Key Success Factors That Enable IT Service Providers to Achieve Organizational Performance: Evidence from Romania

Abstract

:1. Introduction

2. Literature Review and Hypothesis Development

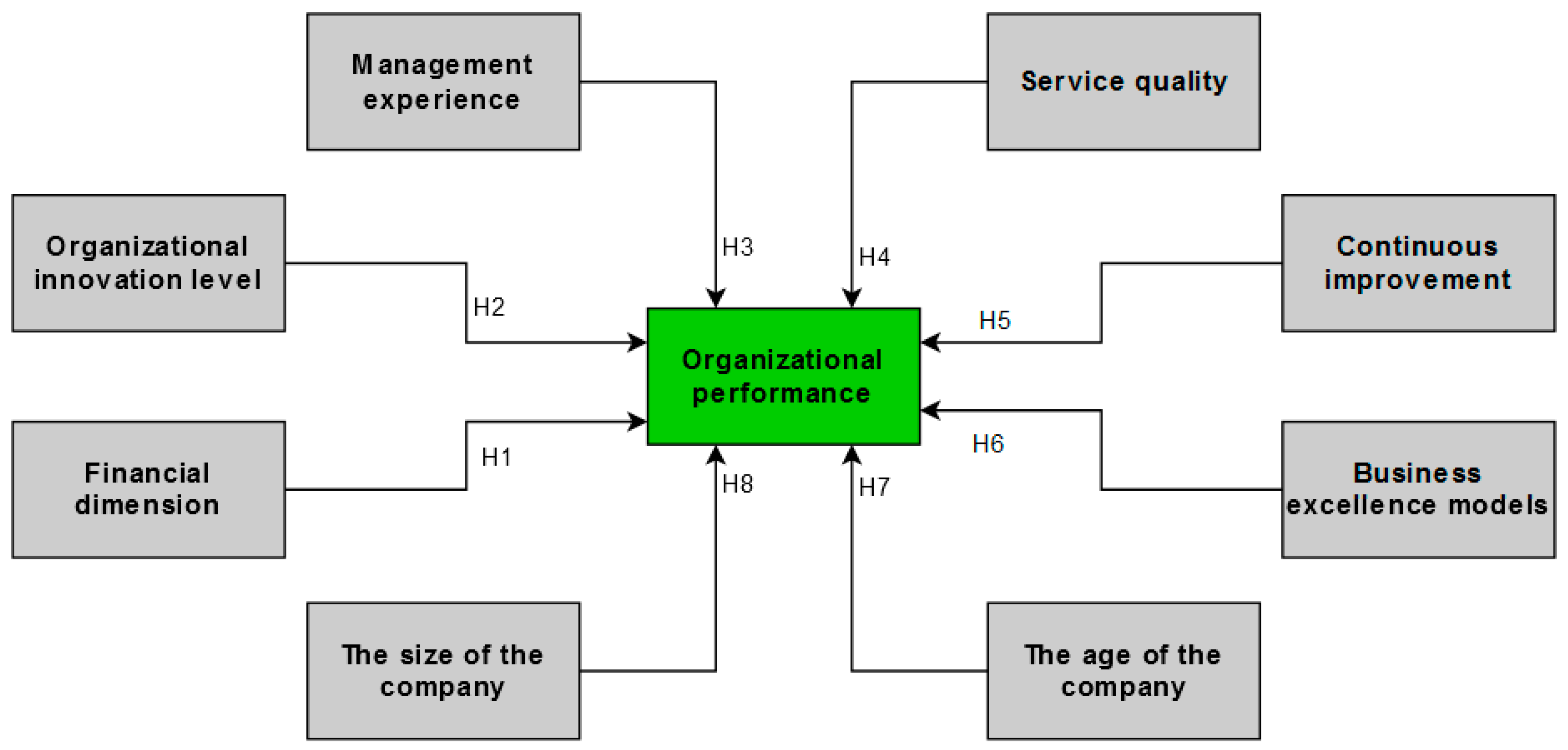

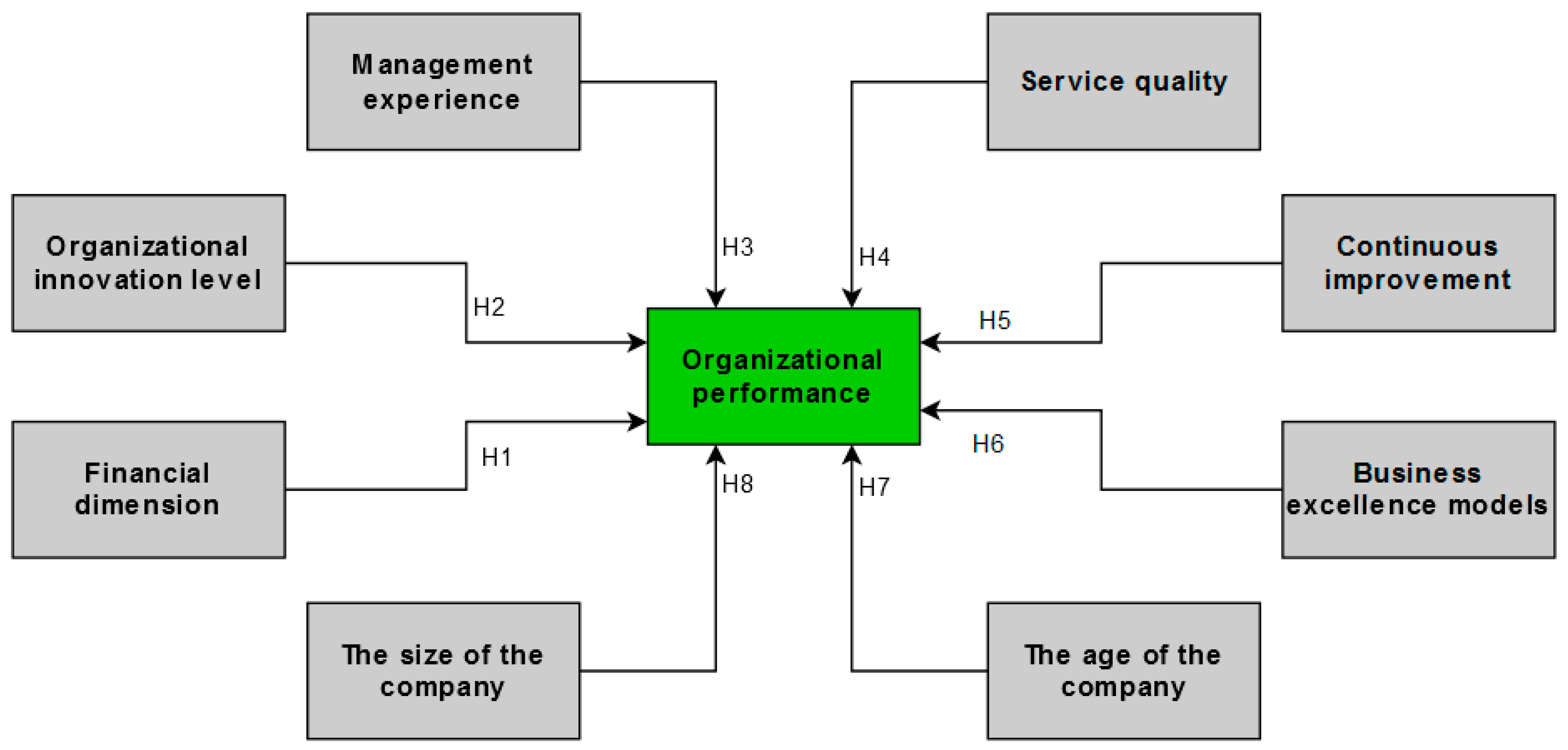

2.1. Relationship between the Financial Dimension and Organizational Performance

2.2. Relationship between the Organizational Innovation Level and Organizational Performance

2.3. Relationship between Management Experience and Organizational Performance

2.4. Relationship between Service Quality and Organizational Performance

2.5. Relationship between Continuous Improvement and Organizational Performance

2.6. Relationship between Business Excellence and Organizational Performance

2.7. Relationship between Organizational Performance, the Size of the Company, and the Age of the Company

2.8. Conceptual Framework

3. Research Methodology

3.1. Survey Data

3.2. Measurement Instrument

3.3. The Reliability of the Data

4. Results

4.1. Analyzing the Level of Perceived Organizational Performance of Companies Providing IT Services

4.2. Determining the Main Factors That Influence the Organizational Performance of Companies Providing IT Services

5. Discussion

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Cucinotta, D.; Vanelli, M. WHO Declares COVID-19 a Pandemic. Acta Biomed. Atenei Parm. 2020, 91, 157–160. [Google Scholar]

- Jung, J.-H.; Shin, J.-I. Big Data Analysis of Media Reports Related to COVID-19. Int. J. Environ. Res. Public Health 2020, 17, 5688. [Google Scholar] [CrossRef]

- Chowdhury, S.A.; Akter, S.; Chowdhury, M.M.; Ahsan, S.M.H.; Yasir Arafat, A.B.M. Is COVID-19 a Blessing for Ecommerce: A View from Bangladesh. Glob. J. Manag. Bus. Res. 2021. Available online: https://journalofbusiness.org/index.php/GJMBR/article/view/3366 (accessed on 28 July 2021).

- Bhatti, A.; Akram, H.; Basit, H.M.; Khan, A.U.; Raza, S.M.; Bilal, M. E-commerce trends during COVID-19 Pandemic. Int. J. Future Gener. Commun. Netw. 2020, 13, 5. [Google Scholar]

- Priyono, A.; Moin, A.; Putri, V.N.A.O. Identifying Digital Transformation Paths in the Business Model of SMEs during the COVID-19 Pandemic. J. Open Innov. Technol. Mark. Complex. 2020, 6, 104. [Google Scholar] [CrossRef]

- Hasanat, M.W.; Hoque, A.; Shikha, F.A.; Anwar, M.; Hamid, A.B.A.; Tat, H.H. The Impact of Coronavirus (Covid-19) on E-Business in Malaysia. Asian J. Multidiscip. Stud. 2020, 3, 85–90. [Google Scholar]

- Xayrullaevna, S.N.; Pakhritdinovna, K.D.; Anvarovna, B.G. Digitalization of the economy during a pandemic: Accelerating the pace of development. J. Crit. Rev. 2020, 7, 2491–2498. [Google Scholar]

- Jung, S.; Wortmann, F.; Bronner, W.; Gassmann, O. Platform Economy: Converging IoT Platforms and Ecosystems. In Connected Business; Gassmann, O., Ferrandina, F., Eds.; Springer: Cham, Switzerland, 2021. [Google Scholar]

- Hamann, P.M.; Schiemann, F.; Bellora, L.; Guenther, T.W. Exploring the dimensions of organizational performance: A construct validity study. Organ. Res. Methods 2013, 16, 67–87. [Google Scholar] [CrossRef]

- Devinney, T.M.; Yip, G.S.; Johnson, G. Using frontier analysis to evaluate company performance. Br. J. Manag. 2010, 21, 921–938. [Google Scholar] [CrossRef]

- Combs, J.G.; Crook, T.R.; Shook, C.L. The dimensionality of organizational performance and its implications for strategic management research. In Research Methodology in Strategy and Management; Ketchen, D.J., Bergh, D.D., Eds.; Emerald Group Publishing Limited: Bingley, UK, 2005; Volume 2, pp. 259–286. [Google Scholar]

- Wong, C.-S.; Law, K.S.; Huang, G.-H. On the importance of conducting construct-level analysis for multidimensional constructs in theory development and testing. J. Manag. 2008, 34, 744–764. [Google Scholar] [CrossRef] [Green Version]

- Sink, S.; Tuttle, T. Planning and Measurement in your Organization of the Future; Industrial Engineering and Management Press: Norcross, GA, USA, 1989. [Google Scholar]

- Rolstadas, A. Enterprise performance measurement. Int. J. Oper. Prod. Manag. 1998, 18, 989–999. [Google Scholar] [CrossRef]

- Cozza, C.; Malerba, F.; Mancusi, M.L.; Perani, G.; Vezzulli, A. Innovation, profitability and growth in medium and high-tech manufacturing industries: Evidence from Italy. Appl. Econ. 2012, 44, 1963–1976. [Google Scholar] [CrossRef]

- Fukuyama, H.; Tan, Y. Implementing strategic disposability for performance evaluation: Innovation, stability, profitability and corporate social responsibility in Chinese banking. Eur. J. Oper. Res. 2021, 296, 652–668. [Google Scholar] [CrossRef]

- Verboncu, I.; Zalman, M. Management şi Performanţe; Universitary Publishing House: Bucharest, Romania, 2005. [Google Scholar]

- Albu, N.; Albu, C. Soluţii Practice de Eficientizare a Activităţilor şi de Creştere a Performanţei Organizaţionale; Editura CECCAR: Bucharest, Romania, 2005. [Google Scholar]

- Menu, M. Controlul Performanței în Management; Editura Tehnica-Info: Chişinău, Republic of Moldova, 2009. [Google Scholar]

- Manciu, I.; Marian, L.; Leşe, I.; Chibelean, C. The impact of using the mathematic model on managerial performance. Rev. De Manag. Şi Ing. Econ. 2018, 17, 504–513. [Google Scholar]

- Lebas, M. Performance measurement and performance management. Int. J. Prod. Econ. 1995, 41, 23–35. [Google Scholar] [CrossRef]

- Suárez-Gargallo, C.; Zaragoza-Sáez, P. How the Balanced Scorecard Is Implemented in the Spanish Footwear Industry. Sustainability 2021, 13, 5641. [Google Scholar] [CrossRef]

- Perkbox. Available online: https://www.perkbox.com/uk/resources/blog/why-employee-motivation-is-important-and-how-to-improve-measure-and-maintain-it (accessed on 1 July 2021).

- Richard, P.J.; Devinney, T.M.; Yip, G.S.; Johnson, G. Measuring organizational performance: Towards methodological best practice. J. Manag. 2009, 35, 718–804. [Google Scholar] [CrossRef] [Green Version]

- Pollard, C.; Cater-Steel, A. Justifications, strategies, and critical success factors in successful ITIL implementations in U.S. and Australian companies: An exploratory study. Inf. Syst. Manag. 2009, 26, 164–175. [Google Scholar] [CrossRef] [Green Version]

- Bordoloi, S.; Fitzsimmons, J.; Fitzsimmons, M. Service Management: Operations, Strategy, Information Technology; McGraw-Hill Education: New York, NY, USA, 2018. [Google Scholar]

- The European Commission Mutual Learning Programme for Public Employment Services, 2012, Organisational Development, Improvement and Innovation Management in Public Employment Services. Available online: https://ec.europa.eu/social/BlobServlet?docId=14104&langId=en (accessed on 13 November 2020).

- Financial Paper. Available online: https://www.zf.ro/banci-si-asigurari/it-ul-vedeta-economiei-romanesti-sectorul-castigator-pandemiei-prima-19654861 (accessed on 22 June 2021).

- Global Knowledge. Available online: https://www.globalknowledge.com/us-en/resources/resource-library/articles/12-challenges-facing-it-professionals/#gref (accessed on 22 June 2021).

- Yoopetch, C.; Nimsai, S.; Kongarchapatara, B. The Effects of Employee Learning, Knowledge, Benefits, and Satisfaction on Employee Performance and Career Growth in the Hospitality Industry. Sustainability 2021, 13, 4101. [Google Scholar] [CrossRef]

- Hannabarger, C.; Buchman, R.; Economy, P. Goals, Scores, and the Balanced Scorecard. In Balanced Scorecard Strategy for Dummies; John Wiley and Sons: Indianapolis, IN, USA, 2007. [Google Scholar]

- Barbu, A.; Militaru, G. The Key Indicators Used to Measure the Performance of the Service Companies: A Literature Review. Ovidius Univ. Ann. Ser. Econ. Sci. 2019, 19, 355–364. [Google Scholar]

- Cleary, P.; Quinn, M. Intellectual capital and business performance. J. Intellect. Cap. 2016, 17, 255–278. [Google Scholar] [CrossRef] [Green Version]

- Holler, A. New Metrics for Value-Based Management. Enhancement of Performance Measurement and Empirical Evidence on Value-Relevance; Gabler: Heidelberg, Germany, 2009. [Google Scholar]

- Ebert, C.; Dumke, R.; Bundschuh, M.; Schmietendorf, A. Best Practices in Software Measurement: How to Use Metrics to Improve Project and Process Performance; Springer: Berlin, Germany, 2005. [Google Scholar]

- Kerzner, H. Project Management Metrics, KPIs, And Dashboards. A Guide to Measuring and Monitoring Project Performance, 3rd ed.; John Wiley and Sons: New Jersey, NJ, USA, 2017. [Google Scholar]

- Okes, D. Performance Metrics. The Levers for Process Management; ASQ Quality Press: Milwaukee, WI, USA, 2013. [Google Scholar]

- Militaru, G. Financial Management; Politehnica Press: Bucharest, Romania, 2015. [Google Scholar]

- Horváthová, E. Does environmental performance affect financial performance? A meta-analysis. Ecol. Econ. 2010, 70, 52–59. [Google Scholar] [CrossRef]

- Huang, C.J. Corporate governance, corporate social responsibility and corporate performance. J. Man. Org. 2010, 16, 641–655. [Google Scholar] [CrossRef]

- Magness, V. Strategic posture, financial performance and environmental disclosure: An empirical test of legitimacy theory. Account. Audit. Account. 2006, 19, 540–563. [Google Scholar] [CrossRef]

- Donker, H.; Poff, D.; Zahir, S. Corporate values, codes of ethics, and firm performance: A look at the Canadian context. J. Bus. Ethics 2008, 82, 527–537. [Google Scholar] [CrossRef]

- Berrone, P.; Surroca, J.; Tribó, J.A. Corporate ethical identity as a determinant of firm performance: A test of the mediating role of stakeholder satisfaction. J. Bus. Ethics 2007, 76, 35–53. [Google Scholar] [CrossRef]

- Chang, W.; Ellinger, A.E.; Kim, K.; Franke, G.R. Supply chain integration and firm financial performance: A meta-analysis of positional advantage mediation and moderating factors. Eur. Manag. J. 2016, 34, 282–295. [Google Scholar] [CrossRef]

- Prajogo, D. The relationship Between Innovation and Business Performance—A Comparative Study Between Manufacturing and Service Firms. Knowl. Process. Manag. 2006, 13, 218–225. [Google Scholar] [CrossRef]

- Hall, L.A.; Bagchi-Sen, S. A study of R&D, innovation, and business performance in the Canadian biotechnology industry. Technovation 2002, 22, 231–244. [Google Scholar]

- Barbu, A.; Militaru, G. The Moderating Effect of Intellectual Property Rights on Relationship between Innovation and Company Performance in Manufacturing Sector. Procedia Manuf. 2019, 32, 1077–1084. [Google Scholar] [CrossRef]

- Barbu, A.; Militaru, G.; Fleacă, B.; Corocăescu, M. The Mediating Role of the Policy of Rewarding Creative Employees on the Relationship between the Personal Innovation Potential and Organizational Innovation. Evidence from Romania. In Proceedings of the 6th Review of Management and Economic Engineering International Management Conference, Cluj-Napoca, Romania, 20–22 September 2018; Todesco Publishing House: Cluj-Napoca, Romania, 2018; pp. 315–322. [Google Scholar]

- Barbu, A.; Militaru, G. Investigating the Innovation Potential of a Company Obtained Through Social Media. In Proceedings of the 12th International Management Conference “Management Perspectives in the Digital Era”, Bucharest, Romania, 1–2 November 2018; Editura ASE: Bucharest, Romania, 2018; pp. 247–258. [Google Scholar]

- Fang, S.C.; Wang, M.C.; Chen, P.C. The influence of knowledge networks on a firm’s innovative performance. J. Manag. Organ. 2017, 23, 22–45. [Google Scholar]

- Wooldridge, B.; Floyd, S.W. The strategy process, middle management involvement, and organizational performance. Strateg. Manag. J. 1990, 11, 231–241. [Google Scholar] [CrossRef]

- Armistead, C. Knowledge management and process performance. J. Knowl. Manag. 1999, 3, 143–157. [Google Scholar] [CrossRef]

- Chang, J. Business Process Management Systems. Strategy and Implementation, 1st ed.; Auerbach Publications: New York, NY, USA, 2006. [Google Scholar]

- Prajogo, D.; Toy, J.; Bhattacharya, A.; Oke, A.; Cheng, T.C.E. The Relationships Between Information Management, Process Management and Operational Performance: Internal and External Contexts. Int. J. Prod. Econ. 2018, 199, 95–103. [Google Scholar] [CrossRef]

- Miers, D. BPM: Driving Business Performance. BP Trends 2005, 5, 1–13. [Google Scholar]

- Salomo, S.; Weise, J.; Gemünden, H.G. NPD Planning Activities and Innovation Performance: The Mediating Role of Process Management and the Moderating Effect of Product Innovativeness. J. Prod. Innov. Manag. 2007, 24, 285–302. [Google Scholar] [CrossRef]

- Jacot, J. De la trilogie: Productivité, compétitivité, réntabilité a l’évaluation sociale de la performance industrielle. In Entreprise et Performance Globale: Outils, Évaluation, Pilotage; Economica: Paris, France, 1997; pp. 29–37. [Google Scholar]

- Pottier, P. Introduction à la gestion; Faucher: Paris, France, 2000. [Google Scholar]

- Militaru, G. Service Management; C.H. Beck: Bucharest, Romania, 2010. [Google Scholar]

- Fitzsimmons, J.; Fitzsimmons, M. Service Management; McGraw-Hill: New York, NY, USA, 2003. [Google Scholar]

- Deming, W. Quality, Productivity and Competitive Position; Cambridge: Cambridge, MA, USA, 1982. [Google Scholar]

- Halawi, A.; Haydar, N. Effects of Training on Employee Performance: A Case Study of Bonjus and Khatib & Alami Companies. Int. Humanit. Stud. 2018, 5, 24–45. [Google Scholar]

- Iqbal, A. The strategic human resource management approaches and organisational performance: The mediating role of creative climate. J. Adv. Manag. Res. 2019, 16, 181–193. [Google Scholar] [CrossRef]

- Deselnicu, D.C.; Swiger, J.A.; Albu, L.; Doman, C. Leadership Performance in Romanian Companies. Case Study. In Proceedings of the 3rd International Conference on Advanced Materials and Systems, Bucharest, Romania, 16–18 September 2010; Certex Publishing House: Bucharest, Romania; pp. 509–514. [Google Scholar]

- Harrington, H. The five pillars of organizational excellence. Handb. Bus. Strategy 2005, 6, 107–114. [Google Scholar] [CrossRef]

- McAdam, R. Quality models in an SME context. Int. J. Qual. Reliab. Manag. 2000, 17, 305–323. [Google Scholar] [CrossRef]

- Cameron, K.S.; Quinn, R.E. Diagnosing and Changing Organizational Culture: Based on the Competing Values Framework; John Wiley & Sons: Hoboken, NJ, USA, 2011. [Google Scholar]

- Cătuneanu, V. Quality Improvement; Romanian Foundation for Quality Promotion: Bucharest, Romania, 2003; pp. 100–103. [Google Scholar]

- Crişan, C. Elaboration of Recommendations for Public Policies at Central and Local Level. Available online: https://econ.ubbcluj.ro/documente2013/Documente%20justificative%20martie%202013-%20iulie%202013/Activitatea%20WP%2011.5/Wp.11.5%20Recomandari%20pentru%20politicile%20publice%20la%20nivel%20central%20si%20local.docx (accessed on 13 November 2020).

- Mann, R.; Adebanjo, D.; Tickle, M. Deployment of business excellence in Asia: An exploratory study. Int. J. Qual. Reliab. Manag. 2011, 28, 604–627. [Google Scholar] [CrossRef] [Green Version]

- Vadari, S.; Parandker, S.R. A systems approach to business excellence to improve the sustainability of an organization. In Proceedings of the 2011 Annual IEEE India Conference, Engineering Sustainable Solutions, Hyderabad, India, 16–18 December 2011; pp. 1–4. [Google Scholar]

- EFQM. Available online: https://www.efqm.org/ (accessed on 16 March 2021).

- Business Excellence Tools. Available online: https://www.businessexcellencetools.com/business-excellence/ (accessed on 1 September 2021).

- Araújo, M.; Sampaio, P. The path to excellence of the Portuguese organisations recognised by the EFQM model. Total Qual. Manag. Bus. Excell. 2014, 25, 427–438. [Google Scholar] [CrossRef] [Green Version]

- Dahlgaard-Park, S. Reviewing the European excellence model from a management control view. TQM J. 2008, 20, 98–119. [Google Scholar] [CrossRef]

- Majumdar, S.K. The Impact of Size and Age on Firm-Level Performance: Some Evidence from India. Rev. Ind. Organ. 1997, 12, 231–241. [Google Scholar] [CrossRef]

- Coad, A.; Segarra, A.; Teruel, M. Like milk or wine: Does firm performance improve with age? Struct. Chang. Econ. Dyn. 2013, 24, 173–189. [Google Scholar] [CrossRef] [Green Version]

- Pervan, M.; Pervan, I.; Ćurak, M. The Influence of Age on Firm Performance: Evidence from the Croatian Food Industry. J. East. Eur. Res. Bus. Econ. 2017, 2017, 1–10. [Google Scholar] [CrossRef] [Green Version]

- Odalo, S.K.; Achoki, G.; Njuguna, A. Relating Company Size and Financial Performance in Agricultural Firms Listed in the Nairobi Securities Exchange in Kenya. Int. J. Econ. Financ. 2016, 8, 34–40. [Google Scholar] [CrossRef] [Green Version]

- Utami, E.S.; Hasan, M. The Role of Corporate Social Responsibility on the Relationship between Financial Performance and Company Value. J. Asian Financ. Econ. Bus. 2021, 8, 1249–1256. [Google Scholar]

- Fujiant, L. Top Management Characteristics and Company Performance: An Empirical Analysis on Public Companies Listed in the Indonesian Stock Exchange. Eur. Res. Stud. J. 2018, XXI, 62–76. [Google Scholar] [CrossRef] [Green Version]

- Becker-Blease, J.R.; Kaen, F.R.; Etebari, A.; Baumann, H. Employees, firm size and profitability in U.S. manufacturing industries. Invest. Manag. Financ. Innov. 2010, 7, 7–23. [Google Scholar]

- Mahzura, T.A.S. The Analysis of the Influence of Financial Performance, Company Size, Ownership Structure, Leverage and Company Growth on Company Values in Food and Beverage Industry Companies Listed in IDX 2012–2016 Period. Int. J. Public Budg. Account. Financ. 2018, 1, 1–12. [Google Scholar]

- Commission Recommendation of 6 May 2003 Concerning the Definition of Micro, Small and Medium-Sized Enterprises (Text with EEA Relevance) (Notified under Document Number C(2003) 1422) OJ L 12420.5. 2003, pp. 36–41. Available online: http://data.europa.eu/eli/reco/2003/361/oj (accessed on 16 July 2021).

- Kaplan, R.; Norton, D. The Balanced Scorecard: Measures That Drive Performance. Harv. Bus. Rev. 1992, 70, 71–79. [Google Scholar]

- Heskett, J.L.; Jones, T.O.; Loveman, G.W.; Sasser, E., Jr.; Schlesinger, L.A. Putting the Service-Profit Chain to Work. Harv. Bus. Rev. 1994, 72, 164–170. [Google Scholar]

- Koys, D.J. The Effects of Employee Satisfaction, Organizational Citizenship Behavior, and Turnover on Organizational Effectiveness: A Unit-Level, Longitudinal Study. Pers. Psychol. 2001, 54, 101–114. [Google Scholar] [CrossRef]

- Larivière, B. Linking Perceptual and Behavioral Customer Metrics to Multiperiod Customer Profitability: A Comprehensive Service-Profit Chain Application. J. Serv. Res. 2008, 11, 3–21. [Google Scholar] [CrossRef]

- Coviello, N.; Winklhofer, H.; Hamilton, K. Marketing Practices and Performance of Small Service Firms: An Examination în the Tourism Accommodation Sector. J. Serv. Res. 2006, 9, 38–58. [Google Scholar] [CrossRef]

- Tseng, L.-M.; Wu, J.-Y. How can financial organizations improve employee loyalty? The effects of ethical leadership, psychological contract fulfillment and organizaţional identification. Leadersh. Organ. Dev. J. 2017, 38, 679–698. [Google Scholar] [CrossRef]

- Meyer, J.; Stanley, D.; Herscovitch, L.; Topolnytsky, L. Affective, Continuance, and Normative Commitment to the Organization: A Meta-analysis of Antecedents, Correlates, and Consequences. J. Vocat. Behav. 2002, 61, 20–52. [Google Scholar] [CrossRef]

- Cotton, J.; Tuttle, J. Employee Turnover: A Meta-Analysis and Review with Implications for Research. Acad. Manag. Rev. 1986, 11, 55–70. [Google Scholar] [CrossRef]

- Griffeth, R.W.; Hom, P.W.; Gaertner, S. A Meta-Analysis of Antecedents and Correlates of Employee Turnover: Update, Moderator Tests, and Research Implications for the Next Millennium. J. Manag. 2000, 26, 463–488. [Google Scholar] [CrossRef]

- Brown, S.P.; Lam, S.K. A Meta-Analysis of Relationships Linking Employee Satisfaction to Customer Responses. J. Retail. 2008, 84, 243–255. [Google Scholar] [CrossRef]

- Saks, A. Antecedents and consequences of employee engagement. J. Manag. Psychol. 2006, 21, 600–619. [Google Scholar] [CrossRef] [Green Version]

- International Organization for Standardization. Available online: https://www.iso.org/iso-9001-quality-management.html (accessed on 22 June 2021).

- Siougle, E.; Dimelis, S.; Economidou, C. Does ISO 9000 certification matter for firm performance? A group analysis of Greek listed companies. Int. J. Prod. Econ. 2019, 209, 2–11. [Google Scholar]

- Kakouris, A.; Sfakianaki, E. Impacts of ISO 9000 on Greek SMEs business performance. Int. J. Qual. Reliab. Manag. 2018, 35, 2248–2271. [Google Scholar]

- Chiarini, A. From Total Quality Control to Lean Six Sigma. Evolution of the Most Important Management Systems for the Excellence; Springer: New York, NY, USA, 2012. [Google Scholar]

- Chams, N.; García-Blandón, J.; Hassan, K. Role Reversal! Financial Performance as an Antecedent of ESG: The Moderating Effect of Total Quality Management. Sustainability 2021, 13, 7026. [Google Scholar] [CrossRef]

- Klefsjo, B.; Wiklund, H.; Edgeman, R.L. Six sigma seen as a methodology for total quality management. Meas. Bus Excell. 2001, 5, 31–35. [Google Scholar] [CrossRef]

- Adebanjo, D. TQM and business excellence: Is there really a conflict? Meas. Bus. Excell. 2001, 5, 37–40. [Google Scholar] [CrossRef] [Green Version]

- The Association of Accountants and Financial Professionals in Business. Available online: https://higherlogicdownload.s3.amazonaws.com/IMANET/9c3fec55-8e4a-4c76-80f7-e0f5f2927b3f/UploadedImages/Six_Sigma_n_Process_Improvement_25Jan20.pdf (accessed on 23 July 2021).

- Przekop, P. Six Sigma for Business Excellence: A Manager’s Guide to Supervising Six Sigma Projects and Teams; McGraw-Hill: New York, NY, USA, 2003. [Google Scholar]

- Charantimath, P. Total Quality Management, 3rd ed.; Pearson: Uttar Pradesh, India, 2017. [Google Scholar]

- Snee, R.D. Lean Six Sigma–Getting better all the time. Int. J. Lean Six Sigma 2010, 1, 9–29. [Google Scholar] [CrossRef]

- Zhan, W.; Ding, X. Engineering Management Collection: Lean Six Sigma and Statistical Tools for Engineers and Engineering Managers; Momentum Press: New York, NY, USA, 2016. [Google Scholar]

- EFQM. The EFQM Model Brochure; EFQM: Brussels, Belgium, 2019; pp. 1–42. [Google Scholar]

- Anbuselvan, S.; Kumar, D.N. Challenges Faced by Professors in Online Teaching during COVID-19 Pandemic with Special Reference to Madurai District of Tamilnadu. Res. Explor. Blind Rev. Ref. Q. Int. J. 2020, 1, 1–9. [Google Scholar]

- Alipour, S.; Zohreh, Z.; Ghadiri, M. Validating Factor Structure of the Persian Version of Emotion Regulation Strategies Inventory among Iranian EFL University Teachers. Appl. Res. Engl. Lang. 2021, 10, 81–104. [Google Scholar]

- Perry, R.H.; Charlotte, B.; Isabella, M.; Bob, C. SPSS Explained; Routledge Taylor & Francis Group: New York, NY, USA, 2004. [Google Scholar]

- Taber, K.S. The Use of Cronbach’s Alpha When Developing and Reporting Research Instruments in Science Education. Res. Sci. Educ. 2017, 48, 1273–1296. [Google Scholar] [CrossRef]

- Evans, J.D. Straightforward Statistics for the Behavioral Science; Brooks/Cole Publishing Company: Pacific Grove, CA, USA, 1996. [Google Scholar]

- Jankalová, M.; Jankal, R. Sustainability Assessment According to the Selected Business Excellence Models. Sustainability 2018, 10, 3784. [Google Scholar] [CrossRef] [Green Version]

- Slapper, T.F.; Hall, T.J. The Triple Bottom Line: What Is It and How Does It Work? Indiana Bus. Rev. 2011, 2011, 1–8. [Google Scholar]

- Cai, S.; Jun, M. A qualitative study of the internalization of ISO 9000 standards: The linkages among firms’ motivations, internalization processes, and performance. Int. J. Prod. Econ. 2018, 196, 248–260. [Google Scholar] [CrossRef]

- Azanha, A.; Argoud, A.R.T.T.; Camargo Junior, J.B.; Antoniolli, P.D. Agile project management with Scrum. Int. J. Proj. Manag. Bus. 2017, 10, 121–142. [Google Scholar] [CrossRef]

- Lei, H.; Ganjeizadeh, F.; Jayachandran, P.K.; Ozcan, P. A statistical analysis of the effects of Scrum and Kanban on software development projects. Robot Comput. Integr. Manuf. 2017, 43, 59–67. [Google Scholar] [CrossRef]

- Barbu, A.; Militaru, G.; Savu, I.C. The Influence of the Financial-Accounting Process on the Performance of the Organizations in the Field of Services. In Proceedings of the 7th Review of Management and Economic Engineering, International Management Conference, “Management Challenges Within Globalization”, Cluj-Napoca, Romania, 17–19 September 2020; Todesco Publishing House: Cluj Napoca, Romania, 2020; pp. 530–536. [Google Scholar]

- Economica.net. Available online: https://www.economica.net/analiza-industria-de-software-din-romania-va-creste-la-un-maxim-istoric-de-peste-8-miliarde-de-euro-in-2020-topul-companiilor_193563.html (accessed on 30 June 2021).

{kind=link}

| Gender | Position | Experience in the IT Sector | Total | ||

|---|---|---|---|---|---|

| Less than 3 Years | Between 3 and 5 Years | Between 5 and 10 Years | |||

| Male | Leadership | 0 | 1 | 1 | 2 |

| Execution | 18 | 5 | 3 | 26 | |

| Total | 18 | 6 | 4 | 28 | |

| Female | Execution | 11 | 3 | 2 | 16 |

| Total | 11 | 3 | 2 | 16 | |

| Construct | Variables | References |

|---|---|---|

| Organizational performance (OP) | Profitability | [36,37,38,39,40,41,42,43,44,45,46,85,86,87,88] |

| Revenue | [36,37,38,39,40,41,42,43,44,45,46,85,86,87,88] | |

| Market share | [85,86,87,88] | |

| Service quality | [73,85,86,87,88,89] | |

| Customers’ satisfaction | [73,85,86,87,88,89] | |

| Employees’ satisfaction | [73,85,86,87,88,89] | |

| Processes | [73,85,86,87,88,89] | |

| Stakeholders’ satisfaction | [85] |

| Factors | Variables | References |

|---|---|---|

| Financial dimension (F) | •Financial resources | [33,34,35,36,37,38,39,40,41,42,43,44,85] |

| •Financial results | [33,34,35,36,37,38,39,40,41,42,43,44,85] | |

| Organizational innovation level (I) | •Innovative products and services •Innovation methods and technics | [46,47,48,49,50] |

| Management experience (Me) | •Management experience | [55,56] |

| Service quality (Q) | •Perceived service quality | [59,60] |

| •Process improvement | [61] | |

| Continuous improvement (Ci) | •Employee skills | [62,90,91,92,93,94,95] |

| •Employee skills development programs | [61,90,91,92,93,94,95,96] | |

| •Application of ISO 9000 standards | [96,97,98] | |

| •Using the Six Sigma method | [99,100,101,102,103,104] | |

| •Using the Lean Six Sigma method | [105,106,107] | |

| Business excellence models (BEMs) | •Clear definition of the company’s purpose, vision, and mission | [108] |

| •Developing an organizational culture | [108] | |

| •Leadership style | [108] | |

| •Stakeholder involvement | [108] | |

| •Creating a sustainable value | [108] | |

| •Adaptation to changes in the environment | [108] | |

| •Stakeholder perceptions analysis | [108] | |

| •Analysis of the results obtained by the company | [108] | |

| Size of the company | •The size of the company | [79,80,81,82,83,84,85] |

| Age of the company | •The age of the company | [76,77,78] |

| Variables | Factor Loadings | Factor | Eigenvalues | %Variance | Cronbach’s Alpha |

|---|---|---|---|---|---|

| Financial resources | 0.843 | Financial dimension | 1.42 | 71.14 | 0.686 |

| Financial results | 0.843 | ||||

| Innovative products and services | 0.834 | Innovation | 1.37 | 68.97 | 0.645 |

| Innovation methods and techniques | 0.824 | ||||

| Service quality | 0.817 | Quality | 1.33 | 66.68 | 0.601 |

| Process improvement | 0.817 | ||||

| ISO 9000 standards | 0.881 | Continuous improvement | 2.91 | 58.26 | 0.819 |

| Six Sigma | 0.783 | ||||

| Lean Six Sigma | 0.838 | ||||

| Employees’ skills | 0.680 | ||||

| Employees’ skills development programs | 0.598 | ||||

| Company’s purpose, vision, and mission | 0.751 | Business excellence models | 4.53 | 56.67 | 0.888 |

| Leadership style | 0.760 | ||||

| Organizational culture | 0.709 | ||||

| Sustainable value | 0.808 | ||||

| Stakeholder involvement | 0.746 | ||||

| Adaptation to environmental changes | 0.630 | ||||

| Stakeholders’ perceptions | 0.735 | ||||

| Results | 0.862 | ||||

| Profitability | 0.871 | Organizational performance | 4.37 | 54.71 | 0.857 |

| Revenue | 0.679 | ||||

| Market share | 0.864 | ||||

| Service quality | 0.841 | ||||

| Customers’ satisfaction | 0.811 | ||||

| Employees’ satisfaction | 0.808 | ||||

| Processes | 0.682 | ||||

| Stakeholders’ satisfaction | 0.702 |

| Variable | Calculation Method |

|---|---|

| Organizational performance | P = (Pr + Re + Ms + Pc + Pe + Pig + Pp + Qs)/8 = 4.34 |

| Values | Frequency | Percent | Valid Percent | Cumulative Percent |

|---|---|---|---|---|

| Less concerned | 5 | 11.4 | 11.4 | 11.4 |

| Concerned | 24 | 54.5 | 54.5 | 65.9 |

| Very concerned | 15 | 34.1 | 34.1 | 100.0 |

| Total | 44 | 100.0 | 100.0 |

| Variables | Values | Sum of Squares | df | Mean Square | F | Sig. |

|---|---|---|---|---|---|---|

| Size | Between Groups | 0.187 | 2 | 0.093 | 0.218 | 0.805 |

| Within Groups | 17.541 | 41 | 0.428 | |||

| Total | 17.727 | 43 | ||||

| Age | Between Groups | 1.342 | 3 | 0.447 | 1.092 | 0.364 |

| Within Groups | 16.385 | 40 | 0.410 | |||

| Total | 17.727 | 43 |

| Factors | OP | BEMs | Ci | F | Q | Me | I |

|---|---|---|---|---|---|---|---|

| OP | - | ||||||

| BEMs | 0.755 ** | - | |||||

| Ci | 0.438 ** | 0.721 ** | - | ||||

| F | 0.264 | 0.490 ** | 0.593 ** | - | |||

| Q | 0.640 ** | 0.529 ** | 0.198 | 0.018 | - | ||

| Me | 0.478 ** | 0.569 ** | 0.573 ** | 0.300 * | 0.563 ** | - | |

| I | 0.577 ** | 0.513 ** | 0.314 * | 0.190 | 0.696 ** | 0.345 * | - |

| Variables | The Relationship with OP | Types of Correlations | |

|---|---|---|---|

| Pearson Correlation | Sig. (Two-Tailed) | ||

| Financial resources | 0.205 | 0.182 | No correlation |

| Financial results | 0.245 | 0.109 | No correlation |

| Innovation | 0.577 ** | 0.000 | Positive, moderate |

| Innovative products and services | 0.570 ** | 0.000 | Positive, moderate |

| Innovation methods and techniques | 0.584 ** | 0.000 | Positive, moderate |

| Management experience | 0.478 ** | 0.001 | Positive, moderate |

| Perceived service quality | 0.638 ** | 0.000 | Positive, strong |

| Process improvement | 0.417 ** | 0.005 | Positive, moderate |

| Application of ISO 9000 standards | 0.401 ** | 0.007 | Positive, moderate |

| Using the Six Sigma method | 0.172 | 0.263 | No correlation |

| Using the Lean Six Sigma method | 0.123 | 0.425 | No correlation |

| Employee skills | 0.543 ** | 0.000 | Positive, moderate |

| Employee skills development programs | 0.474 ** | 0.001 | Positive, moderate |

| Clear definition of the company’s purpose, vision, and mission | 0.387 ** | 0.010 | Positive, weak |

| Developing an organizational culture | 0.735 ** | 0.000 | Positive, strong |

| Leadership style | 0.575 ** | 0.000 | Positive, moderate |

| Creating a sustainable value | 0.584 ** | 0.000 | Positive, moderate |

| Stakeholder involvement | 0.506 ** | 0.000 | Positive, moderate |

| Adaptation to changes in the environment | 0.482 ** | 0.001 | Positive, moderate |

| Stakeholder perceptions analysis | 0.576 ** | 0.000 | Positive, moderate |

| Analysis of the results obtained by the company | 0.665 ** | 0.000 | Positive, strong |

| Manager’s age | 0.098 | 0.526 | No correlation |

| The Independent Variable | Equation | Model Summary | Parameter Estimates | ||||||

|---|---|---|---|---|---|---|---|---|---|

| R-Square | F | df1 | df2 | Sig. | Constant | b1 | b2 | ||

| Size of the company | Linear | 0.054 | 2.404 | 1 | 42 | 0.129 | 3.652 | 0.199 | |

| Logarithmic | 0.073 | 3.328 | 1 | 42 | 0.075 | 3.488 | 0.701 | ||

| Inverse | 0.095 | 4.393 | 1 | 42 | 0.042 | 5.036 | −2.281 | ||

| Quadratic | 0.202 | 5.199 | 2 | 41 | 0.010 | −1.642 | 3.788 | −0.571 | |

| Compound | 0.080 | 3.650 | 1 | 42 | 0.063 | 3.414 | 1.068 | ||

| Power | 0.104 | 4.869 | 1 | 42 | 0.033 | 3.255 | 0.227 | ||

| Growth | 0.080 | 3.650 | 1 | 42 | 0.063 | 1.228 | 0.066 | ||

| Exponential | 0.080 | 3.650 | 1 | 42 | 0.063 | 3.414 | 0.066 | ||

| Logistic | 0.080 | 3.650 | 1 | 42 | 0.063 | 0.293 | 0.936 | ||

| Age of the company | Linear | 0.086 | 3.933 | 1 | 42 | 0.054 | 3.903 | 0.142 | |

| Logarithmic | 0.058 | 2.609 | 1 | 42 | 0.114 | 4.083 | 0.260 | ||

| Inverse | 0.034 | 1.478 | 1 | 42 | 0.231 | 4.508 | −0.369 | ||

| Quadratic | 0.169 | 4.159 | 2 | 41 | 0.023 | 4.976 | −1.014 | 0.226 | |

| Compound | 0.082 | 3.746 | 1 | 42 | 0.060 | 3.818 | 1.039 | ||

| Power | 0.053 | 2.354 | 1 | 42 | 0.132 | 4.013 | 0.067 | ||

| Growth | 0.082 | 3.746 | 1 | 42 | 0.060 | 1.340 | 0.038 | ||

| Exponential | 0.082 | 3.746 | 1 | 42 | 0.060 | 3.818 | 0.038 | ||

| Logistic | 0.082 | 3.746 | 1 | 42 | 0.060 | 0.262 | 0.963 | ||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Barbu, A.; Militaru, G.; Deselnicu, D.C.; Catană, Ş.-A. Key Success Factors That Enable IT Service Providers to Achieve Organizational Performance: Evidence from Romania. Sustainability 2021, 13, 10996. https://doi.org/10.3390/su131910996

Barbu A, Militaru G, Deselnicu DC, Catană Ş-A. Key Success Factors That Enable IT Service Providers to Achieve Organizational Performance: Evidence from Romania. Sustainability. 2021; 13(19):10996. https://doi.org/10.3390/su131910996

Chicago/Turabian StyleBarbu, Andreea, Gheorghe Militaru, Dana Corina Deselnicu, and Ştefan-Alexandru Catană. 2021. "Key Success Factors That Enable IT Service Providers to Achieve Organizational Performance: Evidence from Romania" Sustainability 13, no. 19: 10996. https://doi.org/10.3390/su131910996

APA StyleBarbu, A., Militaru, G., Deselnicu, D. C., & Catană, Ş.-A. (2021). Key Success Factors That Enable IT Service Providers to Achieve Organizational Performance: Evidence from Romania. Sustainability, 13(19), 10996. https://doi.org/10.3390/su131910996