Economic Transition and Changing Location of Manufacturing Industry in China: A Study of the Yangtze River Delta

Abstract

:1. Introduction

2. Research Background and Conceptual Framework

2.1. Literature Review

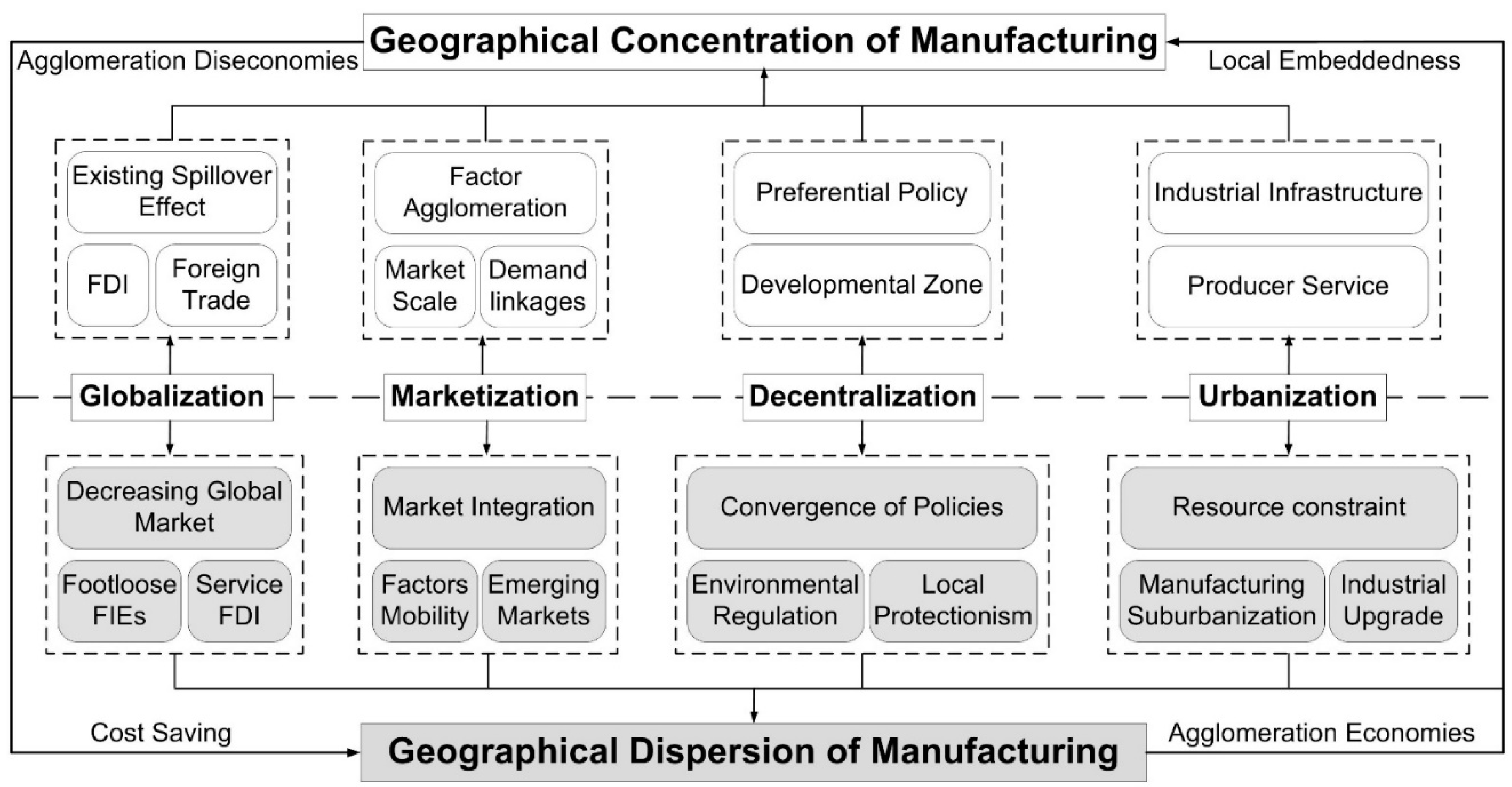

2.2. Conceptual Framework

3. Data and Methodology

3.1. Study Area

3.2. Data

3.3. Methodology

3.3.1. Geographically Weighted Shift-Share Model (GW-SSM)

- a

- National/regional effect (NE), i.e., . This effect indicates the growth of industry in city based on the national/regional all-sector growth rate.

- b

- Neighbor-regional-shift effect (NRSE), i.e., . This effect represents the difference between all industries in the city ’s neighbor and those in the entire region.

- c

- Neighbor industry-mix effect (NIME), i.e., , which manifests industry ’s growth in the city ’s neighbor compared to all industries in that area.

- d

- Urban-neighbor industrial shift effect (UNISE), i.e., , which indicates the difference in the growth shift of industry between city and its neighboring areas.

- e

- Urban-neighbor-shift effect (UNSE), i.e., , which indicates the growth of all industries in city compared with their growth in ’s neighbor.

- f

- Urban industry-mix effect (UIME), i.e., . This effect can be used to indicate industry ’s growth compared with all industries inside city .

3.3.2. Geographically and Temporally Weighted Regression (GTWR)

4. Spatiotemporal Pattern of Manufacturing Location in the YRD

4.1. Overall Spatiotemporal Pattern of Manufacturing Distribution

4.2. Sectoral Heterogeneities in Manufacturing Distribution

4.2.1. Garment, Shoe, and Hat Making (S18)

4.2.2. Chemical Materials and Chemical Products (S26)

4.2.3. Transportation Equipment (S37)

4.2.4. Telecommunication, Computers, and Other Electronic Equipment (S40)

5. Driving Factors and Mechanisms of Manufacturing Distribution

5.1. Variables and Models

5.2. Overall Picture of Driving Mechanisms

5.3. Regional Heterogeneities in Driving Mechanisms

5.4. Sectoral Heterogeneities in Driving Mechanisms

6. Conclusions and Discussion

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Wei, Y.D.; Liefner, I. Globalization, industrial restructuring, and regional development in China. Appl. Geogr. 2012, 32, 102–105. [Google Scholar] [CrossRef]

- He, C.; Wei, Y.D.; Xie, X. Globalization, institutional change, and industrial location: Economic transition and industrial concentration in China. Reg. Stud. 2008, 42, 923–945. [Google Scholar] [CrossRef]

- Liao, H.F.; Wei, Y.D. Space, scale, and regional inequality in provincial China: A spatial filtering approach. Appl. Geogr. 2015, 61, 94–104. [Google Scholar] [CrossRef] [Green Version]

- Wei, Y.D. Geography of inequality in Asia. Geogr. Rev. 2017, 107, 263–275. [Google Scholar] [CrossRef]

- Lin, J.; Yu, Z.; Wei, Y.D.; Wang, M. Internet Access, Spillover and Regional Development in China. Sustainability 2017, 9, 946. [Google Scholar] [CrossRef]

- Xiong, L.; Yu, C.; de Jong, M.; Wang, F.; Cheng, B. Economic Transformation in the Beijing-Tianjin-Hebei Region: Is It Undergoing the Environmental Kuznets Curve? Sustainability 2017, 9, 869. [Google Scholar] [CrossRef]

- Li, H.; Zhang, J.; Osei, E.; Yu, M. Sustainable Development of China’s Industrial Economy: An Empirical Study of the Period 2001–2011. Sustainability 2018, 10, 764. [Google Scholar] [CrossRef]

- Wei, Y.D. Decentralization, marketization, and globalization: The triple processes underlying regional development in China. Asian Geogr. 2001, 20, 7–23. [Google Scholar] [CrossRef]

- Zhu, S.; Lan, T. New economic geographies of manufacturing in China. Geogr. Compass 2016, 10, 470–481. [Google Scholar] [CrossRef]

- Chen, M.; Liu, W.; Lu, D. Challenges and the way forward in China’s new-type urbanization. Land Use Policy 2015, 55, 334–339. [Google Scholar] [CrossRef]

- Yang, C. Restructuring the export-oriented industrialization in the Pearl River Delta, China: Institutional evolution and emerging tension. Appl. Geogr. 2012, 32, 143–157. [Google Scholar] [CrossRef]

- Wei, Y.D.; Bi, X.; Wang, M.; Ning, Y. Globalization, economic restructuring, and locational trajectories of software firms in shanghai. Prof. Geogr. 2016, 68, 211–226. [Google Scholar] [CrossRef]

- Yang, C.; He, C. Transformation of China’s ‘World Factory’: Production Relocation and Export Evolution of the Electronics Firms. Tijdschr. Voor Econ. Soc. Geogr. 2017, 108, 571–591. [Google Scholar] [CrossRef]

- He, C.; Pan, F.; Chen, T. Research progress of industrial geography in China. J. Geogr. Sci. 2016, 26, 1057–1066. [Google Scholar] [CrossRef]

- Wei, Y.D.; Li, W.; Wang, C. Restructuring industrial districts, scaling up regional development: A study of the Wenzhou model, China. Econ. Geogr. 2007, 83, 421–444. [Google Scholar] [CrossRef]

- Liao, H.F.; Chan, R.C. Industrial relocation of Hong Kong manufacturing firms: Towards an expanding industrial space beyond the Pearl river delta. GeoJournal 2011, 76, 623–639. [Google Scholar] [CrossRef]

- Shen, J.; Wei, Y.D.; Yang, Z. The impact of environmental regulations on the location of pollution-intensive industries in China. J. Clean. Prod. 2017, 148, 785–794. [Google Scholar] [CrossRef]

- Liu, Y.; Wu, J.; Yu, D. Disentangling the Complex Effects of Socioeconomic, Climatic, and Urban Form Factors on Air Pollution: A Case Study of China. Sustainability 2018, 10, 776. [Google Scholar] [CrossRef]

- Wen, M. Relocation and agglomeration of Chinese industry. J. Dev. Econ. 2004, 73, 329–347. [Google Scholar] [CrossRef]

- Long, C.; Zhang, X. Patterns of China’s industrialization: Concentration, specialization, and clustering. China Econ. Rev. 2012, 23, 593–612. [Google Scholar] [CrossRef]

- Yang, C. Strategic coupling of regional development in global production networks: Redistribution of Taiwanese personal computer investment from the Pearl River Delta to the Yangtze River Delta, China. Reg. Stud. 2009, 43, 385–407. [Google Scholar] [CrossRef]

- Wei, Y.D. Beyond new regionalism, beyond global production networks: Remaking the Sunan model, China. Environ. Plan. C 2010, 28, 72. [Google Scholar] [CrossRef]

- Jiang, H.; Xu, W.; Zhang, W. Transportation Accessibility and Location Choice of Japanese-Funded Electronic Information Manufacturing Firms in Shanghai. Sustainability 2018, 10, 390. [Google Scholar] [CrossRef]

- Gao, J.; Yuan, F. Economic Transition, Firm Dynamics, and Restructuring of Manufacturing Spaces in Urban China: Empirical Evidence from Nanjing. Prof. Geogr. 2017, 69, 504–519. [Google Scholar] [CrossRef]

- Wei, Y.D.; Ewing, R. Urban Expansion, Sprawl and Inequality; Elsevier: New York, NY, USA, 2018. [Google Scholar]

- Pellenbarg, P.H.; Van Wissen, L.J.; Van Dijk, J. Firm migration. In Industrial Location Economics; McCann, P., Ed.; Edward Elgar Publishing: Cheltenham, UK, 2002; p. 110. [Google Scholar]

- Holl, A. Start-ups and relocations: Manufacturing plant location in Portugal. Pap. Reg. Sci. 2004, 83, 649–668. [Google Scholar]

- Krugman, P. What’s new about the new economic geography? Oxf. Rev. Econ. Policy 1998, 14, 7–17. [Google Scholar] [CrossRef]

- Krugman, P. Increasing returns and economic geography. J. Political Econ. 1991, 99, 483–499. [Google Scholar] [CrossRef]

- Fan, C.C.; Scott, A.J. Industrial agglomeration and development: A survey of spatial economic issues in East Asia and a statistical analysis of Chinese regions. Econ. Geogr. 2003, 79, 295–319. [Google Scholar] [CrossRef]

- Kranich, J. Agglomeration, vertical specialization, and the strength of industrial linkages. Pap. Reg. Sci. 2011, 90, 159–178. [Google Scholar] [CrossRef] [Green Version]

- Porter, M. Location and competitive and economic development: Local clusters in the global economy. Econ. Dev. Q. 2000, 14, 15–34. [Google Scholar] [CrossRef]

- Randelli, F.; Boschma, R. Dynamics of industrial districts and business groups: The case of the Marche region. Eur. Plan. Stud. 2012, 20, 1961–1974. [Google Scholar] [CrossRef]

- Storper, M.; Venables, A.J. Buzz: Face-to-face contact and the urban economy. J. Econ. Geogr. 2004, 4, 351–370. [Google Scholar] [CrossRef]

- Martin, R.; Sunley, P. Towards a developmental turn in evolutionary economic geography? Reg. Stud. 2015, 49, 712–732. [Google Scholar] [CrossRef]

- Hassink, R. The restructuring of old industrial areas in Europe and Asia. Environ. Plan. A 2005, 37, 571–580. [Google Scholar] [CrossRef] [Green Version]

- Coe, N.M.; Dicken, P.; Hess, M. Global production networks: Realizing the potential. J. Econ. Geogr. 2008, 8, 271–295. [Google Scholar] [CrossRef]

- Yeung, H.W.C.; Coe, N.M. Toward a dynamic theory of global production networks. Econ. Geogr. 2015, 91, 29–58. [Google Scholar] [CrossRef]

- Sjöberg, Ö.; Sjöholm, F. Trade liberalization and the geography of production: Agglomeration, concentration, and dispersal in Indonesia’s manufacturing industry. Econ. Geogr. 2004, 80, 287–310. [Google Scholar] [CrossRef]

- Flores, M.; Villarreal, A.; Flores, S. Spatial Co-location Patterns of Aerospace Industry Firms in Mexico. Appl. Spat. Anal. Policy 2017, 10, 233–251. [Google Scholar] [CrossRef]

- Liefner, I.; Brömer, C.; Zeng, G. Knowledge absorption of optical technology companies in Shanghai, Pudong: Successes, barriers and structural impediments. Appl. Geogr. 2012, 32, 171–184. [Google Scholar] [CrossRef]

- Meliciani, V.; Savona, M. The determinants of regional specialisation in business services: Agglomeration economies, vertical linkages and innovation. J. Econ. Geogr. 2015, 15, 387–416. [Google Scholar] [CrossRef]

- Okubo, T.; Tomiura, E. Industrial relocation policy, productivity and heterogeneous plants: Evidence from Japan. Reg. Sci. Urban Econ. 2012, 42, 230–239. [Google Scholar] [CrossRef]

- Zheng, D.; Kuroda, T. The impact of economic policy on industrial specialization and regional concentration of China’s high-tech industries. Ann. Reg. Sci. 2013, 50, 771–790. [Google Scholar] [CrossRef]

- Zhang, K.H. Globalization and regional industrial performance: Evidence from China. Pap. Reg. Sci. 2014, 93, 269–280. [Google Scholar] [CrossRef]

- Yuan, F.; Wei, Y.D.; Chen, W. Economic transition, industrial location and corporate networks: Remaking the Sunan Model in Wuxi City, China. Habitat Int. 2014, 42, 58–68. [Google Scholar] [CrossRef]

- He, C.; Zhu, S.; Yang, X. What matters for regional industrial dynamics in a transitional economy? Area Dev. Policy 2017, 2, 71–90. [Google Scholar] [CrossRef]

- Wei, Y.D.; Yuan, F.; Liao, H. Spatial mismatch and determinants of foreign and domestic information and communication technology firms in urban China. Prof. Geogr. 2013, 65, 247–264. [Google Scholar] [CrossRef]

- Zhu, S.; Pickles, J.; He, C. Global and Local Governance, and Industrial and Geographical Dynamics: A Tale of Two Clusters. In Geographical Dynamics and Firm Spatial Strategy in China; Springer: Berlin/Heidelberg, Germany, 2017; pp. 143–167. [Google Scholar]

- Guo, Q.; He, C.; Li, D. Entrepreneurship in China: The role of localisation and urbanisation economies. Urban Stud. 2016, 53, 2584–2606. [Google Scholar] [CrossRef]

- Chen, B.; Cheng, Y.-S. The Impacts of Environmental Regulation on Industrial Activities: Evidence from a Quasi-Natural Experiment in Chinese Prefectures. Sustainability 2017, 9, 571. [Google Scholar] [CrossRef]

- Zhang, L.; Yue, W.; Liu, Y.; Fan, P.; Wei, Y.D. Suburban industrial land development in transitional China: Spatial restructuring and determinants. Cities 2018, 78, 96–107. [Google Scholar] [CrossRef]

- Ge, Y. Globalization and industry agglomeration in China. World Dev. 2009, 37, 550–559. [Google Scholar] [CrossRef]

- Huang, H.; Wei, Y.D. Spatial inequality of foreign direct investment in China: Institutional change, agglomeration economies, and market access. Appl. Geogr. 2016, 69, 99–111. [Google Scholar] [CrossRef]

- Wei, Y.D.; Zhou, Y.; Sun, Y.; Lin, G.C. Production and R&D networks of foreign ventures in China: Implications for technological dynamism and regional development. Appl. Geogr. 2012, 32, 106–118. [Google Scholar]

- Xu, Z.; Yeh, A. Origin effects, spatial dynamics and redistribution of FDI in Guangdong, China. Tijdschr. Voor Econ. Soc. Geogr. 2013, 104, 439–455. [Google Scholar] [CrossRef]

- Bai, C.E.; Du, Y.; Tao, Z.; Tong, S.Y. Local protectionism and regional specialization: Evidence from China’s industries. J. Int. Econ. 2004, 63, 397–417. [Google Scholar] [CrossRef]

- Li, Z.; Wu, M.; Chen, B.R. Is road infrastructure investment in China excessive? Evidence from productivity of firms. Reg. Sci. Urban Econ. 2017, 65, 116–126. [Google Scholar] [CrossRef]

- Castells-Quintana, D.; Royuela, V. Are increasing urbanisation and inequalities symptoms of growth? Appl. Spat. Anal. Policy 2015, 8, 291–308. [Google Scholar] [CrossRef] [Green Version]

- Wang, L.; Shen, J. Comparative Analysis of Urban Competitiveness in the Yangtze River Delta and Pearl River Delta Regions of China, 2000–2010. Appl. Spat. Anal. Policy 2017, 10, 401–419. [Google Scholar] [CrossRef]

- Yuan, F.; Gao, J.; Wang, L.; Cai, Y. Co-location of manufacturing and producer services in Nanjing, China. Cities 2017, 63, 81–91. [Google Scholar] [CrossRef]

- Wu, C.; Wei, Y.D.; Huang, X.; Chen, B. Economic transition, spatial development and urban land use efficiency in the Yangtze River Delta, China. Habitat Int. 2017, 63, 67–78. [Google Scholar] [CrossRef]

- Coe, N.M.; Yeung, H.W.-C. Global Production Networks: Theorizing Economic Development in an Interconnected World; Oxford University Press, USA: Cary, NC, USA, 2015. [Google Scholar]

- Nazara, S.; Hewings, G.J. Spatial Structure and Taxonomy of Decomposition in Shift-Share Analysis. Growth Chang. 2004, 35, 476–490. [Google Scholar] [CrossRef]

- Huang, B.; Wu, B.; Barry, M. Geographically and temporally weighted regression for modeling spatio-temporal variation in house prices. Int. J. Geogr. Inf. Sci. 2010, 24, 383–401. [Google Scholar] [CrossRef]

- Kronenberg, K. Firm relocations in the Netherlands: Why do firms move, and where do they go? Pap. Reg. Sci. 2013, 92, 691–713. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Regions | Share (%) | Changes in Share (%) | |||||

|---|---|---|---|---|---|---|---|

| 1999 | 2004 | 2009 | 2013 | 1999–2004 | 2004–2009 | 2009–2013 | |

| Shanghai | 26.30 | 22.75 | 14.87 | 12.48 | −3.55 | −7.87 | −2.39 |

| Southern JS | 29.18 | 33.06 | 32.82 | 30.03 | 3.88 | −0.23 | −2.80 |

| Central JS | 7.19 | 5.95 | 10.07 | 11.33 | −1.24 | 4.12 | 1.26 |

| Northern JS | 6.01 | 3.78 | 6.62 | 11.26 | −2.23 | 2.83 | 4.64 |

| Northern ZJ | 19.11 | 21.58 | 20.97 | 17.65 | 2.47 | −0.61 | −3.31 |

| Southern ZJ | 5.58 | 7.66 | 7.51 | 5.77 | 2.08 | −0.15 | −1.74 |

| Central AH | 4.54 | 4.06 | 5.59 | 8.47 | −0.48 | 1.53 | 2.88 |

| Northern AH | 1.56 | 0.78 | 0.91 | 2.06 | −0.78 | 0.12 | 1.15 |

| Southern AH | 0.54 | 0.38 | 0.64 | 0.96 | −0.16 | 0.26 | 0.31 |

| Regions | Number of Share Increased Sectors | Number of Share Decreased Sectors | ||||

|---|---|---|---|---|---|---|

| 1999–2004 | 2004–2009 | 2009–2013 | 1999–2004 | 2004–2009 | 2009–2013 | |

| Shanghai | 8 | 2 | 5 | 18 | 24 | 21 |

| Southern JS | 12 | 12 | 7 | 14 | 14 | 19 |

| Central JS | 10 | 24 | 17 | 16 | 2 | 9 |

| Northern JS | 7 | 25 | 25 | 19 | 1 | 1 |

| Northern ZJ | 23 | 13 | 4 | 3 | 13 | 22 |

| Southern ZJ | 23 | 14 | 6 | 3 | 12 | 20 |

| Central AH | 7 | 22 | 23 | 19 | 4 | 3 |

| Northern AH | 4 | 18 | 24 | 22 | 8 | 2 |

| Southern AH | 10 | 23 | 21 | 16 | 3 | 5 |

| Typical Sector | Backward/Forward Industries | Typical Sector | Backward/Forward Industries |

|---|---|---|---|

| S18 | S17, S19, S26, S28 | S37 | S32, S33, S35, S36 |

| S26 | S25, S28 | S40 | S26, S28, S39 |

| Categories | Variables | Definitions | Abbreviation | Expected Sign | |

|---|---|---|---|---|---|

| Dependent variable | Share of each city’s manufacturing gross output to the whole region | Ln (first-lagged ratio of a city’s gross output value of industrial enterprises to the whole region)/ | SHAREt | none | |

| Independent variables | Globalization | Foreign direct investment | Ln (first-lagged ratio of industrial gross output by foreign firms to the total) | FDIt−1 | +/− |

| Foreign trade | Ln (first-lagged total value of imports and exports/first-lagged GDP) | IXTt−1 | +/− | ||

| Access to global economy | Dummy variable, 1 for global cities, national and regional hub cities, 0 for other cities | OPENt−1 | +/− | ||

| Marketization | Labor cost | Ln (first-lagged average wage level of employed workers) | WAGEt−1 | +/− | |

| Market scale and potential | Ln (first-lagged ratio of a city’s total retail sales of consumer goods to the whole region) | RSCGt−1 | + | ||

| Market integration | Dummy variable, 1 for member of the Yangtze River Delta Urban Economic Coordination Conferences, 0 for other cities | INTEGt−1 | + | ||

| Industrial linkages | Ln (first-lagged ratio of gross industrial output value of backward-forward sectors to the total) | INTERt−1 | + | ||

| Decentralization | Preferential policies | Ln (first-lagged weighted sum strength of policy and established DZs) | POLt−1 | + | |

| Local protectionism | Ln (first-lagged ratio of value-added tax to gross industrial output) | TAXt−1 | − | ||

| Environmental regulation | Ln (first-lagged ratio a city’s drainage of industrial wastewater to the whole region) | ENVt−1 | − | ||

| Urbanization | Urbanization economies | Ln (first-lagged ratio of a city’s total investment in fixed assets to the whole region) | INVTt−1 | + | |

| Development of service industry | Ln (first-lagged ratio of the value added of service industry to GDP by city) | SERVt−1 | +/− | ||

| Urbanization level | Ln (first-lagged ratio of the urban resident population to the total population by city) | URB t−1 | +/− | ||

| Variables | Model 0 | Model 1 | Model 2 | Model 3 | Model 4 | Model 5 |

|---|---|---|---|---|---|---|

| Constant | 4.020 *** | 4.733 *** | 3.754 *** | 2.969 ** | 3.638 *** | 1.142 |

| Ln (FDIt−1) | 0.100 ** | 0.156 ** | 0.184 *** | 0.163 ** | 0.100 ** | 0.186 *** |

| Ln (IXTt−1) | 0.194 *** | 0.349 *** | 0.362 *** | 0.341 *** | 0.246 *** | |

| OPENt−1 | 0.004 | 0.338 ** | 0.457 *** | 0.399 ** | 0.153 | −0.037 |

| Ln (WAGEt−1) | −0.201 *** | −0.294 *** | −0.179 ** | |||

| Ln (RSCGt−1) | 0.614 *** | 0.895 *** | ||||

| INTEGt−1 | 0.410 *** | 0.787 *** | 0.820 *** | 0.781 *** | 0.433 *** | 0.565 *** |

| Ln (POLt−1) | 0.107 | 0.252 * | 0.039 | |||

| Ln (TAXt−1) | −0.149 ** | −0.308 *** | −0.323 *** | −0.321 *** | −0.097 | −0.393 *** |

| Ln (ENVt−1) | −0.032 | 0.505 *** | 0.519 *** | 0.561 *** | 0.209 *** | |

| Ln (INVTt−1) | 0.391 *** | 0.842 *** | ||||

| Ln (SERVt−1) | −0.901 *** | −0.922 ** | −0.924 ** | −1.043 *** | −1.336 *** | −0.400 |

| Ln (URBt−1) | 0.0005 | −0.102 | −0.110 | −0.241 | −0.043 | −0.099 |

| Hausman Test Chi-Sq. Statistic | 56.50 *** | 79.27 *** | 76.70 *** | 87.60 *** | 53.02 *** | 115.30 *** |

| Adjusted R2 | 0.917 | 0.816 | 0.813 | 0.808 | 0.907 | 0.870 |

| Variables | YRD | Core Region | Peripheral Region | ||||||

|---|---|---|---|---|---|---|---|---|---|

| Model 0 | Model 1 | Model 2 | Model 0 | Model 1 | Model 2 | Model 0 | Model 1 | Model 2 | |

| Mean (Positive) | Mean (Positive) | Mean (Positive) | Mean (Positive) | Mean (Positive) | Mean (Positive) | Mean (Positive) | Mean (Positive) | Mean (Positive) | |

| Ln (FDIt−1) | 0.108 (100%) | 0.133 (93.3%) | 0.248 (90.9%) | 0.171 (85.4%) | 0.155 (85.4%) | 0.230 (85.4%) | 0.090 (100%) | 0.100 (81.9%) | 0.172 (100%) |

| Ln (IXTt−1) | 0.242 (100%) | 0.292 (100%) | 0.137 (87.5%) | 0.163 (85.4%) | 0.246 (100%) | 0.240 (84.5%) | |||

| OPENt−1 | −0.153 (1.2%) | −0.018 (48.8%) | −0.099 (26.2%) | −0.205 (12.5%) | −0.220 (0%) | −0.065 (27.1%) | −0.166 (7.8%) | 0.008 (49.1%) | −0.135 (38.8%) |

| Ln (WAGEt−1) | 0.029 (50%) | 0.163 (70.7%) | −0.094 (34.1%) | −0.231 (27.1%) | −0.303 (20.8%) | −0.355 (6.3%) | −0.015 (50%) | 0.185 (75.9%) | −0.191 (3.4%) |

| Ln (RSCGt−1) | 0.609 (100%) | 0.898 (100%) | 0.979 (100%) | 0.955 (100%) | 0.588 (100%) | 0.921 (100%) | |||

| INTEGt−1 | 0.258 (98.8%) | 0.296 (95.1%) | 0.414 (89.0%) | 3.739 (100%) | 3.487 (97.9%) | 5.467 (100%) | 0.297 (100%) | 0.366 (75.9%) | 0.416 (88.8%) |

| Ln (POLt−1) | −0.158 (45.7%) | −0.081 (51.2%) | −0.136 (45.7%) | 0.069 (64.6%) | 0.105 (79.2%) | 0.158 (77.1%) | −0.151 (47.4%) | −0.133 (37.9%) | 0.004 (63.8%) |

| Ln (TAXt−1) | −0.092 (4.9%) | −0.077 (25.6%) | −0.220 (18.3%) | −0.202 (0%) | −0.252 (0%) | −0.408 (0%) | −0.118 (0%) | −0.087 (23.3%) | −0.216 (13.8%) |

| Ln (ENVt−1) | −0.066 (31.1%) | 0.073 (69.5%) | −0.016 (29.2%) | 0.484 (100%) | −0.097 (25.0%) | −0.002 (60.3%) | |||

| Ln (INVTt−1) | 0.535 (100%) | 0.975 (100%) | 0.057 (58.3%) | 0.489 (97.9%) | 0.572 (100%) | 1.013 (100%) | |||

| Ln (SERVt−1) | −0.380 (15.2%) | −0.756 (7.9%) | −0.311 (39.0%) | −2.845 (0%) | −2.609 (4.2%) | −2.342 (2.1%) | −0.218 (28.4%) | −0.874 (6.9%) | 0.115 (60.3%) |

| Ln (URBt−1) | −0.043 (41.5%) | −0.110 (42.7%) | 0.304 (75.6%) | 2.017 (100%) | 2.063 (100%) | 1.592 (100%) | −0.066 (35.3%) | 0.009 (50.9%) | 0.170 (64.7%) |

| Adjusted R2 | 0.965 | 0.956 | 0.983 | 0.986 | 0.988 | 0.980 | 0.937 | 0.966 | 0.943 |

| Variables | S18 | S26 | ||||||

|---|---|---|---|---|---|---|---|---|

| Model 0 | Model 1 | Model 2 | Model 3 | Model 0 | Model 1 | Model 2 | Model 3 | |

| Mean (Positive) | Mean (Positive) | Mean (Positive) | Mean (Positive) | Mean (Positive) | Mean (Positive) | Mean (Positive) | Mean (Positive) | |

| Ln (FDIt−1) | 0.121 (78.7%) | 0.175 (76.8%) | 0.256 (78.0%) | 0.090 (75.6%) | 0.259 (83.5%) | 0.257 (85.4%) | 0.288 (90.2%) | 0.306 (100%) |

| Ln (IXTt−1) | −0.172 (22.6%) | 0.118 (70.7%) | 0.037 (53.7%) | 0.135 (69.5%) | ||||

| OPENt−1 | −0.088 (36.6%) | −0.211 (28.7%) | −0.434 (22.6%) | −0.105 (36.0%) | −0.047 (38.4%) | −0.009 (43.3%) | −0.009 (48.2%) | 0.320 (82.9%) |

| Ln (WAGEt−1) | 0.387 (89.0%) | 0.475 (82.3%) | 0.175 (54.3%) | 0.326 (79.9%) | 0.047 (44.5%) | −0.032 (40.9%) | −0.295 (18.9%) | −0.021 (38.4%) |

| Ln (RSCGt−1) | 0.056 (55.5%) | 1.112 (98.2%) | 0.691 (97.6%) | 0.928 (100%) | ||||

| INTEGt−1 | 0.353 (70.1%) | 0.900 (86.0%) | 0.917 (78.7%) | 0.363 (72.0%) | 0.348 (78.0%) | 0.375 (77.4%) | 0.539 (80.5%) | 0.556 (78.0%) |

| Ln (INTERt−1) | 0.966 (100%) | 0.939 (100%) | 0.053 (66.5%) | 0.150 (97.6%) | ||||

| Ln (POLt−1) | −0.084 (32.3%) | −0.211 (28.0%) | −0.068 (42.1%) | 0.010 (51.2%) | −0.175 (27.4%) | −0.104 (32.9%) | −0.082 (45.1%) | −0.182 (34.1%) |

| Ln (TAXt−1) | −0.148 (36.6%) | −0.209 (25.0%) | −0.273 (24.4%) | −0.125 (32.3%) | −0.293 (3.7%) | −0.258 (7.9%) | −0.439 (0%) | −0.418 (0.0%) |

| Ln (ENVt−1) | 0.201 (75.6%) | 0.319 (73.2%) | 0.244 (80.5%) | −0.042 (41.5%) | 0.121 (60.4%) | 0.376 (80.5%) | ||

| Ln (INVTt−1) | 0.082 (51.8%) | 0.952 (96.3%) | 0.284 (70.1%) | 0.757 (100%) | ||||

| Ln (SERVt−1) | −1.409 (0%) | −1.983 (2.4%) | −1.165 (26.2%) | −1.174 (3.7%) | −0.072 (51.8%) | −0.158 (39.0%) | 0.491 (80.5%) | 0.074 (63.4%) |

| Ln (URBt−1) | 0.149 (63.4%) | 0.159 (48.2%) | 0.161 (38.4%) | −0.028 (39.0%) | −0.212 (48.2%) | −0.060 (48.2%) | 0.097 (56.7%) | −0.110 (42.7%) |

| Adjusted R2 | 0.959 | 0.951 | 0.966 | 0.963 | 0.953 | 0.932 | 0.929 | 0.892 |

| Variables | S37 | S40 | ||||||

| Model 0 | Model 1 | Model 2 | Model 3 | Model 0 | Model 1 | Model 2 | Model 3 | |

| Ln (FDIt−1) | 0.210 (78.0%) | 0.225 (73.2%) | 0.330 (85.4%) | 0.217 (75.6%) | −0.039 (50.0%) | 0.301 (97.0%) | 0.307 (82.3%) | 0.079 (50.0%) |

| Ln (IXTt−1) | 0.091 (53.7%) | 0.243 (61.0%) | 0.357 (100%) | 0.860 (100%) | ||||

| OPENt−1 | 0.360 (68.3%) | 0.350 (62.2%) | 0.371 (63.4%) | 0.488 (68.3%) | 0.591 (100%) | 0.838 (100%) | 0.301 (76.2%) | 0.665 (100%) |

| Ln (WAGEt−1) | −0.378 (19.5%) | −0.465 (22.0%) | −0.518 (22.0%) | −0.315 (17.1%) | −0.349 (50.0%) | −0.417 (1.2%) | −0.760 (6.7%) | −0.040 (25.0%) |

| Ln (RSCGt−1) | 0.248 (61.6%) | 0.902 (95.1%) | −0.323 (0.0%) | 0.993 (100%) | ||||

| INTEGt−1 | 0.246 (58.5%) | 0.262 (75.6%) | 0.115 (56.1%) | 0.147 (68.3%) | 0.113 (75.0%) | 0.451 (82.9%) | 0.933 (96.3%) | |

| Ln (INTERt−1) | 0.463 (100%) | 0.548 (92.7%) | 0.990 (100%) | 1.148 (100%) | ||||

| Ln (POLt−1) | 0.144 (65.9%) | 0.181 (70.7%) | 0.191 (61.0%) | 0.178 (78.0%) | −0.395 (50.0%) | −0.398 (28.0%) | −0.328 (50.0%) | −0.052 (25.0%) |

| Ln (TAXt−1) | −0.302 (17.1%) | −0.389 (26.8%) | −0.385 (31.7%) | −0.257 (31.7%) | −0.382 (25.0%) | −0.196 (40.9%) | −1.179 (3.0%) | −0.667 (25.0%) |

| Ln (ENVt−1) | 0.320 (68.3%) | 0.480 (75.6%) | 0.468 (68.3%) | 0.438 (75.0%) | 0.266 (93.3%) | 0.389 (75.0%) | ||

| Ln (INVTt−1) | −0.016 (47.6%) | 0.549 (82.9%) | 0.619 (100%) | 1.493 (100%) | ||||

| Ln (SERVt−1) | 0.609 (73.2%) | 0.093 (46.3%) | 0.403 (65.9%) | 0.548 (92.7%) | −0.018 (50.0%) | −0.069 (47.0%) | 0.168 (45.1%) | −1.128 (0%) |

| Ln (URBt−1) | 0.064 (68.3%) | 0.755 (70.7%) | 0.559 (70.7%) | −0.251 (41.5%) | 0.224 (50.0%) | −0.160 (28.7%) | 1.207 (88.4%) | 0.783 (100%) |

| Adjusted R2 | 0.938 | 0.936 | 0.929 | 0.928 | 0.898 | 0.911 | 0.908 | 0.899 |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Wu, J.; Wei, Y.D.; Li, Q.; Yuan, F. Economic Transition and Changing Location of Manufacturing Industry in China: A Study of the Yangtze River Delta. Sustainability 2018, 10, 2624. https://doi.org/10.3390/su10082624

Wu J, Wei YD, Li Q, Yuan F. Economic Transition and Changing Location of Manufacturing Industry in China: A Study of the Yangtze River Delta. Sustainability. 2018; 10(8):2624. https://doi.org/10.3390/su10082624

Chicago/Turabian StyleWu, Jiawei, Yehua Dennis Wei, Qizhai Li, and Feng Yuan. 2018. "Economic Transition and Changing Location of Manufacturing Industry in China: A Study of the Yangtze River Delta" Sustainability 10, no. 8: 2624. https://doi.org/10.3390/su10082624

APA StyleWu, J., Wei, Y. D., Li, Q., & Yuan, F. (2018). Economic Transition and Changing Location of Manufacturing Industry in China: A Study of the Yangtze River Delta. Sustainability, 10(8), 2624. https://doi.org/10.3390/su10082624