Sibling Rivalry vs. Brothers in Arms: The Contingency Effects of Involvement of Multiple Offsprings on Risk Taking in Family Firms

1

School of Management, University of Science and Technology of China, Hefei 230026, China

2

School of Economics, Hefei University of Technology, Hefei 230601, China

*

Author to whom correspondence should be addressed.

Sustainability 2019, 11(16), 4447; https://doi.org/10.3390/su11164447

Submission received: 14 July 2019

/

Revised: 9 August 2019

/

Accepted: 15 August 2019

/

Published: 16 August 2019

(This article belongs to the Special Issue Family Business Model and Practices of Sustainability)

Abstract

:Succession process is a significant matter that is vital to the sustainability of a family firm. Families are generous in involving the offspring(s) into the family business so as to fulfill inter-generational succession. In this paper, we concentrate on the issue on the results of the involvement of multiple offsprings in family firms. By using data collected from China listed family firms between 2009 and 2015, we reveal that there exist contingency effects of the involvement of multiple offsprings on risk taking in different phrases. The involvement of new offspring(s) that leads the sibling rivalry to happen would increase risk taking of the family firm in a short-term. While for those family firms in which offsprings serve together as brothers in arms, risk taking is even lower than that of family firms with no more than one offspring. Our findings have managerial implications for dealing with succession process and maintaining sustainability of family businesses.

1. Introduction

Family firms commonly refer to corporations that are controlled by their founders or by the founders’ families and heirs [1]. A typical difference between family firms and non-family firms is the composition of the board as well as the top manager team (TMT) of which family members occupy larger proportions [2,3]. For hundreds of years, family firms have played a significant role in economies and societies worldwide [4]. As a result, the issues on family business have gained extensive research attention. One of the most important and eternal issues is with respect to succession process [5], which is of great importance to the sustainability of family businesses. This might be derived from the low succession rate of family firms in surviving into the next generation [6]. The statistics of the U.S. Census Bureau have showed that only about 30% of family firms can survive into the second generation and even less into the third generation [7]. Therefore, the elder always attempts to involve the offspring(s) into family businesses as early as possible, so as to accelerate his/her familiarities and commitments toward the businesses.

The literature has indicated that the involvement of the offspring has significant effects on risk taking in family firms. For instance, Liu, et al. [8] found that second-generation involvement increases the family firm’s cash holdings; Weng and Chi [9] showed that the second-generation successor is more likely to diversify the family business. Relatively, however, the effect of involvement of multiple offsprings on the firm’s risk taking has received inadequate research attention. For those families with multiple offsprings, the elder generation usually wants to treat the offsprings equally and thus involves them into business successively [7,10]. Moreover, through the serving process that offsprings perform, the elder anticipates selecting the finest one to be the successor. By our statistics, more than 10% of listed family firms in China have the situation in which multiple offsprings serve on the board or in the top manager team. Before 2015, China implemented the One Child Policy since 1980s and it is reasonable to believe that the ratios of corporate nepotism in many other countries are likely to be higher than that of China.

Intuitively, the effect of involvement of multiple offsprings on the firm’s risk taking seems to be more subtle. On the one hand, apparently, engaging as many as offsprings to serve as executives can largely contribute to strengthening the family’s control over the firm. In doing so, the elder looks forward to full cooperation among the offsprings, namely “brothers in arms”, to advance the family business. Lim et al. [11] argued that “brothers in arms” remain cooperative and will generally frame the firm’s prospects in positive terms and thus exhibit risk aversion and pursue less risky resource commitments for the family business. Ideally, when brothers in arms, family members “meet-in-the-middle” and maintain stabilized operational strategies and thus risk taking in the firm are expected to be decreased. On the other hand, in contrast, the involvement of multiple offsprings is likely to cause potential trouble; i.e., so-called sibling rivalry. Sibling rivalry arises from conflicts over tangible or intangible resources and appears when ego, stress, disagreement, or inequality is perceived among brothers and sisters [12,13], which may result in conflicts among them along with increasing risk taking of the family business [14,15]. Though the elder chooses not to believe, the offsprings are very likely to fight for succession. The literature has argued that the sibling rivalry may result from two aspects, i.e., affect-based competition and strategy-based competition [13,16]. The affect-based competition fundamentally originates from inadequate or unequal cares from the elder during the offsprings’ childhood and hence the adult offsprings who were devoid of love try to adopt abhorrent acts to draw the elder generation’s attention. While the strategy-based competition lies in self-interests for the purpose of acquiring more succession resources, e.g., enhancing managerial position and ownership ratios. Either competition may lead to differences in decision-making and relational conflicts among the offsprings, which directly impact on risk taking in the firm [17]. Plenty of vivid cases in the real world have shown that the sibling rivalry is commonly devastating for the family business [18].

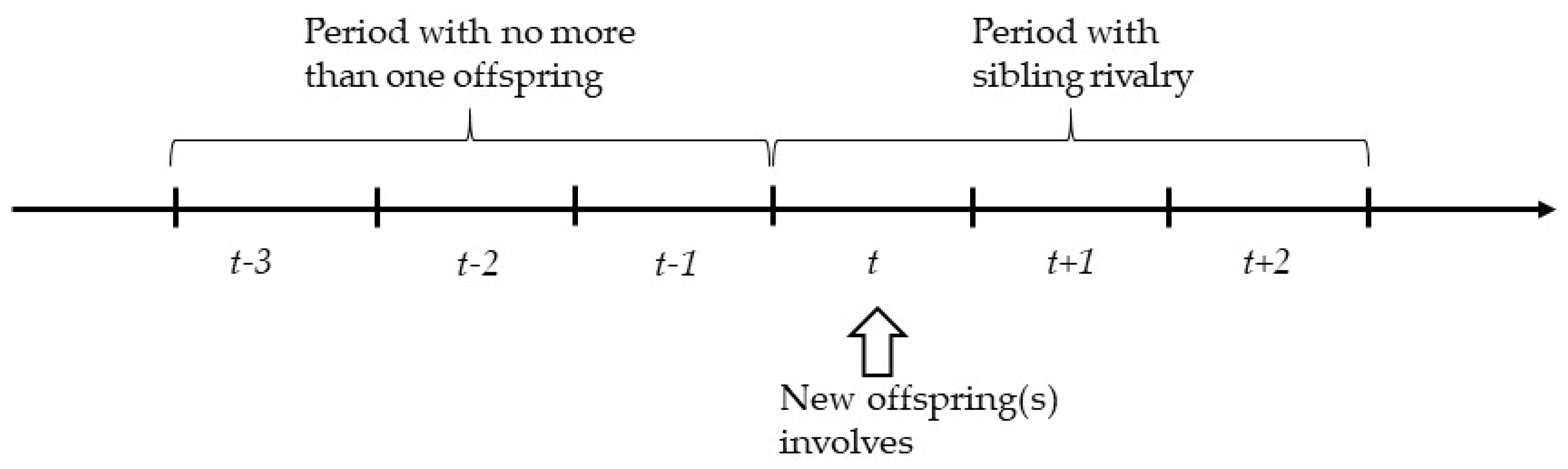

In this paper, we aim to propose a framework and provide empirical evidence to handle the contingency effects of different results of the involvement of multiple offsprings, i.e., the sibling rivalry and brothers in arms, on risk taking in family firms. As presented in Figure 1, we propose that a family with multiple offsprings may undergo three phrases. The first phrase is no competition in which there does not exceed one offspring who serves in the firm. While along with the involvement of new offspring(s) that causes the offsprings’ jointly involvement in the family business, the family firm enters into the second phrase, i.e., the sibling rivalry. The sibling rivalry is the unexpected by-product of the involvement of multiple offsprings and as previously argued it may be harmful to the development of family business. After being aware of the negative results of the sibling rivalry, the elder generation is presented three options: avoid, disregard, and reconcile. The first option retains no more than one offspring in the family firms, so as to avoid direct interactions among the offsprings. The second option is in general along with downfall of family business. While the third option is to reconcile the relationship among the offsprings, the concept of brothers in arms comes into play.

In this paper, to examine the above framework as well as the contingency effects of the involvement of multiple offsprings on risk taking in family firms, we will mainly focus on two questions:

- whether the involvement of new offspring(s) that causes the sibling rivalry can increase risk taking of family firms;

- whether brothers in arms can decrease risk taking of family firms.

Accordingly, we respectively employ two studies to address above two questions. In the first study, building on tournament theory [19], we deal with the effect of sibling rivalry caused by the involvement of new offspring(s) on risk taking of family firms. We regard the involvement of new offspring(s) as a treatment and hence utilize a difference-in-difference (DID) regression model based on the propensity score matching (PSM) approach, which is widely used to estimate the effect of a treatment. Then, in the second study, underpinning on socio-emotional wealth (SEW) theory [20], we handle the effect of brothers in arms where multiple offsprings serve together for a long-term period on risk taking of family firms. Likewise, we use a baseline regression based on the PSM approach. Finally, we conclude our findings and discuss managerial implications and further research pathways.

This paper contributes to the literature in several ways. First, this paper contributes to the literature on inter-generational succession of family firms, by revealing the contingency effects of the involvement of multiple offsprings on risk taking of family businesses in the succession process. Considering that only few studies of the involvement of multiple second-generations, this paper fills the gap in the consequences of involvement of multiple second-generations. Second, this paper provides evidence to the literature on risk taking in tournaments. Since raised, tournaments have been regarded as an effective way to select better contestants. Over the past two decades, however, emerging studies on tournaments have indicated that competition among contestants is likely to promote them to adopt risk-taking so as to enhance their winning probabilities [21]. In Study 1, we suggest that the involvement of new offspring(s) can lead to the sibling rivalry at least in the short-term, finally resulting in the enhancement of risk taking of the family business. Hence, this finding provides new practical evidence to embody contestants’ risk taking in tournaments. Third, this paper enriches the literature on SEW of family firms. Our Study 2 indicates that when multiple offsprings serve together for a long-term, implying a high level of SEW within families, risk taking of family firms is even lower than that of family firms with no more than one offspring. This result provides evidence to highlight the significance of SEW within the family firm. Moreover, our findings also have managerial implications for family business practice.

2. Study 1: The Effect of Sibling Rivalry on Risk Taking

2.1. Hypothesis Development

When new offspring(s) are involved so that multiple offsprings concurrently serve in the family business, a sibling rivalry is likely to happen. The sibling rivalry is defined as “the competitive relationship between siblings and is often associated with the struggle for parental attention, affection and approval, but also for recognition in the world” [15]. The competitive relationship comes from their either affect-based or strategy-based inner activities. The offsprings’ affect-based inner activities aim to seek self-actualization after involving the family business and then lead them to compete for more attention and recognition from the elder. While the strategy-based inner activities lie in personal self-interests and motivate the offsprings to fight for seizing more tangible resources, such as promotion to higher position and ownership enhancement.

The sibling rivalry is effectively a tournament or a contest. As tournament theory argued, when any offspring obtains extra tangible or intangible resources from the elder, there has crowding-out effect on the others. Though traditional tournament theory supported for competition in order to promote selection efficiency, new theoretical and empirical studies over the past two decades had revealed that contestants may take risky acts to enhance their winning probabilities [21]. Similarly, in the sibling rivalry, each offspring may adopt risk taking behaviors to enhance his/her own winning probabilities, so as to acquire more managerial power or ownership.

Furthermore, the sibling rivalry is also likely to cause relational conflicts among the offsprings [22]. Schlippe and Großmann [23] argued that the family business is the breeding ground of conflicts. In family firms, relational conflicts often derive from personal incompatibility among family members. The inheriting tournament among the offsprings is likely to a key inducement of such incompatibility. In addition, differences in educational backgrounds and values between the new involved offspring(s) and the previous involved offspring further enlarge such incompatibility, which reflect relational conflicts [24]. Relational conflicts would lead to hostile behaviors among the offsprings, e.g., inconsistencies in business decision-making and reduce the cooperation within the family members [25]. Noncooperation and divarication are likely to lead to large uncertainty and performance fluctuation of the family business and even put the family firm on the brink of a deep gulf. As a result, to address these conflicts, family firms may adopt risky acts which can lead the level of risk taking of the family business to be enhanced [26]. Thus, underpinning on tournament theory, we propose that:

Hypothesis 1.

The involvement of new offspring(s) which leads the sibling rivalry to happen within the family firms has positively effect on risk taking of the family business in a short-term.

2.2. Research Design

2.2.1. Sample

The sample in this study is collected from China public listed companies from 2009 to 2015. Though the family firm has a simple definition that refers to a corporation or business owned and or managed by a family, there were various screening standards of the family firm in prior empirical studies [27]. Combining the standards in the literature, we define that a family firm should satisfy the following standards concurrently: (1) the firm’s actual controller is a natural person or a family; (2) the control rights of the firm’s actual controller is not less than 20%; and (3) there are at least two members of the actual controller’s family (including the controller) serving on the board or in the top manager team.

We first collect the sample data from the subset of the China Stock Market and Accounting Research (CSMAR) database and then confirmed the relations regarding each firm’s family members through their Initial Public Offerings (IPO) prospectuses and the Sina website. After excluding family firms in the financial section, the amount of listed family firms in China between 2009 and 2015 has been shown in Table 1. On this basis, we single out the family firms with two or more offsprings who are serving on the board or in the TMT in each year during this period. It should be noted that if there are two offsprings who are husband and wife, they will be regarded as one-unit offspring. Then, we further pick out the family firms in each year in which there occurs more than one offsprings serving on the board or in the TMT due to the involvement of new offspring(s) in this year, while there was no more than one offspring served in the previous year.

All the results are listed in the Table 1. “Amount of FFs” indicates total number of family firms which satisfy above three standards concurrently in each sample year. “Amount of FFs with more than one offsprings involved” is the total number of family firms in which there existed the sibling rivalry caused by the involvement of new offspring(s) in each sample year. “Amount of FFs from no sibling rivalry to sibling rivalry” is the total number of family firms in which there were at least two offsprings serving in the firm in current year while there is no more than one offspring serving in the firm in the previous year.

2.2.2. Methodology

The involvement of new offspring(s) can be regarded as an intervention. Hence, to test our hypothesis, a difference-in-difference (DID) method based on propensity score matching (PSM) approach is adopted. DID is widely used to estimate the effect of an intervention event by establishing a counter-factual framework, so as to evaluate the changes of observed factors between the intervention group and the non-intervention group (i.e., control group) [28,29]. According the principle of DID method, the first difference of DID is used to eliminate the time-invariant heterogeneity of samples, and the second difference of DID is to eliminate the time-variant increment, and finally, the net effect of intervention is obtained. In this paper, the DID regression model is given by:

where indicates the level of risk taking in the family firm before () and after () the sibling rivalry caused by the involvement of new offspring(s), is a dummy variable that if it equals one the family firm belongs to the intervention group else it equals zero, is a time dummy variable that indicates the period before (), and after () the sibling rivalry, accordingly, is the interaction term, and the coefficient on such interaction term (i.e., ) suggests the net effect of the sibling rivalry caused by the involvement of new offspring(s). If is positive at a significant level, it indicates that the sibling rivalry can indeed lead to enhancement of risk taking in family firms. In addition, is a combination of control variables, and is a random term.

In order to reduce the heterogeneity bias and endogeneity caused by sample selection bias and confounding factors in the DID analysis [30,31], we further adopt a propensity score matching (PSM) approach to identify a set of family firms as the control group that matches with those of intervention group. The steps of PSM approach are handled as follows [32,33]. First, we choose covariates as matching variables. Second, we calculate propensity score and matching. By using the logit regression based on covariates, we obtain the propensity scores of samples of both the intervention group and the control group. Then, each sample of the intervention group will be matched with several samples of the control group. The commonly used K-nearest neighbor matching method is adopted in this paper ().

2.2.3. Variable Measurements

Risk taking: Following Boubakri et al. [34], we use the volatility of adjusted ROA during the observed period to measure risk taking of family firms. First, we calculate each firm’s annual ROA by dividing earnings before interest, taxes, depreciation and amortization (EBITDA) by the firm’s total assets at the end of year [35,36]. Second, each firm’s adjusted annual ROA is calculated using its annual ROA minus the average value of industry in which the firm is affiliated. Finally, risk taking of the family firms is calculated by:

where indicates adjusted ROA of family firm in year during the observation period, is the total years of the observation period, is the amount of all listed companies in the industry in which the firm is affiliated. Given that the sibling rivalry caused by the involvement of new offspring(s) may have effect on risk taking of the family business in a short-term, we consider a three years observation period (i.e., ), and compare the level of risk taking during the observation period before the involvement with that after the involvement, as shown in Figure 2.

Sibling rivalry: As previously described in the DID method, the sibling rivalry caused by the involvement of new offspring(s) is a dummy variable which is indicated by the interaction item in the formula (1).

Covariates and control variables: Caliendo and Kopeinig [33] pointed out that only variables that affect both the outcome variables and the probability of intervention happening can be used as covariates. Thus, we choose the controller’s age (Age) and the family firm scale as the covariates to handle the PSM analysis. The controller’s age is usually an important factor that drives him/her or his/her family to involve new offspring(s) into the family business, and accordingly, positively affect the probability of the involvement of new offspring(s). Simultaneously, the controller’s age often affects his/her planning of business operations which in return can impact on risk taking of the firm. Similarly, the family in general tends to involve more offsprings into the board or the TMT along with the increase of business scale, in order to ensure the family’s control of the business. In addition, the firm scale is naturally a significant factor that can determine the firm’s level of risk taking. Specifically, the family scale is measured by the natural logarithm of its total assets (Asset). As most literatures did [37,38,39], the controller’s age (Age) and the firm’s scale (Asset) are further adopted as control variables in the DID regression models. It should be noted that considering risk taking of family firms has eliminated industrial effects by using adjusted ROA, we no longer control the industrial factors in the DID model.

In order to describe the variables more clearly and briefly, we display descriptions of variables in Table 2 below.

2.3. Empirical Results

The changes of the family firm’s controller would largely influence the firm’s risk taking. Thus, before dealing with the PSM analysis, we remove the family firms whose controller changed between 2009 and 2015. Then, we obtain 463 alternative sample firms. By using K-nearest neighbor matching (), finally, there remain 19 firms in the intervention group and 60 firms in the control group.

We handle the balance test of PSM as shown in Table 3. The balance test results indicate that the sample in 2012 was excluded because there is no firm of the control group which can match with it. According to [40,41], the absolute value of standard deviation of covariates after matching should be less than 20. Table 3 shows that the matching estimations in each year are reliable. In addition, the t-test after matching in each year are not significant at 10% statistical level. It means that there is no significant difference between the intervention group and the matched control group, such that the sample selection bias could be avoided.

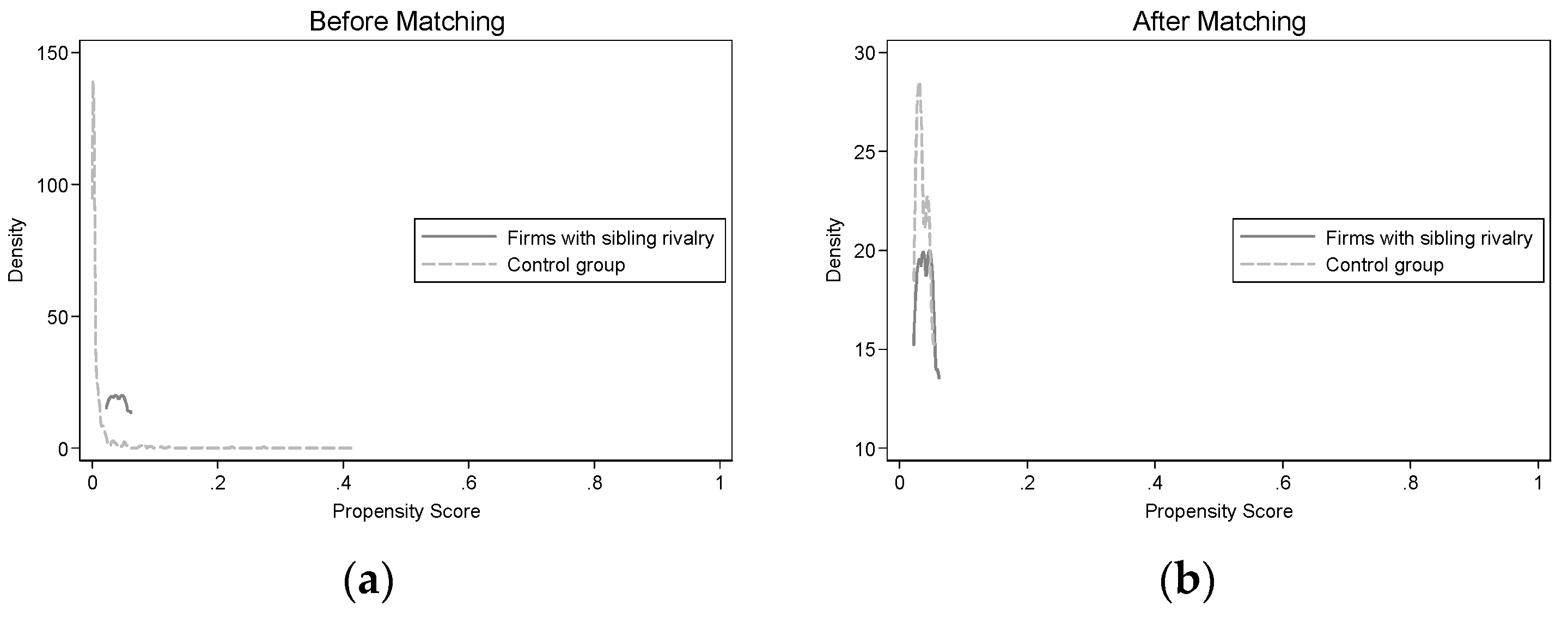

Then, in order to strengthen the effectiveness and visualization of matching results, Figure 3, Figure 4, Figure 5, Figure 6, Figure 7 and Figure 8 show the Kernel density functions of the treatment group and the control group pre- and post-matching. It can be seen that after matching, the Kernel density functions of the treatment group (firms with sibling rivalry) and the control group are much close. This indicates that samples in the control group are comparable relative to those in the treatment group and thus the heterogeneity bias and endogeneity caused by sample selection bias are largely removed.

The results of DID regression are shown in Table 4. As most prior studies did [42], we exclude control variables in Model 1 and add control variables, i.e., the controller’s age and the family firms’ assets, into Model 2. It can be found that the coefficient on the interaction term of the DID regression model after adding control variables changes non-significantly comparing to that without control variables. Furthermore, the coefficient on the interaction term in Model 2 is significant at 5% statistical level. We have also estimated variance inflation factor (VIF) for checking multicollinearity. The largest value of VIF is 2.32, which is much less than the common threshold value (VIF < 5). Consequently, there is no need to worry about multicollinearity toward our regression models [43].

In short, the result demonstrates that the level of risk taking of a family firm would be indeed increased in a short-term if there exists the sibling rivalry caused by the involvement of new offspring(s). Then, Hypothesis 1 is supported.

3. Study 2: The Effect of Brothers in Arms on Risk Taking

3.1. Hypothesis Development

When the sibling rivalry caused by the involvement of new offspring(s) gives rise to conflicts among offsprings, in addition to an increase in risk taking towards the family business, such negative consequence would often be observed in nature by the elder. Apparently, the elder would not remain idle and allows the evolution or even redouble of the sibling rivalry which leads to larger performance fluctuations and even business crises. In general, the preferential reaction of most families is to reconcile the relationship among offsprings to build a breeding ground for groupthink [44]. By adjusting positions, authorities or ownerships and etc., the family elder expects to improve the balance and reduce relationship conflicts among the offsprins. In reality, however, the reconciliation in most family firms does not work, instead intensifies the sibling rivalry among offsprings. It is because that some of offsprings might benefit from the adjustments while others would feel unfairness. Finally, to avoid more serous results of the sibling rivalry, the elder has to take extra actions, e.g., withdrawing some of offsprings and positioning them in other business units of the family to evade direct intersections between the conflict parties. This might be the underlying reason why there are in reality only a few proportions (about 10% in China mainland) of family firms in which more than one offsprings serve together, as shown in Table 1.

While for those families which succeed in the reconciliation, the relationship among offsprings will become harmonious and consequently the scene of “brothers in arms” will come into play. The underpinned theoretical foundation of brothers in arms comes from socioemotional wealth [20,45]. The fundamental of socioemotional wealth in family firms is that “Family owners frame problems in terms of assessing how actions will affect socioemotional endowment. When there is a threat to that endowment, the family is willing to make decisions that are not driven by an economic logic [46], and in fact the family would be willing to put the firm at risk if this is what it would take to preserve that endowment” [47]. The pursuit of socioemotional wealth creates a strong sense of belonging for family members and prompts them to enhance altruism which improves the reciprocity and cooperation within the family which discourages risk taking [48,49]. In consequence, as the primal wish of the elder, the situation in which multiple offsprings serve together would continue to be sustainable, such that the involvement of multiple offsprings will heighten the family’s control towards the firm’s business. As a result, under “brothers in arms”, the strategic decision-making and execution of the family business would be more stable and reliable, and in turn the firm’s risk taking would be decreased [50,51,52]. Thus, we propose that:

Hypothesis 2.

Brothers in arms in family firms in which multiple offsprings serve together for a long-term period has negatively effect on risk taking of those firms during such period.

3.2. Research Design

3.2.1. Sample

In this study, family firms are defined the same as Study 1. Based on the collected samples shown in Table 1, we figure out the family firms in which more than one offsprings are involved and there was no change of their control families from 2009 and 2015. To ensure that the offsprings have served together harmoniously for a long time, we further screen out the family firms whose served offsprings remained unchanged between 2009 and 2015. Finally, we obtain 48 qualified family firm samples as the treatment group. In addition, 463 family firms in which no more than one offspring served and the control families also remained unchanged between 2009 and 2015 are selected as the initial control group.

3.2.2. Methodology

Moreover, to eliminate heterogeneity bias and endogeneity caused by sample selection bias and confounding factors, we adopt a baseline regression model after the sample matching based on the PSM approach [53]. The baseline regression model is given by:

where indicates the level of risk taking of family firm during the observed period; is a dummy variable which is used to indicate whether the firm is the sample under the situation of brothers in arms ( indicates that family firm is the sample in which multiple offsprings serve together harmoniously for a long-term, while indicates family firm is the sample which belongs to the control group). In addition, is a set of control variables, and is the random term.

3.2.3. Variable Measurements

Risk taking: In this study, risk taking of family firms is also measured by the profit volatility during the observed period as Study 1 did. Considering a part of family firm samples involved multiple offsprings in 2009, the observed period in this study is set from 2011 to 2015. Furthermore, to make sure the robustness of our findings, we also test the level of risk taking of family firms between 2011 and 2013, 2012 and 2014, and 2013 and 2015.

Brothers in arms: As previously described, brothers in arms is measured by a dummy variable, denoted by in the formula (3). equals one if family firm is under the situation of brothers in arms, otherwise it equals zero.

Covariate and control variables: In the PSM analysis, we also choose the controller’s age (Age) and family firm scale (Asset) as the covariates. The measurements of both the variables have been described in Study 1. In addition, the covariates are also used as control variables in baseline regression models.

3.3. Empirical Results

By using Stata12.0, 48 qualified family firm samples are matched with those firms of above initial control group based on K-nearest neighbor matching method (K = 4). Then, we obtain the intervention group with 47 family firms and the matched control group with 104 family firms.

Table 5 reports the balance test of PSM. The balance test shows that the absolute values of standard deviation of covariates after matching are less than 20, and t-test after matching are not significant at 10% statistical level. It indicates that the matching results are reliable and there are no significant differences between the intervention group and the matched control group.

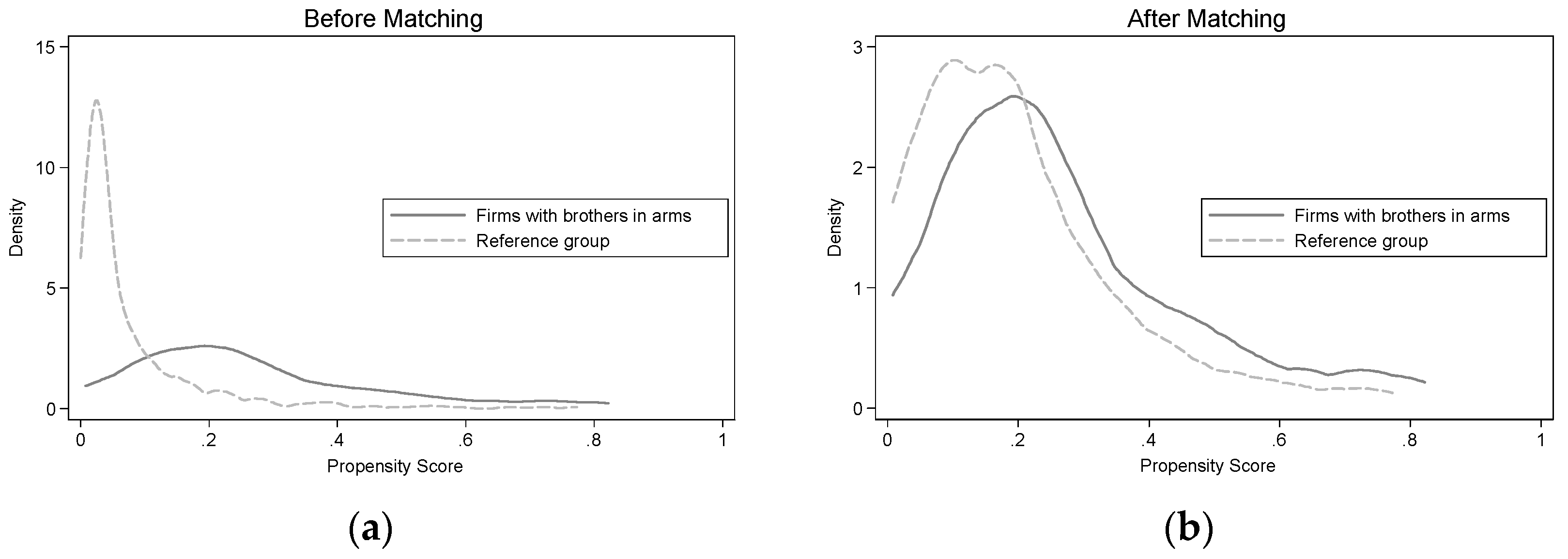

As Study 1 did, we plot the Kernel density functions of the treatment group (firms with brother in arms) and the control group pre- and post-matching, as Figure 9 shows. Similarly, after matching, the Kernel density functions of the treatment group and the control group are much close.

Descriptive statistics of the matched samples are shown in Table 6.

Table 7 shows the results of baseline regression. Model 3 and 4 suggest that the level of risk taking of family firms in which multiple offsprings serve harmoniously is significantly lower than that of family firms in which no more than one offspring serves, at the 5% significant level and the variance inflation factor (VIF) test shows that the multicollinearity is not a concern for any of the variables in the period between 2011 and 2015, because that the largest value of VIF is 1.03. This also implies that brothers in arms indeed contributes to decreasing risk taking of family firms. The finding is robust even when we further test the level of risk taking of family firms during subset periods, as shown in Model 5 to Model 10. Thus, Hypothesis 2 is supported.

4. Conclusions and Discussion

The succession process is a significant aspect which is vital to sustainability of a family firm. Families through the ages have being generous in involving the offsprings into the family business, although their involvement may give rise to various potential consequences such as the sibling rivalry and brothers in arms. In this paper, we handle the issue on the results of the involvement of multiple offsprings in family firms. We propose a framework to illustrate the advance as well as the contingency effects of the involvement of multiple offsprings. To advocate this, based on a collected data of China listed family firms between 2009 and 2015, we deal with two studies that test the effects of sibling rivalry and brothers in arms on risk taking of family firms, respectively.

Study 1 demonstrates that the involvement of new offspring(s) which leads the sibling rivalry to happen positively affects risk taking of the family business in a short-term. In general, the involvement of new offspring(s) would result in a crowding-out effect on either the tangible resources (e.g., managerial power and ownership) or intangible resources (e.g., affective attention from the elder) of existing offsprings. It may lead to an invisible even visible battle between them, namely, the sibling rivalry, while along with many adverse consequences such as relationship conflicts. The sibling rivalry would increase risk taking of the family business at least in a short-term.

Study 2 reveals that the situation in which the offsprings serve together for a long-term period, that is, brothers in arms, has negatively effect on risk taking of the family business. After the phrase of the sibling rivalry, intuitively, the continuous involvement jointly in the family business implies at least a harmonious relationship among the offsprings. During such period, altruism and reciprocity continue to take the lead and thus enhance the cohesiveness of the family. Benefit from this, the firm’s strategy and operation would maintain stable, and accordingly the firm’s risk taking will be decreased.

The findings provide several managerial implications for family firms. First, the sibling rivalry is likely to endanger the sustainability of family businesses. Families should keep close watch on the interaction among offsprings after new offspring(s) involves, and take measures to avoid the spread of the sibling rivalry in time. Second, families ought to enhance socioemotional wealth, including sense of belongingness, closeness and etc., which can contribute to decreasing risk taking of family businesses.

To enrich the literature on succession of family businesses, we also highlight some further research issues. As the relationships between our variables, further research may make efforts in finding the mediating factors that can link the sibling rivalry, brothers in arms and risk taking of family firms. In addition, scholars may further explore other consequences of the sibling rivalry and bothers in arms, especially under different national cultures. Furthermore, case study may be also worth trying to provide practical evidence to present the results of the sibling rivalry versus brother in arms.

Author Contributions

Conceptualization, C.W. and Q.W.; methodology, C.W. and J.C.; software, J.C.; formal analysis, J.C. and C.W.; investigation, J.C.; data curation, J.C.; writing—original draft preparation, J.C.; writing—review and editing, C.W. and Q.W.; visualization, C.W.; supervision, B.L.; project administration, C.W. and B.L.; funding acquisition, C.W. and Q.W.

Funding

This research was funded by the National Natural Science Foundation of China, grant number 71701193 and 71804040.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Xu, N.; Yuan, Q.; Jiang, X.; Chan, K.C. Founder’s political connections, second generation involvement, and family firm performance: Evidence from China. J. Corp. Financ. 2015, 33, 243–259. [Google Scholar] [CrossRef]

- Achmad, T.; Semarang, I.; Rusmin, R. The Iniquitous Influence of Family Ownership Structures on Corporate Performance. J. Glob. Bus. Issues 2009, 3, 41–49. [Google Scholar]

- Gallo, M.Á.; Tàpies, J.; Cappuyns, K. Comparison of Family and Nonfamily Business: Financial Logic and Personal Preferences. Fam. Bus. Rev. 2004, 17, 303–318. [Google Scholar] [CrossRef]

- Cheng, Q. Family firm research—A review. China J. Account. Res. 2014, 7, 149–163. [Google Scholar] [CrossRef]

- Bizri, R. Succession in the family business: Drivers and pathways. Int. J. Entrep. Behav. Res. 2016, 22, 133–154. [Google Scholar] [CrossRef]

- Ramadani, V.; Bexheti, A.; Rexhepi, G.; Ratten, V.; Ibraimi, S. Succession Issues in Albanian Family Businesses: Exploratory Research. J. Balk. Near East. Stud. 2017, 19, 294–312. [Google Scholar] [CrossRef]

- Gaumer, C.J.; Shaffer, K.J. Family business succession: Impact on supplier relations and customer management. Hum. Resour. Manag. Int. Dig. 2018, 26, 1–4. [Google Scholar] [CrossRef]

- Liu, Q.; Luo, T.; Tian, G.G. Family control and corporate cash holdings: Evidence from China. J. Corp. Financ. 2015, 31, 220–245. [Google Scholar] [CrossRef] [Green Version]

- Weng, T.-C.; Chi, H.-Y. Family succession and business diversification: Evidence from China. Pac. Basin Financ. J. 2019, 53, 56–81. [Google Scholar] [CrossRef]

- Bertrand, M.; Johnson, S.; Samphantharak, K.; Schoar, A. Mixing family with business: A study of Thai business groups and the families behind them. J. Financ. Econ. 2008, 88, 466–498. [Google Scholar] [CrossRef] [Green Version]

- Lim, E.N.K.; Lubatkin, M.H.; Wiseman, R.M. A family firm variant of the behavioral agency theory. Strateg. Entrep. J. 2010, 4, 197–211. [Google Scholar] [CrossRef]

- Vera, C.F.; Dean, M.A. An Examination of the Challenges Daughters Face in Family Business Succession. Fam. Bus. Rev. 2005, 18, 321–345. [Google Scholar] [CrossRef]

- Levesque, R.J.R. Sibling Rivalry. In Encyclopedia of Adolescence; Levesque, R.J.R., Ed.; Springer International Publishing: Cham, Switzerland, 2018; p. 3606. [Google Scholar] [CrossRef]

- Friedman, S.D. Sibling Relationships and Intergenerational Succession in Family Firms. Fam. Bus. Rev. 1991, 4, 3–20. [Google Scholar] [CrossRef]

- Avloniti, A.; Iatridou, A.; Kaloupsis, I.; Vozikis, G.S. Sibling rivalry: Implications for the family business succession process. Int. Entrep. Manag. J. 2014, 10, 661–678. [Google Scholar] [CrossRef]

- Kiselica, M.S.; Morrill-Richards, M. Sibling Maltreatment: The Forgotten Abuse. J. Couns. Dev. 2007, 85, 148–160. [Google Scholar] [CrossRef]

- Memili, E. The importance of looking toward the future and building on the past: Entrepreneurial risk taking and image in family firms. In Entrepreneurship and Family Business; Eddleston Kimberly, A., Alex, S., Lumpkin, G.T., Jerome, A.K., Eds.; Emerald Group Publishing Limited: Bingley, UK, 2010; Volume 12, pp. 3–29. [Google Scholar]

- Mokhber, M.; Gi Gi, T.; Abdul Rasid, S.Z.; Vakilbashi, A.; Mohd Zamil, N.; Woon Seng, Y. Succession planning and family business performance in SMEs. J. Manag. Dev. 2017, 36, 330–347. [Google Scholar] [CrossRef]

- Lazear, E.P.; Rosen, S. Rank-Order Tournaments as Optimum Labor Contracts. J. Political Econ. 1981, 89, 841–864. [Google Scholar] [CrossRef] [Green Version]

- Gómez-Mejía, L.R.; Haynes, K.T.; Núñez-Nickel, M.; Jacobson, K.J.L.; Moyano-Fuentes, J. Socioemotional wealth and business risks in family-controlled firms: Evidence from spanish olive oil mills. Adm. Sci. Q. 2007, 52, 106–137. [Google Scholar] [CrossRef]

- Li, Z.; Wang, C.; Wang, Q.; Luo, B. A review on risk-taking in tournaments. J. Model. Manag. 2019, 14, 559–568. [Google Scholar] [CrossRef]

- Caputo, A.; Marzi, G.; Pellegrini, M.M.; Rialti, R. Conflict management in family businesses: A bibliometric analysis and systematic literature review. Int. J. Confl. Manag. 2018, 29, 519–542. [Google Scholar] [CrossRef]

- Schlippe, A.V.; Großmann, S. Family businesses: Fertile environments for conflict. J. Fam. Bus. Manag. 2015, 5, 294–314. [Google Scholar] [CrossRef]

- Ben-Hafaïedh, C. Research Handbook on Entrepreneurial Teams: Theory and Practice; Edward Elgar Publishing: Cheltenham, UK, 2017. [Google Scholar]

- Eddleston, K.A.; Kellermanns, F.W. Destructive and productive family relationships: A stewardship theory perspective. J. Bus. Ventur. 2007, 22, 545–565. [Google Scholar] [CrossRef]

- Wang, Y. Entrepreneurial risk taking: Empirical evidence from UK family firms. Int. J. Entrep. Behav. Res. 2010, 16, 370–388. [Google Scholar] [CrossRef]

- Corten, M.; Steijvers, T.; Lybaert, N. The effect of intrafamily agency conflicts on audit demand in private family firms: The moderating role of the board of directors. J. Fam. Bus. Strategy 2017, 8, 13–28. [Google Scholar] [CrossRef]

- Abadie, A. Semiparametric Difference-in-Differences Estimators. Rev. Econ. Stud. 2005, 72, 1–19. [Google Scholar] [CrossRef]

- Khandker, S.B.K.G.S.H. Handbook on Impact Evaluation; The World Bank: Washington, DC, USA, 2009; p. 239. [Google Scholar] [CrossRef]

- Imbens, G.W.; Wooldridge, J.M. Recent developments in the Econometrics of Program Evaluation. J. Econ. Lit. 2009, 47, 5–86. [Google Scholar] [CrossRef]

- Lechner, M. The Estimation of Causal Effects by Difference-in-Difference MethodsEstimation of Spatial Panels. Found. Trends® Econom. 2010, 4, 165–224. [Google Scholar] [CrossRef] [Green Version]

- Abadie, A.; Imbens, G.W. Matching on the Estimated Propensity Score. Econometrica 2016, 84, 781–807. [Google Scholar] [CrossRef]

- Caliendo, M.; Kopeinig, S. Some practical guidance for the implementation of propensity score matching. J. Econ. Surv. 2008, 22, 31–72. [Google Scholar] [CrossRef]

- Boubakri, N.; Cosset, J.-C.; Saffar, W. The role of state and foreign owners in corporate risk-taking: Evidence from privatization. J. Financ. Econ. 2013, 108, 641–658. [Google Scholar] [CrossRef]

- John, K.; Litov, L.; Yeung, B. Corporate Governance and Risk-Taking. J. Financ. 2008, 63, 1679–1728. [Google Scholar] [CrossRef]

- Li, K.; Griffin, D.; Yue, H.; Zhao, L. How does culture influence corporate risk-taking? J. Corp. Financ. 2013, 23, 1–22. [Google Scholar] [CrossRef]

- Boeker, W.; Fleming, B. Parent firm effects on founder turnover: Parent success, founder legitimacy, and founder tenure. Strateg. Entrep. J. 2010, 4, 252–267. [Google Scholar] [CrossRef]

- Koirala, S.; Marshall, A.; Neupane, S.; Thapa, C. Corporate governance reform and risk-taking: Evidence from a quasi-natural experiment in an emerging market. J. Corp. Financ. 2018. [Google Scholar] [CrossRef]

- Doyle, O.; Hegarty, M.; Owens, C. Population-Based System of Parenting Support to Reduce the Prevalence of Child Social, Emotional, and Behavioural Problems: Difference-In-Differences Study. Prev. Sci. 2018, 19, 772–781. [Google Scholar] [CrossRef] [PubMed]

- Elliott, R.J.R.; Jabbour, L.; Zhang, L. Firm productivity and importing: Evidence from Chinese manufacturing firms. Can. J. Econ./Rev. Can. D’économique 2016, 49, 1086–1124. [Google Scholar] [CrossRef] [Green Version]

- Rosenbaum, P.R.; Rubin, D.B. Constructing a control group using Multivariate Matched Sampling Methods That Incorporate the Propensity Score. Am. Stat. 1985, 39, 33–38. [Google Scholar] [CrossRef]

- Del Prete, D.; Giovannetti, G.; Marvasi, E. Global value chains participation and productivity gains for North African firms. Rev. World Econ. 2017, 153, 675–701. [Google Scholar] [CrossRef]

- Jara-Bertin, M.; López-Iturriaga, F.J.; López-de-Foronda, Ó. The Contest to the Control in European Family Firms: How Other Shareholders Affect Firm Value. Corp. Gov. Int. Rev. 2008, 16, 146–159. [Google Scholar] [CrossRef]

- Schjoedt, L.; Monsen, E.; Pearson, A.; Barnett, T.; Chrisman, J.J. New Venture and Family Business Teams: Understanding Team Formation, Composition, Behaviors, and Performance. Entrep. Theory Pract. 2013, 37, 1–15. [Google Scholar] [CrossRef]

- Schulze, W.S.; Kellermanns, F.W. Reifying Socioemotional Wealth. Entrep. Theory Pract. 2015, 39, 447–459. [Google Scholar] [CrossRef]

- Sharma, P.; Melin, L.; Nordqvist, M. The SAGE Handbook of Family Business; Sage: Newcastle upon Tyne, UK, 2013. [Google Scholar]

- Berrone, P.; Cruz, C.; Gomez-Mejia, L.R. Socioemotional Wealth in family firms: Theoretical dimensions, assessment approaches, and agenda for future research. Fam. Bus. Rev. 2012, 25, 258–279. [Google Scholar] [CrossRef]

- Huybrechts, J.; Voordeckers, W.; Lybaert, N. Entrepreneurial Risk Taking of Private Family Firms The Influence of a Nonfamily CEO and the Moderating Effect of CEO Tenure. Fam. Bus. Rev. 2013, 26, 161–179. [Google Scholar] [CrossRef]

- Gottardo, P.; Moisello, A. Family firms, risk-taking and financial distress. Probl. Perspect. Manag. 2017, 15, 168–177. [Google Scholar] [CrossRef] [Green Version]

- Naldi, L.; Nordqvist, M.; Sjöberg, K.; Wiklund, J. Entrepreneurial Orientation, Risk Taking, and Performance in Family Firms. Fam. Bus. Rev. 2007, 20, 33–47. [Google Scholar] [CrossRef]

- Zahra, S.A. Entrepreneurial Risk Taking in Family Firms. Fam. Bus. Rev. 2005, 18, 23–40. [Google Scholar] [CrossRef]

- Hiebl Martin, R.W. Risk aversion in family firms: What do we really know? J. Risk Financ. 2013, 14, 49–70. [Google Scholar] [CrossRef]

- Vicarelli, C.; Costa, S.; Pappalardo, C. Internationalization Choices and Italian Firm Performance during the Crisis. Small Bus. Econ. 2015, 48, 753–769. [Google Scholar] [CrossRef]

Figure 1.

Framework of development phrases of involvement of multiple offsprings.

Figure 2.

Example for the observation periods before and after the involvement of new offspring(s).

Figure 3.

The Kernel density functions before and after matching in 2015. (a): Before Matching; (b): After Matching.

Figure 3.

The Kernel density functions before and after matching in 2015. (a): Before Matching; (b): After Matching.

Figure 4.

The Kernel density functions before and after matching in 2014. (a): Before Matching; (b): After Matching.

Figure 4.

The Kernel density functions before and after matching in 2014. (a): Before Matching; (b): After Matching.

Figure 5.

The Kernel density functions before and after matching in 2013. (a): Before Matching; (b): After Matching.

Figure 5.

The Kernel density functions before and after matching in 2013. (a): Before Matching; (b): After Matching.

Figure 6.

The Kernel density functions before and after matching in 2011. (a): Before Matching; (b): After Matching.

Figure 6.

The Kernel density functions before and after matching in 2011. (a): Before Matching; (b): After Matching.

Figure 7.

The Kernel density functions before and after matching in 2010. (a): Before Matching; (b): After Matching.

Figure 7.

The Kernel density functions before and after matching in 2010. (a): Before Matching; (b): After Matching.

Figure 8.

The Kernel density functions before and after matching in 2009. (a): Before Matching; (b): After Matching.

Figure 8.

The Kernel density functions before and after matching in 2009. (a): Before Matching; (b): After Matching.

Figure 9.

The Kernel density functions before and after matching. (a): Before Matching; (b): After Matching.

Figure 9.

The Kernel density functions before and after matching. (a): Before Matching; (b): After Matching.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table 1.

Sample distribution of family firms (FFs).

| Year | Amount of FFs | Amount of FFs with More Than One Offsprings Involved | Amount of FFs from No Sibling Rivalry to Sibling Rivalry |

|---|---|---|---|

| 2009 | 545 | 50 | 3 |

| 2010 | 605 | 59 | 2 |

| 2011 | 665 | 69 | 2 |

| 2012 | 732 | 75 | 1 |

| 2013 | 843 | 83 | 5 |

| 2014 | 864 | 87 | 2 |

| 2015 | 988 | 96 | 5 |

Table 2.

Descriptions of variables.

| Variables | Definition | Construction | |

|---|---|---|---|

| Explained variable | risk taking | The deviation of the firm’s EBITDA (earnings before interest, taxes, depreciation, and amortization)/Assets (at the end of the year) subtracting industry average. | |

| Explanatory variables | treated | With the involvement of new offspring(s), Sibling rivalry (brothers in arms) comes to be existing or not. | When sibling rivalry (brothers in arms) comes into play, treated = 1; otherwise, treated = 0. |

| treated × dt | There exist the cases of the intervention group (control group) before or after the year of intervention. | In the intervention group before the year of intervention, treated × dt = 0; otherwise, in control group, treated × dt = 0. In the intervention group after the year of intervention, treated × dt = 1; otherwise, in control group, treated × dt = 0. | |

| dt | The year of intervention, namely, the year of appearance of sibling rivalry. | When sibling rivalry comes into being in the year, dt = 1; otherwise, dt = 0. | |

| Covariates/control variables | Age | Age of the firm’s actual controller. | |

| Asset | Total assets of the firm at the end of the year. | ||

Table 3.

Balance test of propensity score matching.

| Year | Variables | Mean Value | Std (%) | Std Reduction (%) | t-Stat | t-Test (p > t) | ||

|---|---|---|---|---|---|---|---|---|

| Treatment Group | Control Group | |||||||

| 2009 | Age | Before | 58.67 | 50.39 | 137.0 | 100.0 | 1.72 | 0.088 |

| After | 58.67 | 58.67 | 0.0 | 0.00 | 1.000 | |||

| Asset | Before | 20.98 | 21.03 | −5.6 | −178.8 | −0.08 | 0.933 | |

| After | 20.98 | 21.11 | −15.7 | −0.17 | 0.876 | |||

| 2010 | Age | Before | 55.00 | 50.86 | 63.9 | 100.0 | 0.72 | 0.474 |

| After | 55.00 | 55.00 | 0.0 | 0.00 | 1.000 | |||

| Asset | Before | 21.48 | 21.08 | 20.3 | 90.7 | 0.56 | 0.578 | |

| After | 21.48 | 21.44 | 1.9 | 0.02 | 0.987 | |||

| 2011 | Age | Before | 57.50 | 51.71 | 99.5 | 69.7 | 1.03 | 0.306 |

| After | 57.50 | 55.75 | 30.1 | 0.24 | 0.830 | |||

| Asset | Before | 22.12 | 21.22 | 88.1 | 89.0 | 1.29 | 0.200 | |

| After | 22.12 | 22.21 | −9.7 | −0.09 | 0.934 | |||

| 2012 | Age | Before | — | — | — | — | — | — |

| After | — | — | — | — | — | |||

| Asset | Before | — | — | — | — | — | — | |

| After | — | — | — | — | — | |||

| 2013 | Age | Before | 65.40 | 51.36 | 223.9 | 97.9 | 3.71 | 0.000 |

| After | 65.40 | 65.10 | 4.8 | 0.20 | 0.849 | |||

| Asset | Before | 19.62 | 19.68 | −6.6 | −128.5 | −0.13 | 0.898 | |

| After | 19.62 | 19.49 | 15.0 | 0.27 | 0.792 | |||

| 2014 | Age | Before | 57.00 | 52.64 | 74.9 | 91.4 | 0.80 | 0.426 |

| After | 57.00 | 57.38 | −6.4 | −0.08 | 0.946 | |||

| Asset | Before | 21.80 | 21.42 | 52.6 | 82.9 | 0.56 | 0.575 | |

| After | 21.80 | 21.73 | 9.0 | 0.08 | 0.946 | |||

| 2015 | Age | Before | 63.40 | 53.36 | 141.7 | 94.5 | 2.66 | 0.008 |

| After | 63.40 | 63.95 | −7.8 | −0.15 | 0.883 | |||

| Asset | Before | 22.24 | 21.56 | 93.3 | 74.0 | 1.57 | 0.117 | |

| After | 22.24 | 22.06 | 24.3 | 0.49 | 0.636 | |||

Table 4.

Results of difference-in-difference (DID) regression.

| Variables | Risk Taking | |

|---|---|---|

| 1 | 2 | |

| treated | −0.0503 *** (−2.82) | −0.0517 *** (−2.77) |

| dt | −0.0617 *** (−4.22) | −0.0646 *** (−4.13) |

| treated × dt | 0.0447 ** (2.40) | 0.0452 ** (2.37) |

| Age | 0.0008 (1.33) | |

| Asset | −0.0001 (−0.05) | |

| _cons | 0.0909 *** (6.41) | 0.0437 (1.26) |

| N | 79 | 79 |

| 0.1492 | 0.1557 | |

Note: *** and ** are significant at 1% and 5% statistical levels, respectively, with t statistics in the parentheses.

Table 5.

Balance test of propensity score matching (PSM).

| Variables | Mean Value | Std (%) | Std Reduction (%) | t-Stat | t-Test (p > t) | ||

|---|---|---|---|---|---|---|---|

| Treatment Group | Control Group | ||||||

| Age | Before | 64.979 | 53.636 | 128.7 | 98.7 | 8.37 | 0.000 |

| After | 64.564 | 64.415 | 1.7 | 0.09 | 0.930 | ||

| Asset | Before | 21.856 | 21.691 | 15.7 | 57.5 | 1.14 | 0.254 |

| After | 21.876 | 21.946 | −6.7 | −0.31 | 0.754 | ||

Table 6.

Descriptive statistics.

| Variables | Observations | Mean Value | Std | Minimum | Maximum |

|---|---|---|---|---|---|

| treated | 151 | 0.31133 | 0.4645 | 0 | 1 |

| Risk taking | 151 | 0.0628 | 0.1131 | 0.0074 | 1.1172 |

| Asset | 151 | 21.8921 | 1.0425 | 20.2393 | 24.8297 |

| Age | 151 | 62.4934 | 8.7357 | 42.5 | 81.5 |

Table 7.

Baseline regression results.

| Variables | 2011–2015 | 2011–2013 | 2012–2014 | 2013–2015 | ||||

|---|---|---|---|---|---|---|---|---|

| 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | |

| treated | −0.0493 ** (−2.28) | −0.0616 *** (−2.20) | −0.0444 *** (−2.95) | −0.0366 *** (−2.68) | ||||

| Asset | −0.0177 (−1.86) | −0.0179 * (−1.90) | −0.0195 (−1.60) | −0.0202 * (−1.67) | −0.0103 (−1.55) | −0.0102 (−1.58) | −0.0067 (−1.12) | −0.0066 (−1.12) |

| Age | −0.0010 (−0.90) | −0.0006 (−0.54) | −0.0015 (−1.02) | −0.0009 (−0.67) | −0.0008 (−1.04) | −0.0004 (−0.58) | −0.0005 (−0.75) | −0.0002 (−0.33) |

| _cons | 0.5161 (2.34) | 0.5101 ** (2.35) | 0.5900 ** (2.11) | 0.5916 *** (2.14) | 0.3303 ** (2.14) | 0.3193 ** (2.12) | 0.2292 (1.62) | 0.2174 (1.57) |

| N | 151 | 151 | 151 | 151 | 151 | 151 | 151 | 151 |

| 0.0279 | 0.0612 | 0.0240 | 0.0551 | 0.0228 | 0.0774 | 0.0120 | 0.0581 | |

| Adj- | 0.0148 | 0.0421 | 0.0108 | 0.0358 | 0.0096 | 0.0586 | −0.0014 | 0.0389 |

Note: ***, **, * are significant at 1%, 5% and 10% statistical levels, respectively, with t statistics in the parentheses.

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Chen, J.; Wang, C.; Wang, Q.; Luo, B. Sibling Rivalry vs. Brothers in Arms: The Contingency Effects of Involvement of Multiple Offsprings on Risk Taking in Family Firms. Sustainability 2019, 11, 4447. https://doi.org/10.3390/su11164447

AMA Style

Chen J, Wang C, Wang Q, Luo B. Sibling Rivalry vs. Brothers in Arms: The Contingency Effects of Involvement of Multiple Offsprings on Risk Taking in Family Firms. Sustainability. 2019; 11(16):4447. https://doi.org/10.3390/su11164447

Chicago/Turabian StyleChen, Jin, Chengyuan Wang, Qiong Wang, and Biao Luo. 2019. "Sibling Rivalry vs. Brothers in Arms: The Contingency Effects of Involvement of Multiple Offsprings on Risk Taking in Family Firms" Sustainability 11, no. 16: 4447. https://doi.org/10.3390/su11164447

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.