Perspectives of Private Forest Owners toward Investment in Forest Carbon Offset Projects: A Case of Geumsan-Gun, South Korea

Abstract

:1. Introduction

1.1. Research Background

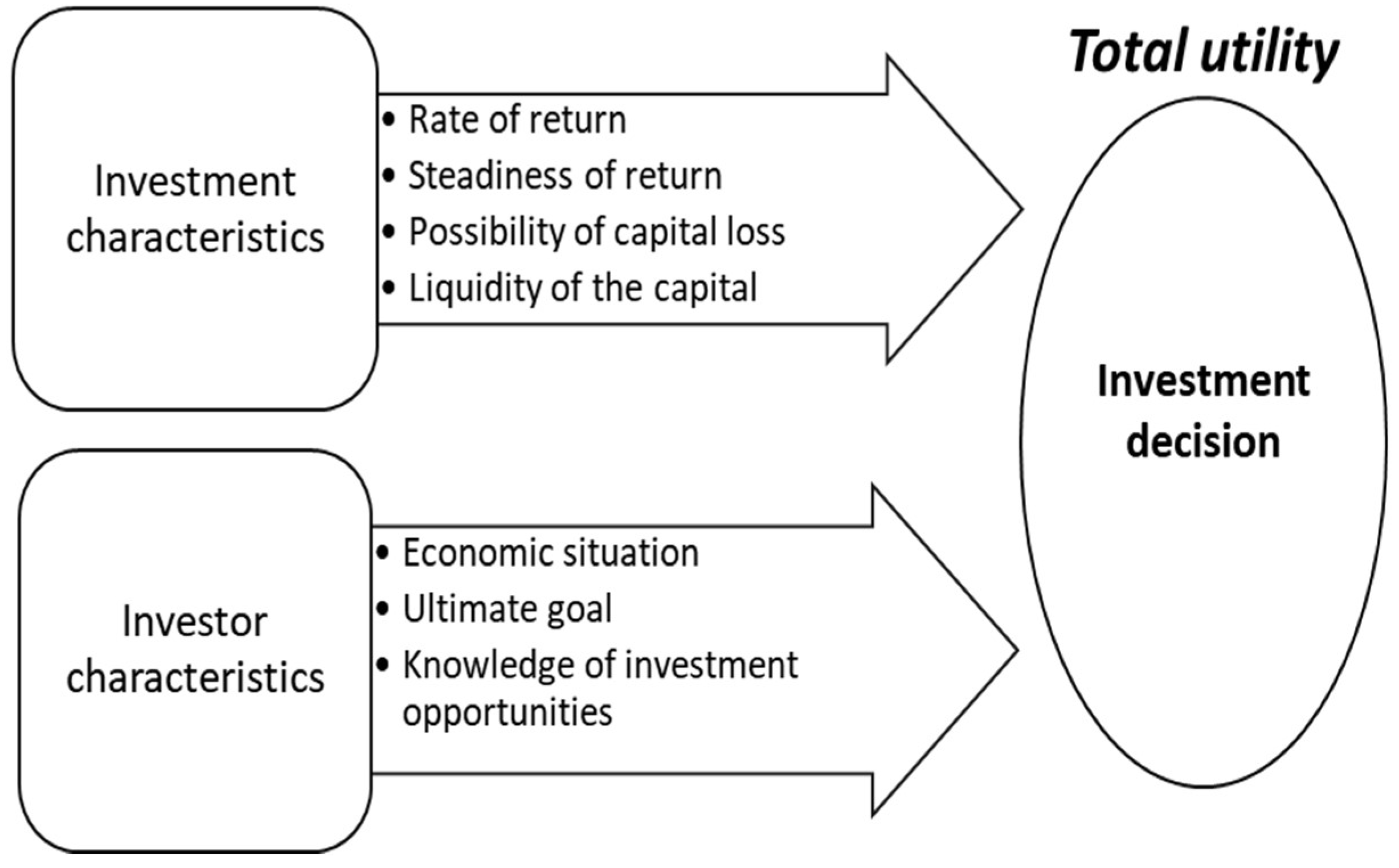

1.2. Theory of Forest Investment

1.3. Literature Review

1.4. Rationale

2. Materials and Methods

2.1. Site Selection and Survey Development

2.2. Variable Description

2.3. Empirical Model

2.4. Impact of an FMC on Willingness to Invest in FCO

3. Results

3.1. Survey Result

3.2. Sample Description

3.3. Logistic Regression Models

3.4. Impact of Forest Management Contract on Willingness to Invest in an FCO Project

4. Discussion

4.1. Model 1 Determinants of Forest Owners’ Willingness to Invest in FCO Projects

4.2. Model 2 Determinants of Forest Owners’ Willingness to Invest in FCO Projects

4.3. Role of Forest Management Contract for Private Forest Owners

5. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Korea Forest Service. Statistical Yearbook of Forestry 2018; Korea Forest Service: Daejeon, Korea, 2018.

- United Nations Framework Convention on Climate Change (UNFCCC). Kyoto Protocol to United Nations Framework Convention for Climate Change; UNFCCC: New York, NY, USA, 1998. [Google Scholar]

- Han, K.; Youn, Y.-C. The feasibility of carbon incentives to private forest management in Korea. Clim. Chang. 2009, 94, 157–168. [Google Scholar] [CrossRef]

- Chun, J.-N.; Youn, Y.-C.; Cha, J. Development of Korean protocol for forest carbon offset project in forest management sector. J. Environ. Policy Admin. 2012, 20, 57–87. [Google Scholar] [CrossRef]

- Korea Forest Service. Forest Carbon Registry. Available online: http://carbonregistry.forest.go.kr (accessed on 10 April 2017).

- Jang, W.; Jang, C. The Measures Revitalizing Private Forest Cooperative Management; Korea Rural Economic Institute: Seoul, Korea, 1999; Research Paper R396. [Google Scholar]

- Lee, S.-H. Study on the Revitalization of the Surrogate Management for Private Forests; Hankyong National University: Anseong, Korea, 2013. [Google Scholar]

- Shin, S.-H. A Study on the Proxy Management System on the Private Forest; Chonnam National University: Gwangju, Korea, 2005. [Google Scholar]

- Jang, I.-H. A Study on the Promotion Plan of Forestry Cooperatives in Korea; Kyungwon University: Seongnam, Korea, 2012. [Google Scholar]

- Romm, J.; Tuazon, R.; Washburn, C. Relating forestry investment to the characteristics of nonindustrial private forestland owners in northern california. For. Sci. 1987, 33, 197–209. [Google Scholar]

- Seo, B.S.; Lee, S.H.; Kang, H.M. A study on the management situation of private forest belonged to non-resident owners. Korean J. For. Econ. 1999, 7, 19–31. [Google Scholar]

- Kim, H.-S.; Park, S.-I.; Lee, S.-H. An attitude of forest owners and importance-performance analysis for management-scale improvement on private forests. J. Agric. Life Sci. 2015, 49, 57–63. [Google Scholar] [CrossRef]

- McMahon, R.O. Private Nonindustrial Ownership of Forest Land: An Economic Theory of Owner and Management Intensity; Yale University: New Haven, CT, USA, 1964. [Google Scholar]

- Kim, N.G. Study on Landowner’s Perception of Forest Investment and Incentive Policies for Private Forest Investment; Seoul National University: Seoul, Korea, 1992. [Google Scholar]

- Seo, Y.W. Analysis of Determinants Affecting Investment of Private Forest Owners with Government Support Programs; Kangwon National University: Chuncheon, Korea, 2001. [Google Scholar]

- Kim, E.-G.; Kim, D.-H.; Kim, H.-G. The analysis of the actual condition of planting investment of private forest owners. Korean J. For. Econ. 2005, 13, 47–55. [Google Scholar]

- Binkley, C.S. Timber Supply from Private Nonindustrial Forests: A Microeconomic Analysis of Landowner Behavior; Yale University, School of Forestry and Environmental Studies: New Haven, CT, USA, 1981. [Google Scholar]

- Boyd, R. Government support of nonindustrial production: The case of private forests. South. Econ. J. 1984, 51, 89–107. [Google Scholar] [CrossRef]

- Conway, M.C.; Amacher, G.S.; Sullivan, J.; Wear, D. Decisions nonindustrial forest landowners make: An empirical examination. J. For. Econ. 2003, 9, 181–203. [Google Scholar] [CrossRef]

- Dennis, D.F. An economic analysis of harvest behavior: Integrating forest and ownership characteristics. For. Sci. 1989, 35, 1088–1104. [Google Scholar]

- Hyberg, B.T.; Holthausen, D.M. The behavior of nonindustrial private forest landowners. Can. J. For. Res. 1989, 19, 1014–1023. [Google Scholar] [CrossRef]

- Joshi, S.; Arano, K.G. Determinants of private forest management decisions: A study on west virginia nipf landowners. For. Policy Econ. 2009, 11, 118–125. [Google Scholar] [CrossRef]

- Brooks, D.J. Public policy and long-term timber supply in the south. For. Sci. 1985, 31, 342–357. [Google Scholar]

- De Steiguer, J.E. Notes: Impact of cost-share programs on private reforestation investment. For. Sci. 1984, 30, 697–704. [Google Scholar]

- Royer, J.P. Determinants of reforestation behavior among southern landowners. For. Sci. 1987, 33, 654–667. [Google Scholar]

- Bell, C.D.; Roberts, R.K.; English, B.C.; Park, W.M. A logit analysis of participation in tennessee’s forest stewardship program. J. Agric. Appl. Econ. 1994, 26, 463–472. [Google Scholar] [CrossRef]

- Esseks, J.D.; Kraft, S.E. Why eligible landowners did not participate in the first four sign-ups of the conservation reserve program. J. Soil Water Conserv. 1988, 43, 251–256. [Google Scholar]

- Nagubadi, V.; McNamara, K.T.; Hoover, W.L.; Mills, W.L. Program participation behavior of nonindustrial forest landowners: A probit analysis. J. Agric. Appl. Econ. 1996, 28, 323–336. [Google Scholar] [CrossRef]

- Amacher, G.S.; Conway, M.C.; Sullivan, J. Nonindustrial Forest Landowner Research: A Synthesis and New Directions; General Technical Report (GTR)-SRS-075; US Department of Agriculture, Forest Service, Southern Research Station: Asheville, NC, USA, 2004; Chapter 22; pp. 241–252.

- Pattanayak, S.K.; Murray, B.C.; Abt, R.C. How joint is joint forest production? An econometric analysis of timber supply conditional on endogenous amenity values. For. Sci. 2002, 48, 479–491. [Google Scholar]

- Roh, T.; Koo, J.-C.; Cho, D.-S.; Youn, Y.-C. Contingent feasibility for forest carbon credit: Evidence from south korean firms. J. Environ. Manag. 2014, 144, 297–303. [Google Scholar] [CrossRef]

- Kim, M.E. Opportunity Costs of Carbon Offsets Project to Private Forest Owners in Korea; Seoul National University: Seoul, Korea, 2013. [Google Scholar]

- Park, M.S.; Koo, J.-C.; Jang, E.-K.; Choi, J.; Han, K. Incentives for vitalizing korean forest carbon offset projects. J. Environ. Policy Admin. 2014, 22, 1–26. [Google Scholar] [CrossRef]

- Maraseni, T.N.; Dargusch, P. Expanding woodland regeneration on marginal southern queensland pastures using market-based instruments: A landowners’ perspective. Australas. J. Environ. Manag. 2008, 15, 104–112. [Google Scholar] [CrossRef]

- Fletcher, L.S.; Kittredge, D.; Stevens, T. Forest landowners’ willingness to sell carbon credits: A pilot study. Northern J. Appl. For. 2009, 26, 35–37. [Google Scholar]

- Dickinson, B.J. Massachusetts Landowner Participation in Forest Management Programs for Carbon Sequestration: An Ordered Logit Analysis of Ratings Data; University of Massachusetts: Amherst, MA, USA, 2010. [Google Scholar]

- Dickinson, B.J.; Stevens, T.H.; Lindsay, M.M.; Kittredge, D.B. Estimated participation in US carbon sequestration programs: A study of nipf landowners in massachusetts. J. For. Econ. 2012, 18, 36–46. [Google Scholar]

- Håbesland, D.E.; Kilgore, M.A.; Becker, D.R.; Snyder, S.A.; Solberg, B.; Sjølie, H.K.; Lindstad, B.H. Norwegian family forest owners’ willingness to participate in carbon offset programs. For. Policy Econ. 2016, 70, 30–38. [Google Scholar] [CrossRef]

- Markowski-Lindsay, M.; Stevens, T.; Kittredge, D.B.; Butler, B.J.; Catanzaro, P.; Dickinson, B.J. Barriers to massachusetts forest landowner participation in carbon markets. Ecol. Econ. 2011, 71, 180–190. [Google Scholar] [CrossRef]

- Miller, K.A.; Snyder, S.A.; Kilgore, M.A. An assessment of forest landowner interest in selling forest carbon credits in the lake states, USA. For. Policy Econ. 2012, 25, 113–122. [Google Scholar] [CrossRef]

- Tian, N.; Poudyal, N.C.; Hodges, D.G.; Young, T.M.; Hoyt, K.P. Understanding the factors influencing nonindustrial private forest landowner interest in supplying ecosystem services in cumberland plateau, tennessee. Forests 2015, 6, 3985–4000. [Google Scholar] [CrossRef]

- Thompson, D.W.; Hansen, E.N. Factors affecting the attitudes of nonindustrial private forest landowners regarding carbon sequestration and trading. J. For. 2012, 110, 129–137. [Google Scholar] [CrossRef]

- Dillmann, D.A.; Smyth, J.D.; Christian, L.M. Internet, Mail, and Mixed-Mode Surveys: The Tailored Design Method; Wiley: Hoboken, NJ, USA, 2009. [Google Scholar]

- Kim, Y.-H. Analysis of the average abatement cost of forest carbon offset projects for the government purchase of forest carbon credits. J. Clim. Chang. Res. 2016, 7, 391–396. [Google Scholar] [CrossRef]

- Kilgore, M.A.; Snyder, S.; Taff, S.; Schertz, J. Family forest stewardship: Do owners need a financial incentive? J. For. 2008, 106, 357–362. [Google Scholar]

- Hanemann, W.M. Welfare evaluations in contingent valuation experiments with discrete responses. Am. J. Agric. Econ. 1984, 66, 332–341. [Google Scholar] [CrossRef]

- Kim, Y.-H.; Jeon, E.-J.; Shin, M.-Y.; Chung, I.-B.; Lee, S.-T.; Seo, K.-W.; Pho, J.-K. A study on the baseline carbon stock for major species in korea for conducting carbon offset projects based on forest management. J. Korean Soc. For. Sci. 2014, 103, 439–445. [Google Scholar] [CrossRef]

- Kwon, O.-B. An analysis on the economic effects of forest management extension service. Korean J. For. Econ. 2014, 21, 13–26. [Google Scholar]

- Rafael, L.P.; Lopez-de-Silanes, F.; Shleifer, A.; Vishny, R.W. Agency problems and dividend policies. J. Financ. 2000, 55, 1–33. [Google Scholar]

{kind=link}

| Characteristic | Explanation |

|---|---|

| Project description | A forest management project that is used to issue forest carbon offset credits through carbon sequestration from tree growth. |

| Project costs | Project development costs and a registration fee are subsidized by the government. |

| Expected revenue | Credits will be sold at 15,000 KRW/tCO2, which corresponds to 80,000–100,000 KRW/ha as expected revenue. |

| Opportunity costs | Timber revenue may decrease as a result of delayed harvest or change of tree species for regeneration. |

| Limitation | Conversion of forest for other land use is prohibited during the project implementation period of 20 to 30 years. |

| Variable | Definition | Hypothesized Effect on Dependent Variable |

|---|---|---|

| Forest characteristics | ||

| FSIZE | Total amount of forest parcel(s) owned in hectare | Positive |

| FAGE | Forest stand age class (I = 1, II = 2, III = 3, IV = 4, V = 5, and VI and older = 6; class interval is 10 years) | Negative |

| BROAD | Majority (75% and higher) of trees are broadleaved (1 if yes, 0 if otherwise) | Positive |

| Experience in forestry support programs | ||

| COSTS | Experience in a cost-sharing program in past five years (1 if yes, 0 otherwise) | Positive |

| ASSIST | Experience in technical assistance or training in past five years (1 if yes, 0 otherwise) | Positive |

| Forest owner characteristics | ||

| AGE | Forest owner age in years | Negative |

| INCOME | Annual income in million KRW (0–10 = 1, 10–20 = 2, 20–30 = 3, 30–40 = 4, and 50 or more = 5) | Positive |

| RESIDE | Residence in Geumsan-gun (1 if yes, 0 otherwise) | Negative |

| EDU | Highest education completed (no education = 1, elementary = 2, middle = 3, high = 4, college = 5, and graduate school = 6) | Positive |

| PURCHASE | Land acquired by purchase (1 if yes, 0 otherwise) | Positive |

| ENVKNOW | Common knowledge in environmental issues (one point for each of five questions) | Positive |

| ENVBELIEF | Agreement with climate change statements (Likert scale 1 “Strongly disagree” to 5 “Strongly agree”) | Positive |

| Management characteristics | ||

| ACTIVE | Active in forest production (1 if full-time or part-time forestry, 0 otherwise) | Negative |

| HARVPAST | Timber harvested in the past (1 if yes, 0 otherwise) | Negative |

| HARVPLAN | Plans to harvest in the future (1 if yes, 0 otherwise) | Negative |

| PRODUCT | Primary management purpose is making forest products (1 if yes, 0 otherwise) | Negative |

| MGMTPLAN | Forest management plan established (1 if yes, 0 otherwise) | Positive |

| Variable | All (n = 132) | Group 1 (n = 62) | Group 2 (n = 32) | Group 3 (n = 38) | χ2 | |||||

|---|---|---|---|---|---|---|---|---|---|---|

| Freq. a | % | Freq. a | % | Freq. a | % | Freq. a | % | |||

| Age | Below 40 | 1 | 0.8 | 0 | 0 | 1 | 3.1 | 0 | 0.0 | 37.096 (p = 0.004) |

| 41–50 | 23 | 17.4 | 6 | 9.7 | 5 | 15.6 | 12 | 31.6 | ||

| 51–60 | 45 | 34.1 | 16 | 25.8 | 21 | 65.6 | 8 | 21.1 | ||

| 61–70 | 45 | 34.1 | 25 | 40.3 | 5 | 15.6 | 15 | 39.5 | ||

| 71–80 | 16 | 12.1 | 13 | 21.0 | 0 | 0.0 | 3 | 7.9 | ||

| 81 and older | 2 | 1.5 | 2 | 3.2 | 0 | 0.0 | 0 | 0.0 | ||

| Mean | 60.4 | 64.3 | 55.1 | 58.6 | ||||||

| Education | Elementary | 13 | 9.8 | 7 | 11.3 | 2 | 6.3 | 4 | 10.5 | 9.845 (p = 0.276) |

| Middle school | 16 | 12.1 | 10 | 16.1 | 2 | 6.3 | 4 | 10.5 | ||

| High school | 54 | 40.9 | 20 | 32.3 | 13 | 40.6 | 21 | 55.3 | ||

| College | 41 | 31.1 | 20 | 32.3 | 12 | 37.5 | 9 | 23.7 | ||

| Graduate | 8 | 6.1 | 5 | 8.1 | 3 | 9.4 | 0 | 0.0 | ||

| Annual income (million KRW) | Less than 10 | 21 | 15.9 | 16 | 25.8 | 2 | 6.3 | 3 | 7.9 | 22.917 (p = 0.011) |

| 10–20 | 24 | 18.2 | 12 | 19.4 | 4 | 12.5 | 8 | 21.1 | ||

| 20–30 | 27 | 20.5 | 10 | 16.1 | 6 | 18.8 | 11 | 28.9 | ||

| 30–40 | 19 | 14.4 | 7 | 11.3 | 5 | 15.6 | 7 | 18.4 | ||

| 40–50 | 22 | 16.7 | 7 | 11.3 | 6 | 18.8 | 9 | 23.7 | ||

| More than 50 | 19 | 14.4 | 10 | 16.1 | 9 | 28.1 | 0 | 0.0 | ||

| Residence | Nearby | 86 | 65.2 | 37 | 59.7 | 23 | 71.9 | 26 | 68.4 | 1.634 (p = 0.442) |

| Absentee | 46 | 34.8 | 25 | 40.3 | 9 | 28.1 | 12 | 31.6 | ||

| Management Characteristics | All (n = 132) | Group 1 (n = 62) | Group 2 (n = 32) | Group 3 (n = 38) | χ2 * | |||||

|---|---|---|---|---|---|---|---|---|---|---|

| Freq. a | % | Freq. a | % | Freq. a | % | Freq. a | % | |||

| Land purchased | 43 | 32.6 | 11 | 17.7 | 20 | 62.5 | 12 | 31.6 | 19.275 (p = 0.000) | |

| Full-time or part-time forestry | 54 | 40.9 | 20 | 32.3 | 26 | 81.3 | 8 | 21.1 | 29.660 (p = 0.000) | |

| Harvest in the past | 49 | 37.1 | 23 | 37.1 | 8 | 25.0 | 18 | 47.4 | 3.724 (p = 0.155) | |

| Harvest in the future | 33 | 25.0 | 16 | 25.8 | 9 | 28.1 | 8 | 21.1 | 0.504 (p = 0.777) | |

| Management plan established | 39 | 29.5 | 9 | 14.5 | 14 | 43.8 | 16 | 42.1 | 12.709 (p = 0.002) | |

| Primary goal is forest products | 37 | 28.0 | 7 | 11.3 | 20 | 62.5 | 10 | 26.3 | 27.515 (p = 0.000) | |

| Broadleaved forest | 50 | 37.9 | 24 | 38.7 | 10 | 31.3 | 16 | 42.1 | 0.904 (p = 0.636) | |

| Experience in cost-sharing | 36 | 27.3 | 21 | 33.9 | 12 | 37.5 | 3 | 7.9 | 10.242 (p = 0.006) | |

| Experience in tech assistance | 51 | 38.6 | 7 | 11.3 | 17 | 53.1 | 27 | 71.1 | 39.231 (p = 0.000) | |

| Forest size (ha) | 0–2.0 | 34 | 25.8 | 15 | 24.2 | 4 | 12.5 | 8 | 21.1 | 22.763 (p = 0.004) |

| 2.1–5.0 | 43 | 32.6 | 21 | 33.9 | 7 | 21.9 | 22 | 57.9 | ||

| 5.1–10.0 | 21 | 15.9 | 9 | 14.5 | 5 | 15.6 | 7 | 18.4 | ||

| 10.1–50.0 | 29 | 22.0 | 15 | 24.2 | 13 | 40.6 | 1 | 2.6 | ||

| 50.0 | 5 | 3.8 | 2 | 3.2 | 3 | 9.4 | 0 | 0.0 | ||

| Mean | 9.77 | 9.97 | 16.83 | 2.5 | ||||||

| Forest stand age class | I | 39 | 29.5 | 36 | 58.1 | 2 | 6.3 | 1 | 2.6 | 55.699 (p = 0.000) |

| II | 11 | 8.3 | 3 | 4.8 | 6 | 18.8 | 2 | 5.3 | ||

| III | 13 | 9.8 | 2 | 3.2 | 5 | 15.6 | 6 | 15.8 | ||

| IV | 37 | 28.0 | 12 | 19.4 | 9 | 28.1 | 16 | 42.1 | ||

| V | 28 | 21.2 | 7 | 11.3 | 8 | 25.0 | 13 | 34.2 | ||

| VI and older | 4 | 3.0 | 2 | 3.2 | 2 | 6.3 | 2 | 6.3 | ||

| Variable | Hypothesized Effect | Model 1 All Respondents (n = 132) | Model 2-1 Group 1 (n = 62) | Model 2-2 Group 2 and 3 (n = 70) |

|---|---|---|---|---|

| FSIZE | Positive | 0.041 *** (0.016) | 0.059 (0.032) | 0.059 ** (0.025) |

| FAGE | Negative | −0.322 ** (0.159) | −0.106 (0.256) | −0.703 (0.436) |

| BROAD | Positive | 0.843 * (0.446) | 1.931 ** (0.957) | 1.482 (1.025) |

| COSTS | Positive | 1.259 ** (0.538) | −0.150 (0.908) | 3.702 *** (1.264) |

| ASSIST | Positive | −0.051 (0.500) | 0.216 (1.444) | −0.258 (0.868) |

| AGE | Negative | −0.004 (0.031) | −0.014 (0.064) | −0.082 (0.066) |

| INCOME | Positive | −0.141 (0.181) | −0.209 (0.337) | −0.195 (0.360) |

| RESIDE | Negative | −0.727 (0.501) | 0.961 (1.059) | −1.107 (0.859) |

| EDU | Positive | −0.124 (0.297) | 0.026 (0.606) | 0.308 (0.560) |

| PURCHASE | Positive | −0.048 (0.504) | 2.457 * (1.361) | −0.963 (0.814) |

| ENVKNOW | Positive | −0.051 (0.173) | −0.695 (0.428) | 0.106 (0.421) |

| ENVBELIEF | Positive | 0.370 *** (0.136) | 1.064 *** (0.346) | 0.281 (0.311) |

| ACTIVE | Negative | −0.282 (0.487) | −1.993 (1.213) | −0.087 (1.042) |

| HARVPAST | Negative | −0.868 * (0.516) | 0.172 (0.903) | −1.141 (1.302) |

| HARVPLAN | Negative | 0.674 (0.501) | 0.534 (1.051) | 0.158 (1.061) |

| PRODUCT | Negative | −0.884 (0.629) | 0.133 (1.822) | −3.002 ** (1.520) |

| MGMTPLAN | Positive | 0.532 (0.531) | 5.618 * (2.886) | 0.315 (0.878) |

| Constant | −1.572 (2.815) | −1.541 (2.813) | 3.494 (5.834) | |

| Goodness-of-fit statistics | ||||

| Log likelihood ratio (χ2) | 39.200 (p = 0.003) | 34.400 (p = 0.007) | 38.600 (p = 0.002) | |

| Cox and Snell R2 | 0.257 | 0.426 | 0.424 | |

| Nigelkerke R2 | 0.343 | 0.571 | 0.578 | |

| Hosmer–Lemeshow (χ2) | 12.262 (p = 0.140) | 8.293 (p = 0.405) | 5.565 (p = 0.696) | |

| Willingness | All (n = 132) | Group 1 (n = 62) | Group 2 (n = 32) | Group 3 (n = 38) | χ2 | ||||

|---|---|---|---|---|---|---|---|---|---|

| Freq. a | % | Freq. a | % | Freq. a | % | Freq. a | % | ||

| Yes | 61 | 46.2 | 35 | 56.5 | 13 | 40.6 | 13 | 34.2 | 5.219 (p = 0.074) |

| No | 71 | 53.8 | 27 | 43.5 | 19 | 59.4 | 25 | 65.8 | |

| Total | 132 | 100.0 | 62 | 100.0 | 32 | 100.0 | 38 | 100.0 | |

| Willingness | All (n = 132) | Group 1 and A (n = 82) | Group B (n = 50) | χ2 | |||

|---|---|---|---|---|---|---|---|

| Freq. a | % | Freq. a | % | Freq. a | % | ||

| Yes | 61 | 46.2 | 42 | 51.2 | 19 | 38.0 | 2.184 (p = 0.139) |

| No | 71 | 53.8 | 40 | 48.8 | 31 | 62.0 | |

| Total | 132 | 100.0 | 82 | 100.0 | 50 | 100.0 | |

| Willingness | All (n = 132) | Group 1 (n = 62) | Group A (n = 20) | Group B (n = 50) | χ2 | ||||

|---|---|---|---|---|---|---|---|---|---|

| Freq. a | % | Freq. a | % | Freq. a | % | Freq. a | % | ||

| Yes | 61 | 46.2 | 35 | 56.5 | 7 | 35.0 | 19 | 38.0 | 4.983 (p = 0.083) |

| No | 71 | 53.8 | 27 | 43.5 | 13 | 65.0 | 31 | 62.0 | |

| Total | 132 | 100.0 | 62 | 100.0 | 20 | 100.0 | 50 | 100.0 | |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Shin, S.; Yeo-Chang, Y. Perspectives of Private Forest Owners toward Investment in Forest Carbon Offset Projects: A Case of Geumsan-Gun, South Korea. Forests 2019, 10, 21. https://doi.org/10.3390/f10010021

Shin S, Yeo-Chang Y. Perspectives of Private Forest Owners toward Investment in Forest Carbon Offset Projects: A Case of Geumsan-Gun, South Korea. Forests. 2019; 10(1):21. https://doi.org/10.3390/f10010021

Chicago/Turabian StyleShin, Seunguk, and Youn Yeo-Chang. 2019. "Perspectives of Private Forest Owners toward Investment in Forest Carbon Offset Projects: A Case of Geumsan-Gun, South Korea" Forests 10, no. 1: 21. https://doi.org/10.3390/f10010021

APA StyleShin, S., & Yeo-Chang, Y. (2019). Perspectives of Private Forest Owners toward Investment in Forest Carbon Offset Projects: A Case of Geumsan-Gun, South Korea. Forests, 10(1), 21. https://doi.org/10.3390/f10010021