Determining Environmental Costs: A Challenge in A Governmental E-Waste Recycling Scheme

1

Institute of Environmental Engineering and Management, National Taipei University of Technology, Taipei 106, Taiwan

2

Center for Green Economy, Chung-Hua Institution for Economic Research, Taipei 106, Taiwan

*

Author to whom correspondence should be addressed.

Sustainability 2019, 11(19), 5156; https://doi.org/10.3390/su11195156

Submission received: 29 July 2019

/

Revised: 11 September 2019

/

Accepted: 12 September 2019

/

Published: 20 September 2019

Abstract

:The Extended Producer Responsibility (EPR) concept involves having producers take environmental responsibility for post-consumer products. Based on this principle, the Waste Electrical and Electronic Equipment (WEEE) Directive of the European Union, enacted in 2006, is the most representative management program in the world and the most popular recycling policy many countries follow. Taiwan’s version of EPR for WEEE recycling, set up in 1998, had a focus on recycling fees determined by a recycling fee equation. Nowadays, the equation takes into account the consideration of the environment in the designs of products, in addition to the cost needed for recycling. The environmental performance upgrades in products, encouraged by the financial incentives from these considerations, is a side-benefit of this program. In this paper, the functions of the recycling fee equation that consider environmental costs are reviewed. It was found that in spite of the difficulty in determining the real environmental costs in practice, pricing is a mechanism which helps us to consider the cost of e-waste recycling, not only in terms of labor and administration, but also environmental quality.

1. Introduction

Environmental damage from littering is the main reason for waste management efforts, which has led to the practice of take-back schemes in many countries [1]. The Extended Producer Responsibility principle (EPR) [1,2] adds environmental cost in as a portion of the sales of durable products, such as electrical and electronic equipment, sold to customers [3]. The cost of collection and recycling can be interpreted as an environmental cost, if articles are scattered in the environment [4]. Therefore, the governmental recycling system for Waste Electrical and Electronic Equipment (WEEE) in Taiwan started in 1998 with the EPR concept, which considers environmental costs caused by e-waste dumped in the environment without further treatment [5,6].

The approach of the EPR system’s operation in Taiwan is to impose the financial responsibility on producers by charging them recycling fees. Every two months, producers and importers of electrical and electronic equipment in Taiwan have to pay recycling fees, based on their domestic sales quantities and the recycling fee rates for different products, to the Recycling Fund Management Board (RFMB) of the Environmental Protection Administration of Taiwan (EPAT), the environmental authority at the cabinet level of the central government [7,8]. The fees are not only for the cost of take-back schemes and recycling, but also for articles scattered in nature without being collected for proper treatment.

In 2012, the RFMB initiated the Green Recycling Fees program, which allowed producers to reduce their recycling fee payments by up to 30% if the articles sold to the market are certified with eco-labels issued in Taiwan such as the Environmental Labels from the EPAT and the Water-Saving Labels and Energy-Saving Labels from the Ministry of Economic Affairs [9]. The purpose of Green Recycling Fees is to encourage the green design of products to facilitate the recycling process later, reducing the costs of recycling operations, and in turn, reducing the environmental costs by recycling.

With the fee-charging EPR system, which originally evolved from environmental cost considerations for better waste management, Taiwan has achieved a 60% take-back rate of total waste and created a mature recycling industry because of the governmental recycling scheme [10]. However, the government’s fee-charging EPR has also been criticized for its inefficiency in the bureaucratic process, slow capital flow, and failure to encourage the improvement of recycling facilities [11,12]. Therefore, the evolution of the fee calculation equations, with more attention to the factor of environmental costs, its impacts on the performance, and management of the governmental recycling system are the focus of this paper.

2. The Structure of EPR in Taiwan

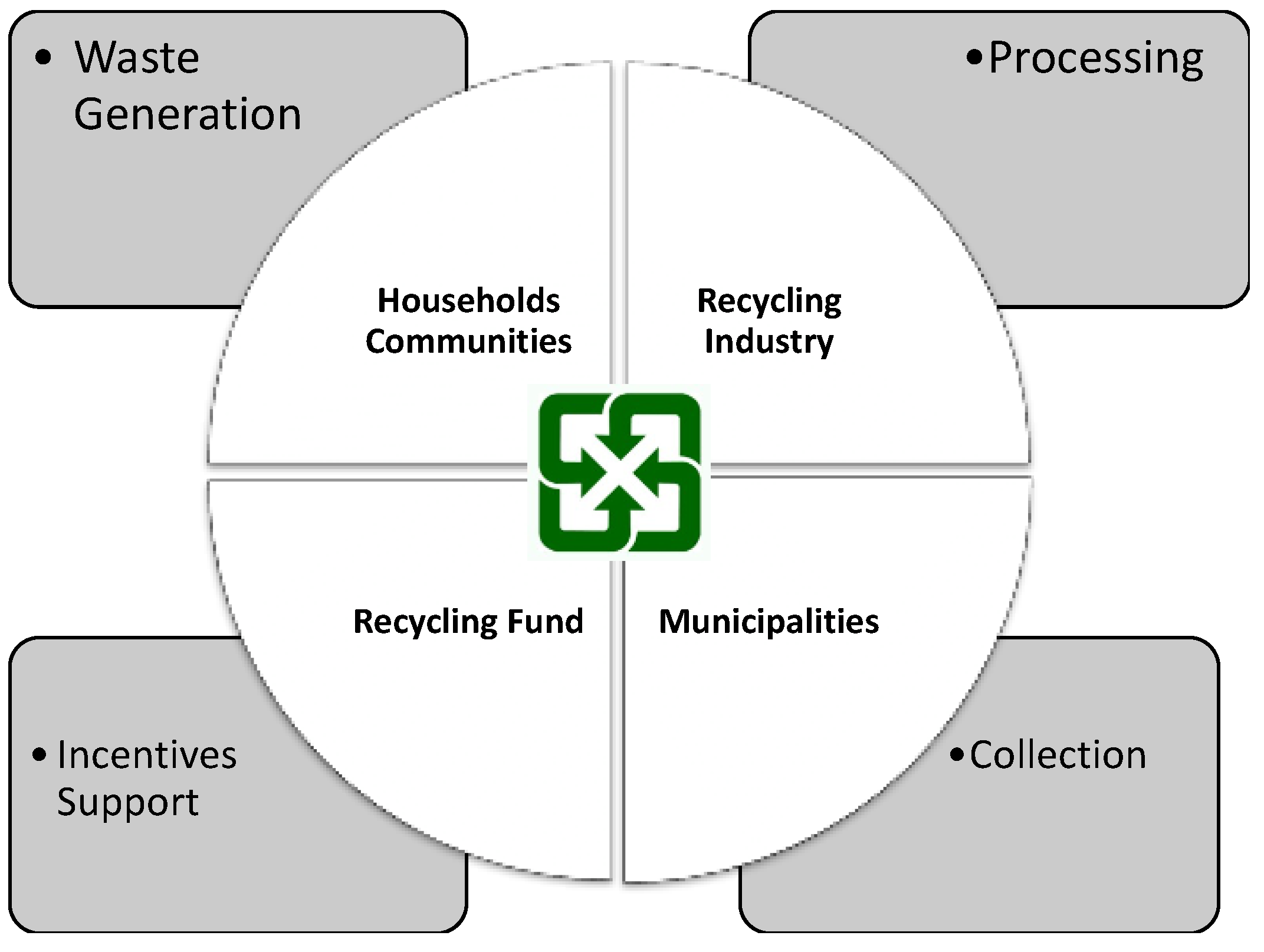

The key players in the EPR system in Taiwan since 1998, the so-called “four-in-one” program, are composed of four major parties: households and communities, private recyclers, the recycling fund, and local governments and municipalities, as shown in Figure 1 [13]. Households are required to sort trash, while municipalities collect recyclables separately and deliver them to recyclers, who receive a subsidy from the recycling fund to process the recycling of those collected recyclables.

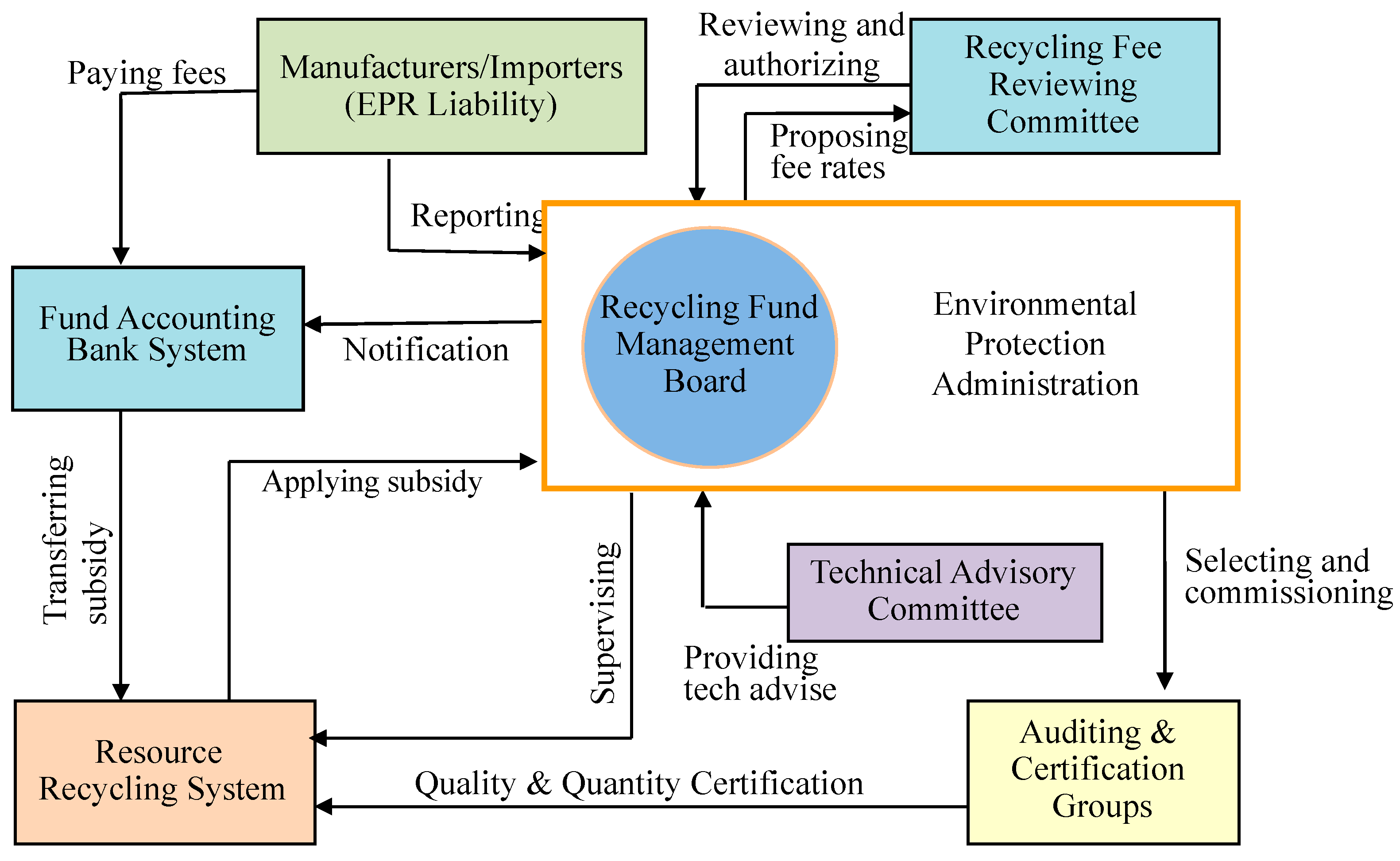

The recycling fund is collected from producers and managed by the RFMB of EPAT. As shown in Figure 2, the RFMB periodically determines the recycling fees charged on each unit of the products required to be recycled by law. At the same time, recyclers receive a subsidy from the RFMB to compensate for the cost of recycling operations. Subsidy fee rates, which differ from product to product, are also determined by the RFMB. Therefore, the state-owned RFMB of the EPAT plays the role of a Private Recycling Organization (PRO). Currently, there are 33 items that are classified into 13 categories which are subject to recycling [13]. E-waste belongs to two of the 13 categories of products: information technology products, such as computers; and home appliances, such as TV sets and washing machines.

3. Evolution of the Recycling Fee Equation

The recycling fee calculation equation plays a crucial role in determining payment from producers. The equation has also become a tool for maintaining the balance of the recycling fund because of the adjustable parameters in the equation, such as the environmental cost, administration cost, etc. For different periods of time, the equation incorporated different considerations and different parameters as follows [5,6,7].

3.1. Recycling Fee Calculation Equation V.1 (1998)

In 1998, when the RFMB started to operate the EPR scheme for e-waste recycling, the recycling fee determination was purely based on the cost needed for the operation without considering other factors, such as the environmental cost of littering with recyclable products that were not collected into the process. For each mandatory recycling product category, such as TV sets, washing machines, air conditioners, refrigerators, and computers, an individual account is set up for the management of recycling work.

where,

R = C × W × α × (1 + p)/S

- R: recycling fee ($/unit)

- C: collection and treatment cost per unit ($/unit)

- W: estimated obsolete amount (units)

- α: collection rate target (%)

- p: administration cost vs recycling operation cost ratio (%)

- S: forecasted yearly new sales amount (units)

3.2. Recycling Fee Calculation Equation V.2 (2001)

In 2001, after 3 years of operation, RFMB revised the fee calculation equation to include the environmental cost from the littering of recyclable products that were not collected into the collection process. Therefore, calculating recycling fees not only for the operational cost but also for the environmental cost of uncollected articles became a challenge for the Taiwanese EPR scheme.

Uncollected articles usually enter incinerators and landfill sites, or are simply discarded in nature, such as in the mountains or places that are difficult to reach. The informal sector for underground recycling is another destination for uncollected articles, but it is difficult to control and consider.

In addition, for some items of e-waste, the funds collected in the past three to four years have been accumulated to a certain level, while the funds for a few other items were insufficient to maintain their balance. Therefore, the fund surplus or deficit in each account will be amortized in the recycling fees over the next several years. The factor of amortization for fund surplus or deficit was included in the fee calculation equation.

where,

R = [C × α + E × (1 − α) ± F] × β

- R: recycling fee ($/unit)

- C: collection and treatment cost per unit ($/unit)

- α: collection rate target (%)

- E: averaged environmental cost of the unrecycled waste products ($/unit)

- F: fund balance amortization ($)

- β: ratio of obsolete vs new sales of product, or W/S (%)

3.3. Recycling Fee Calculation Equation V.3 (2005)

In 2005, the environmental cost for the littering of unrecyclable waste products, denoted by “E” in equation V.2, was further differentiated into two categories: the environmental cost of unrecyclable products with proper collection and final disposal, denoted as E1; and the environmental cost of unrecyclable products without proper final disposal, denoted as E2 in the equation V.3.

where,

R = [C × α + (E1 + E2) × (1 − α) − F/W] × β

- R: recycling fee ($/unit)

- C: collection and treatment cost per unit ($/unit)

- α: collection rate target (%)

- E1: averaged environmental cost of unrecycled but properly disposed products, such as through sanitarily landfilled or incinerated means ($/unit)

- E2: averaged environmental cost of littering for unrecycled and improperly disposed products ($/unit)

- F: fund balance amortization ($)

- W: estimated obsolete amount (units)

- β: ratio of obsolete vs newly sold products, or, W/S (%)

In another expression,

R = {[C × α + (E1 + E2) × (1 − α)] × W − F}/S

In addition, with further consideration for the collection rate, the unrecycled ratio (1 − α) is further divided into two categories for different environmental costs:

- The ratio of the unrecyclable but properly disposed products (α1);

- The ratio of littering involving the unrecyclable and improperly disposed products (α2).

Then, the equation is changed to the following expression:

where,

R = [C × W × α + E1 × W × α1 + E2 × W × α2 + L − F]/S

- R: recycling fee ($/unit)

- C: collection and treatment cost per unit ($/unit)

- α: collection rate target (%)

- α1: ratio of the waste products properly disposed of but not recycled (%)

- α2: ratio of the waste products littered and not properly disposed of (%)α + α1 + α2 = 1

- E1: averaged environmental cost of unrecycled but properly disposed products, such as through sanitarily landfilled or incinerated means ($/unit)

- E2: averaged environmental cost of littering for unrecycled and improperly disposed products ($/unit)

- W: estimated obsolete amount (units)

- F: fund balance amortization ($)

- L: administration cost of the recycling scheme ($)

- S: forecasted yearly new sales amount (units)

The determination of these elements are shown in Table 3.

4. Green Recycling Fee Rates: A Discount Factor in Recycling Fees for Environmentally Designed Products

In order to encourage the industry to bring environmentally friendly products to the market, green designs of electrical and electronic equipment are considered as a factor in reducing the recycling fees for e-waste. The Green Recycling Fee rates means lower recycling fees were required by the EPAT as of 2012, once the mandatory recycling products were certified with eco-labels [16]. This differential mechanism increases the market competitiveness of environmentally friendly products. It can be interpreted as a consideration of the environmental cost of the products throughout their lifetime. The application of this environmental cost concept could involve either a reduction in recycling fees for green product producers, or an increase in recycling fees to discourage the sale of less environmentally friendly products to customers.

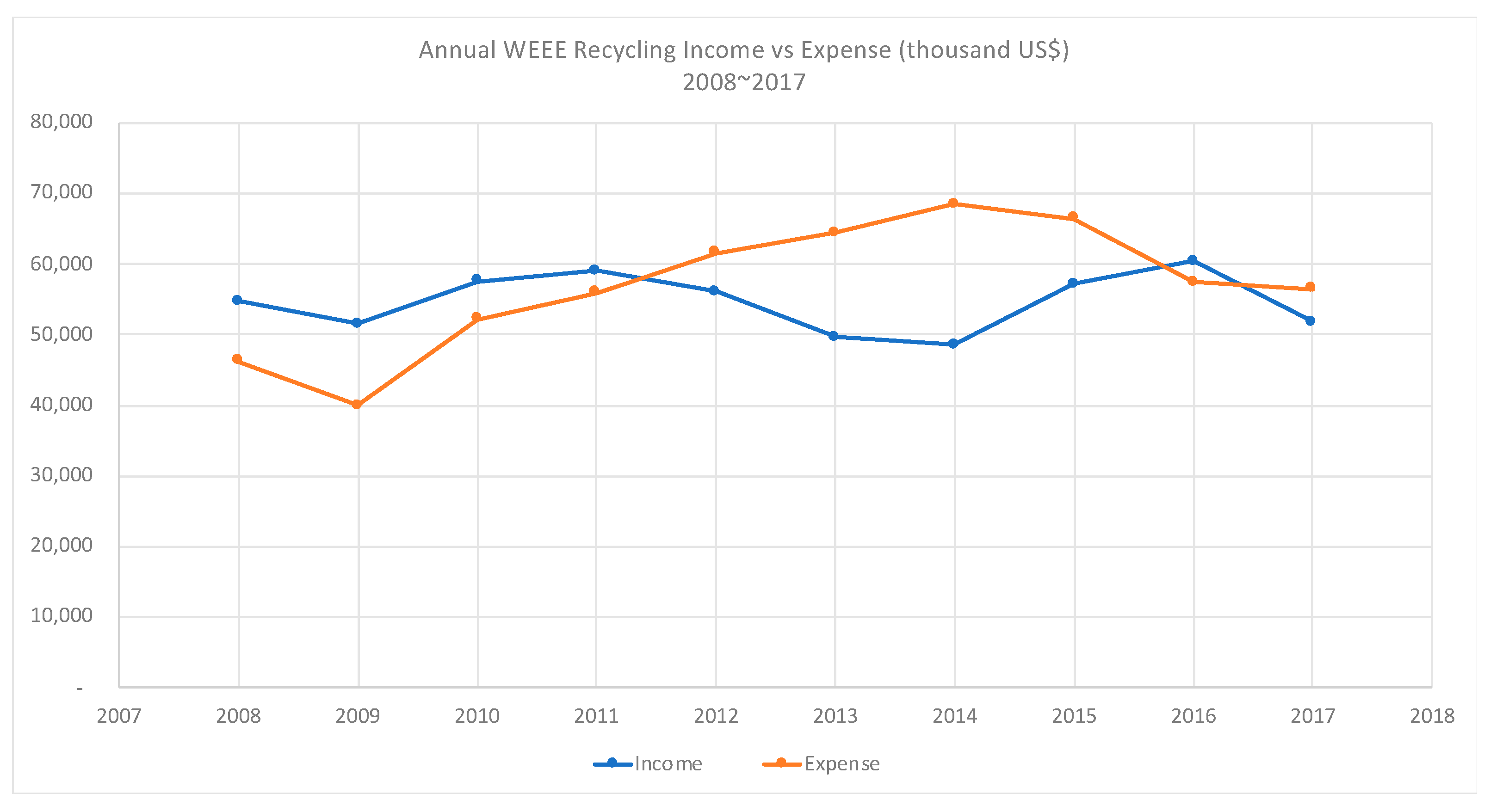

Since 2012, the green discount factor has been set from 10–30% and is expected to give the producers incentives to engage in green design. As long as the EEE sold in the market receives a green certificate such as one of the Environmental Labels in Taiwan, they are entitled to receive a discount on the recycling fees paid to the EPAT. Up until now, more than 55% of the reported volume of produced and imported home appliances and IT equipment have qualified for the green recycling fee rate. For some items, the green-claimed product percentage is over 80%, which indicates producers easily qualify for the Green Recycling Rates. This system has resulted in a risk of unbalancing the Recycling Fund, as shown in the variations of income vs. expense in Figure 3.

5. Consideration of Environmental Costs in the Fee Equations

In the governmental e-waste recycling in Taiwan, environmental cost is taken into account in the recycling fee equation in two different formats: using the government budget as a substitute and implementing green recycling mechanisms for different purposes [8]. Their impacts are also different in the temporal spectrum. In general, properly determining environmental costs is frequently an important but controversial issue in policy discussion. Many theories have been proposed for the calculation, such as the hedonic method and willingness-to-pay/accept method [17]. In order to estimate the monetary cost of environmental degradation by human behavior, the United Nations determined a method, the System of Environmental Economic Accounting (SEEA) [18], to more easily estimate the value of natural resources and the environment in the traditional System of National Accounts. The suggested principles of valuation by SEEA include market-based asset valuation, which considers the market value of the services provided by the environment. If the market value cannot be applied, SEEA suggests two alternatives: the written-down replacement cost method, and the discount value of future returns.

However, the primary reason to operate a recycling scheme is to compensate or prevent environmental costs caused by the littering of e-waste in the environment, and the health problems caused by e-waste pollution. From the Recycling Fee Calculation Equation (1) to Equation (5), more and more considerations are added into calculations in each successive version of the equation. In particular, the environmental costs of littering become an issue. It is hoped that the benefit in recycling and green designed products can be identified through the fee-charging EPR system.

In practice, environmental cost is usually estimated by two approaches: the maintenance cost method and damage assessment method, as shown in Figure 4 [19]. The first approach incorporates the cost of pollution prevention, whereas the second approach focuses more on the financial need to restore environmental damage back to its original state. As the estimation of the cost of the prevention equipment and program operation is easier and also more controllable, the maintenance cost method is usually preferred in the estimation of environmental values and also used in the calculation of Green Gross Domestic Production, or the “Green GDP” system, in Taiwan [20].

The consideration of environmental cost was first introduced in Equation V.2 using the Maintenance Cost Method in Figure 4. After the environmental cost was introduced, the annual balance of the Recycling Fund was directly affected. However, the environmental damage reduced by the adoption of this mechanism is the real concern. It can be split into the impacts on economy and on the environment respectively, for further analysis [21]. Alternatively, it can be simply estimated by using the difference of recycled quantities, before and after, multiplied by the environmental benefit of recycling for each unit of the articles taken back. It is expected that more research will be conducted on this estimation in the future.

6. Findings from the Variation of Recycling Equation and Environmental Cost Consideration

In practice, because the associations between the recycling system and the economy are complex, it is necessary to examine the roles of the major players contributing to the success of the recycling scheme. During the past two decades, the major criticisms of and lessons learned from the operation of the governmental recycling scheme involving the four major players in the Taiwanese system are as follows:

- Consumers do not highly value consumer subsidy or rewards, and instead care more about the convenience of handing over recyclables to collectors.

- Producers care not about how they should physically work on taking back and recycling, but about how much they should pay.

- The government is not able to further achieve better environmental targets simply by managing the recycling fee-charging system. However, the government needs to guide the market towards greener appliances with monetary instruments.

Therefore, three approaches or principles that may improve the efficiency of the governmental recycling system are proposed as follows:

- Establishing a linkage between producers and recyclers to encourage eco-design, as well as a linkage between recyclers and collectors to form a complete alliance.

- Identifying potential profits through innovative and inter-industrial collaboration between manufacturers and recyclers.

- Sharing the subsidy fee with the producers who pay the recycling fees, and executing physical responsibility for recycling.

In addition, a reverse logistic channel is necessary to ensure a stable and sufficient supply of e-waste is directly collected from users for recycling. Furthermore, the integration of informal collectors with formal collectors is the key to further increasing recycling in Taiwan.

The Recycling Fund in Taiwan plays a critical role by financing the recyclers and helping to establish the e-waste treatment infrastructure. However, a well-designed and executed recycling fee system is needed to sustain a healthy financial condition and provide adequate incentives to all the stakeholders, including manufacturers, recyclers, and consumers. Therefore, rationalization of the fee rates requires regular investigation of the market price of recovered resources and the costs of collection, transportation and recycling, which is a difficult task especially for countries with little data available or collectable.

Another important factor for the stability of the fund’s operation, is the balancing of the fund by regularly reviewing surplus, collection ratio, current fee rates, and variance of all costs. In addition to maintaining a healthy system of recycling, the fund system can encourage green production by using economic incentives from the recycling fee reduction as another way of thinking about the environmental costs of products.

7. Conclusions

The environmental cost of e-waste is always a concern in environmental protection and waste management because of its externalities in financial accounting [1,2,3]. This issue is also related to the concept of Environmental Life Cycle Costing (LCC) [22,23] which estimates the real cost of each product through its life cycle. The fee equations in this paper aim to incorporate LCC in a more feasible approach by administration. However, it is not easy to quantify and to impose a realistic charge on producers. It is also not possible to estimate a mutually agreeable environmental cost when e-waste is scattered in the environment. However, the recycling fee equation is an attempt at determining an appropriate number that is feasible and has positive impacts. Consideration of the environmental cost, total cost, or true cost is a well-accepted concept, as an element that can further upgrade the performance of and develop a mature recycling scheme. However, environmental cost would not be an issue for private Producer Responsibility Organizations (PROs). Instead, it would be only considered by a governmental recycling system, since it is likely that only the public sector cares about environmental quality as a public good.

For the environmental cost consideration, the spatial and temporal scope of the environmental cost is the first to be delineated. In the case of Taiwan, the consideration of the environmental cost is embedded in the recycling fee equation, and thus the proper disposal and treatment costs of the products put into the market is imposed on producers. The other factor to be considered is how environmentally designed products can be encouraged and sold on the market. Inclusion of environmental costs in the equation focuses on the damage caused by uncollected obsolete products. However, the Green Recycling Fee is directed more at the whole society in the long run, rather than being merely associated with the environmental damage cost of the products themselves.

Furthermore, maintaining the financial stability of the system is fundamental for further improving the scheme’s efficiency in terms of cost and, to an extent, the environmental benefit gained. The adoption of the Green Recycling Fee System resulted in an imbalance between the income and spending of the recycling fund, which forced the RFMB to reduce the discount rate of the recycling fee for a more limited scope of green certifications; this shows that it is critical to reasonably calculate the recycling fees.

Author Contributions

C.C. collected necessary data, conducted primary analysis and drafted the paper. C.L. was in charge of paper revision and correspondence to editors. L.W. verified the fee equations in different eras and provided the discussion about environmental cost calculation. T.C. summarized the results and conclusions.

Funding

This research received no external funding.

Acknowledgments

The authors would like to thank the Environmental Protection Administration of Taiwan for providing the necessary data for analyses in this paper.

Conflicts of Interest

The authors declare no conflict of interest.

References

- OECD. Extended Producer Responsibility: A Guidance Manual for Governments; Organisation for Economic Co-operation and Development: Paris, France, 2001. [Google Scholar]

- European Parliament and of the Council. Directive 2002/96/EC of the European Parliament and of the Council of 27 January 2003 on Waste Electrical and Electronic Equipment (WEEE). Off. J. Eur. Union 2003, No. 96. L 37/24–L 37/39. [Google Scholar]

- Li, J.; Lin, M.; Liu, L. Producer Responsibility Extension System and Electronic Waste Recycling. In 2011 Circular Economy and Energy Saving Carbon Reduction; CTCI Foundation: Taipei, Taiwan, 2011; pp. 71–86. [Google Scholar]

- Wen, L.; Lo, S.F.; Lin, C.H. Assistance to Fee Committee Member’s Meeting Operation and Review of Recycling-and-Treatment Fee Structure; EPA-96-HA14-03-A127; Chung-Hua Institution for Economic Research: Taipei, Taiwan, 2007. [Google Scholar]

- Fan, K.S.; Lin, C.H.; Chang, T.C. Management and performance of Taiwan’s waste recycling fund. J. Air Waste Manag. Assoc. 2005, 55, 574–582. [Google Scholar]

- Wen, L.; Lee, C.H.; Chang, S.L.; Lin, C.H. Due-Recycling Articles Recycle Rate of Clearance and Disposal Fees Evaluation, Effectiveness and Review Program; EPA-91-HA31-03-A173; Chung-Hua Institution for Economic Research: Taipei, Taiwan, 2003. [Google Scholar]

- Wu, C.-L.; Wang, C.-H.; Wu, J. The Innovaton of Recycling System for Waste Household Appliances and Waste Electronics IT Objects; EPA-98-HA14-03-A177; SGS Taiwan Corporation: Taipei, Taiwan, 2009. [Google Scholar]

- Cheng, C.-P.; Chang, T.-C. The development and prospects of the waste electrical and electronic equipment recycling system in Taiwan. J. Mater. Cycles Waste Manag. 2017, 20, 667–677. [Google Scholar]

- Wang, C.-H.; Lee, Y.-W. Waste Home Appliance and IT Equipment Industrial Investigation and Fee Rate Structure Assessment Project; EPA-103-HA14-03-A058; E-Titanium International Inc.: Taipei, Taiwan, 2014. [Google Scholar]

- Wen, L.; Liao, L.-Q. Project on Investigating the Flow and Improving the Recycling Technology of Waste Home Appliances and IT Equipment Recycling; EPA-106-HA14-03-A066; Chung-Hua Institution for Economic Research: Taipei, Taiwan, 2017. [Google Scholar]

- Xu, Y.; Li, J.; Liu, L. Current Status and Future Perspective of Recycling Copper by Hydrometallurgy from Waste Printed Circuit Boards. Procedia Environ. Sci. 2016, 31, 162–170. [Google Scholar] [Green Version]

- Chang, T.-C.; Ku, Y. A Strategy and Analysis of E-Waste in Taiwan; EPA-105-H103-02-A295; National Taipei Technology University: Taipei, Taiwan, 2016. [Google Scholar]

- Recycling Fund Management Board Website. Available online: https://recycle.epa.gov.tw/en/index.html (accessed on 20 June 2019).

- Jiang, K.Y. Project of Planning Resource Recycling System and Promoting Design for Environment; EPA-96-H103-02-131; Institute of Environment and Resources: Taipei, Taiwan, 2007. [Google Scholar]

- Lin, C.-H. A model using home appliance ownership data to evaluate recycling policy performance. Resour. Conserv. Recycl. 2008, 52, 1322–1328. [Google Scholar]

- Qiu, X. Project of Management and Elevate Efficacy of Waste Home Appliances and Waste IT Equipment Selling and Recycling System; EPA-103-HA14-03-A037; SGS: Taipei, Taiwan, 2014. [Google Scholar]

- Hecht, J.E. National Environmental Account: Bridging the Gap between Ecology and Economy; Resources for the Future: Washington, DC, USA, 2004. [Google Scholar]

- United Nations; European Union; Food and Agriculture Organization of the United Nations; International Monetary Fund; Organisation for Economic Co-operation and Development; The World Bank. System of Environmental-Economic Accounting 2012—Central Framework; United Nations: New York, NY, USA, 2014. [Google Scholar]

- Eshet, T.; Ayalon, O.; Shechter, M. Valuation of externalities of selected waste management alternatives: A comparative review and analysis. Resour. Conserv. Recycl. 2006, 46, 335–364. [Google Scholar]

- Directorate-General of Budget, Accounting and Statistics (DGBAS). Green National Income (Environmental-Economic Account) for 2017; Directorate-General of Budget, Accounting and Statistics (DGBAS): Taipei, Taiwan, 2019. [Google Scholar]

- Shih, H.-S. Policy analysis on recycling fund management for E-waste in Taiwan under uncertainty. J. Clean. Prod. 2017, 143, 345–355. [Google Scholar]

- Rebitzer, G.; Nakamura, S. Environmental Life Cycle Costing. In Environmental Life Cycle Costing; Chapter 3; Hunkeler, H., Lichtenvort, K., Rebitzer, G., Eds.; CPC Press: Webster, NY, USA, 2008; pp. 35–58. [Google Scholar]

- Steen, B.; Hoppe, H.; Hunkeler, D.; Lichtenvort, K.; Schmidt, W.-P.; Spindler, E. Integrating External Effects into Life Cycle Costing in Environmental Life Cycling. In Environmental Life Cycle Costing; Chapter 4; Hunkeler, H., Lichtenvort, K., Rebitzer, G., Eds.; CPC Press: Webster, NY, USA, 2008; pp. 59–76. [Google Scholar]

Figure 1.

Main players in the recycling program in Taiwan.

Figure 2.

Recycling Fund Program Framework in Taiwan.

Figure 3.

Variations of annual WEEE recycling fee income and expense.

Figure 4.

Environmental impact cost investigation approaches for WEEE recycling.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table 1.

Current recycling fees for WEEE items in Taiwan (information technology products).

| Recycling Fee (NT$/Unit *) | |||||||

|---|---|---|---|---|---|---|---|

| PC a | Monitor | Laptop | Printer | Keyboard | |||

| Notebook | Panel | Laser | Ink-Jet | Dot-Matrix | |||

| 111 | 127 | 39 | 25.3 | 159 | 144 | 155 | 14 |

| 78 b | 89 b | 27b | 18 b | 151 b | 137 b | 147 b | 10 b |

Data source: RFMB, 2019. * US $1 is approximately equal to NT $30. a Personal computer containing printed circuit board, hard disk, power supply, and case shell. b Green Certified products with eco-labeling certifications are entitled to lower Green Recycling Fees, as of 2014.

Table 2.

Current recycling fees for WEEE in Taiwan (household appliances).

| Recycling Fee (NT$/Unit) | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| Television | Refrigerator | Washing Machine | Air Conditioner | Electrical Fan | |||||

| ≤27” | >27” | ≤250 L | 250 L | ≤12” | >12” | ||||

| CRT | LCD | CRT | LCD | ||||||

| 247 | 127 | 371 | 233 | 392 | 588 | 307 | 241 | 19 | 34 |

| 222 b | 114 b | 334 b | 210 b | 333 b | 500 b | 261 b | 205 b | 16 b | 29 b |

Data source: RFMB, 2019. b Green Certified products with eco-labeling certifications are entitled to lower Green Recycling Fees, as of 2014.

Table 3.

Principles of the estimated factors used in the recycling fee equation.

| Factors | Principles of Estimation/Calculation |

|---|---|

| C | The costs from the collection, transportation and recycling processes needed for both labor and equipment, minus revenue generated from the sales of secondary materials. |

| W | Substituted by the actual yearly sales amount of the mandatory recycling product, in the supposed year when the product was introduced to the market. |

| α | The target set by the RFMB and the EPAT. |

| E1 xα1 | The cost of collecting mandatory recycling products which are incorrectly or illegally disposed of into the municipal waste collection. Since residents are currently required to cover municipal waste collection through a unit pricing scheme, this cost is set to be 0 for producers in calculations. |

| E2 xα2 | The cost of the environmental impact from the improper disposal of mandatory recycling products, currently substituted by a planned budget, which is the annual amount of funding given by the RFMB to local municipal cleaning teams. |

| L | Administration cost including the expense for the work done by the Auditing and Certification Groups, the support of online reporting and auditing systems, and other administrative costs associated with research, auditing, and certification. |

| F | Fund balance amortization equal to: (Cumulative trust fund surplus—Amount set aside from the previous year’s surplus for the future management of the fund)/life span of the mandatory recycling product. |

| S | Forecasted annual sales amount estimated by the averaged actual sales in the previous three years. |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Cheng, C.-p.; Lin, C.-h.; Wen, L.-c.; Chang, T.-c. Determining Environmental Costs: A Challenge in A Governmental E-Waste Recycling Scheme. Sustainability 2019, 11, 5156. https://doi.org/10.3390/su11195156

AMA Style

Cheng C-p, Lin C-h, Wen L-c, Chang T-c. Determining Environmental Costs: A Challenge in A Governmental E-Waste Recycling Scheme. Sustainability. 2019; 11(19):5156. https://doi.org/10.3390/su11195156

Chicago/Turabian StyleCheng, Chii-pwu, Chun-hsu Lin, Lih-chyi Wen, and Tien-chin Chang. 2019. "Determining Environmental Costs: A Challenge in A Governmental E-Waste Recycling Scheme" Sustainability 11, no. 19: 5156. https://doi.org/10.3390/su11195156

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.