A Spectral Model of Turnover Reduction

1

Quantigic® Solutions LLC, 1127 High Ridge Road #135, Stamford, CT 06905, USA

2

Business School & School of Physics, Free University of Tbilisi, 240, David Agmashenebeli Alley, Tbilisi 0159, Georgia

Econometrics 2015, 3(3), 577-589; https://doi.org/10.3390/econometrics3030577

Submission received: 27 March 2015

/

Revised: 26 June 2015

/

Accepted: 24 July 2015

/

Published: 29 July 2015

{kind=link}

Abstract

:We give a simple explicit formula for turnover reduction when a large number of alphas are traded on the same execution platform and trades are crossed internally. We model turnover reduction via alpha correlations. Then, for a large number of alphas, turnover reduction is related to the largest eigenvalue and the corresponding eigenvector of the alpha correlation matrix.

Keywords:

hedge fund; alpha stream; crossing trades; transaction costs; portfolio turnover; correlation structure; large N limitJEL classifications:

G001. Introduction and Summary

With technological advances, hedge funds and similar investment vehicles can simultaneously trade multiple alpha streams.1 One immediate question that arises is how to allocate capital to these alphas, or, mathematically speaking, how to determine weights with which the alphas should be combined. This is an optimization problem, whose solution depends on the precise optimization criterion as well other factors, such as if and how transaction costs are included and modeled.

The second issue is related to crossing trades between alphas. If, say, within a given hedge fund, Strategy A wants to buy $1M of MSFT while Strategy B wants to sell $1M of MSFT, it makes sense to cross this trade internally—if the execution platform allows this, that is—as opposed to going to the market as internal crossing amounts to substantial savings in transaction costs.2 When internal crossing is employed, portfolio turnover is reduced, so using even the simplest model for transaction costs in portfolio optimization requires accounting for turnover reduction.

As more and more alpha streams are combined, one expects that on average crossing should increase, and therefore the percentage of the dollar turnover with respect to the total dollar investment—which percentage we refer to simply as “turnover”—is expected to decrease. In [1] it was argued that turnover indeed decreases and converges to a non-vanishing limit. Generally, it is no easy feat to precisely describe internal crossing and turnover reduction. In a portfolio consisting of a large number of underlying tradable instruments (e.g., stocks), precise details of internal crossing depend on the detailed portfolio position and trade data. The question then is if one can model expected turnover reduction—on average, that is—with some reasonable assumptions.

One observation is that the more correlated the trades are, the more correlated the alphas are, and the more correlated the trades are, the lower the internal crossing is expected to be. Therefore, while turnover reduction is not necessarily a simple (e.g., linear) function of alpha correlations, it is clear that it is somehow related to them, so one can try to model turnover reduction based on alpha correlations, which are much more tractable than the position and trade data. The key observation in [1] is that, when the number N of alphas is large—the “Large N Limit”—the turnover reduction is indeed expected to simplify. In [1] a simple model of turnover reduction was discussed, where one assumes a uniform pair-wise correlation ρ between different alphas. Then, when the number of alphas is large, the portfolio turnover has a non-vanishing limit, which is linearly proportional to ρ.

In this note we propose a model of turnover reduction for a general alpha correlation matrix. We argue that in the large N limit we can model turnover reduction using a spectral decomposition of the correlation matrix—hence the “Spectral Model”—using its eigenvalues and eigenvectors. In this limit we have a non-trivial formula for turnover reduction, which is a generalization of [1]. The complementary factor-model based approach of [23] confirms our result here that turnover goes to a finite limit when N is large.

To summarize, in this note we give an explicit spectral model of turnover reduction for a general alpha correlation matrix in the limit where the number of alphas is large. In this regime, this model can be used in estimating transaction costs, and in the problem of portfolio optimization with costs. The latter application of our model was implemented in [24,25].

The remainder of this paper is organized as follows. Definitions are in Section 2. Section 3 deals with positive-definiteness of the covariance (or correlation) matrix. Section 4 discusses our spectral model of turnover reduction and caveats. Our main result is given by Equations (31), (34), (37) and (44). We briefly conclude in Section 5.

2. Definitions

We have N alphas , . Each alpha is actually a time series , , where is the most recent time. Below refers to .

Let be the sample covariance matrix of the N time series . Let be the corresponding correlation matrix, i.e.,

where .

To begin with, let us ignore trading costs. Alphas are combined with some3 weights . The portfolio Profit and Loss (P & L) is given by

where I is the investment level (long plus short).

When linear trading costs are included, P & L is given by

where L includes all fixed trading costs (SEC fees, exchange fees, broker-dealer fees, etc.) and linear slippage. The linear cost assumes no impact, i.e., trading does not affect the stock prices. Also, is the dollar amount traded, and T is the turnover. Let be the turnovers corresponding to individual alphas . If we ignore turnover reduction resulting from combining alphas, then

However, turnover reduction can be substantial and needs to be taken into account. To do this, we need to model turnover when N alphas are combined. The basic idea behind such modeling is discussed in [1], including the assumption (and its limitations) that internal crossing can be parameterized by correlations. Here, without repeating the arguments of [1], we will discuss a model of turnover reduction based solely on the correlation matrix . As in [1], in this note our calculations are carried out in the framework where each alpha is traded in its own separate aggregation unit, and matching trades are crossed between separate aggregation units.

3. “Fixing” Covariance Matrix

Generally, the covariance matrix can have the following undesirable properties. First, it can be (nearly) degenerate. Second, it may not be positive (semi-)definite (see footnote 5).

Let be N right eigenvectors of corresponding to its eigenvalues , :

with no summation over a. Let U be the matrix of eigenvectors , i.e., the ath column of U is the vector :

Let Λ be the diagonal matrix of the eigenvalues :

with no summation over j. Then

Note that, because C is symmetric, U can be chosen to be orthonormal: .

Let

Then the volatility R is given by

So, if is not positive semi-definite, i.e., if any of its eigenvalues is negative, then the volatility R is ill-defined. Also, if is (nearly) degenerate, i.e., if any of its eigenvalues is zero (or small), then the corresponding linear combination of alphas given by

has zero (or small) contribution to the volatility R, thereby introducing an instability into the system.

Near degeneracy is caused by alphas that are almost 100% correlated or anti-correlated and can be cured by simply removing such “redundant” alphas:4 for each kept , each () is removed so long as , where is the upper bound on the modulus of the allowed correlations (e.g., ). In the subsequent sections we will assume that .

However, in practice, near degeneracy is usually caused by the fact that . In fact, when , only M eigenvalues of are non-zero, while the remainder have “small” values, which can be positive or negative. These small values are zeros distorted by computational rounding.5 In such cases, the solution is not to remove any alphas (as they are not necessarily “redundant”), but to deform the covariance matrix so it is positive-definite.

A Simple Method

If one is interested in solving just the positive-definiteness problem, there are various ways of doing this. A simple method that does not require removing any alphas is as follows [26]. Suppose some eigenvalues are negative or zero. Let

where one chooses . Next, let

Finally, let

Note that is positive definite, and we have

I.e., this way we obtain a new positive-definite covariance matrix while preserving the diagonal elements of . Note that, instead of applying this method to the covariance matrix , one may choose to apply it directly to the correlation matrix , as this method properly preserves the unit diagonal elements of .

4. Spectral Model

The first observation is that, as we scale , we must have , where . Next, let be the eigenvectors of corresponding to the eigenvalues6 , :

Let be the matrix of eigenvectors , i.e., the pth column of is the vector :

can be chosen to be orthonormal: , which fixes the normalization of . Note that form an orthonormal basis of N-vectors:

Let (so are the principal components of ). Let

This is the basis in which is diagonalized:

In this basis, the only relevant building blocks constructed solely from and are and , together with scalar invariants of . Therefore, we have the following spectral model for the turnover:

where κ is a constant, which must be constructed from a scalar invariant of . The only suitable scalar invariant is the trace.7 Then T is given by

The power of and the overall coefficient are fixed as follows. Let all off-diagonal elements of be identical: (). Also, let all be identical. Then, recalling that is the largest eigenvalue, we have

which reproduces Equation (19) in [1].

The spectral model (25) simplifies in the large N limit. First, we fix the basis of alphas as follows. Under the reflections (and, consequently, ), where , we have , , while are invariant. Therefore, we can always choose the basis such that all . In what follows we always work in this basis. In the large N limit, unless have a highly skewed distribution, the contributions in (25) are suppressed8 as . Therefore, in the large N limit the following simplified model is a good approximation:9

where is the largest eigenvalue of , and is the corresponding eigenvector (in the basis where all ) normalized such that

Thus, assuming equal weights with identical , we have

where

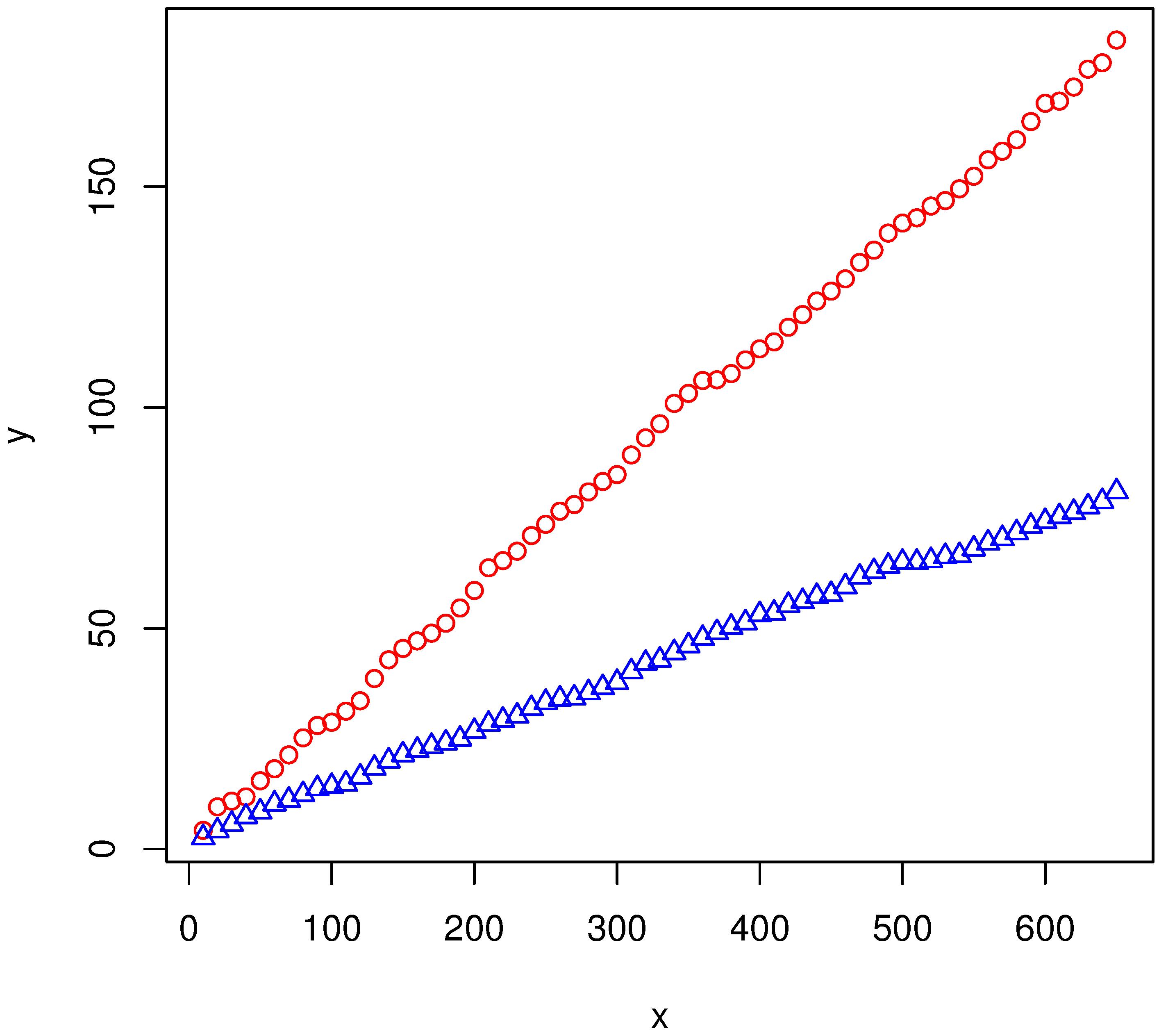

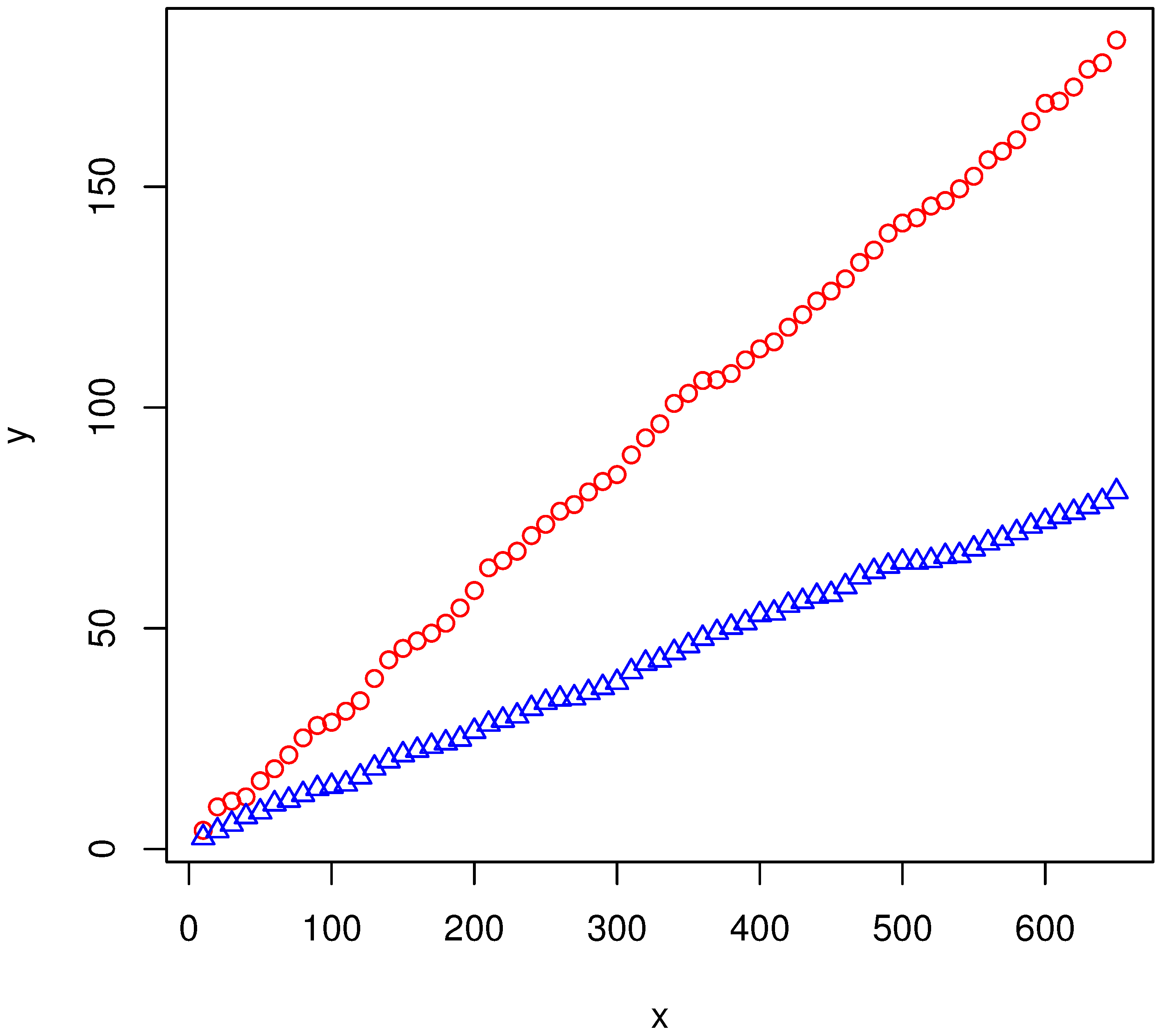

For a generic correlation matrix this quantity is constant with N with high t-statistic. For an illustrative10 example see Figure 1. The regression of y over x (without intercept) in Figure 1 has F-statistic over (upper line with circles) and (lower line with triangles). This confirms what was argued in [1], that the turnover reduction based on the correlation matrix goes to a non-vanishing limit when N is large, i.e., does not vanish in this limit.

Figure 1.

x-axis: N; y-axis: . This graph is based on the same Morningstar data for 1990–2014 for 657 hedge fund returns (HF) as Figure 1 in [1]. The upper line (circles) corresponds to the correlation matrix of the raw HF. The lower line (triangles) correspond to the correlation matrix of the residuals (plus the intercepts, which have no effect) of HF adjusted for RF (whose effect is small) and regressed over Mkt-RF and Fama-French risk factors SMB, HML, WML. Each correlation matrix is taken in the basis where its eigenvector corresponding to the largest eigenvalue has all nonnegative elements.

Figure 1.

x-axis: N; y-axis: . This graph is based on the same Morningstar data for 1990–2014 for 657 hedge fund returns (HF) as Figure 1 in [1]. The upper line (circles) corresponds to the correlation matrix of the raw HF. The lower line (triangles) correspond to the correlation matrix of the residuals (plus the intercepts, which have no effect) of HF adjusted for RF (whose effect is small) and regressed over Mkt-RF and Fama-French risk factors SMB, HML, WML. Each correlation matrix is taken in the basis where its eigenvector corresponding to the largest eigenvalue has all nonnegative elements.

4.1. Caveats

The spectral model (25) is exactly that—a model. Its premise is that T is built solely from building blocks constructed from and . It is meant to work in the large N limit and for generic configurations of . For example, if all are zero except for , (i.e., , so and , ), then we expect as there is no internal crossing. Equation (25) does not have this property. In fact, one can attempt to construct such T as follows. Let

where are coefficients to be determined from the requirement that when we have :

This system of N equations can be solved if the matrix is invertible. However, for a generic some of the coefficients will be negative. In any event, we will not pursue this direction here as our goal is turnover reduction in the large N limit for generic configurations of , which brings us to the next “caveat”.

For some some elements in (31) can be small suppressing the contributions of the corresponding . We can remedy this via the following approximation:

I.e., in the sum over in (31), are replaced by their cross-sectional average, and (33) is reproduced in the case where individual turnovers are uniform.

It might be tempting to replace by

where

is the least-squares solution to the approximate “eigenvalue” equation:

where the minimization in Equation (41) is w.r.t. , and is the properly normalized unit vector. However, using can lead to underestimating turnover (i.e., overestimating turnover reduction).11 In the example of Figure 1, for the upper line (circles) we have and , and for the lower line (triangles) we have and .

In fact, there is a more precise relationship between and . Thus, from

we have

where we have taken into account that in the large N limit the terms in the sum are subleading. Combining (43) and (34), we get

where . Equation (43) makes it evident why in the large N limit choosing the basis where all is equivalent to maximizing (see footnote 6).

4.2. Why Is All This Useful?

In real-life trading, when one combines thousands of not-too-correlated alphas (with some weights) and trades the so-combined single “unified” alpha on a single trading platform (as opposed to trading all these alphas on their own individual execution platforms), one gets an automatic bonus: internal crossing of trades between different alphas, hence turnover reduction, which can be substantial. Why is this important? Because the weights with which alphas are combined are determined via optimization (or a similar procedure) and including trading costs (and impact) into this optimization requires modeling turnover reduction, or else the effect of the costs would be (possibly grossly) overestimated, thereby resulting in a (possibly substantially) suboptimal alpha weights. Our main Equations (31), (34), (37) and (44) model turnover reduction via the first principal component and the corresponding eigenvalue of the alpha correlation matrix, which is general. The model of turnover reduction in [1] is a special simple case of our model where all pairwise correlations are uniform. This special case is an unrealistic toy model used in [1] for the purpose of illustrating—via its simplicity—modeling turnover reduction via correlations and the existence of a nonvanishing limit for the turnover when N goes to infinity (as opposed to a naive guess that turnover goes to zero in the large N limit). However, the toy model of [1] is just that—a toy model. It is not designed for practical applications—in real life correlations are not uniform. In contrast, our spectral model we give in this paper is designed precisely with practical applications in mind as it is applicable to a general (and realistic) alpha correlation structure. Put differently, if one uses Equation (20) of [1] in the general case, it is unclear what ρ in that formula should be. What we have achieved here is that we give a simple explicit formula for this ρ—which we refer to as here—via (34) in the general (that is, practically interesting) case. Furthermore, we cannot emphasize enough that our result here—that is expressed via the first principal component and the corresponding eigenvalue—only holds in the large N limit; higher principal components are suppressed by powers of , which are small when N is sufficiently large. At finite N there is no reason for such contributions to be small. Note that this is irrespective of whether we consider the general case or the toy model of [1]. In fact, Equation (19) of [1] expressly shows that unless N is large, Equation (20) of [1], which is a special case of our model, does not hold.

One evident question arising in the context of the spectral model is out-of-sample stability. Generally, off-diagonal elements of a sample covariance (correlation) matrix are not expected to be too out-of-sample stable. Consequently, principal components of a correlation matrix inherit this instability. Nonetheless, the first principal component—which happily is what our spectral model uses—generally is the most out-of-sample stable, with higher principal components substantially more unstable. Prosaically, further mitigating the stability issue is the fact that turnover reduction is important if alphas have substantial turnover in the first instance, i.e., the holding periods are short and, consequently, the relevant historical lookbacks are also short. With short lookbacks one recomputes quantities such as the correlation matrix and its first principal component on correspondingly high frequencies. In fact, there is yet another way of dealing with the stability issue if one is able to build a multi-factor risk model for alphas along the lines of [27], whereby instead of the sample correlation matrix one uses a constructed one, which by its very construction—if such construction is possible in the first instance, that is—is expected to be substantially more out-of-sample stable. All in all, in real life one works with what one has got and tries to do one’s best with it, be it modeling turnover reduction, alpha covariance matrix, etc.

5. Conclusions

The upshot is that—just as in theoretical physics [28]—the large N limit [1] provides a powerful tool in quantitative finance. In this note we give an explicit spectral model of turnover reduction for a general alpha correlation matrix in the limit where the number of alphas is large. In this regime, this model can be used in estimating transaction costs, and in the problem of portfolio optimization with costs [24,25]. Our spectral model is expected to provide a good approximation for a generic distribution of individual alpha turnovers. In the large N limit, the turnover reduction coefficient based on the spectral model does not appear to vanish but approaches a finite value. In [23] we further confirm the results of this paper by using a complementary factor model approach.

Acknowledgments

The author would like to thank two anonymous reviewers and Kerry Patterson for valuable suggestions.

Conflicts of Interest

The author declares no conflict of interest.

References

- Z. Kakushadze, and J.K.-S. Liew. “Is It Possible to OD on Alpha? ” J. Altern. Invest. (forthcoming). Available online: http://ssrn.com/abstract=2419415 (accessed on 25 February 2015). [CrossRef]

- C. Ackerman, R. McEnally, and D. Revenscraft. “The Performance of Hedge Funds: Risk, Return and Incentives.” J. Financ. 54 (1999): 833–874. [Google Scholar] [CrossRef]

- V. Agarwal, and N.Y. Naik. “On Taking the “Alternative” Route: The Risks, Rewards, and Performance Persistence of Hedge Funds.” J. Altern. Invest. 2 (2000): 6–23. [Google Scholar] [CrossRef]

- V. Agarwal, and N.Y. Naik. “Multi-Period Performance Persistence Analysis of Hedge Funds Source.” J. Financ. Quant. Anal. 35 (2000): 327–342. [Google Scholar] [CrossRef]

- G. Amin, and H. Kat. “Stocks, Bonds and Hedge Funds: Not a Free Lunch! ” J. Portf. Manag. 29 (2003): 113–120. [Google Scholar] [CrossRef]

- C.S. Asness, R.J. Krail, and J.M. Liew. “Do Hedge Funds Hedge? ” J. Portf. Manag. 28 (2001): 6–19. [Google Scholar] [CrossRef]

- C. Brooks, and H.M. Kat. “The Statistical Properties of Hedge Fund Index Returns and Their Implications for Investors.” J. Altern. Invest. 5 (2002): 26–44. [Google Scholar] [CrossRef]

- S.J. Brown, W. Goetzmann, and R.G. Ibbotson. “Offshore Hedge Funds: Survival and Performance, 1989–1995.” J. Bus. 72 (1999): 91–117. [Google Scholar] [CrossRef]

- N. Chan, M. Getmansky, S.M. Haas, and A.W. Lo. “Systemic Risk and Hedge Funds.” In The Risks of Financial Institutions. Edited by M. Carey and R.M. Stulz. Chicago, IL, USA: University of Chicago Press, 2006, pp. 235–338. [Google Scholar]

- F.R. Edwards, and M.O. Caglayan. “Hedge Fund and Commodity Fund Investments in Bull and Bear Markets.” J. Portf. Manag. 27 (2001): 97–108. [Google Scholar] [CrossRef]

- F.R. Edwards, and J. Liew. “Managed Commodity Funds.” J. Futures Mark. 19 (1999): 377–411. [Google Scholar] [CrossRef]

- F.R. Edwards, and J. Liew. “Hedge Funds versus Managed Futures as Asset Classes.” J. Deriv. 6 (1999): 45–64. [Google Scholar] [CrossRef]

- W. Fung, and D. Hsieh. “A Primer on Hedge Funds.” J. Empir. Financ. 6 (1999): 309–331. [Google Scholar] [CrossRef]

- W. Fung, and D. Hsieh. “Performance Characteristics of Hedge Funds and Commodity Funds: Natural vs. Spurious Biases.” J. Financ. Quant. Anal. 35 (2000): 291–307. [Google Scholar] [CrossRef]

- W. Fung, and D. Hsieh. “The Risk in Hedge Fund Strategies: Theory and Evidence from Trend Followers.” Rev. Financ. Stud. 14 (2001): 313–341. [Google Scholar] [CrossRef]

- D.-L. Kao. “Battle for Alphas: Hedge Funds versus Long-Only Portfolios.” Financ. Anal. J. 58 (2002): 16–36. [Google Scholar] [CrossRef]

- B. Liang. “On the Performance of Hedge Funds.” Financ. Anal. J. 55 (1999): 72–85. [Google Scholar] [CrossRef]

- B. Liang. “Hedge Funds: The Living and the Dead.” J. Financ. Quant. Anal. 35 (2000): 309–326. [Google Scholar] [CrossRef]

- B. Liang. “Hedge Fund Performance: 1990–1999.” Financ. Anal. J. 57 (2001): 11–18. [Google Scholar] [CrossRef]

- A.W. Lo. “Risk Management For Hedge Funds: Introduction and Overview.” Financ. Anal. J. 57 (2001): 16–33. [Google Scholar] [CrossRef]

- F.-É. Racicot, and R. Théoret. “The Procyclicality of Hedge Fund Alpha and Beta.” J. Deriv. Hedge Funds 19 (2013): 109–128. [Google Scholar] [CrossRef]

- T. Schneeweis, R. Spurgin, and D. McCarthy. “Survivor Bias in Commodity Trading Advisor Performance.” J. Futures Mark. 16 (1996): 757–772. [Google Scholar] [CrossRef]

- Z. Kakushadze. “Can Turnover Go to Zero? ” J. Deriv. Hedge Funds 20 (2014): 157–176. [Google Scholar] [CrossRef]

- Z. Kakushadze. “Combining Alpha Streams with Costs.” J. Risk 17 (2015): 57–78. [Google Scholar] [CrossRef]

- Z. Kakushadze. “Notes on Alpha Stream Optimization.” J. Invest. Strateg. 4 (2015): 37–81. [Google Scholar] [CrossRef]

- R. Rebonato, and P. Jäckel. “The most general methodology to create a valid correlation matrix for risk management and option pricing purposes.” Available online: http://ssrn.com/abstract=1969689 (accessed on 20 April 2014).

- Z. Kakushadze. “Factor Models for Alpha Streams.” J. Invest. Strateg. 4 (2014): 83–109. [Google Scholar] [CrossRef]

- G. ’t Hooft. “A Planar Diagram Theory For Strong Interactions.” Nuclear Phys. B 72 (1974): 461–473. [Google Scholar] [CrossRef]

- 1 Here “alpha” means a real-life (as opposed to “academic”) alpha, that is, any reasonable expected return on which one may wish to trade, that is, take risk. In fact, real-life alphas (e.g., momentum strategies) often have sizable exposure to risk. Furthermore, there is no “perfect” risk model w.r.t. which one would hypothetically neutralize risk exposure of a portfolio. Otherwise, there would only be mean-reversion caused by temporary trading imbalances, which is evidently not the case in real life. Different time horizons provide different alpha (trading) opportunities.

- 3 For the following discussion it is not important what the actual values of these weights are or how they are computed (e.g., via optimization, regression, etc.). We keep them arbitrary subject to the normalization condition . The weights can be negative (internal crossing).

- 4 The matrix is degenerate if and only if the matrix is degenerate: .

- 5 Actually, this assumes that there are no N/As in any of the alpha time series. If some or all alpha time series contain N/As in non-uniform manner and the correlation matrix is computed by omitting such pair-wise N/As, then the resulting correlation matrix may have negative eigenvalues that are not “small” in the sense used above, i.e., they are not zeros distorted by computational rounding. The deformation method we discuss above can be applied in this case as well. Non-positive-definiteness of the original (undeformed) correlation matrix typically is not a dominant effect in the first principal component (see below) and turnover reduction; however, in practice one would typically use a positive-definite (deformed) correlation matrix and the deformation can have a sizable effect—see Section 7 of [23] for illustrative empirical examples.

- 6 Here we are assuming that, if need be, the method reviewed in Subsection 3.1 has been applied and all . Furthermore, the basis of alphas is taken (i.e., the signs of are chosen) such that is maximized ( is the mean correlation). Thus, consider the case with uniform correlations , , studied in [1]. In this case, in the large N limit, the turnover reduction coefficient (see below) [1]. However, if we flip the signs of some alphas (and then we must also flip the signs of the corresponding weights ), which does not change the portfolio turnover, the mean correlation will no longer be equal ρ, hence the aforementioned choice of the basis for . We will discuss this point in more detail and give a precise prescription for fixing this basis below. For now we will just bear this in mind.

- 7 Note that is not suitable because T is not expected to have a peculiar behavior when is nearly degenerate. Furthermore, only the trace-based scalar invariant reproduces the special case discussed below. Also, see below why relative coefficients in (24) do not change the end result.

- 8 E.g., in the uniform correlation case where (), we have , while the rest of the eigenvectors have zero sums.

- 10 We emphasize the adjective “illustrative” for the reason that, because various hedge funds in this data do/did not all trade the same underlying instruments and also the corresponding time series are not 100% overlapping (some hedge funds are dead, some are newer than others, etc.), it would not necessarily be correct to assume that their trades could be crossed. Therefore, we use this data only to illustrate various properties of the correlation matrix, and not to directly draw any conclusions about turnover reduction had these alpha streams actually crossed their trades.

- 11 One may wish to use , their average or some other value between and .

© 2015 by the authors; licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution license ( http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Kakushadze, Z. A Spectral Model of Turnover Reduction. Econometrics 2015, 3, 577-589. https://doi.org/10.3390/econometrics3030577

AMA Style

Kakushadze Z. A Spectral Model of Turnover Reduction. Econometrics. 2015; 3(3):577-589. https://doi.org/10.3390/econometrics3030577

Chicago/Turabian StyleKakushadze, Zura. 2015. "A Spectral Model of Turnover Reduction" Econometrics 3, no. 3: 577-589. https://doi.org/10.3390/econometrics3030577