Corporate Social Responsibility of Foreign Multinationals in a Developing Country Context: Insights from Pakistan

1

Institute of Management Sciences (IMSciences), 1-A, E-5, Phase VII, Hayatabad 25000, Pakistan

2

Olayan School of Business, American University of Beirut, Beirut 11-0236, Lebanon

*

Author to whom correspondence should be addressed.

Sustainability 2018, 10(10), 3511; https://doi.org/10.3390/su10103511

Submission received: 31 July 2018

/

Revised: 10 September 2018

/

Accepted: 19 September 2018

/

Published: 30 September 2018

(This article belongs to the Special Issue Corporate Social Responsibility (CSR) in Developing Countries: Current Trends and Development)

Abstract

:This paper aims to explore the dynamics of corporate social responsibility (CSR) of multinational companies (MNCs) subsidiaries operating in Pakistan. To do this, the corporate social performance (CSP) model, has been modified and integrated with the relevant models of CSR for multinational companies (MNCs). Empirical evidence from MNCs operating in the developing country context was collected and analyzed from MNCs operating in Pakistan. Findings from semi-structured interviews uncover that CSR is yet to institutionalize and most MNC executives understand CSR in narrow philanthropic and ethical terms and ignore the legal and economic aspects. Interestingly, there is evidence that MNCs are able to modify global CSR strategies to respond to local contexts and issues. In addition, the sample MNCs lack systematic environmental scanning, stakeholder management and demonstrate a short-term reactive approach to CSR. We believe that the proposed theoretical framework of the study can be utilized to understand MNCs CSR practices in both developed and developing countries. However, these empirical findings are context bound and cannot be generalized.

1. Introduction

Globalisation is a new buzz of the recent world. It is a multi-dimensional process that has interlinking yet contradicting interaction of local, global and regional dimensions of social life [1]. Over the years, globalisation has provided an opportunity for MNCs to become an influential and powerful actor in society [2,3]. The power of large MNCs is not only based on the large amount of economic resources they control, but also on their ability to transfer resources around the world. MNCs have the power and latitude to choose the location and legal system within which they want to operate and as a result they can influence the social and political events of the host country or countries [4,5]. Therefore, concern over the influence and power of MNCs has been growing, particularly due to the vast expansion of MNCs in developing countries [6,7].

Academically, most of the previous research related to CSR of MNCs has got attention on the social responsiveness and performance of MNCs in the developed economies [8,9,10]. In the recent past, many scholars [3,11,12,13,14,15] provided a valuable insight regarding CSR of MNCs in the developing world and attempted to fill the vital theoretical and empirical gap. However, there is a consensus that the understanding of CSR of MNCs remains ambiguous and underdeveloped in the context of developing word [15,16,17]. Literature in the context of developing world suggests that examinations of CSR of MNCs involve a great difficulty due relativity and vagueness of the CSR concept itself [13,18,19]. Moreover, theoretical definitional ambiguity of CSR combined with the contested nature of MNCs due to institutional and contextual differences present various challenges to both academic researchers and CSR practitioners. In addition, existing literature suggests various concern and contradictory views over operations of MNCs in the developing world. For instance, developing countries strive to maintain favourable and relaxed fiscal policies to encourage investment and transfer of technology from MNCs with the expectation that foreign direct investment will benefit the local economy [20,21,22,23]. However, many developing countries lack a sufficiently robust legal framework to regulate MNCs and to protect social and environmental rights [24,25]. MNCs often take advantage of this situation, and ask for favourable investment conditions and low cost production facilities [20,21,22,23,24,25,26]. In addition, MNCs are often responsible for a range of negative spillages, from spilling toxic chemicals into rivers to overthrowing democratically elected governments in developing countries [22]. Therefore, operations of MNCs might lead to ‘uneven development’ in developing countries [26,27]. Similarly, MNCs operating in developing countries often compromise on less influential stakeholder and respond to the powerful stakeholders and compromise on the demand of less active [28]. Moreover, the large markets, cheap labour and natural resources of developing countries make MNCs vulnerable to exploitation by the host countries and MNCs [29]. Likewise, previous researchers have found that MNCs are often unable to effectively deal with important issues in the host countries, and there is a need for further examination of MNCs behaviour in the context of developing countries [12,30,31,32].

Multinational corporations are often unable to deal effectively with important issues in the host country. The criticisms documented above are often countered by evidence supporting MNCs’ positive impact on developing countries. For instance, MNCs ‘play a vital role in linking rich and poor economies and in transmitting capital, knowledge, ideas and value systems across borders’ [21] (p. 259). In addition, MNCs can facilitate the efficient use of resources, transfer modern technology and increase production capacity in developing countries. As a result, MNCs contribute to stimulating the economy of developing countries and to bridging the gap between the rich and poor countries [22].

It is very simplistic to assume that the power of MNCs can go uncontested. The recent increased economic and political power of MNCs has exponentially raised public expectations [26,33,34]. MNCs are expected to manage integration of parent company strategies with subsidiaries, address the expectations of local communities, global and local competitors, spur technological development, and achieve economies of scale [35]. Particularly, MNCs operating in developing countries face issues like ‘underdeveloped institutional environment, weak public governance, widespread bribery and corruption, lack of regulatory legislations and rules, public transparency and respect for human rights’ [36] (p. 151). It has become highly desirable to develop ethical standards such as CSR practices to gain credibly in the world of business [37]. In addition, pressure groups and activists have highlighted social inadequacies and inequalities, social cost and unregulated global production processes of MNCs and reacted to these issues through ‘consumer boycotts and media campaigns’ [26] (pp. 323–324). As a result, international organisations such as the United Nations Organization (UNO) and the Organisation for Economic Co-operation and Development (OECD) have established rules and guidelines to regulate the operations of MNCs and to encourage them to adopt socially responsible behaviour [38]. The media and NGOs have also actively brought to light the social and environmental impact of many large MNCs [39,40]. Consequently, MNCs have also begun to assess their role and placed themselves at the forefront of the social responsibility agenda through sponsorship, public relations exercises, dialogues and change in business policies [12,13,14,15,16,17,18,19,20,21,22,23,24,25,26,27,28,29,30,31,32,33,34,35,36,37,38,39,40,41].

It can be concluded from the above discussion that although MNCs can be considered as a key institutional actor in an expanding CSR agenda, they are also blamed for much of the social and environmental disruption in the modern world. Scholars have also recognised that relatively little is known about the management of CSR by MNCs in the context of developing countries [11,21,27,35,36,42,43]. In addition to this, the previous studies of CSR have primarily focused upon survey based, whereas the approach of exploratory case study has been ignored [27,28,29,30,31,32,33,34,35,36].

To fill this gap in the literature, it is much needed to expand our understanding of CSR of MNCs in developing countries from theoretical and empirical perspective. Therefore, this study attempts to contribute to the literature theoretically and empirically in relation to exploration of CSR of operating in Pakistan. More specifically, this research intends to explore CSR approaches, practices and philosophies in the context of Pakistan. These research issues would be captured by understanding the conception of MNCs’ mangers.

In the next section, this research synthesis the relevant theoretical lens from existing literature and integrate the proposed framework to justify our research aim. Then, an interpretive qualitative methodology was utilized on 10 MNCs operating in Pakistan to gather nuanced responses. In addition, empirical data from interviews was discussed in relation to proposed framework. Finally, this research paper outlines relevant theoretical and interesting empirical insights that could help to expand future research agenda in developing country context.

2. Relevant Theoretical Perspectives

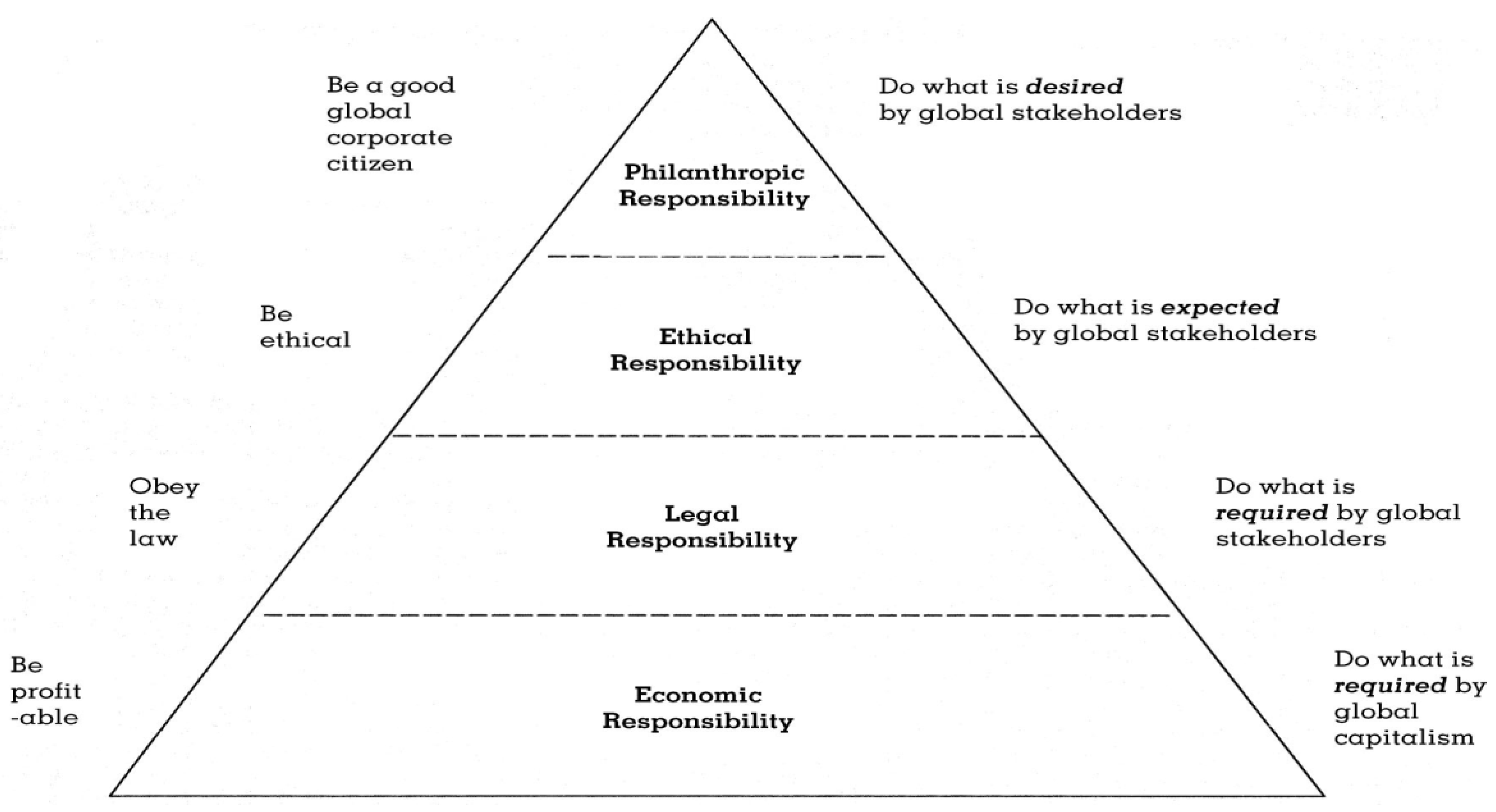

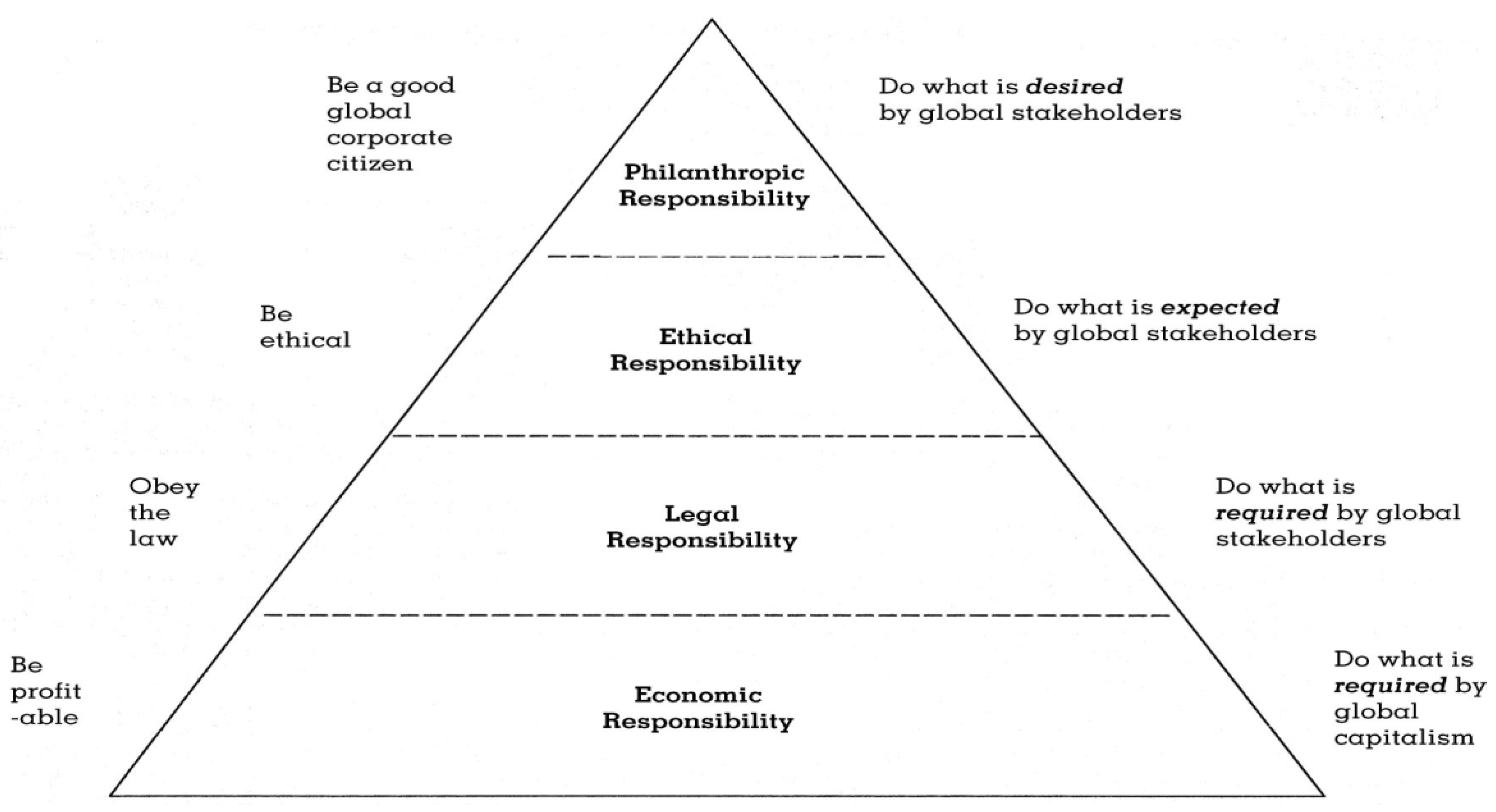

Over the last few decades, several theoretical perspectives are presented on the CSR that can provide a useful understanding of business and society relationship. It is impossible to discuss all of them in a single research article. The first most useful and perhaps one of the earliest theoretical lenses and conception was provided by Carroll [44]. Carroll classified CSR into four conceptual categories (economic, legal, ethical and philanthropic responsibilities) [45]. He argued that business and society enters a social contract and business is obliged to consider society at large. Later, In [46], Carroll revisited his CSR model and added a new rationale in the model by suggesting the inter-dependence of the four components of his previous CSP model. More recently Carroll [45] realised that globalisation and the growing number of MNCs have raised the importance of business ethics in a global context, so he attempted to incorporate the notion of global business ethics in his [46] CSP pyramid. The following (Figure 1) shows Carroll’s [45] CSR conception.

Carroll [45] put the economic responsibilities as a foundation of the pyramid. To bring in the global aspect, he argues that although companies operating in different countries operate for profitability and economic reasons, therefore, the expected rate of return might vary from country to country. Hence, the base of this reinvented framework is the same, namely economic responsibility, but regional expectations may vary. In the legal part of the pyramid, he argues that the legal system and expectations are different between different countries. Therefore, it is important for MNCs to understand and act responsibly according to local legal systems [45]. The third level of Carroll’s [45] pyramid contains ethical responsibility. He argues that MNCs must be concerned with the global community’s norms, standards and beliefs to protect their reputation. Carroll [45] argued that it is vital for MNCs to identify and reconcile home and host country ethics to satisfy the needs of both. At the top of the pyramid, philanthropic responsibilities represent the expectations of the global society, whereby business will participate in social activities that are neither mandatory by law nor expected ethical responsibilities. Moreover, like ethical and legal responsibilities, it is important for executives to identify the philanthropic expectations in the local context [45].

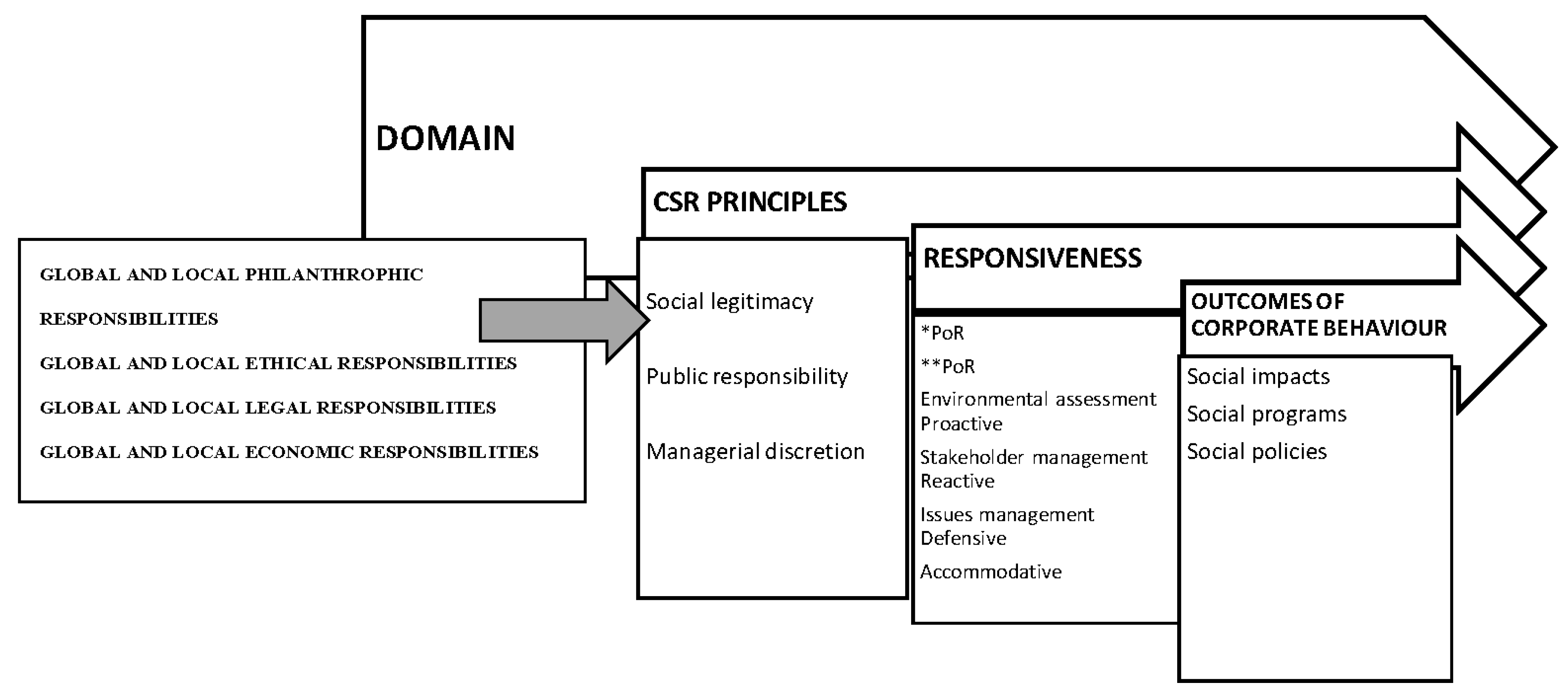

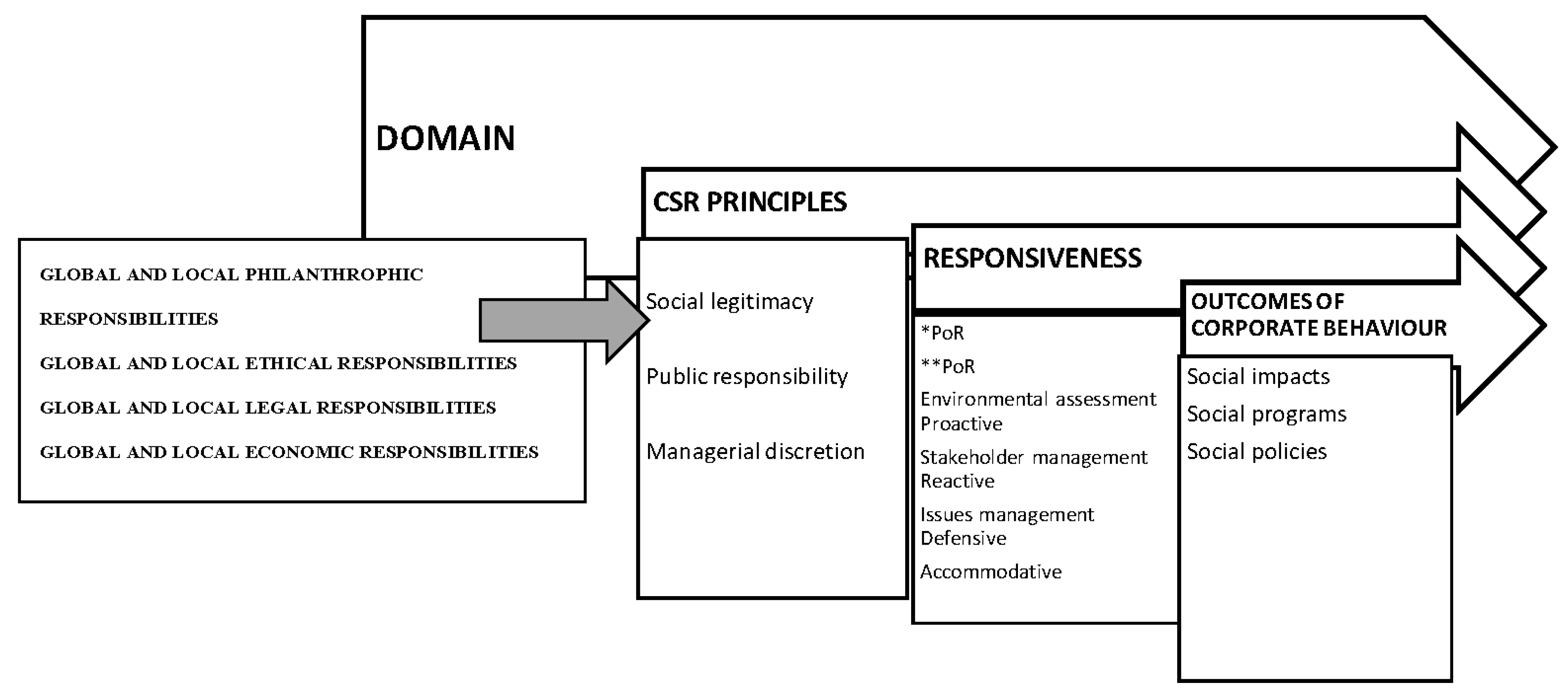

The second useful CSR model was presented by Wood [47], which allows researchers and academics to understand CSR concepts from a broader perspective. Wood [47] argued that society expects certain ‘business behaviour and outcomes’ and that business and society are ‘interwoven rather than distinct entities’ (p. 695). In this regard [48] (p. 43) stated that ‘this CSP model [47] provides a coherent structure for assessing the relevance of research topics to central questions in the business and society field’. This model goes beyond identification of different types of responsibilities and incorporates various theoretical perspectives into a coherent model of CSP. Wood’s [47] model consists of three elements (Table 1).

The first element, principles of CSR, is explained at three different levels: legitimacy, public responsibility, and managerial discretion. These principles of CSR can delineate the motivation behind CSR practices [19,20,21,22,23,24,25,26,27,28,29,30,31,32,33,34,35,36,37,38,39,40,41,42,43,44,45,46,47]. The second element of Wood’s [47] model is the process of corporate social responsiveness. [49] (p. 154) defined corporate social responsiveness as ‘the capacity of a corporation to respond to social pressure’. Wood’s [47] corporate social responsiveness element constitutes environmental assessment, issue management and stakeholder management. Environmental assessment presents the actions and framework that businesses use to identify opportunities and threats from the external environment. Thus, this environmental assessment mechanism allows the business to respond to both positive and negative conditions in its operating environment. Stakeholder management entails responding to and balancing the needs and interests of various groups, internal and external to a business (employees, community members, government, etc.). Issue management includes responding to ad hoc challenges relating to crisis events, lobbying and public relation [47]. Finally, the third element of Wood’s [47] model is the ‘outcome’ of corporate behaviour, designed in conjunction with the principles and processes of corporate social responsiveness. These outcomes are further divided into three parts: (A) assessment of the social impacts (both positive and negative); (B) social programs (a way to manage social impact in favourable ways; (C) social policies (guidelines for decision-making). Wood [47] CSP model articulates and integrates much of the prior work such as social legitimacy [50] and responsibility for organisational outcomes/impacts [51] into a coherent model for assessing an organisation’s social responsibility. However, it has been noted that this model ignores the significance of stakeholder impacts [52]. Over the years, different scholars’ capitalised on Wood’s [47] CSP model for theoretical and empirical studies [19,47,53].

The third and perhaps most influential model in the recent times is presented by Jamali and Mirshak [19]. This perspective integrates two CSP models [45] and Wood [47] and empirically tested the integrated model in the context of a developing country (Lebanon). They claimed that the two models are complementary rather than mutually exclusive. Furthermore, they asserted that Woods’ [47] model is an extension of Carroll’s model.

In terms of principles of responsibility, it was argued in the model that some firms might combine all three principles (legitimacy, public responsibility, and managerial discretion) in one or more domains. It was also argued that proactive firms involve all three principles across all domains. Alternatively, reactive firms might deal with fewer principles and domains. Moreover, it was suggested that the principles might be practiced independently of one another in one or more domains. Similarly, they argued that processes of the corporate social responsiveness aspect should ideally operate across all spheres of responsibility [19,20,21,22,23,24,25,26,27,28,29,30,31,32,33,34,35,36,37,38,39,40,41,42,43,44,45,46,47]. However, it has been argued that “some firms may exhibit better responsiveness in some areas than others, but it is difficult to imagine a firm not according due diligence to responsiveness issues across various domains in this changing and increasingly dynamic environment” [19] (p. 249). Finally, reference [19] maintained that firms need to address their policies, programs, and output across all fields because the social impacts of business behaviour are visible at all four levels of the responsibility domain. Convincingly, it was suggested that the alignment of principle, process and outcome in each sphere is difficult; however, it is important to have effective integration within each domain.

2.1. Proposed Model for This Research: A Global CSR Model

In this research, two changes have been made to the global CSR model. These changes make the model more relevant to the context of MNCs in developing countries. The first change is introduced in the “domain” column of the model (Figure 2), which provides an overall understanding of CSR aspects (economic, legal, ethical, or discretionary).

Several researchers [19,45,54,55,56] suggest that business managers conceptualise responsibilities within these four domains of Carroll’s model. However, Carroll’s [44] CSP model is generic and might not address the difference in global economic, legal, ethical, and discretionary responsibilities as the global environment is more complex for MNCs, especially in the ethical and discretionary fields. For instance, it is more challenging for business managers to integrate different cultural principles or norms of ethics into the strategic management process [45]. Similarly, expectations regarding philanthropic responsibilities often vary according to the level of welfare provision in the host countries. For example Carroll [45] mentioned his unusual experiences in Finland where stakeholders do not rate philanthropic activities very highly due to the high welfare provision enabled by the high tax rate. However, in developing countries MNCs are often involved in philanthropic activities [14,19,27,31,57,58]. Therefore in this study to make a global CSR integrated model more relevant to MNCs, Carroll’s [45] global pyramid of CSR replaces the Carroll [44] model. Carroll [45] argues that the global pyramid facilitates managerial understanding of global stakeholder expectations in a systematic way. He summarised that the pyramid implied that:

- MNCs should make profit according to expectations of the international community (including the international business community).

- MNCs should comply with international and host country laws.

- MNCs should consider both global and host country ethical standards.

- MNCs should meet host country expectations in relation to good corporate citizenship.

The second change incorporated is in the “responsiveness” aspect of the model. [19] Adopted Wood’s [47] responsiveness concept. Wood [47] (p. 703) maintains the concept of “responsiveness” as “process and action”. As discussed earlier, her concept of responsiveness constitutes three parts: environmental assessment, issue management and stakeholder management. From Carroll [44] (p. 501) perspective responsiveness is a ‘strategy behind business (managerial) response to social responsibility and social issues’. In his view the concept of responsiveness is a vital and complementary part of CSR. The corporate responsiveness literature indicates that businesses rationalise responsiveness as four strategies: reactive, defensive, accommodative, and proactive, according to contexts and situations [44]. In this research the “responsiveness” factor is derived from both Wood’s [47] and Carroll’s [44] models, but we also integrate in our revised model the four potential responsiveness strategies (reactive, defensive, accommodative, and proactive) originally identified by Carroll [44] in order to differentiate between different potential orientations to responsiveness of different nuances of responsiveness. This integration enables a more comprehensive and dynamic understanding of the concept of responsiveness.

Capitalizing on the above proposed theoretical framework, this paper aims to explore the CSR initiative of foreign MNCs in Pakistan from a managerial perspective. First this research seeks to explore concept of CSR foreign MNC operating in Pakistan. A greater understanding of the meaning of CSR can provide an opportunity for companies to practice targeted social activities and allocate appropriate and adequate resources for these activities. An understanding of the term “responsibility” is important for business and practitioners in the real world context [59]. The understanding of CSR is mainly dependent on the depth of business social orientation and corporate values [60]. However, the understanding of CSR can differ from company to company, country to country and over time; consequently each company deals with CSR issues in its own way. In the literature different scholars present CSR conceptualisations in distinctive ways. For instance, Friedman [61] argues that the main responsibility of a firm is to earn profit. Other scholars [62,63,64,65] view CSR from a stakeholder lens. As discussed previously CSR is also conceptualised theoretically and empirically from the CSP perspective [19,44,45,46,47]. In this research we explore and collect empirical evidence on the understanding of CSR among MNC managers from Carroll’s [45] perspective and further discuses under the light of theoretical framework.

Secondly, this research aims to explore “principles of motivation” behind companies’ social initiatives. Most of the CSR literature considers financial performance as a key driver of CSR initiative [66,67]. A number of studies suggest firm size [68,69] and firm profitability as CSR drivers [70,71]. In the CSR literature, institutional conditions of the context are also considered as a driving force behind CSR initiative [31,66]. For instance, legal and regulatory issues can pressure companies to pursue CSR practices. In industries like tobacco, food and packaging where the threat of additional regulations is high, the companies are more sensitive towards CSR practices [72]. Similarly, pressure groups (i.e., NGOs and labour unions) may press for new regulations but they primarily use non-legal sanctions including boycotts and negative publicity [59]. Wood [47] presented a set of ‘principles’ to explain the motivation behind CSR practices. Jamali and Mirshak [19] used Wood’s [47] principles to empirically examine the motivations driving CSR in a developing country context. In this research we capitalised on Wood’s [47] principles (i.e., legitimacy, managerial discretion, and public responsibility) to explore motivations behind CSR initiatives in the context of Pakistan.

A third dimension of our broader research aim is to investigate MNCs’ action and implementation of CSR in a developing country. At this stage emphasis shifts from moral attributes to operational aspects. Carroll [44] suggested that corporations rationalise the action phase of responsibility (responsiveness) as a set of four strategies: proactive, reactive, defensive, and accommodative, according to the situation and context they face. However, corporations in practice do not follow a single strategy, but shift and adjust as necessary to control public perception [73]. Wood [47] conceptualised this action phase of CSR in the CSP model as a “process of responsiveness”. The whole process of responsiveness is based on knowledge of the external environment and this knowledge can be used to formulate an appropriate strategy in response to environmental pressure [19]. In this research we used Carroll’s [44] and Wood’s [47] responsiveness perspective to collect empirical evidence in the context of Pakistan.

In the fourth and last stage, this research aims to identify the outcomes of CSR practices. As discussed previously in detail, Wood [47] divided the potential outcomes of CSR into three parts: social impacts, social programs and social policies, and a Global CSR model systematically examined these outcomes in a developing country context. This research collects empirical evidence on outcomes of CSR by utilising Wood’s [47] classification.

This proposed global CSR model argues that ideally MNCs should integrate CSR principles, processes, and outcomes with all CSR domains (economic, legal, ethical, and discretionary). Ideally, an extensive and coherent approach to CSR across all domains of an organization’s operations would entail an equal attention to the aspects of CSP, that is, principles, processes and outcomes. Although in practice, organizations may display inadequate compliance towards CSP and its aspects across several domains. Some might opt for an alternative by prioritizing their responsibilities and fully concentrating on one or two types of social responsibility, at the cost of others. However, such alternatives might risk the image of the firm, especially if the firm is focused on the traditional economic domain of CSR. To the extent principles are concerned, some firms might be motivated by combination of all three principles in one or more domains. Most proactive firms are motivated by all three principles across all domains while reactive firms care for fewer principles and domains [47]. Independent operation of these principles has also been noticed in one or more domains, such as some managers to their discretion, might prefer philanthropic CSR without regarding institutional legitimacy and public responsibility [47]. Such managerial discretion can be reasoned with, as philanthropic CSR provides managers with a wider room for personal preference in the selection of CSR programs.

Similarly, responsiveness strategies should be formulated across all domains of social responsibility such as it complements its principled reflection [47]. This suggests that managers monitor each responsibility domain exclusively and devise exclusive strategic plans to deal with emerging concerns specific to each. This may call for better responsiveness processes in few domains as compared to others in some firms. In this increasingly dynamic environment it’s hard to imagine a firm that’s not taking reasonable steps towards responsiveness issues across its domains. Furthermore, Firms also need to track their programs, policies and outcomes in a similar fashion. All four domains of responsibility exhibit the firm’s social impacts in their own way. It is also essential to keep track of the essence of the programs selected for investment across all the domains plus the integration of social issues inside the group of organization strategy. Their alignment in each respective domain (economic, legal, ethical and discretionary) may be a challenge, but its effective integration across the responsibility domains is the most exigent of all which needs continuous refinement over time.

Hence, this research article posit various combinations of CSR orientations with mixing of the multiple and complex dimensions outlined in this proposed model. Guided by this proposed framework, the empirical data proceeds to understand conception, motivation, process, and outcomes of CSR by sample MNCs operating in Pakistan.

2.2. Contextual Background-Pakistan

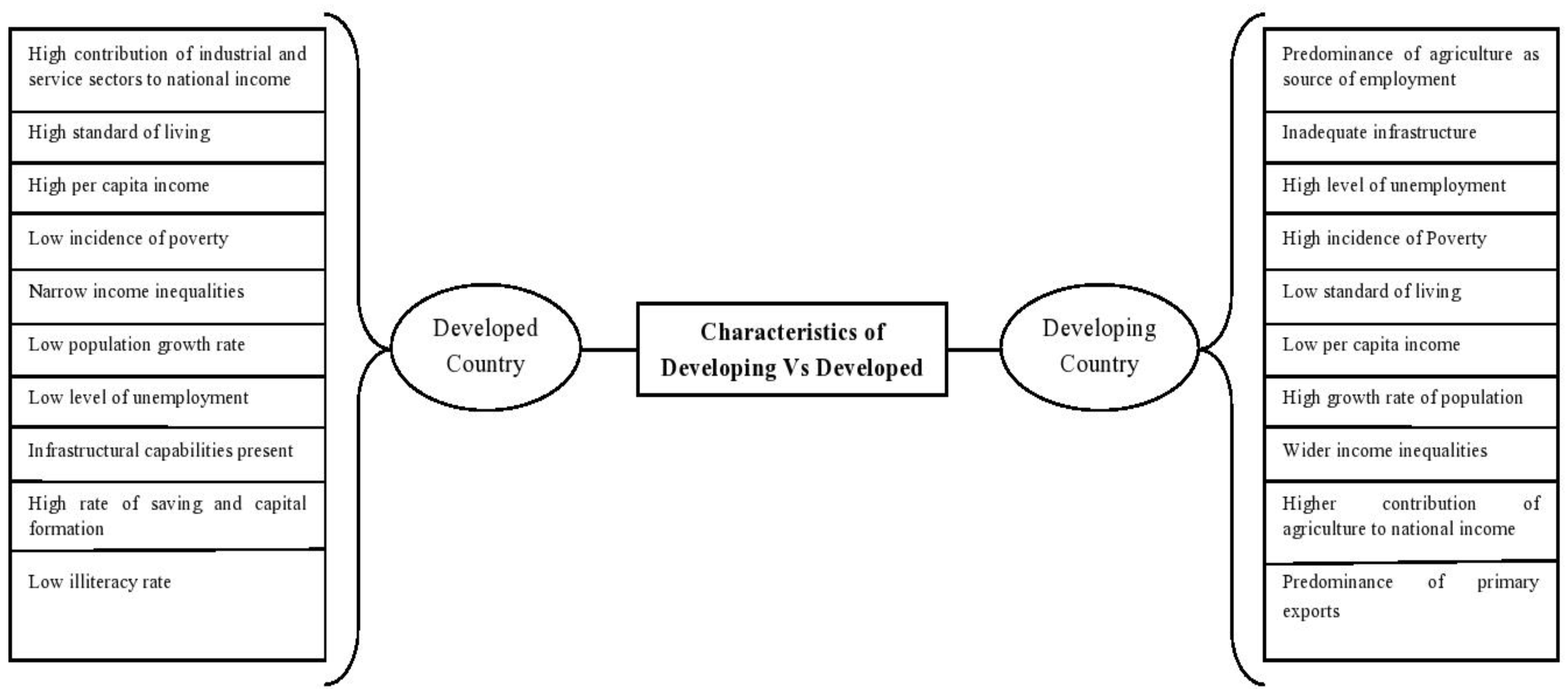

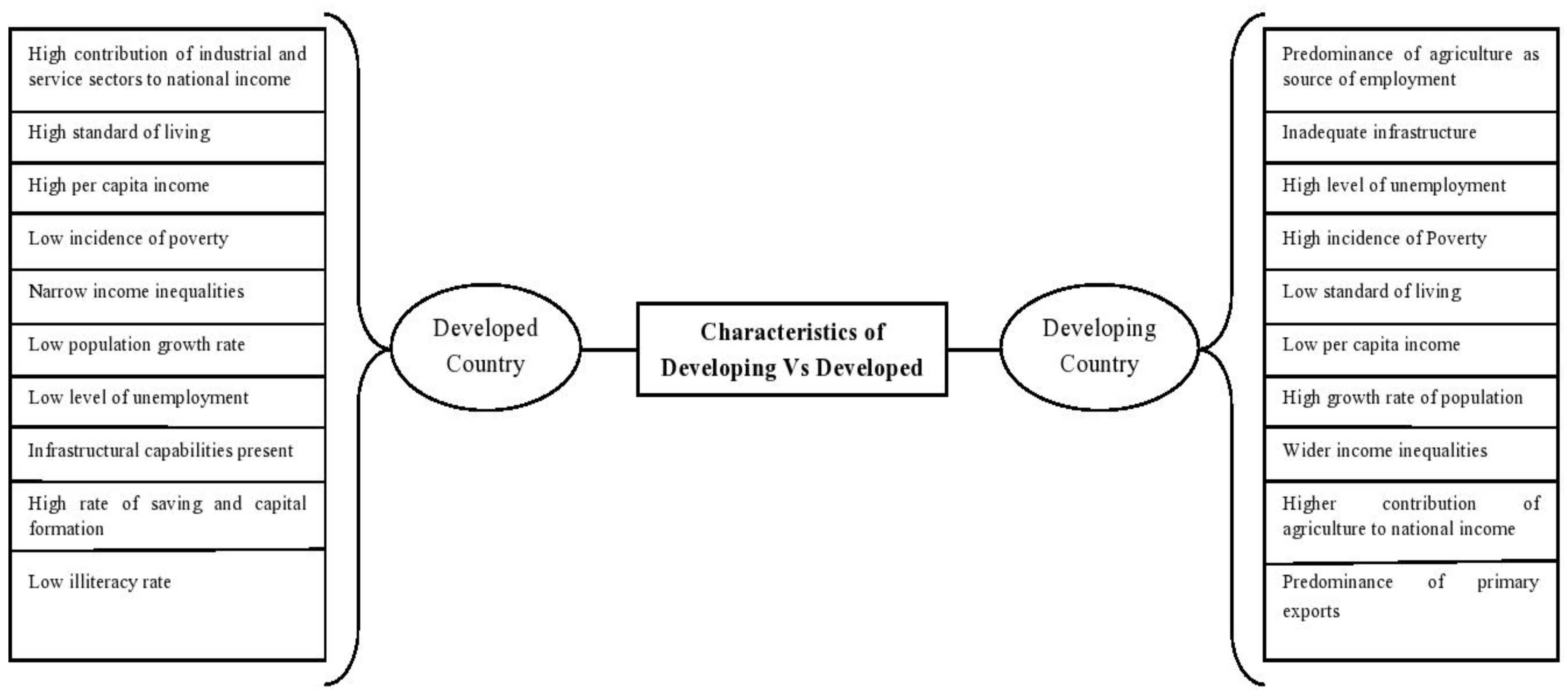

Pakistan is an underdeveloped country with a largely agro-based economy. The agriculture sector contributes 25.1% of country’s GDP, provides employment to 45% of labour force and supplies raw materials to industry, hence contributing to Pakistan’s exports. However, during the last decade measures have been taken to attract FDI in the service and manufacturing sectors. For instance, investors can hold 100% of foreign equity, and only pay 5% custom duty on imports of plants, machinery and equipment [74,75]. Figure 3 shows that these are developing country characteristics.

Like all developing countries Pakistan faces several economic, social, and political problems. Since the creation of Pakistan, the military has played an important role in political governance. Serious conflict with its neighbouring country over Kashmir, international politics (including the support of the West) and the strategic location of the country has further strengthened the power of the military and its dominant role in the country’s politics. Consequently, in the last 60 years sustainable political and institutional setup has not been established in Pakistan.

Society in Pakistan is composed of different ethnic groups, culture and languages. This diversity has weakened the idea of strong civic moment for political reforms. Religious bonds can provide some unity in the midst of diversity. However, in the last two decades, elite religious groups with vested interest have also brought elements of sectarianism and extremism. After the 11 September 2001 attack on the US, Pakistan dropped its support for the Taliban regime in Afghanistan and became a front-line state in the fight against terrorism.

Consequently, there have been increased insurgencies and terrorist attacks in Pakistan. These attacks have resulted in further social and economic problems. For instance, when the Pakistani army started operations in the Swat valley of Khyber Pakhtoonkhwa, three million people were displaced, this put a huge burden on the infrastructure of urban cities of Pakistan. In addition, terrorists often target infrastructure and facilities such as schools and bridges etc. The business environment has been negatively affected by this dire security situation. Local and foreign investors are reluctant to invest in Pakistan due to the uncertain and risky situation. Over the last year, local investors withdrew eight billion dollars and foreign investors withdrew four billion dollars from the economy. This existing insurgency and insecurity make MNCs’ strategies and operations (including CSR initiatives) more difficult and complex. This study represents an element of novelty, given the unique institutional and cultural characteristics of Pakistan. See Figure 3 below.

3. Research Methodology

Firstly, we used the literature to help identify and refine the research problem in this context. The literature showed many useful and informed accounts of dimensions of the concept. The study of literature and the nature of the characteristics of our study, this led us to adopt an interpretivist approach to the study. Interpretivism advocates that it is necessary for the researcher to understand differences between humans in our role as social actors. To respond to the call for greater use of exploratory qualitative research and address our research questions, a qualitative interpretative stance needed to be taken to understand the CSR phenomenon of subsidiaries of foreign MNCs in the context of a developing country [76]. In an interpretive research approach reality and knowledge are socially constructed by interaction of individuals (researcher and participants) in the specific context [77,78]. The researcher believes that the reality is subjective and it needs to be explored in its real life context. In order to find the meaning of an action or to understand it, it requires that the researcher interprets it in a particular way what the actors are doing. Following this reasoning we believe an in-depth exploration of the phenomenon is needed to understand the phenomenon. Therefore, empirical evidence was collected through in-depth semi-structured interviews. The sample of selected companies for interview was based on a purposeful snowball sampling technique. The sample of respondents on the basis of purposeful sampling was selected on the basis of four criteria: (1) the company is a subsidiary of a foreign MNC operating in Pakistan; (2) the sample MNC subsidiary is involved in CSR activities (this information was obtained from the companies’ sustainability reports on their websites); (3) accessibility to the respondents; and (4) the respondents (managers) in the sample must be responsible for CSR in their companies.

In the frame of the above criteria, between September 2011 and August 2015, a total of 18 interviews were conducted with respondents. As the research evolved theoretically over time, 10 companies were interviewed at multiple points in time and a sample size of 10 was decided on the basis of saturation, depth, and utility of data. MNCs were identified from the Karachi Stock Exchange website (KSE) database. Initially, contact details and names for each MNC were traced from their websites. An email with the aims and objectives of the research was sent to twenty MNCs requesting an interview appointment. As this did not yield sufficient responses, personal references and a snowballing strategy were used to obtain further interview appointments. Before each interview, the interviewees were called to explain the interview objectives, issues of confidentiality, and specify a time and meeting place. All interviews were held on the companies’ premises. Interview timings varied from 50 to 140 min. Except for one, all interviews were conducted in English. Interviewees were also given the liberty to stop the interview at any stage they liked. However, this option was not exercised at any stage by any of the companies visited, though the level of cooperation was different in different companies. All respondents consented to tape-recording the interviews. Alphabetical symbols (A B C…) are assigned to sample companies to keep the identity of the managers anonymous. See following (Table 2) for details.

A set of semi-structured interview themes based on the proposed framework were prepared prior to the interviews. The semi-structured interview guide helped to focus discussion around the theoretical framework themes. In addition, the order of the questions asked sometimes varied, and different contingency questions were asked on the basis of the respondents’ answers.

Interview data was recorded digitally and transcribed manually. The transcription was double checked and also sent to respondents for more reliability. In line with [79], raw qualitative data from transcription was reduced by thematic analysis. For this, commonalities or patterns of agreement and disagreements were detected in the respondent statements. Furthermore, abstraction and reductions of themes were carried out with reference to proposed frameworks. It is important to note that the empirical data does not provide an overall and complete picture of MNCs CSR profile. Rather, the analysis provides a qualitative interpretation of themes from empirical data, which could help us to identify general convergence and divergence in relation to framework and existing relevant literature.

For analysis presentation purposes, an exploratory case study approach has been adopted. Often, an exploratory case study strategy is compiled of many small sub-cases [78], where these smaller sub-cases provide a deeper understanding of the main case [80]. These smaller cases or sub-cases within the case can each be considered as a ‘unit of analysis’ [79] (p. 25). Hence, individually each MNC represents a unit of analysis and collectively all eight MNCs represent the main case. The aggregate findings of study are based on qualitative thematic analysis and fleshed out below in a systematic manner. Therefore, the following findings present a holistic but critical outline of the sample in relation to the previously proposed CSR model, rather than analysing each company individually. As a qualitative case, this research claims internal validity. However, this research does not claim external validity (or generalization) of empirical data to different contexts [79].

4. Research Findings

Following to the relevant literature and referring to Figure 2, this section first attempts to gauge the CSR conception of sample MNCs in Pakistan (economic, legal, ethical, and discretionary domain). CSR motivation of MNCs in reference to organizational legitimacy, managerial discretion, and public responsibility were delineated. The next step involved presentation of MNCs responsiveness strategies followed by outcome of CSR practices in the context of Pakistan.

4.1. CSR Conceptualisation

To explore CSR conceptualisation in the context of Pakistan, qualitative themes from the interviews are presented through Carroll’s [45] CSP model. The empirical evidence suggests that all respondents of sample MNCs interviewed participated in voluntary or philanthropic initiatives (Table 3), for instance cash donations to sponsor poor students (Companies H, B, J), sponsoring the construction of a sports complex (Company D), blood donation (Companies C, D, E, H), and cash donations to charities and NGOs (Companies A, D, G, I). In addition, most of the MNC managers also explicitly mentioned ethical obligations. The manager of Company B illustrated this very succinctly and stated that “As a corporate business we are very aware that there are certain ethical responsibilities.” Similarly, the executive of Company E stated, “First of all we [the company] do not do it [CSR activities] in order to be acclaimed …we do it because we feel that we have an ethical responsibility and obligation towards society.”

None of the respondents in the sample presented any views regarding the legal domain of responsibility. Only one executive (Company H) touched on the primacy of the economic domain and cast doubt on the concept of CSR altogether. He mentioned, “To be honest, there is no such thing as CSR.” and “The [senior] management may think differently, but their motive is business, their motive is earning revenue and net profit.”

There was evidence that managers from MNCs not only defined CSR from a moral and ethical perspective, but also tailored CSR activities according to local ethical expectations. In this regard, the manager of Company E expressed: “Since our company’s president is from Pakistan, he understands the local issues better than a foreigner. This local understanding is translated into our CSR initiatives.” All the managers of MNCs explicitly mentioned that they follow global standards regarding issues like child labour, health and safety, equal opportunities, etc. In addition, the MNCs also showed flexibility in adapting to local expectations of stakeholders (particularly employees). For instance, some companies altered their global health and insurance policies according to local needs and included parents of employees in health benefits in Pakistan (Companies I, C, D, A).

4.2. Motivation for CSR Practices

Empirical evidence regarding motivation is framed (Table 4) according to Wood’s [47] principles of CSR.

Organisational legitimacy is the key principle to which all of the interviewees referred explicitly or implicitly in their conversation. Most of the executives interviewed believed that business has societal obligations and is accountable towards society for their actions. Managers of five companies (Companies B, E, D, F, J) used the same phrase, i.e., “giving back to the society.” This illustrates businesses’ obligation towards society. On the other hand phrases like “business cannot survive if it does not cater to society’s expectations” (Company A, I) and “acceptance in the community” (Company C) provide evidence of the reactive aspect of organizational legitimacy. In addition, some managers took this point further and extended their view of CSR to accountability towards expectations of society. According to the manager of Company G: “Business plays an important role in the growth of the community, environment and country.” and also it is “accountable and responsible towards society” for its actions. Similarly, CSR drivers are mentioned as “genuine interest to serve society” (Company E) and to “meet needs and expectations of society” (Company D).

Managerial discretions the second principle to which executives referred most frequently. Three respondents from different companies identified “interest,” “emphasis” and “encouragement” from senior management as the key factors motivating CSR activities. As articulated by the manager of Company E: “The CEO himself is very serious about CSR. In our meetings he always puts emphasis on CSR and encourages us to get involved.” The manager of Company F mentioned another example of senior management support for CSR activities. He stated: “I felt the requirement [for CSR strategy] and my senior management also supported me and helped me in developing CSR strategy for 2009.” Furthermore in terms of operational independence the manager of Company A stated: “We have broad guidelines from the parent company and senior management but I am absolutely independent to manage and implement my CSR strategy.”

The above-mentioned examples of “managerial discretion” show discretionary support from senior management for CSR initiatives. However, the views of two managers (Company H and B) show a potentially negative impact of the discretionary power of senior managers on CSR activities. The manager of Company H states: “Though they [employees] spend some time in knowledge sharing… [Community work], it depends on the management…. if they [senior management] feel that an employee’s job is not affected by community services then he/she can go ahead and do it.” Similarly, the manager of Company B mentioned financial dependence on senior management for carrying out CSR activities. Although this reliance might be considered operational practice, nevertheless, this does not show any encouragement or interest from the senior manager as the quote states: “We go out to corporate [senior management] and ask for finances and they will evaluate the initiatives.” Empirical evidence suggests that all MNCs in our sample, with the exception of H, supplement the broad guidelines on CSR strategy from the parent company with insights and details derived from managerial discretion locally. From a public responsibility perspective, only the manager of Company D and I considered CSR as a core value of their business along with historical involvement in CSR activities, while two other companies (Companies E, F) indirectly mentioned examples of CSR activities linked to their primary or secondary operations. The manager of Company D articulated CSR as its “traditional activity,” in line with its business operations and stakeholder considerations. According to the manager of Company D: “For decades we have had a specific CSR department and they are already involved in CSR in one way or another by educating farmers and providing certain services.” He strongly believed that CSR activities should be related to business operations and emphasized that “We have CSR projects directly related to our operations. This helps carry out CSR more effectively.” At another point he stated “It [CSR] starts from the moment you begin your productions processes, it includes the supply chain as well.” However, the manager of Company H clearly mentioned that CSR is not a core business function. He states that “Yes—we have a group of volunteers (employees) who are responsible for such [CSR] initiatives, coming up with such initiatives and maintaining such initiatives. However, it’s a second-hand role for all of the people of this group and it’s not a primary responsibility.”

4.3. Corporate Social Responsiveness Strategies

The following interview themes are framed through Wood’s [47] and Carroll’s [44] corporate social responsiveness perspectives. See Table 5.

With only one exception (Company D), no respondent acknowledged the importance of the environmental scanning process. Even the company that noted the importance of this process mentioned that the environmental scanning process is done “not directly but indirectly. We operate in this market and we live in this environment so we are aware of the problems that need to be fixed.” (Company D). It is clear from the previous section (public responsibility) that CSR is not a core value for most of the companies; as a result MNCs’ operations in Pakistan do not recognise or execute a systematic environmental scanning process.

The empirical investigation provides interesting insights regarding stakeholder management issues as the data shows some extremely polarized views. When asked about stakeholder management issues, one respondent implied that this concept is not practical: “Stakeholders have anything to do with the CSR?” and “It is very bookish” to talk about this issue (Company E). On the other hand, the manager of Company C defined CSR as “managing stakeholders” and later she asserted “we have defined our stakeholders and the ways [strategies] to deal with them.” However, most of the companies do not involve stakeholders during the strategic formulation process. However, there was evidence that one of the companies interviewed (Company D) does include stakeholders at this stage. According to the Company D manager, “The whole process involves having stakeholders sit with you on a table, putting forward their expectations. Naturally when we do that whatever CSR strategy may follow reflects the needs of stakeholders.”

Despite the fact that companies do not include stakeholders at the planning stage of their CSR strategy, most of the companies interviewed had partnerships with stakeholders during the execution phase of CSR activities. Companies are in partnership with government (Companies E, D, C, B, J and F), communities (Companies E, C, D, F, I, J) and NGOs (Companies E, D, J). In the stakeholder management process, a few companies complained of “red-tape-ism and corruption” (Companies E, C) when dealing with government, while others (Companies D, F) expressed that “It is worth working with government.” Views regarding partnerships with NGOs also differed, as one manager said “The most important thing a corporation can do is work with the expertise which is there in some really large NGOs. Some organizations are specialized and did actually a very good job like for example Edhi, the adult basic education society. NGOs have been on the ground and have been working in Pakistan for a very long time so they have a lot of expertise.” (Company D). On the other hand, we found evidence that some companies prefer to exercise their CSR internally. For instance, the manager of Company C argued that involvement of external partner (such as NGOs) is a waste of money because NGOs consume a large portion of donated money as administrative expenses and the community does not get the full benefits of it.

In addition, four companies (A, B, D, G) have a specific person and department to deal with CSR issues. In some companies (F and E) CSR issues are handled by the marketing department and are seen as a marketing or publicity tool. However, for the other companies, CSR is not part of company philosophy (as previously suggested by the principle of public responsibility) so they manage CSR on an ad hoc basis. These activities are also event-based and volunteers from different departments are engaged when these activities are performed.

None of the companies explicitly mentioned proactive CSR responsive strategies, and our study indicates a synthesis of accommodative, reactive and defensive responsiveness strategies. It is evident from the data that all MNCs included in the sample used accommodative strategies, especially in the case of disaster or national crises. The most common example was that all executives mentioned their contribution after the 2005 earthquake in Pakistan. The manager of Company C provided an example of a reactive strategy due to pressure from the community to maintain legitimacy. She stated: “I remember in 2003 and 2004, the company was not welcomed in that local area because communities felt we [the company] were disturbing their privacy.” Similarly, an executive from Company D mentioned an example of a defensive responsiveness strategy, acknowledging that the “nature of the product is controversial [producing tobacco]”and describing constant engagement with stakeholders and CSR activities to reduce the negative image [if any] of the company.

4.4. Outcomes of CSR Practices

This section provides empirical insights in relation to the outcomes of CSR practices in a developing country. We found that most companies do not have a consistent CSR policy which is integrated with company philosophy and is part of a broader strategy to address external stakeholders. Instead, the majority of the companies are involved in discrete philanthropic activities. Only two companies (C and D) have specific polices and budgetary arrangements. Both of these companies have guidelines and policies to address their relationship with the community, and a specific department to execute CSR activities. However, with no exception, all the companies interviewed have clear CSR policies pertaining to internal stakeholders (for example regarding child labour, occupational health and equal employment opportunities).

In most cases companies devise CSR programmes based on the local needs of the community, which include education (E, B, D, C, J), public health (Companies D, E, I) and the environment (Companies C, D, E). However, these programs are not a result of a formal environmental scanning or stakeholder management, rather they are a reflection of a general understanding of the local environment. In addition, MNCs design social programs related to their operations. For instance, Company E introduced a scheme through which they established free public call offices in a remote area of Pakistan, and volunteers from Companies A and B were involved in a series of information technology training courses in local schools and universities.

In terms of social impact, companies like G and E get involved in social activities because they see themselves as responsible for doing it. Other companies see the impact as a tool of “soft image” (Company F), “reputation” (Company D), and “public relations” (Company A). However, none of the executives made explicit statements about any monetary impact of CSR.

5. Discussion on Empirical Findings

With reference to Carroll’s four domains of responsibility, the CSR literature suggests that companies in developing countries often focus on philanthropic aspects of CSR [16,19,27]. In the context of Pakistan, our results suggest that alongside the philanthropic conception of CSR, MNCs also conceptualise CSR in ethical terms. We also found that only one company executive in our sample perceived responsibility in the economic domain as important and none of the sample companies referred to the legal domain. This suggests that MNCs in developing countries actually internalize the lax legal environment, ignoring issues such as exploitation of law, corruption, tax evasion, and creation of employment opportunities in the developing host country. This is in contrast to Jamali and Mirshak [19] contention that it is essential for the business to consider a wide range of issues including economic and legal factors in developing countries. In addition, it has been argued that CSR conceptualisation should focus on global and local expectations of stakeholders [45,46,47,48,49,50,51,52,53,54,55,56,57,58,59,60,61,62,63,64,65,66,67,68,69,70,71,72,73,74,75,76,77,78,79,80,81,82]; however often in developing countries CSR is considered a western concept that is exported from developed countries [32,33,34,35,36,37,38,39,40,41,42,43,44,45,46,47,48,49,50,51,52,53,54,55,56,57,58,59,60,61,62,63,64,65,66,67,68,69,70,71,72,73,74,75,76,77,78,79,80,81,82,83]. In the context of Pakistan our data suggests that MNCs translate global CSR standards and customize to some extent to local needs, however, this local tailoring focuses more on the internal stakeholders of MNCs than on external stakeholders.

The key motivational or driving principles for CSR that emerged from this study are organisation legitimacy and managerial discretion. Empirical evidence regarding principles of motivation is similar to [19] findings. Except for one, all MNCs included in this research acknowledged their social contract with society and frequently mentioned their genuine interest in “giving back to society.” Most of the executives interviewed explicitly expressed their discretion to initiate and execute CSR activities. This discretion also provides the opportunity for MNC managers operating in Pakistan to adapt CSR strategies to local conditions. None of the MNCs explicitly mentioned CSR as a core business philosophy, indeed three companies mentioned clearly that they do not believe CSR is a core business philosophy. However, a few companies are involved in CSR activities which are related to their day-to-day business activities.

In the context of Pakistan, the empirical evidence from our sample companies suggests that none of the MNCs are involved in a formal and systematic environmental assessment process. The CSR activities of most of the MNCs operating in Pakistan address general social issues such as education, health and tree planting. As previously discussed, CSR is not considered a core business function. Rather than making a planned environmental assessment, MNCs in Pakistan tend to perform CSR activities on an ad hoc basis when volunteers get the chance and time to do them. The choice of themes for CSR activities and programs is, therefore, not based on a systematic assessment of needs and salient issues in the local context, but rather determined through a process of selective attention and instrumental contextual adjustment.

Our study indicates that MNCs in Pakistan tend not to involve external stakeholders in the planning stage of CSR strategizing. However, a few companies do engage stakeholders (communities and NGOs) during the execution of CSR activities. The majority of the MNCs showed serious concern regarding past experience with the government and NGOs relating to issues of corruption and red-tape-ism. Issue management requires monitoring of business responses to social issues and is a product of environmental scanning [84]. Earlier, it was discussed that there is no evidence of an environmental scanning process in Pakistan; consequently, there is no explicit or implicit evidence of systematic issue management. For most of the MNCs, issue management comes under the marketing and public relations lens or in other words falls in the jurisdiction of the marketing function.

As discussed above MNCs do not have a systematic stakeholder management process, this indicates that companies are not proactive. Although the evidence of managerial discretion might imply a proactive strategic approach, the presence of the legitimacy principle and management focus on philanthropic activities leads us to conclude that MNCs in Pakistan do not use proactive strategies. The findings of a predominant focus on philanthropic activities, with little conception of public responsibility suggest that the MNCs sampled adopted mostly accommodative and reactive responsiveness strategies. This is an important finding, suggesting discrepancy in the CSR practice of MNCs across their home and host environments. We know first-hand that MNCs have very sophisticated and proactive CSR practices in their home countries, which touch on all the domains of responsibility and involve systematic stakeholder management practices. This discrepancy has also been noted in recent research in the developing world [14] and may even be suggestive of symbolic window-dressing of MNC CSR initiatives in the developing world [13].

The investigation of outcomes suggests that MNCs have a range of social programs which are designed to address general social issues such as public health and education, rather than as an outcome of a specific environmental assessment exercise. More importantly, in the case of a natural disaster, all the MNCs devised discretionary programs to help the affected element of society as part of expected ethical behaviour in the local context. Therefore, despite good intentions, the social impacts of MNC activities in Pakistan are limited, particularly given that their social programs are ad-hoc, and not grounded in a systematic assessment of needs or management of relevant issues, particularly from the perspective of the community. Exceptions are when MNCs come under direct pressure from the community to address natural unexpected crises or disasters.

There is also evidence of clear and coherent social policies dealing with internal stakeholders. Without exception, all companies have clear guidelines regarding issues like child labour, equal employment opportunities, health and safety, and working conditions. None of the executives interviewed mentioned clear social polices relating to external stakeholders and society at large. However, in two companies, evidence was found of social policies concerned with environmental issues as part of the permanent business strategy and historical practice of the company. In addition, none of the MNC executives measured the social impact of their CSR activities. It appears that the executives believe that CSR (philanthropic activities) is simply expected ethical behaviour and they are not interested in outcomes. However, a few MNC managers did expect payoffs from CSR in terms of long-term public relations and branding, although they seemed less interested or concerned about impacts on society.

Overall the evidence gathered is consistent with previous research relating to CSR in developing countries. While internal CSR issues are accorded more systematic attention by MNCs (e.g., employment, health and safety), external CSR initiatives are accorded less planning and priority. Most of the CSR initiatives discussed are reactive and ad hoc, suggestive of symbolic attempts to earn legitimacy in host environments. This adds to the substantive bulk of evidence now accumulating about CSR practice in the developing world, which questions the effectiveness of CSR despite its noble goals and aspirations pertaining to improving the quality of life of marginalized communities. Recent research has indeed cast doubt about the potential and promise of CSR in the developing world, and whether beyond positive rhetoric, CSR is indeed meeting substantive development goals in the poorer nations and countries [14]. Our findings in this paper lend support to this critical literature and dissenting voices that have recently pointed to and documented the exaggerated promise and limited effectiveness of CSR in the developing world [85,86].

6. Conclusions

In general, literature on CSR is scant in the context of developing countries. The importance of the role of MNCs in the context of developing countries is recognised but literature on CSR and MNCs is still limited. To understand the role of MNCs in a developing country we adapted a theoretical framework based on previous work [19,45,46,47]. This paper presented empirical evidence in the light of the proposed theoretical framework which suggests that MNCs operating in Pakistan understand responsibility in mostly philanthropic and ethical terms with little or no focus on the economic and legal dimensions of CSR. This reflects that MNCs’ focus on discretionary and ethical responsibility to gain legitimacy in the local context of Pakistan. Lack of public responsibility may account for the absence of systematic environmental scanning and stakeholder management. Consequently, MNCs deal with CSR issues on an ad hoc basis, employing discrete CSR polices, and without a plan for external stakeholder management.

This research has important implications for the CSR practice of MNCs in Pakistan. The findings are consistent with accumulating evidence in the literature suggesting symbolic patterns of CSR engagement for MNCs across the developing world [13,14]. However, it is time for the CSR agenda to move beyond the stage of rhetoric to actual substantive interventions that help address needs and improve the quality of life in country like Pakistan and the developing world. On the basis of our findings we conclude that MNCs are manipulating CSR in Pakistan to gain much needed legitimacy; however, their commitment in practice beyond symbolic window dressing can be questioned, particularly if we consider systematically as we have done in this paper their motivations for CSR, and their actual policies, processes, and outcomes of CSR intervention.

The empirical evidence from this research qualifies within the parameters of the existing context. However, the proposed framework in this paper can be used empirically (both in a developed and a developing country context) to examine and understand CSR practices of MNCs. Our research suggests a number of issues that deserve further investigation in the context of a developing country. For future research it is recommended to include a larger sample size and sample companies in diverse industries. In addition, we suggest that empirical evidence collected from different stakeholder perspectives can give more useful insights with the help of this framework. Finally, there is a pressing need for continued research relating to CSR in the developing world to shed more light on the practices and orientation of MNCs and draw out related important insights and implications from a development perspective.

Author Contributions

All the authors have contributed to this manuscript. M.S.Y. conceived and designed the main write-up, provided the theoretical contribution, development of theoretical framework, and analysis. D.J. provided conceptual comments and contributed to the papers review while H.H. collected the data, transcribed the data, conceived the basic thematic coding, and contributed to the formatting of the paper.

Funding

This research received no external funding.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Pieterse, J.N. Globalization and Culture: Global Mélange; Rowman & Littlefield: Lanham, MD, USA, 2015. [Google Scholar]

- Geppert, M.; Dörrenbächer, C. Politics and power in the multinational corporation: An introduction. In Politics and Power in the Multinational Corporation: The Role of Institutions, Interests and Identities; Cambridge University Press: Cambridge, UK, 2011. [Google Scholar]

- Karam, C.M.; Jamali, D. A cross-cultural and feminist perspective on CSR in developing countries: Uncovering latent power dynamics. J. Bus. Ethics 2017, 142, 461–477. [Google Scholar] [CrossRef]

- Jackson, G.; Rathert, N. Multinational Corporations and CSR: Institutional Perspectives on Private Governance. 2015. Available online: http://ilera2015.com/dynamic/full/IL204.pdf (accessed on 20 June 2017).

- Scherer, A.G.; Palazzo, G.; Baumann, D. Global rules and private actors: Toward a new role of the transnational corporation in global governance. Bus. Ethics Q. 2006, 16, 505–532. [Google Scholar] [CrossRef]

- Edwards, T.; Sanchez-Mangas, R.; Bélanger, J.; McDonnell, A. Why are some subsidiaries of multinationals the source of novel practices while others are not? National, corporate and functional influences. Br. J. Manag. 2015, 26, 146–162. [Google Scholar] [CrossRef] [Green Version]

- Kostova, T.; Marano, V.; Tallman, S. Headquarters–subsidiary relationships in MNCs: Fifty years of evolving research. J. World Bus. 2016, 51, 176–184. [Google Scholar] [CrossRef]

- Brammer, S.; Brooks, C.; Pavelin, S. Corporate social performance and stock returns: UK evidence from disaggregate measures. Financ. Manag. 2006, 35, 97–116. [Google Scholar] [CrossRef]

- Doh, J.P.; Guay, T.R. Corporate social responsibility, public policy, and NGO activism in Europe and the United States: An Institutional-Stakeholder perspective. J. Manag. Stud. 2006, 43, 47–73. [Google Scholar] [CrossRef]

- Maignan, I.; Ralston, D.A. Corporate social responsibility in Europe and the US: Insights from businesses’ self-presentations. J. Int. Bus. Stud. 2002, 33, 497–514. [Google Scholar] [CrossRef]

- Hah, K.; Freeman, S. Multinational enterprise subsidiaries and their CSR: A conceptual framework of the management of CSR in smaller emerging economies. J. Bus. Ethics 2014, 122, 125–136. [Google Scholar] [CrossRef]

- Khan, Z.; Lew, Y.K.; Park, B.I. Institutional legitimacy and norms-based CSR marketing practices: Insights from MNCs operating in a developing economy. Int. Mark. Rev. 2015, 32, 463–491. [Google Scholar] [CrossRef]

- Jamali, D. MNCs and International Accountability Standards Through an Institutional Lens: Evidence of Symbolic Conformity or Decoupling. J. Bus. Ethics 2010, 95, 617–640. [Google Scholar] [CrossRef]

- Jamali, D. The CSR of MNC Subsidiaries in Developing Countries: Global, Local, Substantive or Diluted? J. Bus. Ethics 2010, 93, 181–200. [Google Scholar] [CrossRef]

- Yin, J.; Jamali, D. Strategic corporate social responsibility of multinational companies subsidiaries in emerging markets: Evidence from China. Long Range Plan. 2016, 49, 541–558. [Google Scholar] [CrossRef]

- Chapple, W.; Moon, J. Corporate social responsibility (CSR) in Asia. Bus. Soc. 2005, 44, 415–441. [Google Scholar] [CrossRef]

- Rodriguez, P.; Siegel, D.S.; Hillman, A.; Eden, L. Three lenses on the multinational enterprise: Politics, corruption, and corporate social responsibility. Palgrave Macmillan J. 2006, 37, 733–746. [Google Scholar]

- Garriga, E.; Melé, D. Corporate social responsibility theories: Mapping the territory. J. Bus. Ethics 2004, 53, 51–71. [Google Scholar] [CrossRef]

- Jamali, D.; Mirshak, R. Corporate social responsibility (CSR): Theory and practice in a developing country context. J. Bus. Ethics 2007, 72, 243–262. [Google Scholar] [CrossRef]

- Lu, J.; Liu, X.; Wright, M.; Filatotchev, I. International experience and FDI location choices of Chinese firms: The moderating effects of home country government support and host country institutions. J. Int. Bus. Stud. 2014, 45, 428–449. [Google Scholar] [CrossRef] [Green Version]

- Meyer, K.E. Perspectives on multinational enterprises in emerging economies. J. Int. Bus. Stud. 2004, 35, 259–276. [Google Scholar] [CrossRef]

- O’callaghan, T. Disciplining multinational enterprises: The regulatory power of reputation risk. Glob. Soc. 2007, 21, 95–117. [Google Scholar] [CrossRef]

- Yunis, M.S. CSR research “Back Home”: A critical review of literature and future research options in Pakistan. Bus. Econ. Rev. 2009, 1, 1–7. [Google Scholar]

- Lauwo, S.G.; Otusanya, O.J.; Bakre, O. Corporate social responsibility reporting in the mining sector of Tanzania: (Lack of) government regulatory controls and NGO activism. Account. Audit. Account. J. 2016, 29, 1038–1074. [Google Scholar] [CrossRef]

- Marsden, C. The new corporate citizenship of big business: Part of the solution to sustainability? Bus. Soc. Rev. 2000, 105, 8–25. [Google Scholar] [CrossRef]

- Detomasi, D.A. The multinational corporation and global governance: Modelling global public policy networks. J. Bus. Ethics 2007, 71, 321–334. [Google Scholar] [CrossRef]

- Yunis, M.S.; Durrani, L.; Khan, A. Corporate Social Responsibility (CSR) in Pakistan: A Critique of the Literature and Future Research Agenda. Bus. Econ. Rev. 2017, 9, 65–88. [Google Scholar] [CrossRef]

- Newenham-Kahindi, A.M. A global mining corporation and local communities in the lake Victoria zone: The case of Barrick Gold multinational in Tanzania. J. Bus. Ethics 2011, 99, 253–282. [Google Scholar] [CrossRef]

- Belal, A.R.; Cooper, S.M.; Roberts, R.W. Vulnerable and exploitable: The need for organizational accountability and transparency in emerging and less developed economies. Account. Forum 2013, 37, 81–91. [Google Scholar] [CrossRef]

- Idemudia, U. Corporate social responsibility and developing countries. Prog. Dev. Stud. 2011, 11, 1. [Google Scholar] [CrossRef]

- Jamali, D.; Neville, B. Convergence Versus Divergence of CSR in Developing Countries: An Embedded Multi-Layered Institutional Lens. J. Bus. Ethics 2011, 102, 599–621. [Google Scholar] [CrossRef] [Green Version]

- Muthuri, J.N.; Gilbert, V. An Institutional Analysis of Corporate Social Responsibility in Kenya. J. Bus. Ethics 2011, 98, 467–483. [Google Scholar] [CrossRef]

- Henry, L.A.; Nysten-haarala, S.; Tulaeva, S.; Tysiachniouk, M. Corporate Social Responsibility and the Oil Industry in the Russian Arctic: Global Norms and Neo-Paternalism. Eur.-Asia Stud. 2016, 68, 1340–1368. [Google Scholar] [CrossRef] [Green Version]

- Zhao, M.; Park, S.H.; Zhou, N. MNC strategy and social adaptation in emerging markets. J. Int. Bus. Stud. 2014, 45, 842–861. [Google Scholar] [CrossRef]

- Husted, B.W.; Allen, D.B. Corporate social responsibility in the multinational enterprise: Strategic and institutional approaches. J. Int. Bus. Stud. 2006, 37, 838–849. [Google Scholar] [CrossRef] [Green Version]

- Tan, J. Institutional structure and firm social performance in transitional economies: Evidence of multinational corporations in China. J. Bus. Ethics 2009, 86, 171–189. [Google Scholar] [CrossRef]

- Moon, J.; Shen, X. CSR in China research: Salience, focus and nature. J. Bus. Ethics 2010, 94, 613–629. [Google Scholar] [CrossRef]

- Kostova, T.; Zaheer, S. Organizational legitimacy under conditions of complexity: The case of the multinational enterprise. Acad. Manag. Rev. 1999, 24, 64–81. [Google Scholar] [CrossRef]

- Bashir, N.; Papamichail, K.N.; Malik, K. Use of Social Media Applications for Supporting New Product Development Processes in Multinational Corporations. Technol. Forecast. Soc. Chang. 2017, 120, 176–183. [Google Scholar] [CrossRef]

- Belal, A.; Owen, D.L. The rise and fall of stand-alone social reporting in a multinational subsidiary in Bangladesh: A case study. Account. Audit. Account. J. 2015, 28, 1160–1192. [Google Scholar] [CrossRef]

- Utting, P. Corporate responsibility and the movement of business. Dev. Pract. 2005, 15, 375–388. [Google Scholar] [CrossRef]

- Bondy, K.; Starkey, K. The dilemmas of internationalization: Corporate social responsibility in the multinational corporation. Br. J. Manag. 2014, 25, 4–22. [Google Scholar] [CrossRef] [Green Version]

- Islam, M.A.; Deegan, C. Media pressures and corporate disclosure of social responsibility performance information: A study of two global clothing and sports retail companies. Account. Bus. Res. 2010, 40, 131–148. [Google Scholar] [CrossRef]

- Carroll, A.B. A three-dimensional conceptual model of corporate performance. Acad. Manag. Rev. 1979, 4, 497–505. [Google Scholar] [CrossRef]

- Carroll, A.B. Managing ethically with global stakeholders: A present and future challenge. Acad. Manag. Exec. (1993–2005) 2004, 18, 114–120. [Google Scholar] [CrossRef]

- Carroll, A.B. The pyramid of corporate social responsibility: Toward the moral management of organizational stakeholders. Bus. Horiz. 1991, 34, 39–48. [Google Scholar] [CrossRef]

- Wood, D.J. Corporate social performance revisited. Acad. Manag. Rev. 1991, 16, 691–718. [Google Scholar] [CrossRef]

- Swanson, D.L. Addressing a theoretical problem by reorienting the corporate social performance model. Acad. Manag. Rev. 1995, 20, 43–64. [Google Scholar] [CrossRef]

- Frederick, W.C. From CSR1 to CSR2: The maturing of business-and-society thought. Bus. Soc. 1994, 33, 150–164. [Google Scholar] [CrossRef]

- Davis, K. The case for and against business assumption of social responsibilities. Acad. Manag. J. 1973, 16, 312–322. [Google Scholar]

- Preston, L.; Post, J. Measuring corporate responsibility. J. Gen. Manag. 1975, 2, 45–52. [Google Scholar] [CrossRef]

- Meehan, J.; Meehan, K.; RICHARDS, A. Corporate social responsibility: The 3C-SR model. Int. J. Soc. Econ. 2006, 33, 386–398. [Google Scholar] [CrossRef]

- Agle, B.R.; Kelley, P.C. Ensuring validity in the measurement of corporate social performance: Lessons from corporate United Way and PAC campaigns. J. Bus. Ethics 2001, 31, 271–284. [Google Scholar] [CrossRef]

- Wood, D.J.; Jones, R.E. Stakeholder mismatching: A theoretical problem in empirical research on corporate social performance. Int. J. Org. Anal. 1995, 3, 229–267. [Google Scholar] [CrossRef]

- Aupperle, K.E.; Carroll, A.B.; Hatfield, J.D. An empirical examination of the relationship between corporate social responsibility and profitability. Acad. Manag. J. 1985, 28, 446–463. [Google Scholar]

- Pinkston, T.S.; Carroll, A.B. Corporate citizenship perspectives and foreign direct investment in the US. J. Bus. Ethics 1994, 13, 157–169. [Google Scholar] [CrossRef]

- Rondinelli, D.A.; Berry, M.A. Environmental citizenship in multinational corporations: Social responsibility and sustainable development. Eur. Manag. J. 2000, 18, 70–84. [Google Scholar] [CrossRef]

- Shamir, R. The de-radicalization of corporate social responsibility. Crit. Soc. 2004, 30, 669–689. [Google Scholar] [CrossRef]

- Hess, D.; Warren, D.E. The meaning and meaningfulness of corporate social initiatives. Bus. Soc. Rev. 2008, 113, 163–197. [Google Scholar] [CrossRef]

- Harrison, J.S.; Freeman, R.E. Stakeholders, social responsibility, and performance: Empirical evidence and theoretical perspectives. Acad. Manag. J. 1999, 42, 479–485. [Google Scholar]

- Friedman, M.A. Friedman doctrine: The social responsibility of business is to increase its profits. N. Y. Times Mag. 1970, 13, 32–33. [Google Scholar]

- Donaldson, T.; Preston, L.E. The stakeholder theory of the corporation: Concepts, evidence, and implications. Acad. Manag. Rev. 1995, 20, 65–91. [Google Scholar] [CrossRef]

- Freeman, R.E. Strategic Management: A Stakeholder Approach; Cambridge University Press: Pitman, NJ, USA, 1984. [Google Scholar]

- Jones, T.M. Corporate social responsibility revisited, redefined. Calif. Manag. Rev. 1980, 22, 59–67. [Google Scholar] [CrossRef]

- Mitchell, R.K.; Agle, B.R.; Wood, D.J. Toward a theory of stakeholder identification and salience: Defining the principle of who and what really counts. Acad. Manag. Rev. 1997, 22, 853–886. [Google Scholar] [CrossRef]

- Campbell, J.L. Institutional analysis and the paradox of corporate social responsibility. Am. Behav. Sci. 2006, 49, 925. [Google Scholar] [CrossRef]

- Waddock, S.A.; Graves, S.B. The corporate social performance–financial performance link. Strateg. Manag. J. 1997, 18, 303–319. [Google Scholar] [CrossRef]

- Da Silva Monteiro, S.M.; GUZMÁN, B.A. The influence of the Portuguese environmental accounting standard on the environmental disclosures in the annual reports of large companies operating in Portugal: A first view (2002–2004). Manag. Environ. Qual. Int. J. 2010, 21, 414–435. [Google Scholar] [CrossRef]

- Lungu, C.I.; Caraiani, C.; Dasclu, C. Research on Corporate Social Responsibility Reporting. Amfiteatru Econ. J. 2011, 13, 117–131. [Google Scholar]

- Apostolou, A.K.; Nanopoulos, K.A. Voluntary accounting disclosure and corporate governance: Evidence from Greek listed firms. Int. J. Account. Financ. 2009, 1, 395–414. [Google Scholar] [CrossRef]

- Meek, G.K.; Roberts, C.B.; Gray, S.J. Factors influencing voluntary annual report disclosures by US, UK and continental European multinational corporations. J. Int. Bus. Stud. 1995, 26, 555–572. [Google Scholar] [CrossRef]

- Oliver, C. Strategic responses to institutional processes. Acad. Manag. Rev. 1991, 16, 145–179. [Google Scholar] [CrossRef]

- Hooghiemstra, R. Corporate communication and impression management–new perspectives why companies engage in corporate social reporting. J. Bus. Ethics 2000, 27, 55–68. [Google Scholar] [CrossRef]

- Government of Pakistan, Ministry of Finance. Economic Survey of Pakistan Islamabad Pakistan 2016. Available online: http://www.finance.gov.pk/survey_1617.html (accessed on 20 June 2017).

- Ministry of Finance. Government of Pakistan Economic Survey 2005–2006. Available online: http://www.finance.gov.pk/survey/home.htm (accessed on 20 June 2017).

- Eisenhardt, K.M.; Graebner, M.E. Theory building from cases: Opportunities and challenges. Acad. Manag. J. 2007, 50, 25–32. [Google Scholar] [CrossRef]

- Cavana, R.Y.; Delahaye, B.L.; Sekaran, U. Applied Business Research: Qualitative and Quantitative Methods; Wiley and Sons: Milton, Austrailia, 2001. [Google Scholar]

- Patton, M.Q. Qualitative Research and Evaluation Methods; Sage Publications, Inc.: Thousand Oaks, CA, USA, 2002. [Google Scholar]

- Huberman, M.; Miles, M.B. The Qualitative Researcher’s Companion; Sage: Thousand Oaks, CA, USA, 2002. [Google Scholar]

- Kvale, S. Interviews: An Introduction to Qualitative Research Interviewing; Sage Publications, Inc.: Thousand Oaks, CA, USA, 1996. [Google Scholar]

- Miles, M.B.; Huberman, A.M. Qualitative Data Analysis: A Sourcebook of New Methods; Sage Publications: Thousand Oaks, CA, USA, 1984. [Google Scholar]

- Begley, T.M.; Boyd, D.P. The need for a corporate global mind-set. MIT Sloan Manag. Rev. 2003, 44, 25–32. [Google Scholar]

- Muller, A.; Kolk, A. CSR performance in emerging markets evidence from Mexico. J. Bus. Ethics 2009, 85, 325–337. [Google Scholar] [CrossRef]

- Wartick, S.L. Issues Management: Corporate Fad or Corporate Function; Edison Electric Institute: Washington, DC, USA, 1987. [Google Scholar]

- Jamali, D.; Sidani, Y. Is CSR counterproductive in developing countries: The unheard voices of change. J. Chang. Manag. 2011, 11, 69–71. [Google Scholar] [CrossRef]

- Khan, F.R.; Lund-Thomsen, P. CSR as imperialism: Towards a phenomenological approach to CSR in the developing world. J. Chang. Manag. 2011, 11, 73–90. [Google Scholar] [CrossRef]

Figure 1.

Pyramid of global corporate social responsibility and performance (Carroll [45], p. 116).

Figure 1.

Pyramid of global corporate social responsibility and performance (Carroll [45], p. 116).

Figure 2.

Proposed model for this study: A global CSR model (author(s) version).

Figure 3.

Characteristics of developing countries as compared to developed countries.

{kind=link}

{kind=link}

{kind=link}

Table 1.

The CSP Model (Wood, [47] p. 694).

Table 1.

The CSP Model (Wood, [47] p. 694).

| Principles of Corporate Social Responsibility |

|---|

| Institutional principle: legitimacy |

| Organizational principle: public responsibility |

| Individual principle: managerial discretion |

| Processes of Corporate Social Responsiveness |

| Environmental assessment |

| Stakeholder management |

| Issues management |

| Outcomes of Corporate Behavior |

| Social impacts |

| Social programs |

| Social policies |

Table 2.

Sample profile.

| Company | Operations | Managerial Position | Duration of Interview | Subsidiary Office Location | Origin |

|---|---|---|---|---|---|

| A | Tobacco & Cigarettes | CSR Manager | 55 m | Islamabad, Pakistan | UK |

| B | Oil & Gas Exploration and Production | CSR Manager | 90 m | Islamabad, Pakistan | Austria |

| C | Telecommunication Service Provider | Strategy Head | 50 m | Islamabad, Pakistan | China |