Low-Carbon Energy Development in Indonesia in Alignment with Intended Nationally Determined Contribution (INDC) by 2030

Abstract

:1. Introduction

2. National Energy Circumstances and Related CO2 Emissions

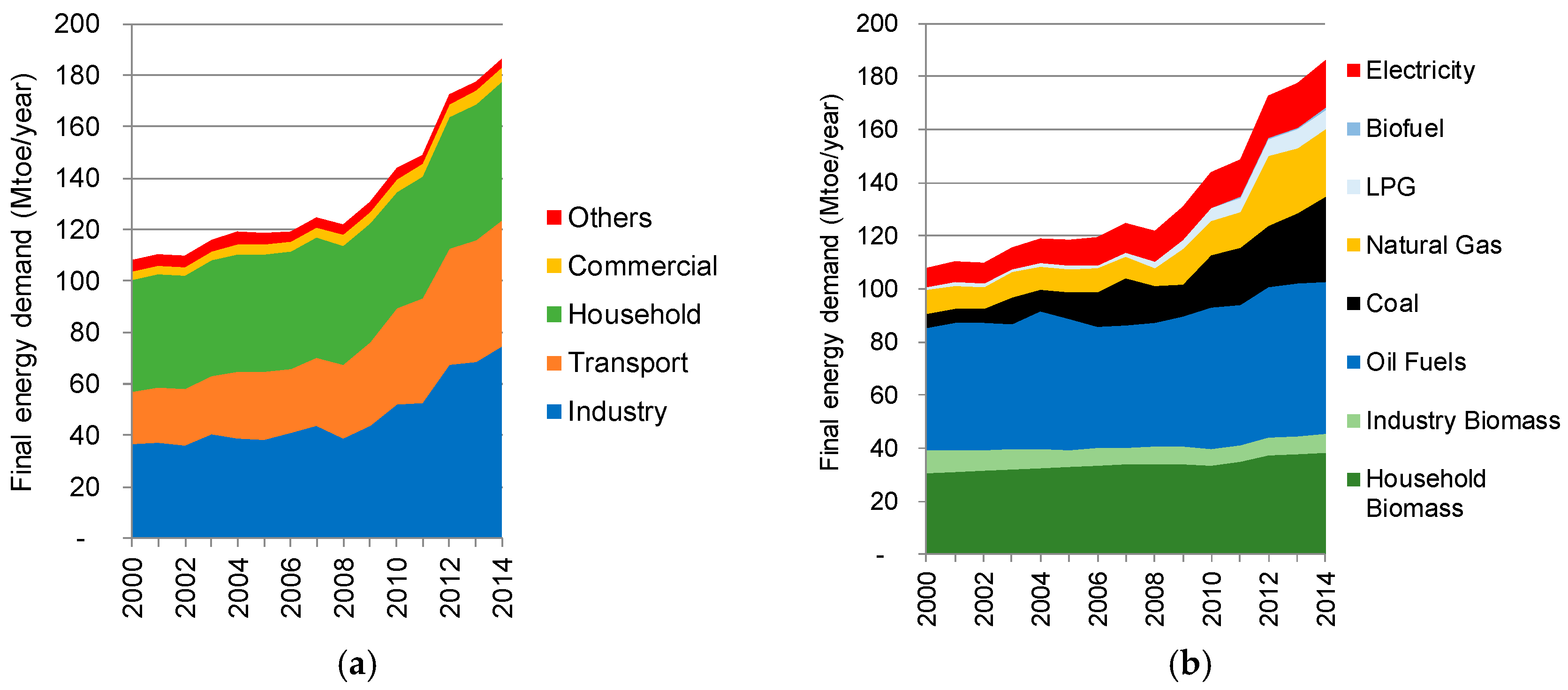

2.1. Energy Resources and Trends

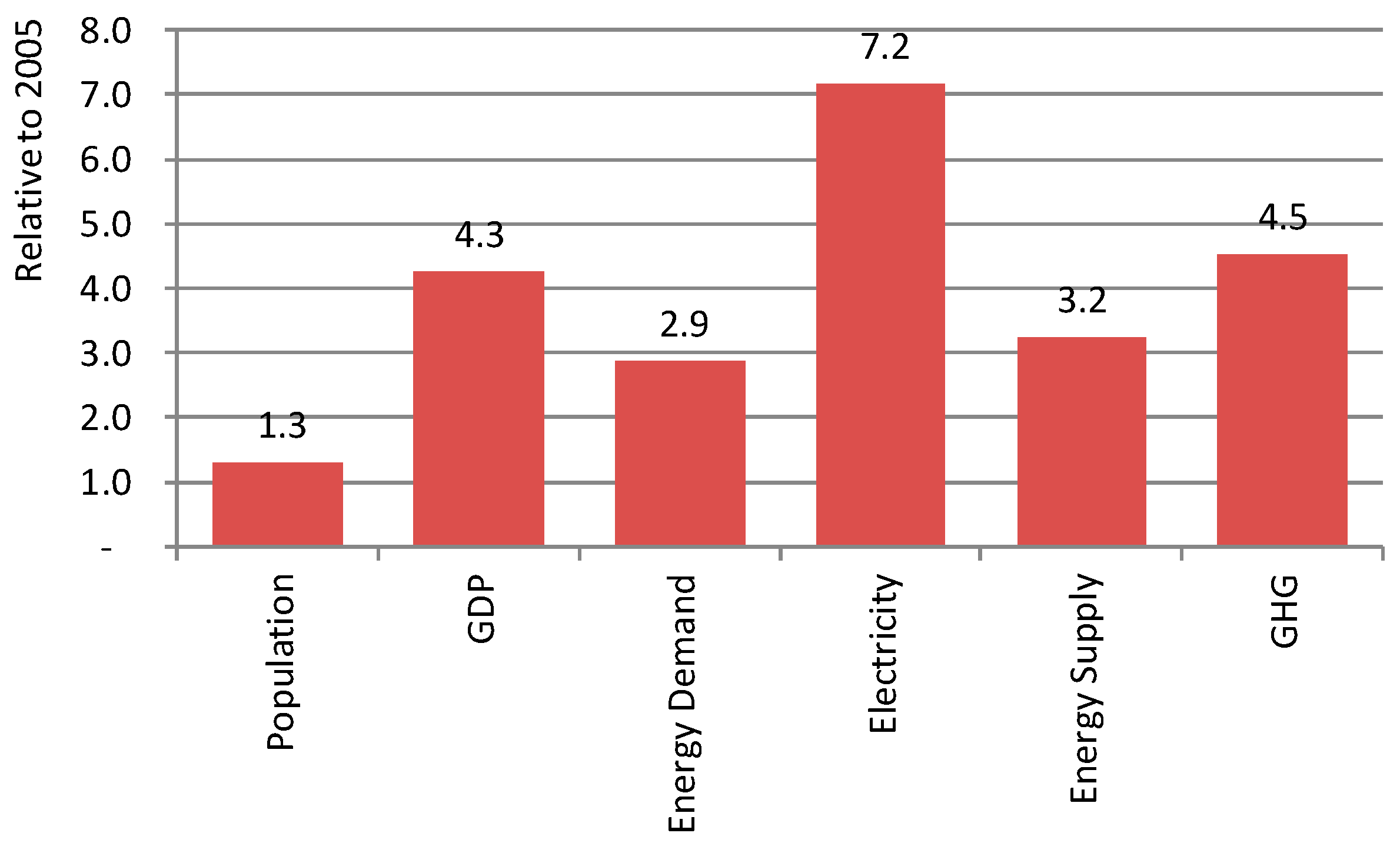

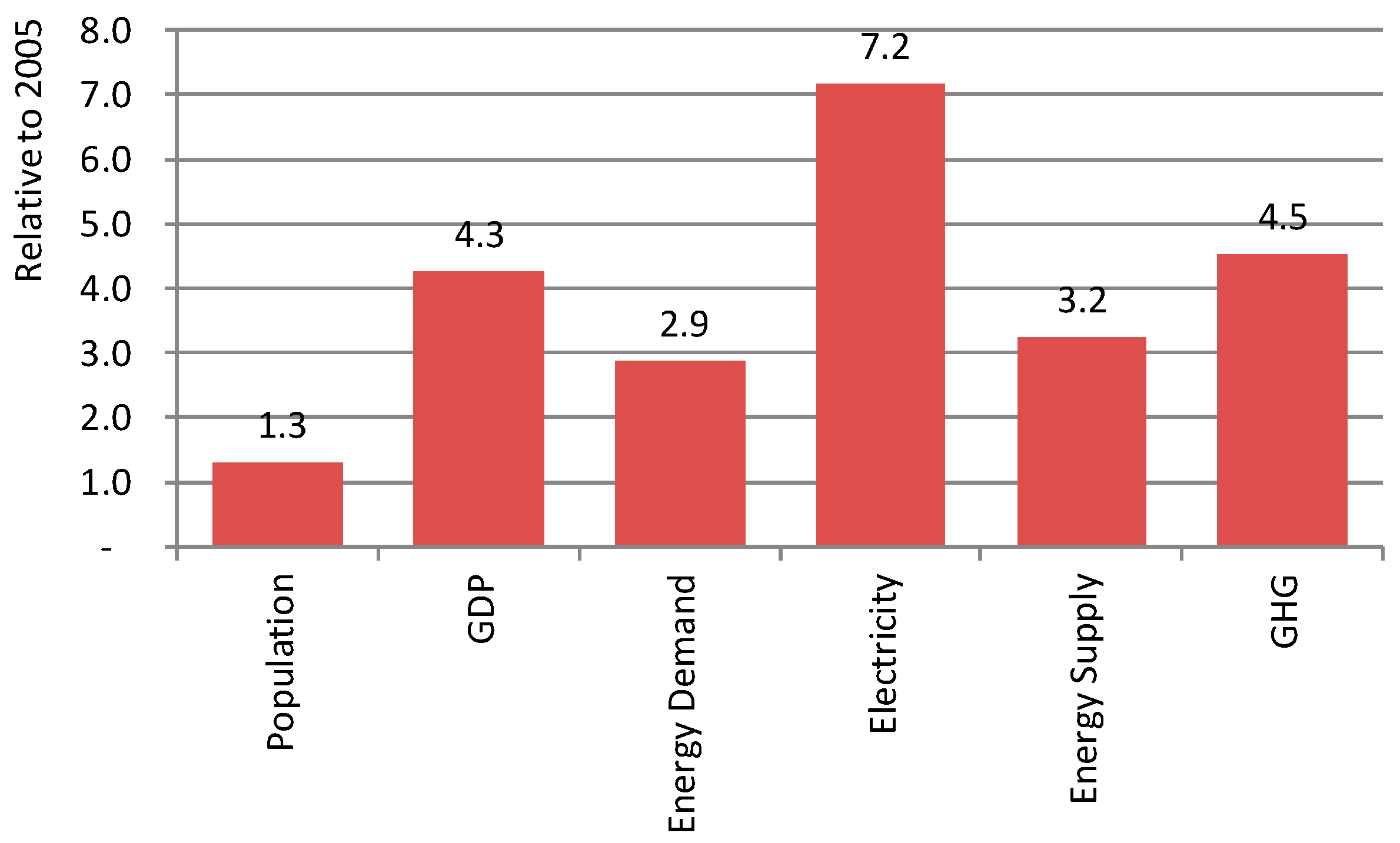

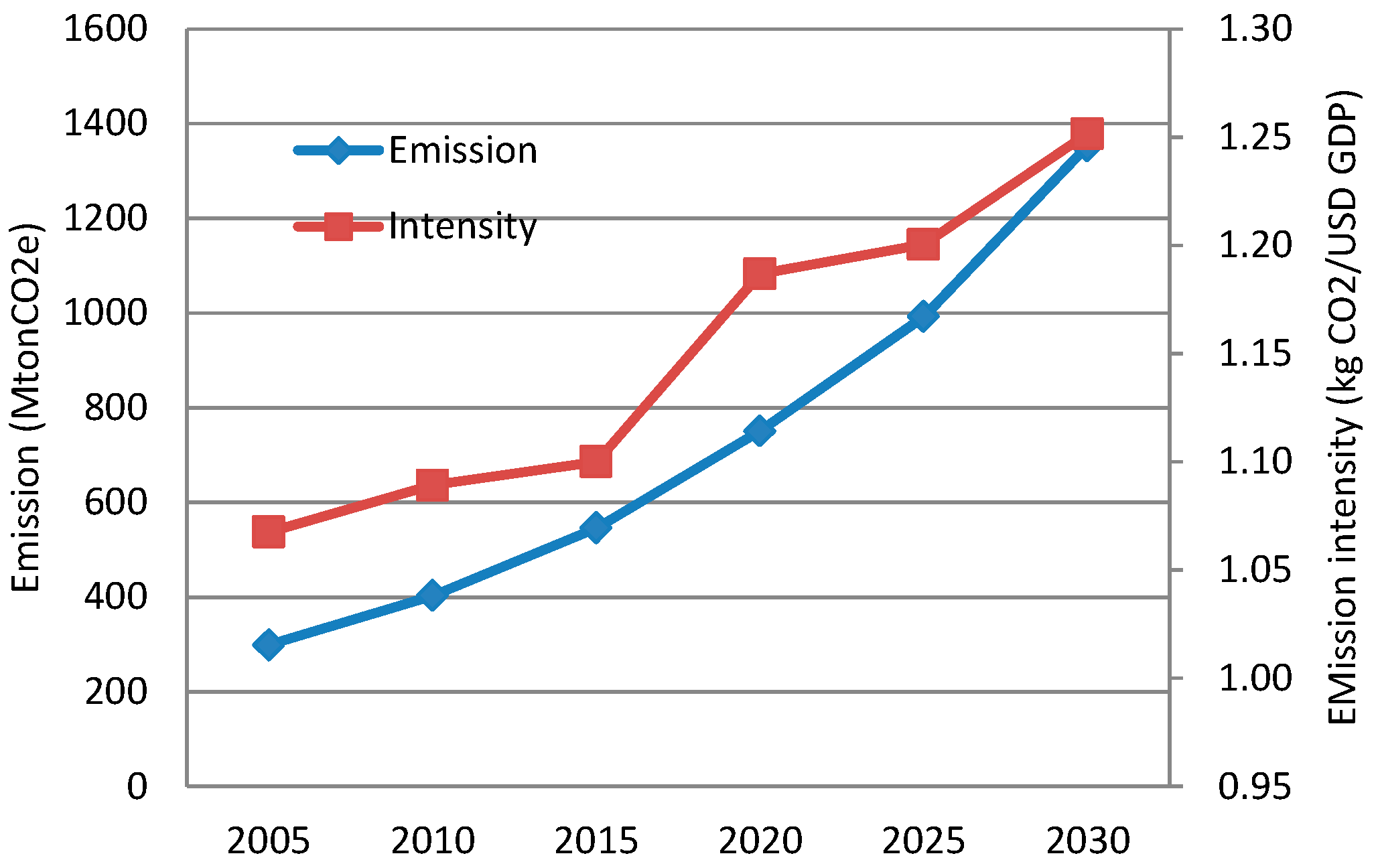

2.2. Greenhouse Gas (GHG) Emissions

3. Methodology

3.1. Model

3.2. Scenarios

3.2.1. Scenario Frameworks, Socioeconomic Assumptions, and Emission Targets

3.2.2. Power Generation Assumptions

3.2.3. Energy Demand Assumptions

4. Results

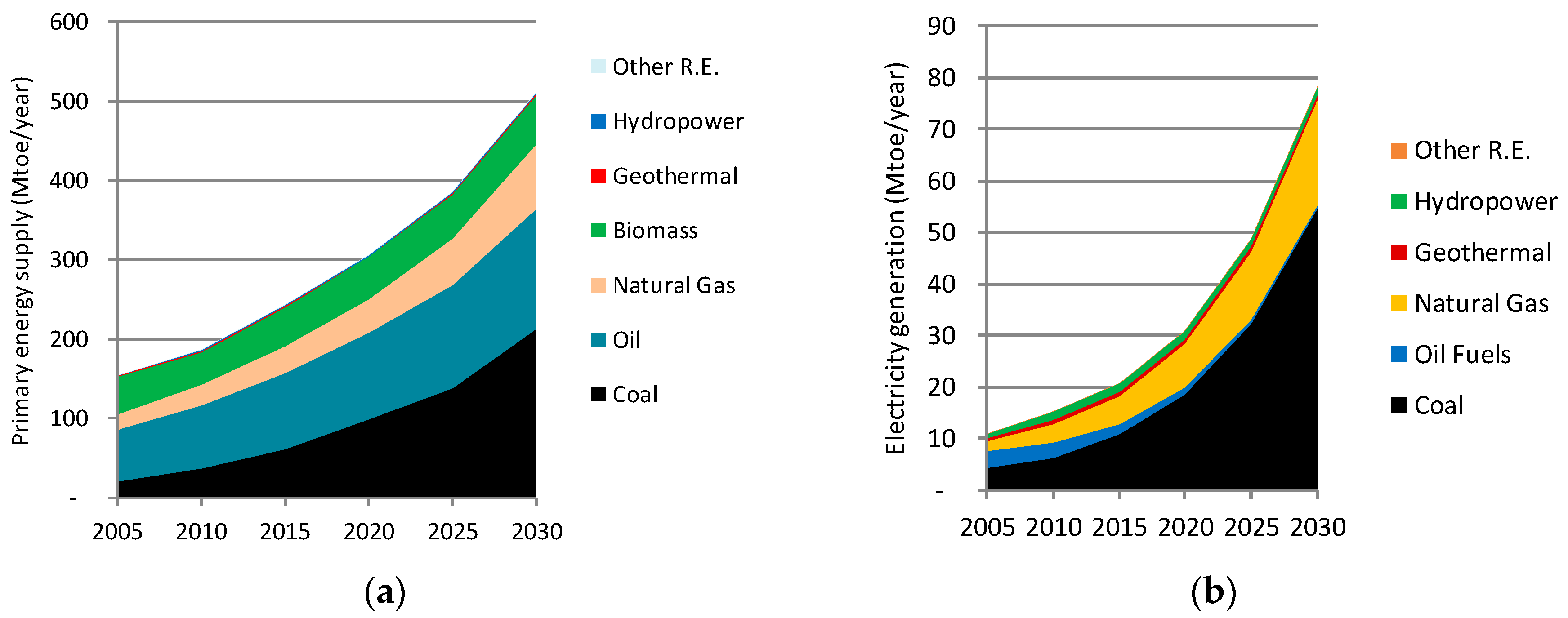

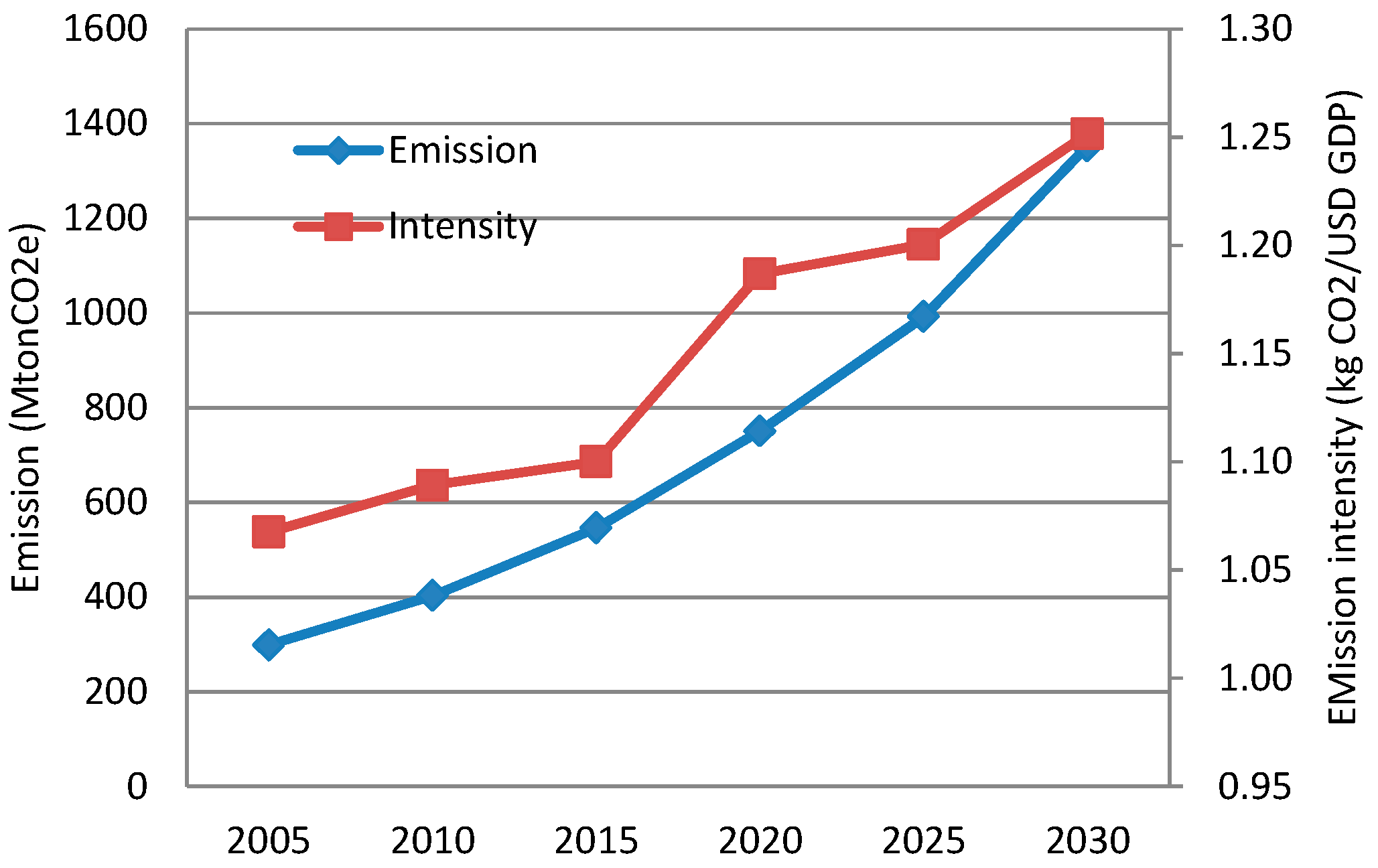

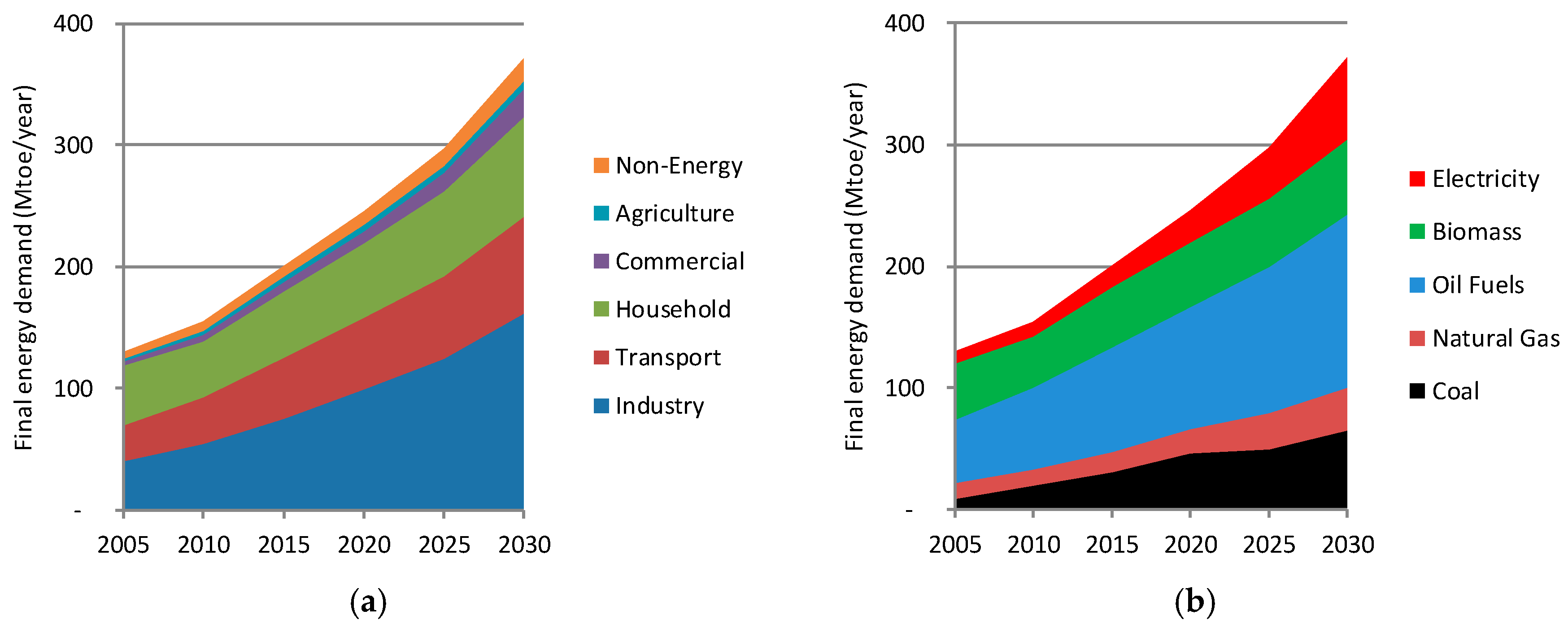

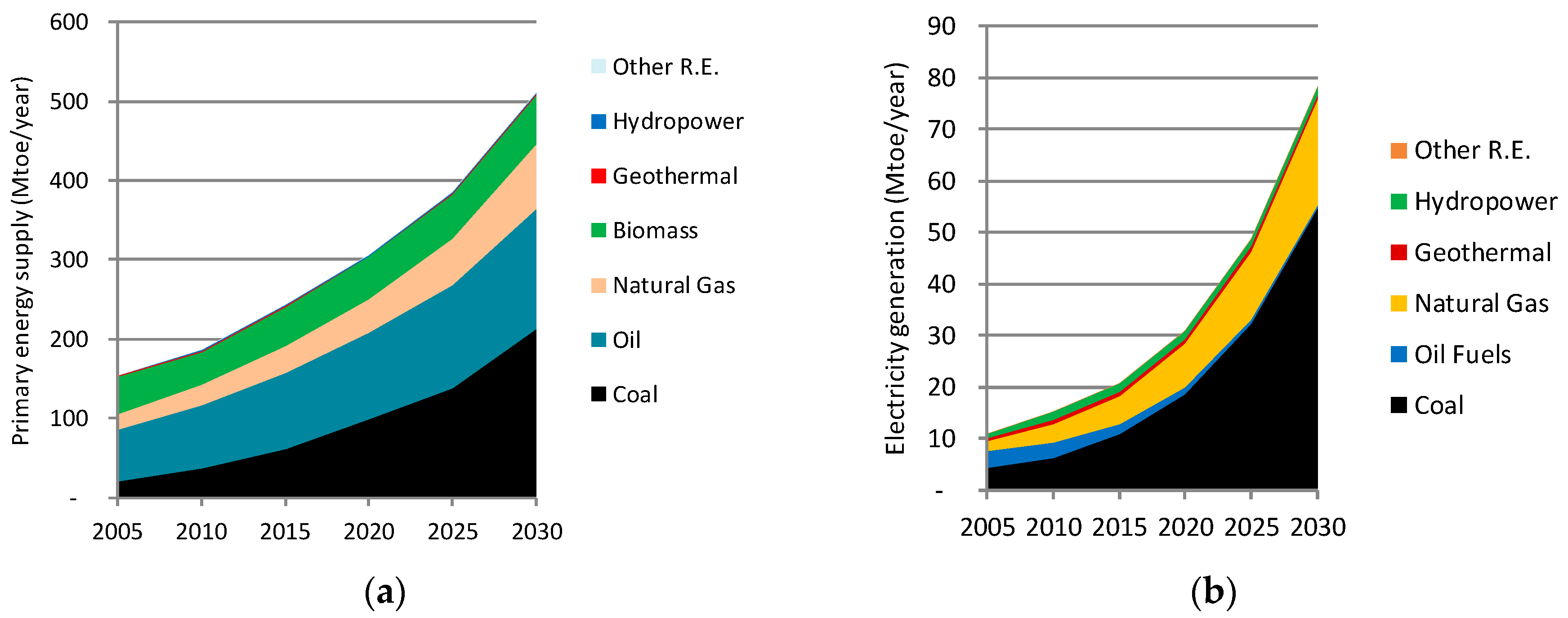

4.1. The Baseline Scenario (Baseline)

4.2. Mitigation Scenarios

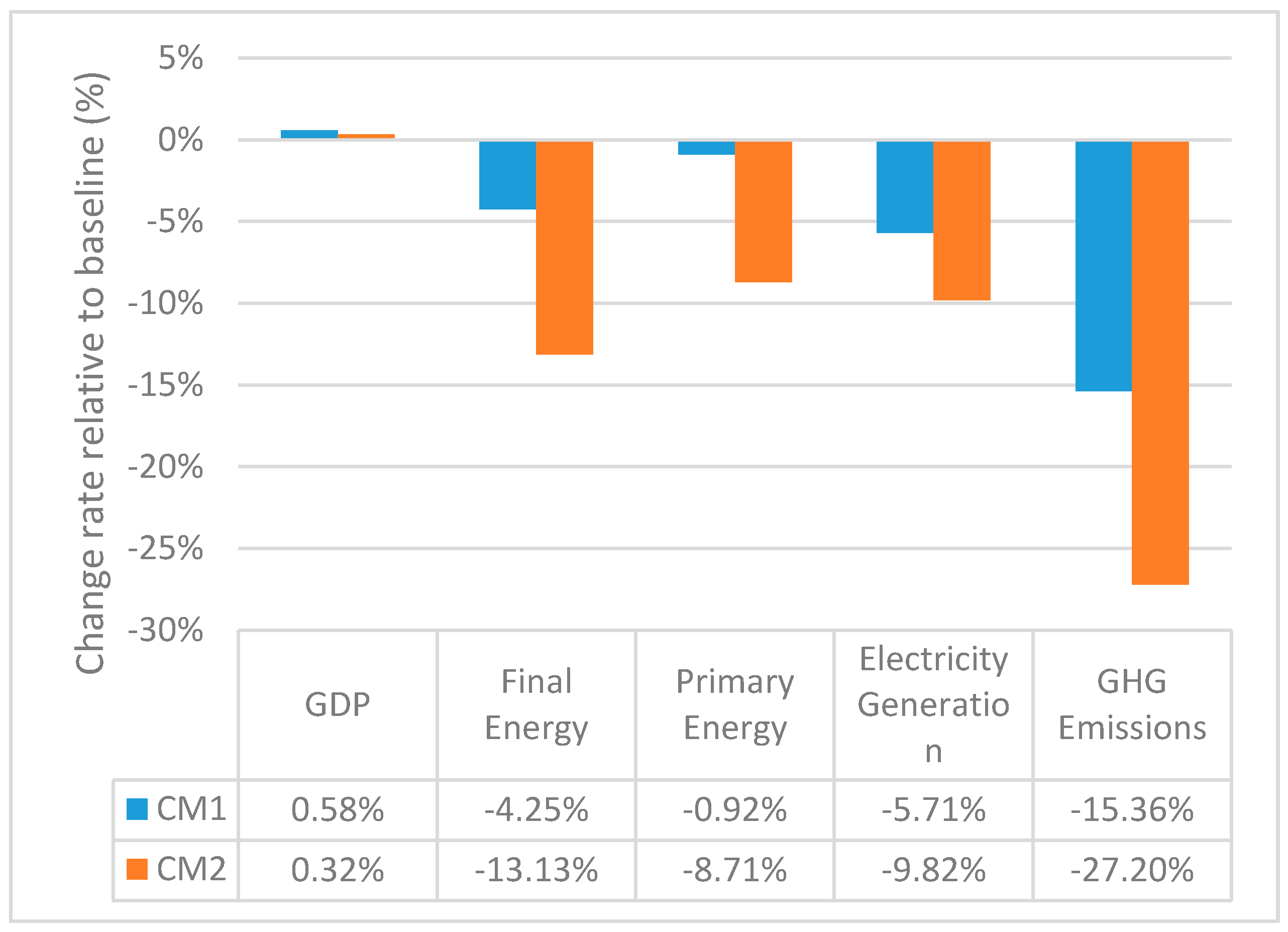

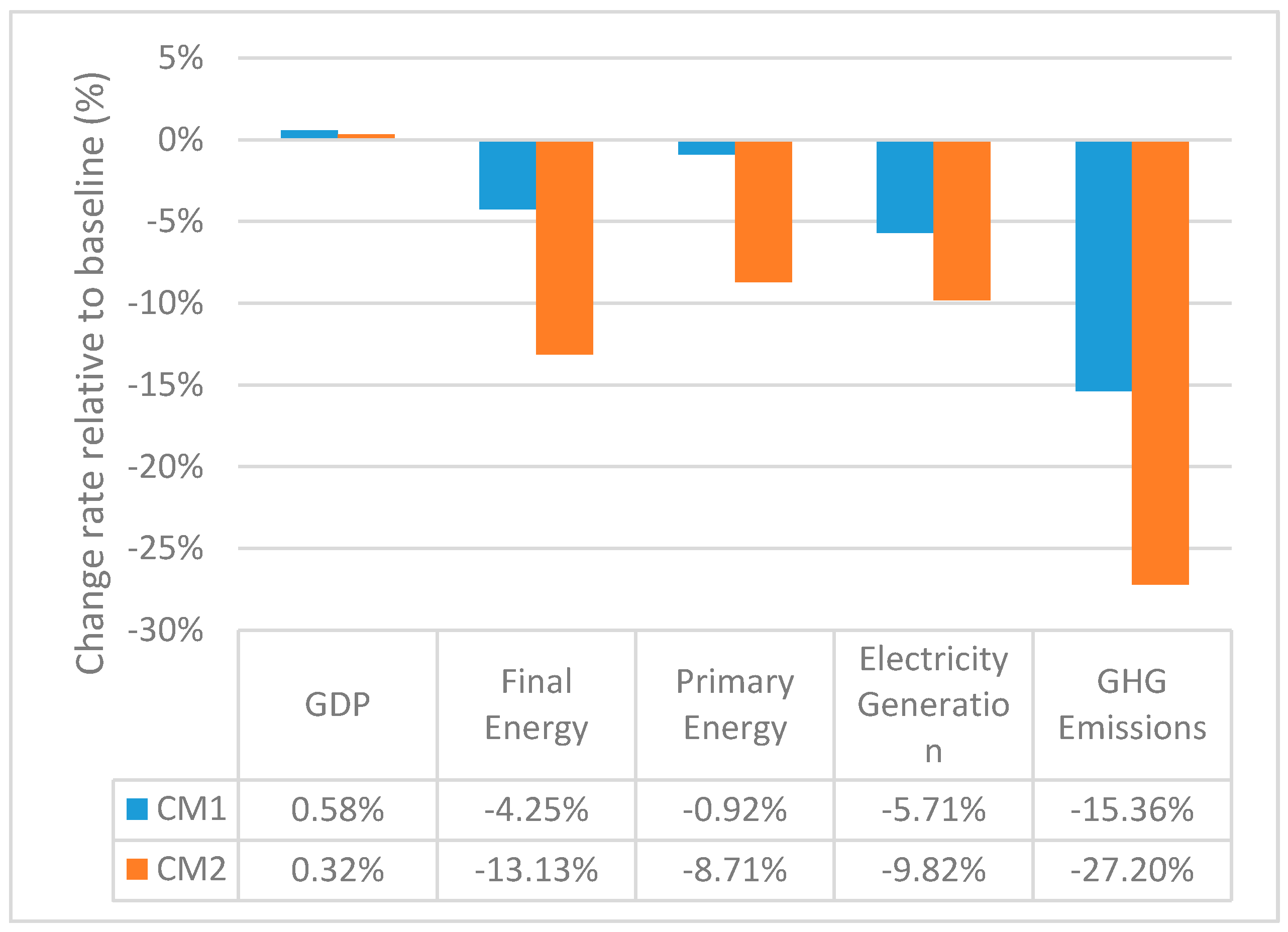

4.2.1. Overall Results

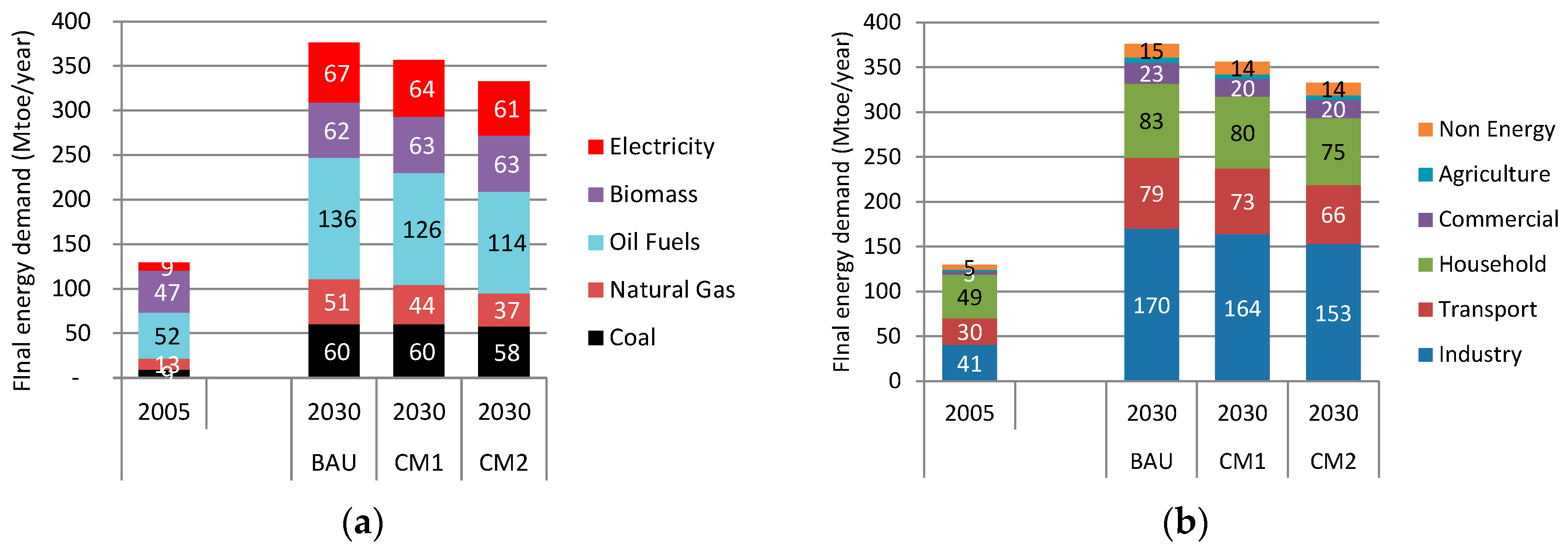

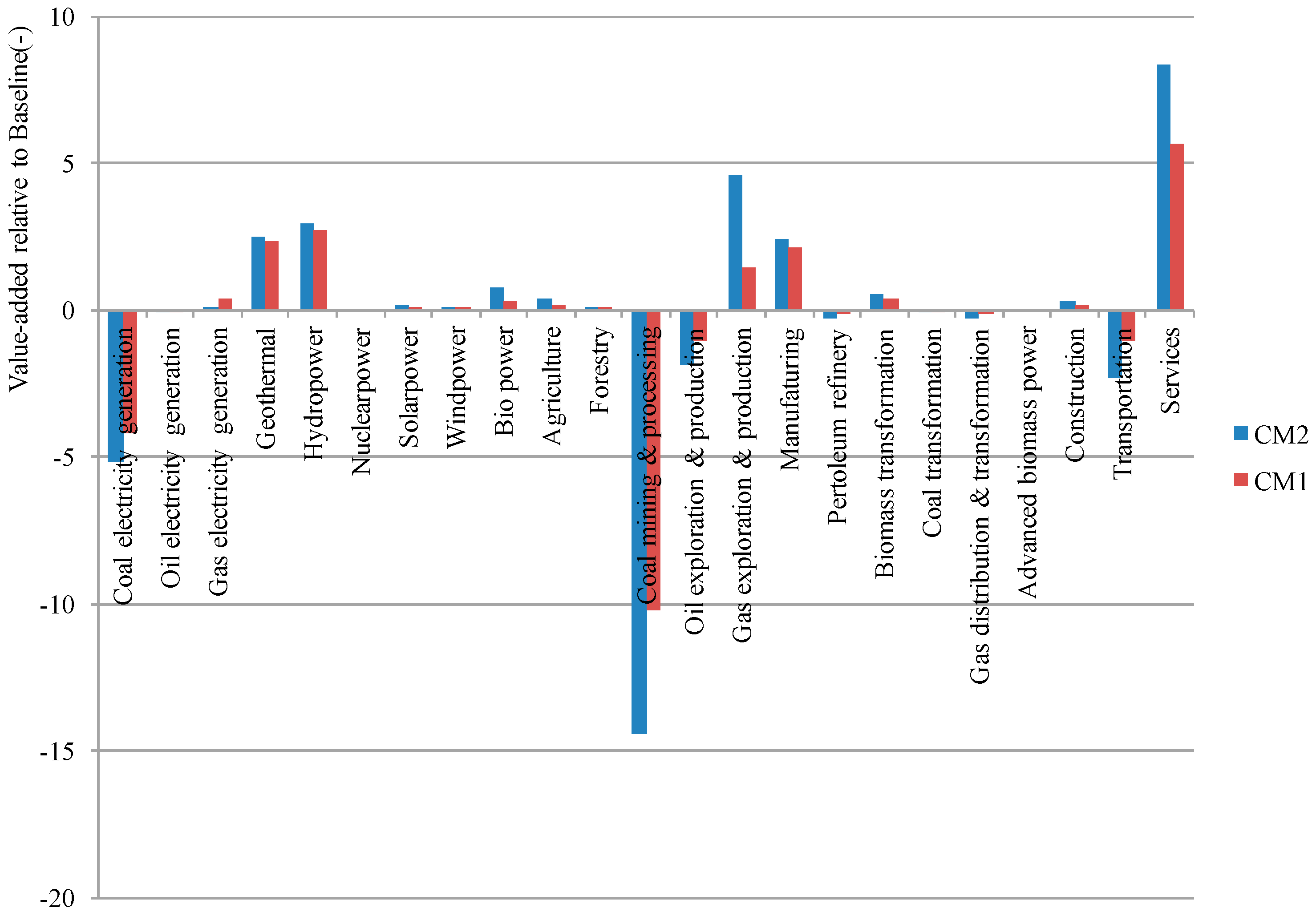

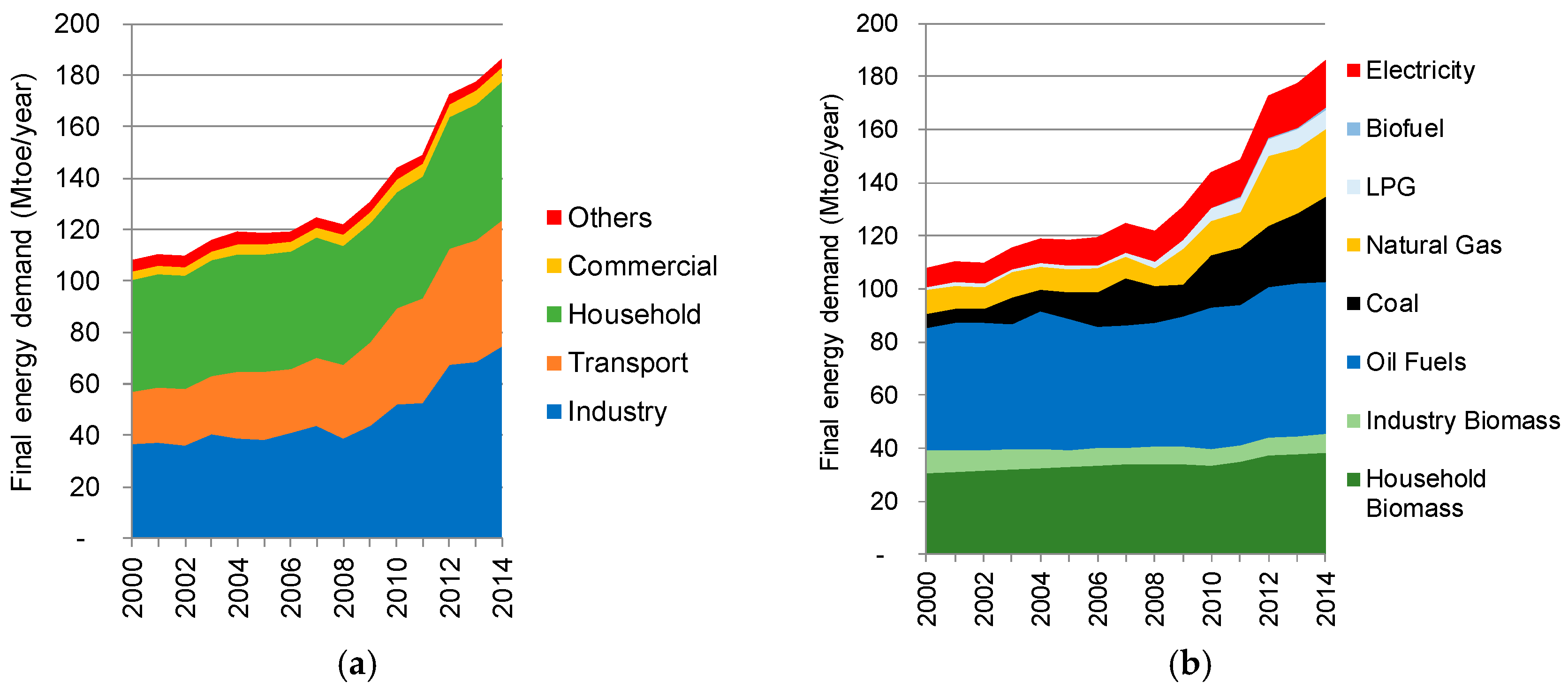

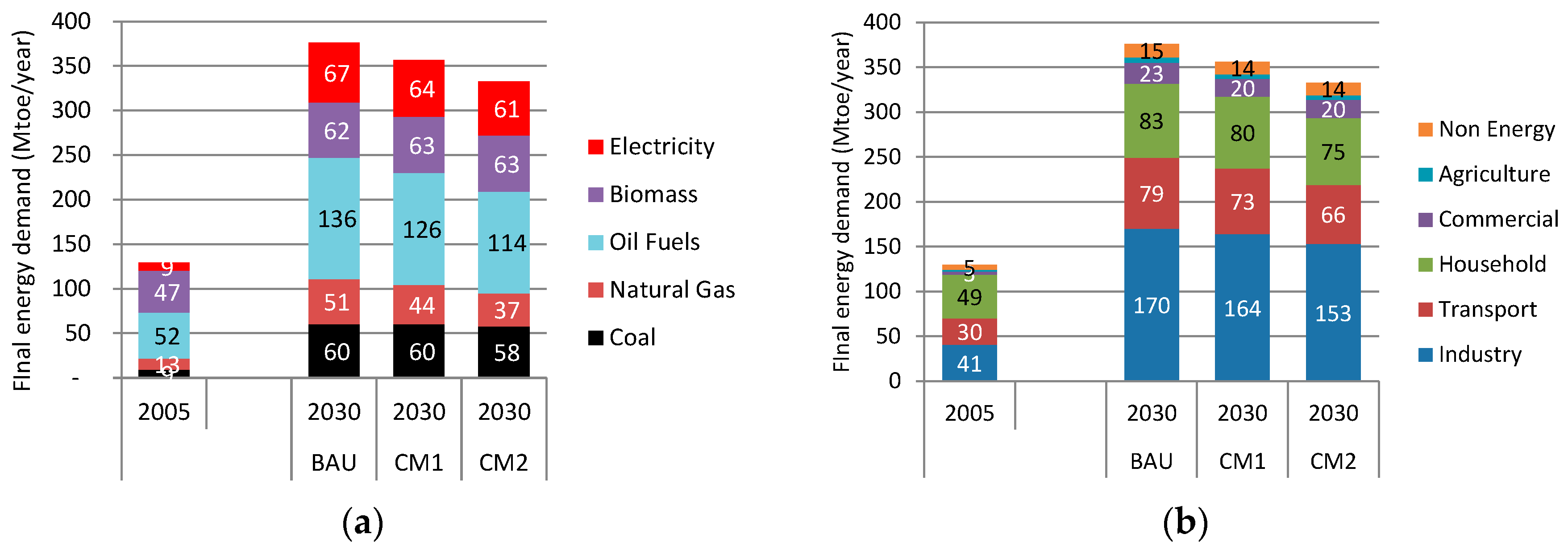

4.2.2. Final Energy

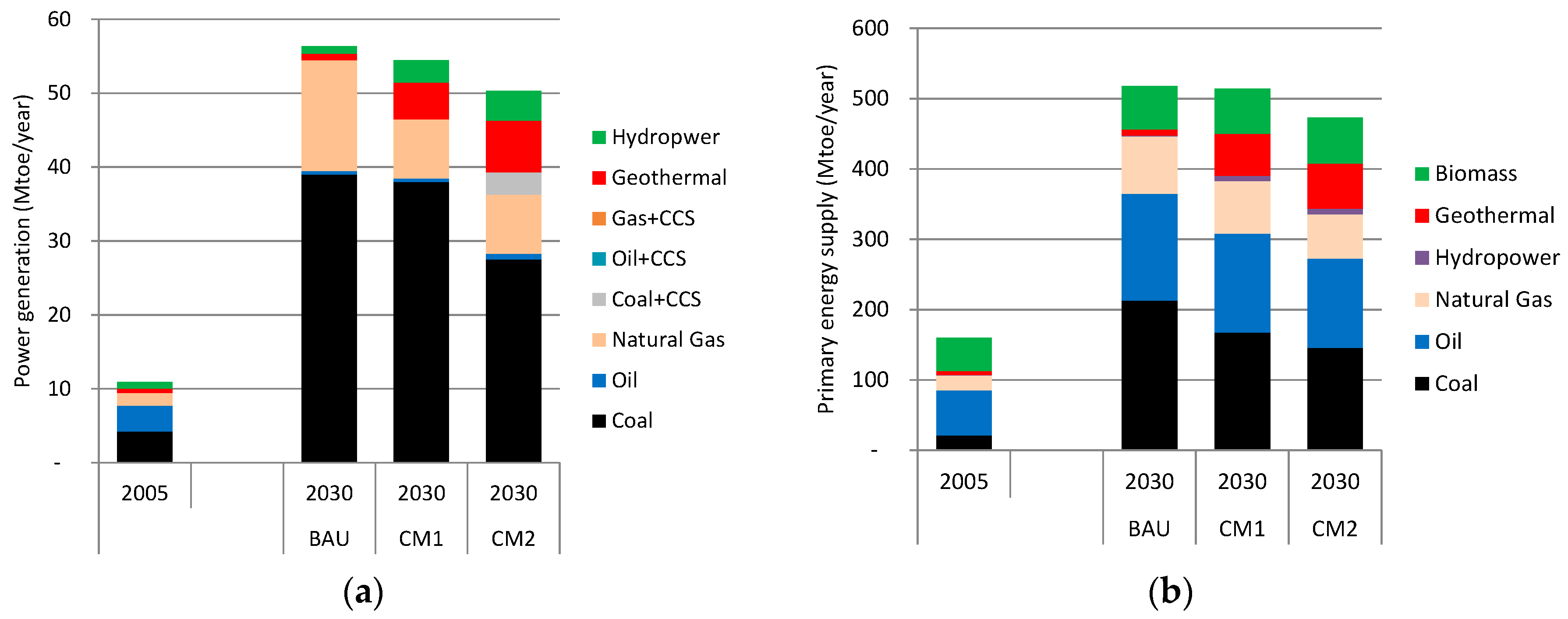

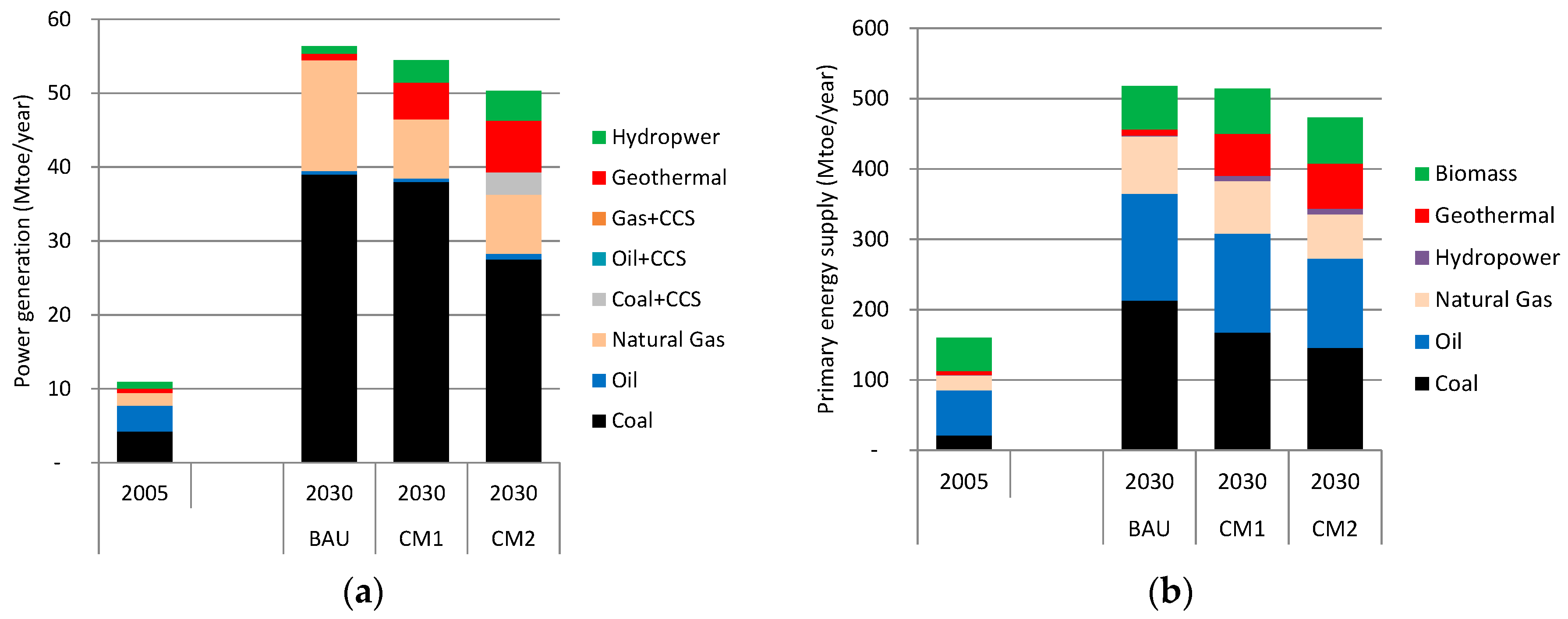

4.2.3. Electricity and Primary Energy Mix Changes

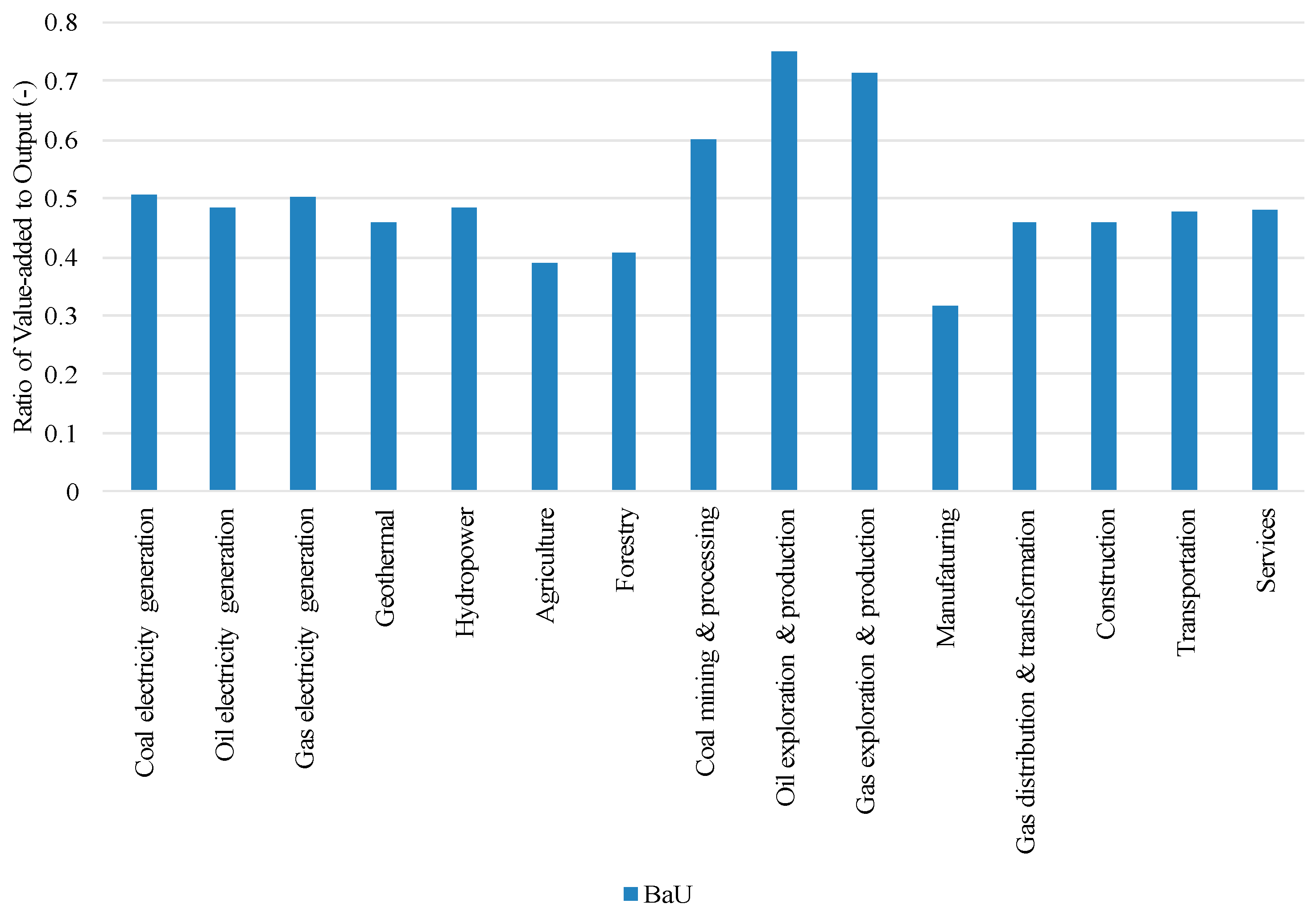

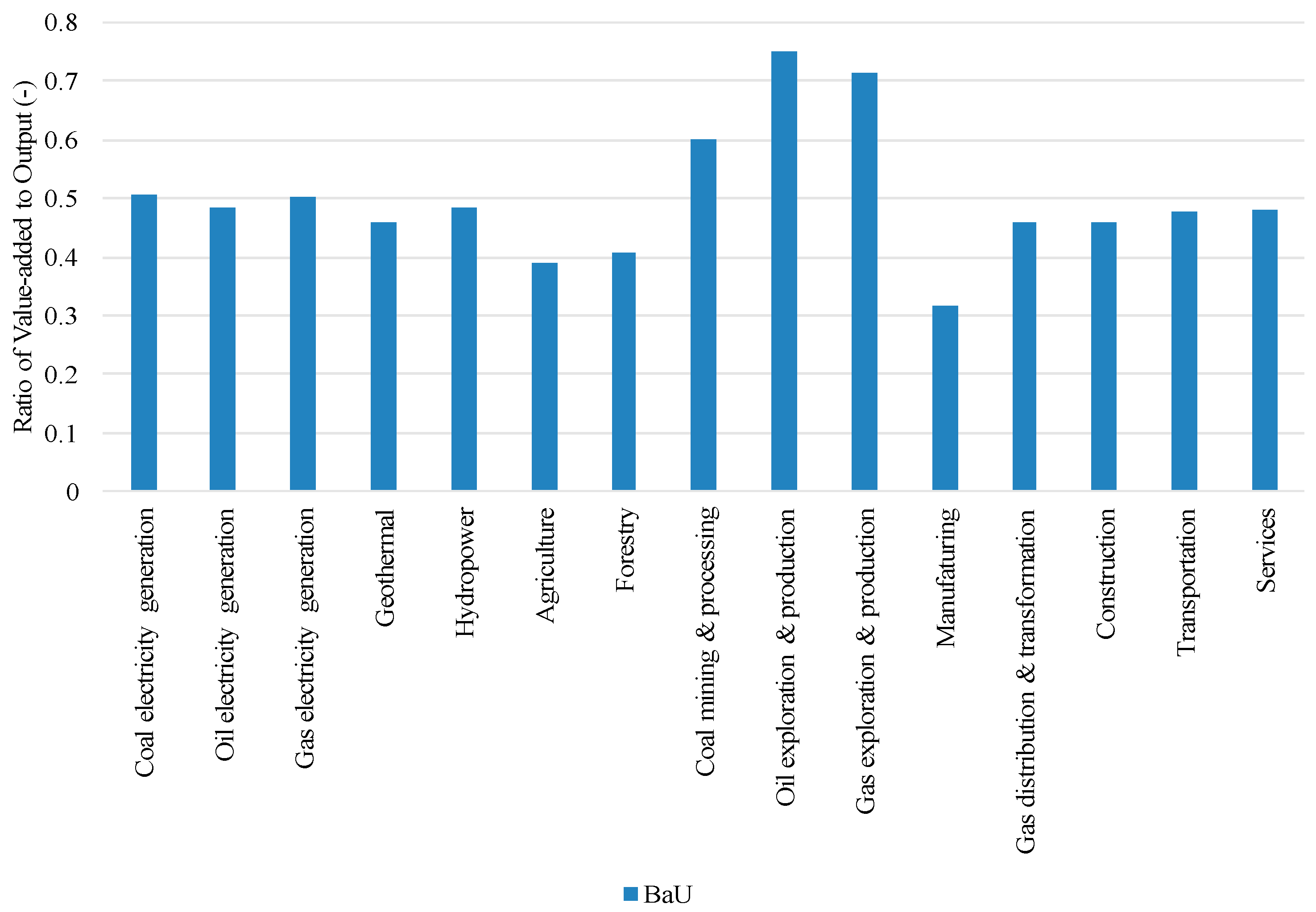

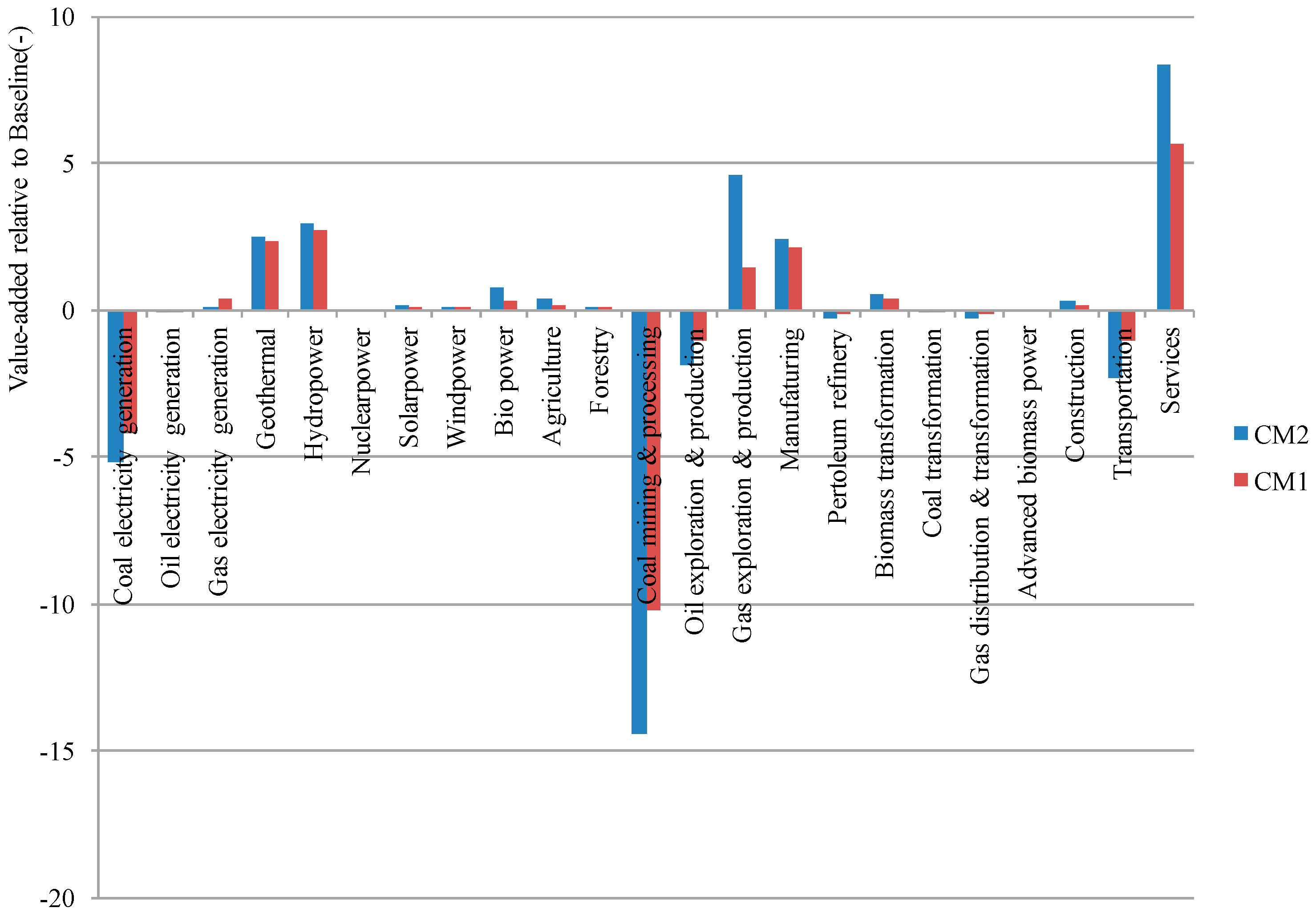

4.2.4. Mitigation Costs

5. Discussion

5.1. The Role of Low-Carbon Energy Systems

5.2. Limitations

6. Conclusions

Supplementary Materials

Acknowledgments

Author Contributions

Conflicts of Interest

References

- Hasan, M.H.; Mahlia, T.M.I.; Nur, H. A review on energy scenario and sustainable energy in Indonesia. Renew. Sustain. Energy Rev. 2012, 16, 2316–2328. [Google Scholar] [CrossRef]

- Jupesta, J. Modeling technological changes in the biofuel production system in Indonesia. Appl. Energy 2012, 90, 211–217. [Google Scholar] [CrossRef]

- Bappenas. Rencana Pembangunan Jangka Menengah Nasional (RPJMN) 2015–2019; Badan Perencanaan Pembangunan Nasional: Jakarta, Indonesia, 2014.

- Ibrahim, H.; Thaib, N.; Abdul Wahid, L. Indonesia energy scenario to 2050: Projection of consumption, supply option and primary energy mix scenarios. In Proceedings of the Energy Links Between Russia and East Asia: Development Strategies for the XXI Century, Irkutsk, Russia, 30 August–3 September 2010.

- Dewi, R.G.; Kobashi, T.; Matsuoka, Y.; Gomi, K.; Ehara, T.; Kainuma, M.; Fujino, J. Low Carbon Society Scenario toward 2050: Indonesia Energy Sector; Global Partnership: Nairobi, Kenya, 2010. [Google Scholar]

- Siagian, U.W.R.; Dewi, R.G.; Boer, R.; Hendrawana, I.; Yuwonoa, B.B.; Ginting, G.E. Pathways to Deep Decarbonization in Indonesia; Sustainable Development Solutions Network (SDSN) and Institute for Sustainable Development and International Relations (IDDRI): New York, NY, USA, 2015. [Google Scholar]

- Nasional, D.E. Outlook Energi Indonesia 2015; Dewan Energi Nasional: Calgary, AB, Canada, 2015. [Google Scholar]

- Statistics, E. Ministry of Energy and Mineral Resource; Center of Data and Information: Jakarta, Indonesia, 2016. [Google Scholar]

- National Action Plan for Reducing GHG Emissions; Government of Indonesia: Jakarta, Indonesia, 2011.

- Fujimori, S.; Masui, T.; Matsuoka, Y. Gains from emission trading under multiple stabilization targets and technological constraints. Energy Econ. 2015, 48, 306–315. [Google Scholar] [CrossRef]

- Hasegawa, T.; Fujimori, S.; Shin, Y.; Tanaka, A.; Takahashi, K.; Masui, T. Consequence of climate mitigation on the risk of hunger. Environ. Sci. Technol. 2015, 49, 7245–7253. [Google Scholar] [CrossRef] [PubMed]

- Hasegawa, T.; Fujimori, S.; Shin, Y.; Takahashi, K.; Masui, T.; Tanaka, A. Climate change impact and adaptation assessment on food consumption utilizing a new scenario framework. Environ. Sci. Technol. 2014, 48, 438–445. [Google Scholar] [CrossRef] [PubMed]

- Fujimori, S.; Masui, T.; Matsuoka, Y. Development of a global computable general equilibrium model coupled with detailed energy end-use technology. Appl. Energy 2014, 128, 296–306. [Google Scholar] [CrossRef]

- Fujimori, S.; Kainuma, M.; Masui, T.; Hasegawa, T.; Dai, H. The effectiveness of energy service demand reduction: A scenario analysis of global climate change mitigation. Energy Policy 2014, 75, 379–391. [Google Scholar] [CrossRef]

- Dai, H.; Silva Herran, D.; Fujimori, S.; Masui, T. Key factors affecting long-term penetration of global onshore wind energy integrating top-down and bottom-up approaches. Renew. Energy 2016, 85, 19–30. [Google Scholar] [CrossRef]

- Fujimori, S.; Masui, T.; Matsuoka, Y. Discussion Paper Series: Center for Social and Environmental Systems Research; AIM/CGE [Basic] Manual; National Institute Environmental Studies: Tsukuba, Japan, 2012; pp. 1–87. [Google Scholar]

- Namazu, M.; Fujimori, S.; Shukla, P.R.; Matsuoka, Y. Two low-carbon development pathways in India. Glob. Environ. Res. 2013, 17, 119–128. [Google Scholar]

- Namazu, M.; Fujimori, S.; Jiang, K.; Matsuoka, Y. Feasibility of low-carbon development in China. Glob. Environ. Res. 2013, 17, 109–118. [Google Scholar]

- Mittal, S.; Dai, H.; Fujimori, S.; Masui, T. Bridging greenhouse gas emissions and renewable energy deployment target: Comparative assessment of China and India. Appl. Energy 2016, 166, 301–313. [Google Scholar] [CrossRef]

- Hasegawa, T.; Fujimori, S.; Masui, T.; Matsuoka, Y. Introducing detailed land-based mitigation measures into a computable general equilibrium model. J. Clean. Prod. 2016, 114, 233–242. [Google Scholar] [CrossRef]

- Tran, T.T.; Fujimori, S.; Masui, T. Realizing the intended nationally determined contribution: The role of renewable energies in Vietnam. Energies 2016, 9, 587. [Google Scholar] [CrossRef]

- International Energy Agency (IEA). Energy Technology Perspectives 2012; International Energy Agency (IEA): Paris, France, 2012. [Google Scholar]

- Perusahaan Listrik Negara (PLN). Electricity Supply Business Plan PT Perusahaan Listrik Negara (PLN) (Persero) 2016–2025; Perusahaan Listrik Negara: Jakarta, Indonesia, 2016.

- Albino, V.; Ardito, L.; Dangelico, R.M.; Messeni Petruzzelli, A. Understanding the development trends of low-carbon energy technologies: A patent analysis. Appl. Energy 2014, 135, 836–854. [Google Scholar] [CrossRef]

- Ardito, L.; Messeni Petruzzelli, A.; Albino, V. Investigating the antecedents of general purpose technologies: A patent perspective in the green energy field. J. Eng. Technol. Manag. 2016, 39, 81–100. [Google Scholar] [CrossRef]

- Cecere, G.; Corrocher, N.; Gossart, C.; Ozman, M. Technological pervasiveness and variety of innovators in Green ICT: A patent-based analysis. Res. Policy 2014, 43, 1827–1839. [Google Scholar] [CrossRef]

- Doeo, B. Review of RAN-GRK: Materials for NDC preparation. In Proceedings of the National Meeting “Intended Nationally Determined Contributions (INDC) to Nationally Determined Contributions (NDC)”, Jakarta, Indonesia, 30 March 2016.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Energy Resource | Reserve | Resource |

|---|---|---|

| Oil, billion barrels | 7.4 | - |

| Natural gas, TSCF * | 150 | - |

| Coal, billion tons | 29 | 119 |

| CBM **, TSCF * | - | 453 |

| Shale gas, TSCF * | - | 574 |

| Potential Power | ||

| Hydro | 75,000 MW | |

| Geothermal | 29,000 MW | |

| Micro-hydro | 750 MW | |

| Biomass | 14,000 MWe | |

| Solar | 4.80 kWh/m2/day | |

| Wind | 3–6 m/s | |

| Power Plant | Baseline | CM1 | CM2 | |||

|---|---|---|---|---|---|---|

| 2020 | 2030 | 2020 | 2030 | 2020 | 2030 | |

| Coal | 18,346 | 54,855 | 15,102 | 37,171 | 14,277 | 33,217 |

| Oil | 1226 | 492 | 1191 | 464 | 1165 | 443 |

| Gas | 8606 | 20,535 | 8855 | 21,742 | 8660 | 20,795 |

| Geothermal | 851 | 863 | 2233 | 5946 | 2315 | 6394 |

| Hydropower | 1587 | 1610 | 3478 | 7732 | 3560 | 8102 |

| Other RE | 1098 | 2068 | 472 | 2896 | 195 | 1719 |

| Total | 31,714 | 80,423 | 31,331 | 75,950 | 30,172 | 70,670 |

| Scenario | NDC–Energy Sector | Present Study | ||||

|---|---|---|---|---|---|---|

| Emission in 2030 MtCO2e | Reduction from Baseline | Emission in 2030 MtCO2e | Reduction from Baseline | |||

| MtCO2e | % | MtCO2e | % | |||

| Baseline | 1444 | - | - | 1403 | - | - |

| Unconditional (CM1) | 1191 | 253 | 17.5% | 1193 | 216 | 15.4% |

| Conditional (CM2) | 972 | 472 | 32.7% | 1026 | 383 | 27.2% |

© 2017 by the authors; licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC-BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Siagian, U.W.R.; Yuwono, B.B.; Fujimori, S.; Masui, T. Low-Carbon Energy Development in Indonesia in Alignment with Intended Nationally Determined Contribution (INDC) by 2030. Energies 2017, 10, 52. https://doi.org/10.3390/en10010052

Siagian UWR, Yuwono BB, Fujimori S, Masui T. Low-Carbon Energy Development in Indonesia in Alignment with Intended Nationally Determined Contribution (INDC) by 2030. Energies. 2017; 10(1):52. https://doi.org/10.3390/en10010052

Chicago/Turabian StyleSiagian, Ucok W.R., Bintang B. Yuwono, Shinichiro Fujimori, and Toshihiko Masui. 2017. "Low-Carbon Energy Development in Indonesia in Alignment with Intended Nationally Determined Contribution (INDC) by 2030" Energies 10, no. 1: 52. https://doi.org/10.3390/en10010052

APA StyleSiagian, U. W. R., Yuwono, B. B., Fujimori, S., & Masui, T. (2017). Low-Carbon Energy Development in Indonesia in Alignment with Intended Nationally Determined Contribution (INDC) by 2030. Energies, 10(1), 52. https://doi.org/10.3390/en10010052