The Effect of Trust on Acquisition Success: The Case of Israeli Start-Up M&A

1

Department of International Competitiveness, Poznań University of Economics and Business, 61-875 Poznań, Poland

2

Hadassah Academic College, Jerusalem 9101001, Israel

*

Author to whom correspondence should be addressed.

Sustainability 2018, 10(7), 2499; https://doi.org/10.3390/su10072499

Submission received: 31 May 2018

/

Revised: 24 June 2018

/

Accepted: 2 July 2018

/

Published: 17 July 2018

(This article belongs to the Special Issue Trust Management: Key Factor of the Sustainable Organizations Embedded in Network)

Abstract

:Given the frequent failure of many M&A deals, the question of their sustainability is a critical one. Still, in existing literature, there is a visible emphasis on the perspective of the acquiring firm and its characteristics in affecting M&A performance. Moreover, the role of trust, both from the acquiring and acquired firms, has not received extensive attention to date. The present paper builds on a quantitative and qualitative study of Israeli high-tech start-ups acquired by international firms to explore the effects of trust on M&A success. Our study indicates that trust from acquired firm managers positively affects acquisition success, although trust from the acquiring firm (expressed with the autonomy that it leaves to the acquired firm) is not a significant predictor of acquisition success.

1. Introduction

Mergers and acquisitions (M&A) belong to the focal strategies for organizations to ensure a sustainable competitive position. Global M&A activities reached $936.8 billion in 1Q2018, representing an increase of 24.9% as compared to the same period of the previous year [1]. (These phenomena include mergers, acquisitions, divestitures, spin-offs, debt-for-equity swaps, joint ventures, private placements of common equity and convertible securities, and the cash injection component of recapitalization according to Bloomberg standards). These transactions involving two organizations are oftentimes used to achieve economies of scale, diversification, and economic growth. M&A can allow companies to grow, shrink, and—more importantly—change the nature of their business or competitive position, particularly by acquiring technological or managerial know-how [2]. However, the volume of these deals stands in sharp contrast to the actual sustainability of M&As. Estimates indicate that a significant proportion of M&As are financial failures [3,4,5] and, overall, the value creation is negligible [6]. Hence, not surprisingly, for the past decades, a number of researchers have dealt with different factors affecting the sustainability of M&A. In spite of this plethora of research, the critical success factors behind M&A and the reasons for their frequent failure still remain rather poorly understood. King et al. [6] concluded that despite a long tradition of research, none of the variables most frequently featured in extant research (including the level of diversification and relatedness, payment method, or earlier acquisition experience) turned out to be significant predictors of variance in post-acquisition performance.

More recently, scholars have concentrated on sociocultural variables and human factors contributing to the sustainability of M&A. A potentially crucial, yet underexplored, variable in the post-merger integration process is trust. Despite significant advances in this field, our understanding of the role of trust in M&A still remains incomplete. M&As increase negative reactions such as ambiguity [7,8] and a lack of organizational commitment [9,10]. Uncertainty arising after the announcement of an M&A deal creates a fertile ground for mistrust, as the situation is turbulent and members of an organization may feel vulnerable. Trust in a brand new top management team (TMT) may be lacking at the beginning, while employees are unsure as to the extent and magnitude of upcoming changes which can affect them in different ways [5]. The period after the announcement of an M&A transaction is therefore full of vulnerability, whereby mutual trust between the involved parties is of vital importance.

The acquiring firm’s TMT can possibly contemplate a couple of activities in order to develop trust and guarantee the commitment on the part of employees of the acquired firm [4]. In specific, trying to accelerate the process of integration, refraining from imposing the own culture on the acquired company, or offering proper structural incentives (such as granting the acquired firm to retain a desirable level of autonomy), may possibly lead to superior post-integration performance.

This human side of M&A, which arguably explains a significant part of the challenges of M&A sustainability, has been studied from the perspective of multiple theorical concepts and approaches. These include, inter alia, the psychological perspective looking at how M&A affect individual stress levels, coping, and involvement [11,12]; the micro-foundations of organizational behavior affecting the pre-acquisition stage, e.g., [13]; the social perspective focusing on group dynamics, social comparison, and status [14,15]; and the cultural perspective considering culture clashes that afflict M&A performance [16]. However, much of the research into M&A to date remains fragmented and suffers from several gaps [17]. We argue that these result from an inadequate and simplified treatment of trust in the related research. Thus, while the integration of foreign units has been examined from the point of view of strategy-related variables, it has rarely been viewed as a manifestation of trust in the acquired entity, which may be crucial for its performance [18]. Moreover, trust in a transaction involving two parties is a mutual phenomenon, which can be analyzed in a one-sided manner.

In light of the above, our paper aims to examine how trust affects a sustainable, successful integration of two companies, viewed both from the perspective of the acquiring and the acquired company’s management. In addressing M&A success, we recur to managerial perceptions, which result from the difficulty of defining and measuring M&A success, particularly for technology acquisitions. As Zollo and Meier [19] noted, no single item can possibly capture all of the important dimensions of M&A performance. Such transactions may have little or no immediate influence over buyers’ stock prices or even over the P&L account. Conversely, TMTs from the acquired firms usually have intimate knowledge on the integration process and its outcomes. Furthermore, past studies found evidence that evaluations provided by managers correlate with objective success measures [20].

In order to address this research question, acquired Israeli start-ups were chosen as the empirical setting. We study the relevance of trust within the context of start-ups, because most acquired companies, nowadays, are small and medium enterprises (SMEs), with a preference for creative and entrepreneurial start-ups. The reasons for acquiring such firms are numerous, ranging from the ability to adopt a flexible strategic approach, through the integration of an entrepreneurial and innovation-oriented culture, to absorbing new technology. And yet, although SMEs do play a crucial role in the economy, as they represent 99% of the number of firms in Europe [21], and they actually drove M&A transactions in the past [22], they are often ignored in current research.

Many companies forge relationships with young, innovative start-up firms in order to provide them with ideas and financial support, while working on joint innovative projects [23]. Such relationships demonstrate how interactions and shared socio-cultures may arise from joint interests, whereby trust plays an important role in ensuring knowledge transfer and a seamless alignment of objectives, as well as connection to each other’s networks. The relevance of trust in this context is accentuated by the fact that the acquiring and acquired firms display divergent characteristics, particularly in terms of the level of formalization and the complexity of organizational structures. Therefore, if the innovation-related objectives driving such deals are to materialize, the acquired unit has to receive trust in its approach, despite potential differences between the companies.

The setting of Israel was selected for its particular relevance to start-ups and innovation. Over the past few decades, large companies have been scouting Israel for their technology acquisitions and for innovative ideas [24]. Starting in early 1990s, Israel has seen an impressive rise in the number of start-ups and the venture capital (VC) industry accompanying high tech sectors [25,26]. Moreover, Israel is famous for its entrepreneurial orientation, its superior technological skills, and its growing start-up-intensive high-tech cluster [27].

The paper is organized as follows. The second section features a literature review devoted to the role of trust in M&A, with a focus on its outcomes, and leads to the formulation of two hypotheses pertaining to trust on both sides of the transaction. Subsequently, we present the mixed-method design of our study, with a focus on the data collection and analytical methods used in the quantitative and qualitative study. In the ensuing section, we elaborate on the results of both studies. Not least, the final section elaborates on the implications and limitations of the study.

2. Theory and Hypotheses Development

Trust is of interest to many scientific disciplines, such as philosophy, psychology, sociology, economics, or management. Mainstream economic theory puts forward a formal process for making rational decisions, in which individuals consider all options available to them [28]. Yet, many important investment decisions are intuitive rather than analytical [28], particularly when the decision-making process is made by a group of people [29]. Hence, trust is a core concept of behavioral economics which enhances the explanatory potential of economic sciences by giving them a more realistic psychological backbone [30,31]. The Nobel Prize winners G.A. Akerlof and R.J. Shiller in their bestseller book [28] regarded trust as the cornerstone of the so-called animal instincts of a man. K.J. Arrow [32] called trust “an important lubricant in the social system”. It is very effective because it allows you to save on the costs of gathering information about business partners. According to Arrow, “in the course of evolution in societies there were quiet agreements” creating ethical and moral principles that contribute to the smooth functioning of economies. The factor of trust and its impact on economic development are the subject of many different studies [33].

Hence, not surprisingly, trust is also regarded as a key element of sociocultural variables that are crucial drivers of M&A performance. Support for the focal role of trust can be found in research indicating that trust is critical to successfully implementing strategic alliances in a form of joint venture, e.g., [34]. As for the M&A context, trust appears to be critical, particularly in the post-merger integration process, e.g., [35,36]. In fact, it may reduce the intention to leave the company by its managers as a result of the takeover. It may also facilitate an effective transfer of knowledge between the parent and the subsidiary, as well as reinforce the commitment and dedication to the redefined business objectives after the acquisition. And yet, in spite of substantial practical, albeit mostly anecdotal, support for the significance of trust in M&A, our knowledge of the facilitators of trust emergence in acquired firms and effects of this trust on sustainable outcomes of M&A still remains quite limited [4].

In this paper, we refer to trust as “a psychological state comprising the intention to accept vulnerability based upon positive expectations of the intentions or behavior of another” [37] (p. 395). These expectations are related to perceptions of the partner organization and its trustworthiness, while the intention to accept vulnerability can be essentially regarded as a risk-taking act [38]. Trust appears to be characteristic of successful integration efforts [4]. Maguire and Phillips [39] point out that institutional trust can be weakened by the ambiguous perception of the identity of a new organization. Stahl and Sitkin [40] suggest that the acquired firm employees’ own image of the acquirer TMT’s trustworthiness can be influenced by the past relations between the two organizations, the distance between them, and—most notably—the approach to integrating both organizations chosen by the acquiring firm.

Thus, we argue that the decision of the acquirer as to the extent of autonomy of the acquired firm is relevant in explaining the success of the cooperation and integration of two organizations, as it reflects the trust given to the acquired organization. While the structural integration can be inevitable in order to exploit potential synergies between the acquired and acquiring firms [41], the loss of autonomy that typically accompanies integration can per se be detrimental to acquisition outcomes [42]. Furthermore, a sustainable merger of both organizations requires a significant involvement of managerial attention on the part of the parent company, which results in possible distraction of the acquiring firm from its strategic priorities [43].

Indeed, the integration-autonomy tension may be particularly important in M&A of high-tech firms. Such deals are oftentimes driven by the intention of getting access to knowledge-related assets [44]. However, integration can eventually afflict the tacit know-how of the purchased organization, as employee turnover may increase, while organizational routines which can be part of the previous competitive advantage, may be discontinued [44,45]. Past research has regarded the integration between the acquiring and acquired firms as something imposed on the acquired organization, rather than an active process which requires a significant involvement by leaders from both sides of the deal. Öberg [46] argues that “if the acquirer aims to keep the innovative firm innovative, its target should not be too young a firm, while it, in compliance with previous research, should be kept autonomous” (p. 400).

However, for the operational process of merging two firms to be truly sustainable, it requires involvement on both sides of the transaction. On the one hand, the acquiring firm must go on to grow independently in order to remain competitive. On the other hand, the acquired firm must continue working on its own technology. Not least, the two organizations must jointly explore the potential for exploiting new solutions and sharing them effectively [47].

Thus, we propose that:

H1:

The retained autonomy level of the acquired company will have a positive influence on acquisition success.

Furthermore, a number of studies stress the relevance of a trust in the contacts between two organizations as a key to initiatives related to organizational change [48]. M&As often lead to a change in ownership for acquired firms, which often leads to changes in their organizational and management practices. Hence, inspiring employees and instilling them with a feeling of trust may be among the key strategies for reducing barriers to change.

There is substantial anecdotal case-based evidence [36] and interviews with acquired managers and employees [35] suggesting that the time after an M&A is characterized by constant risk assessment, whereby trust can be damaged, its restoration being more difficult. New executives functioning within a new organization may not necessarily inspire trust in the acquired firm, as the latter’s members may feel insecure as to their future in the organization [46,49].

Employees of the acquired firm may likely experience ambiguity, uncertainty, and stress related to the change process and its results [50]. Trust can alleviate these concerns, as it is an important tool in managing risk, reducing complexity, and overcoming unfamiliarity [51]. Conversely, the readiness for change on the part of the acquired firm will decline if leaders, which serve as role models to their employees, behave in a manner which is inconsistent with their communication [52]. In other words, TMTs serve as a behavioral point of reference which employees recur to during times of organizational change, therefore trust in them appears to be a crucial determinant of a sustainable merger and cooperation of two organizations. Hence, we posit that:

H2:

The acquired firm management’s trust in management will have a positive influence on acquisition success.

3. Methodology

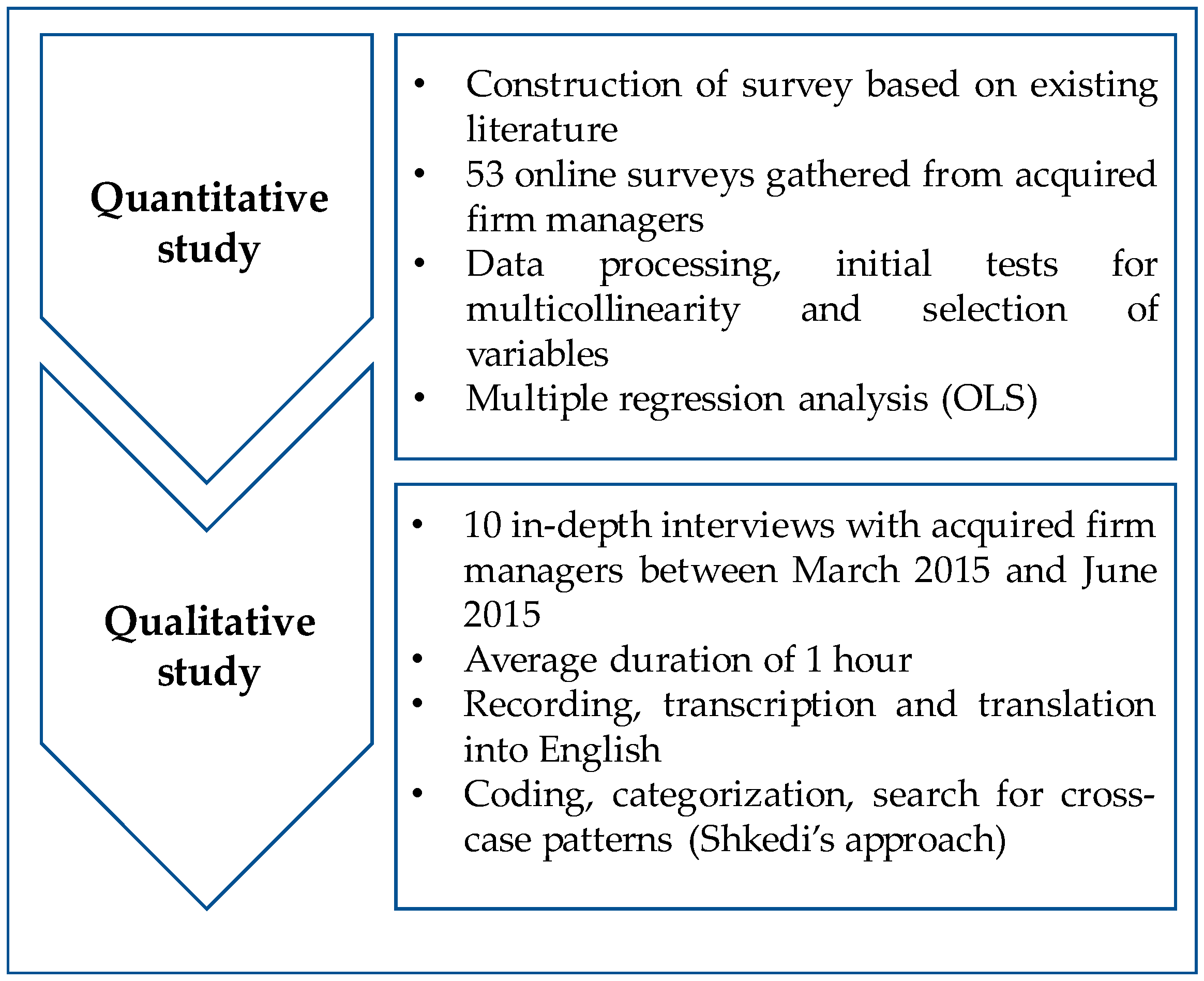

Due to the complex nature of M&A transactions, quantitative evidence alone is insufficient and qualitative data is needed to help explain the initial quantitative data [53,54]. In this current research, the quantitative data collection stage preceded the qualitative data collection stage which utilized in-depth semi-structured interviews [53]. Accordingly, we applied an explanatory sequential research design [55], summarized in Figure 1 below. Over the past few decades, M&A research has used rather standardized methods. However, if researchers are to enhance their knowledge of sustainable M&A facilitators, they ought to rethink the ways in which they generate knowledge in the field, both with regard to research designs and data sources. In this context, a mixed-method design can contribute to exploring M&A success factors more effectively. Mixed methods, furthermore, allow more views to be voiced and therefore can lead to a more balanced evaluation. The next paragraphs describe the procedures and building blocks of this research’s design and the tools developed to cope with the sample and data collection.

To summarize, we employed a two-phased, sequential mixed-methods research design with a key role of quantitative results, followed up with qualitative semi-structured interviews. The reason for the qualitative extension is to enhance the understanding of the quantitative results [56]. More specifically, the purpose of using qualitative analysis was to obtain frontal and “live” information from TMTs concerning their attitudes, drive, interest, and arguments. The interviews allowed us to analyze the processes along the strategic milestone decisions to sell their start-up. Also, the mixed-method design aimed at enhancing the reliability and validity of this research.

3.1. Quantitative Study

3.1.1. Data Collection

The quantitative sample was comprised of TMT members of Israeli high-tech start-ups acquired over a six-year time period (2009–2014). Data analyzed by the IVC-research center (IVC-Meitar Exits Report, 2014) indicates that 547 transactions were executed in Israel during this time period. The research sample was gathered from several sources. Most participants were pulled out of lists containing entrepreneurs’ and TMT members’ names and positions in Israeli start-up companies which have gone through a process of M&A during the six-year period (2009–2014).

In total, 125 invitations were sent via e-mail during the first quarter of 2015. An electronic reminder was sent to those who had not responded within 14 working days. The survey invitations, including a link to the online survey, were e-mailed to the top managers of acquired companies through Qualtrics™. In total, 105 surveys were viewed (but not necessarily completed) and 12 surveys remained incomplete. 53 respondents filled out the survey, leading to a 58% response rate. The size of the acquired firms ranged from 5 to more than 200 employees (48% of them employ 5–50 employees). Ultimately, the sample comprised 53 companies, the basic description of which is provided in Table 1.

3.1.2. Operationalization of Variables

With regard to the operationalization of variables (see Table A1 in Appendix A for a summary), the dependent variable was perceived performance, which we used as an indicator of success and hence a possibly sustainable acquisition. Managers from both firms usually have extensive knowledge about the deal, as well as the subsequent integration phase. Furthermore, numerous studies found clear evidence indicating that the ratings provided by managers correlate with objective success measures, e.g., [57]. Although acquisition results are to some extent uncertain, particularly in technology industries’ settings, one can certainly assume the existence of an alignment between the genuine motives and the outcomes of an acquisition [58]. In the current study, five items measured ‘perceived performance’, with a value of Cronbach’s alpha of 0.87 (see Appendix A for details).

Secondly, satisfaction with the acquisition can be described as the degree to which a manager anticipates feeling satisfied following the acquisition. Participants were requested to evaluate their satisfaction with the acquisition process in five questions with a Cronbach’s alpha value of 0.89.

The use of perceptual measures in our research context also has further reasons. As argued by Podsakoff & Organ [59], reasonable alternatives to perceptual items may be absent with regard to smaller organizations. Moreover, Venkatraman and Ramanujam [60] noted that perceptual data displayed less method variance as compared to secondary data. The perception of integration success was also advocated and used by Graebner [61] in cases where historical data is hardly or not available to the researcher, which holds true for acquired small firms.

With regard to independent variables, retained autonomy was measured using three items regarding asymmetric shift in control from one firm to the other: (a) financial control; (b) administrative control; and (c) operational control. These added three more questions inspired by extant literature [42,62], yielding a scale with six items and the alpha of 0.88.

With regard to trust by the acquired firm, the questions pertained to the managers’ beliefs regarding the acquiring firm management’s trustworthiness and fairness. The survey included six questions regarding trust [63,64], whereby Cronbach’s alpha amounted to 0.63.

Due to a large number of further factors affecting organizational performance identified in extant studies, we incorporated a number of control variables in our analysis. The first one among them, the quality of information regarding the change process, was also measured using a four-item scale adapted from Wanberg and Banas [65]. Further, consistent with Schoenberg’s [66] research, in this study, knowledge transfer was captured with the extent to which knowledge was transmitted from, and to, the acquired organization in such areas as product and service design, R&D, service manufacturing operations, purchasing/supplier relation, distribution/outlets, HRM, or marketing and sales. Readiness for change was measured using a combination of two types of scales: the first one by Holt, Armenakis, Field, and Harris [67] to assess readiness at an individual level and the second by Meyer and Allen [68] to assess affective organizational commitment.

Furthermore, acquired company size was assessed by requesting survey participants to provide the number of their acquired firms’ employees before the acquisition (on a scale ranging between less than 50 to more than 200). Previous experience with M&A was captured as a binary variable. Survey participants were additionally requested to state how many M&As they have experienced on a scale ranging from one to three and more. While all respondents were drawn from high-tech industries, such industries are highly diversified and there is significant difference in their technological and patenting-intensity, which can be to some extent attributed to inter-sector discrepancies in the nature of knowledge and the appropriability regime [69]. For that reason, respondents were asked to mention the sector they work in. Finally, the intention to leave was captured with five questions derived from Cammann et al. [70], with an alpha of 0.87.

3.2. Qualitative Study

The data were gathered from ten acquired firms’ managers by means of in-depth interviews. Each interview lasted roughly one hour and all ten interviews were carried out between March 2015 and June 2015. All the interviews (conducted in the Hebrew language) were recorded, and then transcribed and translated into English. In the analysis of the scripts obtained from the recorded interviews, we followed the approach of Shkedi [71]. Accordingly, we focused on the inductive connections between the sub-texts as units of analysis, which are referred to as ‘themes’. The objective of devising thematic categories pertains to assigning a couple of response codes which have a functionally equivalent meaning to a higher order thematic category.

A phenomenon can usually only be fully understood within its own nature and culture. Therefore, after interviews with informants were conducted, the data was analyzed by splitting the information into categories and by re-arranging the different categories into a meaningful analytical order. The process of categorization, or coding, was conducted by differentiating, classifying, and separating texts in order to find the data’s conceptual meaning. We began the analysis of data with data narrowing by coding of interview texts and preparing data displays by putting all coded data and quotes into a table. A ‘categories tree’, a data driven schematic presentation of the themes, was another tool used to support the analysis.

4. Results

4.1. Quantitative Results

To gain an initial overview of the data, a series of Pearson correlation tests were conducted between all research variables in order to achieve indications regarding the relationships between them. As shown in Table 2, Pearson correlations are generally consistent with the research hypotheses.

Subsequently, a series of multiple regression analyses (OLS) were conducted. In two analyses, shown in Table 3 and Table 4, the expected influence of trust on both sides of the relationship on the two dependent variables, ‘perceived performance’ and ‘satisfaction with acquisition’, was examined. Both analyses display a high percentage of variance explained (R2). The findings suggest that only trust in the acquired firm has a significant effect on the performance measures, both for ‘perceived performance’ and ‘satisfaction with acquisition’. Conversely, trust given by the acquiring firm in the form of autonomy granted to the new subsidiary, does not turn out to be significant.

It appears, accordingly, that acquired firm-related variables have a significant effect on satisfaction and performance. For both dependent variables, on the side of the control variables pertaining to the acquiring firm, knowledge transfer turns out to be significant. While the readiness and commitment to change did not turn out to be significant, one of our control variables, the intention to leave, was negative and significant, partly supporting the relevance of commitment of the acquired firm for acquisition success.

4.2. Qualitative Results

The aim of this section is to better understand the findings of the quantitative analysis and to look for in-depth explanations of unclear or conflicting findings.

No support was found for Hypothesis 1 that the retained autonomy level of the acquired company will have a positive influence on M&A success. However, the qualitative data indicates that there is some support for it. In most cases, the interviewees mentioned that their strategy and negotiating tactics were mainly aimed at realizing and finalizing the deal, which meant that “to retain autonomy is not a must unless in some specific things. The acquirer doesn’t buy in order to replace the owners but to use the acquired company as a multiplier power and you can’t achieve this unless you match yourself to the big company”. This quote, and others, suggest that, in their negotiations, the acquired TMT primarily prioritizes flexibility, openness, reasonable compromises, and taking care of employees’ concerns and culture. Next on the priority list are exclusive projects that do not necessarily require the retention of autonomy.

It can therefore be concluded that acquired start-ups do not necessarily insist on remaining autonomous and that retained autonomy is viewed as part of the negotiations’ ‘give and take’ trade-offs. After the deal has been sealed, some of the interviewees reported regret that they did not insist on retaining some of their authorities and decision-making privileges. A follow-up on the reviewed cases indicated that three out of the six M&A success stories are managed as separate units, retaining a broad autonomy. The factors which limit autonomy are mainly related to purchasing, accounting reporting, hiring approval, legal issues, and administrative regulation (e.g., travelling procedures etc.).

Instead, the continuity of the product development seems to be more important to TMTs than other considerations, such as allowing more autonomy to the acquired firm etc. Only in rare cases did the start-up founders admit that “in the beginning we very much wanted to become integrated. Afterwards we saw that we’ve integrated too deep and were breaking into pieces, so we took a step back. It was a complicated challenge”. Another interviewee summarized: “We won a lot of advantages from working according to the American system but we lost elasticity, bastardy and corner rounding”.

With regard to Hypothesis 2, the results of our qualitative research resonate with earlier studies examining trust, as it found consensus building, providing feedback, and delivering appropriate communication to be important tools for developing trustworthiness. The interviewed managers emphasized the significance of two aspects of trust: trust in the management of the start-up itself and trust in the TMT of the acquirer. Moreover, although the acquirers of our sample of start-up managers were all foreign companies investing in Israel, national cultural clashes were not reported as a hurdle for the development of mutual trust. The mutual agreed upon premise was that “it is good for the company, for the technology and for the employees”. This consensus formed a shared vision with enough transparency for all M&A participants. Once a highly credible acquired leader communicates to his or her employees that the TMT of the acquirer is trustworthy, and that it is likely to keep its promises (during and after the integration process), the employees will usually believe their leader. Therefore, by communicating the above to the employees, the leader reinforces the development of trust in acquiring firms’ TMT.

5. Discussion and Conclusions

The findings of this paper indicate that trust is a significant factor influencing M&A success. While some other studies also emphasize the significance of trust with regard to M&A, the present study is the first one to examine trust on both the side of the acquired and acquiring company. In doing so, it is also arguably the first one to apply this research question to the context of high-tech start-ups. Many of the theories employed in M&A research have used an individual or group level of analysis to address behavioral issues. Only a small number of studies use a firm-level analysis to explore behavioral aspects related to the acquired firm’s management. This paper is one of these studies. Moreover, contrary to the majority of M&A-related research, which focuses on the acquirer’s perspective, this study explores the acquired firm’s perspective in more depth, making it an essential contribution of our paper.

The role of trust also gains importance due to the international dimension of the phenomenon under study. When the acquirer comes from a different country, both sides, the acquirer and the acquired, feel less secure about the outcomes of integration. The said situation leads to tensions when attempting to forge links between the members of both organizations [72]. Integrating two organizations following a cross-border acquisition appears to be so challenging since it necessitates a ‘double-layered’ acculturation, in which both organizations have to adapt not only to a new country culture, but also to different organizational values and practices [73]. Most Israeli start-ups are established with an international orientation and can be viewed as ‘technology-based born global’ firms, which facilitates integration with foreign firms [74].

On the other hand, our quantitative findings did not support the hypothesis postulating that the acquiring firm’s trust, as manifested in the retained autonomy level of the acquired company, has a positive influence on acquisition success. It is worth noting here that also the study by Zaheer et al. [75] recently observed a negative link between acquired unit autonomy and the consolidation of the functional operations of the acquired firm into the reporting hierarchy of the acquirer. We strongly argue that the motive of technology acquisition should coincide with a visible level of trust from the acquirer if the acquired organization is to retain its innovative mandate and flexible approach, a point which resonates in our qualitative study. Although previous research on M&A has often accentuated the challenge of balancing integration and autonomy [41], the loss of autonomy can indeed be detrimental to acquisition performance [42]. An effective integration of the acquired firm demands a substantial commitment of managerial resources, a requirement that may distract the acquirer from its own core business [43]. In particular, this dilemma between integration and autonomy may be important in acquisitions of technology firms. Such deals are oftentimes led by the intention to gain access to tacit knowledge [44]. And yet, as discussed earlier, the negative outcomes of acquisition in the absence of trust may in reality turn out to be counter-productive and detrimental to knowledge generation [43,44].

However, due to the heterogeneity and the small size of our sample, it is impossible to reach to generalizable conclusions regarding attitudes towards autonomy. Nevertheless, it seems that, even for managers who have previous experience with M&A, the recognition of the importance of autonomy retention often only arises post-mortem, after discussions regarding autonomy have been neglected or continuously postponed in the negotiation process. This observation takes into account that while negotiating, managers must deal with a vast number of considerations simultaneously in order to highlight their attractiveness to the acquirer, which is a useful managerial implication of our study.

Another managerial finding is that when the two firms are highly complementary, it may make economic sense for the acquiring firm to grant trust to the acquired firm by leaving it autonomous and not interfering with its operations, even if only temporarily. When a mutual understanding and an agreed performance tracking system are in place, the acquired entity could be managed autonomously as a separate business unit. A similar case is when the acquirer does not have any technological value to add to the knowledge of the acquired firm. In such cases, some responsibilities may be transferred to the acquirer (e.g., budget and performance control, procurement, headcount planning, and accountancy matters), while others, such as R&D responsibilities, may be retained by the acquired company.

In conclusion, even though autonomy is expected to be a subject of great importance to start-ups, Israeli TMTs treat retained autonomy as one of many items listed on their negotiation checklist. During the negotiating process, they tend to adopt a pragmatic approach prioritizing certain topics over others. During this process, the subject of mutual trust and the resulting granted autonomy is at times removed from the list of items that the acquired company wishes to insist on. In retrospect, during the post-merger phase, acquired managers may come to regret their approach towards autonomy retention during the negotiation process.

The authors of this paper recognize that there are several issues which may partly reduce the validity of the findings of this study. The scope of this study was limited to the post-acquisition stage. While studies have demonstrated that the post-acquisition stage is a major predictor of acquisition performance, there are many variables having concurrent effects at each stage of a given merger. Such factors may affect subsequent stages. It was not feasible to address all stages of M&A in this paper. Thus, a future study addressing similar research questions during different stages of M&A, including the buyer’s perspective, may be useful. Such study would also address a limitation of the present paper that for some of the more recent transactions in the sample, the timeframe for managers to assess the outcomes of the acquisition may not be sufficiently long to provide a meaningful assessment.

Furthermore, the outcome of this is highly sensitive to variables such as the form or type of acquisition, the strategy and underlying motivation of the acquiring firms, or the capital control over the acquired unit. As this information was not gathered in this research project, a promising avenue for future research would be to investigate the moderating role that such strategic and structural variables may have on the effects of trust.

The conclusions of this paper may be limited to the Israeli culture of start-up organizations. Therefore, it is assumed that respondents reflect their own domestic culture, which affects their perceptions of the role of leaders’ communication during the post-merger or post-acquisition integration stage. While the literature review consisted of an analysis of both domestic and foreign firms, the study itself featured the ‘organizational culture’ concept, but not the ‘national culture’ concept. National culture shapes the manner in which foreign firms are regarded by the host country and affects any host government’s preferences in economic, social and trade policies. Thus, examining the effect of country cultures on the acculturation of international M&A might lead to divergent findings to those reached in this study. Future studies could therefore be extended to include an analysis of cross-border M&A, focusing on the construct of ‘national culture’ and examining the impact of this construct on mutual trust. This is more relevant given that, as Vaara et al. [76] discovered, both organizational and national cultural differences are positively related to knowledge transfer. Colman and Lunnan [77] investigated how identity threat can support knowledge transfer. They established that the threat to identity intensified the initiatives among acquired managers, who made sure to gain more acknowledgement and appreciation for their know-how and technological solutions in the eyes of the acquirer. This led to the generation of serendipitous value with regard to “new work processes, technologies, and organizational and cultural renewal” ([77], p. 853). Interactions between culture, trust, and innovative initiatives in acquired firms can be interesting a field of enquiry.

The sample size of the study was admittedly small and included mainly executives. It was impossible to reach out to more employees of acquired companies. While we strove to include a wide variety of high-tech industries in the research, the results of this study cannot be generalized to sectors not represented by the sample. The objective of this research was to examine both positive and negative M&A experiences. The quantitative questionnaire was anonymous and it was therefore impossible to distinguish between success and failure cases. The significance of such a distinction only became clear to us during the qualitative phase, and we were therefore unable to monitor the success or failure cases in advance. A future study could extend our methodology to compare success and failure stories with regard to trust or the lack thereof.

Finally, longitudinal studies could be designed in order to further shed light on the development of trust in acquisitions from a process perspective. Such longitudinal research capturing various points along the integration timeline could assess alterations in mutual trust and their effect on integration successes. Contrasting the perspectives of both organizations involved in the process would also generate valuable insights.

Author Contributions

O.Z. conducted the literature review and designed and carried out the quantitative research. J.P. took part in the conceptualization, extended the literature review, consulted the empirical studies, and wrote-up several sections of the paper. P.T. extended the literature review, consulted the design and validity of the empirical studies, and wrote-up the paper.

Funding

This research received no external funding

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

{kind=link}

Table A1.

Operationalization of key variables.

| Construct | Items | Scale |

|---|---|---|

| Dependent Variables | ||

| Performance | Please specify, to what extent the expectations you had before the merger were indeed materialized after its completion: In your opinion—to what extent did the planned merger process was conducted in a similar manner (1) To what extent did the merger’s results meet your expectations (2) In your opinion, to what extent the goals that were set before the merger were achieved (3) Expectations for improvement in company’s decision-making (4) expectations about the company’s ability to meet its forecast regarding its performance (5) | To a very small extent—1; to a very large extent—5 |

| Satisfaction with the merger | To what extent do you agree with the following statements: I was satisfied with the results of the merger (1) The integration process was successful in my opinion (2) I was not satisfied with the way the merger has been implemented (3) I was pleased with the performance of the Company’s management (4) to what extent did the merger meet your expectations of it (5) | To a very small extent—1; to a very large extent—5 |

| Independent Variables | ||

| Retained autonomy | How your company’s management (Acquired) was involved in making these decisions during the merger: Setting performance goals (1) Managing research and development budgets (2) Providing work plan priorities (3) Building periodic company budget (4) Establishing procedures and practices (5) Managing purchases, suppliers and subcontractors (6) Building and managing an employee recruitment plan (7) | Liability of the acquiring company—1; acquired company’s liability—5 |

| Trust | To what extent do you agree with the following statements: I had a feeling I could trust management during the merger (1) Senior management exercised, upon completion of the merger, the promises given to us prior to the merger (2) Management has consistently implemented the policy of the Company in all of its units (3) I thought that the merger could harm the way things are done in the organization (4) I thought the merger and the change followed, would be beneficial for me (5) I thought that if management is entering a merger process, it must have good reasons to think that the merger is necessary for the company’s success (6) | Strongly disagree—1; definitely agree—5 |

References

- Bloomberg Global M&A Market Review Q1 2018. Available online: https://data.bloomberglp.com/professional/sites/10/Bloomberg-Global-MA-Legal-Ranking-Q1-2018.pdf (accessed on 29 May 2018).

- Li, J.; Li, Y.; Shapiro, D. Knowledge seeking and outward FDI of emerging market firms: The moderating effect of inward FDI. Glob. Strateg. J. 2012, 2, 277–295. [Google Scholar] [CrossRef]

- Faulkner, D.; Teerikangas, S.; Joseph, R.J. Introduction. In Handbook of Mergers & Acquisitions; Faulkner, D., Teerikangas, S., Joseph, R., Eds.; Oxford University Press: Oxford, UK, 2002; pp. 1–18. ISBN 0198703880. [Google Scholar]

- Stahl, G.K.; Larsson, R.; Kremershof, I.; Sitkin, S.B. Trust dynamics in acquisitions: A case survey. Hum. Res. Manag. 2011, 50, 575–603. [Google Scholar] [CrossRef] [Green Version]

- Marks, M.L.; Mirvis, P.H. Making mergers and acquisitions work: Strategic and psychological preparation. Acad. Manag. Perspect. 2001, 15, 80–92. [Google Scholar] [CrossRef]

- King, D.R.; Dalton, D.R.; Daily, C.M.; Covin, J.G. Meta-analyses of post-acquisition performance: Indications of unidentified moderators. Strateg. Manag. J. 2004, 25, 187–200. [Google Scholar] [CrossRef]

- Risberg, A. Employee experiences of acquisition processes. J. World Bus. 2001, 36, 58–84. [Google Scholar] [CrossRef]

- Vaara, E. Post-acquisition integration as sensemaking: Glimpses of ambiguity, confusion, hypocrisy, and politicization. J. Manag. Stud. 2003, 40, 859–894. [Google Scholar] [CrossRef]

- Van Dick, R.; Ullrich, J.; Tissington, P.A. Working under a black cloud: How to sustain organizational identification after a merger. Br. J. Manag. 2006, 17, S69–S79. [Google Scholar] [CrossRef]

- Sarala, R.M.; Junni, P.; Cooper, C.L.; Tarba, S.Y. A Sociocultural Perspective on Knowledge Transfer in Mergers and Acquisitions. J. Manag. 2016, 42, 1230–1249. [Google Scholar] [CrossRef]

- Amiot, C.; Terry, D.; Jimmieson, N.; Callan, V. A longitudinal investigation of coping processes during a merger: Implications for job satisfaction and organizational identification. J. Manag. 2006, 32, 552–574. [Google Scholar] [CrossRef]

- Väänänen, A.; Pahkin, K.; Kalimo, R.; Buunk, B.P. Maintenance of subjective health during a merger: The role of experienced change and pre-merger social support at work in white-and blue-collar workers. Soc. Sci. Med. 2004, 58, 1903–1915. [Google Scholar] [CrossRef] [PubMed]

- Angwin, D.N.; Paroutis, S.; Connell, R. Why good things Don’t happen: The micro-foundations of routines in the M&A process. J. Bus. Res. 2015, 68, 1367–1381. [Google Scholar] [CrossRef] [Green Version]

- Haunschild, P.R.; Moreland, R.L.; Murrell, A.J. Sources of resistance to mergers between groups. J. Appl. Soc. Psychol. 1994, 24, 1150–1178. [Google Scholar] [CrossRef]

- Terry, D.J.; Callan, V.J.; Sartori, G. Employee adjustment to an organizational merger: Stress, coping and intergroup differences. Stress Med. 1996, 12, 105–122. [Google Scholar] [CrossRef]

- Veiga, J.; Lubatkin, M.; Calori, R.; Very, P. Research note measuring organizational culture clashes: A two-nation post-hoc analysis of a cultural compatibility index. Hum. Relat. 2000, 53, 539–557. [Google Scholar] [CrossRef]

- Seo, M.; Hill, N.S. Understanding the human side of merger and acquisition: An integrative framework. J. Appl. Behav. Sci. 2005, 41, 422–443. [Google Scholar] [CrossRef]

- Puranam, P.; Singh, H.; Zollo, M. Organizing for innovation: Managing the coordination-autonomy dilemma in technology acquisitions. Acad. Manag. J. 2006, 49, 263–280. [Google Scholar] [CrossRef]

- Zollo, M.; Meier, D. What is M&A performance? Acad. Manag. Perspect. 2008, 22, 55–77. [Google Scholar]

- Homburg, C.; Bucerius, M. A marketing perspective on mergers and acquisitions: How marketing integration affects postmerger performance. J. Mark. 2005, 69, 95–113. [Google Scholar] [CrossRef]

- Avram, D.O.; Kühne, S. Implementing responsible business behavior from a strategic management perspective: Developing a framework for Austrian SMEs. J. Bus. Ethics 2008, 82, 463–475. [Google Scholar] [CrossRef]

- Salvato, C.; Lassin, U.; Wiklund, J. Dynamics of external growth in SMEs: A process model of acquisition capabilities emergence. Schmalenbach Bus. Rev. 2007, 59, 282–305. [Google Scholar] [CrossRef]

- Dooley, L.; O’Sullivan, D. Managing within distributed innovation networks. Int. J. Innov. Manag. 2007, 11, 397–416. [Google Scholar] [CrossRef]

- Zaks, O.; Polowczyk, J.; Trąpczyński, P. Success factors of start-up acquisitions: Evidence from Israel. Entrep. Bus. Econ. Rev. 2018, 6, 201–216. [Google Scholar] [CrossRef]

- Avnimelech, G.; Schwartz, D. Structural changes in mature venture capital industry: Evidence from Israel. Innov. Manag. Policy Pract. 2009, 11, 60–73. [Google Scholar] [CrossRef]

- Dashti, Y.; Schwartz, D.; Pines, A. High technology entrepreneurs, their social networks and success in global markets: The case of Israelis in the US market. In Current Topics in Management; Rahim, A., Ed.; Transaction Publishers: Piscataway, NJ, USA, 2008; Volume 13, pp. 131–144. ISBN 978-0762301508. [Google Scholar]

- De Fontenay, C.; Carmel, E. Israel’s silicon wadi: The forces behind cluster formation. In Building High Tech Clusters: Silicon Valley and Beyond; Bresnahan, T., Gambardella, A., Eds.; Cambridge University Press: Cambridge, UK, 2004; pp. 40–77. ISBN 978-0521143486. [Google Scholar]

- Akerlof, G.A.; Shiller, R.J. Animal Spirits: How Human Psychology Drives the Economy, and Why It Matters for Global Capitalism; Princeton University Press: Princeton, NI, USA; Oxford, UK, 2009; ISBN 978-0691145921. [Google Scholar]

- Kahneman, D.; Lovallo, D.; Sibony, O. Before you make that big decision. Harv. Bus. Rev. 2011, 89, 50–60. [Google Scholar] [PubMed]

- Thaler, R.H. From homo economicus to homo sapiens. J. Econ. Perspect. 2000, 14, 133–141. [Google Scholar] [CrossRef]

- Camerer, C.F.; Loewenstein, G. Behavioral Economics: Past, Present, Future. 2002. Available online: http://www.hss.caltech.edu/~camerer/ribe239.pdf (accessed on 30 March 2018).

- Arrow, K.J. Principals and Agents: The Structure of Business; Harvard Business School Press: Boston, MA, USA, 1985. [Google Scholar]

- Chrupała-Pniak, M.; Grabowski, D.; Sulimowska-Formowicz, M. Trust in Effective International Business Cooperation: Mediating Effect of Work Engagement. Entrep. Bus. Econ. Rev. 2017, 5, 27–50. [Google Scholar] [CrossRef] [Green Version]

- Inkpen, A.; Currall, S.C. The coevolution of trust, control, and learning in joint ventures. Org. Sci. 2004, 15, 586–599. [Google Scholar] [CrossRef]

- Krug, J.A.; Nigh, D. Executive perceptions in foreign and domestic acquisitions: An analysis of foreign ownership and its effect on executive fate. J. World Bus. 2001, 36, 85–105. [Google Scholar] [CrossRef]

- Chua, C.H.; Engeli, H.P.; Stahl, G. Creating a new identity and high performance culture at Novartis. In Mergers and Acquisitions: Managing Culture and Human Resources; Stahl, G.K., Mendenhall, M.E., Eds.; Stanford Business: Stanford, CA, USA, 2005; pp. 379–400. ISBN 9780804746618. [Google Scholar]

- Rousseau, D.M.; Sitkin, S.B.; Burt, R.S.; Camerer, C. Not so different after all: A cross-discipline view of trust. Acad. Manag. Rev. 1998, 23, 393–404. [Google Scholar] [CrossRef]

- Vanhala, M.; Heilmann, P.; Salminen, H. Organizational trust dimensions as antecedents of organizational commitment. Knowl. Proc. Manag. 2016, 23, 46–61. [Google Scholar] [CrossRef]

- Maguire, S.; Phillips, N. ‘Citibankers’ at Citigroup: A study of the loss of institutional trust after a merger. J. Manag. Stud. 2008, 45, 372–401. [Google Scholar] [CrossRef]

- Stahl, G.K.; Sitkin, S.B. Trust dynamics in acquisitions: The role of relationship history, interfirm distance, and acquirer’s integration approach. In Advances in Mergers and Acquisitions; Cooper, C.L., Finkelstein, S., Eds.; Emerald Group Publishing Limited: Bingley, UK, 2010; pp. 51–82. ISBN 978-0-85724-465-9. [Google Scholar]

- Capron, L. The long-term performance of horizontal acquisitions. Strat. Manag. J. 1999, 20, 987–1018. [Google Scholar] [CrossRef]

- Very, P.; Lubatkin, M.; Calori, R.; Veiga, J. Relative Standing and the Performance of Recently Acquired European Firms. Strat. Manag. J. 1997, 18, 593–614. [Google Scholar] [CrossRef]

- Schoar, A. Effects of corporate diversification on productivity. J. Financ. 2002, 57, 2379–2403. [Google Scholar] [CrossRef]

- Ranft, A.L.; Lord, M.D. Acquiring new technologies and capabilities: A grounded model of acquisition implementation. Org. Sci. 2002, 13, 420–441. [Google Scholar] [CrossRef]

- Puranam, P.; Singh, H.; Zollo, M. The Inter-Temporal Tradeoff in Technology Grafting Acquisitions; Working Paper; London Business School: London, UK, 2002. [Google Scholar]

- Öberg, C. Network imitation to deal with sociocultural dilemmas in acquisitions of young, innovative firms. Thunderbird Int. Bus. Rev. 2013, 55, 387–403. [Google Scholar] [CrossRef]

- Graebner, M.E.; Eisenhardt, K.M.; Roundy, P.T. Success and failure in technology acquisitions: Lessons for buyers and sellers. Acad. Manag. Perspect. 2010, 24, 73–92. [Google Scholar] [CrossRef]

- Gomez, C.; Rosen, B. The leader-member exchange as a link between managerial trust and employee empowerment. Group Org. Manag. 2001, 26, 53–69. [Google Scholar] [CrossRef]

- Hurley, R.F. The Decision to Trust. Harv. Bus. Rev. 2006, 84, 55–62. [Google Scholar] [PubMed]

- Stanley, D.J.; Meyer, J.P.; Topolnytsky, L. Employee cynicism and resistance to organizational change. J. Bus. Psychol. 2005, 19, 429–459. [Google Scholar] [CrossRef]

- Van Dam, K. Employee attitudes toward job changes: An application and extension of Rusbult and Farrell’s investment model. J. Occup. Organ. Psychol. 2005, 78, 253–272. [Google Scholar] [CrossRef]

- Simons, T. Behavioral integrity: The perceived alignment between managers’ words and deeds as a research focus. Organ. Sci. 2002, 13, 18–35. [Google Scholar] [CrossRef]

- Creswell, J.W.; Clark, V.L.P.; Gutmann, M.L.; Hanson, W.E. Advanced mixed methods research design. In Handbook of Mixed Methods in Social & Behavioral Research; Tashakkori, A., Teddlie, C., Eds.; Sage: Thousand Oaks, CA, USA, 2003; pp. 209–240. [Google Scholar]

- Creswell, J.W. Mixed method research: Introduction and application. In Handbook of Educational Policy; Cijek, T., Ed.; Academic Press: San Diego, CA, USA, 1999; pp. 455–472. [Google Scholar]

- Ivankova, N.V.; Creswell, J.W.; Stick, S.L. Using Mixed-Methods Sequential Explanatory Design: From Theory to Practice. Field Methods 2006, 18, 3–20. [Google Scholar] [CrossRef] [Green Version]

- Creswell, J.W.; Clark, V.L.P. Designing and Conducting Mixed Methods Research; Sage: Thousand Oaks, CA, USA, 2007; ISBN 978-1412927918. [Google Scholar]

- Homburg, C.; Bucerius, M. Is speed of integration really a success factor in acquisitions and acquisitions? An analysis of the role of internal and external relatedness. Stratg. Manag. J. 2006, 27, 347–367. [Google Scholar] [CrossRef]

- Coff, R. How buyers cope with uncertainty when acquiring firms in knowledge-intensive industries: Caveat emptor. Organ. Sci. 1999, 10, 144–161. [Google Scholar] [CrossRef]

- Podsakoff, P.M.; Organ, D.W. Self-reports in organizational research: Problems and prospects. J. Manag. 1986, 12, 531–544. [Google Scholar] [CrossRef]

- Venkatraman, N.; Ramanujam, V. Measurement of business economic performance: An examination of method convergence. J. Manag. 1987, 13, 109–122. [Google Scholar] [CrossRef]

- Graebner, M.E. Momentum and serendipity: How acquired leaders create value in the integration of technology firms. Stratg. Manag. J. 2004, 25, 751–777. [Google Scholar] [CrossRef]

- Ranft, A. Knowledge Preservation and Transfer During Post-Acquisition Integration. In Advances in Mergers and Acquisitions; Cooper, C., Finkelstein, S., Eds.; JAI: New York, NY, USA, 2006; Volume 5, pp. 51–67. ISBN 978-70-7623-1337-2. [Google Scholar]

- Oreg, S. Personality, context, and resistance to organizational change. Eur. J. Work Organ. Psychol. 2006. [Google Scholar] [CrossRef]

- Van Dam, K.; Oreg, S.; Schyns, B. Daily work contexts and resistance to organisational change: The role of leader–member exchange, development climate, and change process characteristics. Appl. Psychol. 2008, 57, 313–334. [Google Scholar] [CrossRef] [Green Version]

- Wanberg, C.R.; Banas, J.T. Predictors and outcomes of openness to changes in a reorganizing workplace. J. Appl. Psychol. 2000, 85, 132–142. [Google Scholar] [CrossRef] [PubMed]

- Schoenberg, R. Measuring the performance of corporate acquisitions: An empirical comparison of alternative metrics. Br. J. Manag. 2006, 17, 361–370. [Google Scholar] [CrossRef] [Green Version]

- Holt, D.T.; Armenakis, A.A.; Feild, H.S.; Harris, S.G. Readiness for organizational change: The systematic development of a scale. J. Appl. Behav. Sci. 2007, 43, 232–255. [Google Scholar] [CrossRef]

- Meyer, J.P.; Allen, N.J. Commitment in the Workplace: Theory, Research, and Application; Sage: Thousand Oaks, CA, USA, 1997; ISBN 978-0761901051. [Google Scholar]

- Ahuja, G.; Katila, R. Technological acquisitions and the innovation performance of acquiring firms: A longitudinal study. Stratg. Manag. J. 2001, 22, 197–220. [Google Scholar] [CrossRef]

- Cammann, C.; Fichman, M.J.; Klesh, J.R. Assessing the attitudes and perceptions of organizational members. In Assessing Organizational Change: A Guide to Methods, Measures, and Practices; John Wiley & Sons, Inc.: New York, NY, USA, 1983; pp. 71–138. [Google Scholar]

- Shkedi, A. Words of Meaning: Qualitative Research-Theory and Practice; Tel-Aviv University Ramot: Tel-Aviv, Israel, 2003; ISBN 9780471894841. (In Hebrew) [Google Scholar]

- Nikandrou, I.; Papalexandris, N.; Bourantas, D. Gaining Employee trust after acquisition. Empl. Relat. 2000, 22, 334–355. [Google Scholar] [CrossRef]

- Barkema, H.G.; Bell, J.H.J.; Pennings, J.M. Foreign entry, cultural barriers and learning. Stratg. Manag. J. 1996, 17, 151–166. [Google Scholar] [CrossRef]

- Almor, T. Conceptualizing Paths of Growth for Technology-Based Born-Global Firms Originating in a Small-Population Advanced Economy. Int. Stud. Manag. Org. 2013, 43, 56–78. [Google Scholar] [CrossRef]

- Zaheer, A.; Castañer, X.; Souder, D. Synergy sources, target autonomy, and integration in acquisitions. J. Manag. 2011, 39, 604–632. [Google Scholar] [CrossRef]

- Vaara, E.; Sarala, R.; Stahl, G.K.; Björkman, I. The impact of organizational and national cultural differences on social conflict and knowledge transfer in international acquisitions. J. Manag. Stud. 2012, 49, 1–27. [Google Scholar] [CrossRef] [Green Version]

- Colman, H.L.; Lunnan, R. Organizational identification and serendipitous value creation in post-acquisition integration. J. Manag. 2011, 37, 839–860. [Google Scholar] [CrossRef] [Green Version]

Figure 1.

Summary of the research process.

Table 1.

Sample characteristics.

| Characteristics | # (N = 53) | % | |

|---|---|---|---|

| Number of employees | 5–50 | 24 | 45.3 |

| (in the acquired company)/size | 51–200 | 13 | 24.5 |

| 201− | 16 | 30.2 | |

| 0 | 25 | 47.2 | |

| Previous experience in M&A | 1 | 14 | 26.4 |

| 2+ | 14 | 26.4 | |

| Age (group) | 20–39 | 6 | 11.3 |

| 40–59 | 42 | 79.2 | |

| 60+ | 5 | 9.4 | |

| 1–4 | 16 | 30.2 | |

| Tenure (years) | 5–9 | 19 | 35.8 |

| 10− | 18 | 34 | |

| Time since the merger | −2 | 16 | 30.2 |

| announcements (years) | −4 less | 22 | 41.5 |

| 4+ more | 15 | 28.3 |

Table 2.

Statistical distribution of the research variables.

| Variable | Min | Max | Mean | S.D. | 1 | 2 | 3 | 4 | 5 | 6 | 7 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Retained autonomy (1) | 1 | 5 | 2.61 | 0.88 | |||||||

| Knowledge transfer1 (2) | 1 | 5 | 3.15 | 1.03 | 0.038 | ||||||

| Knowledge transfer2 (3) | 1 | 5 | 3.44 | 1.03 | 0.002 | 0.366 ** | |||||

| Trust (4) | 1.33 | 5 | 3.27 | 0.88 | 0.267 * | 0.184 | 0.445 ** | ||||

| Readiness for change (5) | 1.8 | 4.8 | 3.75 | 0.68 | 0.188 | 0.144 | 0.285 * | 0.516 ** | |||

| Performance (6) | 1 | 5 | 3 | 0.95 | 0.058 | 0.362 ** | 0.204 | 0.524 ** | 0.245 * | 0.398 ** | |

| Satisfaction with acquisition (7) | 1 | 5 | 2.99 | 1.12 | 0.15 | 0.382 ** | 0.426 ** | 0.704 ** | 0.327 ** | 0.519 ** | 0.834 ** |

* p < 0.05. ** p < 0.01. *** p < 0.001.

Table 3.

Results of OLS regression on perceived performance. The original analysis also included some further control variables, notably a communication variable, which is not shown for clarity reasons, as it is not key to the present focus of the paper and does not affect the results. The same remark pertains to Table 4.

Table 3.

Results of OLS regression on perceived performance. The original analysis also included some further control variables, notably a communication variable, which is not shown for clarity reasons, as it is not key to the present focus of the paper and does not affect the results. The same remark pertains to Table 4.

| Variable | B | SE B | β | t | ||

|---|---|---|---|---|---|---|

| Independent variables | ||||||

| Retained autonomy (H1) | −0.31 | 0.18 | −0.29 | −1.77 | ||

| Trust (H2) | 0.74 | 0.25 | 0.65 | *** | 2.94 | |

| Control variables | ||||||

| Knowledge transfer1 | 0.4 | 0.15 | 0.42 | ** | 2.66 | |

| Knowledge transfer2 | −0.07 | 0.14 | −0.07 | −0.49 | ||

| Readiness for change | −0.28 | 0.24 | −0.20 | −1.14 | ||

| Intention to leave | −0.40 | 0.12 | −0.47 | *** | −3.39 | |

| Gender | −0.78 | 0.48 | −0.22 | −1.62 | ||

| Education level | 0.31 | 0.29 | 0.15 | 1.06 | ||

| No. of employees | 0.08 | 0.3 | 0.04 | 0.28 | ||

| Previous merger experience | −0.30 | 0.25 | −0.15 | −1.19 | ||

| Time from notice to merger | −0.45 | 0.3 | −0.24 | −1.52 | ||

| R2 | 0.69 | |||||

| F | 3.74 ** | |||||

** p < 0.01. *** p < 0.001.

Table 4.

Results of multiple regression on satisfaction with acquisition.

| Variable | B | SE B | β | t | ||

|---|---|---|---|---|---|---|

| Independent variables | ||||||

| Retained autonomy (H1) | −0.20 | 0.18 | −0.16 | −1.12 | ||

| Trust (H2) | 0.86 | 0.26 | 0.65 | ** | 3.34 | |

| Control variables | ||||||

| Knowledge transfer1 | 0.32 | 0.15 | 0.29 | * | 2.11 | |

| Knowledge transfer2 | 0.11 | 0.14 | 0.11 | 0.8 | ||

| Readiness and commitment to change | −0.35 | 0.25 | −0.21 | −1.40 | ||

| Intention to leave | −0.33 | 0.12 | −0.34 | ** | −2.76 | |

| Gender | −0.25 | 0.49 | −0.06 | −0.52 | ||

| Education level | 0.39 | 0.29 | 0.17 | 1.34 | ||

| No. of employs | −0.28 | 0.3 | −0.13 | −0.93 | ||

| Previous merger experience | −0.13 | 0.25 | −0.06 | −0.50 | ||

| Time from notice to merger | −0.26 | 0.3 | −0.12 | −0.86 | ||

| R2 | 0.75 | |||||

| F | 5.25 *** | |||||

* p < 0.05. ** p < 0.01. *** p < 0.001.

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Trąpczyński, P.; Zaks, O.; Polowczyk, J. The Effect of Trust on Acquisition Success: The Case of Israeli Start-Up M&A. Sustainability 2018, 10, 2499. https://doi.org/10.3390/su10072499

AMA Style

Trąpczyński P, Zaks O, Polowczyk J. The Effect of Trust on Acquisition Success: The Case of Israeli Start-Up M&A. Sustainability. 2018; 10(7):2499. https://doi.org/10.3390/su10072499

Chicago/Turabian StyleTrąpczyński, Piotr, Ofer Zaks, and Jan Polowczyk. 2018. "The Effect of Trust on Acquisition Success: The Case of Israeli Start-Up M&A" Sustainability 10, no. 7: 2499. https://doi.org/10.3390/su10072499

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.