Innovative Exuberance: Fluctuations in the Painting Production in the 17th-Century Netherlands

1

Huygens Institute of Netherlands History, 1001 EW Amsterdam, The Netherlands

2

School of Historical Studies, University of Amsterdam, 1012 WX Amsterdam, The Netherlands

Arts 2019, 8(2), 72; https://doi.org/10.3390/arts8020072

Submission received: 11 January 2019

/

Revised: 13 June 2019

/

Accepted: 13 June 2019

/

Published: 18 June 2019

(This article belongs to the Special Issue Art Markets and Digital Histories)

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

:The surprising and rapid flowering of Dutch art and the Dutch art market from the late 16th century to the mid-17th century have propelled scholars to quantify the volume of production and to determine the source of its growth. However, existing studies have not explored the use of known paintings to specify and visualize the fluctuations of painting production in the Dutch Republic. Employing data mining techniques to leverage the most comprehensive datasets of Netherlandish paintings (RKD), this paper visualizes and analyzes the trend of painting production in the Northern Netherlands throughout the 17th-century. The visualizations verify the existing observations on the market saturation and industry stagnation in 1630–1640. In spite of this market condition, the growth of painting production was sustained until the 1660s. This study argues that the irrational risk-taking behavior of painters and the over-enthusiasm for painting in the public created a “social bubble” and the subsequent contraction of the production was a market correction back to a stable state. However, these risk-taking attitudes during the bubble time spurred exuberant artistic innovations that highlight the Dutch contribution to the development of art.

1. Introduction

From the late 16th century to the mid-17th century the sudden, meteoric rise of Dutch economic power was accompanied by the surprising and rapid flowering of Dutch art, paintings in particular. During the Dutch Golden Age, the volume and the variety of genres and styles of the painting production reached unprecedented levels (Van der Woude 1991; Montias 1990). Although it has been suggested that the Dutch art market reached its pinnacle around 1660 and collapsed after the 1660s (De Vries 1991; Bok 1994, 2001), scholars have not yet been able to elucidate the exact trend and fluctuations of painting production in the Dutch Republic. Due to the lack of historical sources on the painting production, existing studies either extrapolate the available materials to fill the missing data (Van der Woude 1991; Montias 1990; De Marchi and Van Miegroet 2006, 2014), or use the number of painters in the Republic to indicate the size of the art market (Rasterhoff 2017; Nijboer 2010). Nonetheless, both approaches are subject to a wide margin of error and are yet to yield convincing results (Brosens and Van der Stighelen 2012). Meanwhile, several photo archives of paintings were digitalized and published online in the past years, which have offered an alternative framework for estimating the painting production using comprehensive modern databases. Yet, except for Bok’s (2002) study on portraits, no existing studies were able to utilize big data on paintings to provide new insights into the trend of painting production.

This research aims to fill this gap by analyzing big, art historical data to bring the scholarship of the Dutch art market into the digital realm. Even though art history is said to be a discipline that is reluctant to emerge fully into the new digital world (cf. Zorich 2013), digital art historians have already demonstrated how computational methodologies could shed new lights on the existing debates (cf. Lincoln 2016; Klinke et al. 2018, etc.). Extending the digital art history scholarship into the study of the art market in the Dutch Golden Age, this research will employ computational methods and data visualization to facilitate observations of painting production. In particular, I will combine the quantitative analysis through data mining with the qualitative examination of historical sources. This study will first illustrate the trend of painting production in the Golden Age by visualizing the number of surviving/documented paintings produced over time. Then, the observations derived from the data analysis will be interpreted with historical evidence which forms hypotheses using theories in economics and social sciences. In this way, I hope to bridge the digital and traditional art historical scholarships of the art markets of the 17th-century Dutch Republic.

2. Data on Painting Production

The data for this research is drawn from the visual collections preserved in the Netherlands Institute of Art History (RKD). The online version, RKDimages, features broad and deep collections of photographs and reproductions of paintings by Dutch and Flemish artists from 1400 to 1800. In particular, it contains more than 55,000 paintings (including copies of known attributed paintings) produced between 1550 and 1750.1 Together with the images of paintings, the RKD has released meticulous curatorial data about its collection, amenable to computational processing. This research employs the RKDimages data acquired through the public API and uses R for data processing and visualization. It must be noted that while the RKD collection has remarkably rich holdings, it cannot be regarded perfectly representative of the full range of paintings produced in the 17th century. For example, the quality of the paintings may have played an important role in determining what was carefully preserved and what was not.2 RKD’s own collection history may exacerbate this survival bias and inevitably introduces a selection bias favoring the high-quality paintings or the famous Dutch artists of the 17th century. Even though still far from a perfect database, the RKDimages, with its sheer volume, wide coverage, and diverse sources, has grown to be viewed as one of the most complete repositories for surviving and/or identified Netherlandish paintings. Building onto the 19th-century photo archives, the RKDimages covers collections in both public and private holdings and is even able to include the now-lost paintings with only photocopies survived. The RKD database provides an unprecedented opportunity to test, at a larger scale, the existing observations of the 17th-century Dutch art market derived from studies using different sources and approaches.3 Mining this database to calculate painting production will offer a novel perspective, going beyond the scope and scale that previous scholars could ever reach.

As the quantitative analysis in this study inevitably inherits the biases from the RKDimages, it would be ideal to compare it against contemporary archival records.4 If an inventory-based sample was to exhibit similar characteristics to the RKD sample, we could be more confident that the trend is not simply an artifact of the source (De Vries 1991). Therefore, this study will use the inventories in the Getty Provenance Index as a reference.

3. A Probability Approach to Account for Uncertainties

Mining the new dataset also imposes new challenges—the approximate dating of paintings, as an art historical tradition, for the first time, becomes an issue that may impair the accuracy of the estimation of painting production over time. Unless the paintings were dated by the artist or were accurately recorded in contemporary sources, the cataloged date of a painting is often a result of connoisseurship and scholarship. As a common practice in art history, dating paintings to a time period reflects a certain degree of tolerance of uncertainties in art historical research given the limited historical sources. Only one-third of the RKDimages collection is dated to a specific year, leaving the majority either dated to a time period or the active period of the artist. Striving for a more accurate estimation of the production trend by year, it is essential to minimize the impact of the imprecise dating of paintings on the calculation.

The common method of dealing with approximated dates is to pick the average/medium year of the period. This arbitrary approach, however, introduces biases from the number heaping—rounding numbers to the nearest 5 or 10—as art historians are inclined to date paintings to a five- or ten-year period (De Moor and Zuijderduijn 2013). To avoid the number heaping problem, this research takes a probabilistic approach, assuming an even distribution of probability that the painting j was created in each year of its assigned time period.

The undated paintings with attribution are assigned to the active period of the artists, and the undated, unattributed paintings in the RKDimages are often dated to a time period ranging from 25–100 years, which this study employs.

The painting production of year i is thus the sum of all paintings R dated to a period including year i.

This probabilistic approach tries to acknowledge and to accommodate the uncertainties in dates without making arbitrary selections within an assigned time period. Admittedly, this approach is still a proxy of the trend of the actual production each year and contains biases if intended for short-term analysis or a small number of paintings; but for a longer period using tens of thousands of paintings, it could still provide a relatively accurate picture of the general trend of production levels.

This research further divides the total production into five major painting genres commonly used in the historiography of art history: history painting (including mythology, classical history, biblical stories, and religious scenes, etc.), portrait, landscape, still-life, and genre (also known as scenes of everyday life, and others). Although the RKD does not assign genres to its collections, each painting in the RKDimages has a title that often explicitly indicates a subject matter (e.g., Landscape with river scene), and is tagged with a series of keywords describing the content (such as river, boat).5 The RKD uses a hierarchical-structured vocabulary from Getty’s Art & Architecture Thesaurus® (AAT) for the keywords and assigns them to each painting in a systematic way, which minimizes the biases introduced by the heterogeneity in labeling. Using titles and keywords, the whole RKDimages catalog is categorized into the five painting genres, and the painting production of each genre is calculated using the same approach.

4. Production Trend Visualized

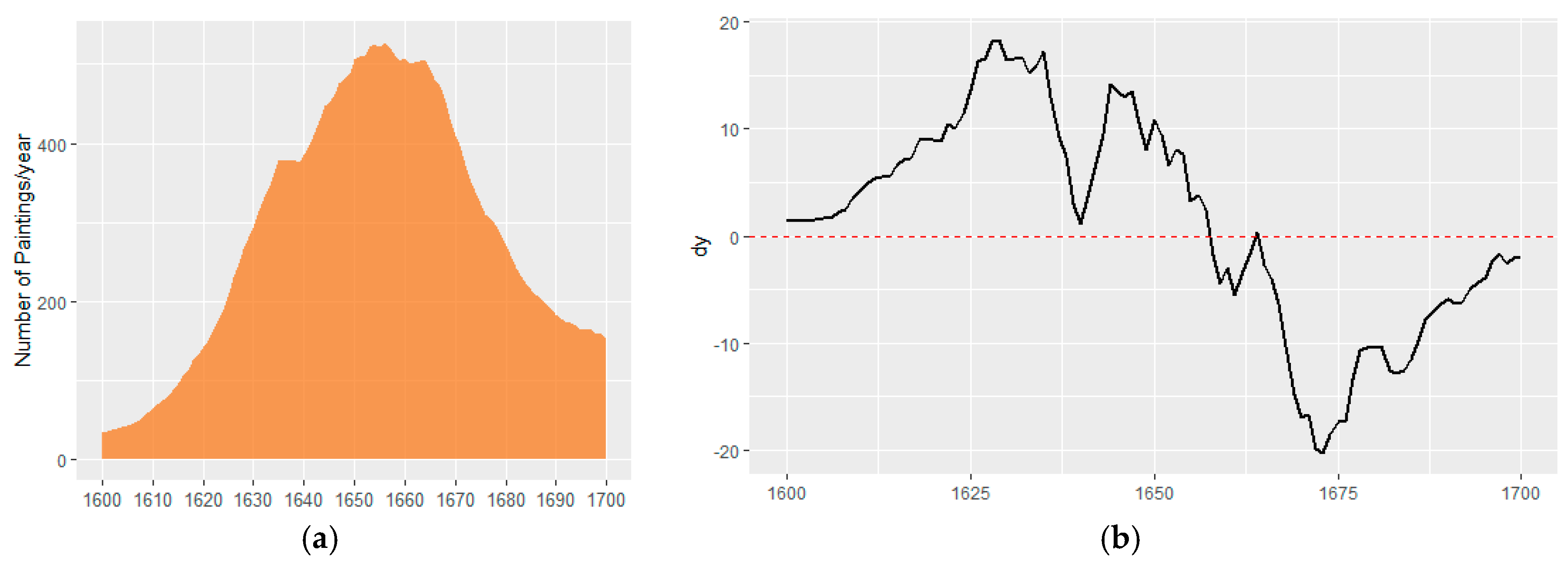

Applying the probabilistic approach to the RKDimages database, I am able to revisit the question that has long intrigued art and economic historians—how did painting production evolve in the 17th-century Dutch Republic? With this new source, Figure 1a shows the total production trend, indicated by the number of paintings in the RKD database. This visualization tallies the trend of the active painter population in the Dutch Republic (Rasterhoff 2017), corroborates the pattern described by Jan de Vries (1991) and parallels the Republic’s economy in the same period (Israel 1997). Beyond confirming existing studies, the trend that emerged from the RKDimages offers more details. Figure 1a demonstrates a steep climb in painting production in the first three decades of the 17th century, which stumbles after 1630. Figure 1b shows the first derivative of the painting production from Figure 1a which indicates the growth rate of painting production. It, too, shows in the first three decades of the 17th century, the painting production grew in an accelerating pace, before hit the wall around 1640, when the growth rate almost dropped to zero. This stagnation shows an early sign of saturation in the art market given the fact that the population of painters underwent a spectacular increase at the same time as Rasterhoff (2017) observed. Remarkably, the production managed to break through and embraced another stage of rapid growth, although at a slightly lower and diminishing rate, in the following two decades (the growth rate see Figure 1b). In the mid-1650s, the growth rate dropped below zero—the contraction started. After the 1660s, a sharp downturn is observed in Figure 1a, as De Vries (1991) suggested using the number of painters active in the Dutch Republic, the fall was more abrupt than its growth (see Figure 1b). The recession of painting production went on till the end of the century; yet, beyond the plummet that De Vries (1991) observed, the decline slows down after 1675, and painting production became stable by the end of the century (the growth rate went back to zero). By the end of the century, the production level returns to that of the 1620s before the explosive growth, making the collapse more like a return to the stable state, which I will elaborate on in Section 7.

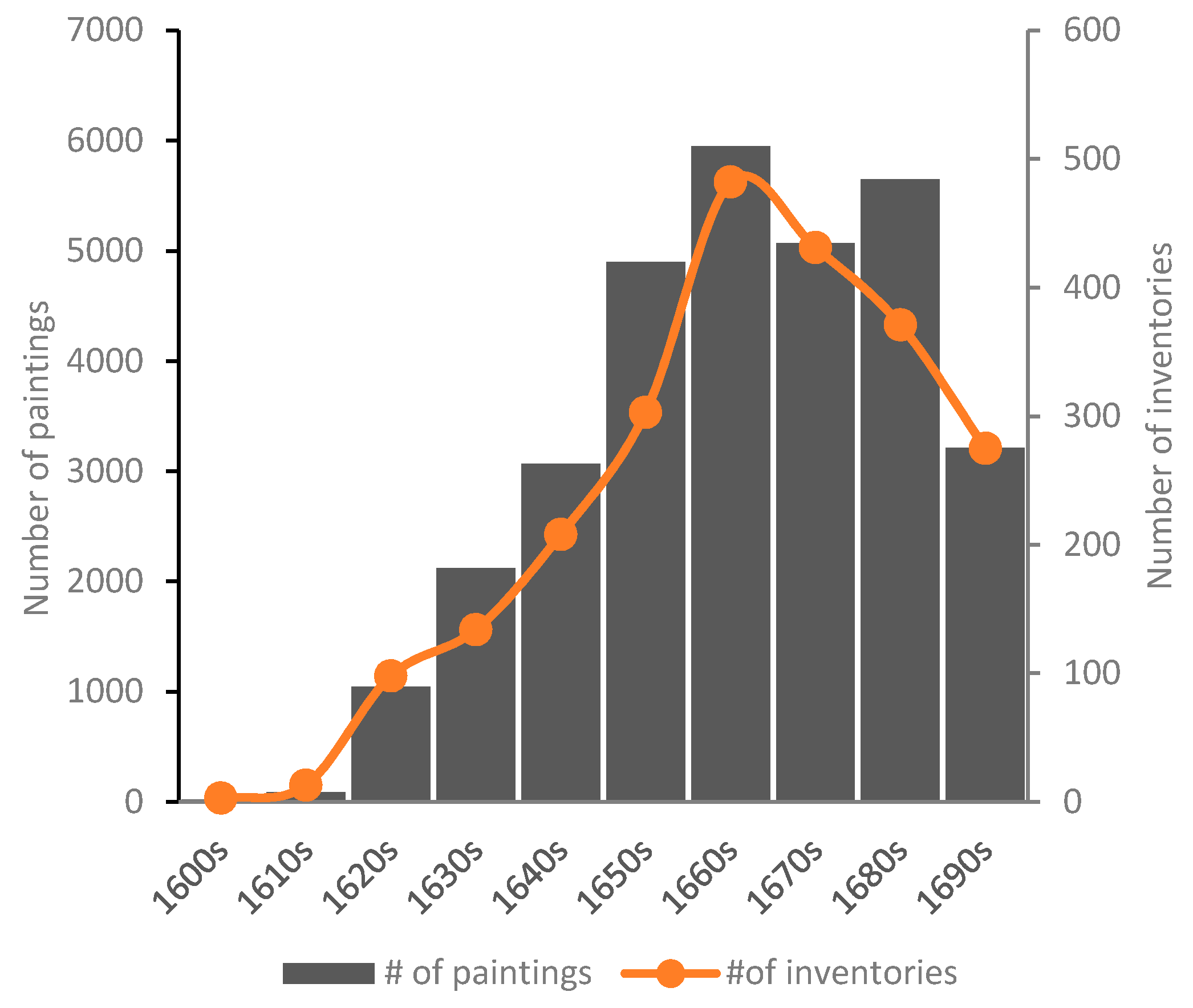

To compare with the trend r.evealed in the RKDimages, the number of paintings in the inventories in the Getty Provenance Index together with the total number of inventories are shown in Figure 2, which resembles the pattern of Figure 1 but with a lag of 10 years. This lag fits Montias’s estimation that the works of art in probate inventories were acquired, on average, 10–11 years before the date of the inventory (Montias 1996). After 1670, a preference for collecting works of the “old (deceased) masters” over those of living masters was observed by Montias. Hence the inventories after 1670 may have suffered from inflation from the secondhand paintings.

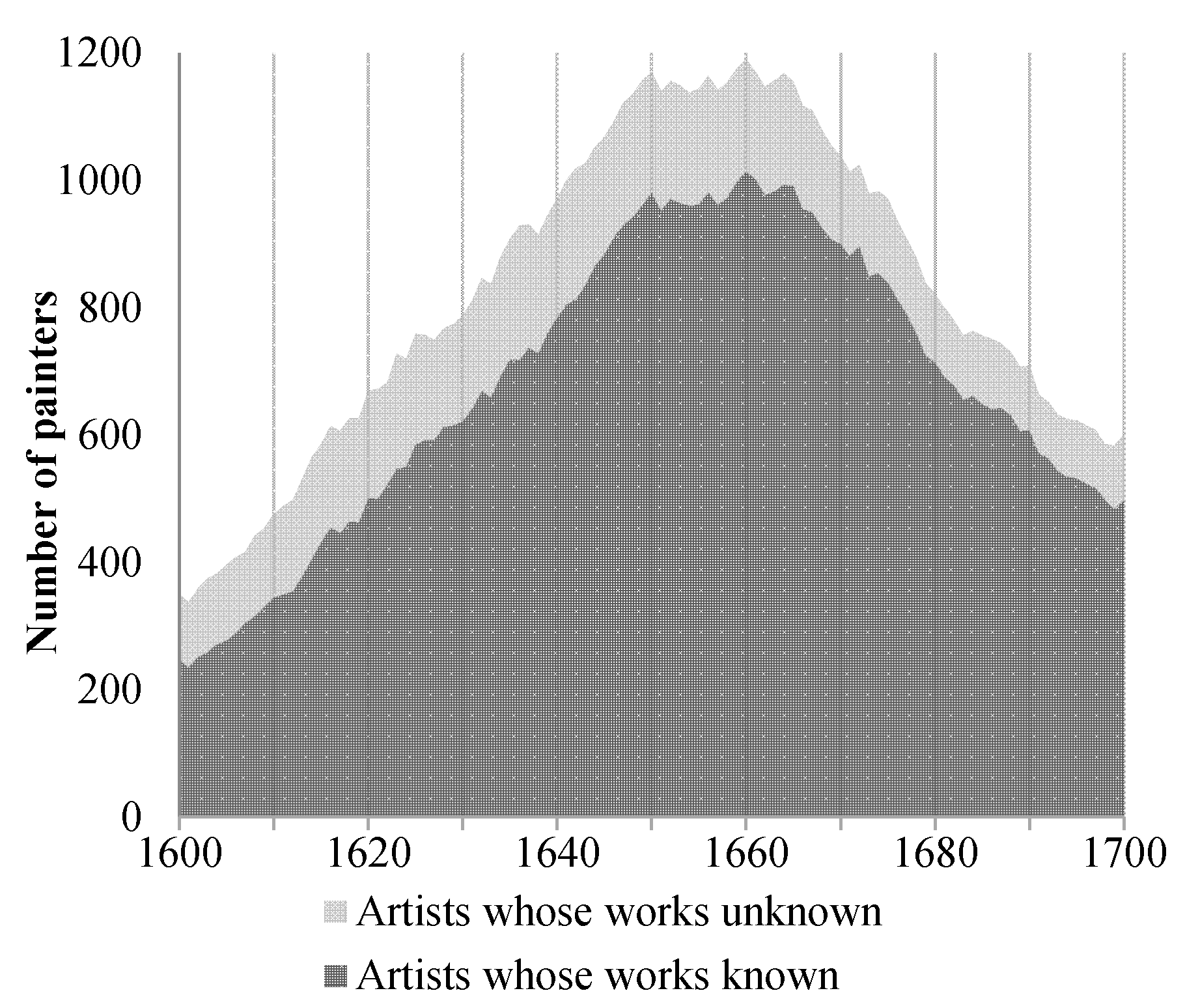

The production trend in Figure 1 is almost perfectly correlated with the total number of painters in the ECARTICO database, a source used by Rasterhoff (2017) and Nijboer (2010) (Figure 3), with a correlation coefficient of 0.99 at the 0.01 significance level. As the inventory-based sample and painter’s population both indicate a similar trend as Figure 1, I am more confident that the RKD data should be able to accurately reflect the production trend of Dutch paintings in the 17th century. The observed biases are most likely random, especially in the short run, and therefore only impact the scale of production without distorting the trend.

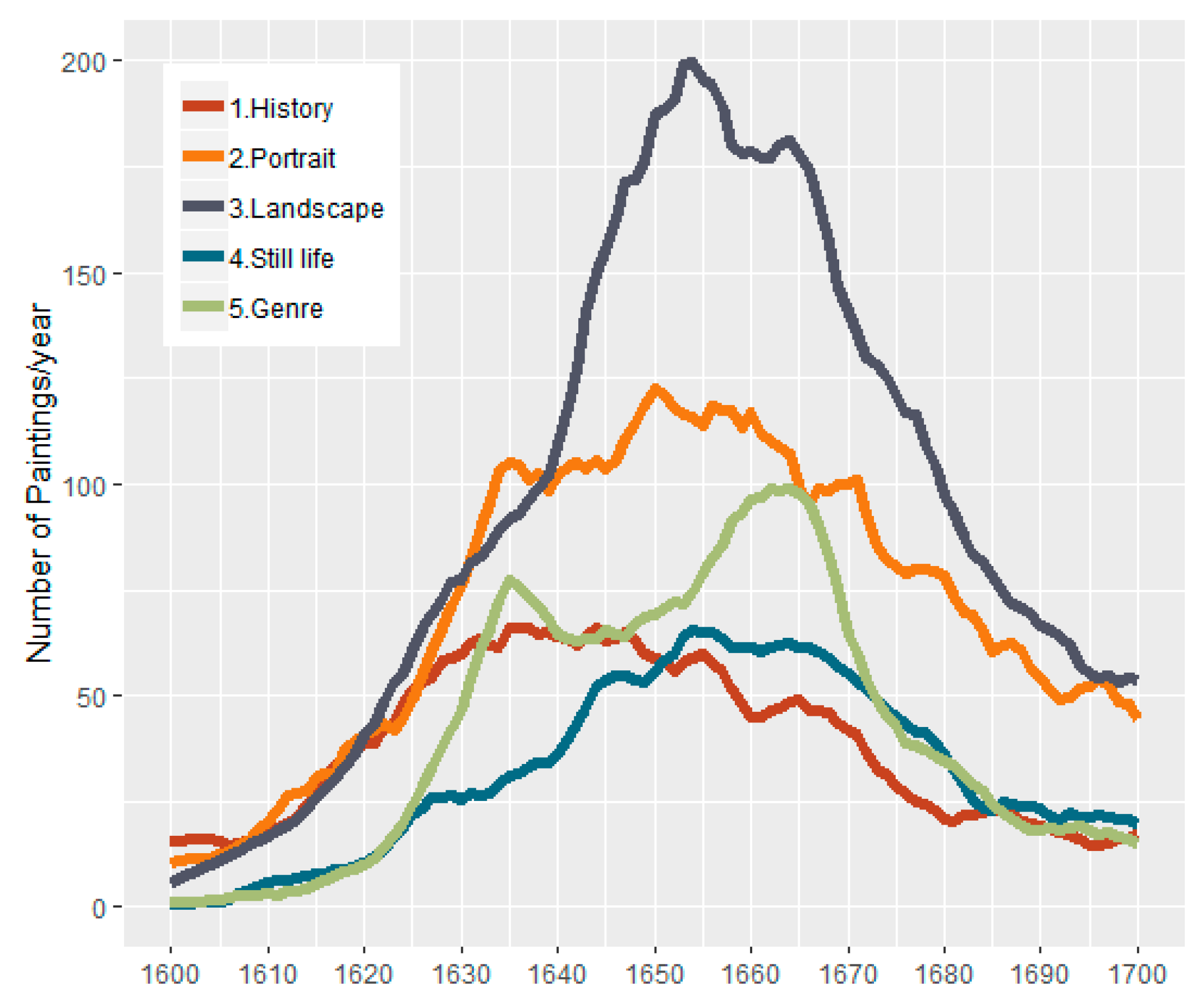

On top of the overall trend of production, the RKDimages allows me to further explore the production trend by individual genres (Figure 4). The variation in the fluctuations for each genre is evident: The difference in the magnitudes of production suggest that each genre developed at its own pace, and partially corresponded to the overall production trend. In general, all genres experienced rapid growth from 1610 to 1635 and managed to push through the stagnation, with landscape paintings taking the lead, and reached new heights between 1650 and 1660 before facing the fall.

Except for history painting, the production trends of different genres are closely correlated, presumably driven by the same factors. History painting (religious painting included), on the other hand, reached its peak around the 1640s and started to decline gradually while the others still enjoyed rapid growth for the next two decades. In particular, history painting, which started as the most-produced painting genre at the beginning of the 17th century (red line in Figure 4), was soon sidelined by other genres, which verifies Bok’s (2008) observation derived from inventories. The secularization of the demand in the protestant Republic seems to have shifted painters and their customers from the sacred to the secular, turning to depict and to appreciate the mundane world, especially landscapes, which, by the 1640s, outshone other genres in terms of production, revealed both in Figure 4 and in the inventories in Bok’s (2008) study. The dominant position of landscape painting (grey line in Figure 4), “a worldly art” as Mariet Westermann (2005) called it, echoes Svetlana Alpers’s controversial argument that the 17th-century Dutch art “turned to describe the world seen” (Alpers 1983). For the “modern” arts that were introduced around the turn of the 17th century, still life painting followed almost the exact same trajectory of development as landscapes, with 0.99 correlation, presumably driven by the same “worldly” forces. As for genre paintings, the camel-hump-shaped production trend matches two phases of the development of this genre. The first generation of portraying merry companies, as Elmer Kolfin (2006) observed, was losing public interest due to the lack of innovation, and by the mid-1640s stagnated both in quantity and quality. Amazingly, the genre overcame this impasse around 1650 with a new generation of artists, led by Gerard Dou, who applied more refined styles, themes, and techniques, catapulting this genre to new heights and making the second growth spurt even more significant than the first one. Finally, portraits, which faced the steadiest demand compared to other genres, enjoyed growth in numbers and suffered less after the collapse with a relatively mild decline.

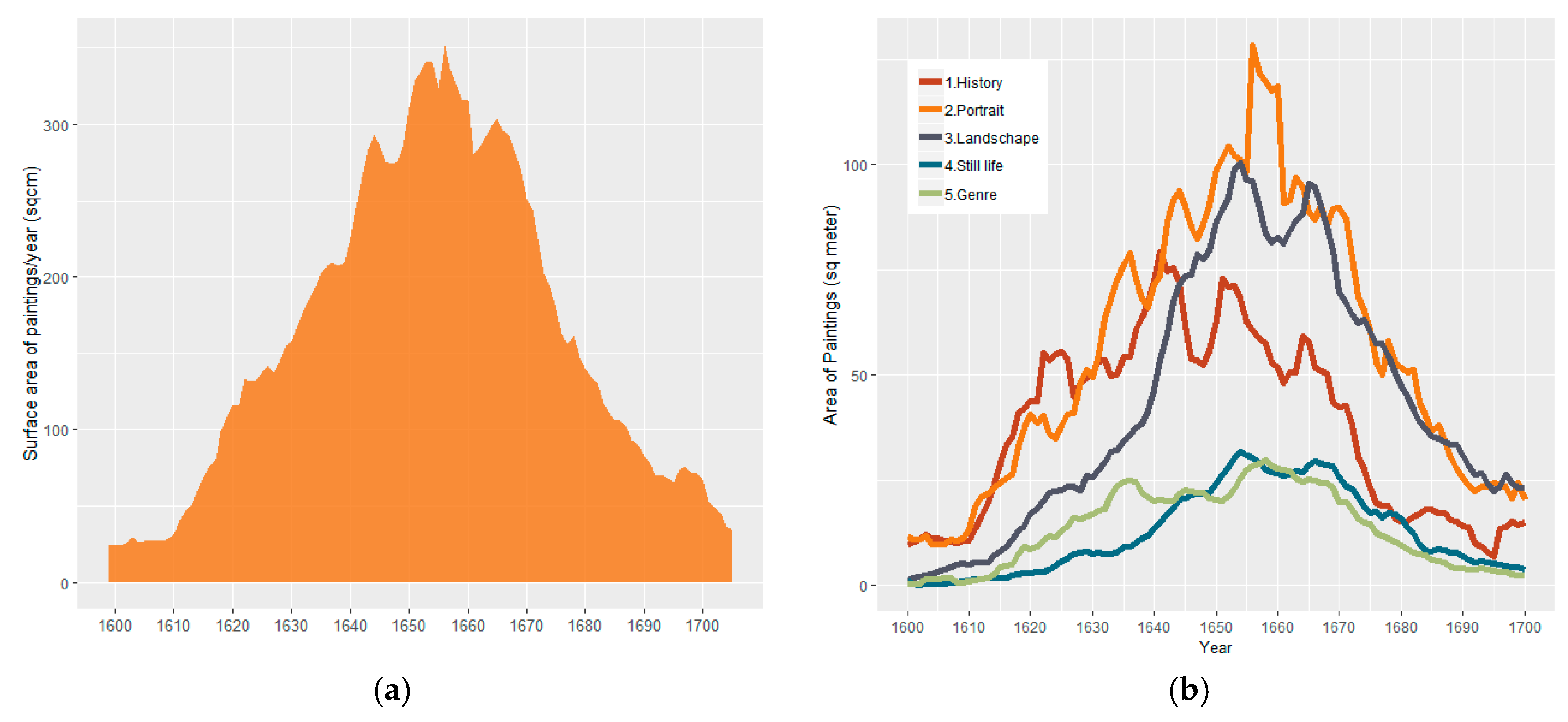

The number of paintings as a measurement of production inevitably overlooks the heterogeneity in paintings: one monumental group portrait is treated the same as a small landscape painting hung above the door. Size, or the area of the painted surface, is known to have a high correlation with the efforts and time spent on painting (Bok 1998). Furthermore, the inventories of dealers sometimes abound the support size with their monetary value (“guilder size”, “26 stuiver size”), pointing out a direct link between size and market value (Bredius 1915–1922, vol. 6). Therefore, I further calculate the production trend using the canvas area based on the width and length measurements recorded in RKDimages (Figure 5a).6 It shows that the production measured by area of the paintings follows the same trend as the production measured by number, with correlation coefficients of 0.95 or higher at the 0.01 significance level for each genre. Yet, the fluctuation in the production measured by size is more volatile, evident in history and portrait paintings (Figure 5b), perhaps due to the fluctuations of commissions. For genres that mainly served the open market (landscape, still life, and genre), the trends are much smoother. Surprisingly, portrait narrowly surpassed the landscape as the most-produced genre. Admittedly, the painted surface area only provides an alternative measurement of painting production. Furthermore, since the surface area is closely correlated with man-hours spent on the painting, this measurement also serves as an indicator for the labor cost of painters. Yet, given the complex and heterogeneous nature of the Dutch art market, this measurement is far from capturing every nuance in the production process. It warrants further investigation into the production measured by surface area separated by different market segments, styles, and techniques.

The meteoric growth of the painting production and the explosive expansion of the Dutch art market shown in Figure 1, Figure 2, Figure 3, Figure 4 and Figure 5 have long propelled scholars to seek the source of its growth and the cause of its collapse. Over the decades, scholars from various fields have done extensive research into this phenomenon and offered numerous, often convincing and sometimes controversial, explanations from various angles. Historians tried the external historical factors such as economic prosperity, population growth, the secularization of demand for paintings, and the influx of skilled craftspeople from the Southern Netherlands (Prak 2008; Bok 2008). Cultural historians used fashion and taste (Fock 2007). Economic historians explored the market conditions and market forces in supply and demand (Bok 1994; Montias 1982). Yet, there are still unaccounted aspects in the existing explanations which are mostly rooted in the neoclassical economic theories of supply and demand. Current explanations fall short in explaining why the painter population kept growing after the market had already become saturated around 1635, and how they managed to break through the stagnation in the absence of internal and external shock. It is worth noting that most existing studies cling to the assumption of homo economicus, which supposes that agents in the art market behaved in exact accordance with their rational self-interest. However, such an assumption has been challenged by behavioral economists who have shed light on the fact that economic agents only have bounded rationality and are subject to the effect of social, psychological, cognitive, and emotional factors (Kahneman and Tversky 1979, 1992, 2013).

The bounded rationality is confirmed by cultural economists that painters and other creative workers in the contemporary cases are willing to settle for a lower income to create more artworks, which is considered irrational in the economic sense (Caves 2000). Furthermore, collectors are often observed to be subject to several cognitive biases (Thaler 1993). These behavioral anomalies, i.e., systematic deviations from the Von Neumann–Morgenstern axioms of rational behavior, are considered to be one of the major characteristics of the contemporary art markets (Frey and Eichenberger 1995; Pesando 1993). In studies of early modern Netherlands, De Marchi and Van Miegroet (1994) have stressed the importance of studying the actual behaviors in the art market using the case of Antwerp. However, the interplay of social, cultural, and psychological underpinnings of the art market have not yet been fully explored to interpret the rise and fall of the painting production. To answer this question that emerged from the data analysis, in Section 5 and Section 6, I will apply behavioral economic theories to show how painters, art dealers, and the public interacted in the art market and created loops of reinforcement, providing a new hypothesis accounting for the unprecedented painting production in the 17th-century Dutch Republic.

5. Becoming a Painter: Expectation and Risk

5.1. Painting as a Promising Profession

Behind the explosive growth of painting production in the first decades of the 17th century was the equally extraordinary rise in the painters’ population, disproportionate to the overall population growth. Rasterhoff (2017) estimated that the average number of painters per 10,000 inhabitants in the ten largest cities in the Dutch Republic almost doubled from 7.9 in the 1610s to 14.9 in the 1640s, and the absolute number of painters active in the Dutch Republic grew seven-fold. By 1630, painting as a profession had already attracted aspiring painters even from well-to-do families with no background in artistic trades, such as Rembrandt’s successful pupil Ferdinand Bol, who was born into a surgeon family (Sluijter 2015). Scholars have noted the long tradition of regarding painting as a respectable trade, which by itself, cannot fully explain the attractiveness of a painting career outside artist and artisan circles (Montias 1982). What else may have attracted so many young men to venture into the painting business?

Since the publication of Karel van Mander’s Lives in 1604, the painter profession was buttressed with a respectable history filled with illustrious “old masters,” reassured by Hendrik Hondius Effigies (1610) and Anthony van Dyck’s Iconography (1630) that portrayed the famous artists. These books and print series seemed to promise each painter the chance to attain a similar status as their predecessors. The painting profession was glorified with public endorsements from numerous laudatory poems dedicated to painters. Famous painters were included in several prestigious city descriptions as a part of the city’s pride.7 In 1642, Philips Angels published De Lof der Schilderkunst, claiming that the art of painting deserves even more praise than that of poetry, as painting is far more “profitable and useful” (profijtelicker en nutter) and can make good money for the artists and his family (Angel 1642).8 All of these publications may have boosted the expectations of painting as a liberal art and elevated the expectation of painting as a profession within and outside the artistic circles. The more people that became painters, the more stories of successful artists appeared, which attracted even more aspiring painters and produced even more stories of success—a positive feedback loop was formed.9

In addition to the potential gain in fame and social status, economic incentives also played a role. An established master painter could expect to earn somewhere between 1000 and 2500 guilders per year, favorable when compared to the income of masters in many other trades (Montias 1982). Apart from the higher average income, certain painters were able to acquire such wealth and social status through painting that they could marry the Burgomaster’s daughter, as in the case of Corstiaen van Couwenbergh in Delft (Montias 1982). Some painters in the 17th-century Dutch Republic seem to have high, if not excessive, expectations towards the value of their work and hence, as Boers-Goosens (2006) shows, demanded exorbitant prices. The marine painter Hendrick Cornelisz Vroom once quoted an astonishing fee of fl. 6000 for a large marine painting for the Amsterdam Admiralty, and the celebrated portrait painter Bartholomeus van der Helst tried to charge fl. 1000 for a family portrait, while 80% of the population earned less than fl. 600 per year (Boers-Goosens 2006). Rembrandt even wrote to Constantijn Huygens, the stadtholder’s secretary, to demand a higher price for his Passion Series made for the stadtholder. Even though this excessive expectation of the price of paintings was often turned down, as in Boers-Goosens’s examples (2006), the rare but successful stories of high charges were perhaps circulated among artists and other agents in the market, tempting the aspiring artists to believe they can do the same.

The superstardom of successful painters made the promised reward for painting so alluring that it may well have stimulated the enthusiasm towards this profession as a shortcut to wealth and status, even though the chance was slim. Ferdinand Bol, after climbing the social ladder through his brushes and palette and finally married to a wealthy widow, retired from painting (Sluijter 2015). But very few, if any, painters were able to copy Bol’s success. Tempted by the elevated expectation of the profession, more and more aspiring painters joined workshops of the successful masters in different cities, like that of Rembrandt in Amsterdam, Abraham Bloemaert in Utrecht, Gerard Dou in Leiden, and Frans Hals in Haarlem, learning the art of painting. Rasterhoff (2017) called the masters’ studios “incubators”; perhaps they can also be called dream-factories—where the apprentices line up hoping to become great masters in their own right and enjoy the same social and economic success of their masters. Even some painters who worked for the lower-end of the art market also fared very well in the financial terms—even better than their more famous peers. Jan Micker, who painted staffage for many cheap landscape paintings, owned a house on the Prinsengracht opposite the Noordermarkt, and another 1/3 of a house in the Langestraat nearby, both of which were prime locations at that time (Bredius 1915–1922, volume 1; Sluijter 2015). Around the same time, the prominent still life painter, Willem van der Aelst, could only afford to rent two bovenkamers (upper rooms) in Bloemgracht, a working-class area in Jordaan in Amsterdam (Bredius 1915–1922, vol. 7).

Nonetheless, an expanding market with an increasing production usually leads to swelling competition and a diminishing marginal return. As early as the 1610s, competitive pressure in the Dutch art market intensified to the extent that local artists complained to the guild or demanded the establishment of new guilds to protect their privileges (Sluijter 1994; De Marchi 1995). These petitions from artists reveal the other side of the glorified painting profession—a competitive business full of uncertainty and risk (Dempster 2014). The enthusiasm and high expectations from the upper layer of the art market may have triggered a ripple effect to the lower segment of the art market with the help of the enthusiastic public who avidly collected paintings (to be discussed in Section 6), attracting young men to this lucrative and possibly promising trade.

5.2. Painting as a Risky Business

Becoming a painter involved considerable cost and significant risks. It was a very costly undertaking for the parents to pay for the full six years of apprenticeship required by the Guild of St. Luke. During his lengthy training, the apprentice was a sheer financial burden to his family, as hardly any income was generated, as opposed to most other kinds of trades in which the apprentice would do practical labor, producing goods and earning an income right away.10 Montias (1982) estimated that pupils who lived at home paid anywhere from fl. 20 to fl. 50 per year to their masters as tuition, while those living with their masters were charged between fl. 50 and fl. 100 (board and tuition), depending on the reputation of the master and the age and previous education of the pupil. Famous masters like Rembrandt charged a tuition fee up to fl. 100 per year, which is a considerable cost to ambitious pupils who expected a prosperous career. More importantly, this costly investment in education was no guarantee for becoming a skilled and artistic craftsman: Many apprentices never became independent masters, and, as a result, often disappeared from the records (Boers-Goosens 2001).11 Pieter Cosijn (1630–?) paid fl. 350 to study with the Hague portrait painter Pieter Nason for a year and then got training in Antwerp at a rate of fl. 255 per year (Jager 2016). In spite of the huge investment in his training, Cosijn had no success in his trade and his wife ended up pleading with an orphanage that her husband could not feed his own children (Jager 2016).

However, the risk of embarking on a career as a painter is not limited to the topmost layer of the market. Apprenticeships at all levels involved financial risks to a varying degree depending on the cost of training. Aspiring painters and their families seem to have been aware of the risks and usually took smaller risks first by choosing less famous masters first—even Gerard Dou did not start his training with Rembrandt, but first with less-famous and thus less expensive painters before gradually advancing to better and often more expensive masters.

Even if the apprentice eventually became an independent master, the return on investment of training is still far from certain, since paintings are luxury goods, rather than substances, for which the demand is closely related to the economic situation. This uncertainty and dependency on external circumstances make professional painters vulnerable during times of economic downturn. Scholars have observed that many painters went bankrupt or died in poverty after the wars broke out (Bok 1994; Crenshaw 2006). Besides, the specialized training for some painters even exacerbates such a risk, as their painting skills are not versatile enough to adapt to the changes in the market. Houbraken (1718–1721, vol. 1) tells us an anecdote of the Utrecht fish still life painter, Jacob Gillig (1636–1701), who, after the Rampjaar of 1672 when the demand for his still life paintings vanished, tried to paint portraits, but was rejected by the sitter for the lack of likeness.

Furthermore, the lack of clarity in the development of taste and preference in the first half of the 17th century added even more uncertainties; and the art market, according to Nijboer (2010), was subject to a permanent state of “crisis.” Painters who produced paintings on spec, were even more vulnerable to the financial risk as they had to invest upfront, not only to pay for the painting materials but also for their opportunity cost of labor consumed. Many painters got into debt and encountered financial troubles, and some of them, including Rembrandt, went bankrupt (Crenshaw 2006; Rasterhoff 2017).12

Professional art dealers, who became more common in the 1630s and 1640s, were able to hedge some of the risks for the painters; yet they also reaped all surplus realized in the market. Art dealers were very much aware of the risks and tried to manage it as Van Miegroet and De Marchi (2012) demonstrated using the case in Antwerp. Beyond the normal business of buying and selling, dealers sometimes ordered works from artists in advance, agreed to pay a fixed fee for the artists’ production during an agreed time, or even operated a “galley,” getting artists to work for a fixed salary (Montias 1987, 1988; Bredius 1891).13 For artists, the dealers took a substantial part of the risk off their shoulders by acquiring their works in advance, and at the same time tied their hands and capped their profits.14

5.3. Decisions under Risk and Uncertainty

With the substantial cost and risk topped with the fierce competition in the art market, the economic man with the perfect, logical, deductive rationality, as assumed in neoclassical economics, would hesitate to take on the painting profession after the 1610s. However, Rasterhoff (2017) observed that the proportion of newcomers to total active painters started to increase in the 1620s without apparent grounds for a surge in demand for paintings while the economy wavered after the war resumed in 1621 (Goldgar 2007). Previous historians explained it as a result of the expectation of future demand (Bok 1994). However, this rational assumption cannot fully account for the inordinate tolerance to the risks brought by the costly investment and highly competitive and ever-changing art market. In fact, the painting production (Figure 1 and Figure 5a) seems to have slowed down in the 1620s and stagnated in the 1630s.

Risk and uncertainty, as behavioral economists have illuminated over the past decades, affect human decision-making in a way that consistently diverges from neoclassical economic theories under the homo economicus assumption (Kahneman and Tversky 1979, 1992, 2013; Thaler and Sunstein 2008). Behavioral observations on decision-making can be traced back to Daniel Bernoulli’s experiment in 1738, in which Bernoulli illuminated the bounded rationality of human nature (Bernoulli [1738] 1954; Kahneman and Tversky 1984). The influential prospect theory developed by Kahneman and Tversky (1979, 1992) arises as a descriptive model not only complicating Bernoulli’s experiments, but also verifying the consistency of human behavior across time and culture. In particular, prospect theory points out exactly where Bernoulli’s risk-averse utility model fails—when individuals are amid a crisis (Kahneman and Tversky 1992), a state which Nijboer (2010) used to describe the 17th-century Dutch art market. Prospect theory further explicates that decision-makers tend to take unreasonably high risks and reject favorable settlements when the promised gain is significant even though the chance of winning is very slim. Decision-makers often overrate small probabilities of winning and underrate large probabilities of losing, exhibiting non-linear probability estimation in the face of risk and uncertainty (Kahneman and Tversky 2013).

Even though prospect theory was developed from highly controlled experiments conducted in the modern Western world, their observations, such as the bounded rationality of human nature and the reduction in risk-aversion, were very present in the early modern Dutch Republic as we can observe from the notorious tulip mania and numerous legal and illegal lotteries spread across the entire country. Many aspects of the early modern Dutch economy echo the modern Western world. At the beginning of the 17th century, modern financial institutions like bank and stock exchange were established, and the derivatives and securities market was developed, revealing the capitalist root of the Dutch Republic (Petram 2014). Petram (2014) further suggests the derivative market tempted the traders to take unbearable risks, like entering into a forward contract with no upfront payment with a prospect of possible profit. It was the exact same reason that triggered the 2008 financial crisis. Not to mention the fast and convenient public transportation system (trekvaart) which connected the whole country, smoothing the commercial activities and facilitating the flow of information (De Vries 1978). It is no wonder De Vries and Van der Woude (1997) claimed that the 17th-century Dutch Republic was the first modern economy. Therefore, given the consistent observations of bounded rationality from Bernoulli to Kahneman, and the higher level of risk tolerance present in the capitalist, “modern” Dutch economy, prospect theory should be applicable, as a theoretical framework, to understand the behaviors observed in the 17th-century Dutch art market.

The world of painting is considered an economy of superstars wherein relatively small numbers of people earn enormous amounts of money and dominate the activities in which they engage (Rosen 1981; Caves 2000). Employing the Prospect Theory, I would argue that aspiring painters, attracted by the glorified rewards of the superstar painters, may have overestimated the chance of becoming a superstar themselves and underestimated the much larger possibility of ending up like the distressed painter in Adriaen Both’s drawing, who sits on a basket in ragged clothes with his family shivering in poverty (Figure 6).

This behavioral hypothesis of the expansion of the art market does not deny the factors of the increase in purchasing power and demand or the fashion of collecting paintings that previous research elucidates. Rather, as I will show below, it was exactly the society-wide enthusiasm towards paintings that kept feeding the aspiring painters with the promise of legendary rewards and reinforcing the painters’ belief in reaching superstardom in their own right.

6. Collective Enthusiasm and Wide-Spread Endorsement

Dutch society, at least in certain segments, in the words of Eric Jan Sluijter (1991), “showed an incredible avidity for paintings.” A substantial number of households in inventories drawn in Leiden between 1625 and 1675 had between 100 and 250 paintings in their collections (Sluijter 1991). An increase in purchasing power is surely an important factor; so are taste and fashion for interior decoration. Yet, hundreds of paintings were far beyond the necessity to fill the blank walls of the houses. The nouveau riche—the affluent merchant class—may have imitated each other and mimicked members of higher status, displaying strong herd behaviors towards collecting paintings (Veblen [1899] 1934). French writer and philosopher Samuel Sorbière observed an “excessive interest in paintings” (l’excessive curiosité pour les peintures) during his sojourn in the Dutch Republic during the 1640s (Martin 1901) and Constantijn Huygens wrote around 1630 in his childhood memoirs that people were “presently” confronted with paintings everywhere (Huygens 1987). Laudatory poems were versed around the famous collections of paintings, publicly endorsing both artists and their collectors. “Here is the stock exchange and the money, and the love of art” (Hier is de beurs en ‘t geld en liefde tot de kunst), wrote Thomas Asselijn in 1653 for a festive occasion in Amsterdam where painters, poets, and art lovers gathered. This line underlines the city’s pride in its flourishing community of not only artists but also art lovers. The frenzy was in the air.

The collective enthusiasm is not limited to collecting arts: Scholars have observed from the surviving diaries of art lovers that it was a common practice for artists and art lovers to visit shops of painters and art dealers, to call on burghers with well-known collections, and to go to numerous auctions and fairs (Sluijter 2015; Roodenburg 2006). Houbraken (1718–1721, vol. 1) tells us the anecdote of Rembrandt being visited by art lovers while still living with his parents in Leiden. Pieter Codde’s painting of 1630 captures one of such visits to an artist’s studio (Figure 7).

Eventually, the hype trickled down to the lower segments of the society as captured in the English merchant Peter Mundy’s travel account of 1640, which tells of butchers, bakers, blacksmiths, and cobblers “all in generall striving to adorn their houses, especially the outer or street roome, with costly peeces” and “such is the generall Notion, enclination and delight that these Countrie Natives have to Paintings” (Mundy 1925). One year later John Evelyn, another English traveler, described a jaarmarkt (annual market) in Rotterdam where “it is an ordinary thing to find a common farmer lay out two or three thousand pounds in this commodity [paintings]. Their houses are full of them, and they vend them at their fairs to very great gains” (Evelyn [1641] 2005). Mundy and Evelyn’s words may be an exaggeration, but it is clear that the lower segment of society was also actively involved in consuming and trading works of art as observed in the probate inventories (Montias 1996).

This enthusiasm for paintings from the public seems to have resulted in unreasonable investments, as Jacques de Ville in his pamphlet bristled at the art lovers who marveled at and paid excessive sums for paintings which did not possess a “good symmetry” (Sluijter 2015). Even though, unlike buying tulips, buying paintings was not harshly criticized as an act of folly by the contemporary writers, this collective enthusiasm for paintings prevailing in the Dutch Republic cannot be fully regarded as an act of rationality. It is perhaps why Jeremias de Decker (1610–1666), in his late brother’s memorial poem, proudly stated that he was “into tulips, shells, paintings, /never [being] foolish or got lost” (Aan tulpen, schulpen, schilderijen/Nooit zottelijke en heft verkwist), putting buying painting on a par with the infamous tulips (Engelberts Gerrits 1844). This wide-spread avidity for paintings can hardly be justified by pure economic reasoning and therefore cannot be fully explained by the neoclassical economic theories.

In spite of De Ville’s warnings, the public still spent a fortune on paintings through various channels, such as bidding in auctions. Montias (2002) summarized over 500 auction sales from 1597 to 1638 held in the Orphan Chamber alone, where almost 10,000 paintings were auctioned off, fetching more than 80,000 guilders. Interestingly, of the buyers in Montias’s sample, nearly one third were merchants who were involved in international trade and were no strangers to risks and uncertainty by trade. In addition to their greater purchasing power, the merchant’s mentality, and risk-seeking aptitude may explain their high representation in auctions while the affluent people in liberal professions (medical doctors, attorneys, and preachers) account for only around 3% of the total buyers.

Besides bidding in auctions, buyers of paintings also took part in more exciting and entertaining events such as lotteries, dice games, and shooting competitions offering paintings among the prizes as witnessed in Buytewech’s drawing of a crowd attracted by the lottery (Figure 8)—clearly painters were not the only ones who were willing to bet on paintings. The lottery events were sometimes celebrated with a huge Landjuweel or pageant, organized by the local rhetorician’s chamber, an occasion where the lottery tickets with their identification “rhymes” (verses or mottos) were read out loud to the public (Bok 2008). The almost 25,000 rhymes that survive from the Haarlem lottery of 1606 offer a solid testimony to the popularity of such events and the widespread endorsement of the sales of art throughout the society.

Poets and art-lovers composed countless verses praising arts; collectors flooded their collections with paintings; governments commissioned painters to paint prestigious works for public display, and consumers from all segments of society decorated their rooms with paintings. Although none of these behaviors are new to scholars, taken together, the direct and indirect social interactions among painters, poets, art-lovers and other members of the society forged into positive feedback loops topped by the psychological craze were a powerful force that amplified the invisible hand of the market and pushed up the painting production to an unstable stage which cannot be justified by an increase of demand.

7. Art Market as a “Social Bubble”

To explain the phenomenal growth in painting production and the abnormal behavior observed in various agents in the art market in the first half of the 17th century, I would like to introduce the concept of “social bubble,” a term coined by Didier Sornette and Monika Gisler (Gisler and Sornette 2008). The concept brings together the social and behavioral underpinnings of the art market, different from existing studies on the art market bubbles that focus on the speculative bubble revealed in the price of artworks fetched in the contemporary auctions (c.f. Kräussl et al. 2016).15 A social bubble is defined as “strong social interactions between enthusiastic supporters weave a network of reinforcing feedbacks that lead to widespread endorsement and extraordinary commitment by those involved, beyond what would be rationalized by a standard cost–benefit analysis in the presence of extraordinary uncertainties and risks.” Social bubbles are characterized by “collective over-enthusiasm as well as unreasonable investments and efforts, derived through excessive public and/or political expectations of positive outcomes associated with a general reduction of risk aversion” (Gisler and Sornette 2009). In the 17th-century Dutch Republic, these features of “social bubble” are clearly present. As mentioned in the previous sections, various agents in the art market reinforced positive feedbacks through their direct or indirect interaction and created a society-wide avidity for paintings that built up the expectation of return and caused neglect of risk. The explosive growth in the painter population and the painting production in the Dutch Golden Age observed in Figure 1, Figure 2, Figure 3, Figure 4 and Figure 5 can be likened to an emerging bubble, which is inherently vulnerable to endogenous and exogenous shocks. In the 1650s, the painting production started to show signs of instability and eventually plunged around 1660—the bubble burst.

The contemporaries attributed this downturn in the art market to changes in taste and a revived interest in old masters, as well as the fallout of the Franco-Dutch war (1672–1673) and the preceding Anglo-Dutch wars (1652–1654, 1665–1667) (Bok 1994; Montias 1987). More recent studies linked the decline of the art market to the structural overproduction of paintings in the first decades and the market impact of second-hand paintings (Bok 2001). I would like to add another hypothesis that the preference for old (deceased) masters and the return of their works to the market ruptures the positive feedback—more young artists in the market no longer produced more celebrated artists and therefore could not attract more newcomers. As a result, I argue that the illusion of the increasing return dissipated, the over-optimism and the excessive expectation of rewards from painting were corrected, and the artists and other agents returned to the risk avoidance. In other words, the market started to correct itself and returned to a stable, mature state. The increasing competitive pressure in the art market accumulating from the first half of the 17th century may have helped the development of a more complex, segmented, and heterogeneous market that we witness during the contraction. The market stratification and occupational differentiation that took place in the last quarter of the 17th century suggest a mature market (Rasterhoff 2017). From a system point of view, a downturn after an unstable exponential growth in painting production and painter population is unavoidable; the cycle of exponential development punctuated by corrections and crashes can also be observed in other complex systems (such as the financial markets and earth ruptures) (Sornette 2008). Social bubbles, per Sornette’s definition, are non-sustainable transient regimes that end at a tipping point, beyond which a new regime is established. The new phase can be a crash followed by revulsion, or simply a plateau or slow decrease of the market (Sornette 2017).16 As seen in Figure 1, after the 1680s, the rate of decline slowed down. Given the unstable state of the art market after the exponential growth, I argue that the downturn could have happened anytime, depending on the timing of internal (change in fashion) or external shocks (wars). It could have even grown further had there been major innovations, although the risk of a fall would have grown with it. But the downturn is inevitable—a complex system like the art market will correct its earlier deviation from the stable state by way of decline or plummet, not only in the art market but perhaps also in other sectors of the Dutch economy (De Vries and Van der Woude 1997).

8. Exuberant Innovation

Besides the explosive growth in painting production, the Dutch art market in the Golden Age is known for its high quality and vigorous innovations of new genres and techniques (Rasterhoff 2017; Prak 2008). The historical and socioeconomic circumstances were favorable to the flourishing of arts, but it has long puzzled scholars where exactly the auspicious circumstances and the artistic geniuses crossed paths. The social bubble hypothesis may provide new insights.

As mentioned before, during bubbles, people take inordinate risks that would not otherwise be justified by standard cost–benefit considerations. Their risk-taking behavior is temporarily rationalized by speculating on the market, fueled by positive feedbacks and herding behavior, and amplified by a wide-spread public endorsement. In this context, people dare to explore new opportunities, many of them unreasonable, a fertile ground for the emergence of outstanding achievements. Alan Greenspan, the former U.S. Federal Reserve Board chairman, described bubbles as “irrational exuberance.” I conjure that it was this “irrational exuberance” in the art market in the first half of the 17th century that led to exuberant innovations—a great number of radical innovations breaking existing traditions in terms of iconography, technique, and composition (Rasterhoff 2017; Li 2018). New genres and new styles were explored and were introduced to the market. Many of the innovations did not survive the market competition, and we can only detect them from the notaries’ descriptions of paintings in the probate inventories (Falkenburg 1997; Li 2018). Besides the product and process innovations that Montias (1990, 1987) described, Rasterhoff (2017) further added the innovations in marketing strategy in the first half of the 17th century. More importantly, this collective over-enthusiasm seems to have compounded the “slices of genius” of individual artists into a “collective genius,” which could have accelerated the innovation process in the development of art as it often does in business (Hill et al. 2014).

The burst of the social bubble also marks a significant shift in the scale and form of innovation. Li (2018) illustrates that the iconographies used in history paintings shrunk after 1660. Furthermore, recent studies on the high-life genre paintings show that the innovations in the last quarter of the 17th century fall back to a small circle of interconnected artists who resorted to very limited and highly repetitive repositories and provoked the connoisseurs to discern their distinctions made through innovative painting techniques (Ho 2017; Gifford and Glinsman 2017). Clearly, the large-scale, diverse, exuberant explorations in all levels of the market during the bubble subsided into the delicate variation of novel techniques in the upper segment of the market after the burst of the social bubble. 18th-century art critics such as Arnold Houbraken, Johan van Gool, and Jacob Campo Weyerman acknowledged the artistic decline in the second half of the 17th century (Houbraken 1718–1721; Van Gool 1750–1751; Weyerman 1729–1769).

Sornette argued that bubbles “break the stalemate of society resulting from its tendency towards stronger risk avoidance.” Social bubbles, he further suggested, are “essential carriers for pushing segments or even sometimes the whole of society to invest considerable efforts in very risky endeavors that bring enormous rewards decades later” and “an absence of bubble psychology would lead to stagnation and conservatism as no large risks are taken and, as a consequence, no large return can be accrued” (Gisler and Sornette 2008). Beyond the art market, this “bubble psychology” or risk-taking attitude was evident and omnipresent in the Dutch society built on the craft- and trade-economy (Goldgar 2007). Therefore, I dare to conjure that the Dutch Golden Age was built on this principle, not only in the art market but also in other sectors of the cultural industry as well as in commerce as the Dutch East Indian Company (VOC)’s share price also witnessed the same surge-and-plunge cycle over the same time period (Petram 2014). The application of the social bubble hypothesis to other sectors of the Dutch economy warrants further investigation.

9. Conclusion

This research analyzes and visualizes the fluctuations of painting production in the 17th-century Dutch Republic using the surviving or known paintings in RKDImages as an indicator. The trend of overall painting production correlates with the expansion and contraction trend in painters’ population, indicating an explosive growth followed by a steep decline all within decades in the 17th century. I further examine the production trend by major genres showing each genre had its own development pattern yet contributed to the same overall trend. I also probe an alternative way to quantify production—canvas area—as opposed to the number of paintings. In this metric, although following the similar growth-decline trend, portraits surpassed landscape and ranked first as the most-produced genre.

Economic art historians have tried to explain the short but intense flowering of the Dutch art market within the framework of neoclassical economic theories. This research challenges their basic assumption that painters made their decisions rationally according to the market condition by introducing the idea of cognitive biases and irrational risk-taking borrowed from behavioral economics and studies in complex systems. Breaking down the homo economicus assumption, I suggest applying the “social bubble” hypothesis to the phenomenon and identify the presence of the essential characteristics of such bubbles in the art market in the Dutch Republic like over-enthusiasm, wide-spread public endorsement, unrealistic expectations of return, herding/imitation, and inordinate risk-taking. All agents in the society created a network of reinforcing feedbacks that drove up the painting production. Although the endogenous instability during the bubble led to the anticipated fall, the inordinate risk-taking behavior had led to exuberant artistic innovations that highlighted the Dutch contribution to the development of art. Without the collective enthusiasm and risk-taking attitude, artistic innovations would probably not have taken place within such a short period. The social bubble and the suspension of rationality may have played a significant role in the flourishing of the Dutch art market and other sectors of Dutch society in the 17th century.

Funding

This research received no external funding.

Acknowledgments

This article came from one chapter of my Master’s thesis. I am grateful to my thesis advisor, Marten Jan Bok, for his generous support throughout my studies. I would like to thank Julia Noordegraaf, Claartje Rasterhoff, and Ivan Kisjes, among other colleagues from the CREATE project at the University of Amsterdam, for supporting the early development of my research. I wish to thank the anonymous reviewers and both editors of this Special Issue for their constructive comments and suggestions. My appreciation also goes to Thomas Jeremy Tait who provided helpful editing of my drafts.

Conflicts of Interest

The author declares no conflict of interest.

References

- Alpers, Svetlana. 1983. The Art of Describing: Dutch Art in the Seventeenth Century. Chicago: University of Chicago Press. [Google Scholar]

- Angel, Philips. 1642. De Lof der Schilderkunst. Leiden. [Google Scholar]

- Haverkamp-Begemann, Egbert. 1968. Hercules Seghers. Art and Architecture in the Netherlands. Amsterdam: J. M. Meulenhof. [Google Scholar]

- Bernoulli, Daniel. 1954. Exposition of a New Theory on the Measurement of Risk. Econometrica 22: 23–36. First published 1738. [Google Scholar] [CrossRef]

- Boers-Goosens, Marion. 2001. Schilders en de markt, Haarlem 1600–1635. Ph.D. Dissertation, Universiteit Leiden, Leiden, The Netherlands. [Google Scholar]

- Boers-Goosens, Marion. 2006. Prices of Northern Netherlandish Paintings in the Seventeenth Century. In His Milieu: Essays on Netherlandish Art in Memory of John Michael Montias. Edited by Amy Golany. Amsterdam: Amsterdam University Press, pp. 59–71. [Google Scholar]

- Bok, Marten Jan. 1994. Vraag en aanbod op de Nederlandse kunstmarkt, 1580–1700. Ph.D. Dissertation, Utrecht Universiteit, Utrecht, The Netherlands. [Google Scholar]

- Bok, Marten Jan. 1998. Pricing the Unpriced. How Dutch 17th-Century Painters determined the Selling Price of their Work. In Art Markets in Europe, 1400–1800. Edited by Michael North and David Ormrod. Aldershot: Routledge. [Google Scholar]

- Bok, Marten Jan. 2001. The Rise of Amsterdam as a cultural center: the market for paintings, 1580–1680. In Urban Achievement in Early Modern Europe: Golden Ages in Antwerp, Amsterdam and London. Edited by Patrick O’Brien. Cambridge: Cambridge University Press, pp. 186–209. [Google Scholar]

- Bok, Marten Jan. 2002. Fluctuations in the Production of Portraits made by Painters in the Northern Netherlands, 1550–1800. In Economia e Arte, Secc. XIII-XVIII. Edited by Simonetta Cavaciocchi. Atti delle Settimane di Studi e altri Convegni. Prato: Istituto Internazionale di Storia Economica F. Datini, pp. 649–62, Data see Appendix I, pp. 654–61. [Google Scholar]

- Bok, Marten Jan. 2008. ‘Paintings for Sale’: New Marketing Techniques in the Dutch Art Market of the Golden Age. In At Home in the Golden Age. Edited by Jannet de Goede and Martine Gosselink. Rotterdam: Kunsthal, Zwolle: Waanders, pp. 9–29. [Google Scholar]

- Bredius, Abraham. 1891. De kunsthandel te Amsterdam in de 17e eeuw. Amsterdamsch Jaarboekje, 54–72. [Google Scholar]

- Bredius, Abraham. 1915–1922. Künstler-Inventare, Urkunden zur Geschichte der holländische Kunst des XVIten, XVIIten und XVIIIten Jahrhunderts. 7 vols, The Hague: Nijhoff. [Google Scholar]

- Brosens, Koenraad, and Katlijne Van der Stighelen. 2002. Paintings, prices and productivity: lessons learned from Maximiliaan de Hase’s Memorie boeck (1744–80). Simiolus: Netherlands Quarterly for the History of Art 36: 173–83. [Google Scholar]

- Caves, Richard Earl. 2000. Creative Industries: Contracts between Art and Commerce. Cambridge: Harvard University Press. [Google Scholar]

- Crenshaw, Paul. 2006. Rembrandt’s Bankruptcy: The Artist, His Patrons, and the Art Market in Seventeenth-Century Netherlands. Cambridge: Cambridge University Press. [Google Scholar]

- De Jager, Ronald. 1990. Meester, leerjongen, leertijd: Een analyse van zeventiende-eeuwse Noord-Nederlandse leerlingcontracten van kunstschilders, goud- en zilversmeden. Oud Holland 104: 69–111. [Google Scholar]

- De Marchi, Neil. 1995. The role of Dutch auctions and lotteries in shaping the art market (s) of 17th century Holland. Journal of Economic Behavior & Organization 28: 203–21. [Google Scholar]

- De Marchi, Neil, and Hans Van Miegroet. 1994. Art, Value, and Market Practices in the Netherlands in the Seventeenth Century. The Art Bulletin 76: 451–64. [Google Scholar] [CrossRef]

- De Marchi, Neil, and Hans Van Miegroet. 2006. The History of Art Markets. In Handbook of the Economics of Art and Culture 1. Edited by Victor A. Ginsburg and David Throsby. Amsterdam: North Holland, pp. 69–122. [Google Scholar]

- De Marchi, Neil, and Hans J. Van Miegroet. 2014. Supply-demand imbalance in the seventeenth-century Antwerp-Mechelen paintings market. In Moving pictures: intra-European trade in images, 16th-18th centuries. Edited by Sophie Raux, Neil De Marchi and Hans. J. Van Miegroet. Turnhout: Brepols Publishers, pp. 37–76. [Google Scholar]

- De Moor, Tine, and Jaco Zuijderduijn. 2013. The Art of Counting: Reconstructing Numeracy of the Middle and Upper Classes on the Basis of Portraits in the Early Modern Low Countries. Historical Methods: A Journal of Quantitative and Interdisciplinary History 46: 41–56. [Google Scholar] [CrossRef]

- De Vries, Jan. 1978. Barges and Capitalism: Passenger Transportation in the Dutch Economy, 1632–1839. Wageningen: A.A.G. Bijdragen. [Google Scholar]

- De Vries, Jan. 1991. Art history. In Art in History/History in Art: Studies in Seventeenth-Century Dutch Culture. Edited by David Freedberg and Jan de Vries. Santa Monica: Getty Center for Art History and the Humanities, pp. 331–72. [Google Scholar]

- De Vries, Jan, and Ad Van der Woude. 1997. The First Modern Economy: Success, Failure, and Perseverance of the Dutch Economy, 1500–1815. Cambridge: Cambridge University Press. [Google Scholar]

- Dempster, Anna M., ed. 2014. Risk and Uncertainty in the Art World. London, New Dehli, New York and Sydney: Bloomsbury Publishing. [Google Scholar]

- Engelberts Gerrits, Gerrit. 1844. Schoonheden uit de Nederlandsche Dichters. Amsterdam: Ten Brink & De Vries, vol. I. [Google Scholar]

- Evelyn, John. 2005. The Diary of John Evelyn. Cambridge: Cambridge University Press, vol. 3. First published 1641. [Google Scholar]

- Falkenburg, Reindert L. 1997. Onweer bij Jan van Goyen. Artistieke wedijver en de markt voor het Hollandse landschap in de 17de eeuw. Nederlands Kunsthistorisch Jaarboek 48: 117–61. [Google Scholar] [CrossRef]

- Fock, C. W. 2007. Het interieur in de Republiek 1670–1750: een plaats voor schilderkunst? In De Kroon op het Werk: Hollandse Schilderkunst 1670–1750. Edited by Ekkehard Mai, Sander Paarlberg and Gregor J. Marlies Weber. Keulen, Dordrecht and Kassel: Keulen Verlag Locher, pp. 63–84. [Google Scholar]

- Frey, Bruno S., and Reiner Eichenberger. 1995. On the Rate of Return in the Art Market: Survey and Evaluation. European Economic Review 39: 528–37. [Google Scholar] [CrossRef]

- Gifford, E. Melanie, and Lisha Deming Glinsman. 2017. Collective Style and Personal Manner: Materials and Techniques of High-Life Genre Painting. In Vermeer and the Masters of Genre Painting: Inspiration and Rivalry. Edited by Adriaan E. Waiboer, Arthur K. Wheelock Jr. and Blaise Ducos. New Haven and London: Yale University Press, pp. 65–83. [Google Scholar]

- Gisler, Monika, and Didier Sornette. 2008. ’Bubbles in Society’—The Example of the United States Apollo Program. May 30. Available online: https://ssrn.com/abstract=1139807 (accessed on 24 April 2018).

- Gisler, Monika, and Didier Sornette. 2009. Exuberant innovations: The Apollo program. Society 46: 55–68. [Google Scholar] [CrossRef]

- Goldgar, Anne. 2007. Tulipmania: Money, Honor, and Knowledge in the Dutch Golden Age. Chicago: Chicago University Press. [Google Scholar]

- Hill, Linda, Greg Brandeau, Emily Truelove, and Kent Lineback. 2014. Collective Genius: The Art and Practice of Leading Innovation. Cambridge: Harvard Business Review Press. [Google Scholar]

- Ho, Angela. 2017. Creating Distinctions in Dutch Genre Painting: Repetition and Invention. Amsterdam: Amsterdam University Press. [Google Scholar]

- Van Hoogstraten, Samuel. 1678. Inleyding tot de Hooge Schoole der Schilderkonst, Rotterdam. Rotterdam. [Google Scholar]

- Houbraken, Arnold. 1718–1721. De groote schouburgh der Nederlantsche konstschilders en schilderessen. 3 vols, Amsterdam. [Google Scholar]

- Huygens, Constantijn. 1987. Mijn jeugd. Edited by Christiaan Lambert Heesakkers. Amsterdam: Querido. [Google Scholar]

- Israel, Jonathan. 1997. Adjusting to Hard Times: Dutch art during its period of crisis and restructuring (c. 1621–c. 1645). Art History 20: 449–76. [Google Scholar] [CrossRef]

- Jager, Angela. 2016. ‘Galey-schilders’ en’dosijnwerck’: De productie, distributie en consumptie van goedkope historiestukken in zeventiende-eeuws Amsterdam. Ph.D. Dissertation, University of Amsterdam, Amsterdam, The Netherlands. [Google Scholar]

- Kahneman, Daniel, and Amos Tversky. 1979. Prospect Theory: An Analysis of Decision under Risk. Econometrica 47: 263. [Google Scholar] [CrossRef] [Green Version]

- Kahneman, Daniel, and Amos Tversky. 1984. Choices, Values and Frames. American Pyschologist 39: 341–50. [Google Scholar] [CrossRef]

- Kahneman, Daniel, and Amos Tversky. 1992. Advances in prospect theory: Cumulative representation of uncertainty. Journal of Risk and Uncertainty 5: 297–323. [Google Scholar]

- Kahneman, Daniel, and Amos Tversky. 2013. Prospect theory: An analysis of decision under risk. In Handbook of the Fundamentals of Financial Decision Making: Part I. Hackensack: World Scientific Pub Co Inc., pp. 99–127. [Google Scholar]

- Klinke, Harald, Liska Surkemper, and Justin Underhill. 2018. Creating New Spaces in Art History. International Journal for Digital Art History: Digital Space and Architecture 3: 9. [Google Scholar]

- Kolfin, Elmer. 2006. The Young Gentry at Play: Northern Netherlandish Scenes of Merry Companies 1610–1645. Leiden: Primavera Press. [Google Scholar]

- Kräussl, Roman, Thorsten Lehnert, and Nicolas Martelin. 2016. Is There a Bubble in the Art Market? Journal of Empirical Finance 35: 99–109. [Google Scholar] [CrossRef]

- Li, Weixuan. 2018. Deciphering the Art and Market in the Dutch Golden Age: Insights from Digital Methodologies. Master’s thesis, University of Amsterdam, Amsterdam, The Netherlands. [Google Scholar]

- Lincoln, Matthew D. 2016. Social Network Centralization Dynamics in Print Production in the Low Countries, 1550–1750. International Journal for Digital Art History. [Google Scholar] [CrossRef]

- Martin, Wilhelm. 1901. Het leven en de werken van Gerrit Dou beschouwd met het schildersleven van zijn tijd. Ph.D. Dissertation, Leiden Universiteit, Leiden, The Netherlands. [Google Scholar]

- Montias, John Michael. 1982. Artists and Artisans in Delft: A Socio-Economic Study of the Seventeenth Century. Princeton: Princeton University Press. [Google Scholar]

- Montias, John Michael. 1987. Cost and Value in Seventeenth-Century Art. Art History 10: 455–66. [Google Scholar] [CrossRef]

- Montias, John Michael. 1988. Art dealers in the seventeenth-century Netherlands. Simiolus: Netherlands Quarterly for the History of Art 18: 244–56. [Google Scholar] [CrossRef]

- Montias, John Michael. 1990. Estimates of the Number of Master-painters, Their Earning and Their Output in 1650. Leidschrift 6: 59–74. [Google Scholar]

- Montias, John Michael. 1996. Works of Art in a Random Sample of Amsterdam Inventories. In Economic History and the Arts. Edited by Michael North. Cologne: Böhlau, pp. 67–88. [Google Scholar]

- Montias, John Michael. 2002. Art at Auction in Seventeenth-Century Amsterdam. Amsterdam: Amsterdam University Press. [Google Scholar]

- Mundy, Peter. 1925. The Travels of Peter Mundy in Europe and Asia, 1608–1667, vol. 4, Travels in Europe, 1639–47. Edited by R. Carnac Temple. London: Hakluyt Society. [Google Scholar]

- Nijboer, Harm. 2010. Een bloeitijd als crisis: Over de Hollandse schilderkunst in de 17de eeuw. Holland 42: 193–205. [Google Scholar]

- Pesando, James E. 1993. Art as an Investment: The Market for Modern Prints. The American Economic Review 83: 1075–89. [Google Scholar]

- Petram, Lodewijk. 2014. The World’s First Stock Exchange. New York: Columbia University Press. [Google Scholar]

- Prak, Maarten. 2008. Painters, Guilds, and the Art Market During the Dutch Golden Age. In Guilds, Innovation, and the European Economy, 1400–1800. Edited by S. R. Epstein and Maarten Prak. Cambridge: Cambridge University Press, pp. 143–71. [Google Scholar]

- Rasterhoff, Claartje. 2017. Painting and Publishing as Cultural Industries: The Fabric of Creativity in the Dutch Republic, 1580–1800. Amsterdam: Amsterdam University Press. [Google Scholar]

- Roodenburg, Herman. 2006. Visiting Vermeer: Performing Civility. In In His Milieu: Essays on Netherlandish Art in Memory of John Michael Montias. Edited by Amy Golahny, Mia M. Mochizuki and Lisa Vergara. Amsterdam: Amsterdam University Press, pp. 385–94. [Google Scholar]

- Rosen, Sherwin. 1981. The Economics of Superstars. The American Economic Review 71: 845–58. [Google Scholar]

- Sluijter, Eric Jan. 1991. Didactic and Disguised Meanings? Several Seventeenth-Century Texts on Painting and the conological Approach to Dutch Paintings of this Period. In Art in History. History in Art. Studies in Seventeenth Century Dutch Culture. Edited by David Freedberg and Jan de Vries. Santa Monica: Getty Center for the History of Art and the Humanities, pp. 175–207. [Google Scholar]

- Sluijter, Eric Jan. 1999. Over Brabantse vodden, economische concurrentie, artistieke wedijver en de groei van de markt voor schilderijen in de eerste decennia van de zeventiende eeuw. Nederlands Kunsthistorische Jaarboek 50: 113–44. [Google Scholar] [CrossRef]

- Sluijter, Eric Jan. 2015. Rembrandt’s Rivals: History Painting in Amsterdam 1630–1650. Amsterdam and Philadelphia: John Benjamins Publishing. [Google Scholar]

- Sornette, Didier. 2008. Nurturing breakthroughs: lessons from complexity theory. Journal of Economic Interaction and Coordination 3: 165–81. [Google Scholar] [CrossRef]

- Sornette, Didier. 2017. Why Stock Markets Crash: Critical Events in Complex Financial Systems. New Haven: Princeton University Press. [Google Scholar]

- Thaler, Richard H. 1993. Advances in Behavioural Finance. New York: Russel Sage. [Google Scholar]

- Thaler, Richard H., and Cass R. Sunstein. 2008. Nudge: Improving Decisions about Health, Wealth, and Happiness. New Haven: Yale University Press. [Google Scholar]

- Van der Woude, Ad. 1991. The volume and value of paintings in Holland at the time of the Dutch Republic. In Art in History, History in Art: Studies in Seventeenth-Century Dutch Culture. Edited by David Freedberg and Jan de Vries. Santa Monica: Getty Center for the History of Art and the Humanities, pp. 284–329. [Google Scholar]

- Van Gool, Jan. 1750–1751. De nieuwe schouburg der Nederlantsche kunstschilders en schilderessen. 2 vols, The Hague. [Google Scholar]

- Van Miegroet, Hans, and Neil De Marchi. 2012. Uncertainty, Family Ties and Derivative Painting in Seventeenth-Century Antwerp. In Family Ties. On Art Production, Kinship Patterns and Connections 1600–1800. Edited by Koenraad Brosens, Katlijne Vam Der Stighelen and Leen Kelchtermans. Turnhout: Brepols Publishers, pp. 55–76. [Google Scholar]

- Veblen, Thorstein. 1934. The Theory of the Leisure Class: An Economic Study of Institutions. New York: The Modern Library. First published 1899. [Google Scholar]

- Westermann, Mariet. 2005. A worldly art: The Dutch Republic, 1585–1718. New Haven: Yale University Press. [Google Scholar]

- Weyerman, Jacob C. 1729–1769. De levens-beschryvingen der Nederlandsche konst-schilders en konst-schilderessen. 4 vols, The Hague. [Google Scholar]

- Zorich, Diane. 2013. Digital Art History: A Community Assessment. Visual Sources: Digital Art History 29: 1–2. [Google Scholar] [CrossRef]

| 1 | RKDimages, contained 55,718 unique paintings in the dataset acquired via the RKD public API, accessed February 2018. |

| 2 | The low-quality paintings, such as “works-by-the-dozen” (dosijnwerck) had a much lower survival rate than those of Rembrandt or Vermeer and are thus under-represented in the modern database. Jager (2016) lifts the curtain to the lower segment of the art market for which the “works-by-the-dozen” were produced. Yet, the inventories of few art dealers can hardly be a representative sample to quantify the degree of distortion in the RKD database. |

| 3 | Cf. (Van der Woude 1991; Montias 1990; De Marchi and Van Miegroet 2006, 2014; Rasterhoff 2017, etc.) |

| 4 | However, there is no thorough survey of all archival inventories, and the majority of known inventories were collected to suit art historical interests and are biased towards the collections of the wealthy with more works of art in the few large cities. The inventories in the Getty Provenance Index only has inventories from Amsterdam, Haarlem, Utrecht, Leiden, and Delft with a focus on the inventories in Amsterdam. As a result, they cannot truly reflect the collecting pattern of the whole society and are therefore also a biased sample (Montias 1996). |

| 5 | The categorization of genres in this study follows the main genre described in the RKD database. For example, a landscape with the staffage figures embodying a religious lesson is still regarded as landscape instead of history painting. |

| 6 | 96.6% of paintings in the RKDimages have size recorded in the dataset. The loss of data due to the change of measurements is thus negligible. |

| 7 | Cf. Hadrianus Junius, Batavia, Leiden, 1589 (the first city description in which painters were included as “famous sons” of the city); J.I. Pontanus, Historische beschrijvinghe der seer wijt beroemde coop-stad Amsterdam, Amsterdam 1614; Jan Orlers, Beschrijvinge der stad Leyden, Leiden 1641. Preacher Samuel Ampzing and theologian Schrevelius wrote in 1628 and 1648 respectively the praise for the city of Haarlem with several laudatory poems dedicated to painters. |

| 8 | Angel went as far as saying: “I win a lot of money, [as] I make large paintings.” (Ick winne machtich gelt, ick maecke groote stucken). See (Angel 1642, pp. 28–29). Mentioned in (De Marchi and Van Miegroet 1994). |

| 9 | More prominent painters (A++, A+ samples according to Rasterhoff’s categorization) were born around 1590–1630, entering the market around the first decades of the 17th century (Rasterhoff 2017, p. 206, Figure 7.4). |

| 10 | An artist-painter (kunstschilder) was often literate and had attended school full-time for three years. After this initial investment in basic education, for which Montias has estimated an accumulated expense of fl. 150 to fl. 200, aspiring artists had to invest in an apprenticeship period. Some pupils finished their training with a trip to Italy at a considerable cost, which was often a privilege of the pupils from affluent families. For basic education see (De Jager 1990; Boers-Goosens 2001, p. 87). And for painting apprenticeships, see (Montias 1982, p. 169). For the entry barriers for artist, see (Rasterhoff 2017, p. 232). See also (Bok 1994, pp. 53–97). |

| 11 | See ECARTICO for numerous cases for pupils of masters of whom we do not know their works. |

| 12 | Jan Porcellis, Jan van Goyen, Frans Hals, Jan Steen, Hercules Seghers, Pieter de Hooch, Vermeer and Rembrandt have been found taking debts. See (Rasterhoff 2017, p. 237). |

| 13 | There are a handful of examples of such contracts. Just to name a few: In 1625, for instance, painter Jacques de Ville decided upon delivering fl. 2400 worth of paintings over the course of a year and a half to skipper Hans Melchiorsz; in 1641, art dealer Leendert Volmarijn is known to have ordered thirteen pictures from Isaac van Ostade; art dealer Joris de Wijs contracted with Emanuel de Witte to paint for fl. 800 a year plus room and board (Montias 1988, pp. 65–66; Montias 1987, p. 99; Bredius 1891, pp. 56–57). |

| 14 | Samuel van Hoogstraten told the tale of Hercules Pietersz Seghers that Seghers sold a copperplate to an art dealer for very little money. The dealer, “after having printed a few copies from his plate he cut it into pieces, saying that the time would come that collectors would pay for one copy four times as much he had asked for the whole plate, which actually did happen because each print later bourught sxteen ducat, […] but poor Hercules did not get any of this” (Hoogstraten 1678, p. 312). Translation is taken from (Haverkamp-Begemann 1968, p. 8). |

| 15 | Existing studies use extensive data on the price of painting in auctions and sales across time to develop a price index to identify abnormal bumps in the price index. However, collecting large and representative 17th century price data of Dutch paintings is almost impossible as most sales of paintings do not have records. Most of the price information of paintings are from probate inventories and contracts: the former can hardly represent the sale price and the latter is too small to be representative. For these reasons, this research will limit its scope to the social bubble without claiming a speculative bubble in the 17th-century Dutch art market. |

| 16 |

Figure 1.

(a) Painting production trend 1600–1700 (5-year moving average). Source: RKDimages, accessed February 2018; (b) First derivative of Painting production trend in Figure 1a (5-year moving average).

Figure 1.

(a) Painting production trend 1600–1700 (5-year moving average). Source: RKDimages, accessed February 2018; (b) First derivative of Painting production trend in Figure 1a (5-year moving average).

Figure 2.

Paintings in the Getty Provenance Index 1600–1700. Source: Getty Provenance Index, accessed February 2018.

Figure 2.

Paintings in the Getty Provenance Index 1600–1700. Source: Getty Provenance Index, accessed February 2018.

Figure 3.

Number of painters active in the 11 big cities in the Dutch Republic, 1550–1750. Source: ECARTICO, accessed February 2018 (5-year moving average).

Figure 3.

Number of painters active in the 11 big cities in the Dutch Republic, 1550–1750. Source: ECARTICO, accessed February 2018 (5-year moving average).

Figure 4.

Painting production trend 1600–1700 (5-year moving average) separated by genre. Source: see Figure 1.

Figure 4.

Painting production trend 1600–1700 (5-year moving average) separated by genre. Source: see Figure 1.

Figure 5.

Painting production trend 1600–1700 by surface area (5-year moving average) stacked (a) separate by genre (b); Source: see Figure 1.

Figure 5.

Painting production trend 1600–1700 by surface area (5-year moving average) stacked (a) separate by genre (b); Source: see Figure 1.

Figure 6.