Can Environmental Information Disclosure Improve Energy Efficiency in Manufacturing? Evidence from Chinese Enterprises

Abstract

1. Introduction

2. Policy Background and Research Hypothesis

2.1. Policy Background

2.2. Research Hypothesis

3. Methodology and Data

3.1. Data Source

3.2. Variable Definition

3.2.1. Explained Variable

3.2.2. Explanatory Variable

3.2.3. Mechanism Variables

3.2.4. Control Variables

3.3. Econometrics Model

4. Empirical Results

4.1. Basical Result

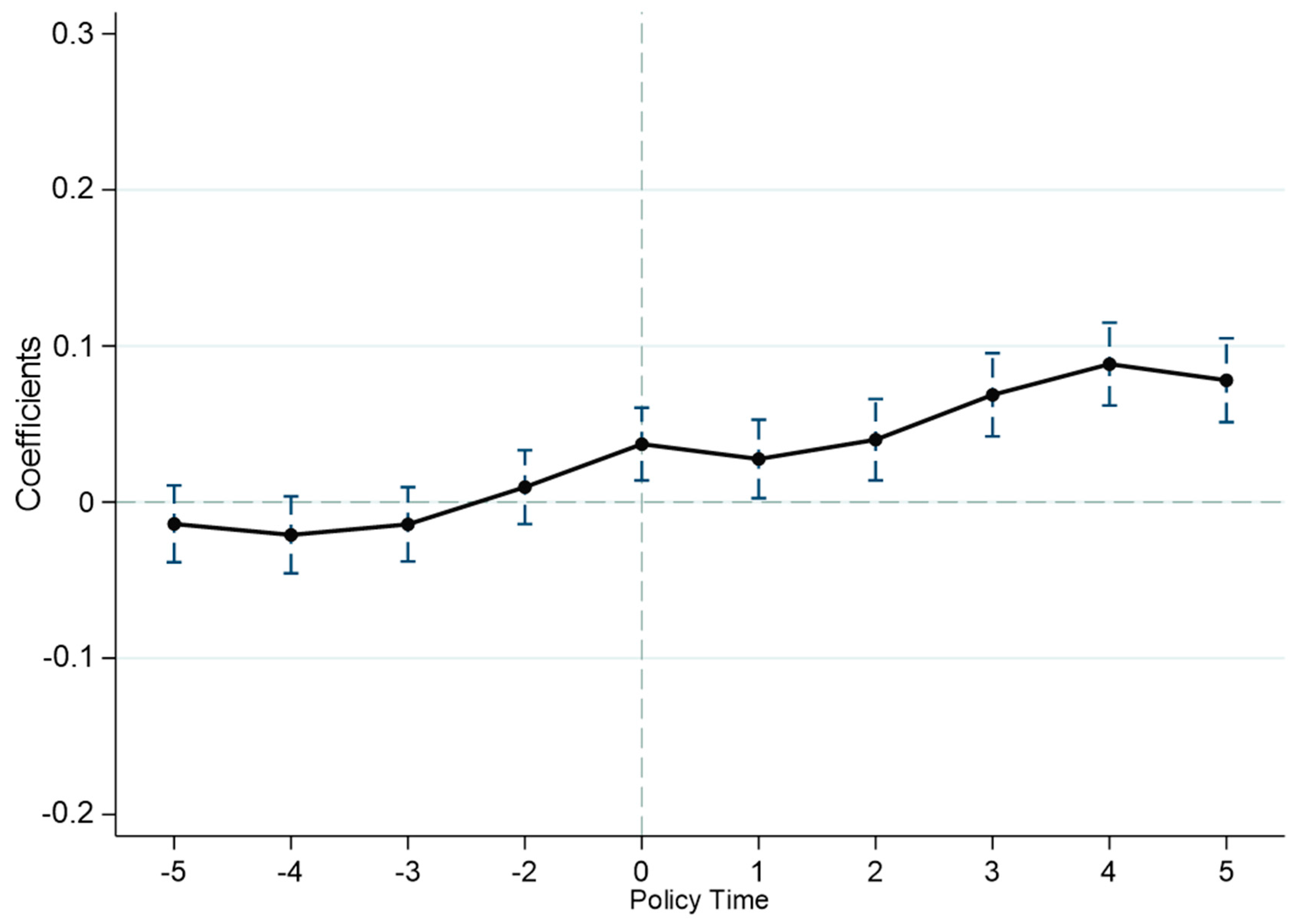

4.2. Parallel Trend Result

4.3. Robustness Test

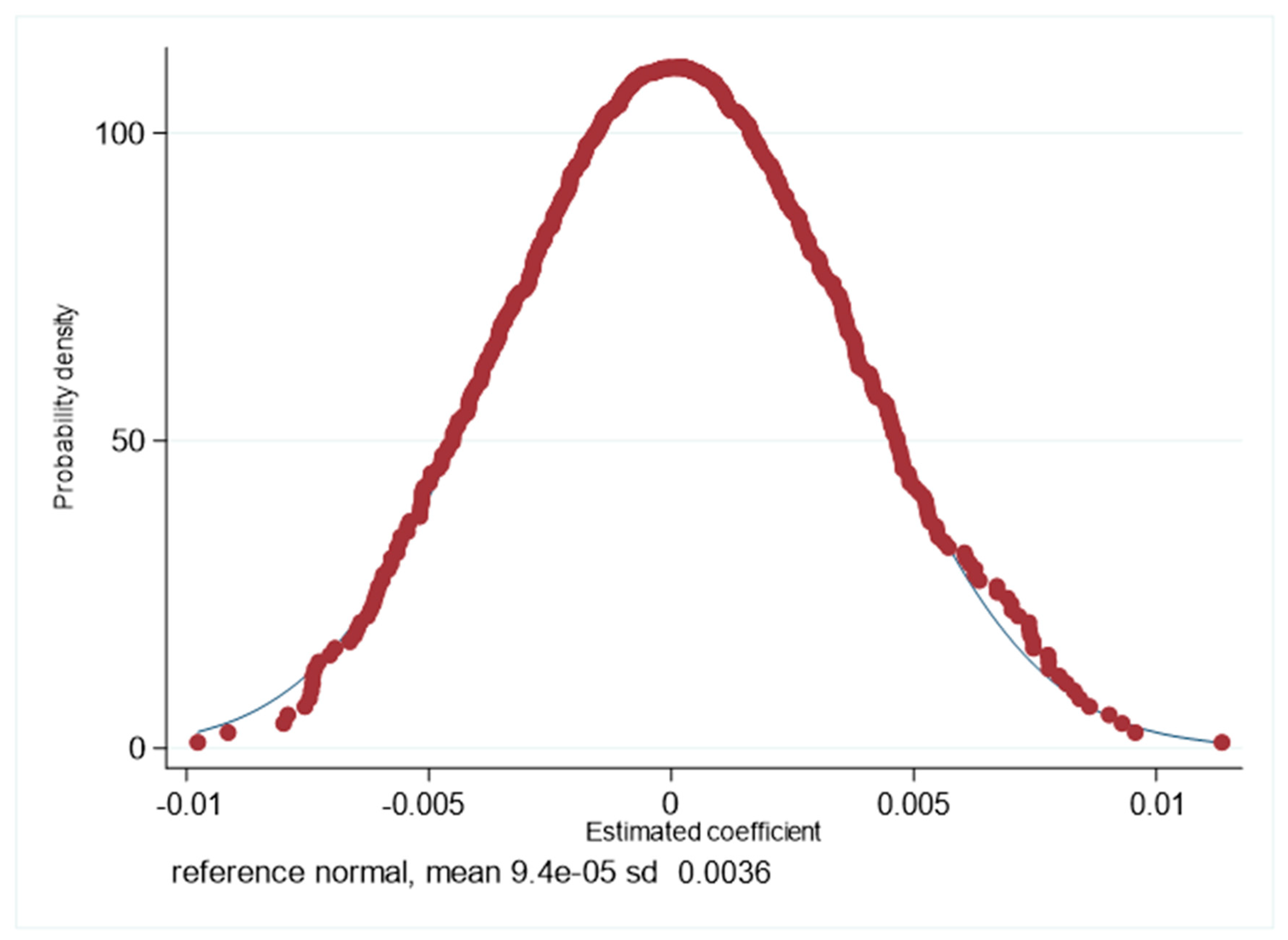

4.3.1. Placebo Test

4.3.2. A Series of Robustness Tests

5. Further Discussion

5.1. Mechanism Analysis

5.2. Heterogeneity Analysis

5.2.1. Regional Heterogeneity

5.2.2. Enterprise-Type Heterogeneity

6. Conclusions and Policy Implications

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Wang, Z.; Wang, X. Research on the impact of green finance on energy efficiency in different regions of China based on the DEA-Tobit model. Resour. Policy 2022, 77, 102695. [Google Scholar] [CrossRef]

- Gao, D.; Zhou, X.; Wan, J. Unlocking sustainability potential: The impact of green finance reform on corporate ESG performance. Corp. Soc. Responsib. Environ. Manag. 2024. [Google Scholar] [CrossRef]

- Gao, D.; Feng, H.; Cao, Y. The spatial spillover effect of innovative city policy on carbon efficiency: Evidence from China. Singap. Econ. Rev. 2024. [Google Scholar] [CrossRef]

- Li, G.; Gao, D.; Shi, X.X. How does information and communication technology affect carbon efficiency? Evidence at China’s city level. Energy Environ. 2023. [Google Scholar] [CrossRef]

- Zhang, J.; Patwary, A.K.; Sun, H.; Raza, M.; Taghizadeh-Hesary, F.; Iram, R. Measuring energy and environmental efficiency interactions towards CO2 emissions reduction without slowing economic growth in central and western Europe. J. Environ. Manag. 2021, 279, 111704. [Google Scholar] [CrossRef]

- Zhang, Y.; Song, Y. Environmental regulations, energy and environment efficiency of China’s metal industries: A provincial panel data analysis. J. Clean. Prod. 2021, 280, 124437. [Google Scholar] [CrossRef]

- Looney, B. Statistical review of world energy, 2020. Bp 2020, 69, 66. [Google Scholar]

- Wu, H.; Xu, L.; Ren, S.; Hao, Y.; Yan, G. How do energy consumption and environmental regulation affect carbon emissions in China? New evidence from a dynamic threshold panel model. Resour. Policy 2020, 67, 101678. [Google Scholar] [CrossRef]

- Li, B.; Han, Y.; Wang, C.; Sun, W. Did civilized city policy improve energy efficiency of resource-based cities? Prefecture-level evidence from China. Energy Policy 2022, 167, 113081. [Google Scholar] [CrossRef]

- Bu, C.; Zhang, K.; Shi, D.; Wang, S. Does environmental information disclosure improve energy efficiency? Energy Policy 2022, 164, 112919. [Google Scholar] [CrossRef]

- Gao, D.; Li, Y.; Tan, L. Can environmental regulation break the political resource curse: Evidence from heavy polluting private listed companies in China. J. Environ. Plan. Manag. 2023, 1–27. [Google Scholar] [CrossRef]

- Jiang, L.; Zhou, H.; He, S. Does energy efficiency increase at the expense of output performance: Evidence from manufacturing firms in Jiangsu province, China. Energy 2021, 220, 119704. [Google Scholar] [CrossRef]

- Liu, Y.; Fan, H.; Wei, X. Pollution charges and firms’ energy efficiency: Evidence from a quasi-natural experiment in China. Appl. Econ. 2023, 1–18. [Google Scholar] [CrossRef]

- Mandal, S.K. Do undesirable output and environmental regulation matter in energy efficiency analysis? Evidence from Indian cement industry. Energy Policy 2010, 38, 6076–6083. [Google Scholar] [CrossRef]

- Tone, K. A slacks-based measure of efficiency in data envelopment analysis. Eur. J. Oper. Res. 2001, 130, 498–509. [Google Scholar] [CrossRef]

- Wu, H.; Hao, Y.; Ren, S. How do environmental regulation and environmental decentralization affect green total factor energy efficiency: Evidence from China. Energy Econ. 2020, 91, 104880. [Google Scholar] [CrossRef]

- Wu, C.Q.; Zheng, K.Y. The measurement of total factor energy efficiency of cities in the Yangtze River Economic Belt and its influencing factors: Based on the Super-MSBM model. J. Jiangxi Norm. Univ. (Philos. Soc. Sci. Ed.) 2020, 53, 56–66. [Google Scholar]

- Wang, Y.; Deng, X.; Zhang, H.; Liu, Y.; Yue, T.; Liu, G. Energy endowment, environmental regulation, and energy efficiency: Evidence from China. Technol. Forecast. Soc. Chang. 2022, 177, 121528. [Google Scholar] [CrossRef]

- Xie, R.H.; Yuan, Y.J.; Huang, J.J. Different types of environmental regulations and heterogeneous influence on “green” productivity: Evidence from China. Ecol. Econ. 2017, 132, 104–112. [Google Scholar] [CrossRef]

- Xu, B.; Xu, R. Assessing the role of environmental regulations in improving energy efficiency and reducing CO2 emissions: Evidence from the logistics industry. Environ. Impact Assess. Rev. 2022, 96, 106831. [Google Scholar] [CrossRef]

- Gray, W.B. The cost of regulation: OSHA, EPA and the productivity slowdown. Am. Econ. Rev. 1987, 77, 998–1006. [Google Scholar]

- Li, X.; Liu, C.; Weng, X.; Zhou, L.A. Target setting in tournaments:Theory and evidence from China. Econ. J. 2019, 129, 2888–2915. [Google Scholar] [CrossRef]

- Porter, M.E.; Van der Linde, C. Toward a new conception of the environment-competitiveness relationship. J. Econ. Perspect. 1995, 9, 97–118. [Google Scholar] [CrossRef]

- Guo, R.; Yuan, Y. Different types of environmental regulations and heterogeneous influence on energy efficiency in the industrial sector: Evidence from Chinese provincial data. Energy Policy 2020, 145, 111747. [Google Scholar] [CrossRef]

- Dirckinck-Holmfeld, K. The options of local authorities for addressing climate change and energy efficiency through environmental regulation of companies. J. Clean. Prod. 2015, 98, 175–184. [Google Scholar] [CrossRef]

- Hancevic, P.I. Environmental regulation and productivity: The case of electricity generation under the CAAA-1990. Energy Econ. 2016, 60, 131–143. [Google Scholar] [CrossRef]

- Gollop, F.M.; Roberts, M.J. Environmental regulations and productivity growth: The case of fossil-fueled electric power generation. J. Political Econ. 1983, 91, 654–674. [Google Scholar] [CrossRef]

- Bi, G.; Luo, Y.; Ding, J.; Liang, L. Environmental performance analysis of Chinese industry from a slacks-based perspective. Ann. Oper. Res. 2015, 228, 65–80. [Google Scholar] [CrossRef]

- Zhang, B.; Chen, X.; Guo, H. Does central supervision enhance local environmental enforcement? Quasi-experimental evidence from China. J. Public Econ. 2018, 164, 70–90. [Google Scholar] [CrossRef]

- Zhang, H.; Xu, T.; Feng, C. Does public participation promote environmental efficiency? Evidence from a quasi-natural experiment of environmental information disclosure in China. Energy Econ. 2022, 108, 105871. [Google Scholar] [CrossRef]

- Bi, G.B.; Song, W.; Zhou, P.; Liang, L. Does environmental regulation affect energy efficiency in China’s thermal power generation? Empirical evidence from a slacks-based DEA model. Energy Policy 2014, 66, 537–546. [Google Scholar] [CrossRef]

- Pan, X.; Ai, B.; Li, C.; Pan, X.; Yan, Y. Dynamic relationship among environmental regulation, technological innovation and energy efficiency based on large scale provincial panel data in China. Technol. Forecast. Soc. Chang. 2019, 144, 428–435. [Google Scholar] [CrossRef]

- Jacobson, L.S.; LaLonde, R.J.; Sullivan, D.G. Earnings losses of displaced workers. Am. Econ. Rev. 1993, 83, 685–709. [Google Scholar]

- Liu, H.; Zhang, Z.; Zhang, T.; Wang, L. Revisiting China’s provincial energy efficiency and its influencing factors. Energy 2020, 208, 118361. [Google Scholar] [CrossRef]

- Yang, Z.; Wang, D.; Du, T.; Zhang, A.; Zhou, Y. Total-factor energy efficiency in China’s agricultural sector: Trends, disparities and potentials. Energies 2018, 11, 853. [Google Scholar] [CrossRef]

- Cai, X.; Lu, Y.; Wu, M.; Yu, L. Does environmental regulation drive away inbound foreign direct investment? Evidence from a quasi-natural experiment in China. J. Dev. Econ. 2016, 123, 73–85. [Google Scholar] [CrossRef]

- Liu, Z.; Huang, H. Research on China’s provincial energy efficiency and its influencing factors—SFA model based on Shephard energy distance function. J. Nanjing Univ. Financ. Econ. 2019, 1, 99–108. [Google Scholar]

- Li, G.; Xue, Q.; Qin, J. Environmental information disclosure and green technology innovation: Empirical evidence from China. Technol. Forecast. Soc. Chang. 2022, 176, 121453. [Google Scholar] [CrossRef]

- Ding, J.; Lu, Z.; Yu, C.H. Environmental information disclosure and firms’ green innovation: Evidence from China. Int. Rev. Econ. Financ. 2022, 81, 147–159. [Google Scholar] [CrossRef]

- Beck, T.; Levine, R.; Levkov, A. Big bad banks? The winners and losers from bank deregulation in the United States. J. Financ. 2010, 65, 1637–1667. [Google Scholar] [CrossRef]

- Porter, M.E. Towards a dynamic theory of strategy. Strateg. Manag. J. 1991, 12, 95–117. [Google Scholar] [CrossRef]

- Jiang, W.; Li, R.; Qiang, L.F.; Wu, Y.M. Research on China’s energy efficiency under environmental constraints. Acc. Inf. Forum 2015, 5, 22–28. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

| VarName | Obs | Mean | SD | Min | Max |

|---|---|---|---|---|---|

| Firm GTFEE | 155,237 | 0.02 | 0.05 | 0.000 | 1.000 |

| Firm age | 155,237 | 2.39 | 0.73 | 0.000 | 7.606 |

| Whether state-owned firm | 155,237 | 0.11 | 0.32 | 0.000 | 1.000 |

| Whether export firm | 155,237 | 0.45 | 0.50 | 0.000 | 1.000 |

| Firm assets | 155,237 | 10.84 | 1.24 | 6.953 | 15.957 |

| Firm asset-liability ratio | 155,237 | 0.60 | 0.32 | 1.104 | 15.116 |

| Total profits | 155,237 | 5.23 | 6.73 | −13.817 | 15.878 |

| R&D expenditure | 155,237 | 0.86 | 2.17 | 0.000 | 12.161 |

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| Variables | GTFEE | GTFEE | GTFEE | GTFEE |

| EID | 0.050 *** | 0.048 *** | 0.032 *** | 0.030 *** |

| (6.233) | (6.197) | (4.051) | (4.011) | |

| _cons | 4.365 *** | 4.316 *** | 2.119 *** | 2.131 *** |

| (6.301) | (3.794) | (2.835) | (2.155) | |

| Control | N | N | Y | Y |

| Firm FE | N | Y | N | Y |

| Year FE | N | Y | N | Y |

| City FE | Y | Y | Y | Y |

| Industry FE | Y | Y | Y | Y |

| N | 155,237 | 155,237 | 155,237 | 155,237 |

| Adj-R2 | 0.391 | 0.312 | 0.556 | 0.617 |

| (1) Advancing the Policy Year | (2) Replacing the Single-Factor Energy Efficiency | (3) Excluding the Four Municipalities’ Sample | (4) Expanding the Sample Interval | |

|---|---|---|---|---|

| EID_adv | 0.021 | |||

| (0.857) | ||||

| EID | 0.034 ** | 0.032 *** | 0.035 *** | |

| (2.569) | (3.964) | (4.517) | ||

| Control | Y | Y | Y | Y |

| Firms FE | Y | Y | Y | Y |

| Year FE | Y | Y | Y | Y |

| City FE | Y | Y | Y | Y |

| Industry FE | Y | Y | Y | Y |

| N | 155,237 | 155,237 | 155,237 | 155,237 |

| Adj-R2 | 0.514 | 0.586 | 0.618 | 0.543 |

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| Variables | Coal | Coal | Clean Gas | Clean Gas | Technology Innovation | Technology Innovation |

| EID | −0.025 ** | −0.022 ** | 0.066 ** | 0.058 ** | 0.065 ** | 0.060 ** |

| (−2.265) | (−1.972) | (2.408) | (2.506) | (1.990) | (1.970) | |

| _cons | 7.284 *** | 5.499 *** | 0.125 *** | 1.159 ** | 1.808 *** | 1.893 *** |

| (3.504) | (2.904) | (2.125) | (1.359) | (2.054) | (2.322) | |

| Control | N | Y | N | Y | N | Y |

| Firm FE | Y | Y | Y | Y | Y | Y |

| Year FE | Y | Y | Y | Y | Y | Y |

| City FE | Y | Y | Y | Y | Y | Y |

| Industry FE | Y | Y | Y | Y | Y | Y |

| N | 155,237 | 155,237 | 155,237 | 155,237 | 155,237 | 155,237 |

| Adj-R2 | 0.206 | 0.307 | 0.152 | 0.252 | 0.453 | 0.563 |

| (1) | (2) | (3) | |

|---|---|---|---|

| Eastern | Central | Western | |

| EID | 0.049 *** | 0.032 * | 0.060 |

| (4.555) | (1.758) | (1.452) | |

| _cons | 2.407 *** | 1.701 *** | 2.054 *** |

| (3.244) | (1.035) | (1.412) | |

| Control | Y | Y | Y |

| Firms FE | Y | Y | Y |

| Year FE | Y | Y | Y |

| City FE | Y | Y | Y |

| Industry FE | Y | Y | Y |

| N | 93,921 | 38,011 | 23,305 |

| Adj-R2 | 0.612 | 0.417 | 0.598 |

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| State-Owned | Export | High Consumption | Polluting | |

| EID | 0.045 *** | 0.031 *** | 0.075 *** | −0.279 *** |

| (5.413) | (3.520) | (8.335) | (−8.069) | |

| EID × State owned | −0.144 *** | |||

| (−8.030) | ||||

| EID × Export | 0.022 ** | |||

| (1.987) | ||||

| EID × High cons | −0.091 *** | |||

| (−10.820) | ||||

| EID × Polluting | 0.318 *** | |||

| (9.261) | ||||

| _cons | 2.114 *** | 2.127 *** | 1.815 *** | 1.142 *** |

| (5.246) | (4.514) | (3.284) | (3.826) | |

| Control | Y | Y | Y | Y |

| Firms FE | Y | Y | Y | Y |

| Year FE | Y | Y | Y | Y |

| City FE | Y | Y | Y | Y |

| Industry FE | Y | Y | Y | Y |

| N | 155,237 | 155,237 | 155,237 | 145,327 |

| Adj-R2 | 0.382 | 0.416 | 0.217 | 0.336 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Tan, L.; Gao, D.; Liu, X. Can Environmental Information Disclosure Improve Energy Efficiency in Manufacturing? Evidence from Chinese Enterprises. Energies 2024, 17, 2342. https://doi.org/10.3390/en17102342

Tan L, Gao D, Liu X. Can Environmental Information Disclosure Improve Energy Efficiency in Manufacturing? Evidence from Chinese Enterprises. Energies. 2024; 17(10):2342. https://doi.org/10.3390/en17102342

Chicago/Turabian StyleTan, Linfang, Da Gao, and Xiaowei Liu. 2024. "Can Environmental Information Disclosure Improve Energy Efficiency in Manufacturing? Evidence from Chinese Enterprises" Energies 17, no. 10: 2342. https://doi.org/10.3390/en17102342

APA StyleTan, L., Gao, D., & Liu, X. (2024). Can Environmental Information Disclosure Improve Energy Efficiency in Manufacturing? Evidence from Chinese Enterprises. Energies, 17(10), 2342. https://doi.org/10.3390/en17102342