Gender and Public Pensions in China: Do Pensions Reduce the Gender Gap in Compensation?

Abstract

:1. Introduction

2. Literature Review

3. Background

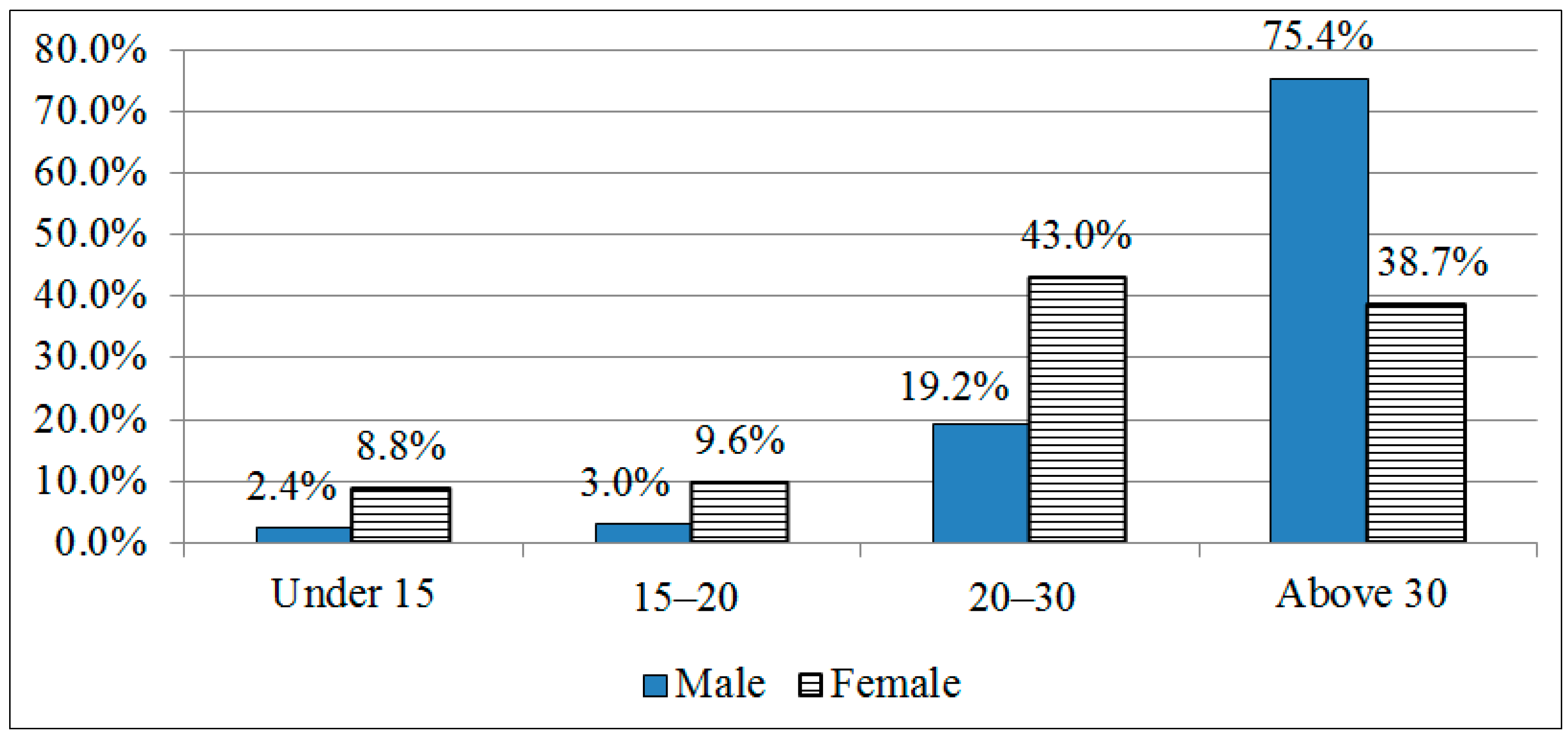

3.1. Sources of Income in Old Age for Males and Females

{kind=link}

{kind=link}

{kind=link}

| Labor income | Retirement benefit | Support from family | Minimum guarantee | Asset income | Others | |

|---|---|---|---|---|---|---|

| Male | ||||||

| In total | 36.6 | 28.9 | 28.2 | 4.1 | 0.4 | 1.8 |

| Single | 38.2 | 4.1 | 14.2 | 36.4 | 0.3 | 6.8 |

| Married with spouse | 39.4 | 31.7 | 24.5 | 2.4 | 0.5 | 1.5 |

| Divorced | 34.8 | 30.7 | 21.1 | 10.0 | 0.5 | 2.8 |

| Widowed | 22.7 | 19.9 | 49.8 | 5.4 | 0.3 | 2.0 |

| Female | ||||||

| In total | 21.9 | 19.6 | 52.6 | 3.7 | 0.3 | 1.9 |

| Single | 16.6 | 15.7 | 45.8 | 14.3 | 0.3 | 7.3 |

| Married with spouse | 28.6 | 22.0 | 44.7 | 2.5 | 0.4 | 1.8 |

| Divorced | 14.3 | 40.5 | 37.2 | 5.1 | 0.5 | 2.4 |

| Widowed | 10.9 | 15.1 | 66.1 | 5.5 | 0.3 | 2.1 |

3.2. Labor Market Participation of Males and Females

3.3. Life Expectancy of Males and Females

4. Effects of Institutional Features of the Public Pension Program on the Pension Benefits of Males and Females

4.1. Contributions

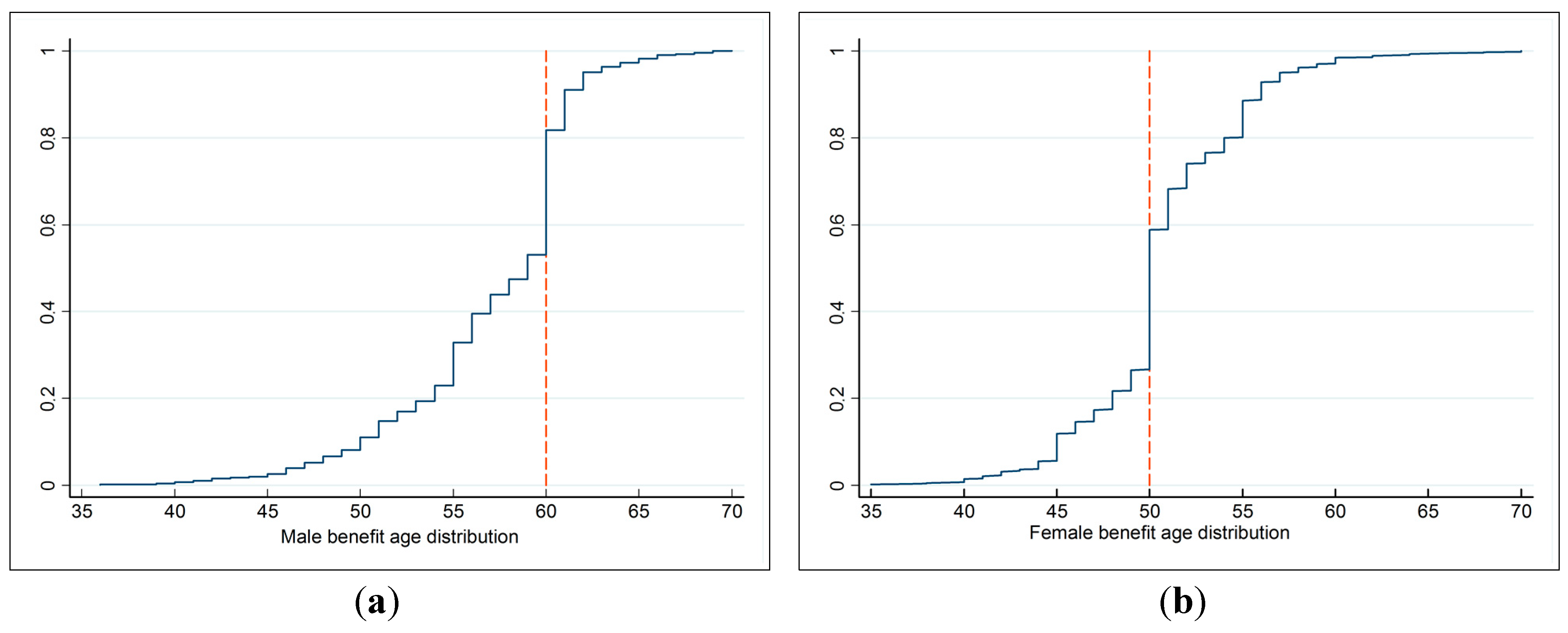

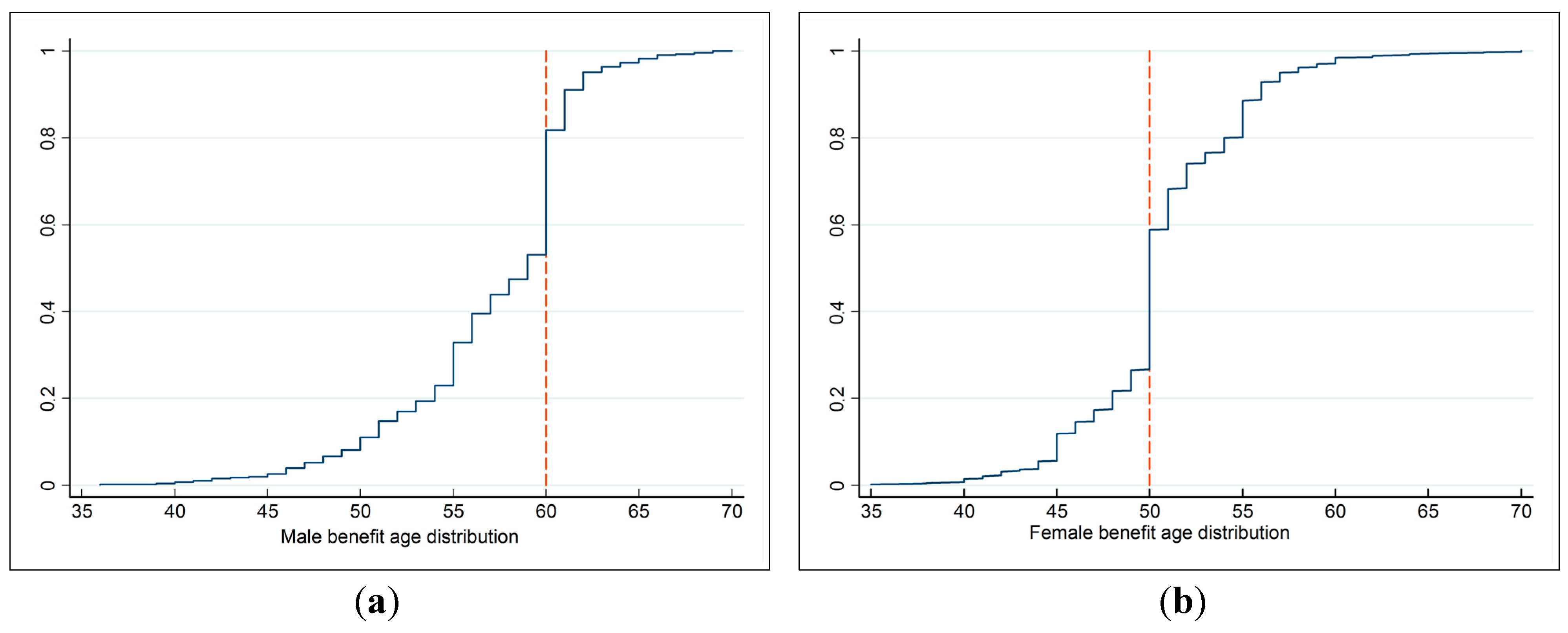

4.2. Retirement Age for Public Pension Benefit Receipt

4.3. Benefits

4.4. Gender Pension Gap Caused by Program Regulations

| Retirement age | Divisor of individual account | Life expectancy after retirement (months) | |

|---|---|---|---|

| Male | Female | ||

| 50 | 195 | 380.4 | 416.1 |

| 55 | 170 | 325.2 | 360.0 |

| 60 | 139 | 272.4 | 304.8 |

| 65 | 101 | 223.2 | 253.2 |

5. Empirical Analysis of Retirement Benefits of Males and Females

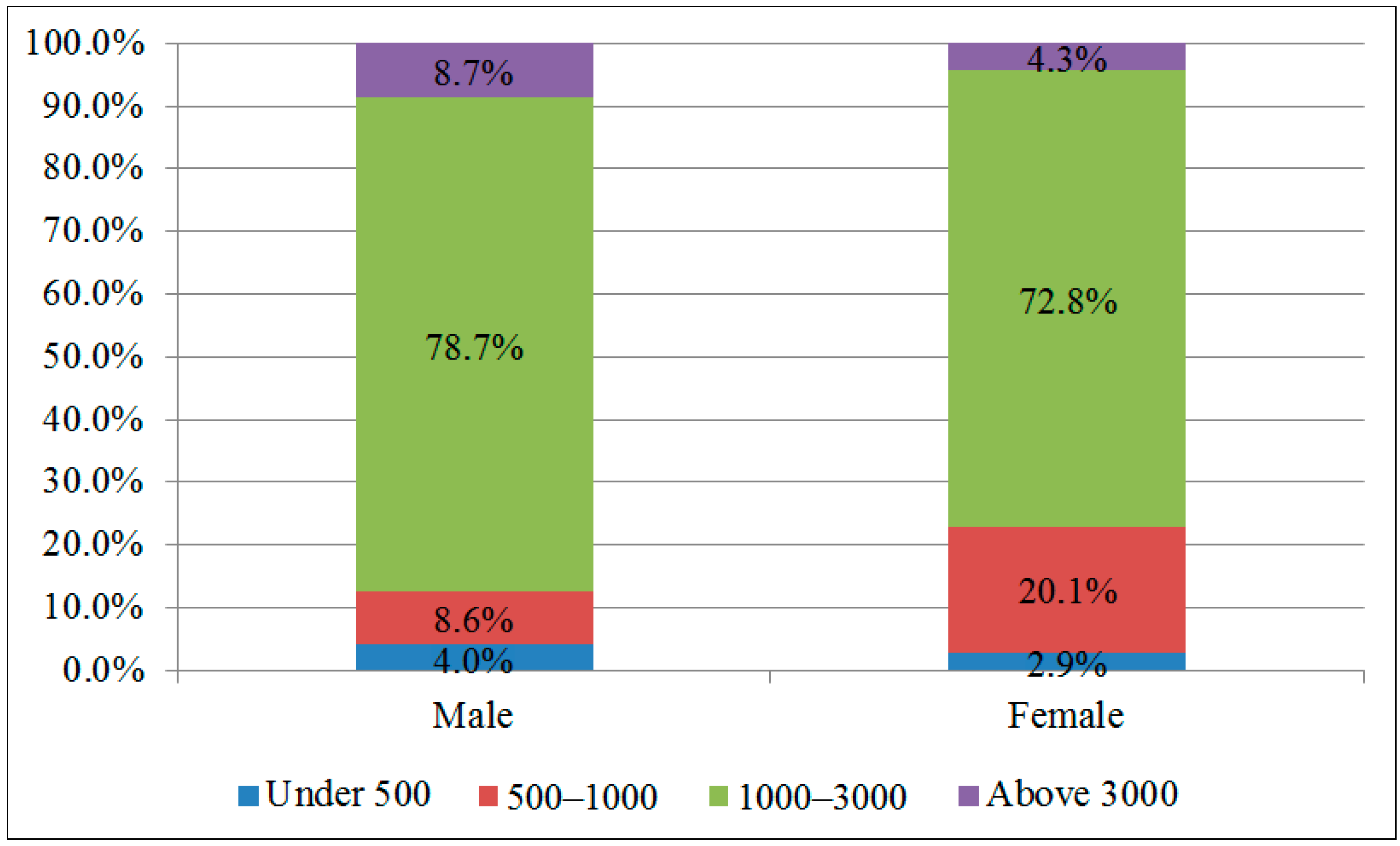

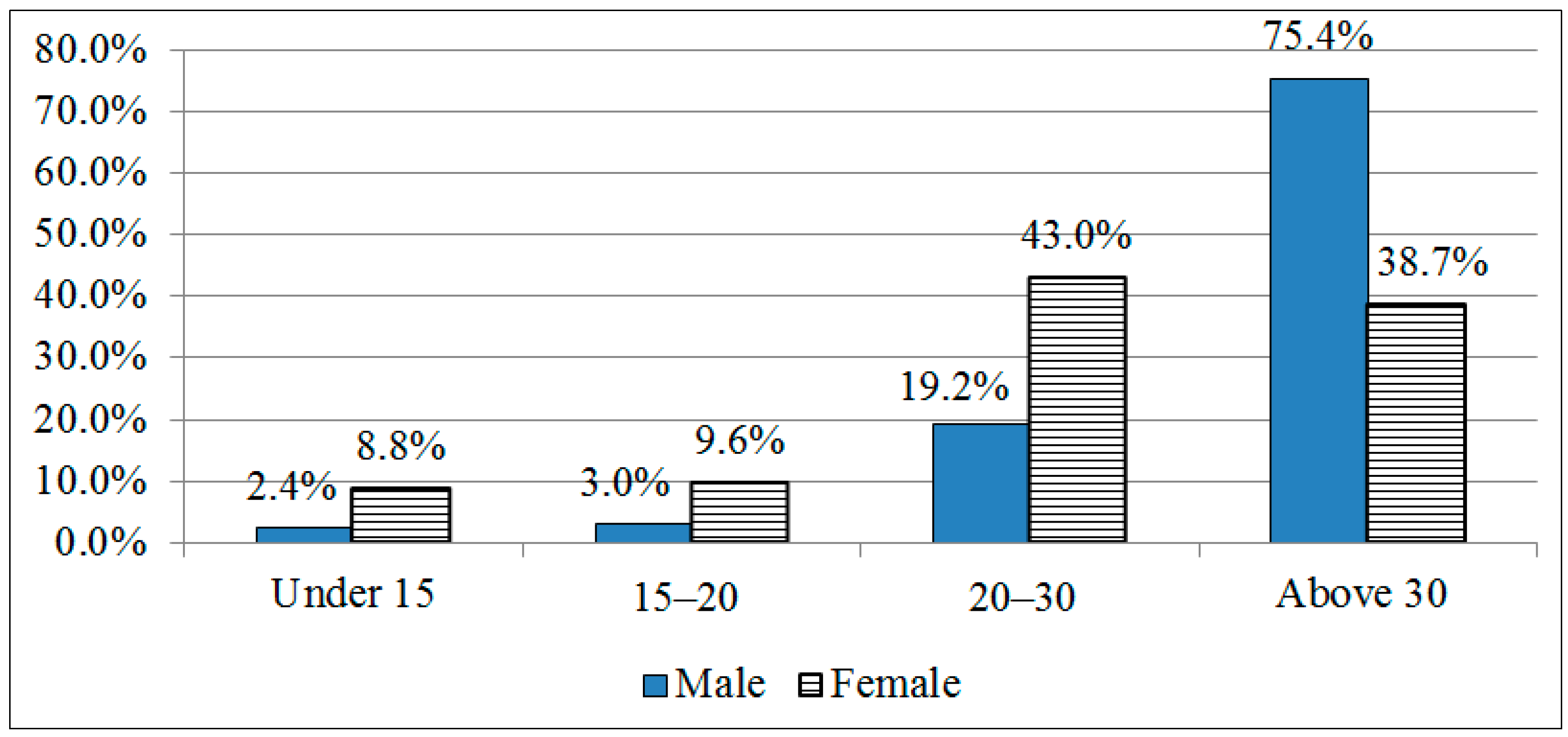

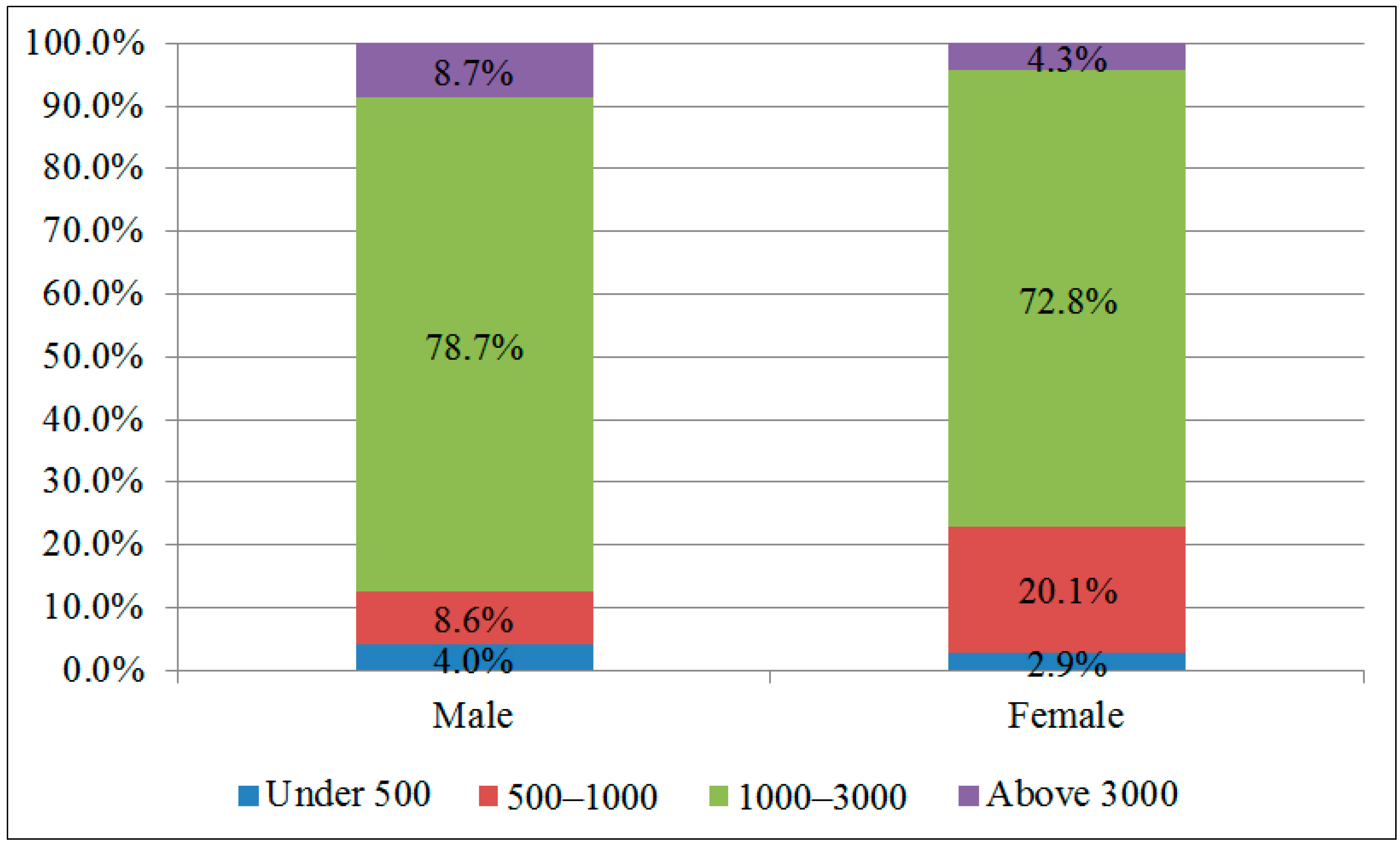

5.1. Summary Statistics for Male and Female Retirees in 2011 CHARLS

| Variables | Male | Female | |||

|---|---|---|---|---|---|

| Frequency | Percent | Frequency | Percent | ||

| Gender distribution | 1039 | 54.8 | 938 | 45.2 | |

| Age distribution | Under 50 | 17 | 1.5 | 52 | 5.5 |

| 50–55 | 35 | 3.1 | 187 | 19.9 | |

| 55–60 | 159 | 14.0 | 237 | 25.3 | |

| 60–80 | 853 | 74.9 | 431 | 46.0 | |

| Above age 80 | 75 | 6.6 | 31 | 3.3 | |

| Health status | Fair or poor | 392 | 40.5 | 259 | 32.7 |

| Good | 577 | 59.6 | 534 | 67.3 | |

| Marital status | Single, divorced or widowed | 82 | 7.2 | 181 | 19.3 |

| Married and having spouse | 1057 | 92.8 | 757 | 80.7 | |

5.2. Calculation of the Gender Pensions Gap and the Gender Earnings Gap and Comparison of Retirement Ages for Males and Females

5.3. Explanations of the Gender Pension Gap and Its Changes in China

| Average pre-retirement salary | Average pre-retirement salary | Average current monthly benefits | ||||||

|---|---|---|---|---|---|---|---|---|

| Female (1) | Male (2) | (1)/(2) | Gender Gap | Female (5) | Male (6) | (5)/(6) | Gender Gap | |

| 1997 and before | 595.8 | 808.5 | 73.7 | 26.3 | 1553.8 | 1951.4 | 79.6 | 20.4 |

| 1997–2005 | 876.2 | 1180.1 | 74.3 | 25.8 | 1527.5 | 1855.3 | 82.3 | 17.7 |

| After 2005 | 1091.9 | 1468.1 | 74.4 | 25.6 | 1387.0 | 1858.9 | 74.6 | 25.4 |

6. Policy Discussion

7. Conclusions

Acknowledgments

Author Contributions

Conflicts of Interest

References

- Bettio, F.; Tinios, P.; Betti, G. The Gender Gap in Pensions in the EU. Available online: http://ec.europa.eu/justice/gender-equality/files/documents/130530_pensions_en.pdf (accessed on 18 June 2014).

- China Health and Retirement Longitudinal Study (CHARLS). 2011. Available online: http://charls.ccer.edu.cn (accessed on 18 January 2014).

- Fultz, E.; Ruck, M.; Steinhilber, S. The Gender Dimensions of Social Security Reform in Central and Eastern Europe: Case Studies of the Czech Republic, Hungary and Poland; International Labor Office Subregional Office for Central and Eastern Europe: Budapest, Hungary, 2003. [Google Scholar]

- Even, W.E.; Turner, J.A. Has the Pension Coverage of Women Improved? Benefits Q. 1999, 15, 37–40. [Google Scholar] [PubMed]

- Even, W.E.; Macpherson, D.A. When will the Gender Gap in Retirement Income Narrow? South. Econ. J. 2004, 71, 182–200. [Google Scholar] [CrossRef]

- Dahl, S.A.; Nilsen, O.A.; Vaage, K. Gender Differences in Early Retirement Behaviour. Eur. Sociol. Rev. 2003, 19, 179–198. [Google Scholar] [CrossRef]

- Wu, K. Gender Difference Should be Considered in Pension Plan. Popul. Econ. 2002, 133, 59–63. [Google Scholar]

- Liu, X.H. Analysis on the Change of Benefits by Sex in the Course of the Old-Age Insurance Reform. Popul. Econ. 2010, 182, 58–64. [Google Scholar]

- Drew, E. Gender Balance in Social Security Reform China, EU-China Social Security Reform Co-Operation Project. Available online: http://www.academia.edu/997306/Gender_Balance_in_Social_Security_Reform_China (accessed on 20 June 2014).

- Pei, D. Gender Difference of Pension Benefits in Urban China. Available online: http://arno.uvt.nl/show.cgi?fid=121849 (accessed on 20 June 2014).

- National Bureau of Statistics of China. China Statistical Yearbook. Available online: http://www.stats.gov.cn/tjsj/ndsj/2013/indexch.htm (accessed on 12 May 2014).

- Organisation for Economic Co-operation and Development (OECD). Ageing Societies. OECD Factbook 2009: Economic, Environmental and Social Statistics; OECD Publishing: Paris, France, 2009. Available online: http://dx.doi.org/10.1787/factbook-2009-3-en (accessed on 12 May 2014).

- National Bureau of Statistics of China. China Population Census. Available online: http://www.stats.gov.cn/tjsj/pcsj/rkpc/6rp/indexch.htm (accessed on 12 March 2014).

- Meng, X. Labor Market Outcomes and Reforms in China. J. Econ. Perspect. 2012, 26, 75–102. [Google Scholar] [CrossRef]

- China Daily. Gender Income Gap Continues to Widen. Available online: http://www.chinadaily.com.cn/china/2013-05/16/content_16502360.htm (accessed on 12 May 2014).

- Feng, J.; Hu, Y. An Empirical Study of Early Retirement in Urban China. Chin. J. Popul. Sci. 2008, 4, 88–96. [Google Scholar]

- Yang, Y.N. Empirical Research on Influencing Factors of Retirement Age in China. Insur. Stud. 2011, 11, 61–71. [Google Scholar]

- Sin, Y. China: Pension Liabilities and Reform Options for Old Age Insurance; Working Paper No. 2005-1; World Bank: Washington, DC, USA, 2005. [Google Scholar]

- Ministry of Human Resources and Social Security (China). Annual Human Resources and Social Security Development Statistical Bulletin of 2011. Available online: http://www.mohrss.gov.cn/SYrlzyhshbzb/zwgk/szrs/ndtjsj/tjgb/201206/t20120605_69908.htm (accessed on 12 May 2014).

- Yang, Y.N.; Shen, S.G. Inflation and Wage Growth: New Method and Systematic Scheme for the Adjustment of China’s Basic Pension System. Insur. Stud. 2012, 8, 95–103. [Google Scholar]

- Wang, Z.Y.; Zeng, X.Q. An Analysis of the Relation between Chinese Social Security Benefit Incentives and Enterprise Staff and Workers Retirement Age. J. Renmin Univ. 2004, 6, 74–78. [Google Scholar]

© 2015 by the authors; licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Chen, T.; Turner, J.A. Gender and Public Pensions in China: Do Pensions Reduce the Gender Gap in Compensation? Sustainability 2015, 7, 1355-1369. https://doi.org/10.3390/su7021355

Chen T, Turner JA. Gender and Public Pensions in China: Do Pensions Reduce the Gender Gap in Compensation? Sustainability. 2015; 7(2):1355-1369. https://doi.org/10.3390/su7021355

Chicago/Turabian StyleChen, Tianhong, and John A. Turner. 2015. "Gender and Public Pensions in China: Do Pensions Reduce the Gender Gap in Compensation?" Sustainability 7, no. 2: 1355-1369. https://doi.org/10.3390/su7021355

APA StyleChen, T., & Turner, J. A. (2015). Gender and Public Pensions in China: Do Pensions Reduce the Gender Gap in Compensation? Sustainability, 7(2), 1355-1369. https://doi.org/10.3390/su7021355