CSR Reporting Practices in Visegrad Group Countries and the Quality of Disclosure

Faculty of Organization and Management, Silesian University of Technology, Roosevelt street 26, 41-800 Zabrze, Poland

Sustainability 2017, 9(12), 2322; https://doi.org/10.3390/su9122322

Submission received: 23 November 2017

/

Revised: 7 December 2017

/

Accepted: 8 December 2017

/

Published: 13 December 2017

(This article belongs to the Special Issue Corporate Social Responsibility (CSR) in Developing Countries: Current Trends and Development)

Abstract

:Companies around the world more often issue publicly available reports to disclose how responsibly they conduct their business. The practices of corporate social responsibility (CSR) reporting are more popular in western part of Europe then in Central and Eastern European (CEE) countries and empirical studies related to these practices in the region are sporadic and fragmented. The Visegrad Group countries have undergone tremendous changes in political, environmental and social area during the last twenty years. The CSR concept in these countries is relatively new but is rapidly spreading, in particular as part of their integration with the European Union, as well as under the influence of transnational corporations (TNCs) and foreign investors. Therefore, acquisition of knowledge, which presents the functioning of CSR reporting practices in the region seems to be of interest to both the scientific community and enterprises themselves. An important part of the analysis conducted in the study was the assessment of quality of CSR reports issued in this region. The quality indicator of the studied reports was based on seventeen criteria related to relevance and credibility of disclosed information. The findings indicate that CSR reporting practices are not widespread among V4 countries and suggest some area of improvements. Furthermore, the achieved results confirm the existence of a relationship between two factors (external verification of a report and usage of the GRI guidelines when developing a report) and the level of quality of the CSR report.

1. Introduction

The growing expectations of stakeholders in regard to the transparency and responsibility of enterprises imply measuring and disclosing the impact of business decisions on society and the natural environment. Different organizations may present results achieved in this field by creating and publishing corporate social responsibility (CSR) reports [1]. Today, we can observe a growing number of companies issuing such reports as a part of their annual reports or as stand-alone CSR reports. Despite the increase in the number of such reports their quality varies. Literature on CSR reporting points to increasing lack of relevance, completeness and credibility of the information reported [2,3,4,5,6]. Thus, the measurement of the quality of CSR reports as well as identification of factors which influence the quality of these reports are recognized as relevant questions that are still open. Prior studies concerning issues related with CSR reporting have mostly focused on countries of Western Europe. It might not be possible to generalize the findings of these studies for Central and Eastern European countries, as they have underlying legal or institutional background that differ from those applied in the old European Union Member States. Moreover, transition from a centrally planned to a market economy in this region, as well as social and political transformations could have caused that stakeholders (i.e., civil organizations, media, consumers) from Visegrad Group (V4) countries might be less influential than from old EU Member States. Some studies also suggest that there are country-specific differences in the extent of CSR reporting [7,8]. The country creates a context in which the company has to legitimize its activities. This specific context may embed different aspects such as governance systems and regulation [9], employment protection and labour conditions [10], environmental protection regulations [11] and others. In the European Union, we can find different approaches to CSR reporting [12,13] and therefore this article tries to contribute to the debate on patterns of current CSR practices, especially in countries which have undergone a transition from a centrally planned to a market economy. Thus, the aim of this paper is to present the current state of CSR reporting in Visegrad Group countries, to identify the quality level of these kinds of practices as well as the relationship of the two factors which influence the quality of those reports.

The rest of the paper is structured as follows. The next section provides an overview of CSR reporting literature, with a particular emphasis on studies focusing on measuring the quality of those reports. This is followed by a section dedicated to methodology used in the research process. The research findings are then presented including current state of CSR reporting practices and quality level of those reports in V4 countries. The paper ends with discussion section and conclusions including limitations as well as recommendations for further research.

2. Literature Review

The literature review reveals that several academics have been analyzed the current situation of CSR reporting in individual countries forming the Visegrad Group, so far [14,15,16,17,18,19,20,21,22]. No research discussing comprehensively the topic in all four Visegrad countries were found. Therefore, the study results presented in this paper intends to complement this gap.

Developing a high quality CSR report may bring benefits both to a reporting company and to interested parties. However, only valuable reports can be used as an important instrument of corporate communication and a key factor in decision making of companies and stakeholders [23,24]. Changes in the disclosure of information by companies have led researchers to increasingly address the topic of CSR reporting. A large part of the research concerns the reasons why companies choose to publish CSR reports and the benefits resulting from such reporting. With the increase in CSR reporting, a wave of criticism regarding the quality of such documents has appeared. CSR reporting has been criticized for its lack of relevance and credibility [3]. Although different studies have expressed concern about the quality of the CSR reporting, there are not many measures of quality developed. Some authors [25,26] use as an assessment criteria quality reporting principles proposed by Global Reporting Initiative (GRI) [27] or World Business Council for Sustainable Development (WBCSD) [28]. Others evaluate the quality of CSR reports using their own frameworks [29,30]. The proposed quality criteria both in the GRI and WBCSD guidelines are quite similar and general in nature. Despite the fact that the criteria relate to the contents of sustainability reports many of them could successfully refer to the quality of different types of data. In the literature can be found an example of measuring the quality of reports against the achievement of higher application levels prescribed in GRI guidelines [31,32], while others authors evaluated the quality of reports using the content analysis of specific indicators [2,33,34]. Lock and Seele [35] investigated the credibility of CSR reports by utilizing four of their own constructs: understandability, truth, sincerity, and truthfulness. However, the quality of CSR reports is still under-investigated [36]. Generally, studies on quality of information disclosed in CSR reports can be divided into at least two groups [29,37]. First group of researches focus on quantity analysis, based on volume (for example content analysis, linguistic analysis). The second group consists of studies searching the way to measure the quality of those reports (see Table 1). The quality analysis are usually related with calculation of a quality index which indicates the level of report’s quality. Disclosure quality index can be defined as an instrument that is designed to measure a number of indicators, which, when the aggregated indicators reveal the score, indicates the level of specific information disclosed [29]. Methods based on quantity of information do not take into account the quality and meaning of the written text, they focus only on the amount of information in a particular area of interest. This kind of analysis relies on measurement of the number of pages, sentences, words or phrases, depending on the unit of analysis. The quality of disclosure and the extent of disclosure may not be equal measures of quality. Extent often refers to the amount, but lengthy reporting may contain irrelevant information or use misleading words, resulting in incomplete or poor quality disclosure [38]. Studies based on quality (calculation of disclosure index) allow for a more comprehensive investigation by using multiple parameters in the assessment process [39]. Study presented in this paper focuses on CSR reports quality and extends the analyses of prior published studies in this field [2,23,25,26,29].

The wide scope and complexity of the corporate social responsibility concept [40,41,42] imply difficulties with assessing the quality of information disclosed in those reports. These problems have caused, among other things, that so far little research has appeared on the determinants of quality of CSR reports because empirical studies of the determinants of quality disclosure require the use of a suitable method for measuring the quality. Most of the literature focuses on external verification, using GRI guidelines and stand-alone CSR report as determinants of quality of CSR reports. Pflugrath et al. [43] and Park and Brorson [44] provided empirical evidence that verification of sustainability reports made by professional accountants enhances their credibility. Lock and Seele [36] found that standardization by means of GRI framework improves the quality of corporate social responsibility reports. Michelon, Pilonato and Ricceri [2] examine whether the use of a stand-alone report, the assurance of CSR information and the adoption of the GRI guidelines are associated with CSR disclosure quality. In view of the above, results of the study presented in this paper contribute also to the literature which refers to the determinants of quality of CSR reports.

3. Research Methodology

The study consisted of several stages. First, the level of CSR reporting in V4 region was identified and compared. Next, current state of CSR practices in V4 countries was examined. An important point of the study was the assessment of quality of CSR reports. Finally, the impact of two factors (using GRI guidelines and independent verification) on quality of these reports was assessed. For the purpose of the study a mixed method research was applied [45]. The analysis presented in the paper focuses on four of the following research questions:

- What is the current state of CSR reporting in V4 countries? (What types of companies publish CSR reports? What types of reports are these? According to which guidelines are these reports prepared? Are the data in these reports subject to external verification?)

- What is the quality level of CSR reports published in V4 countries?

- What are the quality differences between reports prepared according to the GRI guidelines and those not prepared according to the GRI guidelines?

- What are the quality differences between reports externally verified and those not externally verified?

Additionally for each examined report the following were determined: company size, type and sector, type of report, whether or not the CSR report was verified by a third party, whether or not the CSR report was prepared according to the GRI guidelines, whether or not the company was a member of the UN Global Compact Initiative.

3.1. Data Collection

Information about CSR reports from V4 countries was obtained from the online Global Reporting Initiative (GRI) sustainability disclosure database [46]. The study included separate CSR reports, annual reports with CSR sections and integrated reports (financial and non-financial information provided in a single document which shows their mutual impact [47]). After a preliminary analysis of reports included in the database not all of them were included in further study. The premise of the research was the evaluation of CSR reports, and, therefore, the author excluded from the study environmental reports, occupational safety and health (OHS) reports, and several pages brochures dedicated to CSR issues. The excluded reports would score too low in the assessment process and for this reason they would not contribute to the overall conclusions. Only reports that were published in English underwent the quality assessment phase (see Table 2). The reports published in English, together with those that were available with regard to the above considerations, gave a final total of 44 CSR reports admitted to the quality assessment phase of the study.

3.2. Assessment Tool

The quality of CSR reports was assessed using seventeen criteria. The selection of the criteria was based on the author’s previous research in this topic [12,19]. It was assumed that quality of CSR reports equals the quality of the information provided in these types of reports. The quality of information, for the purposes of this study, is defined as the relevance and credibility of information. To assess the quality of the CSR reports, eleven criteria were identified in the category of relevance of information, and six criteria in the category of credibility. The structure and explanation of the quality assessment criteria is shown in Table 3 When assessing the quality of CSR reports a five-point scale (from 0 to 4) was applied (see Table 4).

3.3. Quality Indicators of CSR Reports

In order to assess and determine the relationship between the quality level of examined sustainability reports and other variables, the author aggregated the indicators related to the reporting practices. Two indicators were identified:

- R—relevance of information indicator,

- C—credibility of information indicator.

Indicators were specified using the arithmetic mean of sub-indices constituting a given indicator (R and C). The indicator of relevance consists of eleven sub-indices and the indicator of credibility consists of six sub-indices. In the first step, individual indicators were calculated for each of the analysed reports (Rr and Cr indicators). Then, on this basis, values of the Rc, Cc, and Qc indicators were calculated for each of the analyzed countries. Finally, the aggregate quality of sustainability reports’ indicator for a sample (Qs) was calculated, which was the arithmetic mean of the Rs and Cs indicators.

For statistical analysis, non-parametric tests were used (because not all variables meet the assumption of normality). For checking whether the values of the samples taken from two independent populations are equally large, the U Mann-Whitney test was used. To check the relationships between variables, the Spearman’s rank correlation coefficient was used (due to the fact that the tested variables had a ranked character which was allocated during the testing). The analyses were conducted at the level of statistical significance α = 0.05. For all calculations, SPSS 21.0 software was used.

4. Results

4.1. Current State of CSR Reporting in V4 Countries

We are currently witnessing the emergence of a global trend aimed at the development of corporate social responsibility reporting. In European Union the largest number of CSR reports [46] in 2014 was published in Great Britain, Spain, Germany, Sweden, The Netherlands, France, and Finland; while the smallest number in Lithuania, Estonia, Slovakia, Bulgaria, Slovenia and Latvia. Within the countries belonging to the Visegrad Group, the highest number of reports was recorded in Poland, and the lowest in Slovakia. Table 5 presents the number of CSR reports together with the number of active enterprises in Visegrad group countries (Eurostat data [48]). The number of reports per million enterprises, calculated on this basis, points to differences in practices of this type in the region. Amongst the V4 countries, the highest indicator was achieved by Hungary, followed by Czech Republic and Poland. The lowest indicator was achieved by Slovakia. It should be noted at this point, that the data relating to the number of published reports within a particular country comes from a voluntary database (enterprises are not obliged to deposit their CSR reports in this type of database), and may not necessarily reflect the real state.

The analysis of the status of current CSR reporting practices in V4 countries should include information about the number of companies that participate in the UN Global Compact (UN GC) initiative. The analysis of this data seems justified as signatories of this initiative are obliged to publish the report called Communication on Progress on an annual basis. The analysis of the data listed on the website of UN GC took into consideration signatories defined as companies and small and medium enterprises (Table 6. A great majority of signatories to this initiative are coming from Poland (73%). The second place, with a considerably smaller number of signatories, belongs to enterprises from the Czech Republic (15%). Only 7 enterprises from Hungary and 4 enterprises from Slovakia entered this initiative.

Further studies on the organizational size and type of reporting companies and details of the types of published reports were made on the basis of 82 reports from 4 countries belonging to the Visegrad Group (see Table 7. The results indicate that nearly all of the reports (93%) under analysis were prepared by large enterprises. A large number of reporting companies were multinational enterprises, particularly in the case of the Czech Republic and Hungary. Only 7% of small and medium-sized enterprises published their CSR reports in 2014. Companies of this size prepared their CSR reports in Poland and in Hungary. Taking into consideration the type of reporting enterprises, the largest number of reports in the Visegrad region was prepared by private companies (44%) followed by subsidiary companies (39%). This division also applies to reporting enterprises from Poland. A reverse situation, i.e., the larger share of the subsidiary companies when compared to private companies can be observed in Slovakia, Hungary and the Czech Republic. Reports prepared by state-owned companies constituted the smallest share among the enterprises under analysis (12%). In this case, the highest number of reporting enterprises of this type came from Hungary (Table 7). In Slovakia, none of the reporting enterprises belonged to this group of enterprises. Companies listed on the stock exchange constituted 37% of analysed enterprises in all countries. The largest number of entities of this type prepared CSR reports in Poland and the Czech Republic. When further assessing the enterprises in regard to their business activity sector, they originated from various industries. The highest number of reporting enterprises came from the financial services sector (17%), food and beverage products (16%), energy (8%), energy utilities (7%) and the telecommunication (7%) sector. Other sectors were represented in the research at the level of 5% and lower.

The separate CSR reports were in the sample absolute majority (85%). Annual reports with a CSR section constituted only 2% of all reports. This type of report was developed only in Poland and the Czech Republic; 5% of reports from the Czech Republic and 3% of reports from Poland were prepared as annual reports with a CSR section. Integrated reports, as the most advanced form of reporting, were made only by reporting enterprises from Poland (22%) and Hungary (9%) and constituted only 12% of the total number of reports under analysis. Nearly half (44%) of the analysed reports were made in compliance with the Global Reporting Initiative (GRI), and 16% of the analysed reports were subject to an independent, external verification (see Table 8. In Slovakia none of the analysed reports included an authentication of credibility of the data prepared by an independent entity. Signatories of the UN Global Compact initiative represented 18% of all reporting enterprises in the research. By joining the program of the United Nations Global Compact (UN GC) companies undertake to comply with the rules (principles that relate to human rights, labour standards, the environment and practices, anti-corruption) and publish in the annual report information on how to implement these principles and objectives of the Global Compact, the so-called GC Communication on Progress—COP. The 10 UN principles and the guidelines on how to publish the COP provide guidance to participants, which relate to the content of sustainability report.

Summarizing the current situation on CSR reporting practices among V4 countries, it can be said that the most CSR reports is prepared in Poland. Large, private and subsidiary companies prepare CSR reports most commonly. Reports are most frequently prepared as separate reports, and nearly a half of the analysed reports were developed in compliance with the GRI Guidelines (reports from the Czech Republic were an exception—only 20% of them were prepared in compliance with the GRI Guidelines). Very few of the published CSR reports in V4 countries were subjected to an independent, external verification.

4.2. Quality Level of CSR Reports from the Visegrad Group Countries

In the study the quality of information disclosed in CSR reports was defined by means of its relevance and credibility. In order to assess the quality of CSR reports in individual countries of the Visegrad Group, and in order to define the relationships between the level of this quality and other variables, sub-indices were aggregated (names of the sub-indices are the same as the names of the criteria of the research tool) which applied to CSR reporting. Two indices were identified: relevance of information indicator—R and credibility of information indicator—C.

As many as 44 CSR reports published in English from countries belonging to the Visegrad Group were analysed. Table 9 presents a list of countries from which these CSR reports originated.

The largest number of CSR reports under analysis were reports from Poland—45%. Nearly one third of the analysed reports (32%) came from Hungary, 16% from the Czech Republic, while only 7% from Slovakia.

As confirmed by the CSR report quality assessment, the minimum level of the relevance of information indicator (R) amounted to 0.27 points, while the maximum level of this indicator amounted to 3.27 points. The minimum level of the credibility of information indicator (C) amounted to 0.33 points, while the maximum level of the indicator amounted to 3.33 points. Taking into account the scale according to which the reports were assessed (0–4), it can be stated that the assessment of the individual countries did not provide overly good results. The obtained values of the quality indicators of CSR reports (no country achieved the level of 2.0) suggest the existence of a wide area of improvements in all countries subject to analysis. Table 10 outlines descriptive statistics and results of the test for normal distribution for the level of quality of CSR reports and its components.

The Shapiro-Wilk analyses resulted in statistically significant differences from the normal distribution for all of the tested variables, which suggest the use of non-parametric tests in future analyses.

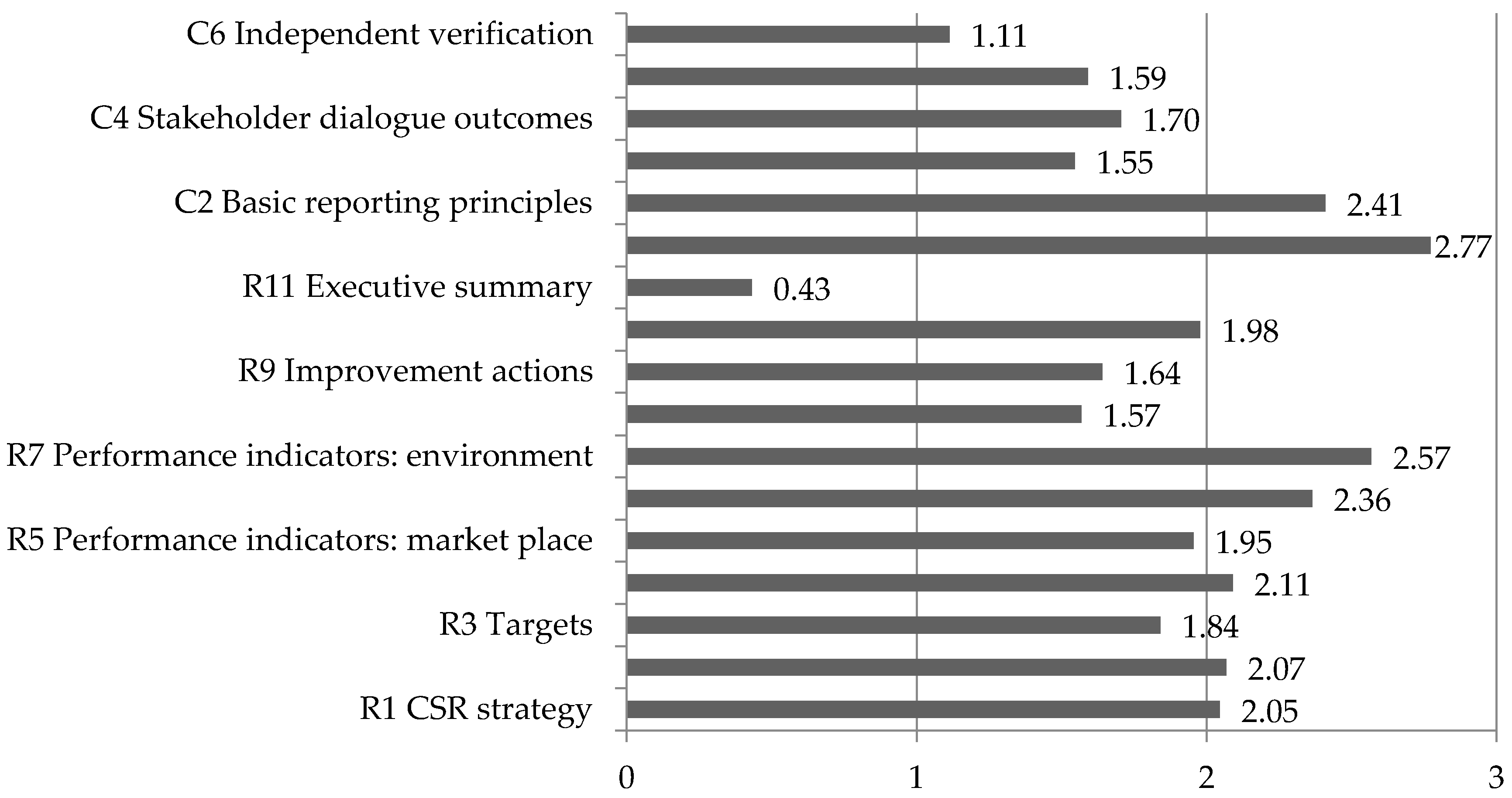

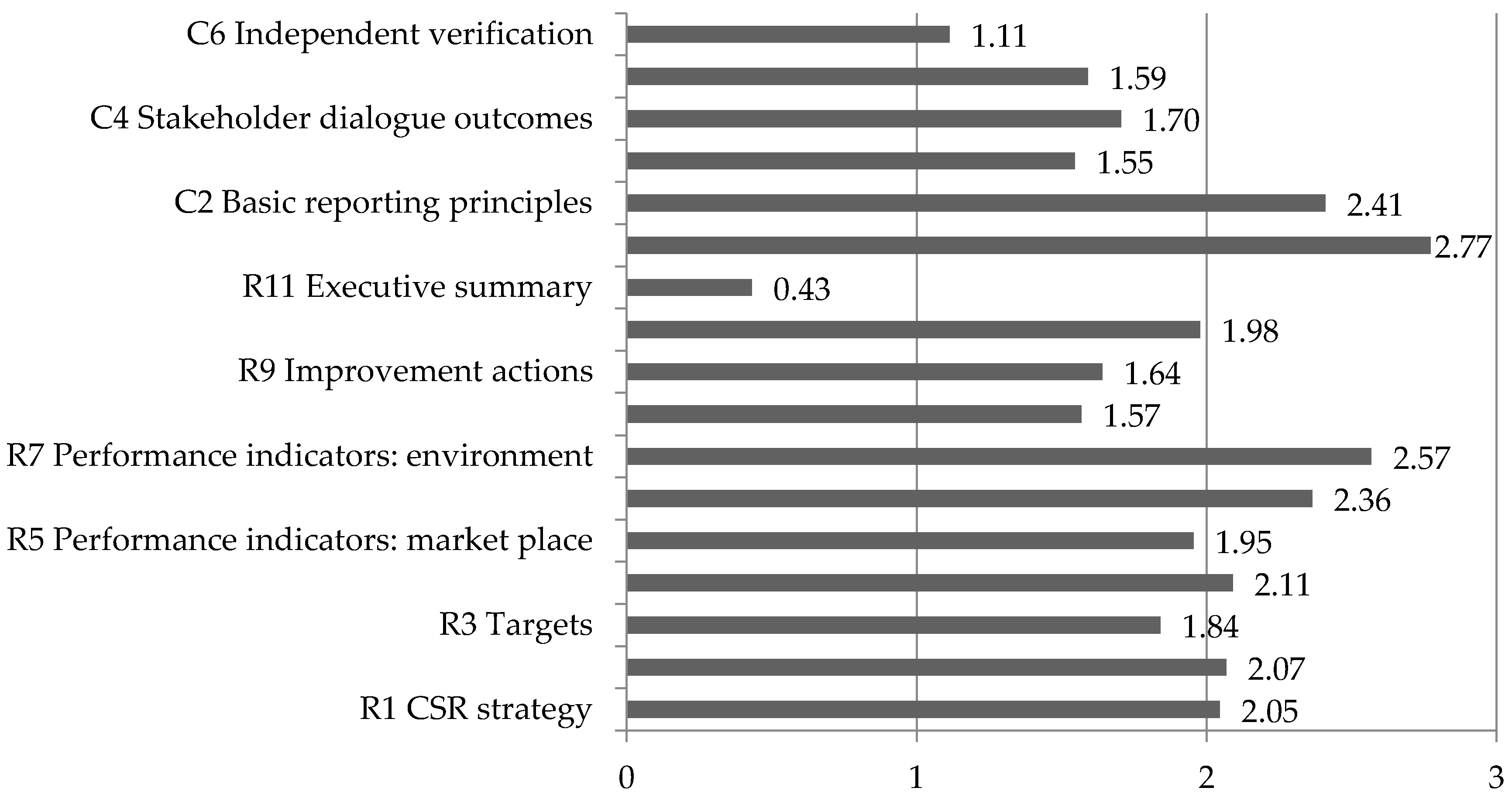

The results obtained by the CSR reports from the V4 Group within the individual components of the relevance (R) and credibility of information (C) indicators are outlined in Figure 1. In regard to components of the relevance of information indicator, the most highly assessed elements in the analysed reports were issues relating to the following corporate areas: performance indicators in the area of environment (2.57 points), performance indicators in the area of the workplace (2.36 points) as well as presentation of trends over time (2.11 points). Executive summaries of CSR reports were given the lowest grades in the assessment (0.43 points). A good summary is a practical and helpful element of a report (especially if a report contains several dozen pages or more) as it allows the reader to identify the key information within a short period of time. In the majority of reports under analysis, such summaries were not included. A low grade was also given to the disclosure of corporate indicators in the area of community (1.57 points). In the reports covered by the analysis, issues linked to corporate involvement in the development of local communities were most often presented in a descriptive form by describing the social projects run by the organisation.

In regard to credibility of information, the readability of a report was rated the highest (2.77 points). In this area, there were no reservations in relation to the majority of reports, as the information was provided in a clear manner, the reports were readable and illustrated with extensive graphical material. The weaknesses of the reports included the issue of independent verification (1.1 points), the quality of disclosed data (1.55 points) and the occasional use of feedback from report recipients (1.59 points). Few reports were externally verified and the results of independent verification were not always included in the report and do not always indicate recommendations in the assurance statement. The information about processes, procedures of collection, aggregation and transformation of data as well as the source of the disclosed data were rarely disclosed in the reports. The analysed reports also rarely contained information which encouraged its readers to contact the individuals responsible for the reports, or allow to express an opinion and provide suggestions relating to these reports.

4.3. Factors Influencing the Level of Quality of CSR Reports

Enterprises disclose data on CSR in many different ways. The studied CSR reports differed from each other in many respects, including in regard to their compliance with the existing standards (GRI guidelines) and the submission of the data disclosed in the reports to independent verification.

In the study as many as 82% of reporting enterprises use the Guidelines developed by the Global Reporting Initiative (GRI) when preparing a CSR report. The Mann–Whitney U tests were conducted in order to analyse if CSR reports prepared in compliance with the GRI Guidelines and those developed using the individual principles of the reporting enterprise varied from each other. Table 11 shows the results of this analysis.

The Mann–Whitney U tests identified statistically significant differences in relation to all variables under analysis. This means that the CSR reports prepared according to the international GRI Reporting Guidelines were characterised by a higher level of the relevance indicator (R) of the information disclosed, a higher level of the credibility indicator (C) of the information disclosed, and a higher level of the quality indicator (Q), when compared to the CSR reports developed using the individual principles of reporting enterprises. The mean level of the quality indicator of the CSR reports prepared according to the GRI Guidelines was 2.05 points. In the case of the CSR reports developed using the individual principles the mean level of the quality indicator was lower and amounted to 1.00 point. Next the rho-Spearman correlation was performed to analyse the relationships between the use of the GRI Guidelines and the level of the quality indicator (Q) of the CSR reports published in English. Table 12 presents the correlation coefficient resulted from this analysis.

Between the variables, a statistically significant rho-Spearman correlation was identified (0.49). The correlation coefficient points to the existence of a positive relationship between the use of the GRI Guidelines in the development of a CSR report and the quality level of that report. The more often the CSR reports in English were prepared in accordance to the GRI Guidelines, the higher level of quality indicator (Q) they received.

The authentication of the veracity of the data disclosed by a company in a CSR report by an independent and external entity was not a popular practice of the reporting enterprises from V4 countries (30% of reports in the research sample were verified externally). The Mann–Whitney U tests were conducted in order to analyse if CSR reports which were and which were not subject to external verification varied from each other in terms of their quality. Table 13 shows the results of this analysis.

The Mann–Whitney U tests identified statistically significant differences in relation to all variables under analysis. This means that the CSR reports in English verified independently were characterised by a higher level of the relevance indicator (R) of the information disclosed, a higher level of the credibility indicator (C) of the information disclosed, and a higher level of the quality indicator (Q), when compared to the CSR reports which were not verified independently. The rho-Spearman correlation was performed to analyse the relationships between the use of independent verification and the level of the quality indicator (Q) of the CSR reports. Table 14 presents the correlation coefficients from this analysis.

Between the analysed variables, a statistically significant rho-Spearman correlation was identified (0.45). The correlation coefficient points to the existence of a positive relationship between the use of independent verification of a CSR report and the quality level of that report. The more often the CSR reports in English were subject to independent verification, the higher level of quality indicator (Q) they received.

In this research sample, all CSR reports which were subject to independent verification were developed in compliance with the GRI Guidelines. These results may suggest that enterprises which decide to submit their CSR reports to external verification (which is linked to additional costs [50]) care more for the content of these reports and use international guidelines in their development. It can therefore be stated that external verification has a positive impact on the level of the data disclosed and is an important factor which contributes to the quality of CSR reports.

5. Discussion

An organisation can inform the interested parties on socially responsible practices and results achieved in this field through the development and publication of CSR reports. The reports of this type constitute a communication tool, which is to serve as an internal and external source of information on the approach and maturity of a corporate social responsibility implementation. Despite the growing popularity of these types of practices year-on-year, the quality of the developed CSR reports continues to be questionable. When preparing CSR reports, enterprises use various standards and guidelines, or they prepare them according to their own design, with various levels of detail and not always regularly. Therefore, these reports sometimes fail to provide complete and specific data which are expected by the readers of the reports, which intensify problems with their assessment and comparison of the results achieved in this area.

The study findings indicate that CSR reporting practices are not widespread among companies in V4 countries. The early stage of disclosing CSR information in the region is aligned with the findings of the research of authors analysing this situation in individual countries, Dočekalova [14], Piskóti and Hajdú [18], Hąbek [19], Kubaščíková [22], among others.

The study presented in this paper focuses also on CSR reports quality and extends the analyses of prior published studies in this field carried out by Michelon, Pilonato and Ricceri [2], Freundlieb, Gräuler and Teuteberg [23], Ching, Gerab and Toste [26]. Studies based on measuring the quality of CSR reports allow for a more comprehensive investigation by using multiple parameters in the assessment process. The analysis are related with calculation of a quality index which indicates the level of report’s quality. Results of the study contribute also to the scarce literature which refers to the determinants of quality of CSR reports. Empirical studies of the determinants of quality disclosure require the use of a method for measuring the quality in the first stage. Most studies pay particular attention to three factors as determinants of quality of CSR reports: external verification of the report, using GRI guidelines when developing the report and disclosing CSR information in a form of a stand-alone CSR report. The result of this study concerning the influence of external verification of CSR report on its quality is aligned with the findings of the research of Pflugrath et al. [43] as well as Park and Brorson [44]. External verification has a positive effect on the quality of the CSR reports developed in V4 countries. These results may suggest that companies when decide to verify the data enclosed in CSR report by independent third-party organization, which is associated with additional costs, are more concerned about the content and quality of the report. It can therefore be stated that the independent verificationof the CSR data contained in the report by an external entity contributes to the quality of the report. The second factor that has been found to influence the quality of CSR report is standardization of the report by using the GRI guidelines when developing the report. Prior research by Lock and Seele [35] has found that voluntary standardization with the GRI guidelines affects CSR reporting credibility positively. The findings of this study reveal that there is a positive correlation between using GRI guidelines when preparing the CSR report and the quality of the report in V4 countries. CSR report will only meet its function when its form will resemble financial report, i.e., the report refer to a specific reporting period, contain comparable and reliable data. Credible CSR report can be developed by using international standards and guidelines. Such guidelines define the scope of the reported information so that a company has no possibility to select data and avoid some of them.

6. Conclusions

Analysis of the CSR reporting in V4 countries indicate that these practices are not widespread among companies, yet. It seems that foreign, multinational companies and investors have brought their own CSR policies and models, which national corporations from V4 region have begun to adopt. Amongst the V4 countries, the highest indicator of CSR reporting was achieved by Hungary, followed by the Czech Republic and Poland. The lowest indicator was achieved by Slovakia. The CSR reports from V4 countries are developed most often by large, private and subsidiary companies. These documents are most frequently prepared as separate CSR reports. Nearly a half of the analysed reports were developed in compliance with the GRI Guidelines. External, independent verification of CSR reports in V4 countries is not a very popular practice. Only 16% of the analysed reports were externally verified. The obtained values of the quality indicators of CSR reports form V4 countries suggest the existence of a wide area of improvements in regard to these practices. The study reveals that more weak points refer to the credibility of information disclosed in CSR reports. A lack of independent verification of the data in these reports is a common element that requires special attention in all of the analysed reports. The second important issue is that the reports from V4 countries contain little or no information about procedures of collection and aggregation of the data as well as do not determine the source of disclosed data. The reports also rarely contain information about bidirectional communication and seldom use mechanism that allows for feedback between stakeholders and the reporting companies. A CSR report can be a valuable tool to communicate with both external and internal stakeholders but to fulfil its role, the report should include information which is expected by the interested parties. If stakeholders are involved in the reporting process, the report is likely to include suitable indicators, the data disclosed is authenticated and presented in a way which is understandable for the recipients of the report. Consequently the stakeholders feel satisfied because they find the required information in the report. In terms of relevance of information the executive summary of CSR report achieved the lowest grades. Only some of the reporting companies provide a concise overview of the key information and indicators from the reporting period. A good summary is a practical and helpful element of a report, especially if the report contains several dozen pages or more. In the majority of reports under analysis, such summaries were not included.

The results obtained also point to factors which have an impact on the quality level of the CSR reports. The research results confirm the existence of a positive relationship between the use of the GRI Guidelines in the development of a CSR report and the quality level of that report. When assessing the dependency of the quality level of a report and its external, independent verification, a statistically significant dependency was identified. The correlation coefficient points to the existence of a positive relationship between the use of external verification of a CSR report and the quality level of that report. The quality level of a CSR report is higher in the case of reports which were verified by an external, independent entity.

The research methodology used in the study is limited by various factors. The restrictions relate particularly to three issues. First limitation is related to sample selection. The selection of CSR reports was based on language criteria and thus raises the question of the representativeness of the sample, however, the objective of the research was to assess the current state of CSR reporting practices in the Visegrad Group (V4) countries and only quality assessment was based on CSR reports published in English. Accordingly, the results and conclusions in the scope of quality assessment do not represent the analysis of CSR reports published in native languages. Another limitation of the study is the subjective way of the assessment of the CSR reports based on the substantive knowledge of the examiner. It seems, that in this case it would be more appropriate to carry out the assessment of quality of the reports by more people to balance the subjective views. The third issue which suffers from limitation is determining the level of CSR reporting. The data relating to the number of published reports within a particular country comes from a voluntary database (enterprises are not obliged to deposit their CSR reports in this type of base) and may not necessarily reflect the real state.

The author of the paper is aware that the topic of the study is multidimensional and can provide a basis for further in-depth research. Possible future directions for research in the field of CSR reporting concern several issues. First of all, future research can be extended to CSR reports developed in native languages of the countries selected for the study however it will require establishment of an international research team. Following the introduction of EU Directive 2014/95/EU certain large undertakings and groups in the Member States are expected to provide important information on at least environmental, social and labor issues, human rights, anti-corruption and bribery, as from 2017. Therefore future research should take into account voluntary and mandatory reporting model in quality assessment of CSR reports. Moreover scientists should further investigate cultural context of CSR reporting practices. It may be assumed that the level of maturity of CSR concept in particular country will result in different stakeholders’ requirements to disclose CSR data, thus the external motives for developing CSR report will be different and this in turn can be reflected in the quality of published reports.

It should be noted at this point that the conducted research measured the scope and quality of the information provided by a company in its corporate social responsibility report. The study does not present an assessment or ranking of the company’s actual performance or activities in the area of corporate social responsibility.

Conflicts of Interest

The author declares no conflict of interest.

References

- Kołodziej, S.; Maruszewska, E.W. Economical Effectiveness and Social Objectives in Corporate Social Reports—A Survey among Polish Publicly Traded Companies. Available online: https://www.researchgate.net/profile/Ewa_Maruszewska/publication/307875171_Economical_effectiveness_and_social_objectiveness_in_corporate_social_reports_-_a_survey_among_Polish_publicly_traded_companies/links/582b376b08ae102f07208568/Economical-effectiveness-and-social-objectiveness-in-corporate-social-reports-a-survey-among-Polish-publicly-traded-companies.pdf (accessed on 7 December 2017).

- Michelon, G.; Pilonato, S.; Ricceri, F. CSR reporting practices and the quality of disclosure: An empirical analysis. Crit. Perspect. Account. 2015, 33, 59–78. [Google Scholar] [CrossRef] [Green Version]

- Husillos, J.; Larrinaga, C.; Gil, M.J.A. The emergence of triple bottom line reporting in Spain. Spanish J. Financ. Account. 2011, 40, 195–219. [Google Scholar] [CrossRef]

- Adams, C.A. The ethical, social and environmental reporting—Performance portrayal gap. Account. Audit. Account. J. 2004, 17, 731–757. [Google Scholar] [CrossRef]

- Dando, N.; Swift, T. Transparency and assurance: Minding the Credibility Gap. J. Bus. Ethics 2003, 44, 195–200. [Google Scholar] [CrossRef]

- Gray, R. Is accounting for sustainability actually accounting for sustainability and how would we know? An exploration of narratives of organisations and the planet. Account. Organ. Soc. 2010, 35, 47–62. [Google Scholar] [CrossRef]

- Chen, S.; Bouvain, P. Is Corporate Responsibility Converging? A Comparison of Corporate Responsibility Reporting in the USA, UK, Australia, and Germany. J. Bus. Ethics 2009, 87, 299–317. [Google Scholar] [CrossRef]

- Maignan, I.; Ralston, D.A. Corporate Social Responsibility in Europe and the U.S.: Insights from Businesses’ Self-presentations. J. Int. Bus. Stud. 2002, 33, 497–514. [Google Scholar] [CrossRef]

- Delbard, O. CSR legislation in France and the European regulatory paradox: An analysis of EU CSR policy and sustainability reporting practice. Corp. Gov. Int. J. Bus. Soc. 2008, 8, 397–405. [Google Scholar] [CrossRef]

- Segal, J.P.; Sobczak, A.; Triomphe, C.E. Corporate Social Responsibility and Working Conditions. Available online: http://www.uni-mannheim.de/edz/pdf/ef/03/ef0328en.pdf (accessed on 12 June 2017).

- Antal, A.B.; Sobczak, A. Corporate Social Responsibility in France: A Mix of National Traditions and International Influences. Bus. Soc. 2007, 46, 9–32. [Google Scholar] [CrossRef] [Green Version]

- Hąbek, P.; Wolniak, R. Assessing the quality of corporate social responsibility reports: The case of reporting practices in selected European Union member states. Qual. Quant. 2015, 50, 399–420. [Google Scholar] [CrossRef] [PubMed]

- Ruževičius, J.; Serafinas, D. The Development of Socially Responsible Business in Lithuania. Eng. Econ. 2015, 51, 36–43. [Google Scholar]

- Dočekalová, M. Corporate Sustainability Reporting in Czech Companies—Case Studies. Trends Econ. Manag. 2012, 6, 9–16. [Google Scholar]

- Petera, P.; Wagner, J.; Boučková, M. An Empirical Investigation into CSR Reporting by the Largest Companies with their seat in the Czech Republic. In Proceedings of the 22nd Interdisciplinary Information Management Talks, Podebrady, Czech Republic, 10–12 September 2014; pp. 321–329. [Google Scholar]

- Kunz, V.; Srpová, J. CSR Reporting and its Use by Enterprises in the Czech Republic. Manag. Sci. Educ. 2013, 1, 31–34. [Google Scholar]

- Karcagi-Kováts, A.; Kuti, I. Diversity of Sustainability Performance Indicators and Corporate Reporting in Hungary. In Proceedings of the Corporate Responsibility Research Conference CRRC, Marseille, France, 15–17 September 2010. [Google Scholar]

- Piskóti, I.; Hajdú, N. A Benchmarking Approach to the Situation and Topics in CSR Reports of Hungarian Corporations, Responsibility and Sustainability. Socioecon. Political Legal Issues 2013, 2, 1–13. [Google Scholar]

- Hąbek, P. Evaluation of sustainability reporting practices in Poland. Qual. Quant. 2014, 48, 1739–1752. [Google Scholar] [CrossRef]

- Astupan, D.; Schönbohm, A. Sustainability Reporting Performance in Poland: Empirical Evidence from the WIG 20 and WIG 40 Companies. Pol. J. Manag. Stud. 2012, 6, 68–80. [Google Scholar]

- Szczepankiewicz, E.I.; Mućko, P. CSR Reporting Practices of Polish Energy and Mining Companies. Sustainability 2016, 8, 126. [Google Scholar] [CrossRef]

- Kubaščíková, Z. Sustainable Development Reporting. Manag. Inf. Syst. 2008, 3, 19–23. [Google Scholar]

- Freundlieb, M.; Gräuler, M.; Teuteberg, F. A conceptual framework for the quality evaluation of sustainability reports. Manag. Res. Rev. 2014, 37, 19–44. [Google Scholar] [CrossRef]

- Hąbek, P.; Brodny, J. Corporate Social Responsibility Report—An Important Tool to Communicate with Stakeholders. In Proceedings of the 4th International Multidisciplinary Scientific Conference on Social Sciences & Arts, Albena, Bulgaria, 22–31 August 2017; pp. 241–248. [Google Scholar]

- Daub, C.-H. Assessing the quality of sustainability reporting: An alternative methodological approach. J. Clean. Prod. 2007, 15, 75–85. [Google Scholar] [CrossRef]

- Ching, H.Y.; Gerab, F.; Toste, T. Analysis of Sustainability Reports and Quality of Information Disclosed of Top Brazilian Companies. Int. Bus. Res. 2013, 6, 62–77. [Google Scholar] [CrossRef]

- G4 Sustainability Reporting Guidelines. Reporting Principles and Standard Disclosures. Available online: https://www.globalreporting.org/resourcelibrary/GRIG4-Part1-Reporting-Principles-and-Standard-Disclosures.pdf (accessed on 7 December 2017).

- Sustainable Development Reporting—Striking the Balance. Available online: http://www.wbcsd.org/Projects/Reporting/Resources/Sustainable-Development-Reporting-Striking-the-balance (accessed on 7 December 2017).

- Leitonienea, S.; Sapkauskiene, A. Quality of Corporate Social Responsibility Information. Procedia Soc. Behav. Sci. 2015, 213, 334–339. [Google Scholar] [CrossRef]

- Baviera-Puig, A.; Gómez-Navarro, T.; García-Melón, M.; García-Martínez, G. Assessing the Communication Quality of CSR Reports. A Case Study on Four Spanish Food Companies. Sustainability 2015, 7, 11010–11031. [Google Scholar] [CrossRef]

- Legendre, S.; Coderre, F. Determinants of GRI G3 application levels: The case of the Fortune Global 500. Corp. Soc. Responsib. Environ. Manag. 2013, 20, 182–192. [Google Scholar] [CrossRef]

- Ruhnke, K.; Gabriel, A. Determinants of voluntary assurance on sustainability reports: An empirical analysis. J. Bus. Econ. 2013, 83, 1063–1091. [Google Scholar] [CrossRef]

- Bachoo, K.; Tan, R.; Wilson, M. Firm value and the quality of sustainability reporting in Australia. Aust. Account. Rev. 2013, 23, 67–87. [Google Scholar] [CrossRef]

- Zorio, A.; García-Benau, M.A.; Sierra, L. Sustainability development and the quality of assurance reports: Empirical evidence. Bus. Strategy Environ. 2013, 22, 484–500. [Google Scholar] [CrossRef]

- Lock, I.; Seele, P. The credibility of CSR reports in Europe. Evidence from a quantitative content analysis in 11 countries. J. Clean. Prod. 2016, 122, 186–200. [Google Scholar] [CrossRef]

- Hahn, R.; Kühnen, M. Determinants of sustainability reporting: A review of results, trends, theory, and opportunities in an expanding field of research. J. Clean. Prod. 2013, 59, 5–21. [Google Scholar] [CrossRef]

- Beretta, S.; Bozzolan, S. Quality versus Quantity: The Case of Forward-Looking Disclosure. J. Account. Audit. Financ. 2008, 23, 333–376. [Google Scholar] [CrossRef]

- Kuzey, C.; Uyar, A. Determinants of sustainability reporting and its impact on firm value: Evidence from the emerging market of Turkey. J. Clean. Prod. 2016, 143, 27–39. [Google Scholar] [CrossRef]

- Bluszcz, A. A comparative analysis of selected synthetic indicators of sustainability. Procedia Soc. Behav. Sci. 2016, 220, 40–50. [Google Scholar] [CrossRef]

- Jonek-Kowalska, I.; Zieliński, M. CSR Activities in the Banking Sector in Poland. In Proceedings of the 29th International-Business-Information-Management-Association Conference, Vienna, Austria, 3–4 May 2017; pp. 1294–1304. [Google Scholar]

- Cierna, H.; Sujova, E. Parallels Between Corporate Social Responsibility and the EFQM Excellence Model. MM Sci. J. 2015, 670–676. [Google Scholar] [CrossRef]

- Hąbek, P.; Molenda, M. Using the FMEA Method as a Support for Improving the Social Responsibility of a Company. In Proceedings of the 6th International Conference on Operations Research and Enterprise Systems (ICORES 2017), Porto, Portugal, 23–25 February 2017; pp. 57–65. [Google Scholar]

- Pflugrath, G.; Roebuck, P.; Simnett, R. Impact of assurance and assurer’s professional affiliation on financial analysts’ assessment of credibility of corporate social responsibility information. Audit. J. Pract. Theory 2011, 30, 239–254. [Google Scholar] [CrossRef]

- Park, J.; Brorson, T. Experiences of and views on third-party assurance of corporate environmental and sustainability reports. J. Clean. Prod. 2015, 13, 1095–1106. [Google Scholar] [CrossRef]

- Alavi, H.; Hąbek, P. Addressing Research Design Problem in Mixed Methods Research. Manag. Syst. Prod. Eng. 2016, 21, 62–66. [Google Scholar] [CrossRef]

- GRI’s Sustainability Disclosure Database. Available online: http://database.globalreporting.org (accessed on 17 January 2017).

- Wolniak, R. The role of Grenelle II in Corporate Social Responsibility Integrated Reporting. Manag. J. 2013, 18, 109–119. [Google Scholar]

- Eurostat Data—Business Demography by Size Class (NACE Rev. 2) in 2014, Business Economy except Activities of Holding Companies. Available online: http://ec.europa.eu/eurostat/statistics-explained/index.php/Business_demography_regional_analysis (accessed on 11 January 2017).

- UNGC Website. Available online: https://www.unglobalcompact.org/what-is-gc/participants (accessed on 29 December 2016).

- Hąbek, P. How do companies in European Union disclose their non-financial data? In Proceedings of the International Masaryk Conference for Ph.D. Students and Young Researchers, Hradec Kralove, Czech Republic, 9–13 December 2013; pp. 92–100. [Google Scholar]

Figure 1.

The results for each criterion in the assessment of the quality of CSR reports in the sample.

Figure 1.

The results for each criterion in the assessment of the quality of CSR reports in the sample.

{kind=link}

Table 1.

The summary of studies on quality of information disclosed in CSR reports.

| Authors | Methods/Sample | Quantity Analysis | Quality Analysis | Findings |

|---|---|---|---|---|

| Michelon, G.; Pilonato, S.; Ricceri, F. (2015) | Content analysis, Global Reporting Initiative framework used to assess CSR information disclosures,112 UK companies | x | x | On average, companies that use CSR reporting practices do not provide a higher quality of information. |

| Ching, H.Y.; Gerab, F.; Toste, T. (2013) | Content analysis, 60 listed Brazilian companies, the Global Reporting Initiative framework used to assess the reports | x | Sustainability reports still have a big room for improvement. Companies need to disclose their information in a more integrated way, addressing sustainability issues under the scope of business strategy. | |

| Daub, C.-H.J. (2007) | 76 companies/33 individual criteria, benchmark study, Swiss companies ranked according to the total score, | x | An evaluation of the performance of the reporting company resulted in a clear weakness in reporting performance indicators. | |

| Leitonienea, S.; Sapkauskiene, A. (2015) | Quality index/48 reports of socially responsible Lithuanian companies | x | The results of the quality of information showed that the quality index of joint stock companies is higher, which belong to those sectors which have a significant impact on the environment, i.e., manufacturing, energy and telecommunications. | |

| Baviera-Puig, A.; Gómez-Navarro, T.; García-Melón, M.; García-Martínez, G. (2015) | Multi-criteria methodology, using the Analytic Network Process, large food Spanish companies | x | Results show varying degrees of quality in the communication of different enterprises from the same sector. This assessment highlights the weaknesses and areas for improvement of each of the reports analyzed from a multi-stakeholder point of view. | |

| Lock, I.; Seele, P. (2016) | Quantitative content analysis, the credibility of 237 European CSR reports is studied, human as well as software coding was applied, listed companies from Austria, Belgium, France, Germany, Italy, The Netherlands, Poland, Spain, Sweden | x | CSR reports are credible at a mediocre level, leaving much room for improvement. Reports must be understandable, before truth, sincerity, appropriateness are addressed. | |

| Hąbek, P.; Wolniak, R. (2015) | Quality disclosure index/507 CSR reports assessed from UK, France, The Netherlands, Sweden, Denmark, Poland | x | The quality level of the studied reports is generally low, and there is space for improvement in all studied countries. Referring to the components of the quality indicator, the relevance of the information provided in the assessed reports is at a higher level than its credibility. |

Table 2.

Number of reports from V4 countries admitted to the study.

| Country | No. of Reports in the GRI Sustainability Disclosure Database Published in 2014 | CSR Reports Admitted to Analysis of Current CSR Reporting Practices in V4 Countries | No. of CSR Reports Admitted to Quality Assessment (Reports only in English) |

|---|---|---|---|

| Czech Republic | 20 | 20 | 7 |

| Hungary | 30 | 22 | 14 |

| Poland | 36 | 36 | 20 |

| Slovakia | 4 | 4 | 3 |

Table 3.

The structure of quality assessment tool.

| Assessment Criteria: Relevance of Information | Scale | |||||

| 0 | 1 | 2 | 3 | 4 | ||

| R1 | Corporate social responsibility strategy The report presents the business strategy which relates to the aspects of CSR | |||||

| R2 | Key stakeholders The report contains identification of organization’s stakeholders, their expectations and a way of engagement with individual groups | |||||

| R3 | Targets The report presents targets for the future, targets set in the previous reporting period and the level of their achievements | |||||

| R4 | Trends over time The report contains indicators shown over several reporting periods indicating this way direction of change and ensuring their comparability | |||||

| R5 | Performance indicators: market place The report contains quantitative information concerning organization’s performance achieved in area of market place | |||||

| R6 | Performance indicators: workplace The report contains quantitative information concerning organization’s performance achieved in area of workplace | |||||

| R7 | Performance indicators: environment The report contains quantitative information concerning organization’s performance achieved in area of environment | |||||

| R8 | Performance indicators: community The report contains quantitative information concerning organization’s performance achieved in area of community | |||||

| R9 | Improvement actions The report describes improvement activities undertaken by the organization in the scope of CSR, e.g., programs to increase resource efficiency, reduction of emission, etc. | |||||

| R10 | Integration with business processes The report contains information confirming that the aspects of CSR are included in the decision-making process and implemented in the basic processes (purchasing, sales, marketing, production, etc.) | |||||

| R11 | Executive summary The report provides a concise and balanced overview of key information and indicators from the reporting period | |||||

| Assessment Criteria: Credibility of Information | Scale | |||||

| 0 | 1 | 2 | 3 | 4 | ||

| C1 | Readability The report has a logical structure, uses a graphical presentation of the data, drawings, and explanations where required or uses other tools to help navigate through the document | |||||

| C2 | Basic reporting principles The reporting period, scope and entity are defined in the report as well as limitations and target audience | |||||

| C3 | Quality of data The report describes the processes, procedures of collection, aggregation and transformation of data and determines the source of the data | |||||

| C4 | Stakeholder dialogue outcomes The report contains a description of the stakeholders’ dialogue and the results of this dialogue in relation to aspects of CSR (surveys, consultations, focus groups, round Tables, programs, engagement, etc.) | |||||

| C5 | Feedback The report contains a mechanism that allows a feedback process (contact point for suggestions or questions, hotline, email, reply card, questionnaire, etc.) | |||||

| C6 | Independent verification The report contains a statement of independent body attesting the authenticity of data presented in the report as well as proposals for future improvements | |||||

Source: [12].

Table 4.

Scoring system.

| Scores | Assessment Requirements |

|---|---|

| 0 | No mention or insufficient information on individual criteria |

| 1 | Some/little/partial mention or coverage |

| 2 | Most important aspects covered, average |

| 3 | Better than average, the report presents detailed information |

| 4 | Best practices and creative approach, innovative disclosure and explanation |

Table 5.

Number of CSR reports and number of reports per million enterprises in V 4 countriesStates.

Table 5.

Number of CSR reports and number of reports per million enterprises in V 4 countriesStates.

| EU Member State | CSR Report 2014 | Population of Active Enterprises * | No. of Reports per Million Enterprises |

|---|---|---|---|

| Czech Republic | 20 | 1,022,045 | 19.6 |

| Hungary | 30 | 522,058 | 57.5 |

| Poland | 36 | 2,025,270 | 17.8 |

| Slovakia | 4 | 438,067 | 9.1 |

* Data according to: GRI database and Eurostat (business demography by size class in 2014).

Table 6.

Number of UN Global Compact signatories from V4 countries.

| Country | Czech Republic | Hungary | Poland | Slovakia |

|---|---|---|---|---|

| Number of signatory (type: company and SME) | 14 | 7 | 67 | 4 |

Source: based on data gathered from [49].

Table 7.

Number of UN Global Compact signatories from V4 countries.

| Country | Organization Size | Organization Type | ||||||

|---|---|---|---|---|---|---|---|---|

| SME | Large | MNE | Listed | Private | Subsidiary | State-Owned | Others | |

| Czech Republic N = 20 | - | 40% | 60% | 40% | 40% | 45% | 10% | 5% |

| Hungary N = 22 | 14% | 36% | 50% | 27% | 23% | 50% | 18% | 9% |

| Poland N = 36 | 8% | 86% | 6% | 44% | 61% | 25% | 11% | 3% |

| Slovakia N = 4 | - | 100% | - | - | 25% | 75% | - | - |

| Total V4 | 7% | 62% | 31% | 37% | 44% | 39% | 12% | 5% |

Table 8.

Characteristic of reports in the sample.

| Country | Separate CSR Report | Annual Report with CSR Section | Integrated Report | Report according to GRI | Independent Verification | UN Global Compact Signatory |

|---|---|---|---|---|---|---|

| Czech Republic N = 20 | 95% | 5% | - | 20% | 5% | - |

| Hungary N = 22 | 91% | - | 9% | 59% | 23% | 18% |

| Poland N = 36 | 75% | 3% | 22% | 47% | 22% | 28% |

| Slovakia N = 4 | 100% | - | - | 50% | - | 25% |

| Total V4 | 85% | 2% | 12% | 44% | 16% | 18% |

Table 9.

Distribution of countries from which the investigated CSR reports originated.

| Country | Number in Sample | Percentage |

|---|---|---|

| Czech Republic | 7 | 15.91 |

| Hungary | 14 | 31.82 |

| Poland | 20 | 45.45 |

| Slovakia | 3 | 6.82 |

Table 10.

Descriptive statistics and results of the test for normal distribution for the level of quality of CSR reports and its components.

Table 10.

Descriptive statistics and results of the test for normal distribution for the level of quality of CSR reports and its components.

| Variable | M | SD | Mdn | Min | Max | S-W | p |

|---|---|---|---|---|---|---|---|

| Relevance of information—R | 1.87 | 0.80 | 1.95 | 0.27 | 3.27 | 0.95 | 0.036 |

| Credibility of information—C | 1.86 | 0.83 | 2.00 | 0.33 | 3.33 | 0.94 | 0.018 |

| Quality of CSR reports—Q | 1.86 | 0.78 | 2.04 | 0.30 | 3.30 | 0.95 | 0.049 |

Note: M—mean; SD—standard deviation; Mdn—median; S-W—Shapiro-Wilk test value; p—probability value.

Table 11.

The GRI guidelines and the level of quality of CSR reports.

| Variable | GRI | M | SD | Min | Max | Z | p |

|---|---|---|---|---|---|---|---|

| Relevance of information—R | No (n = 8) | 1.16 | 0.72 | 0.36 | 2.27 | 2.65 | 0.007 |

| Yes (n = 36) | 2.03 | 0.74 | 0.27 | 3.27 | |||

| Credibility of information—C | No (n = 8) | 0.83 | 0.53 | 0.50 | 2.00 | 3.53 | <0.001 |

| Yes (n = 36) | 2.08 | 0.71 | 0.33 | 3.33 | |||

| Quality of CSR reports—Q | No (n = 8) | 1.00 | 0.60 | 0.43 | 2.14 | 3.23 | 0.001 |

| Yes (n = 36) | 2.05 | 0.68 | 0.30 | 3.30 |

Note: n—number in subsample; M—mean; SD—standard deviation; Z—Mann-Whitney test value; p—probability value.

Table 12.

The correlation coefficient between the use of the GRI guidelines and the level of quality indicator (Q).

Table 12.

The correlation coefficient between the use of the GRI guidelines and the level of quality indicator (Q).

| GRI | ||

|---|---|---|

| Spearman’s Rho | p-Value | |

| Quality of CSR reports—Q | 0.49 | 0.001 |

Table 13.

Independent verification and the level of quality indicator (Q).

| Variable | Independent Verification | M | SD | Min | Max | Z | p |

|---|---|---|---|---|---|---|---|

| Relevance of information—R | No (n = 31) | 1.72 | 0.86 | 0.27 | 3.27 | 2.05 | 0.040 |

| Yes (n = 13) | 2.23 | 0.48 | 1.45 | 3.00 | |||

| Credibility of information—C | No (n = 31) | 1.57 | 0.80 | 0.33 | 3.33 | 3.80 | <0.001 |

| Yes (n = 13) | 2.54 | 0.43 | 1.83 | 3.33 | |||

| Quality of CSR reports—Q | No (n = 31) | 1.64 | 0.79 | 0.30 | 3.30 | 2.97 | 0.003 |

| Yes (n = 13) | 2.38 | 0.41 | 1.81 | 3.17 |

Note: n—number in subsample; M—mean; SD—standard deviation; Z—U Mann-Whitney test value; p—probability value.

Table 14.

The correlation coefficient between the use of independent verification and the level of quality indicator (Q).

Table 14.

The correlation coefficient between the use of independent verification and the level of quality indicator (Q).

| Independent Verification | ||

|---|---|---|

| Spearman’s Rho | p-Value | |

| Quality of CSR reports—Q | 0.45 | 0.002 |

© 2017 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Hąbek, P. CSR Reporting Practices in Visegrad Group Countries and the Quality of Disclosure. Sustainability 2017, 9, 2322. https://doi.org/10.3390/su9122322

AMA Style

Hąbek P. CSR Reporting Practices in Visegrad Group Countries and the Quality of Disclosure. Sustainability. 2017; 9(12):2322. https://doi.org/10.3390/su9122322

Chicago/Turabian StyleHąbek, Patrycja. 2017. "CSR Reporting Practices in Visegrad Group Countries and the Quality of Disclosure" Sustainability 9, no. 12: 2322. https://doi.org/10.3390/su9122322

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.