J. Risk Financial Manag. 2025, 18(5), 263; https://doi.org/10.3390/jrfm18050263 - 13 May 2025

Abstract

Developing countries face a disproportionate degree of threat from climate change. As such, they require and receive significant financial support to address the menace. However, little is known about the potential externalities of this form of external liquidity for the business sector. This

[...] Read more.

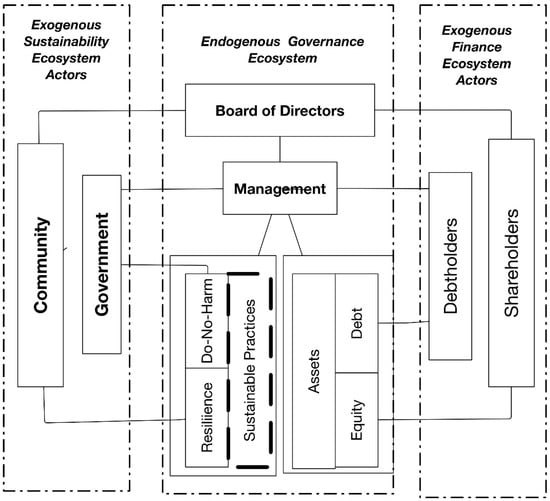

Developing countries face a disproportionate degree of threat from climate change. As such, they require and receive significant financial support to address the menace. However, little is known about the potential externalities of this form of external liquidity for the business sector. This paper evaluates the impact of climate finance on the ease of doing business (EODB). On the one hand, climate finance might lead to an improved business environment as the funds facilitate infrastructure provision, technological innovation, and international collaboration for recipient countries. On the other hand, however, the business environment might be negatively impacted by complex new regulations, disruptive technological transitions, market distortions, and resource diversions. Countries receiving climate funds may also introduce new environmental and business regulations, implement new technologies, and divert resources to new programs to justify the receipt of aid or demonstrate a commitment to balancing economic development with environmental objectives. We theorize that given the expected disruptions to business, climate finance should negatively impact the EODB. We also argue that this negative impact will be more severe for resource-rich countries than for their resource-poor peers. Countries rich in natural resources might experience higher disruptions to business operations as they attempt to balance resource-dependent economic operations with environmental objectives mandated by climate finance. Utilizing panel data for 86 recipient countries for the 2002–2021 period, we test our hypotheses using the Generalized Methods of Moments (GMM) technique. The baseline results suggest that climate finance has a weak positive impact on the EODB. However, as argued, resource-dependence heterogeneity analysis reveals that climate finance significantly negatively disrupts the EODB in resource-rich countries. Furthermore, a sectoral comparative analysis shows that while climate finance has a significant positive impact on the growth of the service sector, it significantly slows the growth of the resource sector, affirming the argument that climate finance might attract higher disruptions to resource-dependent business operations. By implication, lowly diversified economies might realize more negative than positive effects of climate finance, and investors should consider providing support to ease the pains of transitioning from resource-intensive growth to clean energy-driven development strategies.

Full article

(This article belongs to the Special Issue Featured Papers in Climate Finance)

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}