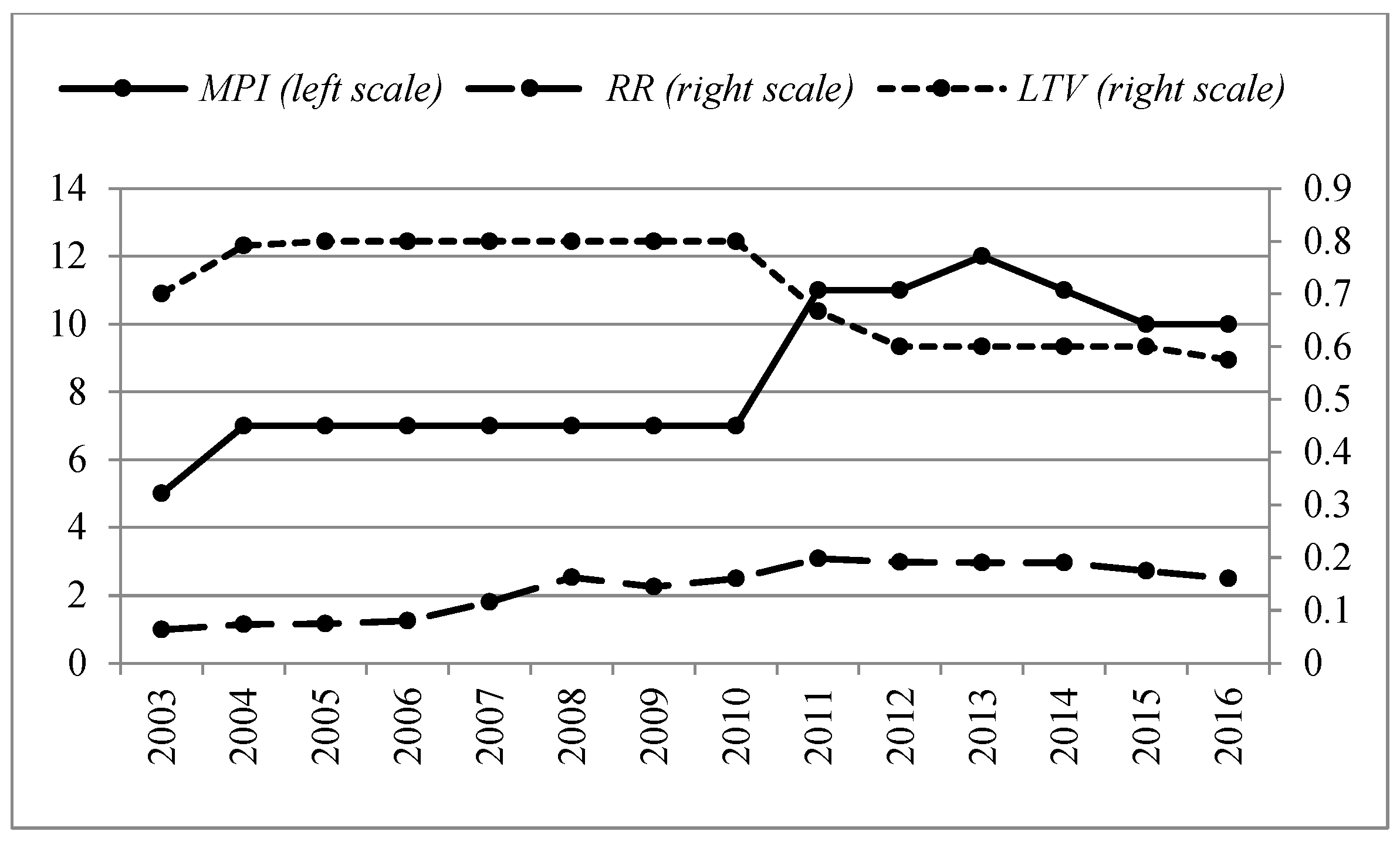

1. Introduction

Macroprudential policies (MPPs) have been placed in an extremely important position by many countries after the global financial crisis of 2008, which was also the starting point for macroprudential supervision in China. An increasing number of macroprudential tools have been introduced to improve countercyclical adjustment and sustainable development in the financial system. The Twelfth Five-Year Plan for the Development and Reform of the Financial Industry puts the establishment and improvement of a MPP framework to the forefront. The report at 19th CPC National Congress proposes to improve the dual-pillar regulation framework of monetary policy and MPP formally. The importance of macroprudential supervision in China is increasingly prominent.

The macroprudential tools are originally aimed to address risks in the bank sector [

1], and the IMF [

2] suggests that a MPP should be extended to the nonbanking financial sector. We focus on the effect of MPPs on bank risk-taking, which is related to the sustainable development of the bank sector and financial system. MPPs can avoid negative externalities that may flow from the financial system to the real economy, including the risk of excessive loans entering a bank’s balance sheets during an economic boom and the risk of providing loans to enterprises with good investment opportunities during a depression. The Countercyclical Capital Buffer (CCB) helps smooth credit supply cycles and is recognized as the most efficient macroprudential tool in Spain [

3]. The dynamic reserve requirement (RR) helps detect credit losses in bank loan portfolios in advance [

4]. The caps on loan-to-value (LTV) can restrain house price growth and bank leverage [

5,

6]. China has implemented MPPs for years and the effectiveness of them is an important research topic for the academic community and policymakers. We attempt to construct a theoretical framework to explain the transmission mechanism of MPPs and provide related empirical evidence. Borio and Zhu [

7] state that the transmission mechanism of monetary policy includes risk-taking channels. Most of the following related studies support that conclusion [

8,

9]. It is believed that changes in policy interest rates affect risk perception and risk tolerance, which are reflected in a risk portfolio. Based on the model proposed by Dell’Ariccia et al. [

10], we focus on an extant work and the interaction between a MPP coordinated with monetary policy and bank risk-taking, and analyze the transmission mechanism of MPPs on bank risk-taking behaviors by adding CCB. CCB and RR affect the willingness of a bank’s lending behavior and LTV restricts borrowers’ access to new property loans [

11], which are related to the balance sheets of commercial banks and thus affect bank risk-taking behaviors. We empirically analyze the effectiveness of three macroprudential tools, i.e., CCB, RR and LTV, including the individual and overall effects of these three tools in reducing bank risk-taking behaviors using the bank-specific data of 231 commercial banks in China. The IMF [

2] proposes that policymakers should use macroprudential tools more actively to understand the signs of late-stage credit cycle dynamics. We therefore are interested in how the credit cycle affect the link between MPPs and bank risk-taking.

The contributions of this paper to the literature on the bank risk-taking channel of MPPs are threefold. First, we provide a further explanation on the bank risk-taking channel of MPPs by establishing a theoretical model, which bridges the gap between conceptual frameworks and empirical evidence on MPPs. Second, we offer some broader reflections on the characteristics of the transmission mechanism of MPPs on bank risk-taking behaviors. We conduct an empirical analysis with a larger commercial bank sample on the effectiveness of MPPs implemented in the past two decades in China. We conclude that MPPs are important elements and policy tools aimed at systemic risk mitigation. We also find that RR is the most efficient macroprudential tool, followed by LTV and CCB. We overcome the challenge of evaluating the effects of MPPs when more than one tool is activated, as the combined effects of three tools are tackled in our estimation. These results help policymakers design coordinated MPPs to stabilize the bank sector and promote the sustainable development of commercial banks. Third, we highlight the role of a credit boom in MPP implementation. Considering the credit cycle in the effect of MPPs on bank risk-taking, we find CCBs are more effective in credit booms than in credit crunch episodes. Thus, commercial banks should accrue more CCBs in credit boom periods than in other periods. Our findings therefore provide certain theoretical and empirical contributions to sustainable development and the stability of the banking sector, thus benefiting the effectiveness and sustainability of MPPs.

The rest of the paper is structured as follows.

Section 2 reviews the literature.

Section 3 presents the theoretical model.

Section 4 describes the data and methodology.

Section 5 shows the empirical results and robustness checks.

Section 6 concludes.

2. Literature Review

Our research relates to two strands of literature. One for the economics of banking, particularly bank risk-taking, and the other for MPPs, especially the transmission mechanism and the effectiveness of MPPs.

There was a burst of literature on bank risk-taking during the post-crisis period as the riskiness of banks from all country groups increased after the global financial crisis of 2008. Regulators attempted to control bank risk-taking behaviors [

12]. Many studies focus on ways to reduce bank risk-taking and guarantee financial stability. Strong supervisory power and discipline can constrain excessive bank risk-taking [

13]. Trade openness and common equity capital help commercial banks smooth out income volatility and decrease overall bank risk [

14,

15]. Bank market power and competitions are associated with the excessive risk appetite of commercial banks, which accounts for fragility [

15,

16]. When market power is transformed to better business models, it will contribute to less overall banking risk and better bank performance [

17]. There are certain papers that investigate the differences in risk-taking behaviors between publicly traded and privately owned banks, and some suggest public banks are likely to exhibit less risk-taking [

18].

To discover a solution to the problem of bank-originated financial instability, many studies research MPPs. The MPP is proposed to mitigate systemic risk, which helps strengthen the resilience of the financial system during economic downturns, reduce build-up of vulnerabilities, and promote the sustainable growth of financial intermediation and financial inclusion [

19]. The central bank is usually in charge with macroprudential supervision [

20]. By adapting the MPP to monetary policy objectives, one can achieve the goal of effectively slowing down procyclicality, lowering both the likelihood and the severity of a crisis originated by the accumulation of bank risk [

21,

22]. The central bank thus can rely on macroprudential supervision and regulation to monitor bank risks [

23]. The MPP is now seen as a possible way to rebalance the misalignment of targets and instruments [

24]. Macroprudential policy action, including CCB, real estate instruments, systemic risk buffer, and other instruments, addressed cyclical risks in the EU in 2017 [

20]. Besides, the MPP can also be used as a policy option to deal with the global financial cycle and the “three dilemmas” of international macroeconomics [

25]. Several papers examine the effectiveness of MMPs. Lim et al. [

26] validate the effectiveness of macroprudential tools in reducing systemic risk using survey data from 49 countries. Olszak et al. [

27] identify the effectiveness of MPP instruments in reducing the procyclicality of loan-loss provision (LLP) using the information of banks from over 65 countries by adopting the two-step GMM method. Macroprudential tools in 19 OECD countries are also assessed to be effective [

28]. Funke et al. [

29] demonstrate that the MPP is a useful addition to the monetary policy using a DSGE model tailored to New Zealand because LTV reduces house prices without derailing monetary policy. Jung et al. [

30] and Alpanda et al. [

31] provide similar conclusions for MPPs in Korea and Canada. However, supervisory monitoring is important for MPP goals, and the effectiveness of macroprudential regulations is challengeable for the revolving door of risk [

32].

Several recent papers on MPPs and bank risk-taking mainly focus on the bank risk-taking channel of the MPP. This paper summarizes a synoptical table containing the main MPPs, previous literature, countries analyzed, and key evidence, which is included in

Table A1 (see

Appendix A). There are certain studies that provide empirical evidence using cross-country data. Claessens et al. [

5] researched MPPs’ effects on 2800 banks in 48 countries from 2000 to 2010. They find that caps on debt-to-income (DTI) and LTV, RR, and dynamic LLP are effective in reducing the bank leverage. Active MPPs help Central and Eastern European countries to preserve the stability of their banking sectors. However, bank profitability and nonperforming loans increase with tighter macroprudential rules [

33,

34]. There is also recent evidence from individual countries. Guidara et al. [

35] find weak evidence that CCBs affect Canadian bank risk-taking, but the appropriateness of both a micro- and macro-prudential “through-the-cycle” approach to capital adequacy explains why Canada performed better during the global financial crisis of 2008. CCB and RR are capable of procyclical mitigation in Indonesia, LTV can reduce credit growth although it cannot mitigate procyclicality [

11,

36]. However, LTV has significant and persistent effects on household debt and real house prices in Korea [

30]. Ma and Yao [

37] investigate the effectiveness of MPPs using the data of 52 Chinese commercial banks and the results show that CCBs help reduce bank risk. Nevertheless, their conclusion is not convincing enough because they ignore the effect of other macroprudential tools such as RR and LTV. In this paper, we attempt to find out whether MPPs reduce bank risk-taking behaviors using a Chinese data set.

Different macroprudential tools have different effects on bank risk-taking [

38], which can be classified into two groups [

1]. The first group includes LTV and DTI, which reduce risk-taking by affecting borrowers. The second group covers the tools of RR, CCB, leverage restrictions (LEV) and LLP, which reduces risk-taking by affecting banks. The CCB can provide banks with greater flexibility to cope with an economic recession [

33], thus helping banks to resist shocks and protect against system vulnerabilities [

39,

40]. Better-capitalized and more liquid banks are less risky [

41]. The LLP helps smooth the credit cycle [

3]. The RR can earlier detect and cover credit losses in bank loan portfolios, creating a buffer in expansion that will alleviate procyclicality and promote the sustainability of the banking system during a recession [

4]. Balla and Mckenna [

42] simulate the dynamic reserve system in the U.S. and the results show that the financial system vulnerability evinced by the global financial crisis of 2008 can be greatly mitigated. The LTV and DTI help to control house price growth, credit growth, and bank leverage [

5,

6]. The LTV is the most effective and least costly tool in Canadian, followed by bank capital regulations [

31]. In our study, we concentrate on whether the effect of macroprudential tools varies from each other.

The effects of MPPs on bank risk-taking are sensitive to the credit cycle. Bank risk-taking behaviors tend to increase in economic downturns and decrease in economic upturns. Most macroprudential actions are stronger in credit booms [

43]. Credit is a leading indicator of the financial crisis and is the best variable to signal the implementation of MPPs [

37]. Monetary expansion will increase the leverage and risk of banks [

44]. As the economy grows, cash flows, incomes and asset prices rise, risk appetite increases, and external funding constraints weaken, which facilitates bank risk-taking behavior [

39]. Dell’ Arriccia et al. [

10] argue that the combination of market competition and credit boom might lead banks to increase profits by easing lending criteria. Dell’ Ariccia et al. [

9] use U.S. data to verify the existence of a risk-taking channel for monetary policy and find that a low interest rate environment significantly increases bank risk-taking behavior. Cerutti et al. [

1] expanded the IMF’s survey to study MPPs in 119 countries during the period of 2000–2013 and found that MPPs did not perform well during the recession. Vandenbussche et al. [

44] investigated the effectiveness of MPPs in Southeastern Europe, and concluded that MPPs help contain credit growth during the boom years, but had no discernible effect during the bust. In our study, we consider whether the negative relationship between MPPs and bank risk-taking is affected by the credit cycle.

According to the above findings, the issue remains open to further theoretical and empirical investigation. Previous studies stress the empirical significance of MPPs’ effect on bank risk-taking, which is seldom explained by theoretical models. The empirical evidence on Chinese commercial banks is limited and the majority of them are drawn from a listed banks sample, which cannot reflect the whole banking sector. Many papers study the role of individual macroprudential tools in bank risk-taking behaviors by setting one macroprudential tool as the explanatory variable in the regression model, which ignores the combined effects of multiple MPPs implemented simultaneously in most cases. We consider the combined effects in this paper and also estimate the cross-effect of the credit cycle and CCB to evaluate whether the central bank implements MPPs properly.

3. Theoretical Analysis

3.1. Assumption and Model

Dell’Ariccia et al. [

10] establish a theoretical model to analyze the impact of monetary policy on bank risk-taking. Jiang and Chen [

45] modify the second hypothesis and propose that monetary policy affects the bank’s liability cost through interest and deposit rates. Based on Jiang and Chen [

45], we add the CCB in the model to research the effect of MPPs on bank risk-taking.

Suppose that the bank faces a loan demand function with a negative slope, where is the loan interest rate. The bank supervises the loan portfolio with the degree of effort q to increase the probability of repayment. A greater q indicates that a higher probability that the bank will recover the loan, and a smaller bank risk-taking. The bank needs to pay for the supervision behavior, where the supervision cost is assumed as per unit lent. Bank assets are financed with bank capital (or equity) and deposit. Thus, we assume that the portion of capital is and the deposit is . Considering China has an invisible deposit insurance system before implementing the deposit insurance, the deposit rate equals the policy rate, = , which means the depositor does not require risk compensation. Assuming the portion of capital is , the loan driven by the unit capital is, the deposit is , where is the reserve requirement, and the loan is , the deposit reserve is . Therefore, the cost of unit capital is , the yield requirement , is an equity premium as a spread over the risk-free rate.

When we do not consider MPPs, the bank’s expected profit is as follows:

When we consider MPPs, the bank’s expected profit is as follows:

where

is the CCB.

3.2. Solution and Analysis

The decision of the bank is divided into two stages. In stage 1, the bank chooses the interest rate charge on loans, . In stage 2, the bank chooses how to monitor their portfolio, .

According to the above results, we consider the effect of the policy rate

on the bank risk-taking.

The first term, , reflects the pass-through of the policy rate on the loan rate and increases monitoring incentives, which implies that the policy rate influences bank risk-taking by influencing the loan rate. Moreover, as and , we have . So, has a positive effect on , which means an increase of will increase the monitoring incentives and decrease bank risk-taking. The second term, , is the risk-shifting effect, decreasing monitoring incentives. , so an increase of will decrease monitoring incentives and increase bank risk-taking.

Similarly, we consider the effect of RR, represented by

, on bank risk-taking.

The first term, , implies that the RR influence bank risk-taking by influencing the loan rate. The second term, , implies that has a negative effect on , which means an increase of RR will decrease monitoring incentives and increase bank risk-taking.

Specially, we consider the effect of CCB, represented by

, on bank risk-taking.

The first term, , implies that the CCB influence bank risk-taking by influencing the loan rate. The second term, , implies that has a positive effect on , which means an increase of the CCB will increase monitoring incentives and decrease bank risk-taking.

From above theoretical analysis, the policy rate, RR and CCB have effects on bank risk-taking, but the mechanism still needs to be verified by empirical evidence. Besides, there are some other macroprudential tools, such as dynamic LLP and LTV, that should be considered.

{kind=link}