1. Introduction

The construction industry provides multiple benefits beyond infrastructural development [

1]. Not only does it boost the economy of a country, but it also creates a sustainable job market at every level [

2,

3]. The construction industry is also responsible for the integration of new technologies and guarding the environment [

4,

5]. Despite the numerous benefits of this sector, the construction industry still faces a multitude of challenges in project deliverables that reduce project productivity, efficiency, sustainability, and inclusive development [

6,

7,

8]. One of the key problems is the overbudgeting of construction projects, which ultimately overburden the client’s finances [

9]. This overbudgeting occurs when the estimated cost exceeds the final closure cost. Overall globally in construction projects, the budget deviation ranges between 5% and 10% [

10,

11]. Several factors contribute to the overbudgeting of a construction project and cause financial setbacks, e.g., wrong estimation [

12], change order, vague project scope [

13], inflation [

14], and unforeseen conditions [

15]. Moreover, project delays also escalate the construction goods and services cost, which burdens the budget [

16,

17]. The construction goods and services costs change with the time in which the role of inflation is not barred [

18,

19].

The impact of inflation is either direct or indirect on the construction industry [

20,

21]. Inflation not only has an impact on the Construction Price Index (CPI), but it also influences construction and other services [

22]. The rise in inflation occurs when the cost of raw materials also increases in the market [

23,

24]. Materials are the fundamental elements for construction projects, and an increase in their prices directly influences the CPI. Inflation also elevates the labor wages to meet living expenses. Such inputs reflect an upward trend in CPI, which makes construction projects costly in general. The CPI is indirectly influenced by inflation as well due to adjustments in the interest rates [

25,

26]. The increase in inflation triggers the alarm in central banks, which then causes a rise in interest rates to maintain the economic threshold. Higher interest rates boost construction projects, deriving costs and ultimately overburdening financial costs [

14]. This behavior adds an additional layer of cost to the project budget through CPI. As a result, more funds are needed to meet the basic demands of the construction projects. In a nutshell, the direct influence of inflation is through materials, labor, and machinery rates increases, and the indirect rate is through the interest rate [

27,

28].

With the help of the Scopus database [

29], the keywords (“Inflation”, AND “Construction”, AND “Cost overrun”) were searched to feature the recent trend and linkage of the literature, which can be seen in

Figure 1. It is obvious from the output that inflation in recent times is the thrust of the research, which is connected with budget control and construction projects and shows a relationship with cost overrun. In fact, inflation is the key indicator that impacts project costs by deviating them over time. Cost overrun through inflation is a global worry, and several studies have highlighted concerns about unsuccessful project completion due to overbudgeting. The literature underlines that this issue pertains to all the regions, either developing or developed, and the construction industry of all the countries is suffering [

11,

15,

30,

31,

32,

33,

34,

35,

36,

37,

38,

39,

40,

41,

42,

43,

44,

45,

46,

47,

48,

49]. Based on the carried-out literature,

Figure 2 shows the world map highlighted with some of the regions marked with red in which the budget deviated from the original cost due to the inflation rate and ultimately led to project overbudgeting.

Jiang, Xu [

50] emphasized construction prices’ reliable prediction as it impacts the decision-making of the contractors and the financiers. The long-run construction prices are dependent on the interest rate, population, and country’s income, while short-run construction prices are dependent on the price itself and the population. In this manner, the vector error correction (VEC) model was used to predict construction prices. The results indicate that, with the help of dummy variables, the forecasting is more efficient for the construction prices. The study showed promising results; however, instead of the dummy variables, the real-time data would be more promising. In another study, Shiha, Dorra [

51] utilized a neural networks model to make the predictions of construction prices with the help of macroeconomic indicators. The model selection was based on mean absolute percentage error ranging from 4% to 11%. There were several limitations in the study, such as selection of the indicators and validation of the models, that leave a study gap for the future. Elfahham [

52] draws a comparison between time series analysis, neural networks, and regression models to forecast construction cost indexes. Based on means absolute error and means squared error, it was observed that by using autoregressive time series, the outcome is better in comparison to the other two used methods for prediction.

Inflation in the economy portrays an expansion in prices, which is why it becomes essential to monitor the price shift [

53]. So far, it is evident that inflation has ruined the mode of construction [

53], and Thailand’s construction industry is also responding in the same manner as other countries’ construction industries [

54]. In 2022, Thailand’s construction market value reached

$23.7 billion, and a 3% growth is expected in the next four years [

55]. The Thailand construction industry is facing several challenges; cost overrun is the major one, hindering the overall sustainable growth of the industry. The major influential factor that triggers this problem is inflation, which changes the prices of goods and services required for construction projects.

One main aspect that was not considered in previous studies is the inflation rate impact on the deviation of the construction price index. Musarat, Alaloul [

56] explored this issue where the impact of the inflation rate was utilized to forecast the construction rates by using the time series analysis; however, the results were limited to the Malaysian industry and could further be extended to the other ASEAN regions to draw a comparison. Although the study methodology is aligned with the current work, this study focuses on the construction prices index rather than the construction rates that have not been addressed previously by adapting the time series analysis. Thus, this study stacks the focus on inflation mobility’s impact on the CPI over time. The CPI is important to estimate the cost and set up the budget before the bidding process. It is one of the key indicators of the cost level, leveling up the value for experts to understand the construction industry environment [

57,

58,

59,

60]. Hence, the CPI prediction is essential to boost the construction industry’s performance [

52,

61]. Currently, no such study is available for Thailand’s construction industry to incorporate the CPI in budgeting upon evaluating a relationship with inflation. Hence, the objective of this study is to evaluate the behavior of CPIs with time and assess the impact of inflation on shifting performance. Four CPIs were taken into consideration for further analysis, which are All Commodities, Lumber and Wood Products, Cement, and Iron Products. Moreover, time series analysis was opted to predict the future price indexes. The inflation issue requires vital attention in altering the construction price indexes that can be adapted initially at the time of contract allotment, which is the focus of this study. Besides inflation impact, there could be other possible reasons for the construction price deviation that led to project cost overrun, e.g., supply and demand, economic conditions, government policies, raw material prices, oil prices, and global market trends, etc.

Looking into the objectives, the following research questions were established:

Do CPIs show any deviations in Thailand’s construction industry?

Does inflation have any correlation with the CPIs in Thailand’s construction industry?

Does Automated Autoregressive Integrated Moving Average (ARIMA) provide significant forecasting of CPIs?

The argument of this study is not based on low or high inflation in any country; rather it focuses on how the inflation rate deviates the prices in the construction market, which ultimately leads to cost overrun of a construction project. The scope of this study was limited to exploring the relationship between inflation and CPI in Thailand’s construction industry. The literature also supports auto machine learning [

62]; however, this study utilized automated ARIMA forecasting, which has shown promising forecasting results for construction elements in the past [

56]. Also, for the prediction of four CPIs, only the ARIMA model of time series analysis was considered without making any comparisons with other existing models due to the fact that the focus was kept on developing a strategy to make CPIs adjustments in the budget rather than drawing the comparison among the model for better predictions. Moreover, within the ARIMA model, there are several runs that give the best-suited value combination for the predictions. This study will help construction industry practitioners understand the seriousness of the matter and choose the outcome that will increase project productivity.

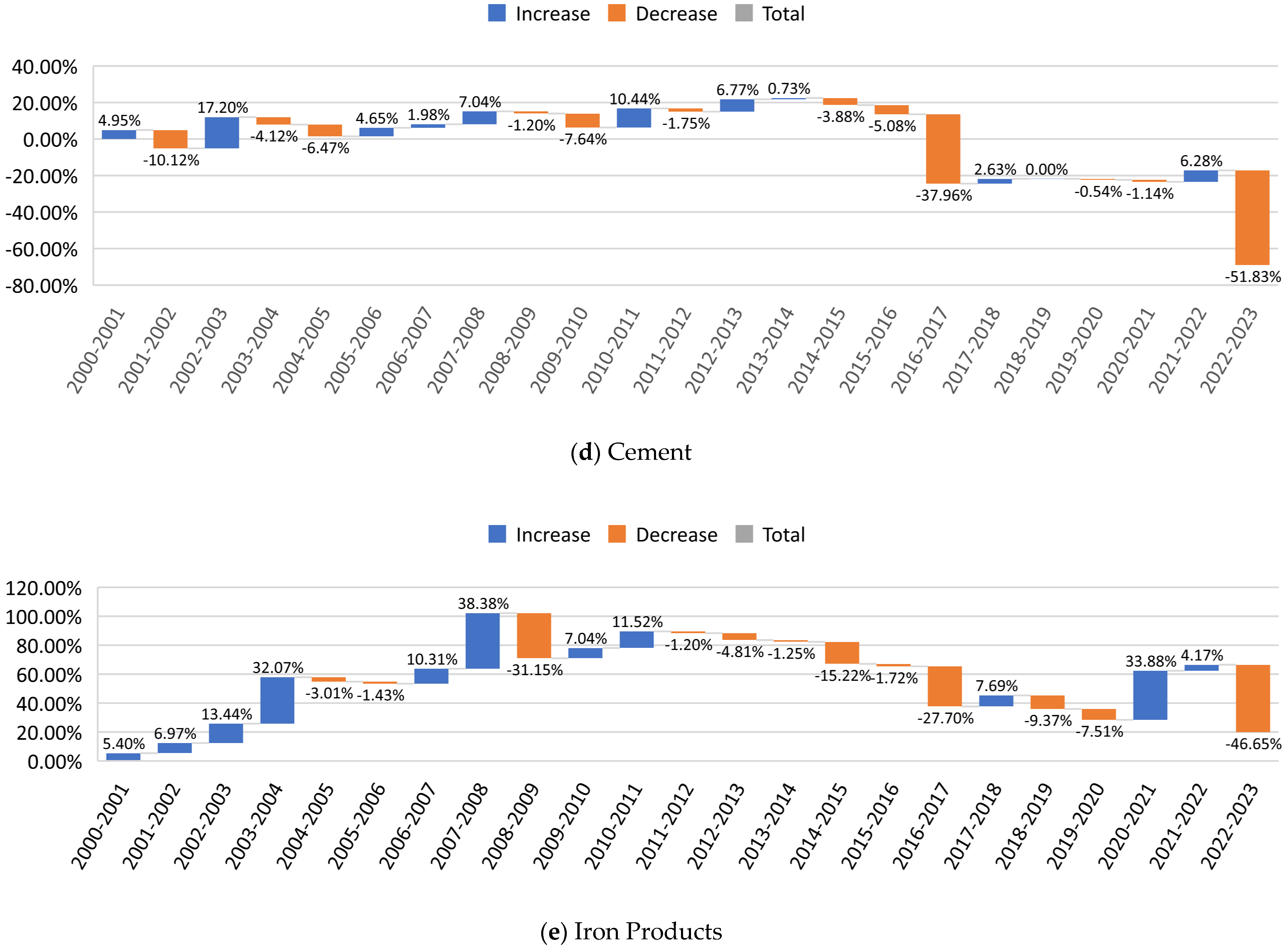

4. Conclusions

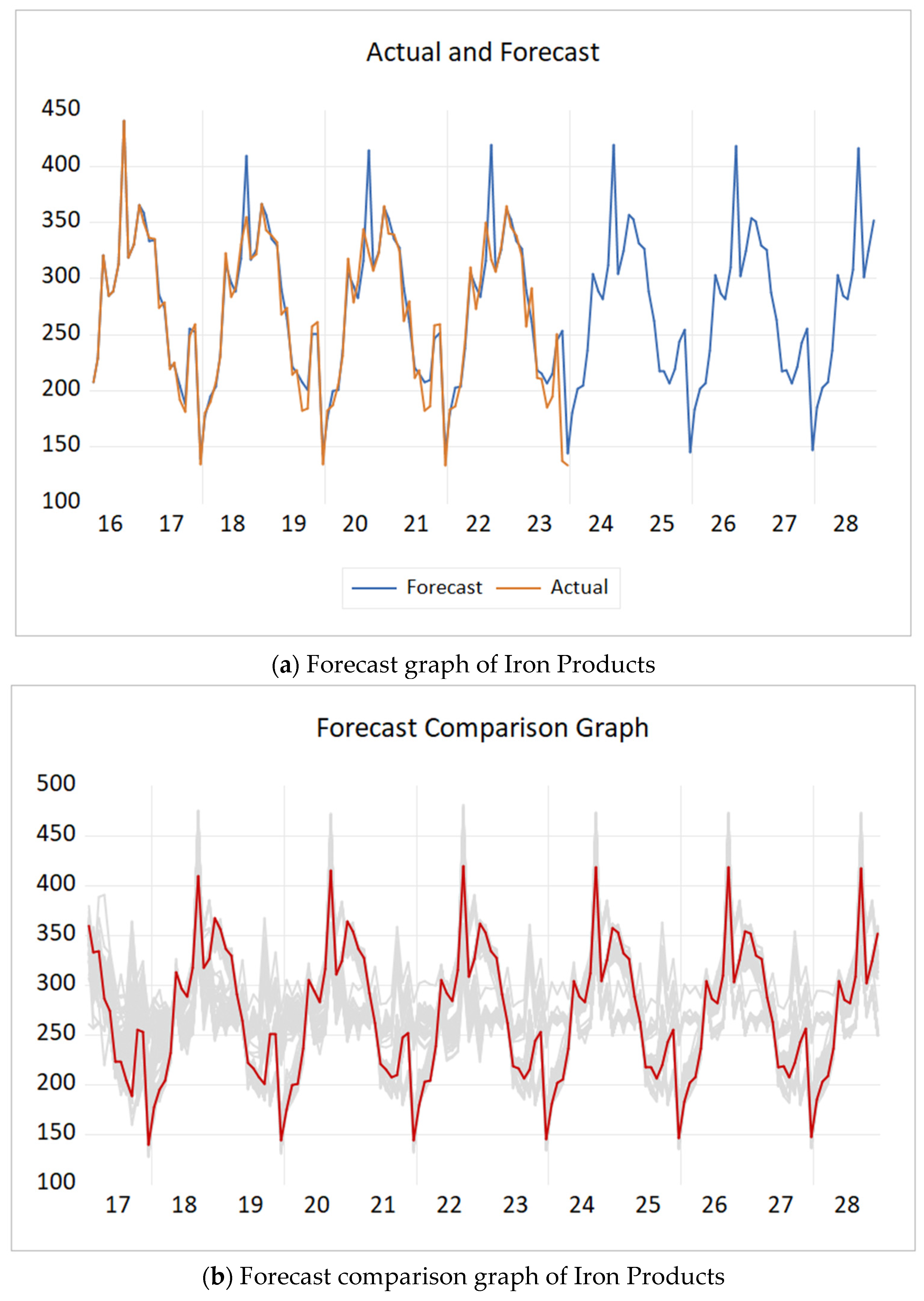

The construction price index (CPI) is the key indicator of the cost estimate as it helps to set up the project budget wisely. However, over time, the CPI becomes elevated, and the fluctuating behavior is unfavorable for all construction practitioners. Hence, this study focuses on evaluating the changing behavior of CPIs with the inflation effect and the prediction of CPIs to overcome the project overbudgeting problem. Four CPIs, i.e., All Commodities, Lumber and Wood Products, Cement and Iron Products, were deemed dependent, whereas inflation was independent. Initially, descriptive analysis, percentage deviation, and correlation coefficient were computed. The deviation showed that the data behavior was nonconsistent and the indexes changed over time, while the correlation coefficient showed a significant relationship between inflation and Iron Products price indexes. After evaluating the correlation, ARIMA forecasting was performed to predict construction price indexes. Inflation as an independent variable was considered for Iron Products price indexes only, whereas a seasonal pattern showed up for Cement and Iron Products. In contrast, for All Commodities and Lumber and Wood Products, the data did not show any specific pattern. This study gives a predicted value for all the CPIs that can be considered for budget adjustments before the time of contract allotment, which will help construction practitioners reduce the cost overrun impact due to price deviation. The forecasted values show the pattern in the coming years that can be considered at the initial budgeting time to avoid over-budgeting.

5. Implications and Limitations

This study provides the prediction of CPI based on the impact of inflation on the construction industry of Thailand. As a theoretical implication, this study clarifies the need for CPI prediction with inflation adjustment. As a practical implication, the formulated strategy can help construction industry practitioners make necessary adjustments. This prediction will help in making modifications at contract time to avoid the cost overrun effects. The predictions will also help to present the best-suited project budget at the time of bidding. This will reduce the impact of cost deviation from the initial budget to the final budget and will reduce the burden on the financiers. Although, as a case study, the data from the Thailand construction industry was analyzed, it can be implicated in other regions’ construction industries as well by keeping the impact of influential factors such as the inflation rate. Further, the results are useful for other ASEAN countries as well, as they have similarities in construction industry characteristics due to their close geographical proximity, interconnected economies, and comparable stages of development.

Some limitations occurred while pursuing this study. The data was taken from 2000 to 2023, and for a better understanding of its behavior, the observations could be increased. Only four categories were taken into account for construction price indexes. Other individual categories need vital attention to study the data behavior more precisely. Automated ARIMA forecasting was implemented on the gathered data. However, other techniques such as ANN, CNN, or AI tools could also be utilized to predict the construction price indexes. Lastly, in this study, inflation was considered as the independent variable; however, other factors may also be measured in the future in order to evaluate the influential relationship with construction price indexes.

,

,

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}