2019.

- Bayerischer Brauerbund. Entwicklung des Exportanteils am Gesamtbierabsatz Bayern und Deutschland ohne Bayern in %. 2020. Available online: https://www.bayerisches-bier.de/bier-wissen/absatz-und-ausstos/ (accessed on 12 March 2020).

- Interview 3. Empirical Research, Interviewer Benedikt Fink, district of Weißenburg-Gunzenhausen, Germany. 19 June 2019.

- Bayerische Landesanstalt für Landwirtschaft (LfL). Agrarmärkte 2018, Gemüse; Bayerische Landesanstalt für Landwirtschaft: Freising-Weihenstephan, Germany, 2019; pp. 120–140. [Google Scholar]

- Interview 5. Empirical Research, Interviewer Benedikt Fink, interview by phone, Erlangen, Germany. 20 September 2019.

- Bayerische Landesanstalt für Landwirtschaft (LfL). Erosionsschutzbeim Anbau von Spargel; Bayerische Landesantstalt für Landwirtschaft: Freising-Weihenstephan, Germany, 2017; pp. 1–12. [Google Scholar]

- Sutor, P. Für und Wider der Folie im Spargelanbau …aus Sicht des Marktes. In Proceedings of the the 11th Produkttag Spargel, Weichering, Germany, 20 February 2019. [Google Scholar]

- Food and Agricultural Organiziation of the United Nations. FAOSTAT. Asparagus. Production of Asparagus: Top 10 Producers; Food and Agricultural Organiziation of the United Nations: Rome, Italy, 2017. [Google Scholar]

- Interview 6. Empirical Research, Interviewer Benedikt Fink, district of Neuburg-Schrobenhausen, Germany. 18 July 2019.

- Bundesanstalt für Landwirtschaft und Ernährung (BLE). Spargel: 1,7 kg pro Kopf im Wirtschaftsjahr 2017/2018 verbraucht; Bundesanstalt für Landwirtschaft und Ernährung: Bonn, Germany, 2019; Available online: https://www.ble.de/SharedDocs/Pressemitteilungen/DE/2019/190418_Spargel.html (accessed on 19 June 2020).

- Statistisches Bundesamt. Erntemenge (Gemüse und Erdbeeren): Deutschland, Jahre, Gemüsearten auf dem Freiland. 2019. Available online: https://www-genesis.destatis.de/genesis//online?operation=table&code=412150001&levelindex=0&levelid=1586355548741 (accessed on 19 June 2020).

- DBV. Frühstart in die Spargelsaison 2019. 2019. Available online: https://www.bauernverband.de/presse-medien/pressemitteilungen/pressemitteilung/fruehstart-in-die-spargelsaison-2019 (accessed on 10 June 2020).

- Bätzing, W. Nutzungskonflikte zwischen Teichwirtschaft, Naturschutz und Freizeitinteressen im Aischgrund. Probleme und Potenziale bei der Aufwertung des “Aischgründer Karpfens” zum Qualitätsregionalprodukt. Available online: http://fgg-erlangen.de/fgg/ojs/index.php/mfgg/article/download/265/245 (accessed on 15 June 2020).

- Ermann, U. Regionalprodukte: Vernetzungen Und Grenzziehungen Bei Der Regionalisierung Von Nahrungsmitteln; Zugl.: Erlangen-Nürnberg, Univ.: Erlangen, Germany, 2003; reprinted by Steiner: Stuttgart, Germany, 2005. [Google Scholar]

- Statistisches Bundesamt. Betriebe mit Erzeugung in Aquakultur, Erzeugte Menge. Available online: https://www.destatis.de/DE/Themen/Branchen-Unternehmen/Landwirtschaft-Forstwirtschaft-Fischerei/Fischerei/Tabellen/aqua-betriebe-menge.html (accessed on 19 June 2020).

- Bayerische Landesanstalt für Landwirtschaft (LfL). Der Karpfen als Motor für die Gastronomie einer ganzen Region. 2019. Available online: https://www.lfl.bayern.de/ifi/karpfenteichwirtschaft/030859/index.php (accessed on 10 June 2020).

- Bayerische Landesanstalt für Landwirtschaft (LfL). Arbeitsbereich Karpfenteichwirtschaft. 2019. Available online: https://www.lfl.bayern.de/ifi/karpfenteichwirtschaft/030014/index.php (accessed on 10 June 2020).

- Sächsische Landesanstalt für Landwirtschaft. Karpfenteichwirtschaft. Bewirtschaftung von Karpfenteichen. Gute fachliche Praxis. 2007. Available online: https://publikationen.sachsen.de/bdb/artikel/13764/documents/15974 (accessed on 7 July 2020).

- Interview 8. Empirical Research, Interviewer Benedikt Fink, district of Schwandorf, Germany. 11 July 2019.

- Interview 7. Empirical Research, Tobias Chilla and Benedikt, district of Erlangen-Höchstädt, Germany. 2 April 2019.

- European Commission. €200 Million to Promote European Agri-Food Products in and outside the EU. 2020. Available online: https://ec.europa.eu/commission/presscorner/detail/en/IP_19_6287 (accessed on 10 June 2020).

- Reviron, S.; Chappius, J.-M. Geographical Indicaitons: Collective Organization and Management. In Labels of Origin for Food: Local Development, Global Recognition; Sylvander, B., Barham, E., Eds.; CABI: Cambridge, MA, USA, 2011; pp. 45–62. [Google Scholar]

- Biénabe, E.; Vermeulen, H.; Bramley, C. The food “quality turn” in South Africa: An initial exploration of its implications for small-scale farmers’ market access. Agrekon 2011, 50, 36–52. [Google Scholar] [CrossRef]

- Babcock, B.A.; Roxanne, C. Geographical Indications and Property Rights: Protecting Value-Added Agricultural Products, Midwest Agribusiness Trade: Research and Information Center (MATRIC); Publications Center for Agricultural and Rural Development (CARD) at Iowa State University: Ames, IA, USA, 2004. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Product Type | Protected Product | Protection Since | Area of Origin |

|---|---|---|---|

| Beer | Bayerisches Bier PGI | 2001 | Federal State of Bavaria |

| Asparagus | Schrobenhausener Spargel PGI | 2010 | 3 municipal districts (Landkreise Neuburg-Schrobenhausen, Aichach-Friedberg, Pfaffenhofen a.d. Ilm) |

| Franken-Spargel PGI | 2013 | 3 regional districts (Bezirke Ober-, Mittel-, Unterfranken) | |

| Carp | Aischgründer Karpfen PGI | 2012 | 13 Municipal districts along the Aischgrund (Landkreise Erlangen-Höchstadt, Neustadt a.d. Aisch, Bad Windsheim, Fürth, Kitzingen, Bamberg, Forchheim Nürnberger Land and the cities of Erlangen, Forchheim, Bamberg, Nürnberg, and Fürth) |

| Oberpfälzer Karpfen PGI | 2002 | 1 regional district (Oberpfalz) |

| Bayerisches Bier PGI | Aischgründer Karpfen PGI | Oberpfälzer Karpfen PGI | Franken-Spargel PGI | Schrobenhausener Spargel PGI | |

|---|---|---|---|---|---|

| Price effects | Neutral | Very positive | Fairly positive | Neutral to price-stabilizing | Price-stabilizing to price-increasing |

| Sales effects | Positive, especially in export | [Unclear] | Increasing sales | Promotion in retail and gastronomy, not in direct sales | Sales-stabilizing |

| Role in consumer information | Product definition abroad/fraud prevention | Image improvement on local/regional level | Image improvement on local/regional level | [Unclear] | Protection against misuse of names/fraud prevention |

| Geographic dimension | Negligible in the region of origin, but clear effects abroad | Clear local effects, but not beyond | Low impact in direct marketing, but higher in sales to food retail, wholesale, gastronomy | Notable local and regional effects | |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Chilla, T.; Fink, B.; Balling, R.; Reitmeier, S.; Schober, K. The EU Food Label ‘Protected Geographical Indication’: Economic Implications and Their Spatial Dimension. Sustainability 2020, 12, 5503. https://doi.org/10.3390/su12145503

Chilla T, Fink B, Balling R, Reitmeier S, Schober K. The EU Food Label ‘Protected Geographical Indication’: Economic Implications and Their Spatial Dimension. Sustainability. 2020; 12(14):5503. https://doi.org/10.3390/su12145503

Chicago/Turabian StyleChilla, Tobias, Benedikt Fink, Richard Balling, Simon Reitmeier, and Karola Schober. 2020. "The EU Food Label ‘Protected Geographical Indication’: Economic Implications and Their Spatial Dimension" Sustainability 12, no. 14: 5503. https://doi.org/10.3390/su12145503

APA StyleChilla, T., Fink, B., Balling, R., Reitmeier, S., & Schober, K. (2020). The EU Food Label ‘Protected Geographical Indication’: Economic Implications and Their Spatial Dimension. Sustainability, 12(14), 5503. https://doi.org/10.3390/su12145503