1. Introduction

In order to succeed, firms have to take into consideration requirements from different categories of stakeholders [

1,

2]. According to Clarkson, stakeholders can be classified as primary stakeholders that are essential to a firm survival (e.g., shareholders and employees) and secondary stakeholders, which cannot directly compromise their existence in the short-term, but are able to influence their decisions [

3]. Starting from a merely business and economic approach, stakeholder theories evolved to an approach that considers also other aspects of firm’s activities [

4]. Implementing Corporate Social Responsibility (CSR) is now crucial for firms to demonstrate the commitment to meet stakeholder expectations, and represent an indicator that firms are behaving responsibly [

5]. To obtain long-term success, firms have to manage the requests of several pressure groups. Environmental sustainability is acquiring a growing importance among external stakeholders, and firms need to integrate environmental management into their processes [

6]. If previously this pressure was determined by public institutions with regulations, nowadays there is an increasing pressure from different stakeholders categories, including citizens, consumers, NGOs, and employees [

7,

8,

9].

To meet stakeholders’ sustainability requirements, firms are forced to introduce environment related actions [

7,

10]. The Environmental Management Systems (EMSs) represents a way through which firms can internalize environmental issues [

4], showing a proactive attitude toward sustainability [

11].

For the first time, in 1992, with the Fifth Environmental Action Programme (5EAP), the European Community (EC) remarked the importance of introducing voluntary instruments for firms to encourage a proactive approach to reduce their impact on the environment. Consequently, in 1993 the first version of the Eco Management and Audit Scheme (EMAS) was launched, as an instrument of firms’ self-regulation in addition to compulsory regulations [

12]. In 2009, the last version of the scheme (EMAS III, Regulation (EC) No 1221/2009) was published [

13,

14]. Three years later, the first version of the EMAS Regulation, the ISO (International Organization for Standardization) introduced its 14001 standard, which gave all firms worldwide the opportunity to implement a third party certified EMS [

15]. The ISO 14001 standard was launched in 1996, and reviewed in 2004 and 2015 [

16]. Both EMAS and ISO 14001 helps firms to implement a formal management system with an environmental policy, program, and practices [

17]. Although the two systems have the same general objective of reducing organizations’ environmental impact, they differ in some aspects [

18]. Testa

et al. (2014) found out differences in firms’ environmental performances. Results suggest that ISO 14001 implementation lead to a stronger improvement of environmental performances in the short run, determining that the maturity of ISO 14001 is not linked with greater environmental performances. Conversely, EMAS improvements are smaller in the short term, but wider in the long term. Authors attribute this result to the fact that firms before implementing EMAS are already highly credible and concerned of their environmental impact [

19]. According to Neugebauer, F. (2012), motivation on the implementation of the EMS are very different referring to EMAS or ISO 14001. While ISO 14001 is often a response to external pressure, EMAS is significantly coupled with internal drivers [

20].

By the end of 2014, over 3300 organizations were registered in Europe according to the EMAS scheme, with Italy accounting for about 35% of the total. Given the importance of the instrument in Italy, a survey on the entire population of EMAS organizations in Italy has been conducted. The aim of the work is to analyze how Italian organizations perceive the EMAS registrations, regarding the effectiveness of reducing their environmental impact and other economic and social aspect of organizations. In the first part of the questionnaire, motivations for the registration have been assessed, then the main difficulties in implementing the scheme, and finally the level of both environmental and economic benefits.

In this paper, we initially present the findings of previous surveys conducted on the EMAS scheme, in order to make possible a confrontation and validation of results. In the second part, the research method is presented and the findings are discussed.

2. Previous Surveys on the Application of EMAS in European Firms

Several studies have been conducted to understand the impact of the EMSs on firms’ performance. Frequently, surveys focused on drivers, benefits, and barriers to their achievement. There are a variety of factors identified by scholar to implement an EMS that can vary significantly due to firms’ size, sector, and national or regional context [

21]. It is important to keep in mind that results obtained from an EMS implementation can vary significantly in relation to companies’ sector, dimension and national context [

15,

22]. Many authors focused on its application in SMEs [

17,

23,

24,

25,

26]; others stressed how its impact is different as regard to the sector of application [

27] or the institutional contest [

28]. Another aspect to consider is the market in which companies operate: export oriented companies tend to gain greater benefits from the certification [

29]. Motivations, benefits, and barriers can also be grouped as internal and external to the company. While the firsts focus on the internal operations, the others put their emphasis to the outcome of the EMS that relate to the external interactions of the organization [

17,

30]. The impacts on firms of the application of ISO 14001 have been deeply investigated by scholars. Recent works concerning benefits of ISO 14001 implementation are [

27,

31,

32,

33,

34,

35,

36,

37,

38,

39,

40,

41]. Scholars also investigated barriers and constraints to ISO 14001 adoption and maintenance [

25,

27,

30,

33,

34,

37,

39,

41,

42,

43,

44,

45]. Conversely, not many surveys deepen organizations’ perception of EMAS implementation. Therefore, this Paragraph focuses on findings from organizations registered with the EMAS regulation.

Since the EMAS regulation was published, several surveys have been conducted, considering drivers, benefits, and difficulties in its implementation by European organizations. Some studies focused on specific countries, especially those in which EMAS is more widespread, like Germany [

15,

20,

46,

47,

48,

49,

50] and Italy [

19,

21,

51,

52,

53,

54]. On the other hand, fewer analyses took into consideration several countries, giving a more general European overview on EMAS organizations [

55,

56,

57,

58,

59,

60,

61].

Conducting surveys, scholars investigated the impact of EMAS both in terms of difficulties and barriers, and in relation to positive outcomes with its implementation. External barriers to EMAS implementation are mainly of two kinds: a lack of market and consumer recognition, and a low institutional support. Sometimes firms do not recognize convenience respect to ISO 14001, which is more required from supply chain partners [

51,

62]. Firms do not have benefits regarding GPP and tenders [

63]. Given the European nature of EMAS, it does not add value in extra-UE markets, even after the introduction of EMAS Global [

49,

57,

62]. Moreover, organizations in many cases declared difficulties in achieving an efficient communication of their efforts to external stakeholders (consumers and costumers), not allowing a competitive advantage on the market [

53]. Concerning internal aspects, firms agree about the low normative simplifications and incentives offered with EMAS [

49,

57,

60]. In addition, they do not perceive a positive differentiation in terms of inspections carried out by public authorities [

49,

53,

57,

62,

64]. With reference to internal barriers to EMAS introduction, implementation costs represent a crucial obstacle for SMEs [

17,

51,

57,

62,

64]. Also the lack of organizational culture in firms is found as an impediment to EMAS renewal [

62,

63,

64,

65]. Probably one of the main barriers is the requirement of legislative compliance to obtain the registration. In fact, organizations must demonstrate the complete normative conformity [

57,

62,

63,

64].

According to Hillary, three macro areas of positive external outcomes regarding EMAS implementation can be grouped: commercial interactions, communication, and environmental performances [

17]. Concerning the first group, there is no common agreement among scholar about the potential positive financial and competitive consequences of EMAS. Especially in early works (between 1990 and early 2000s) a greater competitiveness of EMAS firms was pointed out [

15,

46,

47,

55]. On the other hand, in more recent works this seems to be a troubling point. In fact organizations are not enough satisfied in terms of competitive advantages and increased turnover [

50,

51,

57]. According to the analyzed surveys, improved communication with interested parties is a major benefit of EMAS. In many cases, EMAS allows improvement of an organization’s image and reputation, especially with local community and public institutions [

15,

17,

51,

57,

58,

62]. Improvement of environmental performances is often reported as a main achievement of organizations implementing EMAS. The analysis of the environmental performances follows two paths. The first consists in the analysis of Environmental Indicators trend. According to Daddi

et al. (2011), indicators show a slight positive effect on environmental aspects, especially in reducing waste production and water consumption [

66]. Moreover, EMAS seems to be more effective in the medium-long run, because environmental performance is generally linked in a positive way with the age of the system [

19,

52,

66]. Also analyzing the application of EMAS in Italian clusters (Lucca paper industry), indicators show a positive trend in environmental performances [

54]. Other studies evaluate environmental performances according to organizations’ perception, from the analysis of surveys responses. In general, organizations perceive a positive improvement of environmental performances. Several environmental achievements are pointed out from organizations, the most frequently related to are water consumption, waste management, recycling, energy consumption, and air pollution [

15,

47,

51,

52,

57,

58,

62,

64]. In another study on European EMAS organizations, respondents underlined a positive environmental performance result, with the majority reporting significant improvement in Core Indicators, with the exception of biodiversity [

57]. Merli

et al. (2014) realized a survey targeted to all Italian Clusters applying EMAS at a cluster level, finding that stakeholders perceive environmental performances improvement as the major positive outcome of its application [

53].

The present work enriches the knowledge on organizations’ perception of EMAS in Italy, one of the leading countries for EMAS diffusion. Thanks to the large coverage (over 500 respondents) it allows to obtain significant results, providing useful insights on firms’ viewpoint to the EMAS Competent Body during the present process of revision of the Regulation. Given the recent downturn of EMAS registrations in Europe, a further added value of the work is to present figures on organizations’ intention to renew or drop-out of the EMS in the future.

4. Survey Findings

In order to identify some possible improvements and map the critical issues in the application of EMAS, the questionnaire was submitted to EMAS registered companies in Italy.

The conceptual model proposed for the analysis is divided into three sections:

Drivers, that prompted companies to join the regulation;

Benefits, expected and achieved, on the environmental and economic performance and to further strategic benefits attainable through EMAS;

Critical issues and difficulties, encountered during the realization and the implementation of the EMS.

The first analysis focuses on descriptive investigations, regarding the demographic information of companies as the geographical location, the size of the organization, the number of employees, the public or private nature, the turnover and the duration of the registration.

A general profile of an Italian company registered with EMAS has been determined as follows:

Is mainly located in Northern Italy (regions with the highest concentration are Lombardy, Emilia-Romagna, and Tuscany);

Is a small or medium sized company, with a number of employees ranging from 10 to 49;

Has a mostly private nature and a turnover between 2 and 10 million per year;

It caters mostly to the national market, and to local and regional markets, and has an average length of stay within EMAS certification of 36 months;

In addition, 84.2% of Italian companies registered EMAS have also obtained the ISO 14001 certification, and 55.7% of them has detained such certification for over 36 months.

It is also interesting to track down the sector of registered companies by analyzing the NACE code (Regulation (EC) No 1893/2006). 57% of the responding companies belong to five specific fields of activity:

10-Manufacture of food products;

20-Manufacture of chemicals and chemical products;

35-Electricity, gas, steam, and air conditioning supply;

38-Waste collection, treatment, and disposal activities; materials recovery;

84-Public Administration and defense; compulsory social security.

The sectors in which EMAS is most widespread are Waste collection, treatment and disposal activities, materials recovery (16.1%); Public Administration and defense, compulsory social security (15.8%); and food industries (13.4%) (

Table 1).

Since its second revision (Regulation (EC) No 2001/761), all kind of organizations can implement the scheme. During the analysis, considering the high number of public administrations in the sample and the deep difference both in governance and purpose among public and private organizations, we decided to treat separately in this section the two types. The aim is to catch differences and similarities between these groups of organizations regarding the implementation of the EMAS.

Studying the demographic differences between public administrations and private companies, a greater number of public administrations is located in northern Italy (78.8%) compared to private companies (61.6%). A significant data is the total absence of EMAS public administrations in southern Italy and in the islands, while private companies located in the South represent 14% of the total. The top three regions for the number of private enterprises are Emilia-Romagna, Lombardy, and Tuscany whilst for the public administrations are Veneto, Tuscany, and Trentino Alto Adige. The only relevant difference in terms of organizations dimensions is the greatest number of small organizations for public administrations and, on the other hand, fewer in micro. The average length of registration in the private sector is longer than 36 months. In the Public Administration, instead, 34% implemented the EMS for a period between 12 and 24 months, and 44% for over 36 months (

Table 2 and

Table 3).

4.1. Drivers and Benefits

Our survey also investigates the reasons that led companies to join the EMAS scheme, so the causes of company’s satisfaction or dissatisfaction on certification were examined. In particular, the gaps between the reasons that led companies to apply for certification and the achieved benefits as a result were investigated. First, drivers and benefits have been divided in three main categories: economic, environmental, and strategic. Then, companies were asked to give a score from 1 to 6 regarding the importance of specific drivers and benefits in the decision to join EMAS.

From data analysis, strategic drivers and benefits are the most stimulating for Italian companies than environmental and economics ones. In particular in strategic drivers and benefits, the improvement of image organization and legislative compliance seem to be the most appreciated, whilst the improvement of the relationship with the staff appeared as less important (

Table 4). Among environmental drivers and benefits, organizations pay a particular attention to the reduction of waste generation and to the use of resources, raw materials and energy (

Table 5).

The most important drivers are energy savings and increase in competitiveness, while for benefits, savings in the use of raw materials are the ones with the higher satisfaction (

Table 5).

A key step to understand the attitude of companies towards the EMAS Regulation relates to the benefits achieved after the implementation of the EMS. An expected benefit not achieved, in fact, could negatively affect the opinion on the certification. The organizations participating in the survey are not completely satisfied with regards to the strategic drivers (that can be considered as the main ones), with a gap between expectations and perceived benefits achieved of −0.49. The situation is slightly better about the environmental aspects, with a −0.22 gap, and the economic aspects, with a −0.2 gap (

Table 6).

In

Table 6, the differences between public administrations and private companies are also described in relation with strategic, environmental, and economics drivers and benefits. The major differences are related to environmental drivers. Public administrations are more satisfied for the environmental benefits achieved, while private organizations are more satisfied concerning the economic benefits. Specifically, regarding the strategic drivers, public administrations consider relations with the staff and the incentive for innovation more important than private enterprises. Private companies, instead, gives more importance to the improvement of access to public funds and call for tenders. Concerning the strategic benefits section, the public administrations are more satisfied than enterprises for improvements in relations with staff (

Table 4).

Environmental aspects are generally more motivating for public administrations which are more focused on the effects on biodiversity, reduction of waste generation, and the use and contamination of soil. From the economic viewpoint, private companies consider savings on insurance premiums, the increase in turnover, and competitiveness more important if confronted with public organizations, both for drivers and benefits (

Table 6).

In

Table 4,

Table 5 and

Table 6, a constant is that the average score for drivers is always higher than the average score for perceived benefits. This indicates that expectations of organizations are in most cases not enough satisfied. The difference between strategic drivers and benefits (

Table 4) is the highest (0.49), especially for the “Improvement of the relationship with customers/citizens”. This finding is consistent with existing literature [

53,

57,

58,

62]. On the other hand, the difference in environmental and economic drivers and benefits is less evident, respectively 0.22 and 0.20 (

Table 5 and

Table 6). Moreover, a slight difference exists between public administration and private organizations. In general, public administrations appear as less satisfied concerning environmental aspects (

Table 4,

Table 5 and

Table 6).

Even though benefits are generally lower that drivers, the most significant in the strategic category are “legislative compliance” (4.64) and “improved image” (4.59) (

Table 4). Moreover, EMAS is not only useful for private organizations to improve legislative compliance, but also for public administrations. In fact, public administrations consider the EMS very important (5.10) to ensure that all operations are conducted in accordance with existing regulations. It is probably due to the fact that Italian environmental legislation is particularly complex and also for public bodies it is often hard to maintain the compliance, with the risk of criminal penalties for public administrators.

Concerning the “environment” category, the main benefit is “reduction of waste generation” (3.98) (

Table 5). Finally in relation to “economic factors” is “energy savings” (3.40) (

Table 6). These results agree with findings of scholars that previously investigated EMAS (see Paragraph 2).

4.2. Difficulties

After examining drivers and benefits, the technical and economic difficulties encountered by companies and Public Administration in the implementation of EMS are now presented. The major difficulties were encountered in the preparation of the environmental statement, totalizing an average score of 3.83, followed by the economic difficulties, the elaboration of the initial environmental review, and the EMS implementation. Looking at specific items of the environmental statement, the predispositions of environmental performances indicators, the costs for consultancies, and those related to the maintenance of certification appeared as particularly critical (

Table 7).

Finally, there are not significant differences between public administrations and companies about the financial difficulties encountered during certification. The public administrations however revealed higher difficulties relating to the staff and, in particular, to the lack of time and motivation (

Table 8).

Another step is to investigate what might be the possible actions to improve the efficacy of the EMAS regulation. In this section there are no significant differences between public and private sector, that is why the two groups have been analyzed together.

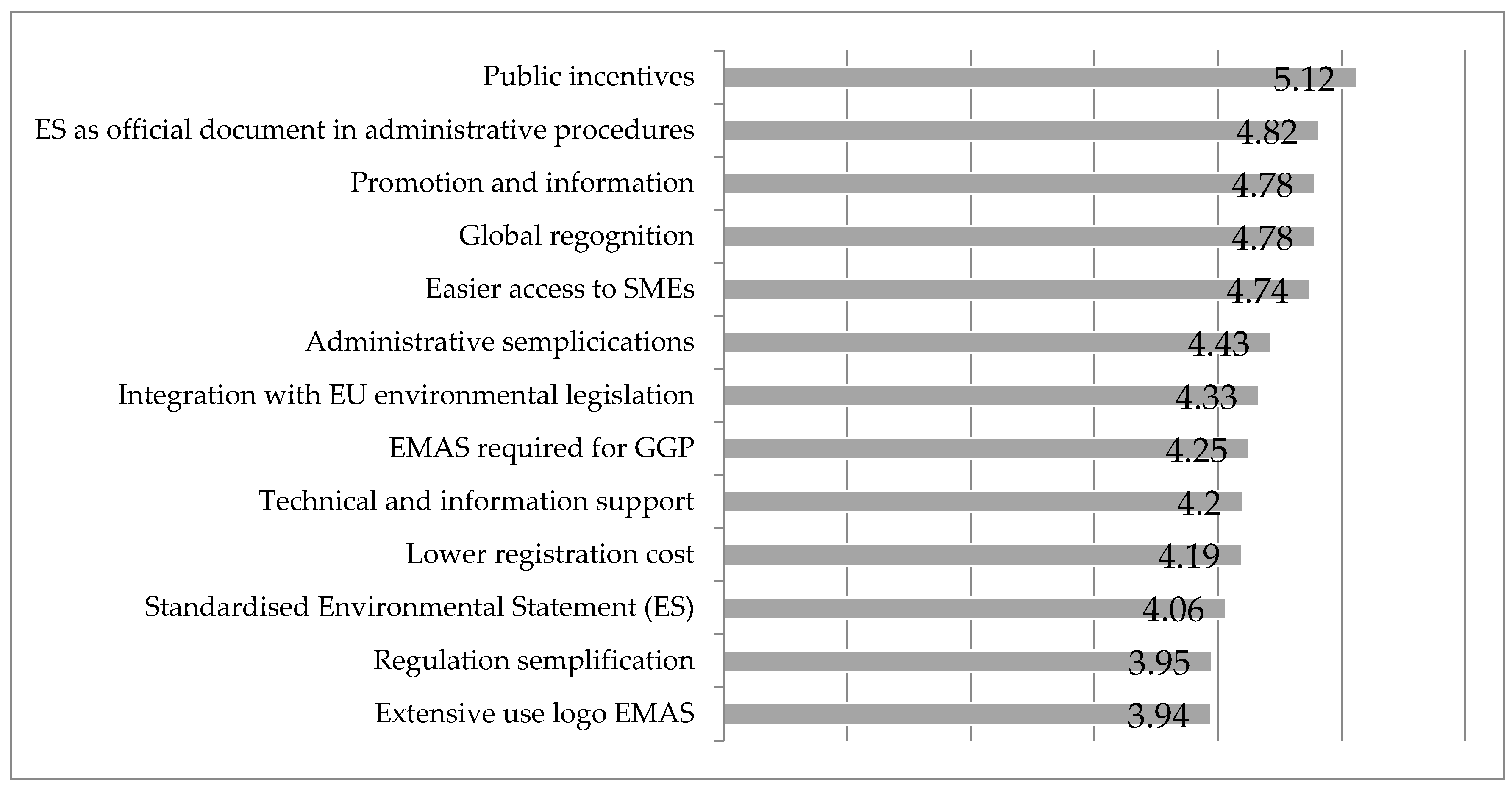

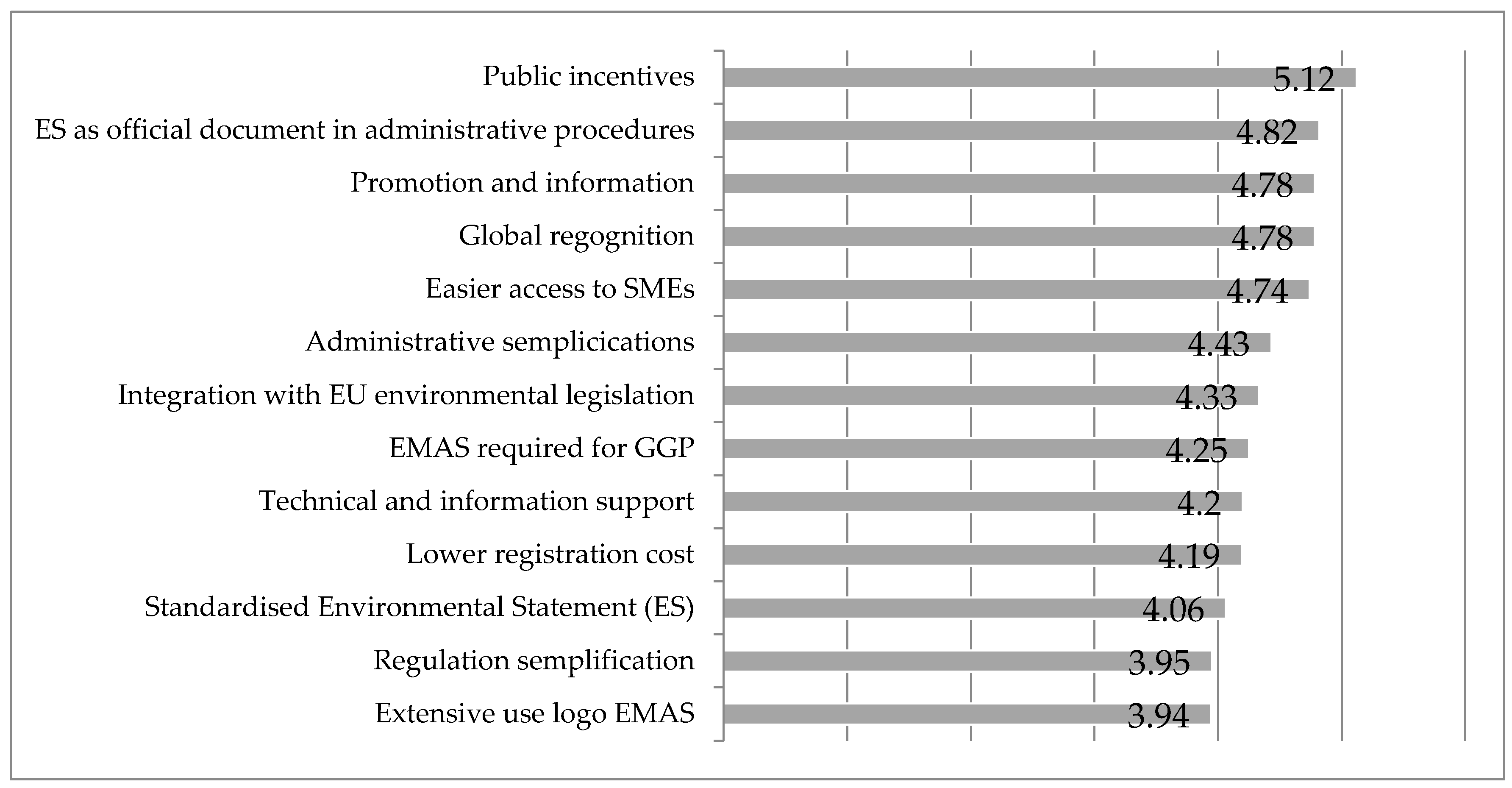

Despite the discrepancy between drivers and benefits achieved seems not so important, the majority of the organizations would improve the access of EMAS registered organizations to public incentives and to simplified administrative procedures, by the use of the environmental statement as an official document (

Table 4 and

Figure 1). Moreover, they ask for a stronger involvement of public authorities on EMAS promotion. Instead, a more extensive use of the logo, the simplification of regulation, and a standardized environmental statement have been considered as less important factors (

Figure 1).

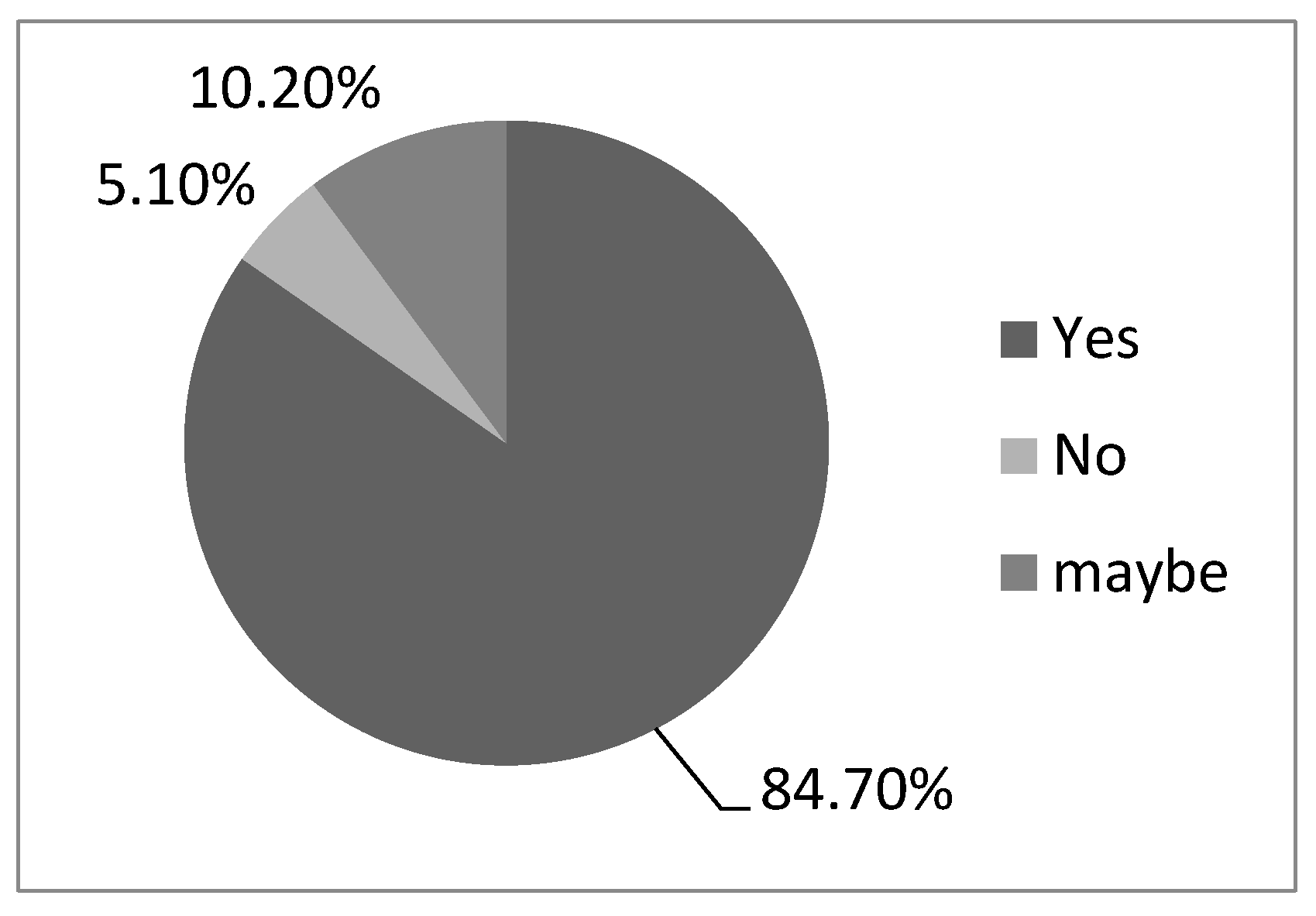

Finally, we discussed how drivers, benefits, and difficulties affect the organizations’ decision to renew EMAS certification.

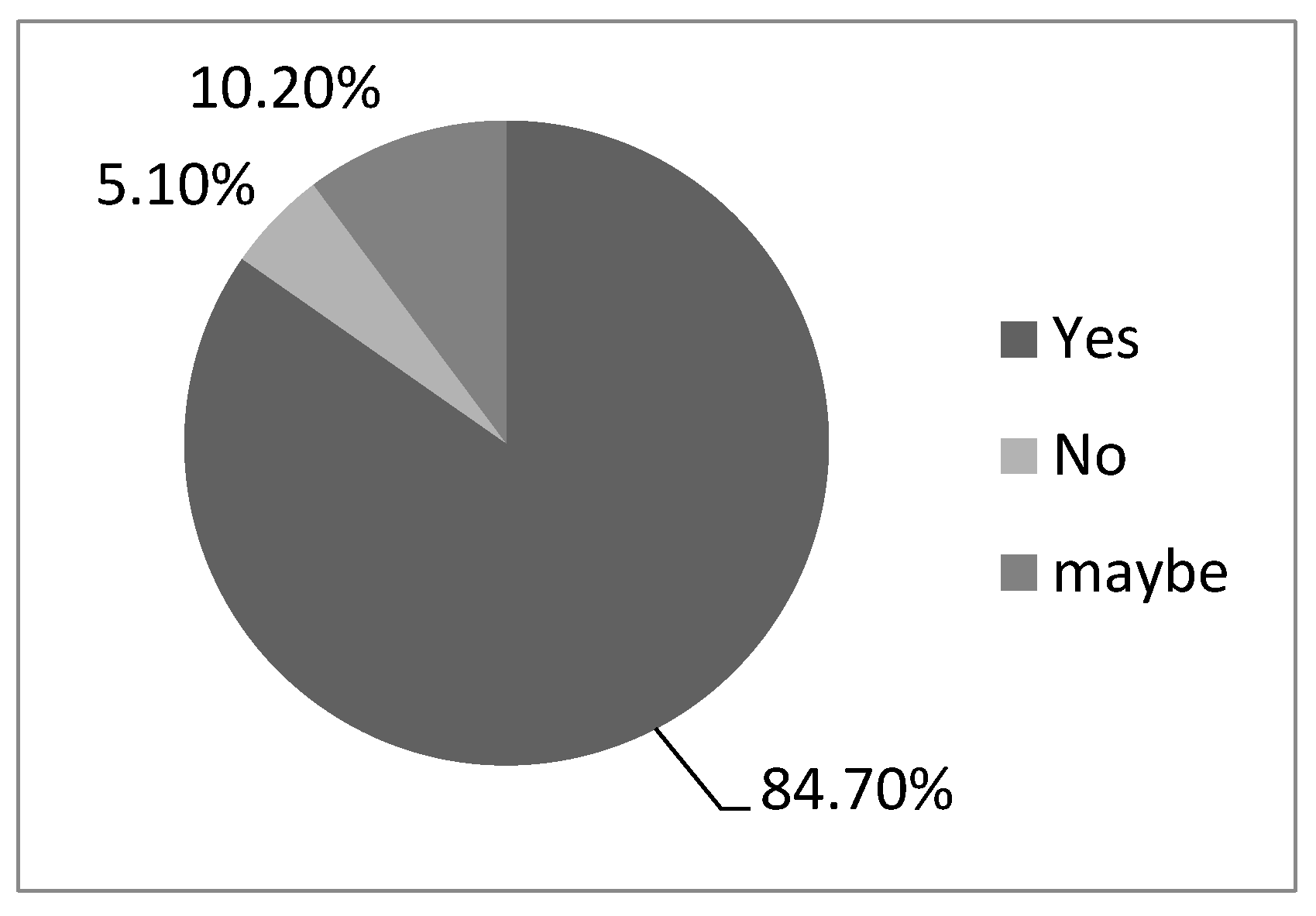

Figure 2 shows that 80.74% of the sample intended to maintain certification and only 5.10% showed the will to drop out of it.

Table 9 shows that the smaller are the dimensions of the organization, the higher the dropout rate is. Respectively, 20.28% of Small and 22.50% of Micro organizations do not intend to renew. Conversely, over 95.00% of Large and 90.91% of Medium will maintain EMAS.

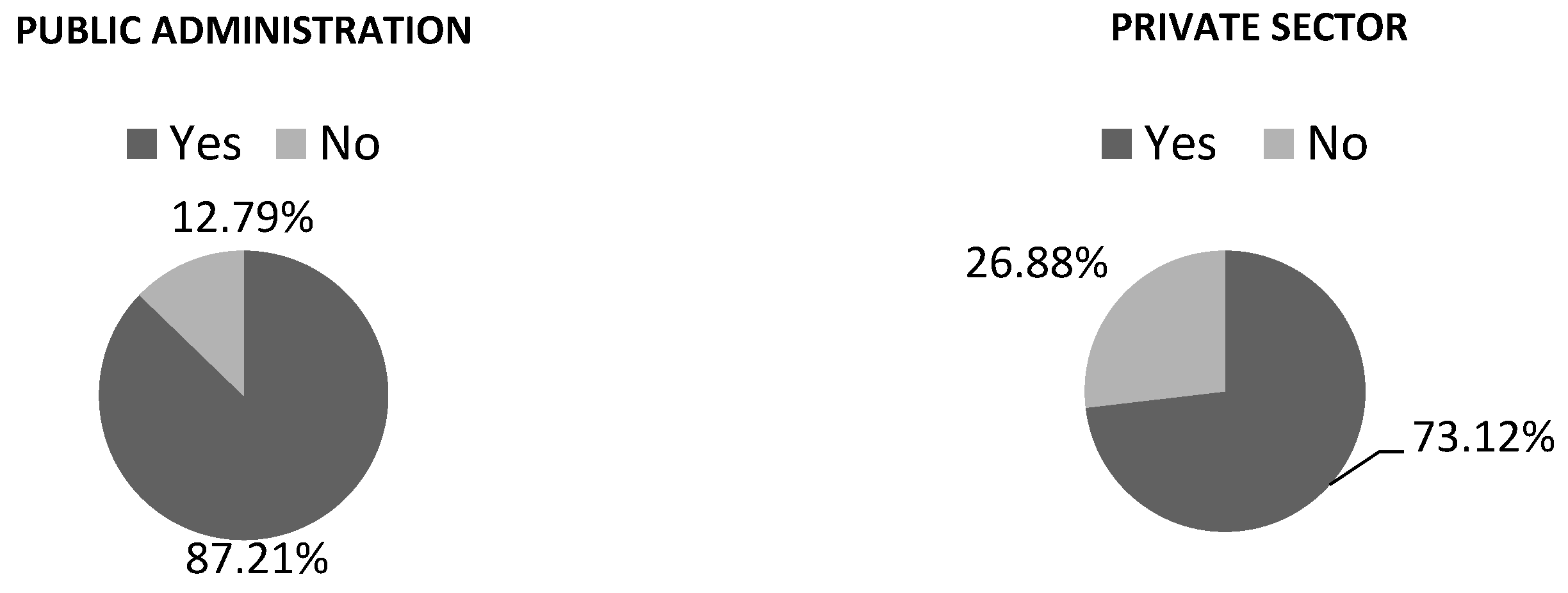

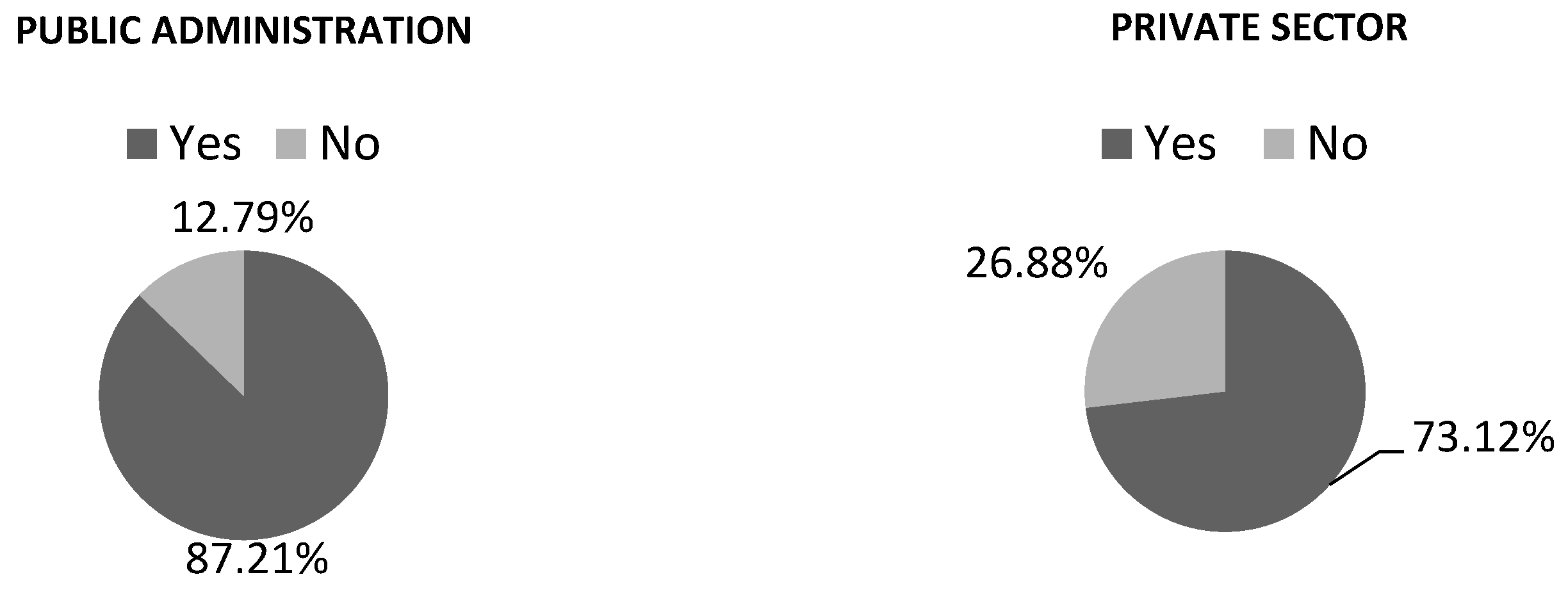

Taking into account the nature of organizations’ ownership, 84.01% are private while 15.99% public. It can be highlighted that public administrations are more satisfied with the EMAS. Just above 13% of them intend to drop out, while the percentage grows to over 25% for private organizations (

Figure 3).

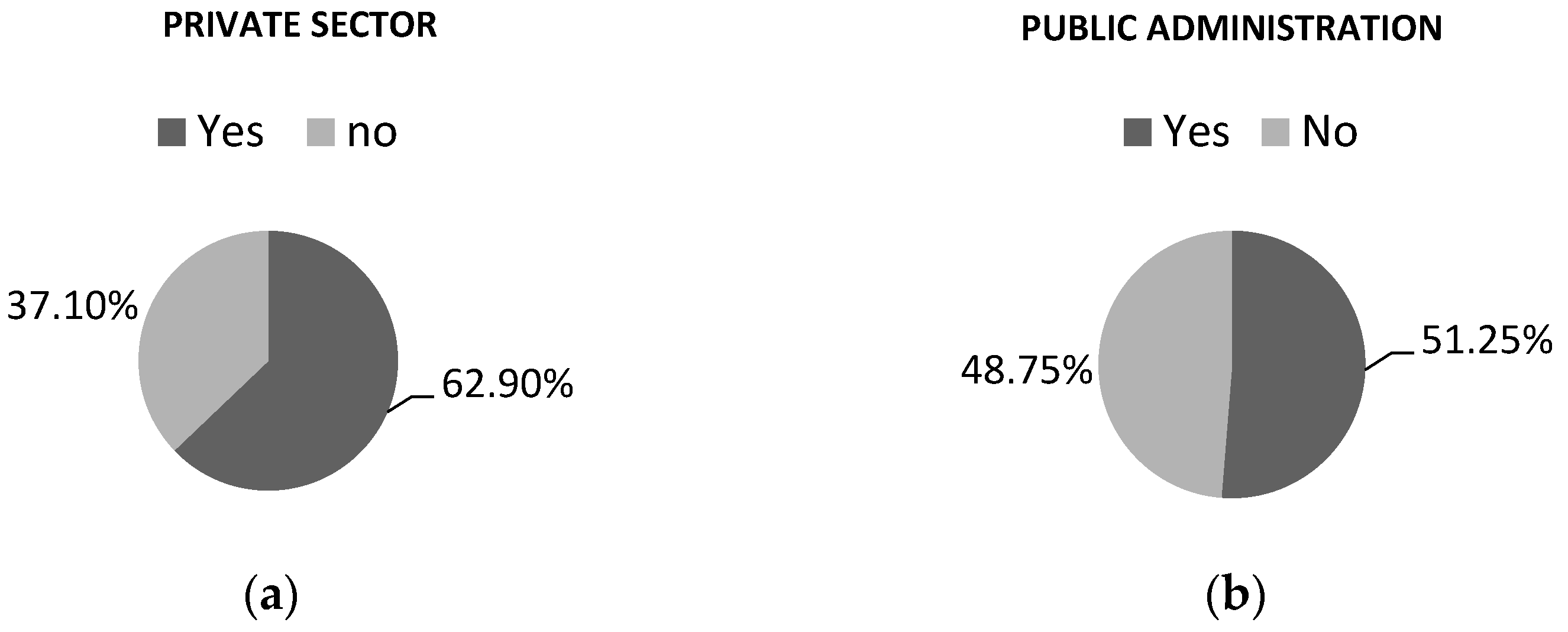

Organizations were asked to indicate if the monetary investment made for EMAS has been paid back. Public administration and private firms’ opinion differ substantially. Looking at

Figure 4, public administrations (

Figure 4a) seem slightly less satisfied than private enterprises (

Figure 4b), and only 51.25% is deemed fully satisfied about the investment made, in respect of the 62.9% of private companies. Public administrations encountered wider organizational and economic difficulties in the implementation of the EMS, and were generally more enthusiastic about benefits achievable with EMAS than enterprises.

Comparing

Figure 3 and

Figure 4 it is interesting to note that while public organizations have an higher propensity to renew, the monetary investment payback is greater for private firms.

It is also interesting to note that even though public administrations perceive a major negative difference between drivers and benefits of EMAS, they declare an higher propensity to renew EMAS and an higher rate of investment pay off (

Table 4,

Table 5 and

Table 6 and

Figure 3 and

Figure 4).

5. Conclusions

This survey attempts to track down barriers and driving forces for the diffusion and promotion of the EMAS regulation. Through the analysis of the gap between drivers and the achieved benefits after the implementation of the EMS, it was possible to figure out the level of satisfaction of the organizations regarding the regulation. In general, EMAS seems to have almost met organizations’ expectations, even if many aspects could be improved. In particular, while from an economic and environmental point of view the gap between expectations and achieved results is not very high, the expectations about strategic factors were not enough satisfied. Differences between public administrations and private organizations drivers’ benefits and difficulties have helped to in-deep the analysis. Public administrations are more committed in relation to the strategic aspects, as the improvement of the organizational image or of the relationship with stakeholders. Conversely, private companies seem more interested in economic aspects, such as public funding access and call for tenders. Regarding the difficulties encountered, there are no significant differences between the two groups. For both, the economic difficulties, as costs for consultancy and for the maintenance of the registration, and technical difficulties, such as those related to the environmental statement to motivation staff and initial environmental analysis, resulted as the most relevant. This analysis aimed to underline aspects of potential improvement of the EMAS, in order to better meet organizations’ needs and reduce difficulties in its implementation. In fact, the differences between the public and private sectors suggest the possibility of creating two different protocols according to the needs and the specific problems of each macro-sector. With the identification of best environmental management practice and the development of EMAS Sectorial Reference Documents for Public Administration, the European Union has already made steps in this direction . Currently, together with ISPRA we are conducting a survey pointed to all Italian organizations that drop out of the EMAS since 2010, with the goal of better understanding critical aspects of its implementation and figuring out which policies and support tools would be more effective in order to encourage new registrations in the future.

{kind=link}

{kind=link}

{kind=link}

{kind=link}