The Effect of Sustainability as Innovation Objectives on Innovation Efficiency

Abstract

1. Introduction

2. Theoretical Background

2.1. Sustainability as Objective of Innovation

2.2. Innovation Efficiency

2.3. Sustainable Innovation

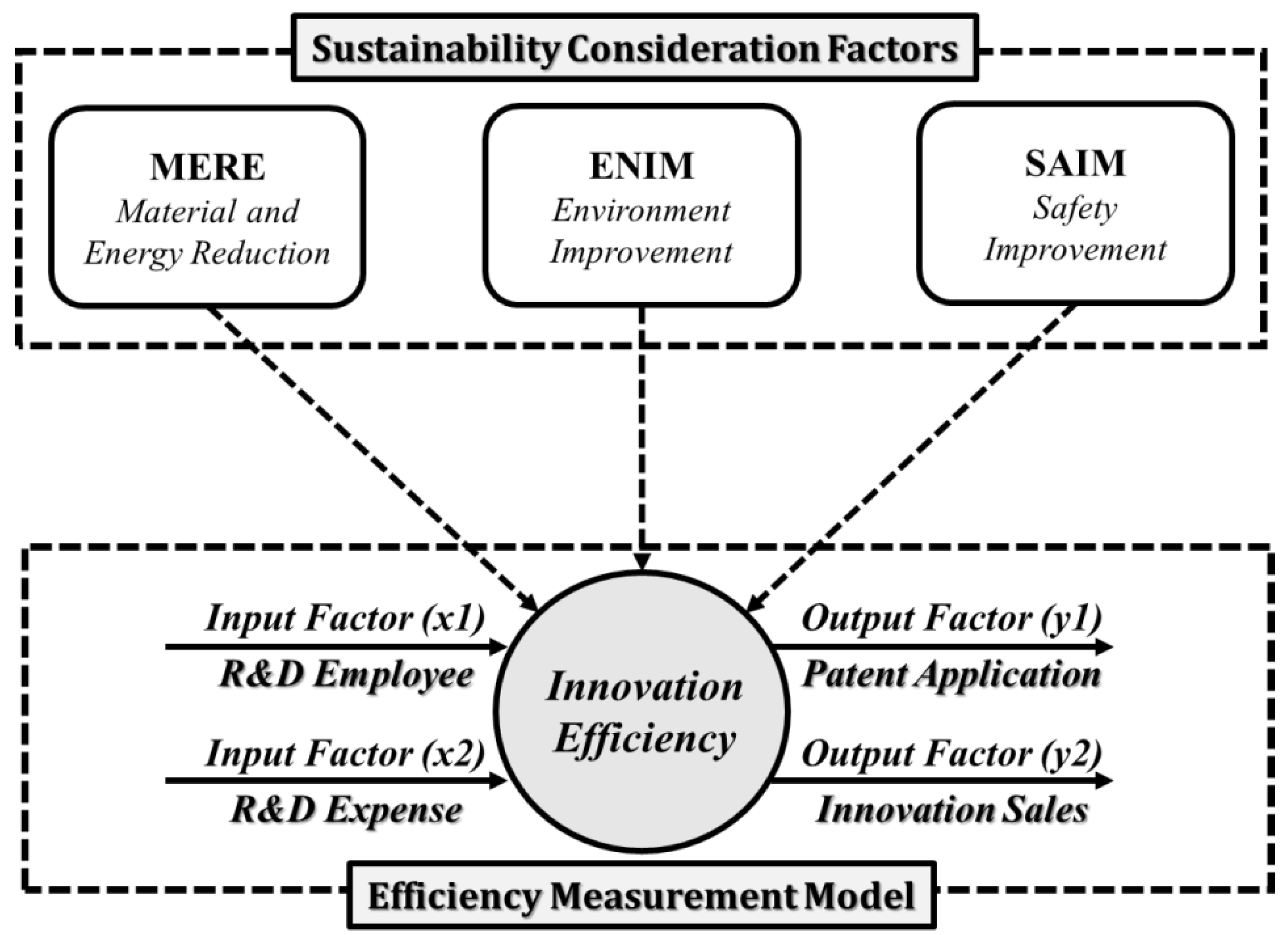

3. Methodology and Model

3.1. Data Envelopment Analysis and Tobit Regression

3.2. Data and Measurement

3.3. Model

4. Results

5. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Lundvall, B.A. National Innovation System: Towards a Theory of Innovation and Interactive Learning; Pinter: London, UK, 1992. [Google Scholar]

- Johannessen, J.A.; Olsen, B.; Olaisen, J. Aspects of innovation theory based on knowledge-management. Int. J. Inf. Manag. 1999, 19, 121–139. [Google Scholar] [CrossRef]

- Korsnes, M.S. The Growth of a Green Industry: Wind Turbines and Innovation in China; University of Oslo: Blindern, Norway, 2012. [Google Scholar]

- Eccles, R.G.; Perkins, K.M.; Serafeim, G. How to become a sustainable company. MIT Sloan Manag. Rev. 2012, 53, 43–50. [Google Scholar]

- Meroño-Cerdan, A.L.; López-Nicolas, C. Understanding the drivers of organizational innovations. Serv. Ind. J. 2013, 33, 1312–1325. [Google Scholar] [CrossRef]

- Wang, T.; Chien, S. Forecasting innovation performance via neural networks—A case of Taiwanese manufacturing industry. Technovation 2006, 26, 635–643. [Google Scholar] [CrossRef]

- Fu, X.; Zanello, G.; Essegbey, G.O.; Hou, J.; Mohnen, P. Innovation in Low Income Countries: A Survey Report. Growth Research Programme. 2014. Available online: https://assets.publishing.service.gov.uk/media/57a089abed915d3cfd00038a/61071_DILIC_Report_2.pdf (accessed on 12 June 2018).

- Schultze, J.; Schröder, A.; Hölsgens, R. Report on the Pilot Application of CASI-F for Assessing Sustainable Social Innovation. 2016. Available online: http://www.sfs.tu-dortmund.de/cms/en/publications/details/index.php?id=1729 (accessed on 17 May 2018).

- Wintjes, R. Systems and Modes of ICT Innovation; JRC Science for Policy Report; European Commission-Joint Research Centre: Bruselas, Belgium, 2016. [Google Scholar]

- Hollanders, H.; Celikel-Esser, F. Measuring Innovation Efficiency. Available online: http://www.pedz.uni-mannheim.de/daten/edz-h/gdb/07/eis_2007_Innovation_efficiency.pdf (accessed on 12 June 2018).

- Guan, J.; Chen, K. Modeling the relative efficiency of national innovation systems. Res. Policy 2012, 41, 102–115. [Google Scholar] [CrossRef]

- Ozkan-Canbolat, E.; Beraha, A. Configuration and innovation related network topology. J. Innov. Knowl. 2016, 1, 91–98. [Google Scholar] [CrossRef]

- Zulu-Chisanga, S.; Boso, N.; Adeola, O.; Oghazi, P. Investigating the path from firm innovativeness to financial performance: The roles of new product success, market responsiveness, and environment turbulence. J. Small Bus. Strategy 2016, 26, 51–67. [Google Scholar]

- Allal-Chérif, O.; Bidan, M. Collaborative open training with serious games: Relations, culture, knowledge, innovation, and desire. J. Innov. Knowl. 2017, 2, 31–38. [Google Scholar] [CrossRef]

- Dudukalov, E.V.; Rodionova, N.D.; Sivakova, Y.E.; Vyugova, E.; Cheryomushkina, I.V.; Popkova, E.G. Global innovational networks: Sense and role in development of global economy. Contemp. Econ. 2016, 10, 299–310. [Google Scholar] [CrossRef]

- Guan, J.; Yam, R.; Tang, E.; Lau, A. Innovation strategy and performance during economic transition: Evidences in Beijing, China. Res. Policy 2009, 38, 802–812. [Google Scholar] [CrossRef]

- Leiponen, S.; Helfat, C.E. Innovation objectives, knowledge sources, and he benefits of breadth. Strateg. Manag. J. 2010, 31, 224–236. [Google Scholar] [CrossRef]

- Yang, H.; Hsiao, S. Mechanisms of developing innovative IT-enabled services: A case study of Taiwanese healthcare service. Technovation 2009, 29, 327–337. [Google Scholar] [CrossRef]

- Naidoo, V. Firm survival through a crisis: The influence of market orientation, marketing innovation and business strategy. Ind. Mark. Manag. 2010, 39, 1311–1320. [Google Scholar] [CrossRef]

- Bala-Subrahmanya, M.H. Technological Innovation in Indian SMEs: Need, Status and Policy Imperatives. Curr. Opin. Creat. Innov. Entrep. 2012, 1, 7–12. [Google Scholar]

- Olomu, M.; Akinwale, Y.; Adepoju, A. Harnessing technological and nontechnological innovations for SMEs profitability in the Nigerian Manufacturing Sector. Am. J. Bus. Econ. Manag. 2016, 4, 75–88. [Google Scholar]

- Albers, J.A.; Brewer, S. Knowledge management and the innovation process: The eco-innovation model. J. Knowl. Manag. Pract. 2003, 4, 1–6. [Google Scholar]

- Kotabe, M.; Murray, J. Linking product and process innovations and modes of international sourcing in global competition: A case of foreign multinational firms. J. Int. Bus. Stud. 1990, 21, 383–408. [Google Scholar] [CrossRef]

- Liu, Z.; Chen, X.; Chu, J.; Zhu, Q. Industrial development environment and innovation efficiency of high-tech industry: Analysis based on the framework of innovation systems. Technol. Anal. Strateg. 2018, 30, 434–446. [Google Scholar] [CrossRef]

- Chen, K.; Guan, J. Measuring the efficiency of China’s regional innovation systems: Application of network data envelopment analysis (DEA). Reg. Stud. 2012, 46, 355–377. [Google Scholar] [CrossRef]

- Cruz-Cázares, C.; Bayona-Sáez, C.; García-Marco, T. You can’t manage right what you can’t measure well: Technological innovation efficiency. Res. Policy 2013, 42, 1239–1250. [Google Scholar] [CrossRef]

- Guan, J.; Chen, K. Measuring the innovation production process: A cross-region empirical study of China’s high-tech innovations. Technovation 2010, 30, 348–358. [Google Scholar] [CrossRef]

- Guan, J.C.; Yam, R.C.; Mok, C.K.; Ma, N. A study of the relationship between competitiveness and technological innovation capability based on DEA models. Eur. J. Oper. Res. 2006, 170, 971–986. [Google Scholar] [CrossRef]

- Wang, Q.; Hang, Y.; Sun, L.; Zhao, Z. Two-stage innovation efficiency of new energy enterprises in China: A non-radial DEA approach. Technol. Forecast. Soc. 2016, 112, 254–261. [Google Scholar] [CrossRef]

- Zhong, W.; Yuan, W.; Li, S.X.; Huang, Z. The performance evaluation of regional R&D investments in China: An application of DEA based on the first official China economic census data. Omega 2011, 39, 447–455. [Google Scholar] [CrossRef]

- Wakil, A.A. When Gambling is Not Winning: Exploring Optimality of VIX Trading under the Expected Utility Theory. J. Bus. Account. Financ. Perspect. 2018. [Google Scholar] [CrossRef]

- Cuomo, M.T.; Tortora, D.; Mazzucchelli, A.; Festa, G.; Di Gregorio, A.; Metallo, G. Impacts of Code of ethics on financial performance in the Italian listed companies of bank sector. J. Bus. Account. Financ. Perspect. 2018, in press. [Google Scholar] [CrossRef]

- Gajdová, D.; Majdúchová, H. Financial Sustainability Criteria and their testing in the conditions of the Slovak Non-Profit Sector. Contemp. Econ. 2018, 12, 33–56. [Google Scholar] [CrossRef]

- De Medeiros, J.F.; Ribeiro, J.L.D.; Cortimiglia, M.N. Success factors for environmentally sustainable product innovation: A systematic literature review. J. Clean. Prod. 2014, 65, 76–86. [Google Scholar] [CrossRef]

- Fussler, C.; James, P. Driving Eco-Innovation: A Breakthrough Discipline for Innovation and Sustainability, Financial Times Management; Pitman Publishing: London, UK, 1996. [Google Scholar]

- Schiederig, T.; Tietze, F.; Herstatt, C. Green innovation in technology and innovation management—An exploratory literature review. R D Manag. 2012, 42, 180–192. [Google Scholar] [CrossRef]

- Doran, J.; Ryan, G. Regulation and firm perception, eco-innovation and firm performance. Eur. J. Innov. Manag. 2012, 15, 421–441. [Google Scholar] [CrossRef]

- Halila, F.; Rundquist, J. The development and market success of eco-innovations: A comparative study of eco-innovations and “other” innovations in Sweden. Eur. J. Innov. Manag. 2011, 14, 278–302. [Google Scholar] [CrossRef]

- Chen, Y.S.; Lai, S.B.; Wen, C.T. The influence of green innovation performance on corporate advantage in Taiwan. J. Bus. Ethics 2006, 67, 331–339. [Google Scholar] [CrossRef]

- Chen, Y.S. The drivers of green brand equity: Green brand image, green satisfaction, and green trust. J. Bus. Ethics 2010, 93, 307–319. [Google Scholar] [CrossRef]

- Chen, Y.S.; Chang, C.H. The determinants of green product development performance: Green dynamic capabilities, green transformational leadership, and green creativity. J. Bus. Ethics 2013, 116, 107–119. [Google Scholar] [CrossRef]

- Lin, R.J.; Tan, K.H.; Geng, Y. Market demand, green product innovation, and firm performance: Evidence from Vietnam motorcycle industry. J. Clean. Prod. 2013, 40, 101–107. [Google Scholar] [CrossRef]

- Peng, Y.S.; Lin, S.S. Local responsiveness pressure, subsidiary resources, green management adoption and subsidiary’s performance: Evidence from Taiwanese manufactures. J. Bus. Ethics 2008, 79, 199–212. [Google Scholar] [CrossRef]

- Rekik, L.; Bergeron, F. Green Practice Motivators and Performance in SMEs: A Qualitative Comparative Analysis. J. Small Bus. Strategy 2017, 27, 1–17. [Google Scholar]

- Baker, W.E.; Sinkula, J.M. Environmental marketing strategy and firm performance: Effects on new product performance and market share. J. Acad. Mark. Sci. 2005, 33, 461–475. [Google Scholar] [CrossRef]

- Fraj-Andrés, E.; Martinez-Salinas, E.; Matute-Vallejo, J. A multidimensional approach to the influence of environmental marketing and orientation on the firm’s organizational performance. J. Bus. Ethics 2009, 88, 263–286. [Google Scholar] [CrossRef]

- Walsh, G.; Beatty, S.E. Customer-based corporate reputation of a service firm: Scale development and validation. J. Acad. Mark. Sci. 2007, 35, 127–143. [Google Scholar] [CrossRef]

- Testa, F.; Iraldo, F.; Frey, M. The effect of environmental regulation on firms’ competitive performance: The case of the building & construction sector in some EU regions. J. Environ. Manag. 2011, 92, 2136–2144. [Google Scholar] [CrossRef]

- Ghisetti, C.; Rennings, K. Environmental innovations and profitability: How does it pay to be green? An empirical analysis on the German innovation survey. J. Clean. Prod. 2014, 75, 106–117. [Google Scholar] [CrossRef]

- Berger, A.N. “Distribution-free” estimates of efficiency in the US banking industry and tests of the standard distributional assumptions. J. Prod. Anal. 1993, 4, 261–292. [Google Scholar] [CrossRef]

- Schmidt, P.; Sickles, R.C. Production frontiers and panel data. J. Bus. Econ. Stat. 1984, 2, 367–374. [Google Scholar] [CrossRef]

- Aigner, D.; Lovell, C.K.; Schmidt, P. Formulation and estimation of stochastic frontier production function models. J. Econom. 1977, 6, 21–37. [Google Scholar] [CrossRef]

- Banker, R.D.; Charnes, A.; Cooper, W.W. Some models for estimating technical and scale inefficiencies in data envelopment analysis. Manag. Sci. 1984, 30, 1078–1092. [Google Scholar] [CrossRef]

- Charnes, A.; Cooper, W.W.; Rhodes, E. Measuring the efficiency of decision making units. Eur. J. Oper. Res. 1978, 2, 429–444. [Google Scholar] [CrossRef]

- Tone, K. A slacks-based measure of efficiency in data envelopment analysis. Eur. J. Oper. Res. 2001, 130, 498–509. [Google Scholar] [CrossRef]

- Honma, S.; Hu, J.L. Analyzing Japanese hotel efficiency. Tour. Hosp. Res. 2012, 12, 155–167. [Google Scholar] [CrossRef]

- Huang, Y.; Mesak, H.I.; Hsu, M.K.; Qu, H. Dynamic efficiency assessment of the Chinese hotel industry. J. Bus. Res. 2012, 65, 59–67. [Google Scholar] [CrossRef]

- Simar, L.; Wilson, P.W. Statistical inference in nonparametric frontier models: The state of the art. J. Prod. Anal. 2000, 13, 49–78. [Google Scholar] [CrossRef]

- Fernandez, J.E. Ergonomics in the workplace. Facilities 1995, 13, 20–27. [Google Scholar] [CrossRef]

- Shikdar, A.A.; Sawaqed, N.M. Worker productivity, and occupational health and safety issues in selected industries. Comput. Ind. Eng. 2003, 45, 563–572. [Google Scholar] [CrossRef]

- Warrack, B.J.; Sinha, M.N. Integrating safety and quality: Building to achieve excellence in the workplace. Total Qual. Manag. 1999, 10, 779–785. [Google Scholar] [CrossRef]

{kind=link}

| Sources | Method | DMUs | Input Factor | Output Factor |

|---|---|---|---|---|

| Wang et al. (2016) [29] | DEA | 38 Chinese new energy enterprises |

|

|

| Cruz-Cázares et al. (2013) [26] | DEA/Malmquist index | 415 (first stage)/362 (second stage) Spanish manufacturing firms |

|

|

| Guan et al. (2006) [28] | DEA | 182 Chinese industrial innovative firms |

|

|

| Chen and Guan (2012) [25] | DEA | 30 Chinese province-level regions |

|

|

| Zhong et al. (2011) [30] | DEA | 30 Chinese province-level regions |

|

|

| Guan and Chen (2010) [27] | DEA | 26 Chinese province-level regions |

|

|

| Guan and Chen (2012) [11] | DEA | 22 Countries |

|

|

| Hollanders and Celikel-Esser (2007) [10] | DEA | 35 Countries |

|

|

| Factors | Questionnaire in KIS Data | |

|---|---|---|

| Input | R&D employee | The number of regular employee |

| The percentage of the number of R&D employee out of the number of regular employee | ||

| R&D expense | Total innovation cost | |

| Output | Patent application | The number of patent application |

| Innovation sales | Total sales | |

| The percentage of innovative product sales out of total sales | ||

| Environmental | Material and energy reduction | How important is the following objective to perform innovation?—“material and energy cost reduction” |

| Environment improvement | How important is the following objective to perform innovation?—“improvement of harmful influence on environment” | |

| Safety improvement | How important is the following objective to perform innovation?—“improvement of working environment or workplace safety” | |

| Factors | Minimum | Maximum | Average | St.dev | Median |

|---|---|---|---|---|---|

| R&D employee | 0 | 134.4 | 10.30 | 13.20 | 6 |

| R&D expense | 20 | 3845 | 621.74 | 782.79 | 300 |

| Patent application | 1 | 130 | 4.19 | 8.44 | 2 |

| Innovation sales | 0 | 14,000,000 | 1,083,976.10 | 1,803,877.57 | 367,950 |

| Material and energy reduction | 0 | 3 | 2.24 | 0.80 | 2 |

| Environment improvement | 0 | 3 | 2.13 | 0.84 | 2 |

| Safety improvement | 0 | 3 | 2.22 | 0.79 | 2 |

| Industry Type | No. of Firms | Ave. R&D Employee | Ave. R&D Expense | Ave. Patent Application | Ave. Innovation Sales | Ave. Material and Energy Reduction | Ave. Environment Improvement | Ave. Safety Improvement |

|---|---|---|---|---|---|---|---|---|

| Food products | 9 | 11.08 | 566.67 | 2.11 | 623,555.56 | 2.33 | 2.33 | 2.22 |

| Beverages | 1 | 30.00 | 1700.00 | 1.00 | 7,980,000.00 | 2.00 | 1.00 | 2.00 |

| Textiles; except for apparel | 6 | 6.75 | 585.83 | 2.83 | 2,798,538.33 | 1.83 | 1.17 | 1.50 |

| Wearing apparel, clothing accessories and fur articles | 1 | 0.39 | 50.00 | 3.00 | 325,000.00 | 3.00 | 3.00 | 3.00 |

| Tanning and dressing of leather, luggage and footwear | 1 | 0.21 | 20.00 | 2.00 | 162,000.00 | 2.00 | 0.00 | 2.00 |

| Wood and cork; except for furniture | 2 | 2.49 | 109.50 | 4.00 | 112,965.00 | 3.00 | 2.50 | 2.50 |

| Pulp, paper and paper products | 3 | 5.22 | 252.67 | 5.33 | 346,936.67 | 2.00 | 1.67 | 2.00 |

| Printing and reproduction of recorded media | 2 | 16.20 | 400.00 | 3.50 | 2,532,595.00 | 2.00 | 2.00 | 2.00 |

| Chemicals and chemical products; except for pharm aceuticals and medicinal chemicals | 15 | 9.52 | 843.33 | 6.87 | 745,283.67 | 2.20 | 2.20 | 2.27 |

| Pharm aceuticals, medicinal chemicals and botanical products | 7 | 23.03 | 1146.86 | 3.29 | 1,635,902.86 | 2.14 | 2.14 | 1.86 |

| Rubber and plastic products | 58 | 7.72 | 428.45 | 3.16 | 1,362,250.69 | 2.41 | 2.48 | 2.59 |

| Other non-metallic mineral products | 8 | 4.45 | 543.63 | 3.75 | 1,416,505.75 | 2.25 | 1.88 | 1.88 |

| Basic metal products | 7 | 6.35 | 315.57 | 2.00 | 3,164,458.57 | 2.00 | 2.00 | 2.29 |

| Fabricated metal products; except for machinery and furniture | 27 | 7.72 | 3347.07 | 3.74 | 1,953,212.96 | 1.85 | 1.41 | 1.78 |

| Electronic components, computer, radio, television and communication equipment and apparatuses | 45 | 15.61 | 867.60 | 6.31 | 1,091,366.11 | 1.78 | 1.71 | 1.69 |

| Medical, precision and optical instruments, watches and clocks | 38 | 15.02 | 302.37 | 4.13 | 879,981.05 | 2.26 | 2.08 | 2.16 |

| Electrical equipment | 40 | 11.24 | 579.38 | 3.28 | 993,990.88 | 2.18 | 2.08 | 2.25 |

| Other machinery and equipment | 133 | 8.30 | 621.57 | 4.21 | 488,040.50 | 2.50 | 2.42 | 2.47 |

| Motor vehicles, trailers and semitrailers | 28 | 12.92 | 1352.04 | 3.96 | 1,949,646.43 | 2.00 | 1.96 | 2.04 |

| Other transport equipment | 4 | 15.23 | 1102.50 | 12.50 | 2,285,910.00 | 2.00 | 1.75 | 1.75 |

| Furniture | 3 | 5.24 | 608.67 | 6.67 | 650,718.00 | 1.67 | 1.33 | 1.67 |

| Other manufacturing | 3 | 4.60 | 150.00 | 3.00 | 21,503.33 | 2.67 | 2.00 | 2.00 |

| Group | Average Score | ||

|---|---|---|---|

| MERE | ENIM | SAIM | |

| High efficiency | 2.2789 | 2.1837 | 2.3061 |

| Medium efficiency | 2.1905 | 2.0204 | 2.1633 |

| Low efficiency | 2.2249 | 2.1769 | 2.1837 |

| Dependent Variable: Innovation Efficiency | ||

|---|---|---|

| Coefficient | Standard Error | |

| (Intercept) | 0.134 *** | 0.030 |

| MERE | 0.003 | 0.019 |

| ENIM | −0.044 ** | 0.021 |

| SAIM | 0.054 ** | 0.022 |

| Log-sigma | −1.605 *** | 0.034 |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Shin, J.; Kim, C.; Yang, H. The Effect of Sustainability as Innovation Objectives on Innovation Efficiency. Sustainability 2018, 10, 1966. https://doi.org/10.3390/su10061966

Shin J, Kim C, Yang H. The Effect of Sustainability as Innovation Objectives on Innovation Efficiency. Sustainability. 2018; 10(6):1966. https://doi.org/10.3390/su10061966

Chicago/Turabian StyleShin, Jaeho, Changhee Kim, and Hongsuk Yang. 2018. "The Effect of Sustainability as Innovation Objectives on Innovation Efficiency" Sustainability 10, no. 6: 1966. https://doi.org/10.3390/su10061966

APA StyleShin, J., Kim, C., & Yang, H. (2018). The Effect of Sustainability as Innovation Objectives on Innovation Efficiency. Sustainability, 10(6), 1966. https://doi.org/10.3390/su10061966