Reporting on Long-Term Value Creation—The Example of Public Canadian Energy and Mining Companies

Abstract

:1. Introduction

2. Materials and Methods

Development of Hypothesis

Control Variables

Sample and Methodology

Dependent Variable

Independent Variables

Control Variables

3. Results

4. Discussion and Conclusions

Conflicts of Interest

References

- Carroll, A.B. Ethics in Management. A Companion to Business Ethics; Wiley: New York, NY, USA, 1999; pp. 141–152. [Google Scholar]

- Lungu, C.I.; Caraiani, C.; Dascalu, C.; Guse, R.; Sahlian, D. Corporate Social and Environmental Reporting: Another Dimension for Accounting Information. Available online: http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1447247 (accessed on 22 May 2016).

- Beretta, S.; Bozzolan, S. A framework for the analysis of firm risk communication. Int. J. Account. 2004, 39, 265–288. [Google Scholar] [CrossRef]

- Boesso, G. How to Assess the Quality of Voluntary Disclosures. Available online: http://papers.ssrn.com/sol3/papers.cfm?abstract_id=826451 (accessed on 22 May 2016).

- Frost, G.; Jones, S.; Loftus, J.; Laan, S. A Survey of Sustainability Reporting Practices of Australian Reporting Entities. Aust. Account. Rev. 2005, 15, 89–96. [Google Scholar] [CrossRef]

- The KPMG Survey of Corporate Responsibility Reporting 2013. Available online: http://www.kpmg.com/Global/en/IssuesAndInsights/ArticlesPublications/corporate-responsibility/Documents/corporate-responsibility-reporting-survey-2013-v2.pdf (accessed on 22 May 2016).

- Vurro, C.; Perrini, F. Making the most of corporate social responsibility reporting: Disclosure structure and its impact on performance. Corp. Gov. 2011, 11, 459–474. [Google Scholar]

- Eng, L.; Mak, Y. Corporate governance and voluntary disclosure. J. Account. Public Policy 2003, 22, 325–345. [Google Scholar] [CrossRef]

- Jaggi, B.; Low, P.Y. Impact of Culture, Market Forces, and Legal System on Financial Disclosures. Int. J. Account. 2000, 35, 495–519. [Google Scholar] [CrossRef]

- PWC. Integrated Reporting: Companies Struggle to Explain What Value They Create. 2013. Available online: https://www.pwc.nl/nl/assets/documents/ir-opmars-geintegreerde-verslaggeving-stagneert.pdf (accessed on 22 May 2016).

- OECD. Corporate Responsibility Practices of Emerging Market Companies. 2005. Available online: https://www.oecd.org/corporate/mne/WP-2005_3.pdf (accessed on 13 September 2016).

- Tschopp, D.; Huefner, R.J. Comparing the Evolution of CSR Reporting to that of Financial Reporting. J. Bus. Ethics 2014, 127, 565–577. [Google Scholar] [CrossRef]

- AccountAbility. AccountAbility 1000 (AA1000) Framework Standards, Guidelines and Professional Qualification. Available online: http://www.accountability.org/ (accessed on 22 May 2016).

- Global Reporting Initiative. The Sustainability Content of Integrated Reports—A Survey of Pioneers. 2013. Available online: https://www.globalreporting.org/resourcelibrary/GRI-IR.pdf (accessed on 22 May 2016).

- Global Reporting Initiative. May 2013. G4 Sustainability Reporting Guidelines, GRI. Available online: https://www.globalreporting.org/standards/g4/pages/default.aspx (accessed on 22 May 2016).

- GRI G4 Mining & Metal Supplement. 2013. Available online: https://www.globalreporting.org/ (accessed on 8 September 2016).

- Global Reporting Initiative. Available online: https://www.globalreporting.org/resourcelibrary/gri-g4-mining-and-metals-sector-disclosures.pdf (accessed on 29 May 2016).

- Dilling, P.F.A. Stakeholder perception of corporate social responsibility. Int. J. Manag. Mark. Res. 2011, 4, 23–34. [Google Scholar]

- Sustainability Accounting Standards Board. 2014. Available online: http://www.sasb.org (accessed on 3 March 2016).

- Jenkins, H. Corporate social responsibility and the mining industry: Conflicts and constructs. Corp. Soc. Responsib. Environ. Manag. 2004, 11, 23–34. [Google Scholar] [CrossRef]

- Deloitte Touche Tohmatsu. Tracking the Trends 2015. The Top 10 Issues Mining Companies Will Face This Year. Tracking the Trends 2015 Keep Calm and Carry on, Deloitte. 2015. Available online: https://www2.deloitte.com/content/dam/Deloitte/fpc/Documents/secteurs/energie-et-ressources/deloitte_etude-tracking-the-trends-2015-en.pdf (accessed on 29 May 2016).

- Sustainable Development and Corporate Social Responsibility: Tools, Codes and Standards for the Mineral Exploration Industry. Prospectors & Developers Association of Canada (PDAC), 2007. Available online: http://www.pdac.ca/docs/default-source/public-affairs/csr-sustainable-development.pdf?sfvrsn=8 (accessed on 22 May 2016).

- ICCM. Sustainable Development Framework. 2012. Available online: http://www.icmm.com/our-work/sustainable-development-framework (accessed on 29 May 2016).

- Oil and Gas Industry Guidance on Voluntary Sustainability Reporting, 2nd ed. Available online: http://www.api.org/~/media/files/ehs/environmental_performance/voluntary-sustainability-reporting-guidance-2015.pdf?la=en (accessed on 30 May 2016).

- Dilling, P.F.A. Long-term value creation, corporate social responsibility and integrated reporting: The example of Canadian mining and energy companies. In Proceedings of the 20th Annual International Sustainable Development Research Conference, Trondheim, Norway, 18–20 June 2014; pp. 439–446.

- International Integrated Reporting Council (IIRC). 2015. Available online: http://integratedreporting.org (accessed on 20 April 2016).

- International Integrated Reporting Council (IIRC). International Framework. 2013. Available online: http://integratedreporting.org/resource/international-ir-framework (accessed on 30 May 2016).

- IRRC Institute and Sustainable Investments Institute. Integrated Financial and Sustainability Reporting in the United States. 2013. Available online: http://irrcinstitute.org/wp-content/uploads/2015/09/FINAL_Integrated_Financial_Sustain_Reporting_April_20131.pdf (accessed on 3 May 2016).

- Eccles, R.G.; Krzus, M.P. One Report: Integrated Reporting for a Sustainable Strategy; John Wiley & Sons: Hoboken, NJ, USA, 2010. [Google Scholar]

- Integrated Reporting Committee South Africa (IRC SA). Framework for Integrated Reporting and the Integrated Report Discussion Paper. 2011. Available online: http://www.sustainabilitysa.org/Portals/0/IRC%20of%20SA%20Integrated%20Reporting%20Guide%20Jan%2011.pdf (accessed on 22 May 2016).

- GRI and IIRC Deepen Cooperation to Shape the Future of Corporate Reporting, Global Reporting Initiative. 1 March 2013. Available online: https://www.globalreporting.org/information/news-and-press-center/pages/gri-and-iirc-deepen-cooperation-to-shape-the-future-of-corporate-reporting.aspx (accessed on 30 May 2016).

- Deegan, C. Financial Accounting Theory; McGraw-Hill: Sydney, Australia, 2000. [Google Scholar]

- Chan, M.C.; Watson, J.; Woodliff, D. Corporate Governance Quality and CSR Disclosures. J. Bus. Ethics 2013, 125, 59–73. [Google Scholar] [CrossRef]

- Freeman, R.E. Strategic Management: A Stakeholder Approach; Cambridge University Press: Cambridge, MA, USA, 2010. [Google Scholar]

- Campbell, D.; Craven, B.; Shrives, P. Voluntary social reporting in three FTSE sectors: A comment on perception and legitimacy. Acc. Audit. Account. J. 2003, 16, 558–581. [Google Scholar] [CrossRef]

- Cho, C.H.; Patten, D.M. The role of environmental disclosures as tools of legitimacy: A research note. Account. Organ. Soc. 2007, 32, 639–647. [Google Scholar] [CrossRef]

- Brammer, S.; Pavelin, S. Voluntary Environmental Disclosures by Large UK Companies. J. Bus. Financ. Account. 2006, 33, 1168–1188. [Google Scholar] [CrossRef]

- Clarkson, P.M.; Li, Y.; Richardson, G.D.; Vasvari, F.P. Revisiting the relation between environmental performance and environmental disclosure: An empirical analysis. Account. Organ. Soc. 2008, 33, 303–327. [Google Scholar] [CrossRef]

- Mining Financial Reporting Survey 2014. KPMG Canada. 2014. Available online: https://www.kpmg.com/ca/en/issuesandinsights/articlespublications/documents/kpmg-mining-financial-reporting-survey-2014.pdf (accessed on 23 May 2016).

- Horowitz, L. Section 2: Mining and sustainable development. J. Clean. Prod. 2006, 14, 307–308. [Google Scholar] [CrossRef]

- Yongvanich, K.; Guthrie, J. Extended performance reporting: An examination of the Australian mining industry. Account. Forum 2005, 29, 103–119. [Google Scholar] [CrossRef]

- Gray, R.; Javad, M.; Power, D.M.; Sinclair, C.D. Social and Environmental Disclosure and Corporate Characteristics: A Research Note and Extension. J. Bus. Financ. Account. 2001, 28, 327–356. [Google Scholar] [CrossRef]

- Jenkins, H.; Yakovleva, N. Corporate social responsibility in the mining industry: Exploring trends in social and environmental disclosure. J. Clean. Prod. 2006, 14, 271–284. [Google Scholar] [CrossRef]

- Dong, S. An Assessment of CSR Reporting Practice in China’s Mining and Minerals Industry. UNISA, 2012. Available online: https://www.unisa.edu.au/global/business/centres/cags/docs/seminars/paper%20shidi.pdf (accessed on 30 May 2016).

- Adams, C.A.; Hill, W.-Y.; Roberts, C.B. Corporate Social Reporting Practices in Western Europe: Legitimating Corporate Behaviour? Br. Account. Rev. 1998, 30, 1–21. [Google Scholar] [CrossRef]

- Kolk, A.; Walhain, S.; Wateringen, S.V.D. Environmental reporting by the Fortune Global 250: Exploring the influence of nationality and sector. Bus. Strategy Environ. 2001, 10, 15–28. [Google Scholar] [CrossRef]

- Scott, P. The Rise of Reporting. Available online: https://www.unisa.edu.au/global/business/centres/cags/docs/seminars/paper%20shidi.pdf (accessed on 12 September 2016).

- Guenther, E.; Hoppe, H.; Poser, C. Environmental Corporate Social Responsibility of Firms in the Mining and Oil and Gas Industries. Greener Manag. Int. 2006, 2006, 6–25. [Google Scholar] [CrossRef]

- Halme, M.; Huse, M. The influence of corporate governance, industry and country factors on environmental reporting. Scand. J. Manag. 1997, 13, 137–157. [Google Scholar] [CrossRef]

- Mammatt, J.; Marx, B.; vanDyk, V. Sustainability Reporting and Assurance: The Way of the Future. Available online: http://www.accountancysa.org.za/special-report-sustainability-2009-7/ (accessed on 12 September 2016).

- National Research Council. Emerging Workforce Trends in the U.S. Energy and Mining Industries: A Call to Action; National Academies Press: Washington, DC, USA, 2013. [Google Scholar]

- Perez, F.; Sanchez, L.E. Assessing the Evolution of Sustainability Reporting in the Mining Sector. Environ. Manag. 2009, 43, 949–961. [Google Scholar] [CrossRef] [PubMed]

- Bewley, K.; Magness, V. Environmental Disclosure in the Canadian Resource Industry—The Impact of Reporting Regulations. Available online: http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1741602 (accessed on 12 September 2016).

- Brown, J.; Dillard, J. Integrated reporting: On the need for broadening out and opening up. Account. Audit. Account. J. 2014, 27, 1120–1156. [Google Scholar]

- Kiron, D. Sustainability nears a tipping point. Strategy Dir. 2012, 53, 2. [Google Scholar] [CrossRef]

- Haller, A.; Staden, C.V. The value added statement—An appropriate instrument for Integrated Reporting. Account. Audit. Account. J. 2014, 27, 1190–1216. [Google Scholar]

- Eccles, R.G.; Herz, R.H.; Keegan, E.M.; Philips, D.M.H. The Value Reporting Revolution (Publication); Price Waterhouse Coopers: New York, NY, USA, 2001. [Google Scholar]

- Ritter, T.; Gemünden, H.G. Network competence. J. Bus. Res. 2003, 56, 745–755. [Google Scholar] [CrossRef]

- Shaukat, A.; Qiu, Y.; Trojanowski, G. Board Attributes, Corporate Social Responsibility Strategy, and Corporate Environmental and Social Performance. J. Bus. Ethics 2015, 135, 569–585. [Google Scholar] [CrossRef] [Green Version]

- Zeng, S.X.; Xu, X.D.; Yin, H.T.; Tam, C.M. Factors that Drive Chinese Listed Companies in Voluntary Disclosure of Environmental Information. J. Bus. Ethics 2011, 109, 309–321. [Google Scholar] [CrossRef]

- Hackston, D.; Milne, M.J. Some determinants of social and environmental disclosures in New Zealand companies. Account. Audit. Account. J. 1996, 9, 77–108. [Google Scholar] [CrossRef]

- Monteiro, S.M.D.S.; Aibar-Guzmán, B. Determinants of environmental disclosure in the annual reports of large companies operating in Portugal. Corp. Soc. Responsib. Environ. Manag. 2009, 17, 185–204. [Google Scholar] [CrossRef]

- Boesso, G.; Kumar, K. Stakeholder prioritization and reporting: Evidence from Italy and the US. Account. Forum 2009, 33, 162–175. [Google Scholar] [CrossRef]

- Burgwal, D.V.D.; Vieira, R.J.O. Determinantes da divulgação ambiental em companhias abertas holandesas. Rev. Contab. Finanç. 2014, 25, 60–78. [Google Scholar] [CrossRef]

- Bebbington, J.; Larrinaga, C.; Moneva, J.M. Corporate social reporting and reputation risk management. Account. Audit. Account. J. 2008, 21, 337–361. [Google Scholar] [CrossRef]

- Chauvey, J.-N.; Giordano-Spring, S.; Cho, C.H.; Patten, D.M. The Normativity and Legitimacy of CSR Disclosure: Evidence from France. J. Bus. Ethics 2014, 130, 789–803. [Google Scholar] [CrossRef]

- Dierkes, M.; Preston, L.E. Corporate social accounting reporting for the physical environment: A critical review and implementation proposal. Account. Organ. Soc. 1977, 2, 3–22. [Google Scholar] [CrossRef]

- Hall, R. A framework linking intangible resources and capabilities to sustainable competitive advantage. Strateg. Manag. J. 1993, 14, 607–618. [Google Scholar] [CrossRef]

- Healy, P.M.; Palepu, K.G. Information asymmetry, corporate disclosure, and the capital markets: A review of the empirical disclosure literature. J. Account. Econ. 2001, 31, 405–440. [Google Scholar] [CrossRef]

- Thijssens, T.; Bollen, L.; Hassink, H. Secondary Stakeholder Influence on CSR Disclosure: An Application of Stakeholder Salience Theory. J. Bus. Ethics 2015, 132, 873–891. [Google Scholar] [CrossRef]

- Unerman, J. Methodological issues—Reflections on quantification in corporate social reporting content analysis. Account. Audit. Account. J. 2000, 13, 667–681. [Google Scholar] [CrossRef]

- Zeghal, D.; Ahmed, S.A. Comparison of Social Responsibility Information Disclosure Media Used by Canadian Firms. Account. Audit. Account. J. 1990, 3. [Google Scholar] [CrossRef]

- Abbott, W.F.; Monsen, R.J. On the Measurement of Corporate Social Responsibility: Self-Reported Disclosures as a Method of Measuring Corporate Social Involvement. Acad. Manag. J. 1979, 22, 501–515. [Google Scholar] [CrossRef]

- Krippendorf, K. Content Analysis: An Introduction to Its Methodology; Sage Publications: New York, NY, USA, 2013. [Google Scholar]

- Al-Tuwaijri, S.A.; Christensen, T.E.; Hughes, K. The Relations among Environmental Disclosure, Environmental Performance, and Economic Performance: A Simultaneous Equations Approach. Available online: http://papers.ssrn.com/sol3/papers.cfm?abstract_id=405643 (accessed on 30 June 2015).

- Guthrie, J.; Petty, R.; Yongvanich, K.; Ricceri, F. Using content analysis as a research method to inquire into intellectual capital reporting. J. Intell. Capit. 2004, 5, 282–293. [Google Scholar] [CrossRef]

- Beck, A.C.; Campbell, D.; Shrives, P.J. Content analysis in environmental reporting research: Enrichment and rehearsal of the method in a British–German context. Br. Account. Rev. 2010, 42, 207–222. [Google Scholar] [CrossRef]

- Govindan, K.; Kannan, D.; Shankar, K.M. Evaluating the drivers of corporate social responsibility in the mining industry with multi-criteria approach: A multi-stakeholder perspective. J. Clean. Prod. 2014, 84, 214–232. [Google Scholar] [CrossRef]

- Mining Association of Canada. Mining Facts. Available online: http://mining.ca/resources/mining-facts (accessed on 6 July 2015).

- Statistics Canada. Gross Domestic Product at Basic Prices, Primary Industries. 2014. Available online: http://www.statcan.gc.ca/tables-tableaux/sum-som/l01/cst01/prim03-eng.htm (accessed on 6 July 2015). [Google Scholar]

- Canadian Association of Petroleum Producers (CAPP). 2015. Available online: http://www.capp.ca/ (accessed on 6 July 2015).

- Zyl, A.S.V. The importance of stakeholder engagement in managing corporate reputations. Int. J. Innov. Sustain. Dev. 2013, 7, 46–60. [Google Scholar] [CrossRef]

- Marx, B.; Dyk, V.V. Sustainability reporting and assurance. Meditari Account. Res. 2011, 19, 39–55. [Google Scholar] [CrossRef]

- Deegan, C.; Rankin, M. Do Australian companies report environmental news objectively? Account. Audit. Account. J. 1996, 9, 50–67. [Google Scholar] [CrossRef]

- Milne, M.J.; Adler, R.W. Exploring the reliability of social and environmental disclosures content analysis. Account. Audit. Account. J. 1999, 12, 237–256. [Google Scholar] [CrossRef]

- Deegan, C.; Gordon, B. A Study of the Environmental Disclosure Practices of Australian Corporations. Account. Bus. Res. 1996, 26, 187–199. [Google Scholar] [CrossRef]

- Patten, D.M. The relation between environmental performance and environmental disclosure: A research note. Account. Organ. Soc. 2002, 27, 763–773. [Google Scholar] [CrossRef]

- Fouque, J.-P.; Papanicolaou, G.; Sircar, R.; Sølna, K. Introduction to Stochastic Volatility Models. In Multiscale Stochastic Volatility for Equity, Interest Rate, and Credit Derivatives; Cambridge University Press: New York, NY, USA, 2011; pp. 51–85. [Google Scholar]

- Brennan, N. Reporting intellectual capital in annual reports: Evidence from Ireland. Account. Audit. Account. J. 2001, 14, 423–436. [Google Scholar] [CrossRef]

- DJSI Family Overview | Sustainability Indices. DJSI Family Overview | Sustainability Indices, RobeccoSAM. Available online: http://www.sustainability-indices.com/index-family-overview/djsi-family-overview/index.jsp (accessed on 22 August 2015).

- Dow Jones Sustainability World Index Fact Sheet. 8 May 2015, Dow Jones Indices, S&P Dow Jones Indices. Available online: http://www.djindexes.com/mdsidx/downloads/fact_info/dow_jones_sustainability_world_index_fact_sheet.pdf (accessed on 23 August 2015).

- Corporate Knights. 2012 Best 50 Issue | Corporate Knights, 2013. Available online: http://www.corporateknights.com/magazines/2012-best-50-issue/ (accessed on 23 August 2015).

- Kleinbaum, D.G.; Kupper, L.L. Applied Regression Analysis and Other Multivariable Methods; Duxbury Press: North Scituate, MA, USA, 1978. [Google Scholar]

- Lodhia, S.; Hess, N. Sustainability accounting and reporting in the mining industry: Current literature and directions for future research. J. Clean. Prod. 2014, 84, 43–50. [Google Scholar] [CrossRef]

- Cheng, M.; Green, W.; Conradie, P.; Konishi, N.; Romi, A. The International Integrated Reporting Framework: Key Issues and Future Research Opportunities. J. Int. Financ. Manag. Account. 2014, 25, 90–119. [Google Scholar] [CrossRef]

- Dong, S.; Burritt, R.; Qian, W. Salient stakeholders in corporate social responsibility reporting by Chinese mining and minerals companies. J. Clean. Prod. 2014, 84, 59–69. [Google Scholar] [CrossRef]

- Magness, V. Strategic posture, financial performance and environmental disclosure. Account. Audit. Account. J. 2006, 19, 540–563. [Google Scholar] [CrossRef]

- Spence, C.; Gray, R. Social and Environmental Reporting and the Business Case; ACCA Commissioned Research Report; ACCA: London, UK, 2007. [Google Scholar]

- Boiral, O.; Henri, J.-F. Is Sustainability Performance Comparable? A Study of GRI Reports of Mining Organizations. Bus. Soc. 2015. [Google Scholar] [CrossRef]

- Fonseca, A.; Mcallister, M.L.; Fitzpatrick, P. Sustainability reporting among mining corporations: A constructive critique of the GRI approach. J. Clean. Prod. 2014, 84, 70–83. [Google Scholar] [CrossRef]

- Coetzee, C.M.; Staden, C.J.V. Disclosure responses to mining accidents: South African evidence. Account. Forum 2011, 35, 232–246. [Google Scholar] [CrossRef]

- Peck, P.; Sinding, K. Environmental and social disclosure and data richness in the mining industry. Bus. Strateg. Environ. 2003, 12, 131–146. [Google Scholar] [CrossRef]

- Villiers, C.D.; Rinaldi, L.; Unerman, J. Integrated Reporting: Insights, gaps and an agenda for future research. Account. Audit. Account. J. 2014, 27, 1042–1067. [Google Scholar]

- Hindley, T.; Buys, P.W. Integrated Reporting Compliance with The Global Reporting Initiative Framework: An Analysis of the South African Mining Industry. Int. Bus. Econ. Res. J. 2012, 11, 1249–1260. [Google Scholar] [CrossRef]

- Roberts Environmental Center. 2010 Sustainability Reporting of the World’s Largest Mining and Crude-Oil Production Companies. Available online: http://roberts-environmental-center.cmc.edu/wp-content/uploads/2014/02/mining2010.pdf (accessed on 30 May 2016).

- Mruck, K.; Breuer, F. Subjectivity and Reflexivity in Qualitative Research—The FQS Issues. Forum: Qualitative Social Research. Available online: http://www.qualitative-research.net/index.php/fqs/article/viewArticle/696 (accessed on 22 May 2016).

- Hamann, R.; Kapelus, P. Corporate Social Responsibility in Mining in Southern Africa: Fair accountability or just greenwash? Development 2004, 47, 85–92. [Google Scholar] [CrossRef]

- Brown, H.S.; Jong, M.D.; Levy, D.L. Building institutions based on information disclosure: Lessons from GRI’s sustainability reporting. J. Clean. Prod. 2009, 17, 571–580. [Google Scholar] [CrossRef]

- SASB. Using SASB Standards. 2014. Available online: http://www.sasb.org/standards/download (accessed on 30 May 2016).

- CERES. Disclosing Climate Risks & Opportunities in Sec Filings (rep.), Disclosing Climate Risks & Opportunities in Sec Filings, 2011. Available online: http://www.igcc.org.au/resources/documents/disclosing%20climate%20risks%20and%20opportunities%20in%20sec%20filings.pdf (accessed on 30 May 2016).

- USSIF. REPORT ON US Sustainable, Responsible and Impact Investing Trends 2014 (rep.), REPORT ON US Sustainable, Responsible and Impact Investing Trends 2014, The Forum of Sustainable and Responsible Investment, 2014. Available online: http://www.ussif.org/files/publications/sif_trends_14.f.es.pdf (accessed on 30 May 2016).

- Global Reporting Initiative. Sustainability and Reporting Trends in 2025—Preparing for the Future (Working Paper). Available online: https://www.globalreporting.org/resourcelibrary/Sustainability-and-Reporting-Trends-in-2025-1.pdf (accessed on 8 September 2016).

- CPA Canada and TMX. A Primer for Environmental and Social Disclosure, March 2014. Available online: https://www.cpacanada.ca/en/business-and-accounting-resources/financial-and-non-financial-reporting/sustainability-environmental-and-social-reporting/publications/a-primer-for-environmental-social-disclosure (accessed on 30 May 2016).

- Disclosure of Non-Financial Information by Certain Large Companies, Directive 2003/51/EC of the European Parliament and of the Council of 18 June 2003. Available online: http://ec.europa.eu/finance/accounting/non-financial_reporting/index_en.htm (accessed on 30 May 2016).

- 2014 SSE Global Dialogue—Press Release Key Capital Market Leaders Convene at Largest Sustainable Stock Exchanges Global Dialogue. Available online: http://www.sseinitiative.org/home-slider/2014-sustainable-stock-exchanges-global-dialogue-press-release/ (accessed on 30 May 2016).

- Mining’s Contribution to Sustainable Development—An Overview. (2012). International Council on Mining & Metals (ICMM). Available online: https://www.icmm.com/document/3716 (accessed on 22 May 2016).

- SEC. SEC Adopts Dodd-Frank Mine Safety Disclosure Requirements. 2011. Available online: https://www.sec.gov/news/press/2011/2011-273.htm (accessed on 22 May 2016). [Google Scholar]

- Ackers, B.; Eccles, N.S. Mandatory corporate social responsibility assurance practices. Account. Audit. Account. J. 2015, 28, 515–550. [Google Scholar] [CrossRef]

- Eccles, R.; Kiron, D.M.I.T. Get Ready: Mandated Integrated Reporting Is the Future of Corporate Reporting; MIT Sloan School of Management: Cambridge, MA, USA, 2012. [Google Scholar]

- Fries, J.; McCulloch, K.; Webster, W.; Fries, J. The Prince’s Accounting for Sustainability Project: Creating 21st-Century Decision Making and Reporting System to Respond to 21st-Century Challenges and Opportunities; Hopwood, A.G., Unerman, J., Eds.; Earthscan: London, UK, 2010. [Google Scholar]

{kind=link}

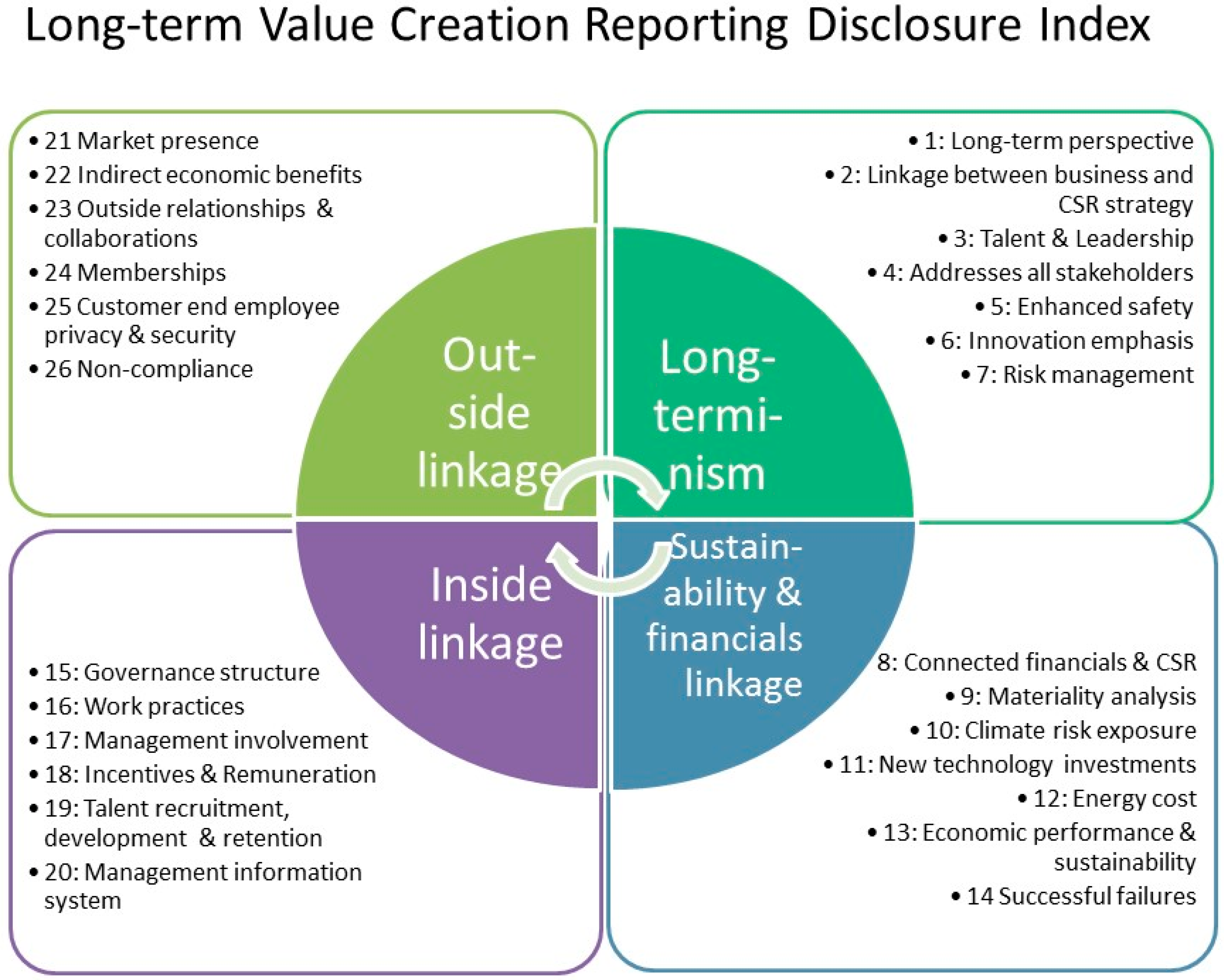

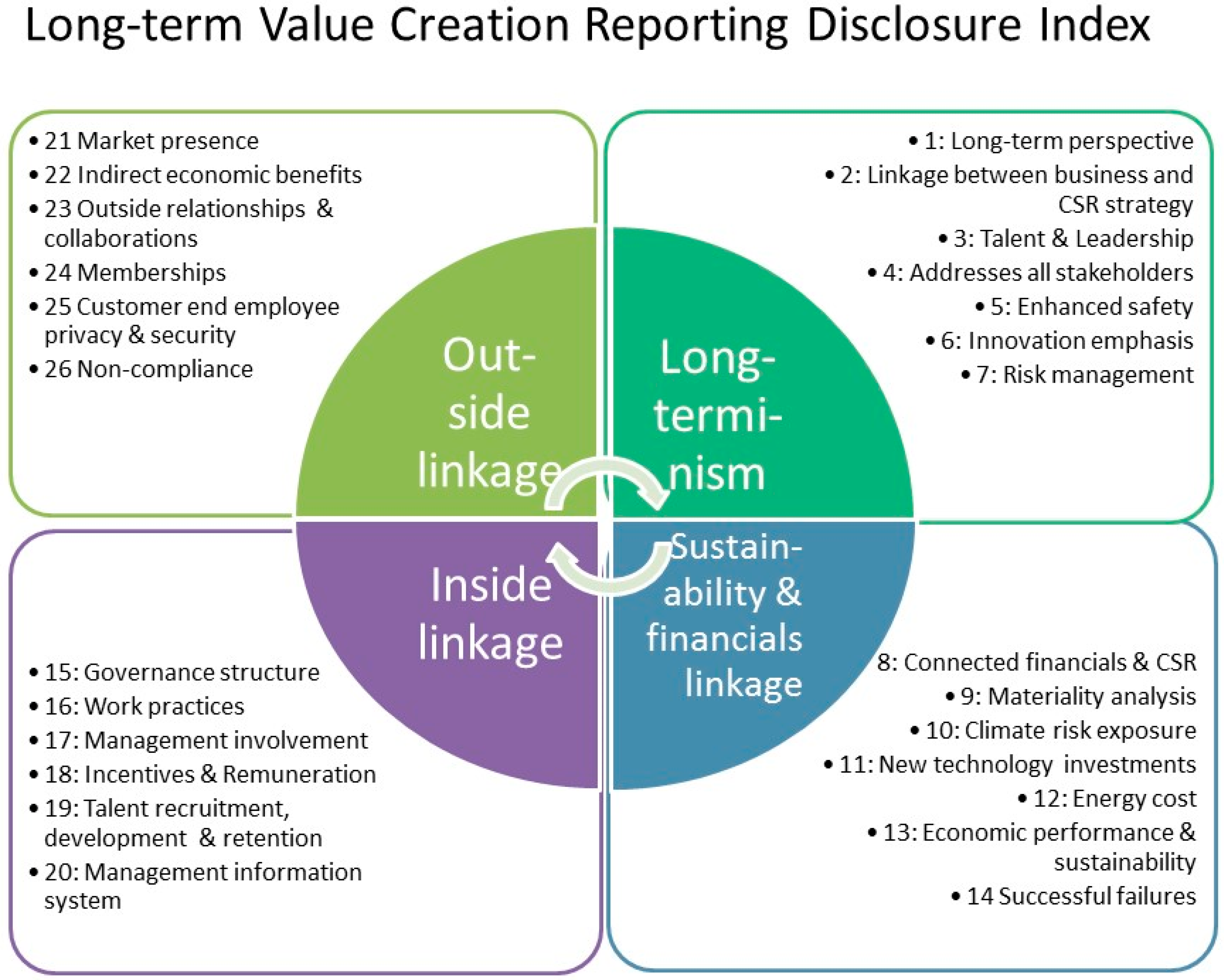

| Long-Term Value Creation Through: | Explanations, Examples | GRI G4 | <IR> Framework | ||

|---|---|---|---|---|---|

| 1. Long-term 360 degree linkage Perspective/point of view | 1 | Long-term perspective | Development of vision, mission, systematic organization and processes; stability; growth of new industries and new markets; long-term supplier networks; ethical conduct | 5.1 General Standard Disclosures: G4-1, G4-3, G4-42, G4-56, G4-57 5.2 SPECIFIC STANDARD DISCLOSURES: G4-EC5 & EC6 | 4A Organizational overview and external environment: Content element 4.5 |

| 2 | Linkage between business and sustainability strategy | Identification of mission, core values in both areas | 5.1 General Standard Disclosures: G4-1, G4-2 | 4C Business model: 4.13 4I General reporting guidance: 4.53 | |

| 3 | Talent & leadership | New hires with long-term perspective with fit into organization and its culture; are leaders well suited for making decisions (competencies), ethical skills, employee development | 5.1 General Standard Disclosures: G4-33 to G-55 | 4B Governance: 4.9 | |

| 4 | Addresses all relevant stakeholders | Examples: dear stakeholders, stakeholder commentaries, etc., stakeholder engagement and feedback | 3.1 The Criteria 4.1 Principles for Defining Report Content 4.2 Principles for Defining Report Quality | 1A Integrated report defined: 1.8 3C Stakeholder relationships: 3.10 to 3.14 | |

| Enhancement linkage Improvements/mitigation | 5 | Enhanced safety | Safety initiatives and their financial implications | 5.2 Specific Standard Disclosures: G4 LA5 to LA8, G4-PR1 & PR2, G4-SO1, G4-HR7 | n/a |

| 6 | Innovation emphasis | Eco-friendly; growth of new industries and new markets; new innovation platforms and their financial implications | n/a | 2D The value creation process: 2.24 4C Business model: 4.16 4E Strategy and resource allocation: 4.29 | |

| 7 | Risk management | Explanations of risk management, incl. threats and opportunities and financial impacts | 4.2 Principles for Defining Report Quality: G4-2, G4-33, G4-45 to 48, 5.2 Specific Standard Disclosures: G4-DMA: G4-EC2, G4-EC2, G4-HR5, G4-HR6, G4-SO3 | 2D The value creation process: 2.26 3D Materiality: 3.34 4D Risks and opportunities: 4.23 to 26 4F Performance: 4.31, 4.36, 4.37 4H Basis of preparation and presentation: 4.43 to 4.46 | |

| 2. Financials and sustainability linkage | 8 | Connectivity between financials and sustainability sections | Quantitative information about outcomes on capitals; KPIs that connect financial outcomes with other sustainability variables (e.g., emissions to sales ratio, financial impact of consumption or employee turnover, etc.) | 4.2 Principles for Defining Report Quality: G4-2, G4-44 5.2 Specific Standard Disclosures: G4-DMA: G4-EC2 | 1C Purpose and users of an integrated report: 1.7, 1.11, 2A Introduction: 2.3 2B Value creation for the organization and for others: 2.4 to 2.9 2C The capitals 3A Strategic focus and future orientation: 3.3 3B Connectivity of information 4C Business model 4E Strategy and resource allocation 4F Performance 4G Outlook 4H Basis of preparation and presentation |

| 9 | Materiality analysis | Materiality analysis, materiality matrix | 4.1 Principles for Defining Report Content 4.2 Principles for Defining Report Quality 2.2 Using the Guidelines to Prepare a Sustainability Report: The Steps to Follow 5.1 General Standard Disclosures: G4-17, G4-17 to 23 5.2 Specific Standard Disclosures: G4-DMA (Disclosure on Management approach) | 1D A principles-based approach: 1.10 2B Value creation for the organization and for others: 2.7 3D Materiality 3F Reliability and completeness 3G Consistency and comparability 4D Risks and opportunities 4F Performance 4H Basis of preparation and presentation 4I General reporting guidance | |

| 10 | Climate risk exposure | Financial implications and other risk due to climate change | 5.2 Specific Standard Disclosures: G4-EC2 | 4A Organizational overview and external environment: 4.7 | |

| 11 | New technology investment | Identification of new technology investments and related financial information | n/a | 2D The value creation process: 2.24 3B Connectivity of information: 3.8, 3.9 | |

| 12 | Energy Costs | Energy consumption practices and related financial impact (not emissions or consumption numbers only); Projects with high climate risk exposure | 5.2 Specific Standard Disclosures: G4-EN3 to EN7 (only consumption information) | 3B Connectivity of information: 3.8 | |

| 13 | Economic performance & sustainability | Connection between economic performance and economic sustainability. | 3.1 The Criteria 4.1 Principles for Defining Report Content 5.2 Specific Standard Disclosures: G4-EC1 to EC4, G4-EC7 & EC8 | 2D The value creation process 3B Connectivity of information | |

| 14 | Successful failures | Identification of failures and the lessons learned from them | 5.1 General Standard Disclosures: G4-1 | n/a | |

| 3. Inside linkage Within the organization | 15 | Governance structure | Diversity & skill set of people in charge and how they benefit company | 5.2 Specific Standard Disclosures: G4-LA12 | 4B Governance: 4.9 |

| 16 | Responsible workplace practices | Sustainable people practices and connection to cost efficiencies, safety practices | 5.2 Specific Standard Disclosures: G4-LA1 to LA16, G4-HR7 | 2B Value creation for the organization and for others: 2.9 3D Materiality: 3.35 4B Governance: 4.9 4C Business model: 4.20 | |

| 17 | Involvement of management | Commitment to sustainability; targets and who is accountable for what; board committees | 5.1 General Standard Disclosures: G4-34 to G4-55 5.2 Specific Standard Disclosures: G4-LA12, G4-SO4 | 1A Integrated report defined 1G Responsibility for an integrated report 2C The capitals 2D The value creation process 3B Connectivity of information: 3.4, 3.15 3D Materiality: 3.21, 3.22, 3.25 3E Conciseness: 3.37 3F Reliability and completeness: 3.41 & 3.42 4. CONTENT ELEMENTS: 4.1 4B Governance: 4.9 4C Business model: 4.22 4H Basis of preparation and presentation: 4.42 4I General reporting guidance: 4.53, 4.62 | |

| 18 | Incentives and remuneration | Is reward system tied to long-term value creation? | 5.1 General Standard Disclosures: G4-33, G4-50 to G4-53 | 4B Governance: 4.9 | |

| 19 | Talent recruitment, development & retention | Training and development expenditures for employees and their impact on company sustainability | 5.1 General Standard Disclosures: G4-33, G4-50 | n/a | |

| 20 | Management information system | Is information system capable to measure and inform about long-term sustainability? | 4.1 Principles for Defining Report Content 4.2 Principles for Defining Report Quality 6.9 Process for Defining Reporting content | ABOUT INTEGRATED REPORTING 1F Application of the Framework: 1.18 2D The value creation process: 2.28 3B Connectivity of information: 3.7, 3.8, 3.9 3F Reliability and completeness: 3.40, 3.46, 3.49, 3.50 | |

| 4. Outside linkage Outside relationships | 21 | Market presence | Locally based suppliers policies, local hiring, wages compared to local market (costs and benefits) | 4.1 Principles for Defining Report Content 5.1 General Standard Disclosures: G4-1, G4-8, G4-13 5.2 Specific Standard Disclosures: G4-EC5 to EC7, G4-EC9, G4-EN9, G4-LA8, G4-LA15, G4-HR4 to HR11, G4-SO1 to SO11 | 1C Purpose and users of an integrated report: 1.8 2B Value creation for the organization and for others: 2.6 3A Strategic focus and future orientation: 3.4 3B Connectivity of information: 3.8 3C Stakeholder relationships: 3.13 3D Materiality: 3.35 4A Organizational overview and external environment: 4.5, 4.7 4C Business model: 4.16, 4.20, 4.21 4G Outlook: 4.31 |

| 22 | Indirect economic impacts | Infrastructure investments, public benefit, extent of impacts, community investment (costs and benefits) | 4.1 Principles for Defining Report Content 5.1 General Standard Disclosures: G4-1, G4-2 5.2 Specific Standard Disclosures: G4-EC1 & EC2, G4-EC6 to EC8, G4-EN12, G4-SO1, G4-SO9 & SO10 | 2C The capitals: 2.15 2D The value creation process: 2.21 3C Stakeholder relationships: 3.12, 3.13 4A Organizational overview and external environment 4H Basis of preparation and presentation: 4.47 | |

| 23 | Positive relationships and collaborations with outside stakeholder | Business partners and collaborations (costs and benefits); Stakeholder relationships and engagement with impact | 4.1 Principles for Defining Report Content 4.2 Principles for Defining Report Quality 5.1 General Standard Disclosures: G4-1, G4-13, G4-24 to G4-27, G4-37, G4-38, G4-40 & 41, G4-45, G4-53 5.2 Specific Standard Disclosures: G4-EC8, G4-SO1 | 2A Introduction: 2.2, 2.3, 2.6, 2.7 2C The capitals: 2.15, 2.18 3B Connectivity of information: 3.8 3C Stakeholder relationships 4B Governance: 4.8 4C Business model: 4.17 4F Performance: 4.31, 4.32 4G Outlook: 4.37 | |

| 24 | Memberships & (industry) associations | Company memberships in industry or other associations (financial impact and benefit) | 5.1 General Standard Disclosures: G4-16 | n/a | |

| 25 | Customer and employee privacy & security | Cyber security breaches, data loss and fraudulent activities and losses therefrom | 5.2 Specific Standard Disclosures: G4-PR8 | n/a | |

| 26 | Non-compliance with laws and regulations | Fines for marketing communication and product and services non-compliance & fines; Reporting of monetary values | 5.2 Specific Standard Disclosures: G4-PR7 & PR9 | n/a | |

| Score | Disclosure Quality | Type of Information |

|---|---|---|

| 0 | No disclosure quality | No information was provided in the report. |

| 1 | Very low disclosure quality | The topic is only mentioned briefly in the report. |

| 2 | Low disclosure quality | Little information was provided but more than just a mention was made. |

| 3 | Medium disclosure quality | Average information was provided. |

| 4 | High disclosure quality | In addition to the average information, a few examples or quantitative information were provided. |

| 5 | Very high disclosure quality | Extensive information was provided with many examples or substantial quantitative information. |

| Variable (Expected Sign) | Measurement | Source |

|---|---|---|

| Company size (+) | Total revenues 2012 | 2012 Annual financial report |

| Sector | Sector 1: Energy (oil and gas) Sector 2: Basic materials | Yahoo Finance Profile page |

| Corporate governance (+) | Percentage of independent board members | 2012 Annual financial reports, circulars or proxies |

| Risk exposure (+) | Fast volatility | Morningstar Investment Center |

| Stakeholder engagement (+) | Dow Jones Sustainability Index World 2012 1: yes, 0: no (dummy variables) | Robecco Sam DJSI World 2012 |

| Corporate Knights Ranking 1: yes, 0: no (dummy variables) | Corporate Knights list 2012 | |

| Intangible asset management (+) | Price-Book-Ratio | Morningstar Investment Center |

| (a) | |||||

| Sector | |||||

| Frequency | Percent | Valid Percent | Cumulative Percent | ||

| Valid | 1 | 9 | 45.0 | 45.0 | 45.0 |

| 2 | 11 | 55.0 | 55.0 | 100.0 | |

| Total | 20 | 100.0 | 100.0 | ||

| Ranking | |||||

| Frequency | Percent | Valid Percent | Cumulative Percent | ||

| Valid | 0 | 7 | 35.0 | 35.0 | 35.0 |

| 1 | 13 | 65.0 | 65.0 | 100.0 | |

| Total | 20 | 100.0 | 100.0 | ||

| DJSI | |||||

| Frequency | Percent | Valid Percent | Cumulative Percent | ||

| Valid | 0.00 | 10 | 50.0 | 50.0 | 50.0 |

| 1.00 | 10 | 50.0 | 50.0 | 100.0 | |

| Total | 20 | 100.0 | 100.0 | ||

| Ext_assurance | |||||

| Frequency | Percent | Valid Percent | Cumulative Percent | ||

| Valid | 0 | 13 | 65.0 | 65.0 | 65.0 |

| 1 | 7 | 35.0 | 35.0 | 100.0 | |

| Total | 20 | 100.0 | 100.0 | ||

| (b) | |||||

| Descriptive Statistics | |||||

| N | Minimum | Maximum | Mean | Std. Deviation | |

| Total Revenues 2012 | 20 | 1148 | 38,616 | 10,865.10 | 11,083.079 |

| Net income | 20 | −2794 | 3766 | 847.10 | 1359.532 |

| Employees | 20 | 500 | 27,000 | 7646.75 | 6270.323 |

| Company age | 20 | 6 | 135 | 43.45 | 32.720 |

| Fast volatility | 20 | 0.02 | 0.06 | 0.0320 | 0.01105 |

| Price-book-ratio | 20 | 1.20 | 5.30 | 1.9250 | 0.93969 |

| Board independence in % | 20 | 54 | 100 | 85.46 | 11.190 |

| DQ_AR | 20 | 0.63 | 1.61 | 1.0825 | 0.33488 |

| DQ_CSR | 20 | 1.15 | 3.39 | 2.1200 | 0.69067 |

| AR_CSR_DISCREP | 20 | 0.15 | 2.11 | 1.0375 | 0.58831 |

| DQ_LTV | 20 | 1.97 | 4.95 | 3.2025 | 0.91228 |

| DQ_AR_LT | 20 | 1.21 | 3.50 | 2.1430 | 0.63923 |

| DQ_AR_FIN | 20 | 0.00 | 1.17 | 0.5340 | 0.39328 |

| DQ_AR_IN | 20 | 0.00 | 1.50 | 0.5625 | 0.47894 |

| DQ_AR_OUT | 20 | 0.00 | 2.25 | 0.8135 | 0.72389 |

| WORDS_AR_LT | 20 | 95.14 | 527.57 | 265.0295 | 131.48773 |

| WORDS_AR_FIN | 20 | 0.00 | 102.67 | 36.7750 | 30.98703 |

| WORDS_AR_IN | 20 | 0.00 | 129.50 | 44.5250 | 42.70585 |

| WORDS_AR_OUT | 20 | 0.00 | 292.50 | 83.1190 | 92.25636 |

| DQ_CSR_LT | 20 | 1.57 | 4.07 | 2.6920 | 0.71057 |

| DQ_CSR_FIN | 20 | 0.33 | 4.08 | 1.7420 | 1.17789 |

| DQ_CSR_IN | 20 | 0.33 | 3.42 | 1.5000 | 0.86427 |

| DQ_CSR_OUT | 20 | 1.13 | 3.50 | 2.6185 | 0.67448 |

| WORDS_CSR_LT | 20 | 125.14 | 811.86 | 337.8710 | 182.67149 |

| WORDS_CSR_FIN | 20 | 19.17 | 702.17 | 167.6580 | 172.47048 |

| WORDS_CSR_IN | 20 | 12.33 | 470.00 | 148.0080 | 121.75734 |

| WORDS_CSR_OUT | 20 | 107.75 | 878.00 | 419.8930 | 256.98874 |

| WORDS_AR_AVERAGE | 20 | 39 | 218 | 116.30 | 50.234 |

| WORDS_CSR_AVERAGE | 20 | 84 | 575 | 255.95 | 155.477 |

| WORDS_AR_TOTAL | 20 | 903 | 5004 | 2674.65 | 1155.137 |

| WORDS_CSR_TOTAL | 20 | 1927 | 13231 | 5927.30 | 3656.503 |

| WORDS_TOTAL | 20 | 3677 | 18235 | 8601.95 | 4231.116 |

| Valid N (listwise) | 20 | ||||

| Correlations | ||||||||

|---|---|---|---|---|---|---|---|---|

| Sector | fast_vol | price_book | in % | Ranking | log_revenues | log_total_words | DJSI | |

| Sector | 1 | −0.672 ** | 0.277 | 0.289 | −0.032 | 0.499 * | −0.202 | 0.101 |

| fast_vol | −0.672 ** | 1 | −0.431 | −0.077 | −0.058 | −0.576 ** | 0.016 | −0.279 |

| price_book | 0.277 | −0.431 | 1 | 0.157 | 0.134 | 0.219 | 0.295 | 0.289 |

| independent % | 0.289 | −0.077 | 0.157 | 1 | −0.142 | −0.293 | −0.152 | −0.034 |

| ranking | −0.032 | −0.058 | 0.134 | −0.142 | 1 | 0.319 | 0.403 | 0.314 |

| log_revenues | 0.499 * | −0.576 ** | 0.219 | −0.293 | 0.319 | 1 | 0.327 | 0.414 |

| log_total_words | −0.202 | 0.016 | 0.295 | −0.152 | 0.403 | 0.327 | 1 | 0.505 * |

| DJSI | 0.101 | −0.279 | 0.289 | −0.034 | 0.314 | 0.414 | 0.505 * | 1 |

| Model Summary b | ||||||

| Model | R | R Square | Adjusted R Square | Std. Error of the Estimate | Durbin-Watson | |

| 1 | 0.948 a | 0.899 | 0.826 | 0.38014 | 2.189 | |

| a Predictors: (Constant), Zscore(log_revenues), Zscore(price_book), Zscore(ranking), Zscore: independent %, Zscore(DJSI), Zscore(log_total_words), Zscore(fast_vol), Zscore(sector) | ||||||

| b Dependent Variable: Combined_score | ||||||

| ANOVA a | ||||||

| Model | Sum of Squares | df | Mean Square | F | Sig. | |

| 1 | Regression | 14.223 | 8 | 1.778 | 12.303 | 0.000 b |

| Residual | 1.590 | 11 | 0.145 | |||

| Total | 15.813 | 19 | ||||

| a Dependent Variable: Combined_score | ||||||

| b Predictors: (Constant), Zscore(log_revenues), Zscore(price_book), Zscore(ranking), Zscore: independent %, Zscore(DJSI), Zscore(log_total_words), Zscore(fast_vol), Zscore(sector) | ||||||

| Coefficients a | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Model | Unstandardized Coefficients | Stand. Coefficients | t | Sig. | Correlations | Collinearity Statistics | |||||

| B | Std. Error | Beta | Zero-Order | Partial | Part | Tolerance | VIF | ||||

| 1 | (Constant) | 3.203 | 0.085 | 37.676 | 0.000 | ||||||

| Zscore(fast_vol) | 0.358 | 0.136 | 0.392 | 2.633 | 0.023 | 0.147 | 0.622 | 0.252 | 0.412 | 2.428 | |

| Zscore(price_book) | 0.193 | 0.106 | 0.212 | 1.824 | 0.095 | 0.334 | 0.482 | 0.174 | 0.678 | 1.474 | |

| Zscore: independent % | 0.264 | 0.105 | 0.289 | 2.509 | 0.029 | 0.006 | 0.603 | 0.240 | 0.687 | 1.456 | |

| Zscore(sector) | −0.311 | 0.140 | −0.341 | −2.214 | 0.049 | −0.155 | −0.555 | −0.212 | 0.385 | 2.595 | |

| Zscore(ranking) | 0.087 | 0.098 | 0.095 | 0.884 | 0.396 | 0.444 | 0.257 | 0.084 | 0.784 | 1.275 | |

| Zscore(DJSI) | 0.245 | 0.109 | 0.268 | 2.242 | 0.047 | 0.600 | 0.560 | 0.214 | 0.638 | 1.568 | |

| Zscore(log_total_words) | 0.409 | 0.120 | 0.449 | 3.399 | 0.006 | 0.823 | 0.716 | 0.325 | 0.525 | 1.906 | |

| Zscore(log_revenues) | 0.443 | 0.159 | 0.486 | 2.793 | 0.017 | 0.297 | 0.644 | 0.267 | .302 | 3.312 | |

© 2016 by the author; licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC-BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Dilling, P.F.A. Reporting on Long-Term Value Creation—The Example of Public Canadian Energy and Mining Companies. Sustainability 2016, 8, 938. https://doi.org/10.3390/su8090938

Dilling PFA. Reporting on Long-Term Value Creation—The Example of Public Canadian Energy and Mining Companies. Sustainability. 2016; 8(9):938. https://doi.org/10.3390/su8090938

Chicago/Turabian StyleDilling, Petra F. A. 2016. "Reporting on Long-Term Value Creation—The Example of Public Canadian Energy and Mining Companies" Sustainability 8, no. 9: 938. https://doi.org/10.3390/su8090938