Economies 2024, 12(5), 122; https://doi.org/10.3390/economies12050122 (registering DOI) - 17 May 2024

Abstract

This study examines the relationship between the business sentiment of Japanese companies regarding promising or potential countries for investment and macroeconomic statistics, such as economic or population growth in Thailand, using data from the Survey Report on Overseas Business Operations by Japanese Manufacturing

[...] Read more.

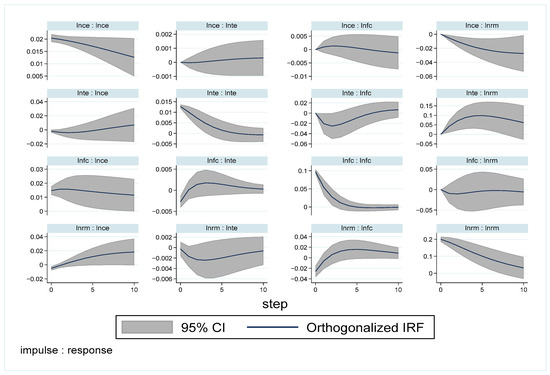

This study examines the relationship between the business sentiment of Japanese companies regarding promising or potential countries for investment and macroeconomic statistics, such as economic or population growth in Thailand, using data from the Survey Report on Overseas Business Operations by Japanese Manufacturing Companies from 1992 to 2022. Although investing in Thailand has been popular among Japanese companies since the late 1980s, it has seemingly become relatively inactive in recent years. The present study’s results are summarized as follows: First, the business sentiment of Japanese companies has some relationships with relatively short-term economic growth and the business cycle in the short run. Second, business sentiment depends on long-term trends, and this stance may have changed after 2020. Third, other elements, such as minimum wage or fewer young people, do not necessarily have a relationship with business sentiment. Although more studies including capital accumulation or the global value chain should be conducted, improving the sentiments of Japanese businesspersons is desirable.

Full article

(This article belongs to the Special Issue The Asian Economy: Constraints and Opportunities)

►

Show Figures

Figure 1

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}