On the Moments and the Distribution of Aggregate Discounted Claims in a Markovian Environment

1

Centre for Actuarial Studies, Department of Economics, The University of Melbourne, Melbourne 3010, Australia

2

Department of Statistics and Actuarial Science, Simon Fraser University, Burnaby, BC V5A 1S6, Canada

*

Author to whom correspondence should be addressed.

Risks 2018, 6(2), 59; https://doi.org/10.3390/risks6020059

Submission received: 7 May 2018

/

Revised: 17 May 2018

/

Accepted: 21 May 2018

/

Published: 23 May 2018

(This article belongs to the Special Issue Risk, Ruin and Survival: Decision Making in Insurance and Finance)

Abstract

:This paper studies the moments and the distribution of the aggregate discounted claims (ADCs) in a Markovian environment, where the claim arrivals, claim amounts, and forces of interest (for discounting) are influenced by an underlying Markov process. Specifically, we assume that claims occur according to a Markovian arrival process (MAP). The paper shows that the vector of joint Laplace transforms of the ADC occurring in each state of the environment process by any specific time satisfies a matrix-form first-order partial differential equation, through which a recursive formula is derived for the moments of the ADC occurring in certain states (a subset). We also study two types of covariances of the ADC occurring in any two subsets of the state space and with two different time lengths. The distribution of the ADC occurring in certain states by any specific time is also investigated. Numerical results are also presented for a two-state Markov-modulated model case.

1. Introduction

Consider a line of business or an insurance portfolio to be insured by a property and casualty insurance company. Suppose that random claims arrive in the future according to a counting process, denoted by , i.e., is the random number of claims up to time t. Assume that is a sequence of random claim occurrence times and is a sequence of corresponding random positive claim amounts (also called claim severities), and is the force of interest at time t, which is modeled by a stochastic process. Then defined by

is the aggregate discounted claims (ADCs) up to certain time t, or the present value of the total amounts paid out by the company up to time t, which describes the random change over time of the insurer’s future liabilities at present time. Accordingly, is the ADC process (compound discounted claims) for this business. At a fixed time t, the randomness of comes from the number of claims up to time t, claim occurrence times, and corresponding sizes as well as the values of . It is an important quantity in the sense that, at the time of issue (), this quantity would help insurers set a premium for this particular line of business, and predict and manage their future liabilities.

A simple case of model (1) is one in which the counting process is a homogeneous Poisson process, independent of claim amounts, and the force of interest is deterministic. In this paper, we assume that the counting process is a Markovian arrival process (MAP) with representation , introduced by Neuts (1979). That is, claim arrivals are influenced by an underlying continuous-time Markov process on state space with an intensity matrix and initial distribution , where , and is assumed to be irreducible. Precisely, represents the intensity of transitions from state i to state j without claim arrivals, while represents the intensity of transitions from state i to state j with an accompanying claim, having a cumulative distribution function , density function k-th moment and Laplace transform Here, the process models the random environment, which affects the frequency and the severity of claims and thus the insurance business; for example, it is well known that the weather or climate conditions have impacts on automobile, property and casualty insurance claims.

Moreover, we assume that the force of interest process in (1) is also governed by the same Markov process and is assumed constant while staying at certain state, that is, when , for all . As the force of interest used for evaluation is mainly driven by the local or global economics conditions, we would reasonably model its random fluctuations by a stochastic process that is different from . Technically, we can assume a two-dimensional Markov process as the environment or background process and other mathematical treatments would be the same as we do below. Hence, we make the above assumption in this paper to simplify notations and presentations. We note that studies of the influence of economic conditions such as interest and inflation on the classical risk theory can be found in papers by Taylor (1979), Delbaen and Haezendonck (1987), Willmot (1989), and Garrido and Léveill (2004).

The MAP has received considerable attention in recent decades due to its versatility and feasibility in modeling stochastic insurance claims dynamics. MAPs include Poisson processes, renewal processes with the inter-arrival times following phase-type distributions, and Markov-modulated Poisson processes as special cases, which are intensively studied in actuarial science literature. Detailed characteristics and properties of MAPs can be found in papers by Neuts (1979) and Asmussen (2003). Below, we present a brief literature review on the related work based on models given by Equation (1) (including its special cases).

Most of the studies on model (1) are under the assumption that is deterministic. For the ADC, Léveillé and Garrido (2001a) give explicit expressions for its first two moments in the compound renewal risk process by using renewal theory arguments, while Léveillé and Garrido (2001b) further derive a recursive formula for the moments calculation. Léveillé et al. (2010) study the moment generating function (mgf) of the ADC by finite and infinite time under a renewal risk model or a delayed renewal risk model. Recently, Wang et al. (2018) studied the distribution of discounted compound phase-type renewal sums using the analytical results of their mgf obtained by Léveillé et al. (2010). Jang (2004) obtains the Laplace transform of the distribution of the ADC using a shot noise process. Woo and Cheung (2013) derive recursive formulas for the moments of the ADC using techniques used by Léveillé and Garrido (2001b), for a renewal risk process with certain dependence between the claim arrival and the amount caused. The impact of the dependency on the ADC are illustrated numerically. Kim and Kim (2007) derive simple expressions for the first two moments of the ADC when the rates of claim arrivals and the claim sizes depend on the states of an underlying Markov process. Ren (2008) studies the Laplace transform and the first two moments of the ADC following a MAP process, and Li (2008) further derives a recursive formula for the moments of the discounted claims for the same model. Barges et al. (2011) study the moments of the ADC in a compound Poisson model with dependence introduced by a Farlie–Gumbel–Morgenstern (FGM) copula; Mohd Ramli and Jang (2014) further derive Neumann series expression of the recursive moments by using the method of successive approximation.

There are few papers that study models described by Equation (1) with a stochastic process in the literature of actuarial science. Leveille and Adekambi (2011, 2012) study the covariance and the joint moments of the discounted compound renewal sum at two different times with a stochastic interest rate where the Ho–Lee–Merton and the Vasicek interest rate models are considered. Their idea of studying the covariance and the joint moments is adopted and extended in this paper. Here, we assume that the components of the ADC process described by Equation (1)—the number of claims, the size of the claims, and the force of interest for discounting—are all influenced by the same Markovian environment process, which enhances the flexibility of the model parameter settings. It follows that depends on the trajectory of this underlying process whose states may represent different external conditions or circumstances that affect insurance claims. The main objective of this paper is to study the moments and the distribution of given in Equation (1), occurring in certain states (e.g., certain conditions) by time t.

In general, while the expectation of at any given time t can be used as a reference for the insurer’s liability, the higher moments of , describing further characteristics of the random variable such as the variability around the mean and how extreme outcomes could go, may be used to determine the marginals on reserves. Furthermore, the distributional results regarding would be useful for obtaining the risk measures such as the value at risk and the conditional tail expectation, which may help insurers prevent or minimize their losses from extreme cases.

Our work is basically a generalization of some aforementioned studies. We first obtain formulas for calculating mean, variance, and distribution of the ADC occurring in a subset of states at a certain time. The subset may represent a collection of similar conditions that the insurer would consider them as a whole. We then derive explicit matrix-analytic expressions for covariances of the ADC occurring in two subsets of the state space at a certain time and those occurring in a certain subset of states with two different time lengths. The motivation of studying these two types of covariance is that we believe they can reveal the correlation between the random discounted sums either between different underlying conditions or with different time lengths, and the information would be helpful for insurers to set their capital requirements for preventing future losses, and make strategic and contingency plans. Moreover, we obtain a matrix-form partial integro-differential equation satisfied by the distribution function of the ADC occurring in certain subset of states. The equation can be solved numerically to obtain the probability distribution function of the ADC, which again could be useful for measuring insurers’ risks of insolvency.

The rest of the paper is organized as follows. In Section 2, we study the joint Laplace transforms of the ADC occurring in each state by time t and pay attention to some special cases. Recursive formulas for calculating the moments of the ADC occurring in certain states are obtained. A formula for computing the covariance of the ADC occurring in two subsets of the state space is derived in Section 3, while the covariance of the ADC occurring in certain states with two different time lengths is studied in Section 4. The distribution of the ADC occurring in certain states is investigated in Section 5. Finally, some numerical illustrations are presented in Section 6.

2. The Laplace Transforms and Moments

We first decompose into m components as

where

is the ADC occurring in state with being the indicator function. For a given ), denote a sub-state space of E. We then define

to be the ADC occurring in the subset of state space In particular, and If and for all , then , where is the number of claims occurring in the sub-state space by time t.

Let and denote conditional probability and conditional expectation given , respectively. Define

to be the joint Laplace transform of given that the initial state is In particular, we have

We define, for the n-th moment of , , and , respectively, as

given that the initial state is i.

We write the following column vectors for the Laplace transforms

with

In this section, we first show that satisfies a matrix-form first-order partial differential equation, and derive recursive formulas for calculating the moments of various ADC depending on the initial state of the underlying Markovian process. We also consider some special cases.

Theorem 1.

satisfies

where and

Proof.

For an infinitesimal , conditioning on three possible events which can occur in —no change in the MAP phase (state), a change in the MAP phase accompanied by no claims, and a change in the MAP phase accompanied by a claim—we have

Remark 1.

Using the same argument, we have the follow results.

- (1)

- satisfies the following matrix-form first-order partial differential equation:where is an diagonal matrix with the -th entry being , for and all other entries being 1.

- (2)

- satisfieswhere

- (3)

- satisfieswhere

We now study the moments of the ADC considered in Theorem 1. Denote the vectors of the n-th moment of the corresponding ADC as

From Equation (7), we obtain in Theorem 2 a matrix-form first-order differential equation satisfied by the moments of and then, in Theorem 3, obtain recursive formulas for calculating them.

Theorem 2.

The moments of satisfy

with initial conditions and In particular,

where , is an diagonal matrix with the -th entry being for and all other diagonal entries being

Proof.

By Taylor’s expansion (its existence is easily justified as we assume that has moment for any ), we have

In matrix notation,

Corollary 1.

We have the following results for the moments of and

- (i)

- satisfies the matrix-form first-order differential equation:where and In particular, satisfies

- (ii)

- satisfieswhere is a diagonal matrix with the j-th entry being and 0 otherwise, and In particular, satisfies

Solving differential Equation (8) with , we obtain the following recursive formulas for .

Theorem 3.

For and we have

In particular,

Clearly, we have where .

Corollary 2.

If we set and in Theorem 3, we have the following recursive formulas for the moments of and :

In particular,

Remark 2.

When , we have the following asymptotic results for the moments of the ADC for :

where

3. The Covariance of ADC Occurring in Two Sub-State Spaces

In this section, we first calculate the joint moment of the ADC occurring in two subsets of the state space and then the covariance between them could be calculated.

For and , where denote and to be two disjoint subsets of E, i.e., The aggregate discounted claim amounts occurring in and are

Define

to be the joint Laplace transform of and . Let be a column vector with the i-th entry being Moreover, let

be the joint moment of and . Denote as an column vector with the i-th entry being . A matrix-form integral expression of and its asymptotic formula when are presented in the theorem below.

Theorem 4.

For two disjoint subsets of E, and , the joint moment of and satisfies

where is given by Equation (10) in Theorem 3. When , we have

Proof.

Following from Equation (3), we have

where is a diagonal matrix with the -th entry being , for with the -th entry being , for and all other elements being 1.

Remark 3.

If and and we have

When , the joint moment of and can be expressed as

Remark 4.

If two subsets and are not disjoint, i.e., then

All the covariance terms in the expression above are for ADCs occurring in two disjoint sets.

4. The Covariance of the ADC with Two Different Time Lengths

In this section, we investigate the covariance of the ADCs occurring in two (overlapped) time periods, i.e., we want to evaluate

for and with Denote as a column vector with the i-th entry being In the following, we first show in a lemma a result that is needed for deriving the expression for . We then present an explicit formula of in a theorem below.

As we have

Define to be -algebra generated by the ADC process by time t. Using the law of iterated expectation, we have

where is the present value, at time t, of the claims occurring in states within over

Denote where

The following lemma gives a matrix-form integral expression for .

Lemma 1.

is of the form

where is a matrix with -th element being

Proof.

Let Then is the transition matrix of the underlying Markov process at time t. It follows from Ren (2008) that

Theorem 5.

can be expressed as

where is the Hadamard product of and , i.e., the -th element of is and is given by Equation (16) in Lemma 1.

Remark 5.

If or , Equation (19) simplifies to the joint moment of and or the joint moment of and .

5. The Distributions of the ADC

In this section, we investigate the distributions of and its two special cases, and , for . To precede, we define for and

with the following conditions:

where is the number of claims occurring in state k and is the number of claims occurring in the subset Denote

We present in the theorem below that satisfies a first-order partial integro-differential equation in matrix form.

Theorem 6.

satisfies

with initial conditions

where is the solution of the differential equation obtained from Equation (20) by setting

Proof.

Using the same arguments as in Section 2, we have, by conditioning on events that may occur over ,

As is differentiable with respect to x and t, we have

The justification of Equation (23) can be done similarly as that for Equation (5) (see Appendix A). Substituting Equation (23) into Equation (22), rearranging terms, dividing both sides by h, and taking limit as give

For we have

Taylor’s expansion gives

Equations for and can then be expressed in matrix form (20). ☐

Remark 6.

If we set and respectively, we have the following results:

with initial conditions

Here, is the solution of the differential equation obtained from Equation (24) by setting

Remark 7.

Remark 8.

If then with where Taking partial derivative with respect to x on both sides of Equation (20) and performing some manipulations, we obtain the following matrix-form second-order partial differential equation for

This partial differential equation can also be solved numerically by using forward finite difference methods.

6. Numerical Illustrations

In this section, we consider a two-state Markov-modulated with intensity matrix

We also assume that , , and . Table 1 gives the first moments of and and their covariance for , and given and respectively, in which the covariances, for are calculated by

It shows that, as expected, the expected values of and (and hence ) are increasing in t given for It is not surprised to see that and are negatively correlated for any t, as claims occurring in the two states compete with each other. Moreover, the larger the time t, the more the negative correlation between and .

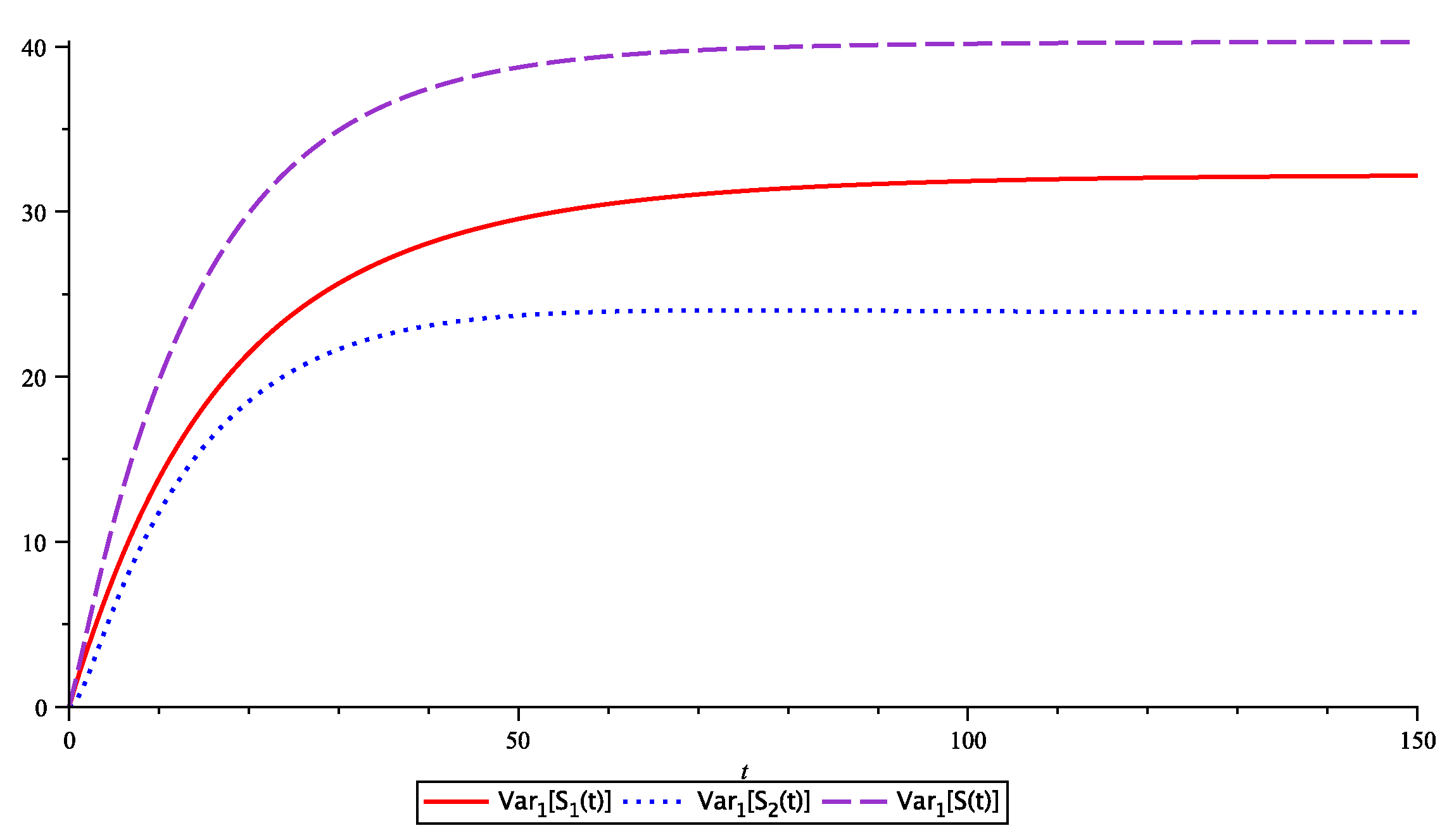

Figure 1 plots the variances of and , given for The variances all increase with time t. The variance of is bigger than those of and for a fixed t. When time t goes to the three variances converge.

Table 2 and Table 3 display the covariances of the ADC at time t and , given , for some selected t values and for and . It is shown that and and and and are all positively correlated. Moreover, when t increases, the covariances increase; moreover, when h increases, the covariances decrease. When the covariances of the pairs and , , and converge to the variances of and , respectively. Similar patterns should be expected for

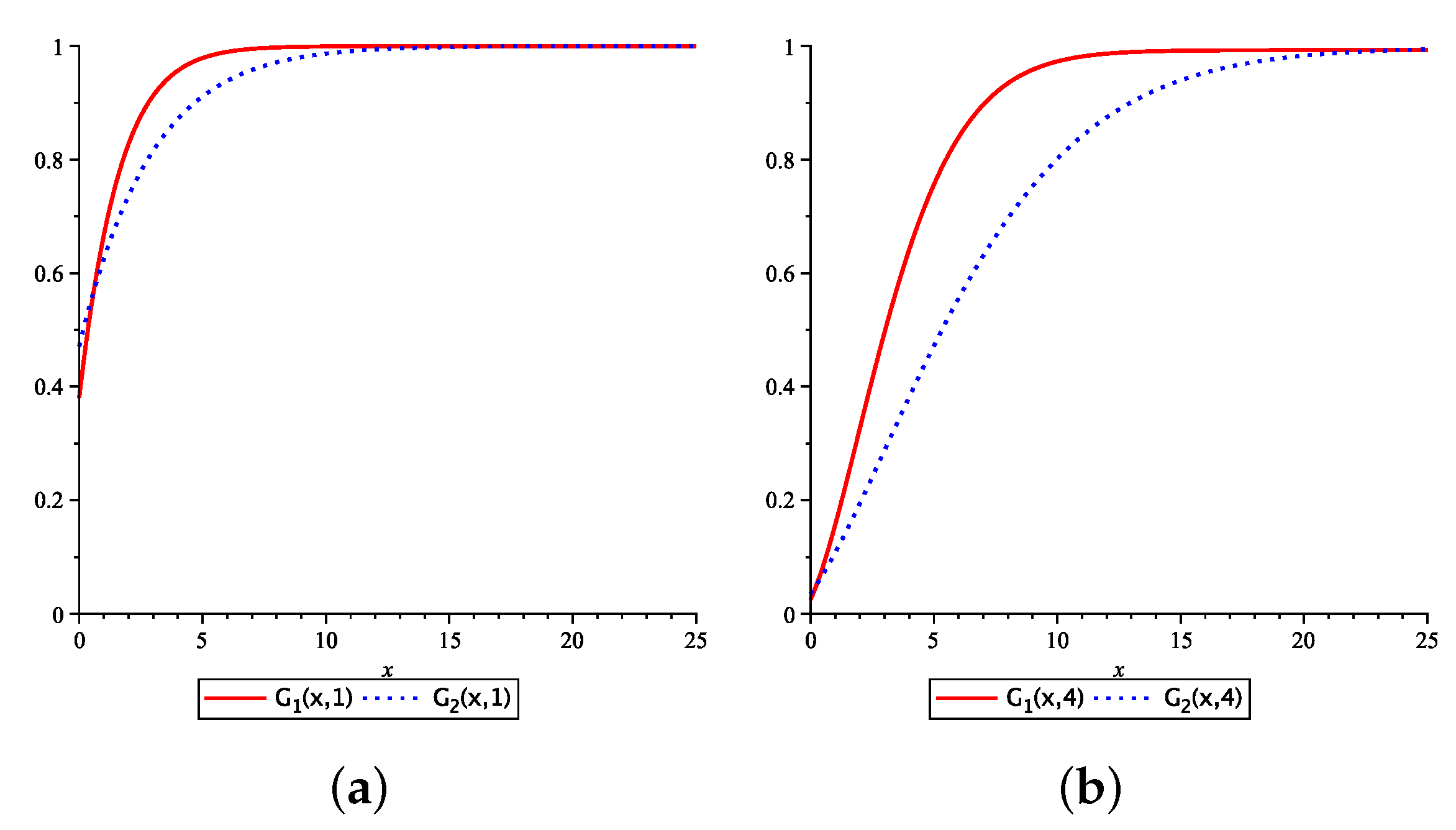

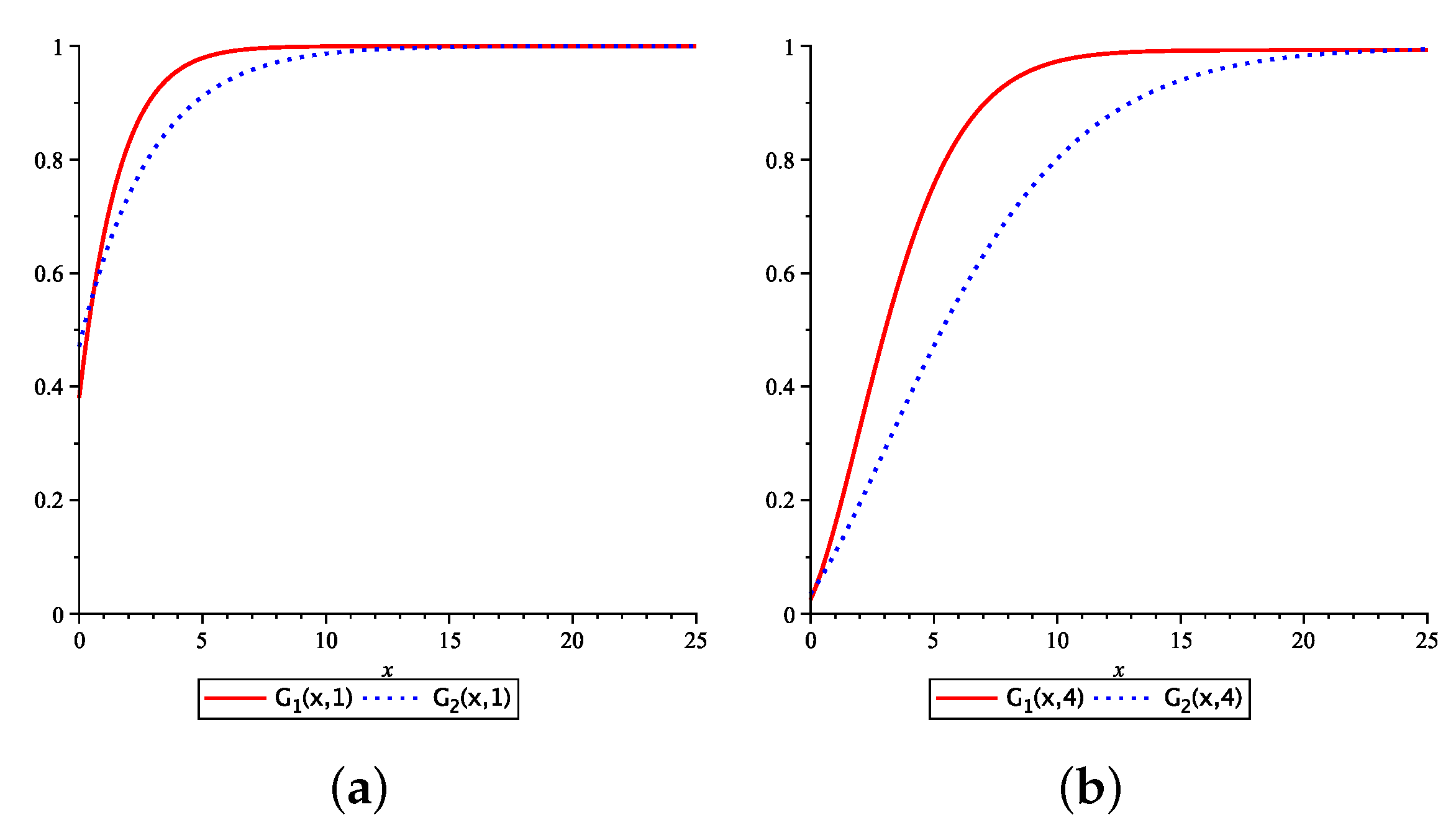

Finally, we display in Figure 2 the numerical values of the distribution function of with initial state i, , for and 4, , and . Note that satisfies the partial differential Equation (25); its solution can be obtained numerically. From the graph, it shows clearly that the probability of being bigger than a fixed x is smaller for small values of t as expected. For most x values, is bigger than due to the fact that the underlying Markov process in our example tends to stay in state 1 more often than staying at state 2.

Author Contributions

The two authors contribute equally to this article.

Acknowledgments

The authors would like to thank two anonymous reviewers for providing helpful comments and suggestions that improved the presentation of this paper. This research for Dr. Yi Lu was supported by the Natural Science and Engineering Research Council (NSERC) of Canada (grant number 611467).

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A. Justification of Equation (5)

It is easy to see that the partial derivation of in Equation (2) with respect to exists for . For its partial derivation with respect to t, we have

Now, under certain regularity conditions, we obtain

Let . Then

Since

it follows from Equation (A1) that

which justifies the existence of the partial derivation of with respect to t.

References

- Asmussen, Søren. 2003. Applied Probability and Queues. New York: Springer. [Google Scholar]

- Barges, Mathieu, Hélene Cossette, Stéphane Loisel, and Etienne Marceau. 2011. On the moments of the aggregate discounted claims with dependence introduced by a FGM copula. ASTIN Bulletin 41: 215–38. [Google Scholar]

- Delbaen, Freddy, and Jean Haezendonck. 1987. Classical risk theory in an economic environment. Insurance: Mathematics and Economics 6: 85–116. [Google Scholar] [CrossRef]

- Garrido, José, and Ghislain Léveillé. 2004. Inflation impact on aggregate claims. Encyclopedia of Actuarial Science 2: 875–78. [Google Scholar]

- Kim, Bara, and Hwa-Sung Kim. 2007. Moments of claims in a Markov environment. Insurance: Mathematics and Economics 40: 485–97. [Google Scholar]

- Jang, Ji-Wook. 2004. Martingale approach for moments of discounted aggregate claims. Journal of Risk and Insurance 71: 201–11. [Google Scholar] [CrossRef]

- Leveille, Ghislain, and Franck Adekambi. 2011. Covariance of discounted compound renewal sums with stochastic interest. Scandinavian Actuarial Journal 2: 138–53. [Google Scholar] [CrossRef]

- Léveillé, Ghislain, and Franck Adékambi. 2012. Joint moments of discounted compound renewal sums. Scandinavian Actuarial Journal 1: 40–55. [Google Scholar] [CrossRef]

- Leveille, Ghislain, and Jose Garrido. 2001a. Moments of compound renewal sums with discounted claims. Insurance: Mathematics and Economics 28: 201–11. [Google Scholar]

- Léveillé, Ghislain, and José Garrido. 2001b. Recursive moments of compound renewal sums with discounted claims. Scandinavian Actuarial Journal 2: 98–110. [Google Scholar] [CrossRef]

- Léveillé, Ghislain, José Garrido, and Ya Fang Wang. 2010. Moment generating functions of compound renewal sums with discounted claims. Scandinavian Actuarial Journal 3: 165–84. [Google Scholar] [CrossRef]

- Li, Shuanming. 2008. Discussion of "On the Laplace transform of the aggregate discounted claims with Markovian arrivals". North American Actuarial Journal 12: 208–10. [Google Scholar] [CrossRef]

- Li, Jingchao, David CM Dickson, and Shuanming Li. 2015. Some ruin problems for the MAP risk model. Insurance: Mathematics and Economics 65: 1–8. [Google Scholar] [CrossRef]

- Mohd Ramli, Siti Norafidah, and Jiwook Jang. 2014. Neumann series on the recursive moments of copula-dependent aggregate discounted claims. Risks 2: 195–210. [Google Scholar] [CrossRef] [Green Version]

- Neuts, Marcel F. 1979. A versatile Markovian point process. Journal of Applied Probability 16: 764–79. [Google Scholar] [CrossRef]

- Ren, Jiandong. 2008. On the Laplace transform of the aggregate discounted claims with Markovian arrivals. North American Actuarial Journal 12: 198–206. [Google Scholar] [CrossRef]

- Taylor, Gregory Clive. 1979. Probability of ruin under inflationary conditions or under experience rating. ASTIN Bulletin 10: 149–62. [Google Scholar] [CrossRef]

- Wang, Ya Fang, José Garrido, and Ghislain Léveillé. 2018. The distribution of discounted compound PH-renewal processes. Methodology and Computing in Applied Probability 20: 69–96. [Google Scholar] [CrossRef]

- Willmot, Gordon E. 1989. The total claims distribution under inflationary conditions. Scandinavian Actuarial Journal 1: 1–12. [Google Scholar] [CrossRef]

- Woo, Jae-Kyung, and Eric CK Cheung. 2013. A note on discounted compound renewal sums under dependency. Insurance: Mathematics and Economics 52: 170–79. [Google Scholar] [CrossRef]

Figure 1.

Variances of , and with initial state .

Figure 2.

Distribution functions of in (a) and in (b) for

{kind=link}

{kind=link}

Table 1.

Expected values and covariances of and .

| t | ||||||

|---|---|---|---|---|---|---|

| 1 | ||||||

| 2 | ||||||

| 5 | ||||||

| 10 | ||||||

| 20 | ||||||

| 30 | ||||||

| ∞ | ||||||

Table 2.

Covariances of discounted claims at t and .

| t | |||

|---|---|---|---|

| 1 | |||

| 2 | |||

| 5 | |||

| 10 | |||

| 20 | |||

| 30 | |||

| ∞ | |||

Table 3.

Covariances of discounted claims at t and .

| t | |||

|---|---|---|---|

| 1 | |||

| 2 | |||

| 5 | |||

| 10 | |||

| 20 | |||

| 30 | |||

| ∞ | |||

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Li, S.; Lu, Y. On the Moments and the Distribution of Aggregate Discounted Claims in a Markovian Environment. Risks 2018, 6, 59. https://doi.org/10.3390/risks6020059

AMA Style

Li S, Lu Y. On the Moments and the Distribution of Aggregate Discounted Claims in a Markovian Environment. Risks. 2018; 6(2):59. https://doi.org/10.3390/risks6020059

Chicago/Turabian StyleLi, Shuanming, and Yi Lu. 2018. "On the Moments and the Distribution of Aggregate Discounted Claims in a Markovian Environment" Risks 6, no. 2: 59. https://doi.org/10.3390/risks6020059

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.