- Article

Bayesian Causal Inference for Credit Default Risk

- Sello Dalton Pitso and

- Taryn Michael

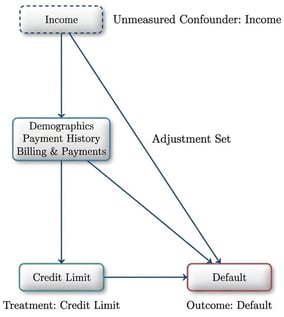

Banks often assume that higher credit limits increase customer default risk because greater exposure appears to imply greater vulnerability. This reasoning, however, conflates correlation with causation. Whether increasing a customer’s credit limit truly raises the likelihood of default remains an open empirical question that this work seeks to answer. We applied Bayesian causal inference to estimate the causal effect of credit limits on default probability. The analysis incorporated Directed Acyclic Graphs (DAGs) for causal structure, d-separation for identification, and Bayesian logistic regression using a dataset of 30,000 credit card holders in Taiwan (April–September 2005). Twenty-two confounding variables were adjusted for, covering demographics, repayment history, and billing and payment behavior. Continuous covariates were standardized, and posterior inference was performed using NUTS sampling with posterior predictive simulations to compute Average Treatment Effects (ATEs). We found that a one-standard-deviation increase in credit limit reduces default probability by 1.44 percentage points (94% HDI: [−2.0%, −1.0%]), corresponding to a 6.3% relative decline from the baseline default rate of 22.1%. The effect was consistent across demographic subgroups, with homogeneous treatment effects observed for age, education, and gender categories, and remained robust under sensitivity analysis addressing potential unmeasured confounding. The findings suggest that increasing credit limits can causally reduce default risk, likely by enhancing financial flexibility and lowering utilization ratios. These results have practical implications for credit policy design and motivate further investigation into mechanisms and applicability across broader lending environments. These estimates are explicitly interpreted as context-specific causal effects for a pre-crisis consumer credit environment, with external validity assessed conceptually rather than assumed.

12 February 2026