Organizational Learning and Corporate Social Responsibility Drivers of Performance in SMEs in Northwestern Mexico

Abstract

:1. Introduction

- Is OLE a determining factor in the increase in CSR practices and in the results of financial performance of the SME? Does CSR have significant effects on the financial performance of the SME;

- Is OLE a variable that has mediation effects between CSR and the financial performance of the SME;

- Of the dimensions of CSR, on which does OLE have most influence?

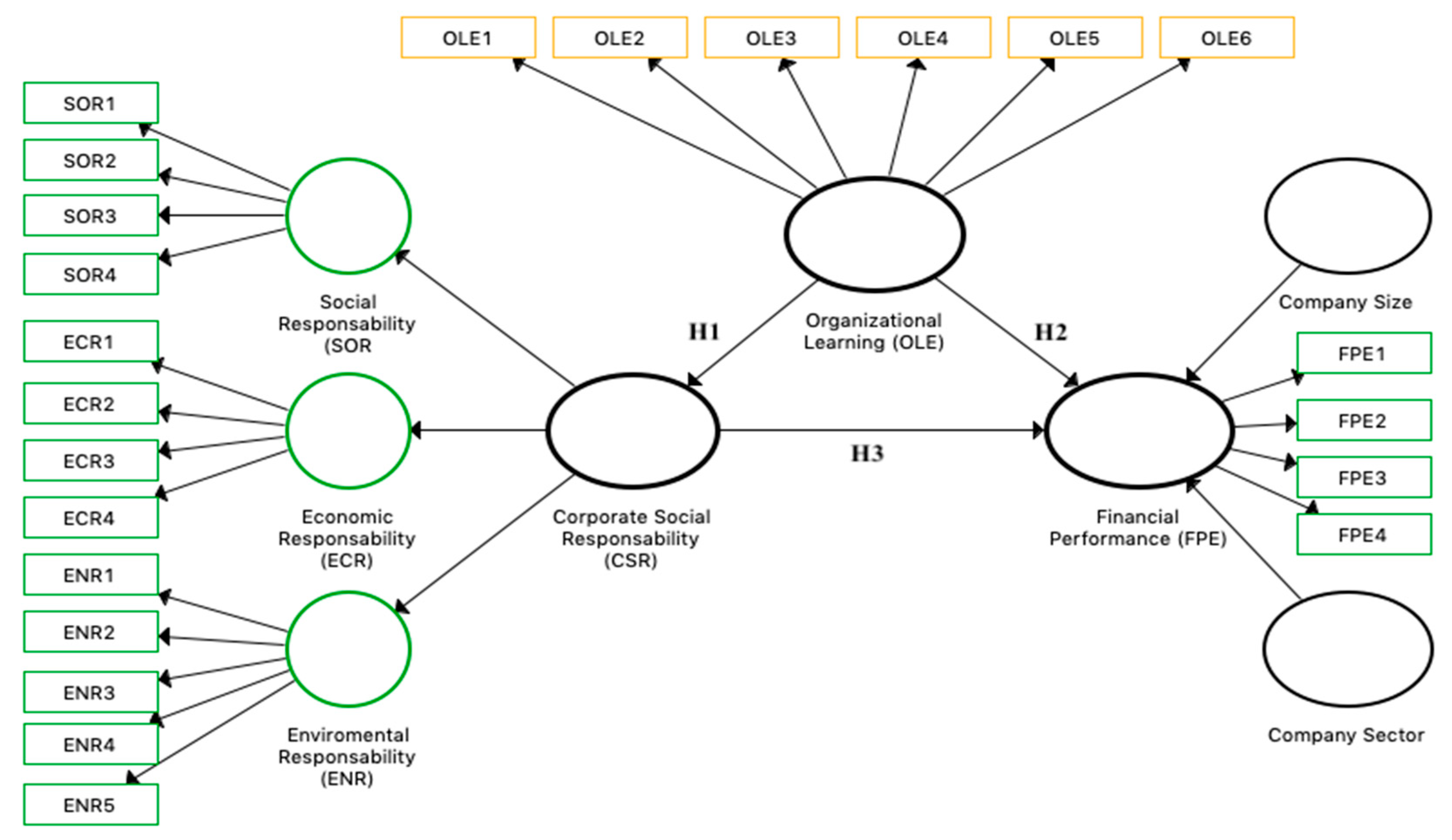

2. Literature Review and Hypothesis Development

2.1. Organizational Learning and Social Responsibility

2.2. Organizational Learning and Corporate Social Responsibility

2.3. Organizational Learning and Financial Performance

2.4. The Relationship of CSR with Financial Performance

3. Materials and Methods

3.1. Participants and Sampling Technique

3.2. Variance Test of the Common Method (CMV)

3.3. Variable Measurement

3.4. Control Variables

3.5. Reliability and Validity

4. Results

4.1. Measurement Model

4.2. Item Reliability

4.3. Construct Reliability

4.4. Convergent Validity

4.5. Discriminant Validity

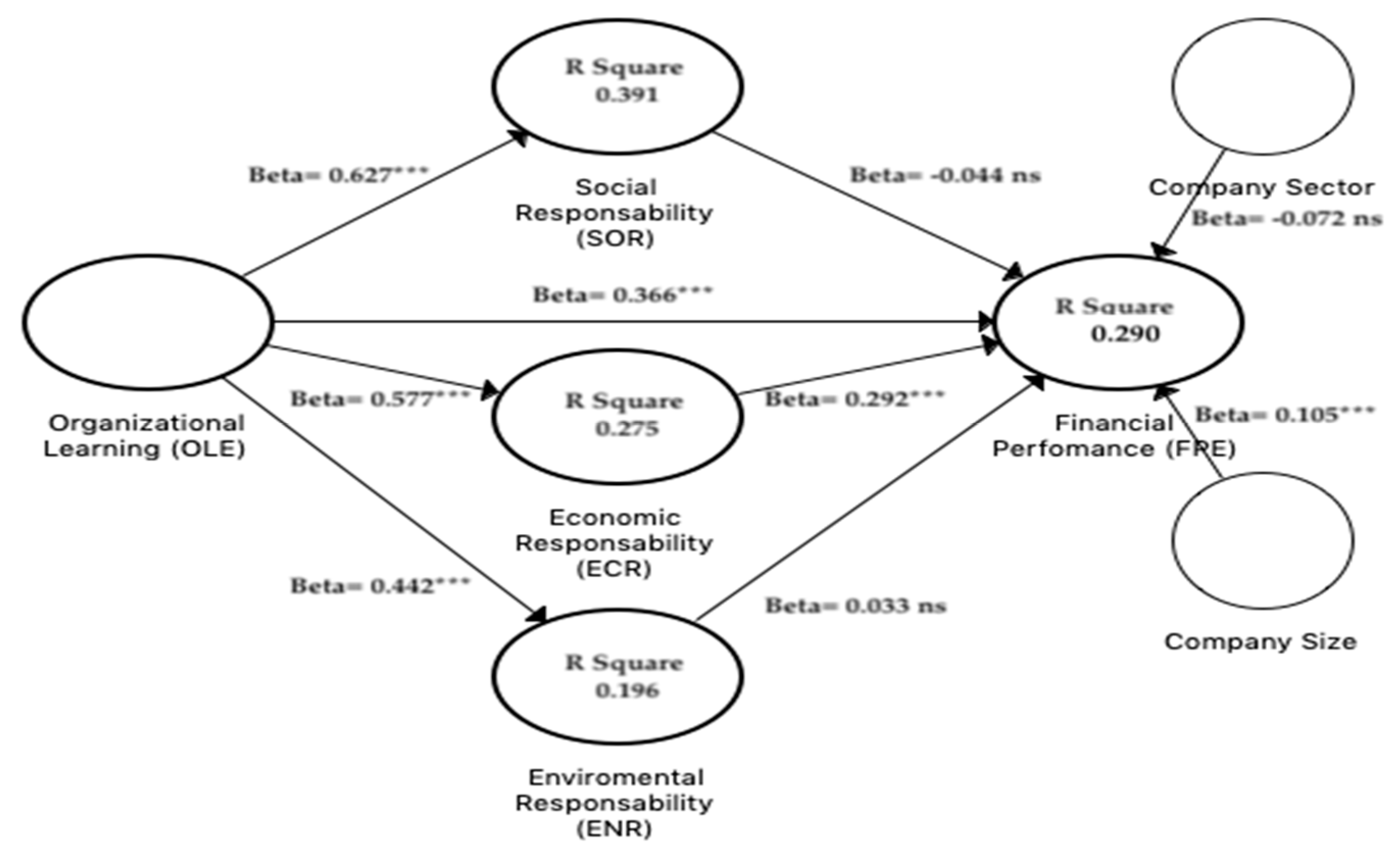

4.6. Structural Model

4.7. Mediation Analysis

4.8. Alternative Model 1

4.9. Alternative Model 2

5. Discussion

6. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- McCormick, K.; Kautto, N. The Bioeconomy in Europe: An Overview. Sustainability 2013, 5, 2589–2608. [Google Scholar] [CrossRef] [Green Version]

- Clinton, L.; Whisnant, R. Business Model Innovations for Sustainability. In Managing Sustainable Business; Springer: Dordrecht, The Netherlands, 2019; pp. 467–507. [Google Scholar]

- Andreeva, T.; Ritala, P. What are the sources of capability dynamism? Reconceptualizing dynamic capabilities from the perspective of organizational change. Balt. J. Manag. 2016, 11, 238–259. [Google Scholar] [CrossRef]

- Bontis, N.; Crossan, M.M.; Hulland, J. Managing an Organizational Learning System by Aligning Stocks and Flows. J. Manag. Stud. 2002, 39, 437–469. [Google Scholar] [CrossRef]

- Bontis, N.; Ciambotti, M.; Palazzi, F.; Sgro, F. Intellectual capital and financial performance in social cooperative enterprises. J. Intellect. Cap. 2018, 19, 712–731. [Google Scholar] [CrossRef]

- Nonaka, I. The knowledge-creating company. Harv. Bus. Rev. 2007, 85, 162. [Google Scholar]

- Diaz-Fernandez, M.; Pasamar-Reyes, S.; Valle-Cabrera, R. Human capital and human resource management to achieve ambidextrous learning: A structural perspective. BRQ Bus. Res. Q. 2015, 20, 63–77. [Google Scholar] [CrossRef]

- March, J.G. Exploration and Exploitation in Organizational Learning. Organ. Sci. 1991, 2, 71–87. [Google Scholar] [CrossRef]

- Zahra, S.A.; Zheng, C.; Yu, J. Learning advantages of newness: A reconceptualization and contingent framework. J. Int. Entrep. 2017, 16, 12–37. [Google Scholar] [CrossRef]

- McWilliams, A.; Siegel, D.S. Creating and Capturing Value. J. Manag. 2011, 37, 1480–1495. [Google Scholar] [CrossRef]

- Serenko, A.; Bontis, N.; Hardie, T. Organizational size and knowledge flow: A proposed theoretical link. J. Intellect. Cap. 2007, 8, 610–627. [Google Scholar] [CrossRef]

- Yu, Y.; Dong, X.Y.; Shen, K.N.; Khalifa, M.; Hao, J.X. Strategies, technologies, and organizational learning for developing organizational innovativeness in emerging economies. J. Bus. Res. 2013, 66, 2507–2514. [Google Scholar] [CrossRef]

- UNESCO. Human Learning in the Digital Era; UNESCO Publishing: París, France, 2019. [Google Scholar]

- OECD Organization for Economic Cooperation and Development. Employment Outlook 2018; OCED Publishing: Paris, France, 2018; p. 3. ISBN 9789264301788. [Google Scholar]

- Bank, W. Doing Business 2019: Training for Reform; World Bank Group: Wshington, DC, USA, 2018. [Google Scholar]

- Dror, I.E.; Makany, T.; Kemp, J. Overcoming learning barriers through knowledge management. Dyslexia 2011, 17, 38–47. [Google Scholar] [CrossRef] [PubMed]

- Thomä, J. DUI mode learning and barriers to innovation—A case from Germany. Res. Policy 2017, 46, 1327–1339. [Google Scholar] [CrossRef]

- Mourtzis, D.; Boli, N.; Dimitrakopoulos, G.; Zygomalas, S.; Koutoupes, A. Enabling Small Medium Enterprises (SMEs) to improve their potential through the Teaching Factory paradigm. Procedia Manuf. 2018, 23, 183–188. [Google Scholar] [CrossRef]

- Crossan, M.M.; Lane, H.W.; White, R.E. An Organizational Learning Framework: From Intuition to Institution. Acad. Manag. Rev. 1999, 24, 522–537. [Google Scholar] [CrossRef]

- Siebenhüner, B.; Arnold, M. Organizational learning to manage sustainable development. Bus. Strategy Environ. 2007, 16, 339–353. [Google Scholar] [CrossRef]

- Engert, S.; Rauter, R.; Baumgartner, R.J. Exploring the integration of corporate sustainability into strategic management: A literature review. J. Clean. Prod. 2016, 112, 2833–2850. [Google Scholar] [CrossRef]

- Freeman, R.E. Strategic Management: A Stakeholder Approach; Cambridge University Press: New York, NY, USA, 2010. [Google Scholar]

- McWilliams, A.; Parhankangas, A.; Coupet, J.; Welch, E.; Barnum, D.T. Strategic Decision Making for the Triple Bottom Line. Bus. Strategy Environ. 2016, 25, 193–204. [Google Scholar] [CrossRef]

- Barney, J.B.; Ketchen, D.J.; Wright, M. The future of resource-based theory: Revitalization or decline? J. Manag. 2011, 37, 1299–1315. [Google Scholar] [CrossRef]

- Teece, D.J. Business models, business strategy and innovation. Long Range Plan. 2010, 43, 172–194. [Google Scholar] [CrossRef]

- Spender, J.-C. Organizational knowledge, learning and memory: Three concepts in search of a theory. J. Organ. Chang. Manag. 1996, 9, 63–78. [Google Scholar] [CrossRef]

- Davenport, T.H. Personal Knowledge Management and Knowledge Worker Capabilities. In Personal Knowledge Management; Routledge: Abingdon-on-Thames, UK, 2016; pp. 189–210. [Google Scholar]

- Cameron, K.; Quinn, R. Diagnosing and Changing Organizational Culture. Based on the Competing Values Framework; Jossey-Bass Business & Management Series; John Wiley & Sons: Hoboken, NJ, USA, 2006. [Google Scholar]

- Huber, G.P. Organizational Learning: The Contributing Processes and the Literatures. Organ. Sci. 1991, 2, 88–115. [Google Scholar] [CrossRef]

- Nonaka, I.; von Krogh, G. Perspective—Tacit Knowledge and Knowledge Conversion: Controversy and Advancement in Organizational Knowledge Creation Theory. Organ. Sci. 2009, 20, 635–652. [Google Scholar] [CrossRef]

- Argote, L.; Miron-Spektor, E. Organizational Learning: From Experience to Knowledge. Organ. Sci. 2011, 22, 1123–1137. [Google Scholar] [CrossRef]

- Namada, J.M. Organizational learning and competitive advantage. In Handbook of Research on Knowledge Management for Contemporary Business Environments; Malheiro, A., Ribeiro, F., Jamil, G.L., Rascao, G.P., Mealha, O., Eds.; IGI Global: Hershey, PA, USA, 2018; pp. 86–104. [Google Scholar]

- Nonaka, I.; Takeuchi, H. The Knowledge-Creation Company; Oxford University Press: New York, NY, USA, 1995; ISBN 019-509269-4. [Google Scholar]

- Slater, S.F.; Narver, J.C. Market Orientation and the Learning Organization. J. Mark. 1995, 59, 63–74. [Google Scholar] [CrossRef]

- Cohen, W.M.; Levinthal, D.A. Absorptive Capacity: A New Perspective on Learning and Innovation. Adm. Sci. Q. 1990, 35, 128–152. [Google Scholar] [CrossRef]

- Zahra, S.A.; George, G. Absorptive capacity: A review, reconceptualization, and extension. Acad. Manag. Rev. 2002, 27, 185–203. [Google Scholar] [CrossRef]

- Mcafee, A.; Brynjolfsson, E. HBR. ORG Spotlight on Big Data Big Data: The Management Revolution; Harvard Business Publishing: Cambridge, MA, USA, 2012. [Google Scholar]

- Jensen, M.B.; Johnson, B.; Lorenz, E.; Lundvall, B.-Å.; Lundvall, B.A. Forms of knowledge and modes of innovation. In The Learning Economy and the Economics of Hope; Anthem Press: London, UK, 2007; Volume 155. [Google Scholar]

- Kim, D.H. The link between individual and organizational learning. MIT Sloan Manag. Rev. 1993, 35, 37–50. [Google Scholar]

- Todorova, G.; Durisin, B. Absorptive capacity: Valuing a reconceptualization. Acad. Manag. Rev. 2007, 32, 774–786. [Google Scholar] [CrossRef]

- Maon, F.; Lindgreen, A.; Swaen, V. Organizational Stages and Cultural Phases: A Critical Review and a Consolidative Model of Corporate Social Responsibility Development. Int. J. Manag. Rev. 2010, 12, 20–38. [Google Scholar] [CrossRef]

- Wood, D.J. Corporate Social Performance Revisited. Acad. Manag. Rev. 1991, 16, 691–718. [Google Scholar] [CrossRef]

- Ma, L.; Ferguson, J.D.; Roper, M.; Wood, M.; Wilson, J. A collaborative approach to learning programming: A hybrid learning model. In Proceedings of the 6th Annual Higher Education Academy Subject Network for Information Computer Science Conference, York, UK, 30 August–1 September 2005. [Google Scholar]

- Zadek, S. The Path to Corporate Responsibility. In Corporate Ethics and Corporate Governance; Springer: Berlin/Heidelberg, Germany, 2007; pp. 159–172. [Google Scholar]

- Zhao, Z.; Meng, F.; He, Y.; Gu, Z. The Influence of Corporate Social Responsibility on Competitive Advantage with Multiple Mediations from Social Capital and Dynamic Capabilities. Sustainability 2019, 11, 218. [Google Scholar] [CrossRef]

- Bontis, N.; Wu, S.; Wang, W.-Y.; Chang, C. Intellectual capital and performance in causal models: Evidence from the information technology industry in Taiwan. J. Intellect. Cap. 2005, 6, 222–236. [Google Scholar]

- Lozano, R. Creativity and Organizational Learning as Means to Foster Sustainability. Sustain. Dev. 2014, 22, 205–216. [Google Scholar] [CrossRef]

- Carroll, A.B. Carroll’s pyramid of CSR: Taking another look. Int. J. Corp. Soc. Responsib. 2016, 1, 3. [Google Scholar] [CrossRef]

- Carroll, A.B.; Shabana, K.M. The Business Case for Corporate Social Responsibility: A Review of Concepts, Research and Practice. Int. J. Manag. Rev. 2010, 12, 85–105. [Google Scholar] [CrossRef]

- Cohen, S.; Kaimenakis, N. Intellectual capital and corporate performance in knowledge-intensive SMEs. Learn. Organ. 2007, 14, 241–262. [Google Scholar] [CrossRef]

- Jiménez-Jiménez, D.; Sanz-Valle, R. Innovation, organizational learning, and performance. J. Bus. Res. 2011, 64, 408–417. [Google Scholar] [CrossRef]

- von Weltzien Hoivik, H. Embedding CSR as a learning and knowledge creating process: The case for SMEs in Norway. J. Manag. Dev. 2011, 30, 1067–1084. [Google Scholar] [CrossRef]

- Fortis, Z.; Maon, F.; Frooman, J.; Reiner, G. Unknown Knowns and Known Unknowns: Framing the Role of Organizational Learning in Corporate Social Responsibility Development. Int. J. Manag. Rev. 2018, 20, 277–300. [Google Scholar] [CrossRef]

- Gomes, G.; Wojahn, R.M. Organizational learning capability, innovation and performance: Study in small and medium-sized enterprises (SMES). Rev. Adm. 2017, 52, 163–175. [Google Scholar] [CrossRef]

- Kilpi, V.; Lorentz, H.; Solakivi, T.; Malmsten, J. The effect of external supply knowledge acquisition, development activities and organizational status on the supply performance of SMEs. J. Purch. Supply Manag. 2018, 24, 247–259. [Google Scholar] [CrossRef]

- Cavaleri, S.; Shabana, K. Rethinking sustainability strategies. J. Strategy Manag. 2018, 11, 2–17. [Google Scholar] [CrossRef]

- Dashwood, H.S. CSR norms and organizational learning in the mining sector. Corp. Gov. Int. J. Bus. Soc. 2012, 12, 118–138. [Google Scholar] [CrossRef]

- Mishra, D.R. Post-innovation CSR Performance and Firm Value. J. Bus. Ethics 2017, 140, 285–306. [Google Scholar] [CrossRef]

- Eikelenboom, M.; de Jong, G. The impact of dynamic capabilities on the sustainability performance of SMEs. J. Clean. Prod. 2019, 235, 1360–1370. [Google Scholar] [CrossRef]

- Lichtenthaler, U. Absorptive capacity, environmental turbulence, and the complementarity of organizational learning processes. Acad. Manag. J. 2009, 52, 822–846. [Google Scholar] [CrossRef]

- Swee Lin Tan, C.X.; Smyrnios, K.; Xiong, L. What drives learning orientation in fast growth SMEs? Int. J. Entrep. Behav. Res. 2014, 20, 324–350. [Google Scholar] [CrossRef]

- Real, J.C.; Roldán, J.L.; Leal, A. From Entrepreneurial Orientation and Learning Orientation to Business Performance: Analysing the Mediating Role of Organizational Learning and the Moderating Effects of Organizational Size. Br. J. Manag. 2014, 25, 186–208. [Google Scholar] [CrossRef]

- Battisti, M.; Beynon, M.; Pickernell, D.; Deakins, D. Surviving or thriving: The role of learning for the resilient performance of small firms. J. Bus. Res. 2019, 100, 38–50. [Google Scholar] [CrossRef]

- Friedman, M. The Social Responsibility of Business Is to Increase Its Profits. In Corporate Ethics and Corporate Governance; Zimmerli, W.C., Holzinger, M., Richter, K., Eds.; Springer: Berlin/Heidelberg, Germany, 2007; pp. 173–178. ISBN 978-3-540-70818-6. [Google Scholar]

- Herrera Madueño, J.; Larrán Jorge, M.; Lechuga Sancho, M.P.; Martínez-Martínez, D. Responsabilidad social en las pymes: Análisis exploratorio de factores explicativos. Rev. Contab. 2016, 19, 31–44. [Google Scholar] [CrossRef]

- Flammer, C. Does Corporate Social Responsibility Lead to Superior Financial Performance? A Regression Discontinuity Approach. Manag. Sci. 2015, 61, 2549–2568. [Google Scholar] [CrossRef] [Green Version]

- Nunes, M.F.; Park, C.L. Self-claimed sustainability: Building social and environmental reputations with words. Sustain. Prod. Consum. 2017, 11, 46–57. [Google Scholar] [CrossRef]

- Schramm-Klein, H.; Zentes, J.; Steinmann, S.; Swoboda, B.; Morschett, D. Retailer Corporate Social Responsibility Is Relevant to Consumer Behavior. Bus. Soc. 2016, 55, 550–575. [Google Scholar] [CrossRef]

- Berrone, P.; Surroca, J.; Tribó, J.A. Corporate Ethical Identity as a Determinant of Firm Performance: A Test of the Mediating Role of Stakeholder Satisfaction. J. Bus. Ethics 2007, 76, 35–53. [Google Scholar] [CrossRef]

- Torugsa, N.A.; O’Donohue, W.; Hecker, R. Proactive CSR: An Empirical Analysis of the Role of its Economic, Social and Environmental Dimensions on the Association between Capabilities and Performance. J. Bus. Ethics 2013, 115, 383–402. [Google Scholar] [CrossRef]

- Saeidi, S.P.; Sofian, S.; Saeidi, P.; Saeidi, S.P.; Saaeidi, S.A. How does corporate social responsibility contribute to firm financial performance? The mediating role of competitive advantage, reputation, and customer satisfaction. J. Bus. Res. 2015, 68, 341–350. [Google Scholar] [CrossRef]

- Valdez-Juárez, L.; Gallardo-Vázquez, D.; Ramos-Escobar, E.; Valdez-Juárez, L.E.; Gallardo-Vázquez, D.; Ramos-Escobar, E.A. CSR and the Supply Chain: Effects on the Results of SMEs. Sustainability 2018, 10, 2356. [Google Scholar] [CrossRef]

- De, D.; Chowdhury, S.; Dey, P.K.; Ghosh, S.K. Impact of Lean and Sustainability Oriented Innovation on Sustainability Performance of Small and Medium Sized Enterprises: A Data Envelopment Analysis-based framework. Int. J. Prod. Econ. 2018. [Google Scholar] [CrossRef]

- Danso, A.; Adomako, S.; Lartey, T.; Amankwah-Amoah, J.; Owusu-Yirenkyi, D. Stakeholder integration, environmental sustainability orientation and financial performance. J. Bus. Res. 2019. [Google Scholar] [CrossRef]

- Khan, S.Z.; Yang, Q.; Waheed, A. Investment in intangible resources and capabilities spurs sustainable competitive advantage and firm performance. Corp. Soc. Responsib. Environ. Manag. 2019, 26, 285–295. [Google Scholar] [CrossRef]

- Pislaru, M.; Herghiligiu, I.V.; Robu, I.-B. Corporate sustainable performance assessment based on fuzzy logic. J. Clean. Prod. 2019, 223, 998–1013. [Google Scholar] [CrossRef]

- INEGI. Economic Census, Summary of the Final Results; INEGI: Aguascalientes, Mexico, 2018. [Google Scholar]

- Cochran, W.G. Sampling Techniques; John Wiley & Sons: Hoboken, NJ, USA, 2007; ISBN 8126515244. [Google Scholar]

- Podsakoff, P.M.; MacKenzie, S.B.; Lee, J.; Podsakoff, N.P. Common Method Bias in Behavioral Research: A Critical Review of the Literature and Ecommended Remedies. J. Appl. Psychol. 2003, 88, 879–903. [Google Scholar] [CrossRef] [PubMed]

- Bagozzi, R.P.; Yi, Y.; Phillips, L.W. Assessing Construct Validity in Organizational Research. Adm. Sci. Q. 1991, 36, 421–458. [Google Scholar] [CrossRef]

- Jarvis, C.B.; MacKenzie, S.B.; Podsakoff, P.M. A Critical Review of Construct Indicators and Measurement Model Misspecification in Marketing and Consumer Research. J. Consum. Res. 2003, 30, 199–218. [Google Scholar] [CrossRef]

- Wetzels, M.; Odekerken-Schröder, G.; van Oppen, C. Using PLS Path Modeling for Assessing Hierarchical Construct Models: Guidelines and Empirical Illustration. MIS Q. 2009, 33, 177–195. [Google Scholar] [CrossRef]

- Kristandl, G.; Bontis, N. Constructing a definition for intangibles using the resource based view of the firm. Manag. Decis. 2007, 45, 1510–1524. [Google Scholar] [CrossRef] [Green Version]

- McWilliams, A.; Siegel, D.S.; Wright, P.M. Corporate social responsibility: Strategic implications. J. Manag. Stud. 2006, 43, 1–18. [Google Scholar] [CrossRef]

- Carroll, A.B. Corporate Social Responsibility. Bus. Soc. 1999, 38, 268–295. [Google Scholar] [CrossRef]

- Turker, D. Measuring Corporate Social Responsibility: A Scale Development Study. J. Bus. Ethics 2009, 85, 411–427. [Google Scholar] [CrossRef]

- Jenkins, H. Small Business Champions for Corporate Social Responsibility. J. Bus. Ethics 2006, 67, 241–256. [Google Scholar] [CrossRef]

- Orlitzky, M.; Schmidt, F.L.; Rynes, S.L. Corporate Social and Financial Performance: A Meta-Analysis. Organ. Stud. 2003, 24, 403–441. [Google Scholar] [CrossRef]

- Surroca, J.; Tribó, J.A.; Waddock, S. Corporate responsibility and financial performance: The role of intangible resources. Strategy Manag. J. 2010, 31, 463–490. [Google Scholar] [CrossRef]

- Fagerberg, J. Schumpeter and the revival of evolutionary economics: An appraisal of the literature. J. Evol. Econ. 2003, 13, 125–159. [Google Scholar] [CrossRef]

- Augier, M.; March, J.G. A retrospective look at A Behavioral Theory of the Firm. J. Econ. Behav. Organ. 2008, 66, 1–6. [Google Scholar] [CrossRef]

- Barney, J. Firm resources and sustained competitive advantage. J. Manag. 1991, 17, 99–120. [Google Scholar] [CrossRef]

- Barney, J.; Wright, M.; Ketchen, D.J. The resource-based view of the firm: Ten years after 1991. J. Manag. 2001, 27, 625–641. [Google Scholar] [CrossRef]

- Griffin, J.J.; Mahon, J.F. The Corporate Social Performance and Corporate Financial Performance Debate. Bus. Soc. 1997, 36, 5–31. [Google Scholar] [CrossRef]

- Bagnoli, C.; Vedovato, M. The impact of knowledge management and strategy configuration coherence on SME performance. J. Manag. Gov. 2014, 18, 615–647. [Google Scholar] [CrossRef]

- Benitez, J.; Castillo, A.; Llorens, J.; Braojos, J. IT-enabled knowledge ambidexterity and innovation performance in small U.S. firms: The moderator role of social media capability. Inf. Manag. 2018, 55, 131–143. [Google Scholar] [CrossRef]

- Sigler, K. CEO Compensation and Company Performance. Bus. Econ. J. 2011, 31, 1–8. [Google Scholar]

- Lo, S.-F.; Lu, W.-M. Does size matter? Finding the profitability and marketability benchmark of financial holding companies. Asia-Pac. J. Oper. Res. 2006, 23, 229–246. [Google Scholar]

- Reverte, C.; Gómez-Melero, E.; Cegarra-Navarro, J.G. The influence of corporate social responsibility practices on organizational performance: Evidence from Eco-Responsible Spanish firms. J. Clean. Prod. 2016, 112, 2870–2884. [Google Scholar]

- Martinez-Conesa, I.; Soto-Acosta, P.; Palacios-Manzano, M. Corporate social responsibility and its effect on innovation and firm performance: An empirical research in SMEs. J. Clean. Prod. 2017, 142, 2374–2383. [Google Scholar] [CrossRef]

- Benitez-Amado, J.; Walczuch, R.M. Information technology, the organizational capability of proactive corporate environmental strategy and firm performance: A resource-based analysis. Eur. J. Inf. Syst. 2012, 21, 664–679. [Google Scholar] [CrossRef]

- Barclay, D.; Higgins, C.; Thompson, R. The partial least squares (PLS) approach to causal modeling: Personal computer adoption and use as an illustration. Technol. Stud. 1995, 2, 285–309. [Google Scholar]

- Avkiran, N.K.; Ringle, C.M. Partial Least Squares Structural Equation Modeling: Recent Advances in Banking and Finance; Springer: Cham, Switzerland, 2018. [Google Scholar]

- Schuberth, F.; Henseler, J.; Dijkstra, T.K. Partial least squares path modeling using ordinal categorical indicators. Qual. Quant. 2018, 52, 9–35. [Google Scholar] [CrossRef] [PubMed]

- Wright, R.T.; Campbell, D.E.; Bennett Thatcher, J.; Roberts, N.; Bennett, J. Operationalizing Multidimensional Constructs in Structural Equation Modeling: Recommendations for IS Research. CAIS 2012, 30, 367–412. [Google Scholar] [CrossRef]

- Van Riel, A.C.R.; Henseler, J.; Kemény, I.; Sasovova, Z. Estimating hierarchical constructs using consistent partial least squares. Ind. Manag. Data Syst. 2017, 117, 459–477. [Google Scholar] [CrossRef] [Green Version]

- Chin, W.W. Issues and Opinion on Structural Equation Modeling. MIS Q. 1998, 22, 7–16. [Google Scholar]

- Vinzi, V.E.; Chin, W.W.; Henseler, J.; Wang, H. Handbooks of Partial Least Squares; Springer: Berlin, Germany, 2010. [Google Scholar]

- Henseler, J.; Ringle, C.M.; Sinkovics, R.R. The use of partial least squares path modeling in international marketing. In New Challenges to International Marketing; Emerald Group Publishing Limited: Bingley, UK, 2009; pp. 277–319. [Google Scholar] [Green Version]

- Roldán, J.L.; Cepeda, G. Modelos de Ecuaciones Estructurales basados en la Varianza: Partial Least Squares (PLS) para Investigadores en Ciencias Sociales; Universidad de Sevilla: Sevilla, Spain, 2016. [Google Scholar]

- Hair, J.F.; Hult, G.T.; Ringle, C.M.; Sarstedt, M.; Castillo-Apraiz, J.; Cepeda Carrion, G.; Roldán, J.L. Manual de Partial Least Squares Structural Equation Modeling (pls-sem); OmniaScience: Terrassa, Barcelona, Spain, 2019. [Google Scholar]

- Marcoulides, G.A.; Chin, W.W.; Saunders, C. A critical look at partial least squares modeling. MIS Q. 2009, 33, 171–175. [Google Scholar] [CrossRef]

- Richter, N.; Cepeda-Carrión, G.; Roldán Salgueiro, J.L.; Ringle, C.M. European management research using partial least squares structural equation modeling (PLS-SEM). Eur. Manag. J. 2016, 34, 589–597. [Google Scholar] [CrossRef]

- Chin, W.W.; Dibbern, J. Handbook of Partial Least Squares; Springer: Berlin, Germany, 2010. [Google Scholar]

- Ringle, C.; Wende, S.; Becker, J. SmartPLS—Statistical Software for Structural Equation Modeling. In Handbook of Market Research; Homburg, C., Klarmann, M., Vomberg, A., Eds.; Springer International Publishing: Cham, Switzerland, 2017. [Google Scholar]

- Wold, H. Systems Analysis by Partial Least Squares. In Measuring the Unmeasurable; Nijkamp, P., Leitner, H., Wrigley, N., Eds.; Kluwer Academic Publisher: Dordrecht, The Netherlands, 1985; pp. 221–251. [Google Scholar] [Green Version]

- Hair, J.F.; Ringle, C.M.; Sarstedt, M. PLS-SEM: Indeed a Silver Bullet. J. Mark. Theory Pract. 2011, 19, 139–152. [Google Scholar] [CrossRef]

- Gliem, J.A.; Gliem, R.R. Calculating, Interpreting, and Reporting Cronbach’s Alpha Reliability Coefficient for Likert-Type Scales. In Proceedings of the 2003 Midwest Research to Practice Conference in Adult, Continuing, and Community Education, The Ohio State University, Columbus, 8–10 October 2003. [Google Scholar]

- Nunnally, J. Psychometric Methods; McGraw-Hill: New York, NY, USA, 1978. [Google Scholar]

- Chin, W.W. The partial least squares approach to structural equation modeling. Mod. Methods Bus. Res. 1998, 295, 295–336. [Google Scholar]

- Henseler, J.; Dijkstra, T.K.; Sarstedt, M.; Ringle, C.M.; Diamantopoulos, A.; Straub, D.W.; Ketchen, D.J.; Hair, J.F.; Hult, G.T.M.; Calantone, R.J. Common Beliefs and Reality About PLS: Comments on Rönkkö and Evermann (2013). Organ. Res. Methods 2014, 17, 182–209. [Google Scholar] [CrossRef]

- Nunnally, J.C.; Bernstein, I.H. Psychometric Theory (McGraw-Hill Series in Psychology); McGraw-Hill: New York, NY, USA, 1994. [Google Scholar]

- Nunnally, J.C.; Bernstein, I.H. The reliability of Reliability. In Psychometric Theory, 3rd ed.; McGraw-Hill: New York, NY, USA, 1994. [Google Scholar]

- Dijkstra, T.K.; Henseler, J. Consistent partial least squares path modeling. MIS Q. 2015, 39, 297–316. [Google Scholar] [CrossRef]

- Henseler, J.; Ringle, C.M.; Sarstedt, M. A new criterion for assessing discriminant validity in variance-based structural equation modeling. J. Acad. Mark. Sci. 2015, 43, 115–135. [Google Scholar] [CrossRef]

- Ringle, C.M.; Wende, S.; Will, A. Finite Mixture Partial Least Squares Analysis: Methodology and Numerical Examples. In Handbook of Partial Least Squares; Springer: Berlin/Heidelberg, Germany, 2010; pp. 195–218. [Google Scholar]

- Fornell, C.; Larcker, D.F. Evaluating Structural Equation Models with Unobservable Variables and Measurement Error. J. Mark. Res. (JMR) 1981, 18, 39–50. [Google Scholar] [CrossRef]

- Henseler, J.; Ringle, C.M.; Sarstedt, M. Testing measurement invariance of composites using partial least squares. Int. Mark. Rev. 2016, 33, 405–431. [Google Scholar] [CrossRef]

- Franke, G.; Sarstedt, M. Heuristics versus statistics in discriminant validity testing: A comparison of four procedures. Internet Res. 2019, 29, 430–447. [Google Scholar] [CrossRef]

- Henseler, J. Bridging Design and Behavioral Research with Variance-Based Structural Equation Modeling. J. Advert. 2017, 46, 178–192. [Google Scholar] [CrossRef]

- Sarstedt, M.; Cheah, J.-H. Partial least squares structural equation modeling using SmartPLS: a software review. J. Mark. Anal. 2019, 7, 196–202. [Google Scholar] [CrossRef]

- Urbach, N.; Ahlemann, F. Structural Equation Modeling in Information Systems Research Using Partial Least Squares. J. Clean. Prod. Inf. Technol. Theory Appl. 2010, 11, 5–40. [Google Scholar]

- Hair, J.F.; Sarstedt, M.; Hopkins, L.; Kuppelwieser, V.G. Partial least squares structural equation modeling (PLS-SEM): An emerging tool in business research. Eur. Bus. Rev. 2014, 26, 106–121. [Google Scholar] [CrossRef]

- Cohen, J. Set Correlation and Contingency Tables. Appl. Psychol. Meas. 1988, 12, 425–434. [Google Scholar] [CrossRef]

- Henseler, J.; Hubona, G.; Ray, P.A. Using PLS path modeling in new technology research: Updated guidelines. Ind. Manag. Data Syst. 2016, 116, 2–20. [Google Scholar] [CrossRef]

- Hu, L.; Bentler, P.M. Cutoff criteria for fit indexes in covariance structure analysis: Conventional criteria versus new alternatives. Struct. Equ. Model. Multidiscip. J. 1999, 6, 1–55. [Google Scholar] [CrossRef]

- Hayes, A.F.; Scharkow, M. The Relative Trustworthiness of Inferential Tests of the Indirect Effect in Statistical Mediation Analysis. Psychol. Sci. 2013, 24, 1918–1927. [Google Scholar] [CrossRef]

- Carrión, G.C.; Nitzl, C.; Roldán, J.L. Mediation Analyses in Partial Least Squares Structural Equation Modeling: Guidelines and Empirical Examples. In Partial Least Squares Path Modeling; Springer International Publishing: Cham, Switzerland, 2017; pp. 173–195. [Google Scholar]

- Nitzl, C.; Roldan, J.L.; Cepeda, G. Mediation analysis in partial least squares path modeling. Ind. Manag. Data Syst. 2016, 116, 1849–1864. [Google Scholar] [CrossRef]

- Hair, J.J.; Hult, G.; Ringle, C.; Sarstedt, M. A Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM); Sage publications: Thousand Oaks, CA, USA, 2016. [Google Scholar]

- Bontis, N.; Cabrita, M.D.R. Intellectual capital and business performance in the Portuguese banking industry Maria do Rosário Cabrita. Int. J. Technol. Manag. 2008, 43, 212–237. [Google Scholar]

- Teece, D.J. Dynamic Capabilities and Strategic Management: Organizing for Innovation and Growth; Oxford University Press: New York, NY, USA, 2009; ISBN 978-0-19-969190-6. [Google Scholar]

- Brink, T. Organising of dynamic proximities enables robustness, innovation and growth: The longitudinal case of small and medium-sized enterprises (SMEs) in food producing firm networks. Ind. Mark. Manag. 2018, 75, 66–79. [Google Scholar] [CrossRef]

- Laudal, T. Drivers and barriers of CSR and the size and internationalization of firms. Soc. Responsib. J. 2011, 7, 234–256. [Google Scholar] [CrossRef]

- Carroll, A. Corporate social responsibility: A review of current concepts, research, and issues. Corp. Soc. Responsib. 2018, 2, 39–69. [Google Scholar]

- Teece, D.J. Explicating Dynamic Capabilities: The Nature and Microfoundations of (Sustainabile) Enterprise Performance. Strategy Manag. J. 2007, 298, 1319–1350. [Google Scholar] [CrossRef]

- Aksoy, M.; Apak, S.; Eren, E.; Korkmaz, M. Analysis of the effect of organizational learning-based organizational culture on performance, job satisfaction and efficiency: A field study in banking sector. Int. J. Acad. Res. 2014, 6, 301–313. [Google Scholar] [CrossRef]

- Freeman, R.E.; Harrison, J.S.; Wicks, A.C.; Parmar, B.L.; de Colle, S. Stakeholder Theory: The State of the Art; Cambridge University Press: Cambridge, UK, 2010; ISBN 9781139484114. [Google Scholar]

- Yu, H.-C.; Kuo, L.; Kao, M.-F. The relationship between CSR disclosure and competitive advantage. Sustain. Account. Manag. Policy J. 2017, 8, 547–570. [Google Scholar] [CrossRef]

- Jain, A.; Leka, S.; Zwetsloot, G. Managing Health, Safety and Well-Being: Ethics, Responsibility and Sustainability; Springer: Berlin, Germany, 2018. [Google Scholar]

- Evans, M.; Dalkir, K.; Bidian, C. A holistic view of the knowledge life cycle: The knowledge management cycle (KMC) model. Electron. J. Knowl. Manag. 2014, 12, 85–97. [Google Scholar]

- Wood, D.J. Measuring corporate social performance: A review. Int. J. Manag. Rev. 2010, 12, 50–84. [Google Scholar] [CrossRef]

- Murillo, D.; Lozano, J.M. SMEs and CSR: An approach to CSR in their own words. J. Bus. Ethics 2006, 67, 227–240. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Characteristic | Micro | Small | Medium |

| Company size (number of employees) | 42 (1–10) | 189 (11–50) | 112 (51–250) |

| Total % | 12.2% | 55.1% | 32.7% |

| Primary | Secondary | Tertiary | |

| Business sector | 21 | 224 | 98 |

| Total % | 6.1% | 65.3% | 28.6% |

| Initial Values Component | Sums of the Square Saturations of the Extraction | |||||

|---|---|---|---|---|---|---|

| Component | Total | % of variance | % accumulated | Total | % of variance | % accumulated |

| 1 | 9.092 | 37.885 | 37.885 | 9.092 | 37.885 | 37.885 |

| 2 | 2.677 | 11.153 | 49.038 | 2.677 | 11.153 | 49.038 |

| 3 | 1.584 | 6.599 | 55.637 | 1.584 | 6.599 | 55.637 |

| 4 | 1.385 | 5.770 | 61.407 | 1.385 | 5.770 | 61.407 |

| 5 | 1.151 | 4.794 | 66.202 | 1.151 | 4.794 | 66.202 |

| 6 | 0.895 | 3.728 | 69.930 | |||

| 7 | 0.865 | 3.603 | 73.533 | |||

| 8 | 0.734 | 3.059 | 76.592 | |||

| 9 | 0.647 | 2.695 | 79.287 | |||

| 10 | 0.573 | 2.389 | 81.676 | |||

| 11 | 0.547 | 2.280 | 83.956 | |||

| 12 | 0.472 | 1.965 | 85.921 | |||

| 13 | 0.447 | 1.862 | 87.783 | |||

| 14 | 0.394 | 1.641 | 89.423 | |||

| 15 | 0.376 | 1.565 | 90.988 | |||

| 16 | 0.340 | 1.417 | 92.406 | |||

| 17 | 0.300 | 1.250 | 93.655 | |||

| 18 | 0.278 | 1.160 | 94.815 | |||

| 19 | 0.240 | 0.998 | 95.814 | |||

| 20 | 0.235 | 0.981 | 96.795 | |||

| 21 | 0.224 | 0.934 | 97.729 | |||

| 22 | 0.208 | 0.867 | 98.595 | |||

| 23 | 0.187 | 0.781 | 99.376 | |||

| 24 | 0.150 | 0.624 | 100.000 | |||

| Construct. | ECR | ENR | FPE | OLE | SOR |

|---|---|---|---|---|---|

| ECR | 1.000 | 0.627 | 0.477 | 0.527 | 0.674 |

| ENR | 0.627 | 1.000 | 0.346 | 0.443 | 0.635 |

| FPE | 0.477 | 0.346 | 1.000 | 0.505 | 0.407 |

| OLE | 0.527 | 0.443 | 0.505 | 1.000 | 0.627 |

| SOR | 0.674 | 0.635 | 0.407 | 0.627 | 1.000 |

| LF | CR | CA | |

|---|---|---|---|

| Organizational Learning (OLE) (First order) | 0.933 | 0.914 | |

| The OLE is key to the competitive advantage | 0.812 *** | ||

| The business philosophy is based on continuous OLE | 0.845 *** | ||

| Constantly search for information and knowledge | 0.801 *** | ||

| Employees have acquired skills and abilities | 0.839 *** | ||

| It has transformed knowledge into an added value | 0.857 *** | ||

| Organizational performance is the product of the OLE | 0.867 *** | ||

| Corporate Social Responsibility (CSR) (Second order) | 0.923 | 0.920 | |

| SOR (Social Responsibility) | 0.906 | 0.862 | |

| It favors the hiring of people at risk of social exclusion | 0.741 *** | ||

| Value the contribution of disabled people | 0.711 *** | ||

| It deals with improving the quality of life of employees | 0.820 *** | ||

| Pay salaries above the industry average | 0.768 *** | ||

| ECR (Economic Responsibility) | 0.846 | 0.758 | |

| Offer customers complete information about our products | 0.800 *** | ||

| Respecting the rights of consumers is a priority | 0.832 *** | ||

| Have socially responsible suppliers | 0.903 *** | ||

| It promotes commercial relations with companies in the region | 0.827 *** | ||

| ENR (Environmental Responsibility) | 0.928 | 0.902 | |

| Use of consumables with low environmental impact | 0.834 *** | ||

| Save and monitor energy efficiency | 0.822 *** | ||

| Value the introduction of alternative energies | 0.813 *** | ||

| Perform environmental control and protection activities | 0.839 *** | ||

| Plan its finances based on the reduction of environmental impact | 0.872 *** | ||

| Financial Performance (FPE) (First order) | LF | 0.910 | 0.877 |

| Increase in profits | 0.745 *** | ||

| Sales increase | 0.813 *** | ||

| Increase in contribution margin | 0.820 *** | ||

| Increase in market share | 0.847 *** | ||

| Increase in pre-tax benefits | 0.858 *** |

| Construct | AVE | OLE | CSR | FPE |

|---|---|---|---|---|

| OLE | 0.701 | 0.837 | ||

| CSR | 0.514 | 0.606 | 0.717 | |

| FPE | 0.696 | 0.505 | 0.462 | 0.834 |

| Construct | OLE | CSR |

|---|---|---|

| CSR | 0.649 | |

| FPE | 0.568 | 0.516 |

| Hypothesis | Beta/Path Coefficients | T Score | Standard Deviation | P Value | F2 | Accepted/Rejected |

|---|---|---|---|---|---|---|

| H1. OLE- > CSR | 0.606 *** | 12.578 | 0.048 | 0.000 | 0.580 | Accepted |

| H2. OLE- > FPE | 0.361 *** | 6.255 | 0.058 | 0.000 | 0.115 | Accepted |

| H3. CSR- > RF | 0.245 *** | 4.063 | 0.060 | 0.000 | 0.055 | Accepted |

| Hypothesis | Beta/Path Coefficients | Percentile CI 5.0% | Percentile CI 95.0% | Bias Corrected CI 5.0% | Bias Corrected CI 95.0% |

|---|---|---|---|---|---|

| H1. OLE- > CSR | 0.606 *** | 0.525 | 0.691 | 0.526 | 0.686 |

| H2. OLE- > FPE | 0.361 *** | 0.268 | 0.458 | 0.266 | 0.459 |

| H3. CSR- > RF | 0.245 *** | 0.136 | 0.341 | 0.141 | 0.338 |

| Dimension | R2 | Q2 | SRMR | RMStheta |

|---|---|---|---|---|

| CSR | 0.365 | 0.354 | 0.099 | 0.139 |

| FPE | 0.300 | 0.283 |

| Coefficient | Booststrap 90% CI | |||||

|---|---|---|---|---|---|---|

| Percentile CI | Bias Corrected CI | |||||

| Direct effects | ||||||

| H1: c | 0.245sig | 0.136 | 0.341 | 0.140 | 0.144 | |

| a1 | 0.606sig | 0.525 | 0.687 | 0.523 | 0.520 | |

| b2 | 0.361sig | 0.263 | 0.460 | 0.264 | 0.265 | |

| Indirect effects | Point estimate | Percentile | BC | VAF | ||

| H2: a1 x b1 | 0.219 sig | 0.198 | 0.671 | 0.187 | 0.176 | 47.17% |

| Total indirect effect | 0.219sig | |||||

| Total effect | 0.464 sig | |||||

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Valdez-Juárez, L.E.; Gallardo-Vázquez, D.; Ramos-Escobar, E.A. Organizational Learning and Corporate Social Responsibility Drivers of Performance in SMEs in Northwestern Mexico. Sustainability 2019, 11, 5655. https://doi.org/10.3390/su11205655

Valdez-Juárez LE, Gallardo-Vázquez D, Ramos-Escobar EA. Organizational Learning and Corporate Social Responsibility Drivers of Performance in SMEs in Northwestern Mexico. Sustainability. 2019; 11(20):5655. https://doi.org/10.3390/su11205655

Chicago/Turabian StyleValdez-Juárez, Luis Enrique, Dolores Gallardo-Vázquez, and Elva Alicia Ramos-Escobar. 2019. "Organizational Learning and Corporate Social Responsibility Drivers of Performance in SMEs in Northwestern Mexico" Sustainability 11, no. 20: 5655. https://doi.org/10.3390/su11205655