Measuring Knowledge Management Performance in Organizations: An Integrative Framework of Balanced Scorecard and Fuzzy Evaluation

Abstract

:1. Introduction

2. Literature

3. A Framework of KM Performance Evaluation Indicators Based on BSC

3.1. BSC for KM Performance Evaluation

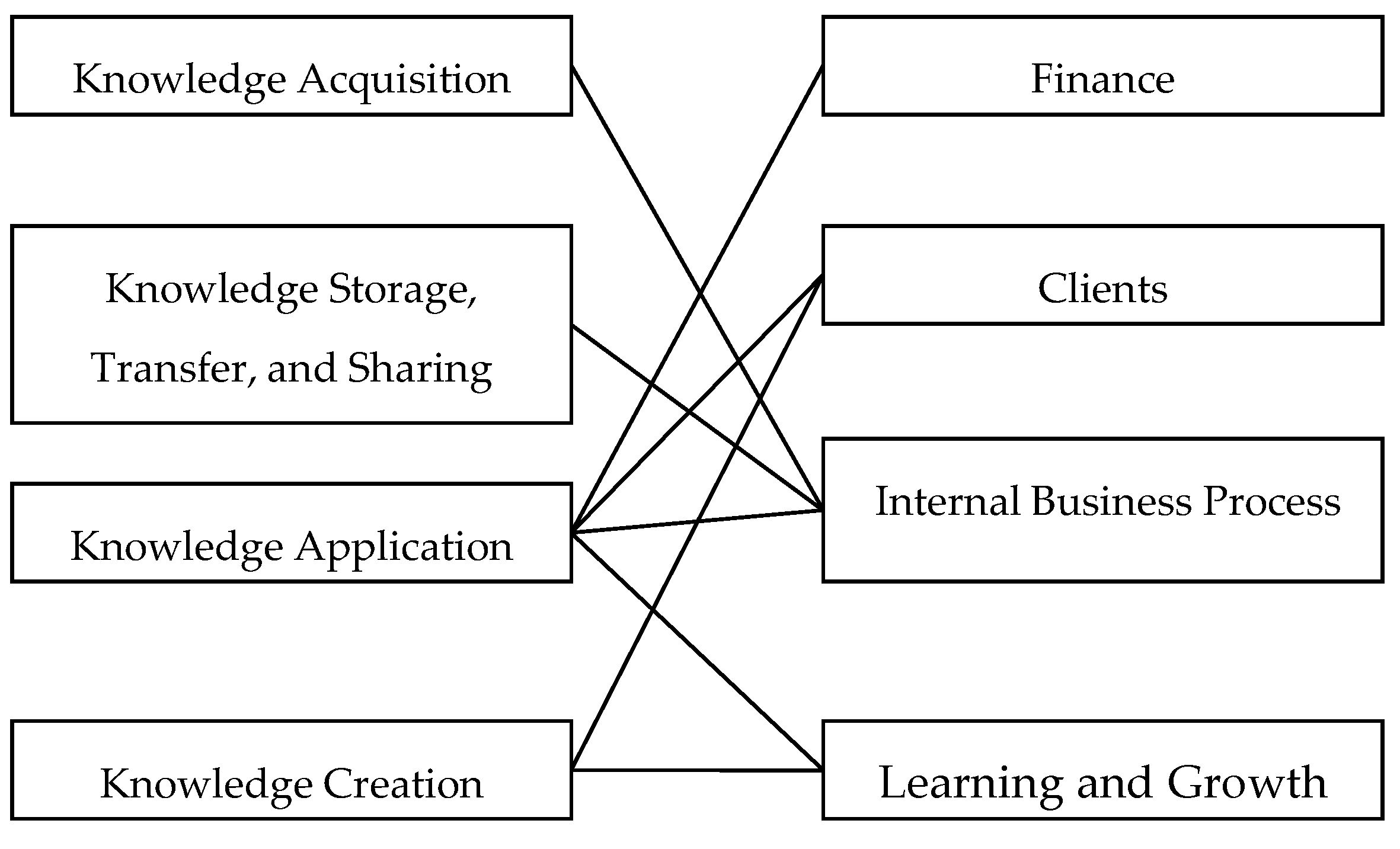

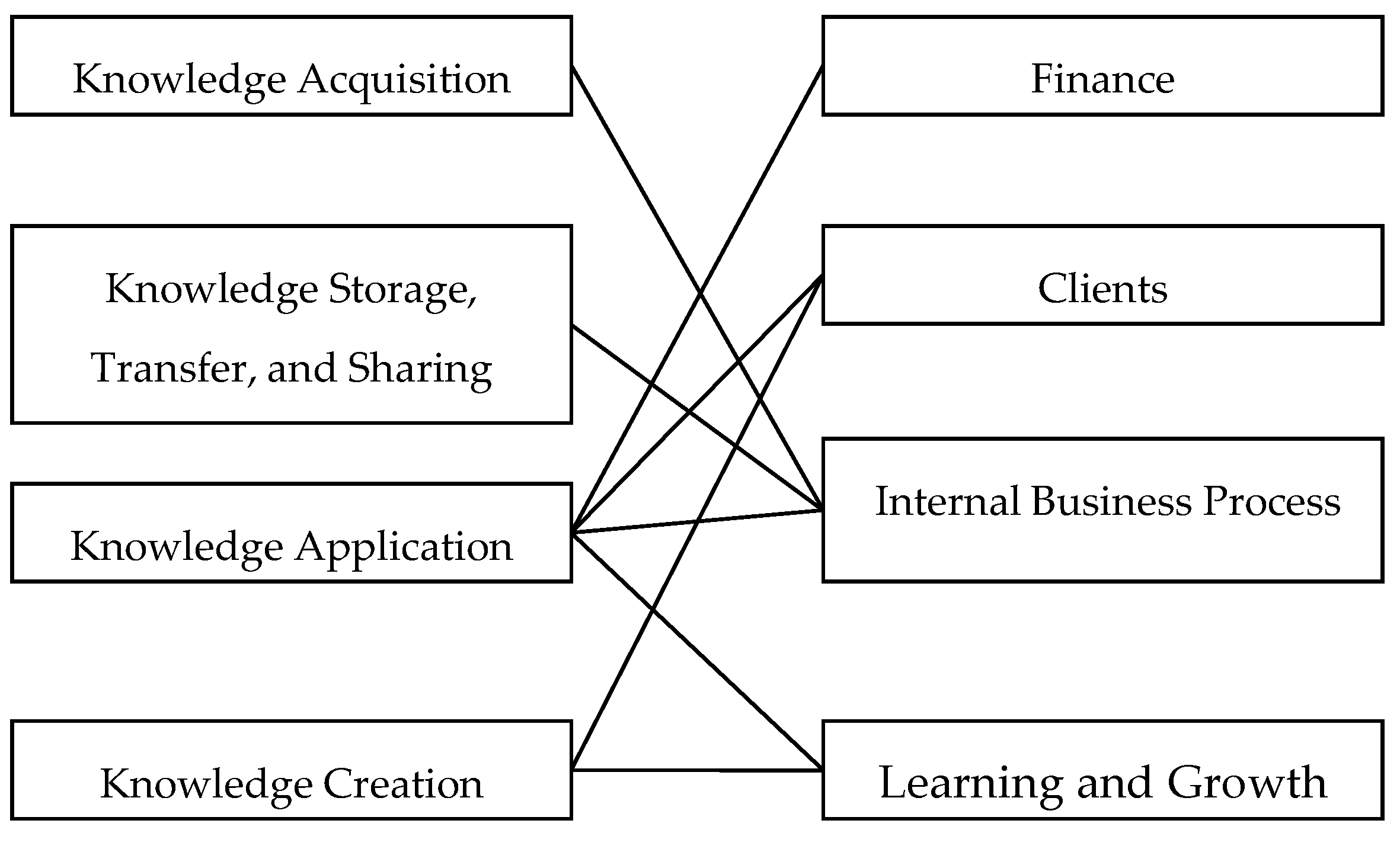

3.2. The Mapping between KM and BSC

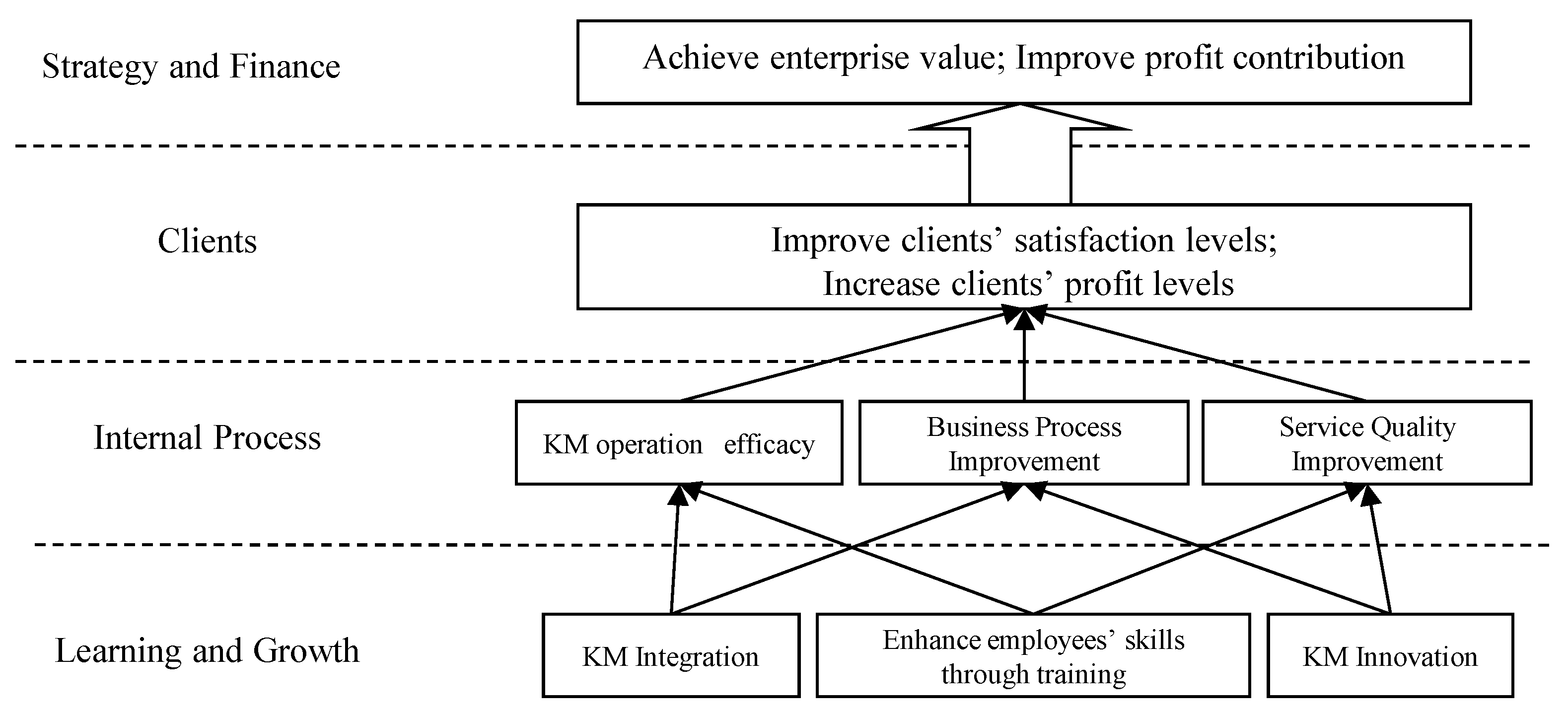

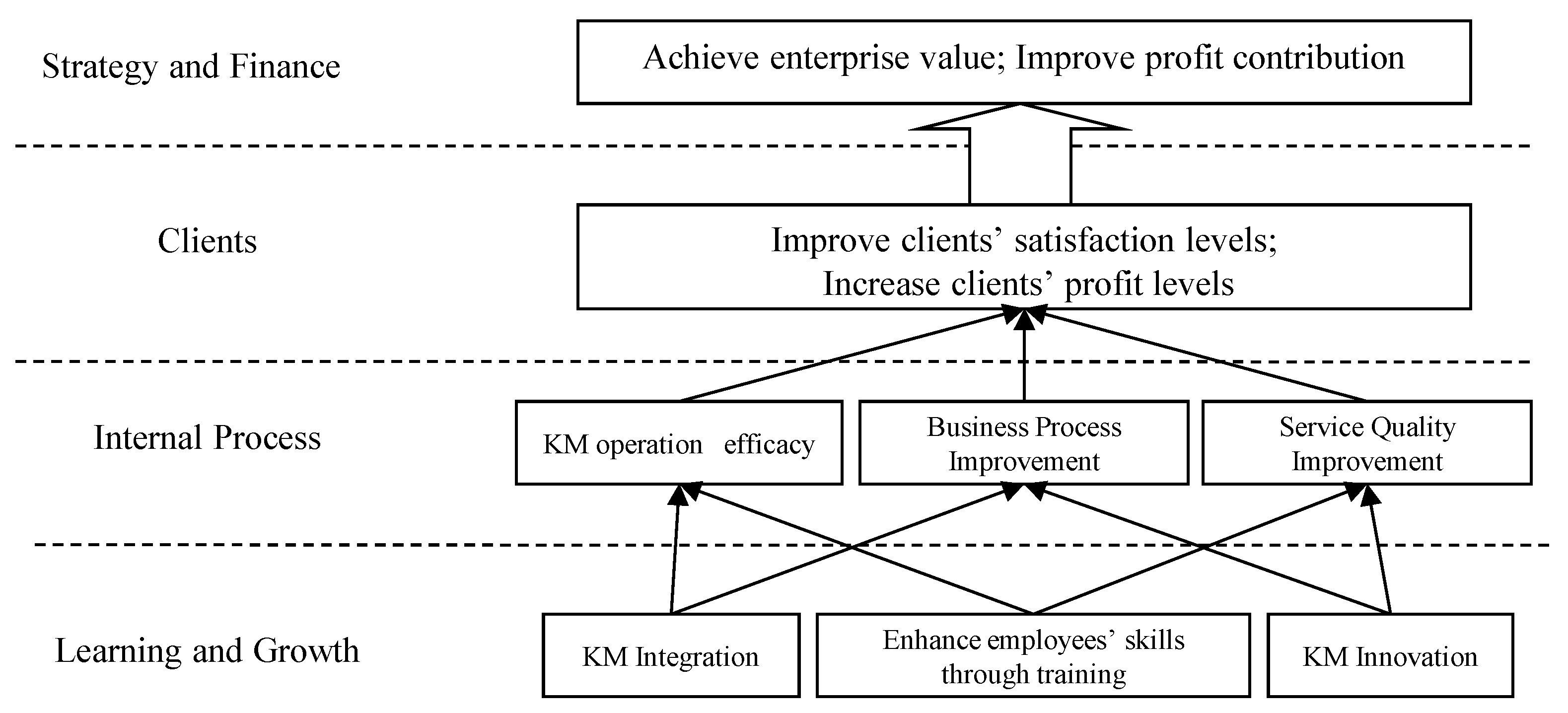

3.3. The Causal Relationship between KM and BSC

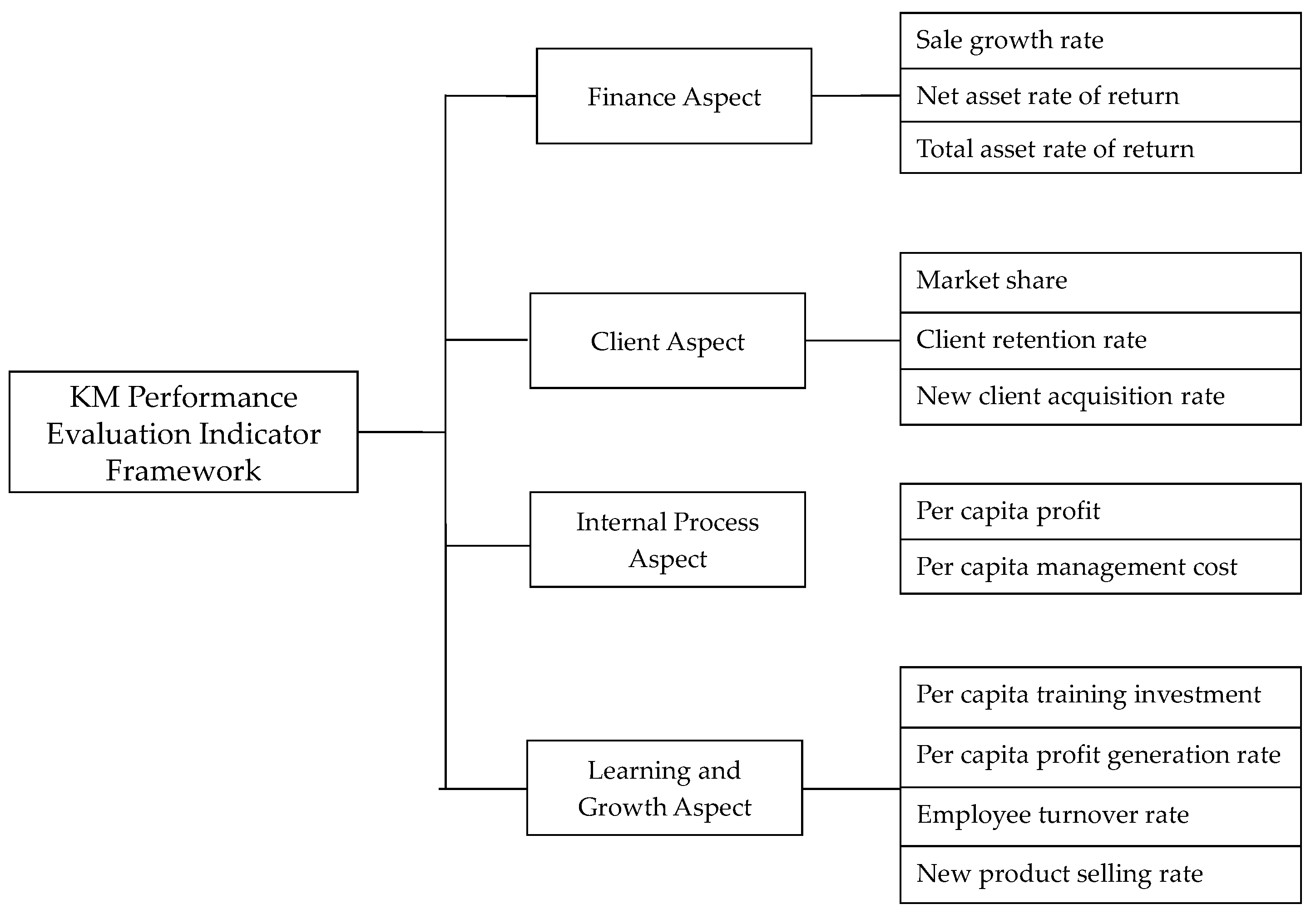

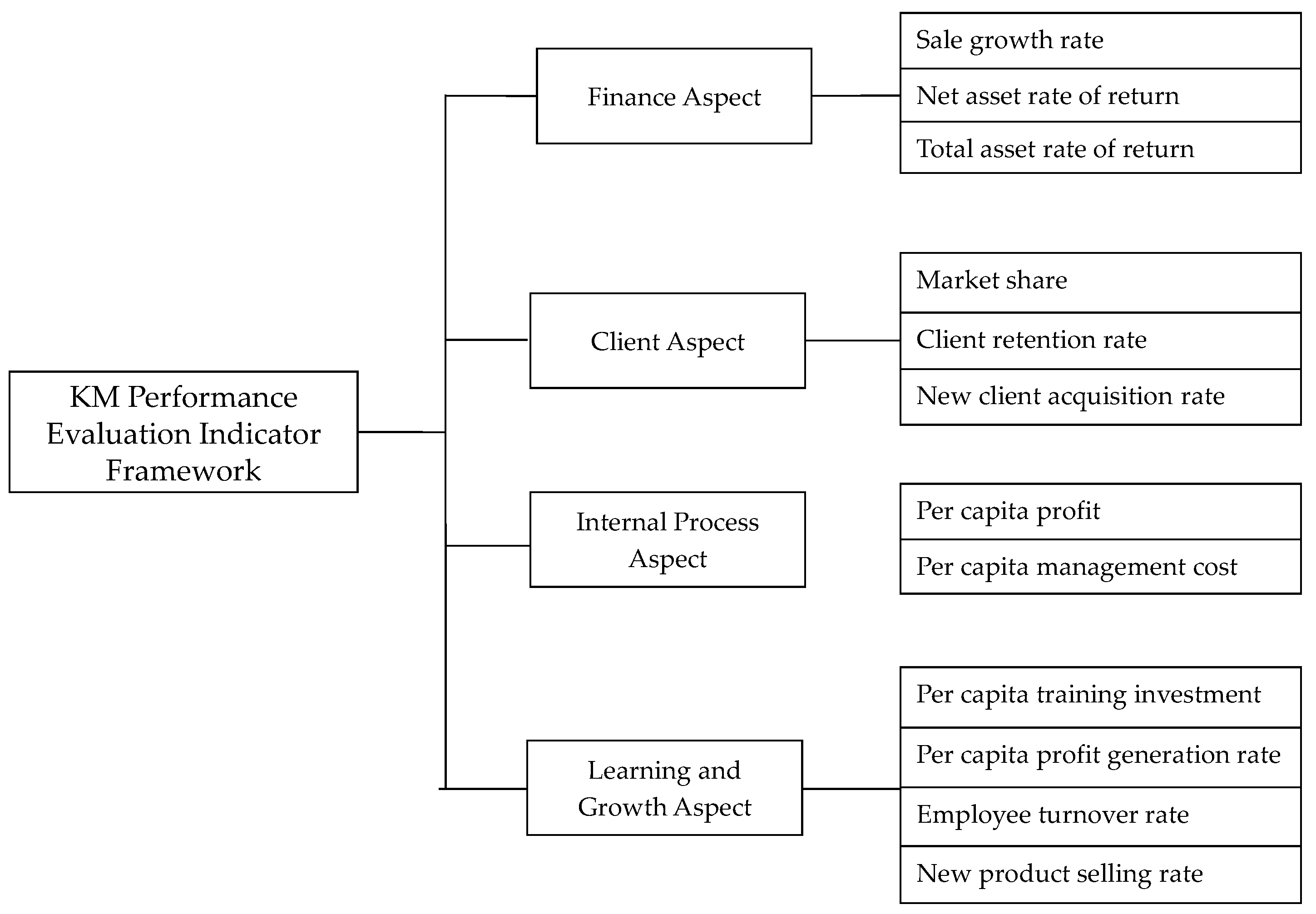

3.4. The Framework of Indicators

4. Evaluation Model

4.1. Evaluation Object Factor Sets

4.2. Comment Sets

4.3. Weighted Distribution of the Indicators

4.4. Determine the Membership Value of Indicators and Create Fuzzy Relationship Matrix R

4.4.1. Membership Value of Positive Indicators

4.4.2. Membership Value of Negative Indicators

4.5. Overall Evaluation Result

4.6. Analysis of Overall Fuzzy Evaluation Result

5. Numerical Example

6. Conclusions

Acknowledgments

Author Contributions

Conflicts of Interest

References

- Aggestam, L.; Durst, S.; Persson, A. Critical Success Factors in Capturing Knowledge for Retention in IT-Supported Repositories. Information 2014, 5, 558–569. [Google Scholar] [CrossRef]

- Wu, I.L.; Chen, J.L. Knowledge management driven firm performance: The roles of business process capabilities and organizational learning. J. Knowl. Manag. 2014, 18, 1141–1164. [Google Scholar] [CrossRef]

- Cohen, J.F.; Olsen, K. Knowledge management capabilities and firm performance: A test of universalistic, contingency and complementarity perspectives. Expert Syst. Appl. 2015, 42, 1178–1188. [Google Scholar] [CrossRef]

- Donate, M.J.; de Pablo, J.D.S. The role of knowledge-oriented leadership in knowledge management practices and innovation. J. Bus. Res. 2015, 68, 360–370. [Google Scholar] [CrossRef]

- Kim, T.H.; Lee, J.N.; Chun, J.U.; Benbasat, I. Understanding the effect of knowledge management strategies on knowledge management performance: A contingency perspective. Inf. Manag. 2014, 51, 398–416. [Google Scholar] [CrossRef]

- Lee, S.; Gon Kim, B.; Kim, H. An integrated view of knowledge management for performance. J. Knowl. Manag. 2012, 16, 183–203. [Google Scholar] [CrossRef]

- Wong, K.Y.; Tan, L.P.; Lee, C.S.; Wong, W.P. Knowledge Management performance measurement: Measures, approaches, trends and future directions. Inf. Dev. 2013. [Google Scholar] [CrossRef]

- Yin Rebecca Yiu, M.; Fai Pun, K. Measuring knowledge management performance in industrial enterprises: An exploratory study based on an integrated model. Learn. Org. 2014, 21, 310–332. [Google Scholar] [CrossRef]

- Kao, S.C.; Huang, C.L.; Wu, C.H. Online Knowledge Community Evaluation Model: A Balanced Scorecard Based Approach. In Multidisciplinary Social Networks Research; Springer: Berlin/Heidelberg, Germany, 2014; pp. 28–35. [Google Scholar]

- Lin, H.F. Linking knowledge management orientation to balanced scorecard outcomes. J. Knowl. Manag. 2015, 19, 1224–1249. [Google Scholar] [CrossRef]

- OECD. The knowledge-based economy. 1996. Available online: http://www.oecd.org/sti/sci-tech/theknowledge-basedeconomy.htm (accessed on 25 May 2016).

- APQC. KM capabilities assessment tool. 2016. Available online: https://www.apqc.org/km-capability-assessment-tool (accessed on 25 May 2016).

- Lee, K.C.; Lee, S.; Kang, I.W. KMPI: Measuring knowledge management performance. Inf. Manag. 2005, 42, 469–482. [Google Scholar]

- Kuah, C.T.; Wong, K.Y.; Wong, W.P. Monte Carlo data envelopment analysis with genetic algorithm for knowledge management performance measurement. Expert Syst. Appl. 2012, 39, 9348–9358. [Google Scholar] [CrossRef]

- Chen, L.; Fong, P.S. Evaluation of knowledge management performance: An organic approach. Inf. Manag 2015, 52, 431–453. [Google Scholar] [CrossRef]

- Lee, C.S.; Wong, K.Y. Development and validation of knowledge management performance measurement constructs for small and medium enterprises. J. Knowl. Manag. 2015, 19, 711–734. [Google Scholar] [CrossRef]

- Wang, J.; Ding, D.; Liu, O.; Li, M. A synthetic method for knowledge management performance evaluation based on triangular fuzzy number and group support systems. Appl. Soft Comput. 2016, 39, 11–20. [Google Scholar] [CrossRef]

- Chen, M.Y.; Chen, A.P. Knowledge management performance evaluation: A decade review from 1995 to 2004. J. Inf. Sci. 2006, 32, 17–38. [Google Scholar] [CrossRef]

- Fairchild, A.M. Knowledge management metrics via a balanced scorecard methodology. In System Sciences, 2002. HICSS, Proceedings of the 35th Annual Hawaii International Conference on System Sciences, Big Island, HI, USA, 7–10 January 2002; pp. 3173–3180.

- Kaplan, R.S.; Norton, D.P. Linking the balanced scorecard to strategy. Calif. Manag. Rev. 1996, 39, 53–79. [Google Scholar] [CrossRef]

- Kim, J.; Suh, E.; Hwang, H. A model for evaluating the effectiveness of CRM using the balanced scorecard. J. Interact. Market. 2003, 17, 5–19. [Google Scholar] [CrossRef]

- Lehmann, D.R.; Zahay, D.; Peltier, J.W. Survey analyze customer relationship management using balanced scorecard. J. Interact. Market. 2013, 27, 1–16. [Google Scholar]

- McPhail, R.; Herington, C.; Guilding, C. Human resource managers’ perceptions of the applications and merit of the balanced scorecard in hotels. Int. J. Hosp. Manag. 2008, 27, 623–631. [Google Scholar] [CrossRef]

- Becker, W.; Brandt, B.; Eggeling, H. Determining Outcomes of HRM Practices. In Human Resource Management Practices; Springer: Cham, Switzerland, 2015; pp. 223–235. [Google Scholar]

- Milis, K.; Mercken, R. The use of the balanced scorecard for the evaluation of information and communication technology projects. Int. J. Proj. Manag. 2004, 22, 87–97. [Google Scholar] [CrossRef]

- Loeser, F.; Grimm, D.; Erek, K.; Zarnekow, R. Information and Communication Technologies for Sustainable Manufacturing: Evaluating the Capabilities of ICT with a Sustainability Balanced Scorecard. In Proceedings of the 10th Global Conference in Sustainable Manufacturing, Istanbul, Turkey, 31 October–2 November 2012; pp. 429–434.

- Brewer, P.C.; Speh, T.W. Using the balanced scorecard to measure supply chain performance. J. Bus. Logist. 2000, 21, 75–93. [Google Scholar]

- Wu, L.; Chang, C.H. Using the balanced scorecard in assessing the performance of e-SCM diffusion: A multi-stage perspective. Decisi. Support Syst. 2012, 52, 474–485. [Google Scholar] [CrossRef]

- De Gooijer, J. Designing a knowledge management performance framework. J. Knowl. Manag. 2000, 4, 303–310. [Google Scholar] [CrossRef]

- Valmohammadi, C.; Ahmadi, M. The impact of knowledge management practices on organizational performance: A balanced scorecard approach. J. Enterp. Inf. Manag. 2015, 28, 131–159. [Google Scholar] [CrossRef]

- Hu, Y.; Wen, J.; Yan, Y. Measuring the performance of knowledge resources using a value perspective: Integrating BSC and ANP. J. Knowl. Manag. 2015, 19, 1250–1272. [Google Scholar] [CrossRef]

- Zadeh, L.A. Fuzzy sets. Inf. Control 1965, 8, 338–353. [Google Scholar] [CrossRef]

- Goguen, J.A. L-fuzzy sets. J. Math. Anal. Appl. 1967, 18, 145–174. [Google Scholar] [CrossRef]

- Alavi, M.; Leidner, D.E. Review: Knowledge management and knowledge management systems: Conceptual foundations and research issues. MIS Q. 2001, 25, 107–136. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Paper | Representative Methodologies of KM Performance Evaluation |

|---|---|

| Lee et al. ([13], 2005) | Associating knowledge management performance index (KMPI) with three financial indicators (stock price, price earnings ratio, and research and development expenditure) |

| Kuah et al. ([14], 2012) | Integration of data envelopment analysis (DEA), Monte Carlo simulation, and genetic algorithm (GA) |

| Yin and Fai ([8], 2014) | Integrated knowledge management (IKM) model |

| Chen and Fong ([15], 2015) | Structural equation modeling (SEM) and system dynamic (SD) simulation |

| Lee and Wong ([16], 2015) | Survey instrument in small and medium companies |

| Wang et al. ([17], 2016) | Synthetic evaluation method by using triangular fuzzy numbers |

© 2016 by the authors; licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC-BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Lyu, H.; Zhou, Z.; Zhang, Z. Measuring Knowledge Management Performance in Organizations: An Integrative Framework of Balanced Scorecard and Fuzzy Evaluation. Information 2016, 7, 29. https://doi.org/10.3390/info7020029

Lyu H, Zhou Z, Zhang Z. Measuring Knowledge Management Performance in Organizations: An Integrative Framework of Balanced Scorecard and Fuzzy Evaluation. Information. 2016; 7(2):29. https://doi.org/10.3390/info7020029

Chicago/Turabian StyleLyu, Hongbo, Zhiying Zhou, and Zuopeng Zhang. 2016. "Measuring Knowledge Management Performance in Organizations: An Integrative Framework of Balanced Scorecard and Fuzzy Evaluation" Information 7, no. 2: 29. https://doi.org/10.3390/info7020029