How Does Distress Acquisition Incentivized by Government Purchases of Distressed Loans Affect Bank Default Risk?

1

Department of Statistics, Tamkang University, New Taipei City 25137, Taiwan

2

Department of Wealth and Taxation Management, National Kaohsiung University of Science and Technology, Kaohsiung City 82444, Taiwan

3

School of Economics, Southwestern University of Finance and Economics, Chengdu 611130, China

*

Author to whom correspondence should be addressed.

Risks 2018, 6(2), 39; https://doi.org/10.3390/risks6020039

Submission received: 27 January 2018

/

Revised: 13 April 2018

/

Accepted: 17 April 2018

/

Published: 19 April 2018

(This article belongs to the Special Issue Risks in Financial and Real Estate Markets)

Abstract

:The topic of bank default risk in connection with government bailouts has recently attracted a great deal of attention. In this paper, the question of how a bank’s default risk is affected by a distress acquisition is investigated. Specifically, the government provides a bailout program of distressed loan purchases for a strong bank to acquire a bank in distress. The acquirer bank may likely refuse the acquisition with a bailout when the amount of distressed loan purchases is large or the knock-out value of the acquired bank is high. When the acquirer bank realizes acquisition gains, the default risk in the consolidated bank’s equity return is negatively related to loan purchases, but positively to the knock-out value of the acquired bank. The government bailout, as such, in large part contributes to banking stability.

1. Introduction

During a financial crisis, strategic bailout decisions often need to be taken by a government to resolve distress. Distressed bank acquisition incentivized by a government bailout is one of the most important strategic decisions apparent in the literature as a remedy for financial distress (Berger et al. 1999). For example, Merrill Lynch when in distress was acquired by Bank of America on 15 September 2008, and Bank of America received a government bailout package on 16 January 2009. Citigroup acquired Wachovia banking operations on 29 September 2008, and received a government bailout package on 24 November 2008 (Breitenfellner and Wagner 2010). However, whether distress acquisition is effective at reducing default risk and contributes to banking stability remains an open question (Vallascas and Hagendorff 2011). Motivated by the ongoing arguments in the literature, we assess the extent to which distress acquisition incentivized by a government bailout at taxpayers’ expense and the early closure problem of the acquired target bank affect (i) a strong acquirer bank’s incentive in a distress acquisition; (ii) the consolidated bank’s interest margin, i.e., the spread between the loan rate and the deposit rate, which is often used in the literature as a proxy for the efficiency of liquidity intermediation; and (iii) the default risk in the consolidated bank’s equity returns.

There are several reasons why the issue of bank incentives to take a government bailout is important in the context of distress acquisition. First, a financial bailout plan should encourage broad participation by lowering banks’ incentives to reject government assistance (Hoshi and Kashyap 2010). The reason is that banks may have disincentives to take support because infusions may send an adverse signal, in particular when a distressed bank acquisition is made. Second, a debt overhang problem may increase equity-holder disincentives to receive support, since the gains in the event of a recovery may accrue largely to debt holders, in particular when the protection of the debt holders is focused. Third, as pointed out by Bayazitova and Shivdasani (2011), large banks are less likely to reject government support, and banks with weak asset quality are also less likely. Thus, the size and quality of assets held by a bank are important determinants of its decision to accept or reject government bailouts.

Our analysis differs from existing literature in two ways. First, we construct a contingent claim model along the lines of Mullins and Pyle (1994) for the equity valuation of an acquirer bank, and Episcopos (2008) for the equity valuation of an acquired bank. Their main contribution is to explicitly consider default risk in a contingent claim model to value the equity of a bank. In Mullins and Pyle (1994), default can only occur at the maturity date. The equity value of the acquirer bank with acquisition-status quo ante can be viewed as a standard call (SC) option. The SC is a path-independent approach because its payoff depends on the underlying asset value only at maturity. In Episcopos (2008), default can occur at any time before the maturity date. The equity value of the distressed acquired bank can be viewed as a down-and-out call (DOC) option. The DOC is a path-dependent approach because creditors do not wait for debt to mature, but instead force the acquired bank to bankruptcy before the value of assets depletes. This paper focuses on both the approaches that distinguish the acquired bank from the distressed acquired bank in the acquisition decision.1 We develop a model for consolidation equity valuation based on a DOC option since default has highlighted the role of early closure identification of the acquired bank. Under the circumstances, we emphasise that the government provides, for example, a bailout program of loan purchases in order to incentivize the strong bank to acquire the distressed bank.

Second, both the Mullins and Pyle (1994) and Episcopos (2008) approaches to valuing the bank’s equity are based on a critical assumption that loan markets faced by banks are assumed to be perfectly competitive. This assumption does not reflect the reality well, since loan markets are always highly concentrated where banks strategically set interest rates and face random loan levels. Therefore, we extend their models in order to capture a feature of an imperfectly competitive loan market. In particular, our paper includes acquisition of the distressed target explicitly considering bank spread decisions.

Our results can be summarized as follows. First, the acquirer bank likely opts out of the distress acquisition when the purchases of distressed loans by the government is high. The result is understood, because the credit risk of the distress acquisition incentivized by the government’s support is decreased, hence inducing a decrease in the acquirer bank’s equity return. Second, the acquirer bank may also refuse the acquisition if the acquired bank has a high level of asset variability when the likelihood of meeting the knock-out level is substantial. Third, once the acquisition is taken, the purchase of distressed loans by the government leads to a decrease in the default risk in the consolidated bank’s equity return due to the significant government-sponsored benefits. Fourth, increasing the knock-out value generates an increase in the default risk in the consolidated bank’s equity return due to the increased distress costs. Finally, acquisition as such makes the consolidated bank less prone to risk-taking, thereby contributing to banking stability. Our results highlight the importance that the acquirer bank attaches to the government incentive in the design of a bailout program to resolve the distress by distress acquisition.

One frequent suggestion is for a bank to acquire a low-distressed bank rather than a high-distressed one in order not to increase the consolidated default risk in the future. This paper provides one explanation why this should be expected. An acquirer bank may refuse government assistance when the target bank is deeply in distress. The government, instead, may directly launch a rescue package to the distressed bank for the stabilization of the financial system. In a related work, Vallascas and Hagendorff (2011) analyse the implications of bank consolidation on the default risk of acquirer banks. They find that consolidation generates a significant increase in default risk. Unlike Vallascas and Hagendorff (2011), we study a distress acquisition incentivized by government assistance that allows us to examine a bank’s acquisition decision along with its associated valuation effects. We show that consolidation backed by government loan purchases decreases default risk. We note that there are many aspects of debates over optimal rescue packages for distressed acquisition that we remain silent on. However, this paper does demonstrate the important role played by a government bailout in a distress acquisition in contributing to banking stability.

The paper proceeds as follows. In the next section, we review related literature. In Section 3, the framework and assumptions are presented. The theoretical model is developed in Section 4. Section 5 derives the solution and examines the comparative static results. A numerical analysis follows in Section 6. The final section concludes the paper.

2. Related Literature

Our banking theory of distress acquisition is related to three strands of the literature. The first is the recent literature on bank incentives to participate in a government bailout program. Hoshi and Kashyap (2010) argue that a bank may likely reject a government bailout if the government’s direct capital injection generates an adverse signal that the assisted bank is expected to have high future losses. Wilson (2010) examines the Public Private Investment Plan and shows that only the solvent bank will be willing to participate in the plan by selling distressed assets. Bayazitova and Shivdasani (2011) demonstrate that strong banks rather than weak ones opt out of taking the Capital Purchase Program. While we also examine participation incentives, our focus on a strong acquirer bank’s excepted equity return aspects of distress acquisition incentivized by the government’s purchases of distressed assets takes our analysis in a different direction.

The second strand is bank acquisition on default risk. As regards the risk behind acquisition, several related studies estimate the diversification potential of bank acquisition. These studies report that acquisition lowers the default risk of US banks as a result of geographic diversification (Hughes et al. 1999), and asset portfolio diversification (Emmons et al. 2004). In addition, Hoggarth et al. (2003) argue that with regard to acquisition driven by business motives, a rescue option can be used to resolve a troubled bank problem. Kasman et al. (2010) suggest that the government should promote acquisitions to increase the efficiency of bank operation management. Vallascas and Hagendorff (2011) show that for the least risky banks, acquisitions without being backed by government support generate a significant increase in default risk. We contribute to the literature by analyzing bank consolidation incentivized by government assistance on the default risk of the consolidated bank, in particular through bank spread management.

The third strand of the literature to which our work is directly related is that on conformity, particularly the work of Breitenfellner and Wagner (2010). Other examples are Gorton and Huang (2004); Sahut and Mili (2011); Vallascas and Hagendorff (2011). The insight shared by these papers is that conformity is generated by distinguishing oneself from the type with which one wishes not to be identified. This insight is an important aspect of bank interest margin and default risk management as well, since bank managers and regulators agree with acquisition incentivized by government support at the taxpayer’s expense to avoid being identified as untalented in managing returns and risks. The primary difference between our model and these papers is that we propose a path-dependent, barrier option model to examine the effect of a government bailout on bank interest margins. What distinguishes our work from this literature is our focus on the commingling of the assessment of an acquirer bank with the assessment of an acquisition incentive and, in particular, the emphasis we put on the relationships among government incentivized assistance, early bank closure, and default risk in the context of bank interest margins with strategic distress acquisition.

3. The Framework and Assumptions

In the model, several critical assumptions are made in order to obtain tractable solutions. We shall point out when these assumptions affect the qualitative results derived in the model.

First, we consider a minimalist framework with two dates, 0 and 1, . There are three related banks: a strong acquirer bank, an acquired bank in distress, and a consolidated bank. The strong acquirer bank is incentivized to acquire the distressed bank by a government bailout. This bailout program is specified as one in which the government purchases some of the consolidated bank’s loans subject to non-performance at taxpayer expense. As we discuss further below, the beneficiary can be motivated based on a bailout argument in the spirit of Breitenfellner and Wagner (2010), while the cost can be motivated based on a bank early closure argument in the spirit of Episcopos (2008).

Second, competitive markets are assumed for all financial assets except the loan markets faced by the three banks. Each bank is a price-taker and the interest rate it will have to pay on deposit is market-determined. The interest rate the banks will be repaid from the liquid-asset investments is also market determined. Moreover, financial markets are complete in that any financial claim can be replicated in the marketplace by combination of other financial assets (Crouhy and Galai 1991). According to this assumption, market-determined values for the financial claims on the assets can be derived since the price of any asset is identical to the value of the replicating portfolio.

Third, it is assumed that financial assets are traded continuously; however, bank depositors can withdraw funds only at discrete time intervals. Money deposited is committed for one period. We rule out the case that banks try to stem deposit outflows by raising deposit rates. Our conclusion continues to apply with an endogenously determined deposit rate, so long as depositors’ liquidity demands are somewhat inelastic. This assumption is based on Wong (1997).

Fourth, as mentioned in the introduction section, we construct a contingent claim framework along the lines of Mullins and Pyle (1994) and Episcopos (2008) for the valuation of bank equity. In Mullins and Pyle (1994), default can only occur at maturity date, whereas in Episcopos (2008), default can occur at any time before the maturity date. A relevant distinction for our argument is whether the early bank closure is addressed. In our model, we argue that the acquired bank in distress is likely to exhibit a higher probability of hitting the early closure problem before the expiration date than the strong acquirer bank. Specifically, an equity valuation for the acquired bank is based on Episcopos (2008), while an equity valuation for the acquirer bank is based on Mullins and Pyle (1994).

4. The Model

This section consists of four parts based on the balance-sheet activities shown in Table 1. The first part constructs an equity function for the acquirer bank, explicitly considering the loan rate-setting behavioral mode. The second part models an equity function for the acquired bank. With information about the acquirer and the acquiree, we develop an objective function for the consolidated bank, explicitly considering an incentivized bailout program. The remaining part of this section focuses on a strategic acquisition.

4.1. The Acquirer Bank

Consider a strong acquirer bank and that default can only occur at the maturity date, as the bank in the pre-acquisition status. At , the acquirer bank owns a capital structure as illustrated in the following balance sheet in Table 1:

where is the amount of loans, is the quantity of default-free liquid assets, is the amount of deposits, and is stock of initial capital. Loans mature at . The demand for loans is governed by a downward-sloping demand function where is the loan rate chosen by the acquirer bank. Loans are risky in that they are subject to non-performance. in the bank’s earning-asset portfolio during the period earns the security-market interest rate of . The supply of is perfectly elastic at a constant market interest rate of . The acquirer bank’s shareholders contribute capital on their investment. held by the acquirer bank is regulated by a fixed proportion of the acquirer bank’s deposits, where is the required capital-to-deposits ratio. Equation (1) can be specified as when the capital constraint is binding.2 We focus on this binding case.

Given information about (1), we value the equity of the acquirer bank as a SC option on its risky assets. The reason is that equity holders are residual claimants on the acquirer bank’s assets after all liabilities have been paid. The strike price of the SC is the book value of the acquirer bank’s liabilities. When the value of the acquirer bank’s assets is less than the strike price, the value of equity is zero. The market value of the acquirer bank’s underlying assets specified as follows a geometric Brownian motion (GBM) of the following form: , where is the value of the acquirer bank’s loan repayments from its borrowers, with an instantaneous drift , and an instantaneous volatility . A standard Wiener process is . follows a lognormal distribution, implying that is normally distributed with mean and standard deviation . is the net-obligation payments between the payments to depositors and the repayments from the liquid-asset investment that have maturity at . can be specified as the strike price. The market value of the acquirer bank’s equity will then be priced by:

where

and where is specified as the risk-free discount rate of the net-obligation payments, and represents the cumulative density function of the standard normal distribution.

A related issue is that the acquirer bank defaults when it fails to service its obligations. The default probability is the probability that the acquirer bank’s assets will be less than the book value of its liabilities. Our approach in calculating default risk measures follows Merton’s (1974) model. With the information about (2), the default probability will then be given by:

where

The term in (3) can be explained as the distance to default. Default occurs when the ratio of the value of assets to debt is less than 1. Notice that although the equity value in (2) does not depend on , does. This is because depends on the future value of assets which is given in and . Accordingly, we can use the measure to examine the relation between default risk and equity return.

4.2. The Acquired Bank

Consider an acquired bank in distress, that default can occur at any time before the maturity date, as the bank in the pre-acquisition status. At , the acquired bank has the following balanced sheet as shown in Table 1:

where , , , and is the amount of loans, liquid assets, deposits, and capital, respectively. The capital requirement faced by the acquired bank is also limited to . We again endow the acquired bank with some market power in its loan market, which is governed by where is the loan rate. held by the acquired bank earns the market rate of . Deposits pay the market rate of .

To capture a distressed situation where the acquired bank’s default occurs at any time before the maturity date, we introduce the risk of a premature default to the valuation of the acquired bank’s equity. With the condition of (4), we adopt the barrier option formula of Merton (1973) as a tool to understand the DOC approach to the acquired distressed bank’s equity valuation. In this context, the market value of the acquired bank’s equity can be stated as:3

where

In (5), is the acquired bank’s underlying assets following a GBM of , with an instantaneous drift an instantaneous volatility , and a standard Wiener process . is the net-obligation payments, which is the strike price of the call option. is the barrier on knock-out value of the bank. For tractability, we follow Episcopos (2008) and assume that the default barrier is proportional to the net-obligation payments by a barrier-to-debt ratio .4 is the continuously compounded riskless spread rate of .

The first term on the right-land side of (5) can be interpreted as the acquired bank’s equity value using the SC option view. The second term can be interpreted as the down-and-in call (DIC) value that comes into effect when the value of the underlying asset crosses the barrier from above in the life of the option. The DIC offers protection to bondholders by allowing them to “call in their chips” before asset values deteriorate further. We apply Brockman and Turtle (2003) and argue that firms with high asset variability are likely to exhibit a higher probability of hitting the barrier before the expiration date than firms without such a characteristic. Thus, we assume the conditions of and to demonstrate the distressed state of the acquired bank in the following acquisition analysis.

4.3. The Consolidated Bank

One aim in this paper is to take consolidation into account. Consider a contingent claim model framework for a consolidated bank based on the settings of the acquirer bank and the acquired bank specified as previously. Using (1) and (4), the consolidated bank has the balance sheet as illustrated in Table 1:

where with is the amount of risky loans, and is the amount of risky loans purchased by the government when the bank decides to participate in the assistance program.5 The excepted value of the loan repayments at guaranteed by the government is specified as , which becomes default-free repayments.6 This bailout program can be identified as a credit risk-transfer program that creates an incentive for the acquirer bank to acquire the distressed bank. A simple type of credit swap in the government-guaranteed debt issue programs is a credit risk-transfer program. In the bailout program, take two parties, the consolidated bank and the government. To execute the credit risk transfer, the bank sends the loan payments it may receive from of its risky loans to the government. Simultaneously, the bank receives of bond payments from the government which guarantees the payments. This bailout swap allows the bank to diversify away some of its credit risk and consequently is a cost to the taxpayer. With distress acquisition, credit risk is also present because the amount of is still subject to non-performance.

We also adopt the DOC approach to value the equity value of the consolidated bank. There is a chance that the acquired target bank has the early-closure problem. The market value of the consolidated bank’s underlying assets follows a GBM of the form:

where

and where is the bank’s asset value, with an instantaneous drift , an instantaneous volatility , and a standard Wiener process . By following (7) with the balance-sheet constraint of (6), the market value of the bank’s equity can be stated as:

where

and where is the promised future net obligations on the discount spread rate and due at . includes the payments to depositors, , the repayments from the liquid-asset investments, , and the repayments from the loans purchased by the government. is defined as the compounded spread rate of .

The same pattern as previously applies. The former term on the right-hand side of (8) can be motivated based on the consolidation of banking management with possible distress acquisition incentivized by the government’s loan-purchased program. A potential design of a government-funded asset purchase program presented in our model is limited to a part of the consolidated bank’s risky assets. The latter term can be motivated based on the knock-out value from only the acquired distressed bank, since the acquirer bank is strong. Note that one can attach a number of interpretations to the assistance parameter in (8). For example, controlling the level of by the government becomes crucial to a cost-benefit analysis for the efficiency of the bailout program.

With information about (8), we further illustrate an application of the DOC framework to the problem of default prediction. The valuation of (8) implies a risk-neutral default probability over the interval from that the probability is then given by the Brockman and Turtle (2003) formula for the DOC option:

where

It is interesting that we can also use information about in (5) to obtain the default probability formula which is identical to in (9). This is because the knock-out value of the consolidated bank in (8) is based on only that of the acquired distressed bank, not on that of the consolidated bank. Strictly speaking, Equation (8) represents a “partial” DOC framework. We then argue that for the total default probability, besides , assets include in (3), which is the acquirer bank’s default probability in of (2) without conducting the acquisition. Accordingly, we further define the default probability in the consolidated bank’s equity returns as:

where .

4.4. Incentivized Acquisition

We are now ready to study a decision by a strong acquirer bank to acquire the distressed bank with the incentivized assistance of the loan purchases. Specifically, the decision of the acquirer bank is made based on whether or not the post-acquisition net equity value is expected to be greater than the pre-acquisition one. This decision condition based on the acquirer bank’s equity maximization purposes can be written as:

The term on the left-hand side of condition (11) can be interpreted as the realized market value of equity held by the shareholders of the acquirer bank after the acquisition, while the term on the right-hand side can be interpreted as the realized market value of equity held by those prior to the acquisition. The realized equity value here is defined as the value associated with default probabilities in the equity returns instead of the commonly used expected equity value. The advantage of this approach is the explicit treatment of the ex ante versus ex post default risk in the acquisition decision. Note that the strong acquirer bank may refuse the government’s assistance if the condition of (11) is violated.7

5. Solutions and Results

Here, we are ready to solve the optimal loan rates for the consolidated bank. Partially differentiating (8) with respect to and , the first-order conditions are given by:

where

The equilibrium conditions in (12) aim at determining the optimal loan rates. In the following, we focus on only the case where the optimal choices of and are dichotomized. One reason is that either the acquirer bank or the acquired bank in the pre-acquisition state tends to concentrate their loans geographically or in particular industries. This assumption may offer a potential diversification gain for the consolidated bank to diversify its credit risks across segmented or geographical borrowers.8 We expect that results to be derived from our model do not extend to the case where the consolidated bank makes simultaneous decisions on both the loan rates. Under the dichotomous setting, we require that only the second-order conditions, , , , be satisfied, and the optimal loan rates and can be obtained based on (12), respectively.

In (12), the first term on the right-hand side can be identified as the marginal equity using the SC option view, while the second term can be identified as the marginal knock-out value using the DIC option view. The optimal is obtained where the first term of the marginal equity value of equals zero for the equity maximization when remains fixed. This is understood because the second term on the determination state of (12) vanishes. The optimal is obtained where the first term of the marginal equity value of is equal to the second term of the marginal knock-out value for the equity maximization when remains fixed. We further substitute either the optimal loan rate to obtain the default risk in (10) staying on either optimization, respectively.

One optimal bank interest margin in our model can be specified as the spread between the optimal loan rate and the fixed deposit rate when remains constant. Since is not a choice variable of the consolidated bank, examining the impact of parameters on the optimal bank interest margin is tantamount to examining that on the optimal loan rate . In the following, we consider the impacts on the default risk in the consolidated bank’s equity return evaluated at the optimal from changes in the amount of loan purchases in the assistance program and the barrier-to-debt ratio.9 Differentiation of (10) with respect to and when remains constant yields, respectively:

where

The first term on the right-hand side of (13) can be explained as the direct effect, while the second term can be explained as the indirect effect. The direct effect captures the change in due to an increase in , holding the optimal constant. This direct effect vanishes because the default risk in the consolidated bank’s equity return ( in (10)) is independent of in our model. The indirect effect arises because an increase in changes in the default risk by in every possible state. The total effect in (13) is then equal to the indirect effect. Again, the first term on the right-hand side of (14) can be interpreted as the direct effect of on when the optimal bank interest margin remained fixed, while the second term can be interpreted as the indirect effect through adjustments of the optimal bank interest margin. Based on our model, the direct effect is from only the impact on from changes in . This explains the acquirer bank as a strong one before acquisition by the term in (14). The comparative static results of (13) and (14) are valid if and only if the condition of (11) holds. In general, the added complexity of path dependent/independent options does not always lead to clear-cut results, but we can certainly speak of reasonable parameter levels corresponding roughly to an acquisition position in our analysis. In the following section, we will use numerical exercises to demonstrate the results of (11), (13), and (14).

6. Numerical Exercises

In the following section, we first present the baselines of the parameter values and the endogenous variables. For each result, we discuss the numerical procedure used to obtain it. Then, we show the major results and provide the intuition for each main finding.

6.1. Baselines

First of all, we assume that the parameter levels, unless otherwise indicated, are , , , , , , , , and . Let demand for loan bundle , change from {(4.50, 200), (4.00, 180)} to {(6.00, 182), (5.50, 168)} due to the condition of and , respectively. The assumption of these bundles indicates that the acquirer bank faces a more elastic loan demand and has a larger margin than the acquired bank.10 This indication, motivated based on an acquisition argument in the spirit of Beccalli and Frantz (2013), demonstrates a possible scenario situation that the acquirer bank is strong and the acquired bank is weak in our analysis.

The numerical parameter levels assumed above are explained as follows: (i) the conditions of and demonstrate fund reserves as liquidity and substitution in the earning-asset portfolio (Kashyap et al. 2002); (ii) the bank’s interest margins captured by the conditions of and indicate a proxy for the efficiency for financial intermediation; (iii) the condition of is an alternative to explain management quality in the pre-acquisition that the strong bank is assumed to use less capital for bank management more efficient than the weak bank uses more capital (Maudos and de Guevara 2004). In addition, the assumed levels of and indicate regulation that the capital to asset ratios in the three cases, 9.00%, 11.11%, and (18 + 20)/(200 + 180) = 10.00%, meet the Basel requirements in our analysis (VanHoose 2007); (iv) the condition of implies that the strong acquirer bank has a lower asset variability than the acquired weak bank. The condition of implies diversification gains realized in the distress acquisition (Elsas 2004). In addition, two possible scenarios related to the acquisition decisions discussed in this paper are that (i) let increase from 0.10 to 0.80 at a given level of ; and (ii) let increase from 0.600 to 0.950 at a given level of .

6.2. Effect of the Government’s Purchases of Distressed Loans on Default Risk

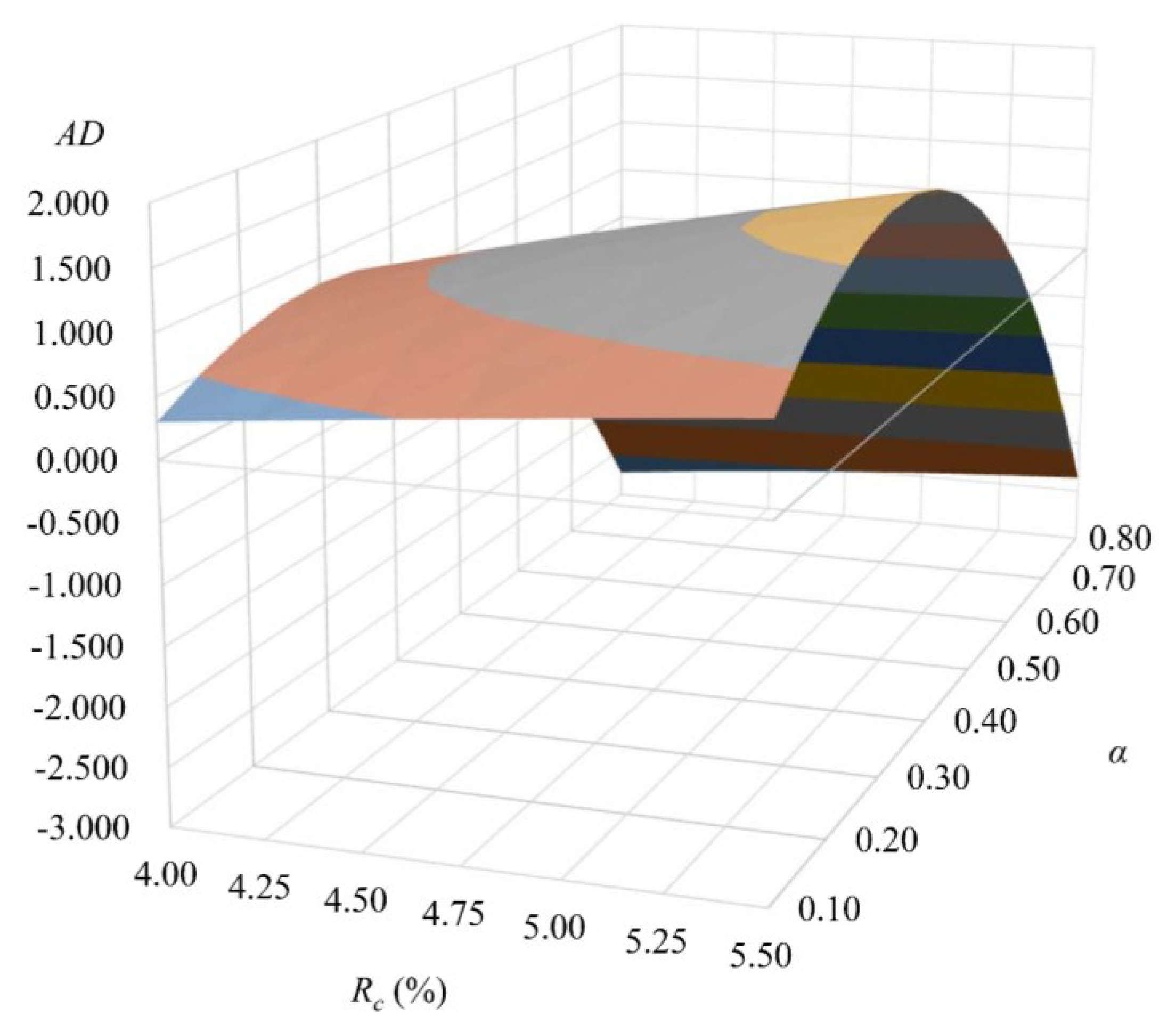

Before proceeding with the analysis of (13), we first confirm the acquisition decision by the acquirer bank based on (11) in our model. The acquisition decision surface presented in Figure 1 illustrates that the government’s assistance program is an appropriate program to incentivize the acquirer bank to acquire the distressed bank when the purchase amount is low. The illustration is understood because the loan-repayment value of the consolidated bank is less likely to come into effect as the loan purchase amount increases. The purchased loans by the government become risk-free at an opportunity cost of a reduced consolidation gain due to the efficient liquidity management of the acquirer bank. A large amount loan purchased by the government is not guaranteed to create a high incentive for the strong bank to acquire the distressed bank. This is because the acquisition decision depends on future gain/loss expectation, emphasizing that acquisition brings about benefits/costs. In related work, Hoshi and Kashyap (2010) study the adverse signal effects of government interventions which lead to future losses. Based on an implicit future-loss argument, we argue that the assistance program of the large loan purchase amount may discourage a strong bank to acquire a distressed bank because this program creates a low equity return for the acquirer bank as a result of reducing risk by loan portfolio diversification.

Next, two related questions are to consider the impact of an increase in the amount of loan purchase on the consolidated bank’s interest margin decision, and further on its default risk. Based on the observed results from Figure 1, we initially limit the ratio to 0.50 from 0.10 for the following numerical exercises. The demand for the loan is limited to a case of (4.00, 180) due to the non-simultaneous assumption for our analysis. The findings are summarized in Table 2.

Table 2 presents the computed results of , and explained as follows. First, as the amount of the government’s purchases of distressed loans increases, the interest margin of the consolidated bank is increased. As the amount of the distressed loans purchased increases, the bank now provides a return to a less-risk base. One way the bank may attempt to augment its total returns is by shifting its investments to liquid assets and away from its loans. If loan demand is relatively rate-elastic, a lower loan amount is possible at an increased margin. Our analysis confirms that the consolidated bank reduces loan volume (and thus credit risk) and increases interest margin as a reaction to an increase in the distressed loans purchased by the government. More government assistance induces the bank to increase loan rate, which mitigates credit risk of the bank’s lending in the consolidation process. Our result is implicitly supported by the empirical finding of Williams (2007): a decrease in the credit risk (due to an increase in the loan purchases by the government in our model) increases the bank interest margin. One policy application of our result is also consistent with the finding of Bebchuk (2008): government asset purchases are suitable to cope with the financial crisis since the bank becomes less risk prone.

Next, we show that an increase in the amount of the distressed loans purchased by the government decreases the default risk in the consolidated bank’s equity return. Once the bank has an incentive to participate in the program of government assistance to acquire a distressed bank, our result suggest that loan purchases occurs in a manner consistent with lower default risk, thereby lowering financial distress costs. Note that reducing the default risk in the consolidated bank does not result from the direct effect of the assistance program, but from the indirect effect of the program through efficient margin management. Accordingly, we argue that even with a government as the lender of last resort, there is an incentive for the consolidated bank to pursue sophisticated risk management. In particular, we suggest that the government should promote distress acquisitions to increase the efficiency of bank management. Our argument is supported by Cebenoyan and Strahan (2004) that loan purchases by the government help manage bank default risk.

6.3. Effect of the Acquired Bank’s Knock-Out Value on Default Risk

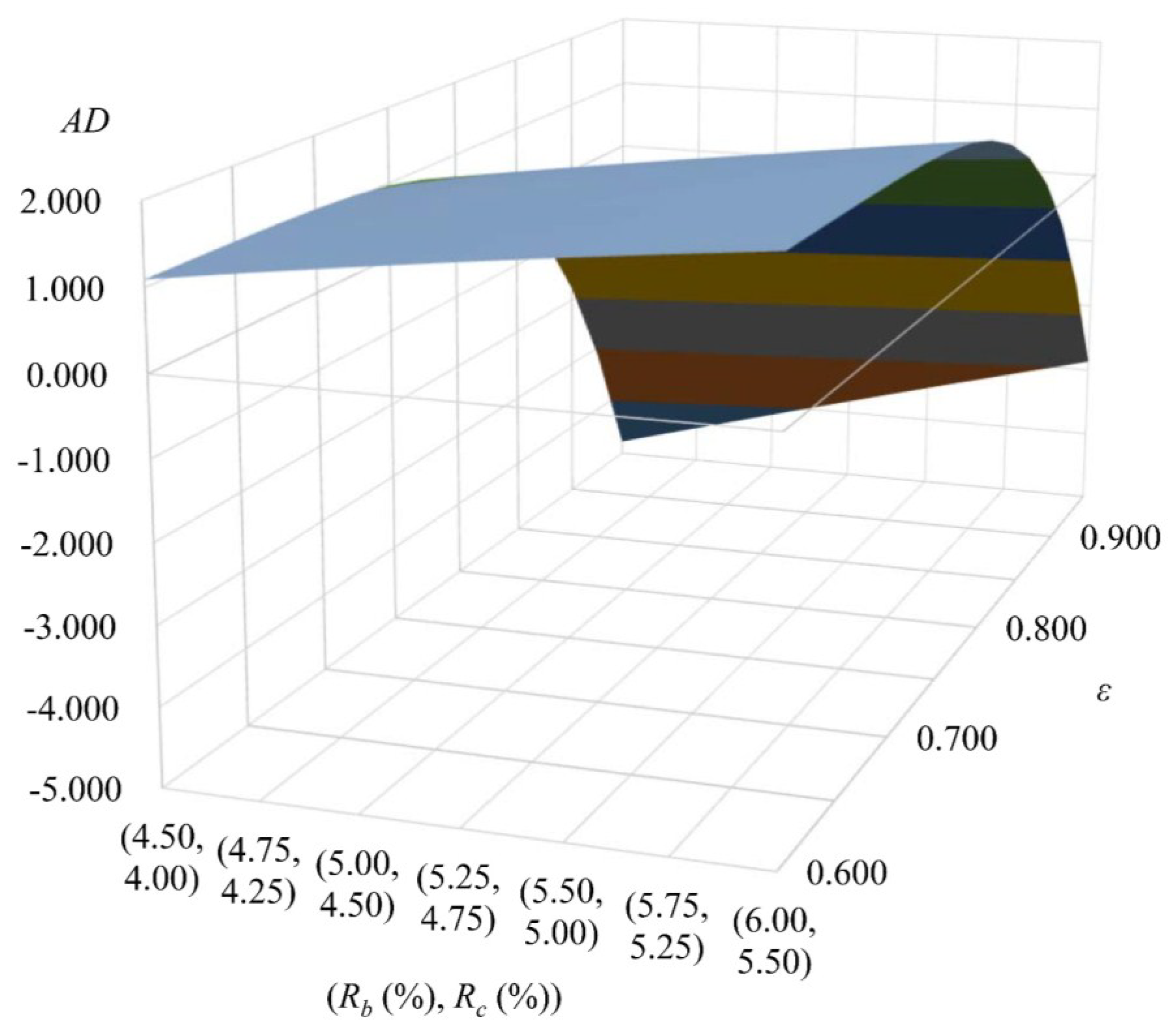

A related issue is to consider the acquisition decision, focusing on the various levels of the acquired target bank’s knock-out value. The finding is shown in Figure 2.

Results observed from Figure 2 demonstrate that the condition of (11) is valid when the barrier ratio is low. An obvious result is that the willingness of acquisition for the strong acquirer bank becomes conservative when the knock-out value of the acquired bank is relatively high. Hence, the acquirer bank perceives generating a relatively low level of default-risk target as an incentive for distress acquisition. This is because the default risk in the consolidated bank’s equity returns depends on the knock-out value of the acquired distressed bank at a given level of government assistance. As the knock-out value increases, the equity return realized is decreased and the protection of debt holders is increased (Episcopos 2008). Therefore, qualifying the level of the barrier on bank contingent claims is an important incentive for bank acquisition.

We next consider the impact of an increase in the barrier level on the consolidated bank’s default risk when the acquirer bank has an incentive to participate in the assistance program. For simplicity, the demand for a loan is further limited to the case of (4.00, 180) for our analysis. The condition of (11) is invalid at the level of where the results are presented in Figure 2 with various levels of . The findings are summarized in Table 3.

The total effect presented in Table 3 indicates that an increase in the barrier level results in increasing the default risk in the consolidated bank’s equity returns. The intuition is very straightforward. As a barrier increases, the default risk from the SC is very insignificant and that from the DIC call is very significant. It is unambiguously positive because an increase in the barrier level of the acquired bank makes it more costly to conduct an acquisition. Vallascas and Hagendorff (2011) argue that consolidation generates an increase in default risk. The extension of their argument obtained from our result suggests that consolidation generates a much more significant increase in default risk when the acquired bank is at the high level of the barrier. This is because raising the barrier induces a transfer of wealth from shareholders to the insurance authority, implying better protection of the insurance fund resulting in increasing the default risk in the bank’s equity return.

7. Conclusions

The paper develops a contingent claim model for bank distress resolution through acquisition. We show that the acquirer bank incentivized by the government’s purchases of distressed loans under a certain level is likely to proceed with the distress acquisition. Under the circumstances, it is shown that an increase in the amount of loan purchase assistance from the government decreases the default risk in the consolidated bank’s equity return. Loan purchase assistance, as such, makes the bank less prone to risk-taking, thereby contributing to the stability of the banking system. Equally important, we demonstrate that the strong bank is likely to proceed with the distress acquisition with government assistance when the distressed target bank generates a low knock-out value. Furthermore, raising the barrier, implying better protection of the insurance fund, as such makes the bank more prone to risk-taking, thereby adversely affecting banking stability.

The theoretical model presented here is fairly general. An immediate outgrowth of the model is to introduce so-called standard and cumulative Parisian barrier options, appealing interpretations in terms of bank liquidation related to the early closure problem. It is not expected in that case that, more realistically, early bank closure and bank liquidation are recognized as different events. Such concerns are beyond the focus of this paper and so are not addressed here. What this paper does demonstrate, however, is the important role played by distress acquisition with government assistance in affecting banking stability.

Author Contributions

Jyh-Jiuan Lin worked out concepts and assumptions. Chuen-Ping Chang worked out methods. Shi Chen conducted of the research. Jyh-Jiuan Lin and Chuen-Ping Chang wrote the paper.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Bayazitova, Dinara, and Anil Shivdasani. 2011. Assessing TARP. Review of Financial Studies 25: 377–407. [Google Scholar] [CrossRef]

- Bebchuk, Lucian Arye. 2008. A Plan for Addressing the Financial Crisis. Economics and Business Discussion Paper Series, Paper 620. Cambridge: Harvard Law School, Available online: http://lsr.nellco.org/harvard_olin/620 (accessed on 20 January 2018).

- Beccalli, Elena, and Pascal Frantz. 2013. The determinants of mergers and acquisitions in banking. Journal of Financial Services Research 43: 265–91. [Google Scholar] [CrossRef]

- Berger, Allen N., Rebecca S. Demsetz, and Philip E. Strahan. 1999. The consolidation of the financial services industry: Causes, consequences, and implications for the future. Journal of Banking & Finance 23: 135–94. [Google Scholar] [CrossRef]

- Breitenfellner, Bastian, and Niklas Wagner. 2010. Government intervention in response to the subprime financial crisis: The good into the pot, the bad into the crop. International Review of Financial Analysis 19: 289–97. [Google Scholar] [CrossRef]

- Brockman, Paul, and Harry J. Turtle. 2003. A barrier option framework for corporate security valuation. Journal of Financial Economics 67: 511–29. [Google Scholar] [CrossRef]

- Cebenoyan, A. Sinan, and Philip E. Strahan. 2004. Risk management, capital structure and lending at banks. Journal of Banking & Finance 28: 19–43. [Google Scholar] [CrossRef]

- Crouhy, Michel, and Dan Galai. 1991. A contingent claim analysis of a regulated depository institution. Journal of Banking & Finance 15: 73–90. [Google Scholar] [CrossRef]

- Elsas, Ralf. 2004. Preemptive Distress Resolution through Bank Mergers. Working Paper. Frankfurt: Goethe University Frankfurt, Available online: http://publikationen.ub.uni-frankfurt.de/opus4/frontdoor/deliver/index/docId/3705/file/454.pdf (accessed on 20 January 2018).

- Emmons, William R., R. Alton Gilbert, and Timothy J. Yeager. 2004. Reducing the risk at community banks: Is it size or geographic diversification that matters? Journal of Financial Services Research 25: 259–81. [Google Scholar] [CrossRef]

- Episcopos, Athanasios. 2008. Bank capital regulation in a barrier option framework. Journal of Banking & Finance 32: 1677–86. [Google Scholar] [CrossRef]

- Gorton, Gary, and Lixin Huang. 2004. Liquidity, efficiency, and bank bailouts. American Economic Review 94: 455–83. [Google Scholar] [CrossRef]

- Hoggarth, Glenn, Jack Reidhill, and Peter Sinclair. 2003. Resolution of banking crises: A review. In Financial Stability Review. London: Bank of England, vol. 15, pp. 109–23. [Google Scholar]

- Hoshi, Takeo, and Anil. K. Kashyap. 2010. Will the U.S. bank recapitalization succeed? Eight lessons from Japan. Journal of Financial Economics 97: 398–417. [Google Scholar] [CrossRef]

- Hughes, Joseph P., William W. Lang, Loretta J. Mester, and Choon-Geol Moon. 1999. The dollars and sense of bank consolidation. Journal of Banking & Finance 23: 291–324. [Google Scholar] [CrossRef]

- Kashyap, Anil K., Raghuram G. Rajan, and Jeremy C. Stein. 2002. Banks as liquidity providers: An explanation for the coexistence of lending and deposit-taking. Journal of Finance 57: 33–73. [Google Scholar] [CrossRef]

- Kasman, Adnan, Gokce Tunc, Gulin Vardar, and Berna Okan. 2010. Consolidation and commercial bank net interest margins: Evidence from the old and new European Union members and candidate countries. Economic Modelling 27: 648–55. [Google Scholar] [CrossRef]

- Maudos, Joaquín, and Juan Fernández de Guevara. 2004. Factors explaining the interest margin in the banking sectors of the European Union. Journal of Banking & Finance 28: 2259–81. [Google Scholar] [CrossRef] [Green Version]

- Merton, Robert C. 1973. Theory of rational option pricing. Bell Journal of Economics and Management Science 4: 141–83. [Google Scholar] [CrossRef]

- Merton, Robert C. 1974. On the pricing of corporate debt: The risk structure of interest rates. Journal of Finance 29: 449–70. [Google Scholar] [CrossRef]

- Mullins, Helena M., and David H. Pyle. 1994. Liquidation costs and risk-based bank capital. Journal of Banking & Finance 18: 113–38. [Google Scholar] [CrossRef]

- Neal, Robert S. 1996. Credit derivatives: New financial instruments for controlling credit risk. Economic Review, Federal Reserve Bank of Kansas City 81: 15–27. [Google Scholar]

- Sahut, Jean-Michel, and Mehdi Mili. 2011. Banking distress in MENA countries and the role of mergers as a strategic policy to resolve distress. Economic Modelling 28: 138–46. [Google Scholar] [CrossRef]

- Vallascas, Francesco, and Jens Hagendorff. 2011. The impact of European bank mergers on bidder default risk. Journal of Banking & Finance 35: 902–15. [Google Scholar] [CrossRef]

- VanHoose, David. 2007. Theories of bank behavior under capital regulation. Journal of Banking & Finance 31: 3680–97. [Google Scholar] [CrossRef]

- Williams, Barry. 2007. Factors determining net interest margins in Australia: Domestic and foreign banks. Financial Markets, Institutions & Instruments 16: 145–65. [Google Scholar] [CrossRef]

- Wilson, Linus. 2010. The put problem with buying toxic assets. Applied Financial Economics 20: 31–35. [Google Scholar] [CrossRef]

- Wong, Kit Pong. 1997. On the determinants of bank interest margins under credit and interest rate risks. Journal of Banking & Finance 21: 251–71. [Google Scholar] [CrossRef]

| 1 | Alternatively, Beccalli and Frantz (2013) point out that a higher likelihood of becoming an acquirer exists for larger banks with a history of high growth, greater cost X-efficiency, and low capitalization. In contrast, banks are more likely to be targets if they have lower free cash flows, are less efficient, are illiquid, and are under-capitalized. |

| 2 | This capital constraint will be binding as long as is sufficiently higher than (Wong 1997). |

| 3 | |

| 4 | |

| 5 | As pointed out by Breitenfellner and Wagner (2010), the possible government supports generally include government guaranteed debt-issuance programs, direct equity injections, and purchases of distressed assets by the government. The design of a government assistance program largely depends on its targets, such as financial stabilization, taxpayer protection, or separation between good and bad management performance. This paper focuses on purchases of distressed assets by the government as an acquisition incentive. We argue that an alternative assistance program used as an incentive for acquisition may result in different outcomes. |

| 6 | Funds will be collected in fines, penalties, and forfeitures from the consolidated bank if violations related to the Bank Secrecy Act and U.S. sanctions programs require this. These requirements are significant tools that aid the financial authorities in detecting, disruption and inhibiting corruption. We remain silent on the issue in our model. |

| 7 | Equation (11) is an alternative decision used in our model for the strong acquirer bank incentivized to participate in the government’s assistance program. Hoshi and Kashyap (2010) argue that a bank may refuse government assistance if a bailout program generates an adverse signal that the bank is expected to have high future losses. We are silent on this issue. |

| 8 | Neal (1996) argues that banks are exposed to the risk that borrowers will default on their loans and the credit risk faced by banks is relatively high. This is understood because banks tend to concentrate their loans geographically or in particular industries, which limits their ability to diversify credit risks across borrowers. |

| 9 | Nevertheless, our results generally apply to other cases of as well. |

| 10 | The linear slope of and are and . The margins at and , for example, are and , respectively. |

Figure 1.

Example of acquisition decision surface at various levels of . Parameter values: (4.50, 200), and . rearranged from (11).

Figure 1.

Example of acquisition decision surface at various levels of . Parameter values: (4.50, 200), and . rearranged from (11).

Figure 2.

Example of acquisition decision surface at various level of . Parameter values: , and . rearranged from (11).

Figure 2.

Example of acquisition decision surface at various level of . Parameter values: , and . rearranged from (11).

{kind=link}

{kind=link}

Table 1.

Three simplified balance sheets at .

| Asset | Liability and Equity | ||

|---|---|---|---|

| Acquirer bank: | |||

| Loan | Deposit | 1 | |

| Liquid asset | Equity | ||

| Acquired bank: | |||

| Loan | Deposit | ||

| Liquid asset | Equity | ||

| Consolidated bank: | |||

| Loan | Deposit | ||

| Loan purchased by | Equity | ||

| government | |||

| Liquid asset |

1 is the required capital-to-deposits ratio, .

Table 2.

Impacts on bank interest margin and default risk from changes in 1.

| (4.50, 200) | (4.75, 197) | (5.00, 194) | (5.25, 191) | (5.50, 188) | (5.75, 185) | (6.00, 182) | |

|---|---|---|---|---|---|---|---|

| 0.10~0.15 | - | 2.1448 | 2.0753 | 1.9664 | 1.8867 | 1.8212 | - |

| 0.15~0.20 | - | 1.7013 | 1.5987 | 1.5641 | 1.4625 | 1.4367 | - |

| 0.20~0.25 | - | 1.2744 | 1.2182 | 1.1768 | 1.1012 | 1.0663 | - |

| 0.25~0.30 | - | 0.9294 | 0.8779 | 0.8208 | 0.7816 | 0.7356 | - |

| 0.30~0.35 | - | 0.5989 | 0.5618 | 0.5251 | 0.4972 | 0.4611 | - |

| 0.35~0.40 | - | 0.3187 | 0.2826 | 0.2623 | 0.2337 | 0.2120 | - |

| 0.10~0.15 | - | −0.0916 | −0.0803 | −0.0684 | −0.0592 | −0.0512 | - |

| 0.15~0.20 | - | −0.0726 | −0.0619 | −0.0544 | −0.0459 | −0.0404 | - |

| 0.20~0.25 | - | −0.0544 | −0.0471 | −0.0410 | −0.0346 | −0.0300 | - |

| 0.25~0.30 | - | −0.0397 | −0.0340 | −0.0286 | −0.0245 | −0.0207 | - |

| 0.30~0.35 | - | −0.0256 | −0.0217 | −0.0183 | −0.0156 | −0.0130 | - |

| 0.35~0.40 | - | −0.0136 | −0.0109 | −0.0109 | −0.0073 | −0.0060 | - |

1 Parameter values, unless stated otherwise: , , and (4.00, 180). Note that the total effect equals the indirect effect since the direct effect vanishes according to (13).

Table 3.

Impact on default risk from changes in acquired knock-out value. 1

| (4.50, 200) | (4.75, 197) | (5.00, 194) | (5.25, 191) | (5.50, 188) | (5.75, 185) | (6.00, 182) | |

|---|---|---|---|---|---|---|---|

| 0.600~0.625 | - | 0.0036 | 0.0036 | 0.0036 | 0.0036 | 0.0036 | - |

| 0.625~0.650 | - | 0.0101 | 0.0101 | 0.0101 | 0.0101 | 0.0101 | - |

| 0.650~0.675 | - | 0.0254 | 0.0255 | 0.0254 | 0.0255 | 0.0254 | - |

| 0.675~0.700 | - | 0.0585 | 0.0584 | 0.0584 | 0.0584 | 0.0584 | - |

| 0.700~0.725 | - | 0.1228 | 0.1229 | 0.1229 | 0.1228 | 0.1229 | - |

| 0.725~0.750 | - | 0.2389 | 0.2388 | 0.2389 | 0.2389 | 0.2389 | - |

| 0.750~0.775 | - | 0.4322 | 0.4325 | 0.4320 | 0.4324 | 0.4320 | - |

| 0.775~0.800 | - | 0.7322 | 0.7323 | 0.7324 | 0.7324 | 0.7326 | - |

1 Parameter values, unless stated otherwise: , , and (4.00, 180).

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Lin, J.-J.; Chang, C.-P.; Chen, S. How Does Distress Acquisition Incentivized by Government Purchases of Distressed Loans Affect Bank Default Risk? Risks 2018, 6, 39. https://doi.org/10.3390/risks6020039

AMA Style

Lin J-J, Chang C-P, Chen S. How Does Distress Acquisition Incentivized by Government Purchases of Distressed Loans Affect Bank Default Risk? Risks. 2018; 6(2):39. https://doi.org/10.3390/risks6020039

Chicago/Turabian StyleLin, Jyh-Jiuan, Chuen-Ping Chang, and Shi Chen. 2018. "How Does Distress Acquisition Incentivized by Government Purchases of Distressed Loans Affect Bank Default Risk?" Risks 6, no. 2: 39. https://doi.org/10.3390/risks6020039

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.