Int. J. Financial Stud. 2024, 12(2), 55; https://doi.org/10.3390/ijfs12020055 - 6 Jun 2024

Abstract

The Constant Leverage covering strategy for the equity momentum portfolio (CLvg) developed in this project cannot mask its shortcomings by increasing leverage. It has to successfully forecast and avoid more losses than profits to perform better than the momentum portfolio. This approach is

[...] Read more.

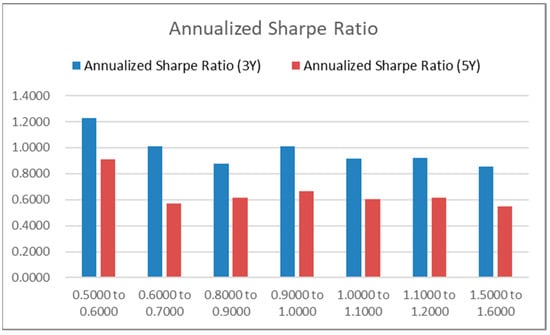

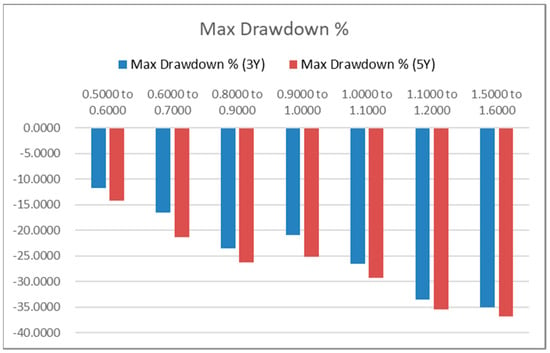

The Constant Leverage covering strategy for the equity momentum portfolio (CLvg) developed in this project cannot mask its shortcomings by increasing leverage. It has to successfully forecast and avoid more losses than profits to perform better than the momentum portfolio. This approach is different from other covering strategies available in the literature that focus on increasing the right tail of the momentum returns distribution at a faster rate than they increase the left tail. The CLvg strategy only depends on past information and uses the daily volatility of the loser portfolio to determine episodes of high and low volatility. The daily volatility of the loser portfolio has a stronger relationship with large negative momentum returns than the daily volatility of the momentum portfolio. The daily volatility of the loser portfolio also has a weaker relationship with larger positive monthly returns, and it is more predictable because it has a higher volatility persistence. The negative effects of transaction costs on the CLvg strategy are measured using bid and ask prices reported by CRSP from 1992 to 2021. During this period, the stock market presented an average excess return of 9.19% and a Sharpe ratio of 0.61, and 9.74% of its returns were crashes, which is a better performance than the momentum portfolio. The CLvg adjusted by transaction costs presented excess returns of 16.93% and a Sharpe ratio of 0.84, and only 8.31% of its returns were crashes.

Full article

(This article belongs to the Special Issue Accounting and Financial/Non-financial Reporting Developments)

►

Show Figures

Figure 1

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}