1. Introduction

Since the industrial revolution, western countries have gradually achieved material prosperity, but with it have come the destruction of the environment. The awareness of environmental protection has sprouted in industrialized countries, and people have slowly realized that although the natural process of the earth will slow down the increase of pollution, it cannot offset the environmental pollution burden caused by human activities [

1,

2]. Examples of this include population explosion, rapid depletion of resources, and increasing industrialization and urbanization. Since China’s Reform and Opening-up put forward a development guiding principle with economic construction as the top priority, China has become the second largest economy in the world. However, the rapid growth of China’s GDP has come at the expense of the environment; after years of focusing on economic development and neglecting environmental protection, China’s ecological environment can no longer be ignored. Recently, the Chinese government has increasingly mentioned a green development concept that considers economic and environmental benefits. China’s current imperfect handling and feedback mechanism for ecological pollution has brought many problems. On the one hand, there is a long tail and massive amount of environmental liability compensation, and on the other hand, there has been irreversible damage to the air, land, water quality, and human body [

3]. In this case, small and medium-sized companies that are required to bear the responsibility for pollution will face a huge burden. Even for a large company that can afford it, high litigation and claims costs would seriously affect the daily operations and innovation. Since the 21st century, many countries have begun implementing effective policies to urge enterprises to take care of the environment and reduce the risk of pollution. A standard method is to jointly formulate policies with insurance associations to require or even force corporations that may have environmental pollution risks to purchase EPLI as part of a new market-based approach to environmental risk management [

4]. Due to its relatively limited coverage, high premium rates, low loss rates, and lack of legal backing and specialized capabilities [

5], EPLI suffers a “Best Game No One Played” dilemma and EPLI’s development in China has stalled [

6].

The findings of this study can be summarized in the following three aspects. First of all, the future developmental logic of human beings must be based on the premise of environmental protection through the development of technology and energy technology iterations to achieve industrial upgrading and improve the green governance system [

7,

8]. The direction of industrial upgrading and development has always been highly valued by Chinese national strategy [

9], so it is necessary to continue studying EPLI, which is regarded as a new green governance method. Secondly, China’s EPLI has appeared for more than 30 years. Compared with developed countries, its application degree is still in its infancy. Although there are urgent practical needs, the absence of legislation and the failure of supporting policies [

6], as well as various economic reasons, means that the promotion of EPLI in various regions encounters different problems. Even though scholars have attempted some interdisciplinary approaches to help EPLI advance the range of its applications [

10,

11,

12], they are still rarely used in practice. On the whole, the rise of EPLI has not met expectations. The progress in most promoted areas is relatively slow, and the sites that have not been promoted are still passively watching. It is strategically vital to find out its problems in the market promotion. Thirdly, for the literature research on EPLI in China, most of the existing literature research on EPLI is in the stage of theoretical analysis [

13], most of which is discussion of legislation issues [

14]. The few empirical studies are mainly aimed at financing costs [

15], environmental management effects [

16], and other issues, and there are few empirical studies on the green governance effects and eventual economic effects of EPLI. The supplementary discussion on the impact of EPLI on corporate performance is of reference value for corporate decision making and local policy formulation. The primary purpose of this study is to find out how EPLI for environmental issues affects corporate performance in the background of corporate green economic development. At the same time, as a corporate management tool for green growth, EPLI’s supervisory attributes and resulting green governance effects are of great significance to the direction of future green policies and the development prospects of other types of liability insurance.

This paper firstly consults a large number of literatures on EPLI and corporate performance, summarizes the research ideas, methods and conclusions of scholars, and forms the research hypothesis and empirical research path. This paper’s primary work and marginal contribution are to study the impact of EPLI on corporate performance and the mediating effect of CSR and heterogeneity analysis. The steps are as follows: the first is to measure and verify the overall impact of EPLI on corporate performance through the fixed effect model and robustness test, where it is found that EPLI has a specific inhibitory effect on corporate performance. The second is to study the relationship between EPLI’s insurance and CSR evaluation. On the one hand, EPLI and CSR evaluation are negatively correlated; on the other hand, CSR has played a specific mediating role in the impact of EPLI on corporate performance. The third is to study the heterogeneity of the effects of EPLI on corporate performance. Among them, for corporations with different property ownership, the impact of EPLI on state-owned corporations is lower than that of non-state-owned corporations, and it can be seen from the empirical test that the difference is relatively significant. Subsequently, the impact of EPLI on heavily polluting corporations is significant, but it does not show substantial adverse effects on non-heavy polluting corporations. Third, EPLI has a considerable impact on corporations in the eastern and western regions, which are the two poles of Chinese marketization, but not significant on insurance corporations in the middle region, whose marketization condition is more complex. From the perspective of influence degree, EPLI has a higher impact on the western region than the eastern region, which shows that there is indeed heterogeneity in the effects of EPLI on corporate performance with different types.

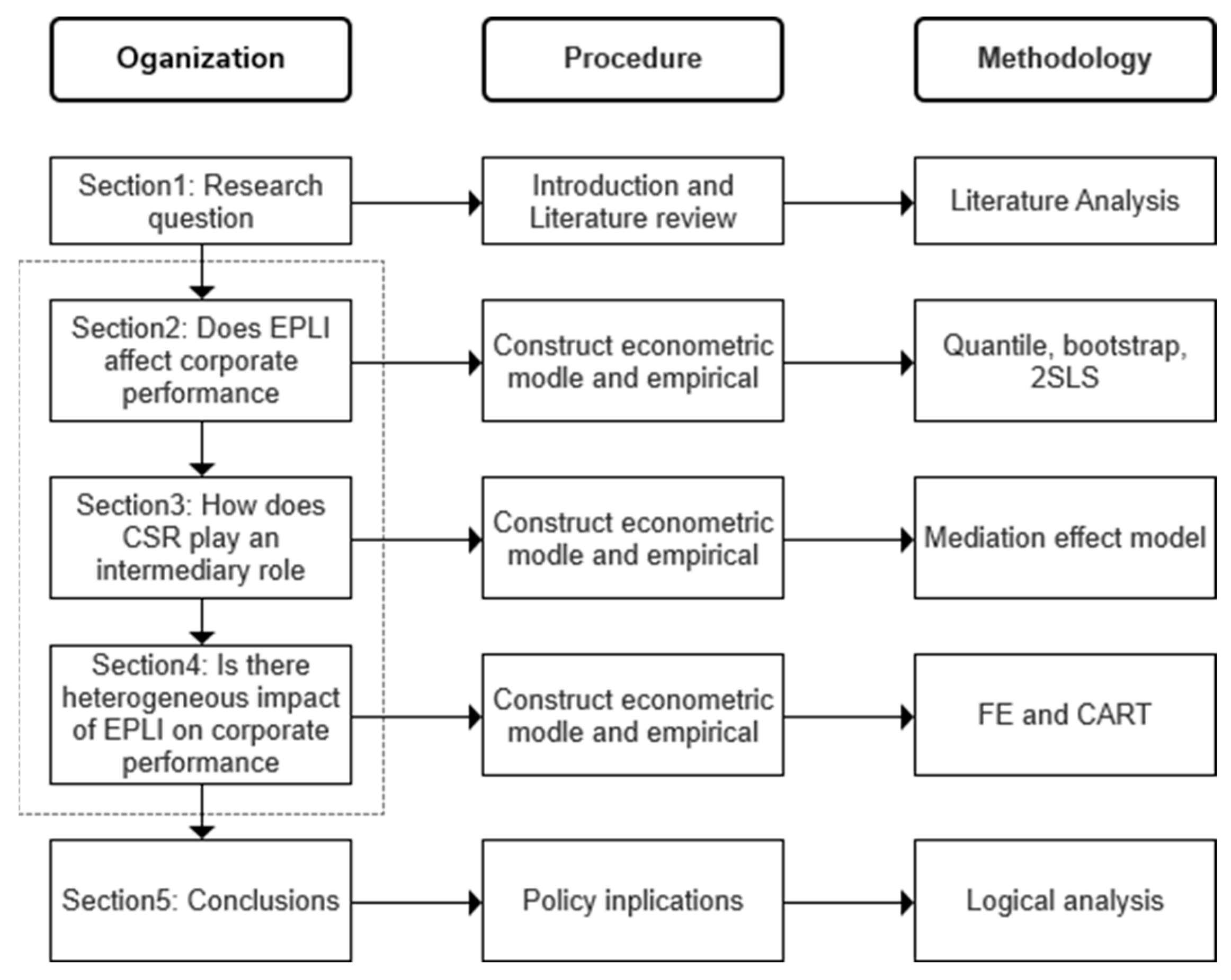

The rest of this paper is structured as follows (see

Figure 1 for the logical framework): the second part is a literature review. The third part is the econometric test of the impact of EPLI on corporate performance. The purpose is to empirically test the effect and significance of the impact of EPLI on corporate performance through sample data, econometric models and robustness testing. The fourth part is the mechanism analysis of the impact of EPLI on corporate performance, considering the mediating effect of CSR evaluation. The fifth part is the heterogeneity analysis of corporate performance by EPLI. According to the ownership of corporate property, different pollution levels and marketization degree, the influence degree and significance of EPLI on corporate performance in different samples are studied. The sixth part draws the basic conclusions.

2. Literature Review

Liability insurance plays several critical roles in corporate management. From the perspective of corporate performance, corporate risk-taking means the risk choice of corporate governance and shareholders when making decisions. It reflects that enterprise managers integrate various internal and external factors to analyze and select uncertain capital investment projects. It is also the strategic trend of enterprises to strive for competitive advantages and high returns [

17]. Increasing the degree of risk-taking can optimize the efficiency of capital allocation [

18] and improve corporate performance [

19], which is the driving force for sustainable economic growth and sustainable corporate development [

20,

21]. Since information asymmetry in China’s financial market is more severe than in Western countries, and the cost of entrusting environmental pollution liability control via insurance accounts for a higher proportion of working capital. The enterprise value would be affected if the degree of risk-taking is reduced and the conservative production and operation mode is adopted [

20]. The importance of liability insurance for enterprises is mainly reflected in the following points: firstly, it can alleviate the distortion of industrial structure caused by judgment-proof problems [

22,

23]. Debtors can file for bankruptcy in numerous legal systems to eliminate insolvent debts. The problem caused by this is that small corporations are willing to take liability risks that exceed their assets to increase output at lower average production costs and increase their market share [

24], forcing industry leaders to conduct vicious competition [

25,

26]. However, insurance can cover the risk of bankruptcy and ensure that the corporations can afford the loss. Small corporations need to consider the difficulty of filing for bankruptcy when increasing production [

27]. Secondly, insurance can create incentives for corporations to reduce their own risks. After insurance participation in business operations, the bureaucratic management phenomenon in government supervision can be replaced with market-based incentive measures [

28]. Adding insurance gives insurance companies access to detailed data on historical corporate liability events and helps actuaries develop detailed pricing. Since premium depends on expected losses, it increases the enterprise’s incentive to maintain a good history. From a social perspective, insurance is a “general technology to rationalize society” in promoting corporations by improve green supply chain management [

29]. Thirdly, insurance can give insurance companies the right to monitor in the form of contracts, reducing the frequency of environmental pollution losses. Since insurance pricing occurs before the next accident, corporations could be motivated to raise their safety standards and seek the most significant possible reduction in insurance premiums to conduct a cost–benefit analysis and implement preventive measures [

30].

The previous literature has shown that EPLI affects businesses in several ways. Environmental pollution occurs in the lifecycle of modern industries, including production, transportation, consumer use and waste disposal. Public attention has increased the need for environmental governance, and the resulting regulations have increased the risk of corporate bankruptcy [

31]. Dropulić and Cular (2019) [

32] believe that EPLI can improve the disclosure quality of corporate environmental information, and the supervision of local governments shows a “complementary effect”. Similar studies have also assessed the impact of EPLI on corporate pollution, the likelihood of environmental hazards and corporate environmental performance [

25,

33]. Their findings are that EPLI participation can improve the ecological outcomes of polluting corporations. However, some views believe in a premise that only if insurance corporations do not pay for corporate bankruptcy due to environmental pollution, EPLI will enhance environmental protection efforts, and the result of insurance is reduced production [

34]. This suggests that, although insurance can urge corporations to appear environmentally friendly, the actual economic utility may not be as expected because they cannot achieve the desired output of corporations. In practice, the information asymmetry between insurance companies and corporations can be severe, and insurance can easily become a tool used by corporations to transfer responsibility. When the management of corporations take compensation as their motive for insurance, they may take some “masking effect” behaviors to justify their “risk reduction efforts” to obtain compensation [

35]. If it is challenging to monitor corporations’ contamination and cover-up, insurers will take on greater payout risk, creating a moral hazard problem [

24]. Some scholars have also proposed the promotion model of EPLI, such as the industry co-insurance [

36] and the establishment of securitization products [

11]. However, in the end, it may not alleviate the problem of enterprise performance, so it is not easy to really improve the stagnation of EPLI promotion.

Many scholars believe that a multi-layered relationship exists between CSR and environmental pollution, affecting corporate performance from various perspectives, such as the heterogeneity of industry categories or the lag effect [

12,

37]. With the continuous improvement of corporate governance structure, CSR has gradually attracted the attention of academia. In the early literature, that representative of neoliberal economists, Friedman and others, believed that the only social responsibility that corporations need to undertake was the interests of shareholders [

34]. However, more and more scholars believe that CSR also includes multiple responsibilities to consumers, communities and the environment [

38,

39]. The CSR score of the Hexun survey used in this paper combines five categories, including responsibility to shareholders (30%), responsibility to employees (15%), responsibility to suppliers, customers and consumers (15%), environmental responsibility (20%), and social contribution responsibility (20%). Among them, environmental responsibility is scored by combining five dimensions: corporate environmental protection awareness, environmental management system certification, environmental protection investment amount, pollutant discharge type and energy-saving type, and the score is related to the environmental performance of corporations [

40]. Although in the corporations participating in the EPLI, insurers may play several roles under contractual deductibles, such as the review and supervision of management, production, operations and risk control. There are also obligations to urge enterprises to protect the environment and prevent pollution. But in the end, the impact on corporations has little effect [

13], and it will expose the behavior of corporations to transfer responsibility for environmental pollution. According to stakeholder-related theory and social contract theory, corporate management needs to maintain a principal–agent relationship formed by multiple contracts, and the execution effect of the contract directly affects the CSR evaluation of corporations [

41]. However, the reputation increase brought by CSR has no obvious impact on financial value and performance, so management may be reluctant to assume social responsibility during non-crisis periods [

42]. Although the government will promulgate various laws and regulations to promote corporations to implement CSR, the initiative of corporations mainly comes from corporate governance goals and strategies aimed at maximizing profits.

The investment into EPLI will help corporations avoid high liability and compensation and increase the expectation of operating at a profit, much as corporate management and shareholders will reach a better Pareto insurance decision and have the opportunity to seek government subsidies to achieve the best multi-party game strategy [

43], but then there will be severe adverse selection and moral hazard problems. Specifically, first of all, due to China’s gradual loose monetary policy in recent years, corporations have increased access to financing [

44], and at the same time, corporations are also required to increase profit margins and speed up producing on and operating cycles to maximize profits. With the accumulation of market monopoly, corporations have less incentive to improve the market through innovation [

45], and it is easier to choose between taking risks and increasing production in the form of expanding scale. Indeed, the lowering of entry barriers for manufacturing industries has intensified competitive pressures [

46]. Secondly, according to the perfect competition model, the production and operation of corporations under tremendous competitive pressure will either choose to pollute but make a profit, or strive for compensation or no pollution to obtain a small profit [

47]; therefore, corporations would choose the former in the game of high premium investment. In the end, there may be a phenomenon in which bad money drives out good money in any area where EPLI exists: all corporations that can transfer pollution liability and obtain higher profits by taking out environmental liability insurance choose to insure. The increase in the loss ratio will increase EPLI premiums, crowding out corporations with less serious pollution, and further increasing the loss ratio and premiums. After such an upward spiral, in the end, only corporations with poor CSR evaluations are willing to take the initiative to choose insurance. A similar situation also occurs in other types of liability insurance, such as directors’ and officers’ liability insurance (D&O), which has been discussed frequently in recent years, and its intervention will instead contribute to the risk of corporate litigation [

48]. Finally, because of corporations’ CSR disclosure, third-party audits and the disclosure of professional information platforms, corporations with serious pollution and EPLI will receive lower CSR scores because of their irresponsibility to multiple parties and poor environmental performance.

The above studies provided reference experience and new ideas for this research and related topics, and some Chinese viewpoints provide a reference value for the research route of this paper. For example, the study of the economic significance of insurance, of environmental pollution performance, of environmental information gaps, and of financing constraints are helpful to this paper’s methodology. Although they do not cover the research topic and purpose of this paper, they provide a reference for the research route of this paper and are listed in

Table 1.

5. Conclusions

First, the purchase of EPLI by corporations can have a significant negative impact on corporate performance. On the one hand, EPLI purchases can affect the capital flow of corporations, resulting in less capital being available to corporations for operations. On the other hand, the supervision and control of insurance corporations brought by the purchase of EPLI, as well as the constraints of regulations, will enhance the self-prevention level of corporations, which cannot fully maximize production. Furthermore, negative effects remained significant after excluding outliers, sample size bias, and cluster hierarchical standard errors.

Second, CSR, as a score of corporate responsibility to various fields of objects, has a mediating effect on the impact of EPLI on corporate performance. The purchase of EPLI by corporations will not only hurt the evaluation of CSR but will ultimately further affect corporate performance. The impact of EPLI on corporate performance is partly through price and insurance effects, and partly through the disclosure of environmental information, which reduces CSR scores and corporate reputation.

Finally, the impact of EPLI on corporate performance is heterogeneous, reflected in the differences in property ownership, corporate pollution degree and the degree of marketization in the region. First, EPLI has a more significant impact on non-SOEs than SOEs; second, the impact on heavily polluting corporations is greater; third, regions with a high degree of regional marketization will offset the negative effects of some EPLI purchases.

The existing literature has focused on branch studies of EPLI, CSR, and firm performance, providing useful evidence for this study, but not directly reflecting their relation. The research in this paper increases the marginal contribution of EPLI’s economic effects, which may provide a reference for corporate green management decisions. However, the research content of this paper has certain limitations. First of all, since the public data on EPLI purchases include too few years, the lagging effect of EPLI cannot be studied, and the effect of long-term renewal is also worth researching; secondly, the reasons for each enterprise to purchase EPLI need to be analyzed from the perspective of cost. However, the current development of EPLI in China may lead to the fact that the terms of the insurance policy cannot be formulated according to the individual risk level but can only reflect the differences between regions and industries. Thirdly, the influence of the development of the times on the theme needs to be studied. However, due to data availability, this paper cannot cover this part of the analysis for the time being. It is hoped that the research in this paper will take these limitations into account in the future and provide valuable risk management approaches for corporate green development strategies.

Based on the research in this paper, the following insights can be obtained: first, government departments should continue to support the reform of China’s EPLI system. They should further develop and refine the division of EPLI subjects and formulate differentiated insurance cooperation models for corporations in different regions, with different property ownership and different pollution degrees, and gradually extend to other liability insurance application scenarios, to better play the social management function of insurance and promote the sustainable development of the green economy. Second, they should unswervingly adhere to the basic guiding principle of “government promotion and market operation.” Based on the existing state of supply and demand, the supply of insurance is promoted in the form of policy subsidies. Government should encourage corporations to participate in insurance and disclose environmental information governance, and to steadily resolve the embarrassing situation of “double cold supply and demand” caused by adverse selection of liability insurance. They should promote the preference for cleaner production and the commitment to environmental liability in the process of deepening the reform of corporations, so that corporations can combine internal and external governance with improving corporate performance. Third, government departments should pay more attention to and improve the construction of an ecological and environment legal system. Government should not only improve the compensatory punishment for pollution, but also make efforts to create a better atmosphere for social supervision, to stimulate the concern and enthusiasm of the general public, media, social organizations and other groups for measures to protect the environment. Finally, they should act by formulating policies to help insurance institutions maximize their professional supervision and management functions, thereby helping liability insurance to play its essential functions from multiple directions.

{kind=link}