1. Introduction

The increasing internationalization of emerging firms is receiving notable attention in the literature of International business [

1,

2,

3,

4,

5,

6]. Studies reveal that internationalization takes place with an overall increased investment pattern by firms because of growing economic activities. This growth in economic activities, along with pro-market reforms, boost market activities and make this process successful [

7]. This internationalization process moves from the traditional perspective of internationalization, which is to get international involvement through exporting to a more growth-enhancing internationalization process as firms start their international involvement through outward foreign investment. Chou et al. [

8] emphasize that capital flow supports the industrial competitiveness, competitive edge, and generate technological spill overs for domestic firms. This internationalization process enables firms to lower their dependency on domestic resources and increase their international exposure and reliance on international resources to achieve the sustainable growth. Yue et al. [

9] find after applying the OLS (Ordinary Least Squares regression) estimation technique that China maintained stable and sustained economic growth in the last three decades. This rapid economic growth benefitted the advancement of many key macroeconomic factors including inward and outward Foreign Direct Investment (FDI). Since the implementation of successful liberalization reforms of early 1990s, the country has witnessed the huge capital inflows and outflows of FDI and it became one of the main beneficiaries of the capital flow among the emerging countries.

With a rapidly growing economy, the inefficiency regarding resource allocation and the rising environmental degradation in terms of air pollution and high energy consumption indicated by Yue et al. [

9] have provoked the Chinese government to transform their economic system and allow their domestic firms to enter the global business stream by introducing institutional reforms. These domestic financial reforms enable domestic firms to learn international business strategies to increase their global share and domestically implement this learned environmental friendly business model to achieve long-term sustainable economic growth. After applying the OLS panel technique, Wang and Liu [

10] identify that the level of innovation, trade openness, human capital, financial development, and the technological gap can be regarded as the equivalent threshold effects of the sustainable internationalization process. Studies on the internationalization process of Chinese firms indicate that firm-specific advantages like ownership advantages, market-motives, resource-seeking motives, and diversifying motives driving the internationalization process of the country [

11,

12]. These reasons can be realized when there exists financial development, credit availability, and foreign currency regulations.

Lenzo et al. [

13] identify that for firms, the key thing is to improve their sustainability performance and for this, they need supported financial settings, where they can have access to finance and they can make investments easily, so they can increase their resources and enhance their global and domestic market shares. Desbordes and Wei [

14] highlight the importance of financial development in the shape of positive effect on expansion and greenfield of a financial system which stimulates the significant rise in foreign direct investment. In the 1990s, the implementation of financial liberalization reforms in many countries, eliminating the former policy limitations regarding the credit provision and foreign currency regulation enabled firms to make the overseas investment. Chinese firms also followed the same path [

11,

15,

16]. The increase in current outward FDI from Chinese firms appeared to follow the pattern of global financial markets in terms of easy credit provisions and liberalization of domestic financial market [

17]. Yet, the role of financial institutions is understudied in inducing the OFDI of emerging firms despite the magnificent work of Buckley et al. [

18] which highlighted the existence of imperfect financial markets in emerging economies. The work of Buckley et al. [

18], which highlights the issue of the financial constraints faced by emerging transnational firms, and the work of Laeven [

19], which highlights the importance of domestic financial reforms to improve financial availability, has given rise to the following empirical questions: how do institutional factors, such as the increased availability of finance and cross listing introduced under the domestic financial reforms of the 1990s and 2000s impact on the outward foreign investments of Chinese firms? How do these institutional reforms play a pivotal role in boosting the internationalization process in China, given that their importance was highlighted by the study of Saeed and Athreye [

17]? How do increased financial availability and cross listing enhance the internal net worth of these non-financial firms, since Fisman and Khanna [

20] and Laeven [

19] identify the importance of internal net worth when making investment decisions, so they can avoid the financial constraints they face, and make foreign investments? These are the key questions addressed in this study. To answer these questions, this empirical study uses the firm-specific data extracted from the renowned ORBIS database. Based on the sample consisting of 210 non-financial Chinese firms for the period of 2005–2015, this study will find out whether the introduction of institutional factors such as cross listing and the increased financial availability under the domestic financial reforms did initiate the internationalization process and induce outward foreign investment from China or not, and whether state-owned firms and member firms of major Business Houses (BH). Business houses are large groups which combine different independent companies containing the joint control and ownership and BH have gained more in terms of financial support through the increased financial availability than the private and stand-alone firms, or whether firms’ affiliation does not matter.

Studying the role of domestic financial reforms as the causation of early internationalization process of Chinese firms, this study would contribute in the existing literature by demonstrating that institutional factors in terms of easy financial availability could possibly initiate the internationalization process. Due to the elimination of erstwhile financial constraints domestically and an increase in overseas investment prospects because of global financial reforms, the study emphasizes that institutional factors boost-up the economic environment. This has also enabled the Chinese firms to make investment exuberantly. Nayyar [

21] also identifies that global capital markets are an important and independent source for supporting the foreign investments of many emerging transnational firms, along with domestic capital markets. Hence, allowing domestic firms to list internationally enables them to have access to international resources. As Desbordes and Wei [

14], Pelzman [

22], and Rugman and Li [

23] explain, Chinese firms—regardless of successful internal reforms—have failed to induce innovations in production, such as switching from cheap, labor-based production to an innovation and technology based production system, and prefer merger-acquisitions as a means of acquiring the required R&D. Therefore, this study also presumes that even if they are part of a successful internationalization process, some Chinese firms will fail to sustain their growth or grow further in the future.

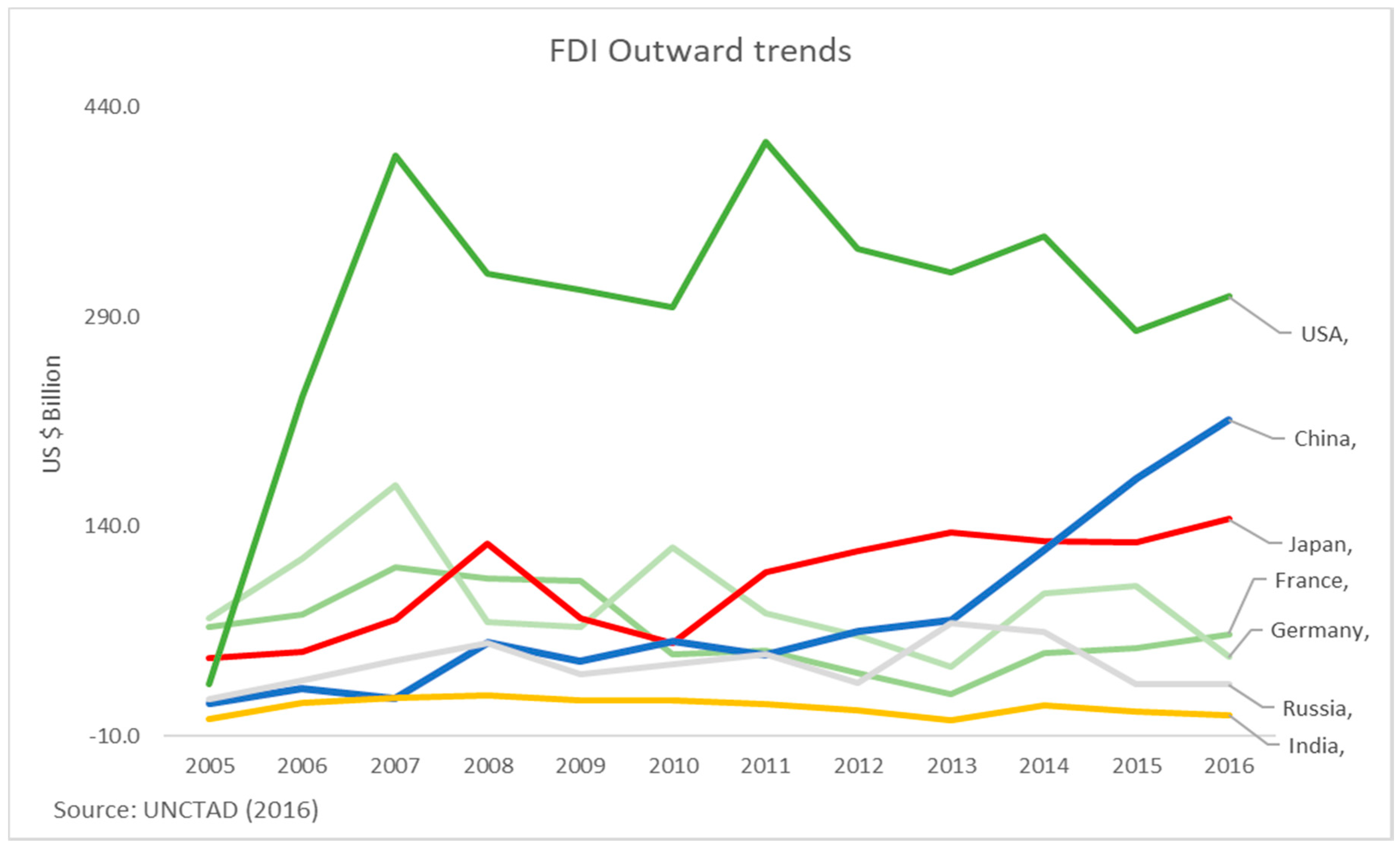

Figure 1 shows the outward investment trends of China and other major economies over time. The outward investment of China is increasing over time while other major economies, such as USA, Germany, Japan, France, Russia, and India, are facing much fluctuation in their outward foreign direct investments. This indicates the progress of Chinese internationalization process. Even after the occurrence of the Global Financial Crisis of 2008–2009, the OFDI of all these major economies deteriorated but the Chinese OFDI sustained the pressure of the Global Financial Crisis as well. This indicates the sustainability of Chinese internationalization process. It is evident that Chinese firms already converted their internationalization process into a source of competitive benefit before the emergence of a credit crunch situation due to the arrival of the global financial crisis of 2008–2009 because these are less demand sensitive. Hence, this trend of Chinese outward foreign direct investment indicates the sustainable economic growth pattern of China as it is withstanding the Global Financial Crisis and sustaining the global pressure successfully. As Chinese firms are still making huge outward foreign investments while others are suffering, this phenomenon needs explanation. While other major economies were exposed to the Global Financial Crisis of 2008–2009 and face much greater fluctuations in their OFDI after the crisis because of increased financial constraint, the Chinese OFDI is showing resistance to global economic downfall and making sufficient progress.

The paper’s structure is as follows.

Section 2 discusses the theories related to the internationalization process and institutional factors based on the research questions. This is followed by an empirical strategy and hypothesis development

Section 3.

Section 4 describes the data.

Section 5 discusses the empirical findings and the last section presents the conclusion.

2. Financial Availability and Internationalization

Studies by Desbordes and Wei [

14], Oláh et al. [

24], Sadaf et al. [

25], Forssbæck and Oxelheim [

26], Yang et al. [

5], and Yoo and Reimann [

6] explain the reason for internationalization in terms of outward foreign investment from the country by focusing on the real determinants of the international activities of firms. Athreye and Godley [

27] and Desbordes and Wei [

14] identify that without real advantages, such as economic prosperity and economic development, internationalization cannot be successful. The outward investment activities must possess these real advantages to sustain the global pressure [

28]. This aspect identifies the starting of the virtuous circle when the outward foreign investment increases the competitiveness and generates real advantages which inspires more foreign investment activities, but, what initiates the virtuous circle stays unidentified. Freeman [

29] argues that determining factors of investment policy can be complexed and evolve over time and these can be conflicted as well. The emphasis on this aspect of outward foreign investment within the internationalization literature has covered the probable impact of financial availability and the financing cost on the propensity of the firms to start and maintain the outward foreign investment.

The internationalization process, especially through cooperative strategies like alliances or networks [

30,

31], creates profitable opportunities for the firms, but to enter into the international process by making outward foreign investment, firms need optimal financing and healthy coordination across the boundaries. Eftekhari and Bogers [

32] emphasize that an open environment has a direct influence on the survival of the firms. Firms need favorable government regulations which stimulate their investment activities by supporting them. In this regard, in the early 1990s when Chinese firms made the first largest outward investment, China’s domestic financial reforms were mainly focusing on financial availability and providing a supportive environment for profitable foreign investment. These domestic financial reforms became beneficial for the firms in terms of financial availability but state-owned enterprises get more benefits [

16]. Along with this, Chinese firms started cross-listing to experience global exposure and finance their international investment activities [

18,

21]. Chinese firms make their international investment portfolio to avoid political and sovereign risk. Despite its importance and these findings, there exists no exclusive study to explore the dynamics of financial availability and its impact on internal net worth to induce the internationalization process of emerging transnational firms, though different studies focus on financial liberalization and its impact on financial constraints and efficiency of investment allocation [

19,

33]. Generally, the determining financial factors of corporate investment activities are studied either using the recently established Euler model [

34] or the Jorgenson neoclassic model (1963).

The Jorgenson model is a modified form of the neo-classical production model which was established to explore the relationship of the capital–labor ratio in terms of input prices and investment rate. Yoshikawa [

35] states that the Jorgenson model is frequently used to identify the factors of internationalization, and the key factors were the output level in the host country (consistent with Dunning [

36]) and the external cost of capital. But, this model has many several shortcomings and is not applicable when a foreign investment function contains a downward demand curve slope and when a production function does not yield constant returns [

37,

38]. In terms of Western conglomerates, the Jorgenson model does not consider credit access an issue due to its assumption about the perfect capital market, but, in terms of emerging economies, this assumption of easy credit access cannot be justified. Because credit constraint in terms of high interest rate and lower credit supply is a key issue for the conglomerates of emerging markets in foreign as well as domestic financial markets, these institutional voids can halt or slow down the process of investment expansion [

18,

19,

39]. So, to explain the behavior of emerging multinational enterprises, an alternative conceptual approach is required.

The alternative to external finance is the ability to finance through internal resources [

40,

41]. If the accessibility of internal funds increases for any reason, it will expand the ability of firms to increase their investment [

42]. This effect has no impact on investment in Jorgenson’s model as it does not take place via impact on profitability or demand, but operating in an imperfect capital market, a firm can get huge boost in terms of making investment decisions. This is principally based on the internal capital availability because external financing is high in this kind of financial and economic system. Empirically, investment models which contain various variable to measure the investment–cash flow sensitivity and substitute it as a proxy for internal funds, are highly criticized in the studies of Kaplan and Zingales [

43] and Povel and Raith [

44], thus allow us to use it for financial constraints. Empirically, the Euler model is an improved method of Jorgenson’s model. Particularly, when firms have internal capital resources it means they have high internal net worth, so the Euler equation holds over the period of time. Oppositely, if firms’ internal capital declines, investment declines too, as it depends on firms’ wealth by holding other investment opportunities constant. Thus, the Euler model of investment financing is also relevant to outward foreign investment. So, these arguments about the importance and salience of internal finance in financial constrained situations can apply to outward foreign investment. Multinational enterprises do face high financing cost when they raise their transnational capital for foreign activities [

45]. The possible reasons could be asymmetry of information, the liability of origin, political risk, corruption etc. [

39,

46]. Hence, the only economical way left to finance these activities is through their internal capital [

40,

41].

3. Theoretical Background and Empirical Approach

Financial availability plays a pivotal role in the outward foreign investment of firms of emerging markets and which, in return, boost the growth of firms. Hernández and Nieto [

47] show that the simultaneous combination of outward and inward operations exerts a positive impact on the growth of firms. Alvarez and López [

48] identify that the level of international activities of those firms which are mainly reliant on external finance is more pronouncedly affected by financial development. Forssbæck and Oxelheim [

26] demonstrate the strong positive association between the cost of equity and foreign investment using a Probit regression technique, while the insignificant impact of cost of debt was realized. De Santis et al. [

49] and Klein et al. [

50] find using Fixed effect and Logit regression techniques, respectively, show that both aggregate foreign investment and firm level investment are determined by stock market valuations. Aguiar and Gopinath [

51] discuss that in terms of acquisition, liquidity plays a key role in determining the intensity of foreign investment of firms.

In the early 1990s, many emerging economies, including China, applied domestic financial reforms, intending to raise the influence of market forces to determine the credit supply and the interest rates. The study of Galindo et al. [

33] finds that financial liberalization strengthens the efficiency of investment allocation after applying the generalized method of moments (GMM) and other panel estimation techniques. These domestic financial reforms consisted of certain actions to improve and expand the domestic financial markets [

17]. These reforms included the development of the financial markets to decrease the external financing cost, improving the security of financial systems, improving the screening skills of commercial banks, and removing the barriers to access to the banking system through an easy entrance to encourage bigger penetration to the financial system of the country. Laeven [

19], using a GMM dynamic panel estimation technique, identifies that the key factors of these financial reforms in terms of removing the credit ceilings, lowering the administrative controls over interest rates, and reducing credit programmes. Correspondingly, another important measure was the deregulation of transactions denominated in foreign currency and for investment purposes, allowing local firms to bring in and take out foreign currency easily from their country. These institutional factors improved the credit supply to domestic firms by overcoming the domestic institutional voids and allowing them to make an outward foreign investment [

17,

18,

46,

52,

53].

In financially constrained economies [

3,

52] a shadow cost trade-off exists among the external finance and internal capital which varies across the firms based on the differences in costs and on the comparative nature of asymmetry information. Hence, in the same economy, small entrepreneurial firms may be more credit constrained than the business groups. So, these differences describe the heterogeneity among the firms in investment activities. Studies like Correa [

54] and Gilchrist and Himmelberg [

55], and Love [

56] indicate that if market frictions exist, then the firms mainly depend on their internal cash reserves as an alternative to external financing to avoid the shadow cost of capital [

19,

20,

40,

41].

3.1. Impact of Domestic Financial Reforms on the Internationalization Process

As domestic financial reforms were intended to encourage the flow of capital and improve the efficiency of a capital market, and hence remove the financial constraints on firms’ investments, their outcome was most probably to decrease the firms’ external financing cost and to increase credit flow to the firms. Thus, the shadow cost of capital after the implementation of successful domestic financial reforms is expected to become zero, while in the period before reforms, firms must face the shadow cost of capital because of the shortage of capital. However, the shadow capital cost could not be lower than the risk-free rate or actually be zero, but in a controlled financial access, this cost increases. Empirical research focuses to explain whether these financial reforms accomplished their objectives in emerging economies [

17,

18,

19,

57].

In this study, we study two facets of financial domestic reforms related to the investing behavior of Chinese firms, namely improved supply of credit due to improvements in domestic lending, and because of foreign currency deregulation, e.g., by allowing the cross listing. Also, the study assumes that the desired results of domestic financial reforms are not realized immediately, but take time. So, we expect that financial constraint declines with the progress of domestic financial reform, and/or is mitigated through cross listing and borrowing through global financial markets. Our alternative hypotheses to the null hypothesis are:

Hypothesis 1 (H1). Domestic financial reforms have reduced the credit constraints on firms’ foreign investments.

Hypothesis 2 (H2). Cross listing has decreased the financial constraints for firms’ outward foreign investments.

The null hypotheses of both H1 and H2 are that these reforms i.e., domestic financial reforms and cross-listing do not reduce the financial constraints for the firms’ foreign investment.

3.2. Impact of Firms’ Affiliation on Financial Constraint and Foreign Investment

Generally, firms of emerging markets are operating in a situation where financial markets contain institutional voids. To stay in the business environment and to sustain the pressure, firms frequently practice the strategy of being part of any business group (BG). These business groups are the joint product of many or a few autonomous firms from different industries and they stay allied either informally or formally, but generally through those groups that reorganize and reallocate the resources among the specific group members. Empirical research on business groups reveals their role in terms of sharing risk between group members [

58], aiding the members in terms of easy access to the external financing [

59], and combining and allocating the resources between their members [

60]. Our hypothesis for this purpose will be:

Hypothesis 3 (H3). Business group affiliation decreases the financial constraints for firms’ foreign investments.

Getting into state-ownership firm affiliation by firms of numerous emerging economies is an alternative strategy to overcome the credit constraints for making investments. Generally, state-owned enterprises (SOE) are considered to have lenient budget limits since the main function of firms is not the maximization of profits, instead supporting the strategic investing goals set in industrial policies [

61]. Desbordes and Wei [

14] and Bai et al. [

62] claim that government has incentives in terms of market share and getting financial support from these enterprises to keep them alive via support through easy credit supply as this financial aid plays a crucial role in smooth operation and progress of these firms. Hence, market fluctuations that create credit constraints do not prevent these firms from making investments, and studies of Poncet et al. [

63] and Cull et al. [

64] confirm that the financing cost is significantly lower for SOEs compared to stand-alone firms. Athreye and Kapur [

11] identify that credit constraint is alleviated because of inside capital markets for SOEs. We assume similar impact for transnational firms and the hypothesis for this purpose will be:

Hypothesis 4 (H4). State-ownership decreases the financial constraints for firms’ foreign investments.

The null hypotheses of both H3 and H4 are that these firms’ affiliations i.e., Business Group and State-owned affiliations do not reduce the financial constraints for the firms’ foreign investment, respectively.

3.3. Empirical Model

Studies follow the panel estimation approaches of Ratti et al. [

65] and Laeven [

19], as they use long-run investing decisions constructed on shadow financing costs in their models, and model foreign outward investment as a direct function of the vector form of firm-specific factors. Further, it is obvious that the current investment decision is based on previous period investment decision, so the model considers this characteristic too by adding the lag-dependent variable. The variable CF is the cash flow from operations, calculated as the income from operation plus current depreciation of that specific year. A firm is classified as a financially constrained firm if its access to external finance is limited and is required to mostly depend on its internal capital (cash flow for operation). Hence, the study uses the cash flow-investment sensitivity to measure the financial constraint following the work of Meyer et al. [

66]. Based on these assumptions, the empirical model has the following standard specification:

where

Ii,t is firm investment,

CF measured as internal capital at the beginning of t period,

SOF and

BG are dummy variables representing the state-ownership and business group affiliation, respectively.

YSR is years since reforms Poncet et al. [

63],

CLIST shows whether a firm is listed internationally or not,

Di,t-1 is indicating the lagged value of total debt,

Si,t-1 is indicating lagged value of total sale. Capital stock (K) is used to scale all financial variables of that specific period.

As recognized earlier, international activity offers both profitable opportunities and risks that include political risk and exchange rate risk. Involvement in global activities, nevertheless, is tough since domestic investors must get information and make predictions about financial and economic conditions of international firms, and Bodnar and Weintrop [

67] claim that firms face higher credit constraints for their international investment activities than their domestic investment activities. Thus, our focus is on foreign investment and we use foreign investment in the model instead of total investment and predict that the shadow cost of financing is possibly high for foreign investment. Thus, the modified form of Equation (1) for foreign investment is as follows:

where

If is a foreign investment.

Idt-1, is 1-year lagged domestic investment (instead of using total investment because latter includes the foreign investment as well).

A generalized method of moments (GMM) is more suitable as the model (2) is dynamic in nature by containing the auto-regressive process (existence of lag-dependent variable on right hand side of the model) and possibly contains the problem of heteroskedasticity (due to a large number of samples) and endogeneity (due to existence of reverse causality between dependent and independent variables), as the literature indicates that foreign investment also determines cash flow. The study uses lagged foreign and domestic investments as instruments along others in the estimation (maximum up to 3 lags) which, correspondingly, improves the model’s estimates [

68].

4. Data and Variables Measurement

4.1. Sample Selection and Data Source

The data is taken from the ORBIS database, which was given by BvD (Bureau van Dijk). The ORBIS database contains a huge magnitude of firm specific data consisting of detailed financial and other firm level information of up to 650,000 firms. Our sample consists of 210 large non-financial Chinese firms possessing foreign subsidiaries. The ORBIS database labels a firm as a large company when its operating revenue is up to US

$40 million or it contains up to 1000 workers. The study uses an unbalanced panel as it partially removes potential survival and selection bias [

69]. The focus of the study is on non-financial listed firms of the period 2005 to 2015 which were involved in initial outward foreign investment from China (

Figure 1). The study includes those firms which have data for at least five years. To tackle the potential errors and outliers in data, following the approach of Ratti et al. [

65], the study removes extreme values of those variables which were greater than their respective means, such as observation greater than CF/K above 0.7, D/K above 10, I/K above 2.5, and S/K above 20. The study also removes observation for sale and capital stock which contains negative values.

4.2. Measurement of Variables

Value of total investment is calculated as an annual change in capital stock value plus annual depreciation value. The annual value of depreciation is measured as the change in the accumulated depreciation of the current and previous year. Value of capital stock (K) is measured as equivalent to the value of current year tangible fixed assets, that consist of the sum of machinery, equipment, plant, land, other tangible assets, property, construction-in-progress, and buildings. Inventories were reported independently, so not considered in the valuation. For the value of the foreign investment (FI), the study used annual financial statements of each foreign subsidiary and combined the values of change in capital stock plus depreciation values of each year to get the value of the foreign investment of each firm. For value of the domestic investment (DI), we subtracted the value of foreign investment from the value of total investment.

To measure the effect of institutional factors under domestic financial reforms, the study considers two components of domestic financial reforms. Firstly, the study use years since reforms (YSR) as the difference between current year and base year in which reforms were introduced to indicate the financial progress of domestic reforms. The study considers the year 1993 as the base year, as in this year, financial reforms were introduced. The study uses the time variant figure to indicate the difference between periods i.e., the base year of reforms and current period, t. To assess the nature of financing from global markets, the study includes the cross-listing variable, (CList), which is binary in nature as it takes value 1 when a firm is listed internationally and 0 otherwise. A firm is affiliated with state-ownership if it contains a proportion of state ownership, and it is affiliated with a business group if it is a part of any bunnies group. State-ownership (SOF) is binary in nature and takes value 1 if the firm contains any proportion of state ownership, otherwise it is 0. Business group (BG) is binary in nature and takes value 1 if a firm is a part of any business group and otherwise takes 0. The affiliation information of firms is retrieved from the annual financial statements of each year. The control variables are Debt (D), lagged (1-year) domestic investment (Idt-1) and Sale (S). Debt (D) is calculated as the value of total i.e., short-term and long-term debt. Sale (S) is calculated as the total value of sales of a firm in a given period.

5. Results

This section discusses the descriptive statistics, correlation matrix, and regression estimation results of model 2, which is measuring the impact of institutional factors on internationalization of emerging transnational firms.

Table 1 presents descriptive statistics, such as the number of observations, means, standard deviations, minimum, and maximum values of variables of interest. Chinese firms are heavily invested domestically (almost 67% of their capital stock) compared to foreign investment (almost 13% of their capital stock). The values of standard deviation are close to the mean values of the respective variables. This indicates that the variables of interest are normal and do not contain potential outliers. The ratio of cash flow to capital stock is almost 50%, this indicates the availability of internal funds to finance these investment activities. Sale to capital stock ratio measures the operational efficiency of firms and indicates that Chinese firms are operationally efficient, as it is 2 times higher than the capital stock, suggesting a huge role in driving the market demand. Debt to capital stock i.e., leverage ratio, is much higher, i.e., 4 times higher, indicating the utilization and reliance of Chinese firms on debt. Almost 29% of the sampled firms are internationally listed. Regarding affiliation to a business group, 21% of Chinese firms are associated, while state ownership is higher, i.e., 27% among sampled firms.

5.1. Correlation Matrix

Table 2 shows the correlation values among the variables of interest. All the values are below the 0.70, so there is no issue of multicollinearity in the model. These correlation values indicate the direction of co-movement and not at a significant level. Lagged foreign investment, lagged domestic investment, and debt show positive correlation with foreign investment, while the remaining variables i.e., cf., total-sale, business-group, state-owned-firms, and clist show negative correlation with foreign investment.

5.2. Financial Availability and Internationalization

Table 3 presents the estimation results of Equation (2). We estimated the model twice, first with all variables and second with only the significant explanatory variables. The 1st column contains the results of all variables, while column 2 contains the regression results of the significant explanatory variables. The results remain consistent in both regressions in terms of significant explanatory variables (column 1 and 2), only their magnitudes changed, indicating the robustness of our results. These results are obtained by using GMM regression. The result indicates that foreign investment depends on foreign investment of the previous year, as the coefficient of λ1 is positive and statistically significant, accepting the presence of the VAR process. This indicates the consistency of the internationalization process. The coefficient λ2 indicates that the impact of cash flow on foreign investment is positively significant, which indicates the dependence of foreign investment on the level of credit availability and demonstrates the credit constrained situation of the firms for whom it is difficult to access external finance (consistent with the findings of Bhaduri [

40] and Ghosh [

70]). Hence, transnational firms mainly depend on their internal net worth to enhance their internationalization.

6. Discussion

Our findings provide strong support for an alternative Hypothesis 1 that states that an increased supply of credit because of domestic financial reforms has reduced the credit constraint on firms’ foreign investment, rejecting the null hypothesis. The coefficient (λ5) of the YSR interactive variable is significantly negative at the 5% level for foreign investment (consistent with studies of Laeven [

19] and Poncet et al. [

63] and Huang [

71]). This also verifies the successful implementation of financial liberalization reforms by China as it was evident from

Figure 1. This successful liberalization reform helped China to sustain the credit crunch pressure created by the Global Financial Crisis of 2008–2009 as the Chinese capital market helped transnational firms to sustain the global economic windfall. The coefficient λ6, the second variable capturing the effect of financial reforms i.e., cross-listing, is negatively insignificant. This rejects the alternative Hypothesis 2 about the positive impact of cross-listing on financial availability and accepts the null hypothesis.

The interactive term between cash flow and business group i.e., λ3, is negative but statistically insignificant which failed to accept the alternative Hypothesis 3 and accepts its null hypothesis. The coefficient λ4, an interactive term of cash flow and state-ownership, is negative and statistically significant which indicates that there is an impact of affiliation to the state-ownership for firms for their foreign investment. This result rejects the null hypothesis and accepts Hypothesis 4. This result is consistent with the Poncet et al. [

63] and Cull, Xu, and Zhu [

64]. This emphasizes the role of firms’ affiliation in terms of getting benefits from the financial liberalization reforms. The magnitude of coefficient λ4 also indicates that the impact of firm affiliation in terms of state ownership on credit constraint further strengthens the financial availability. So, state-owned enterprises have a competitive edge in terms of reduced financial constraint and having access to resources to support their investment activity than the stand-alone firms (referring to the λ2).

The other controlling variables include debt, sales, and lagged domestic investment. The result of sale, i.e., coefficient λ7, has a positive but insignificant impact on foreign investment. Coefficient λ8, measuring the impact of debt, indicates a significant and positive relationship with firms’ outward foreign investment. This indicates the dependence of firms’ foreign investment on debt. This result also has the important implication that Chinese transnational firms possess asset-seeking motives as they mainly depend on debt financing. The impact of lagged domestic, i.e. λ9, is negative but insignificant. The value of the Hansen–Sargan test indicates the acceptance of the null hypothesis. It means that the instruments used are valid. The null of AR (2) was also accepted, which indicated that there exists no serial correlation in error terms. So, the results of the Hansen–Sargan test and AR (2) verify the validity of the estimates. Also, we performed the unit root test to check the robustness of the regression results and the results indicated that there exists no serial correlation as the probability of Wooldridge test is greater than 10%, so we failed to reject the null hypothesis of no autocorrelation. Hence, we received the same results after estimating the model twice, indicating that our results are consistent and robust.

7. Conclusions

The existing literature on the internationalization process of transnational firms of emerging markets has discussed competitive advantages and firm-specific strategies as the driving force of their foreign investment. For sustainable economic growth, firms require competitive advantages, institutional support, and technological innovation in terms of having access to international resources and lowering their dependency on domestic resources. Emerging countries like China can only sustain global pressure and maintain their economic growth if they create a business-friendly environment by supporting domestic firms by implementing successful institutional reforms. This study argues that although firm-specific advantages are essential to continue the internationalization process, other factors (like domestic financial reforms) can be the cause of initiating internationalization in terms of outward foreign investment, which establishes the roadmap for future growth and also helps transnational firms to sustain global pressure. Specifically, this study examines whether institutional factors, in terms of increased financial availability, were a source of initial internationalization for Chinese firms. Thus, firms with specific affiliations were able to get more benefits in terms of financial availability to invest in overseas opportunities as compared to other types of firms. Finally, these reforms work efficiently and drove outward foreign investment and enhance the internationalization process. This study adopted the Euler model of internal financing to explain the determinants of Chinese outward foreign investment in terms of explaining the role of domestic financial reforms in kick-starting foreign investment. This successful internationalization process helped Chinese firms to withstand the Global Financial Crisis of 2008–2009 and maintain their internationalization process with the financial support of their government.

Analyzing the behavior of large 210 Chinese firms, study finds that easing financial availability by introducing domestic financial reforms caused the initial internationalization process by Chinese firms, in terms of increased outward foreign direct investment. The benefits of cross listing are limited. Our study also finds that having being at least partly state-owned reduced the financial constraint to support their foreign investment. Lastly, Chinese firms are more dependent on debt than sale. This indicates the aim of the Chinese government to achieve sustainability through supporting their domestic firms, such that they survive global pressure, and this is what we witnessed by looking at the outward foreign direct investment trend. The key implication of this study that institutional factors, such as increased financial availability, caused a rise in firms’ outward foreign investment from China, while investment of some firms will fail, as most firms, irrespective of their credit ratings, get the benefit of these financial reforms. Good investments are financed along with poor ones, as reforms were general in nature. So, some firms that have internationalized because of increased financial availability will ultimately survive after developing and applying strategic advantages like involvement in merger-acquisition. Another implication of this study is that frontier or young emerging economies can learn from the successful internationalization process of Chinese firms by applying the domestic financial reforms of China to boost their international involvement by eliminating the institutional void. The successful implementation can lead to sustained economic development in their respective countries. Hence, the lesson from this study is that the development of domestic capital markets and the financial system plays a crucial role in achieving sustainable economic growth and it also helps domestic firms to withstand the global pressure. Therefore, future research should try to examine when and how the internationalization process can fail, and which strategies firms should adopt to make their internationalization process successful.

,

,

{kind=link}