A Study of Incentive Policies for Building-Integrated Photovoltaic Technology in Hong Kong

Abstract

:1. Introduction

2. Subsidies in PV Leading Countries

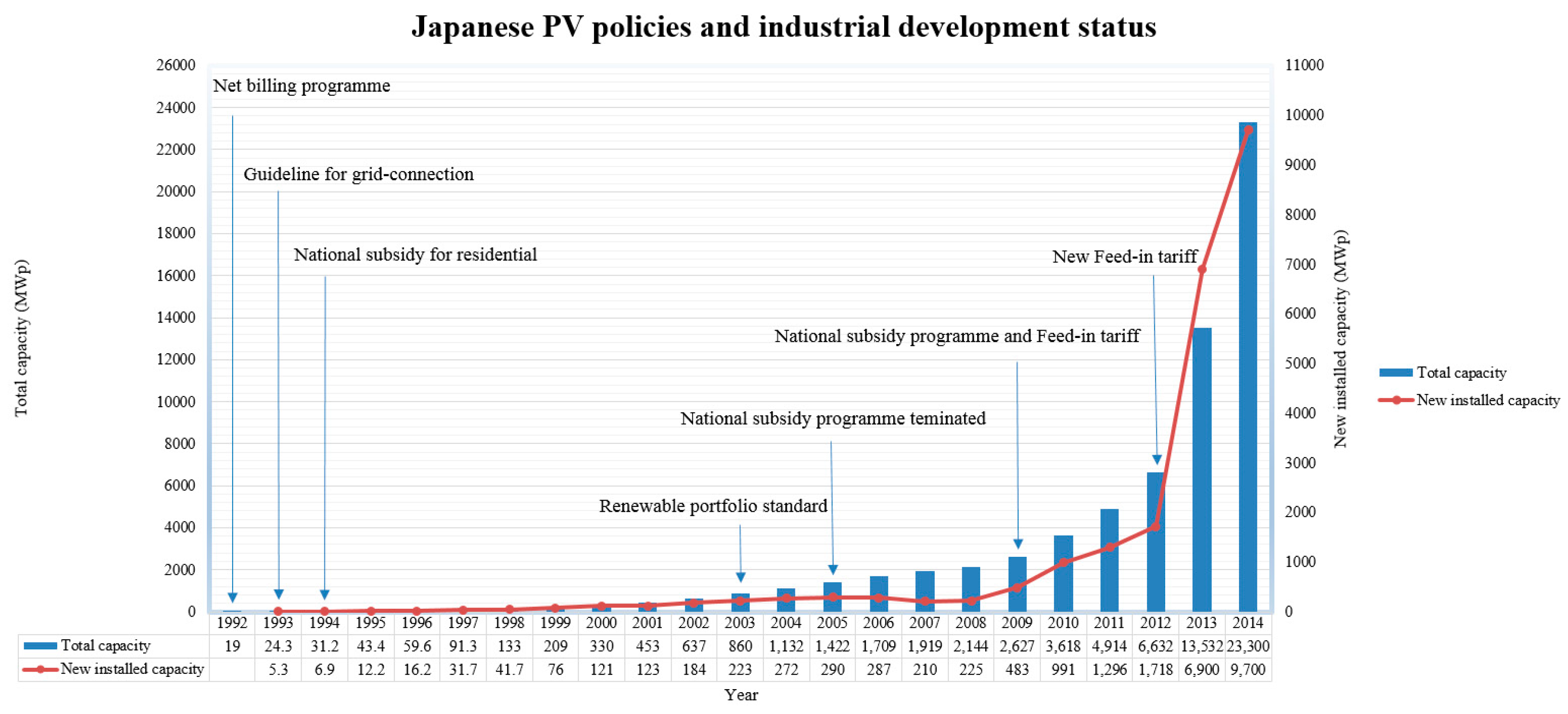

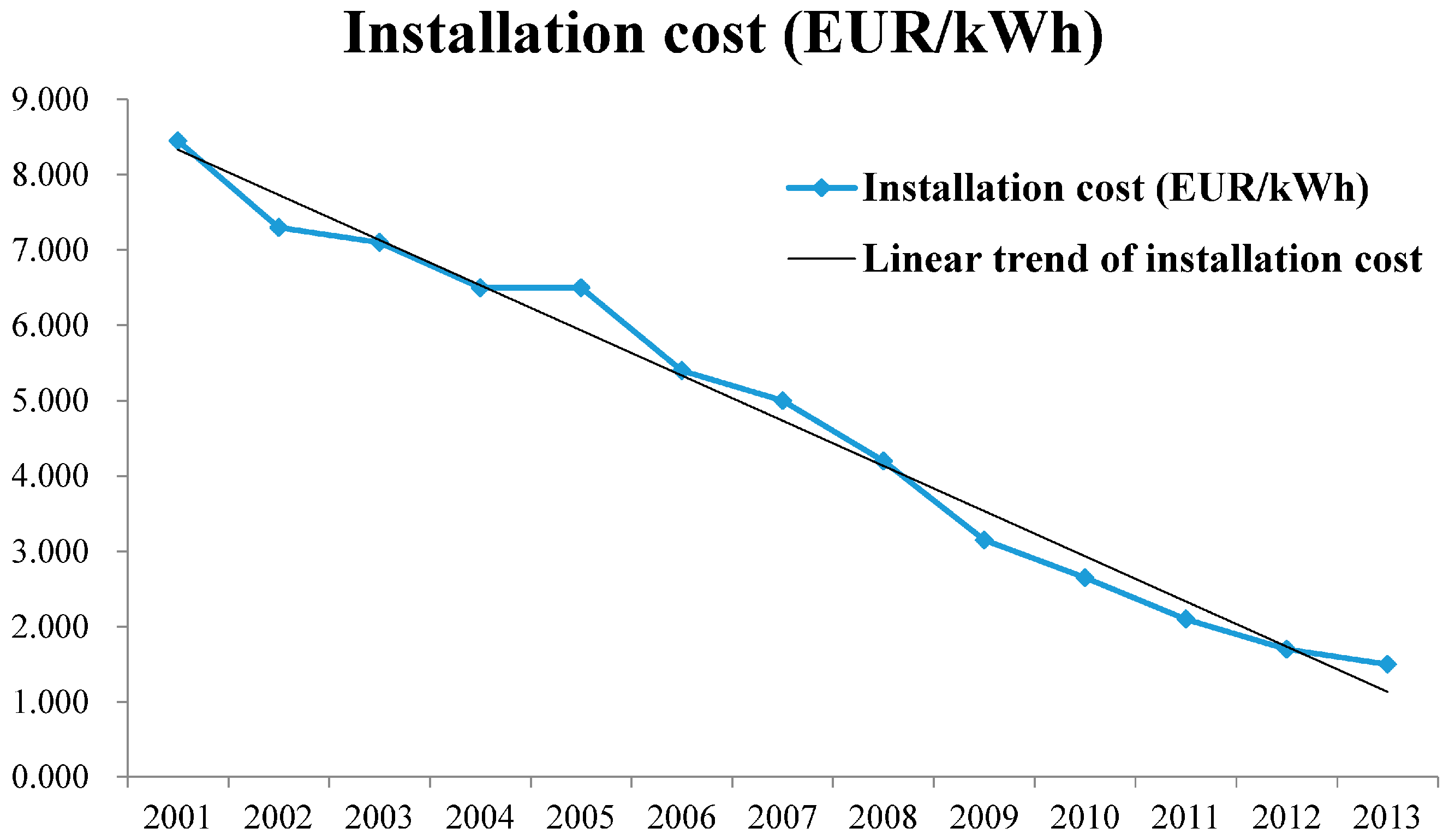

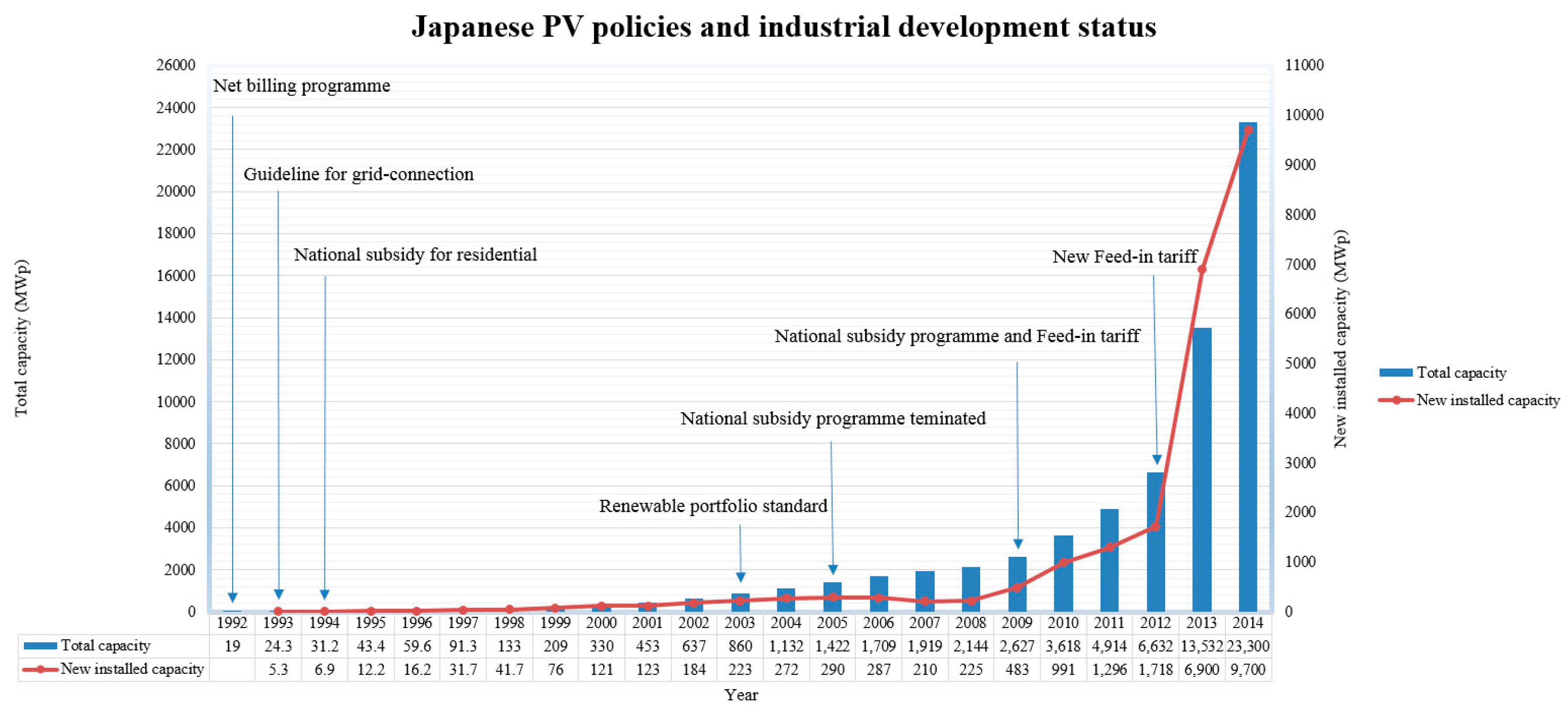

2.1. PV Incentive Policies in Japan

2.2. PV Incentive Policies in Germany

2.3. PV Incentive Policies in Italy

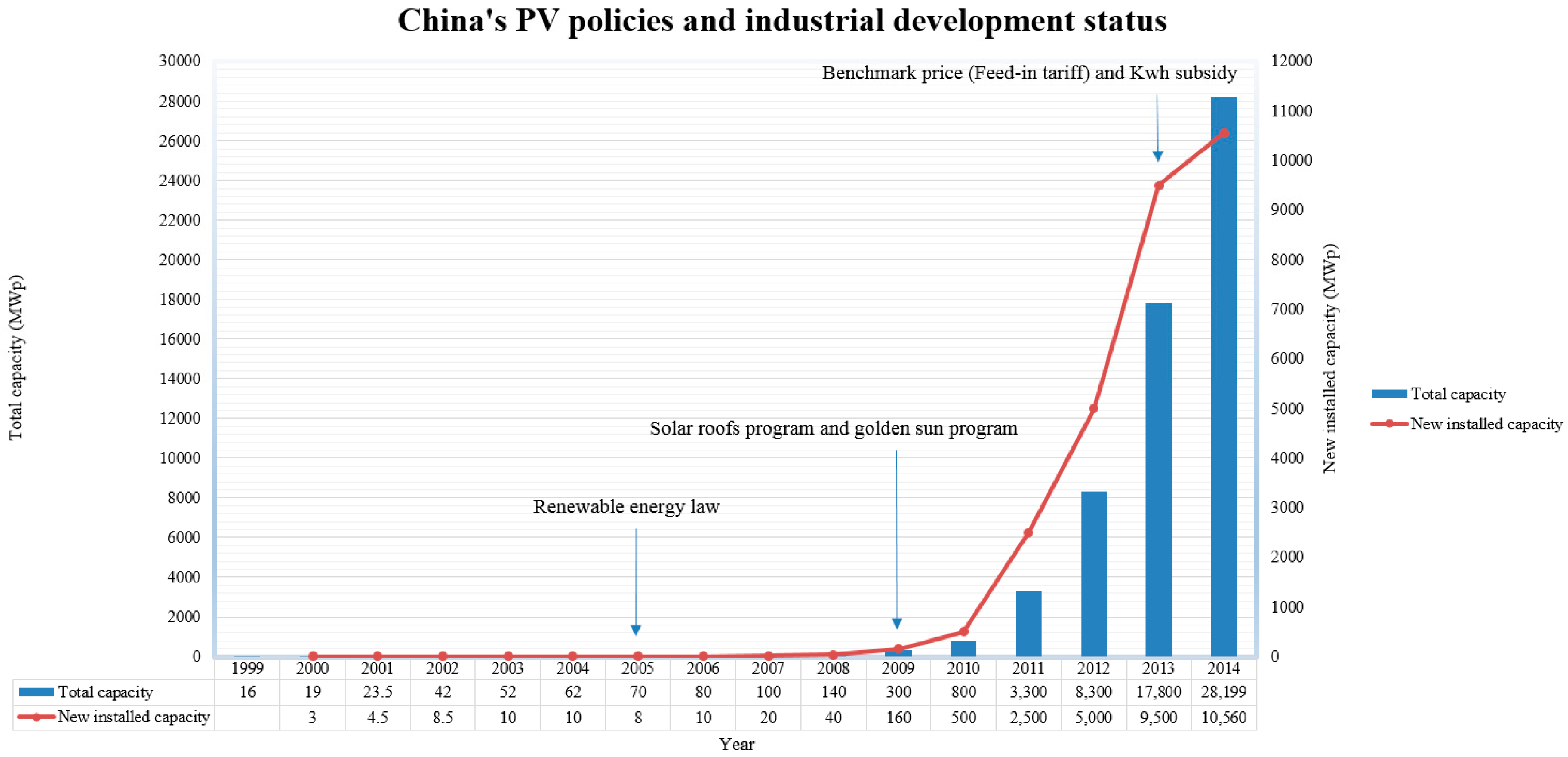

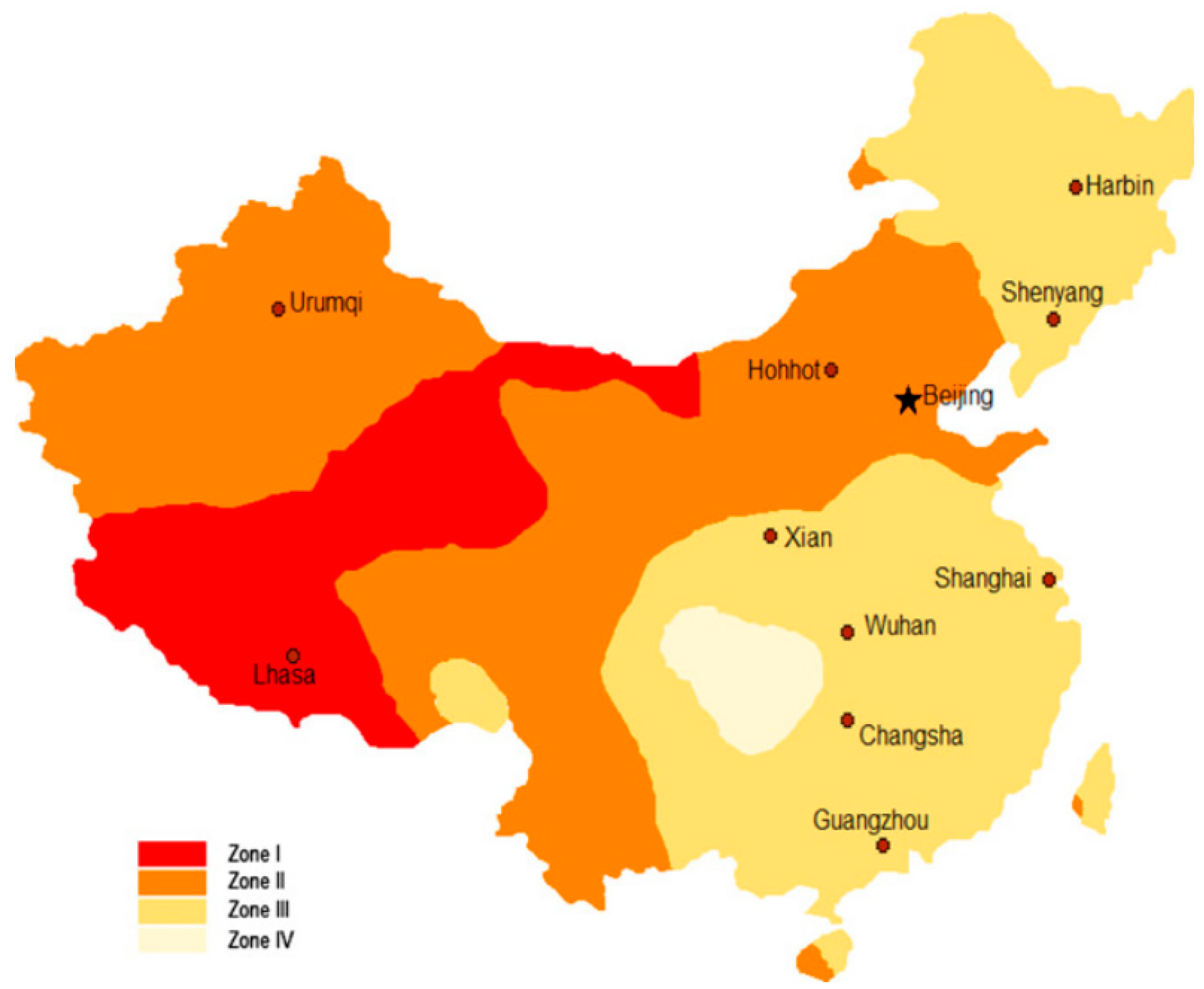

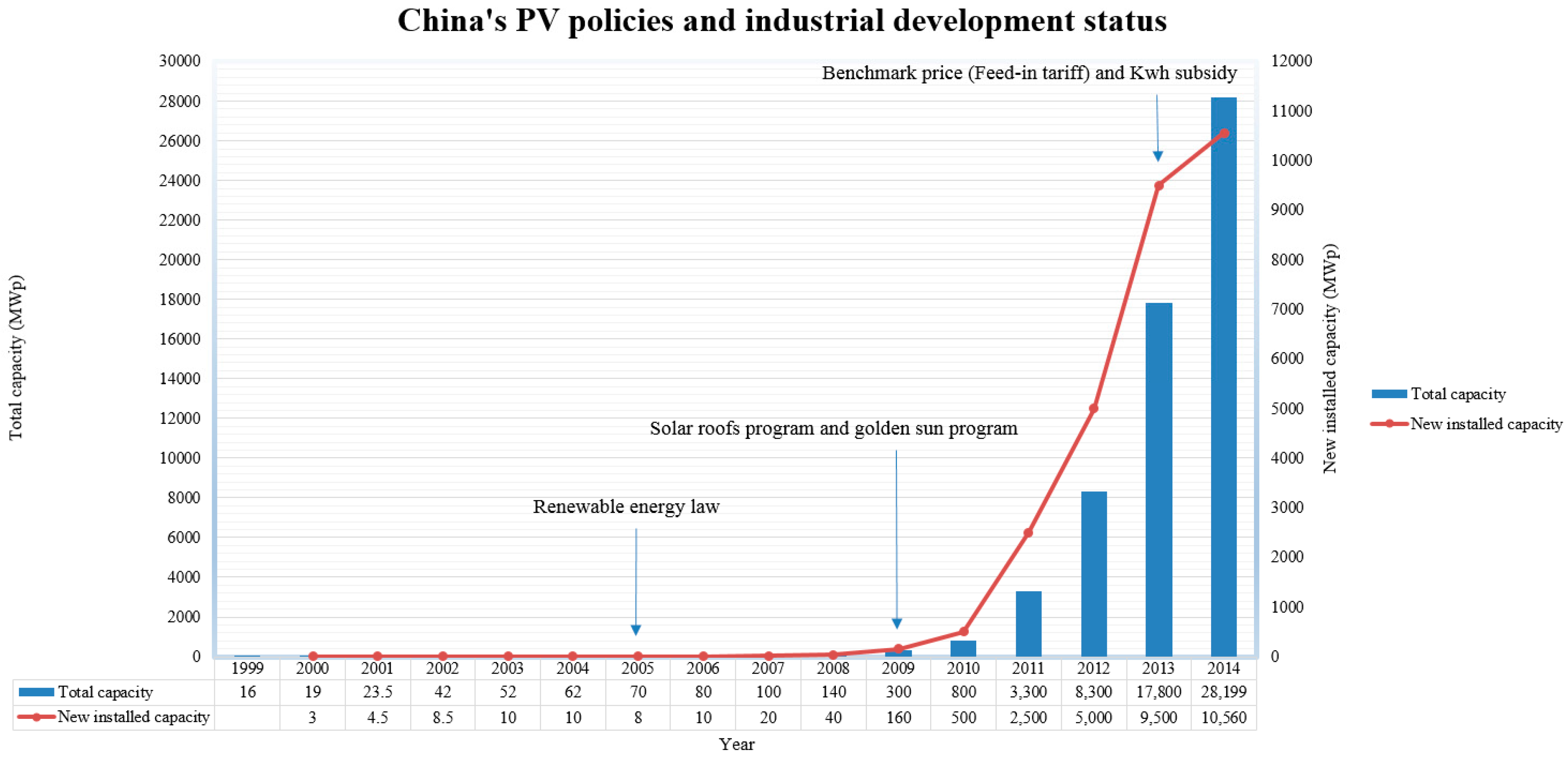

2.4. PV Incentive Policies in Mainland China

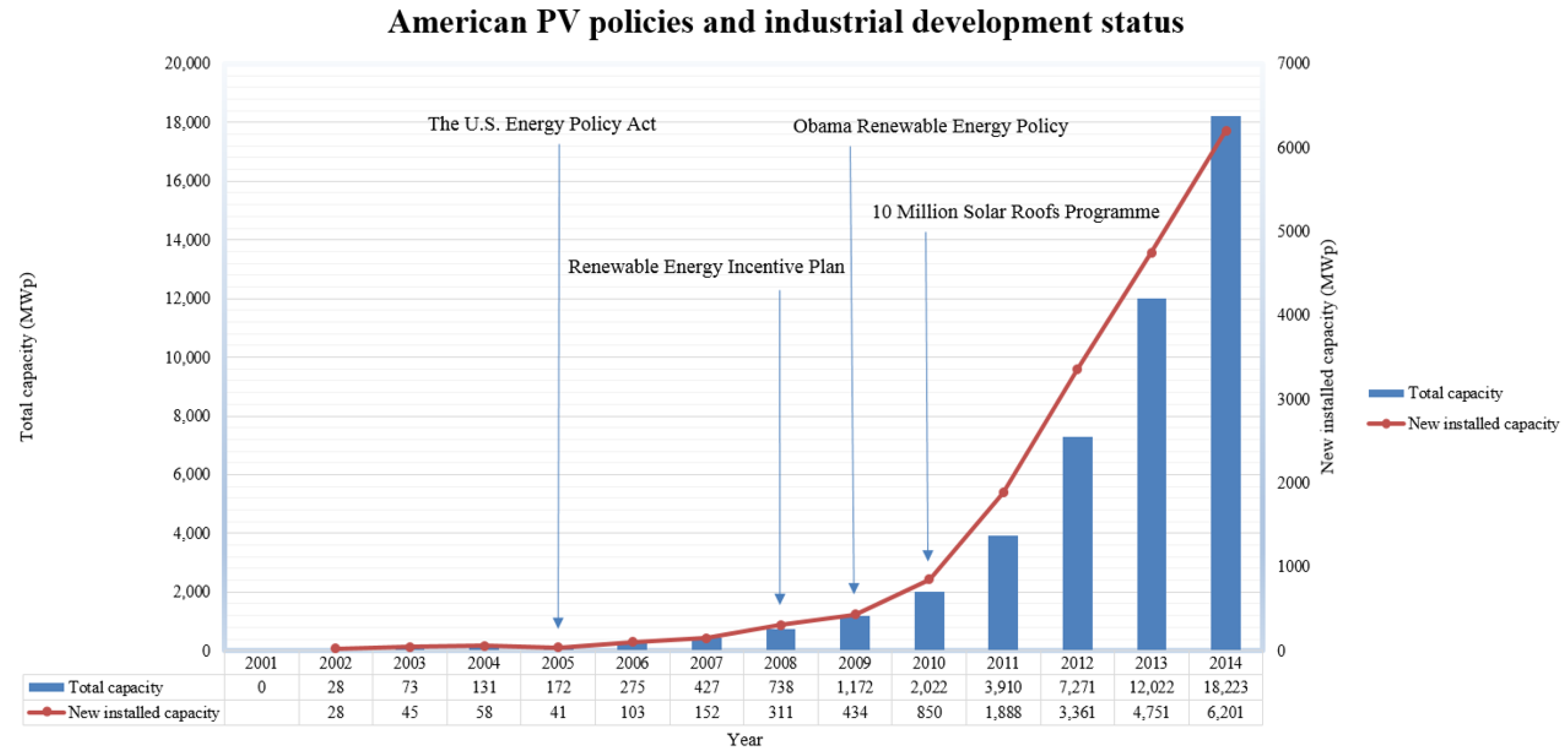

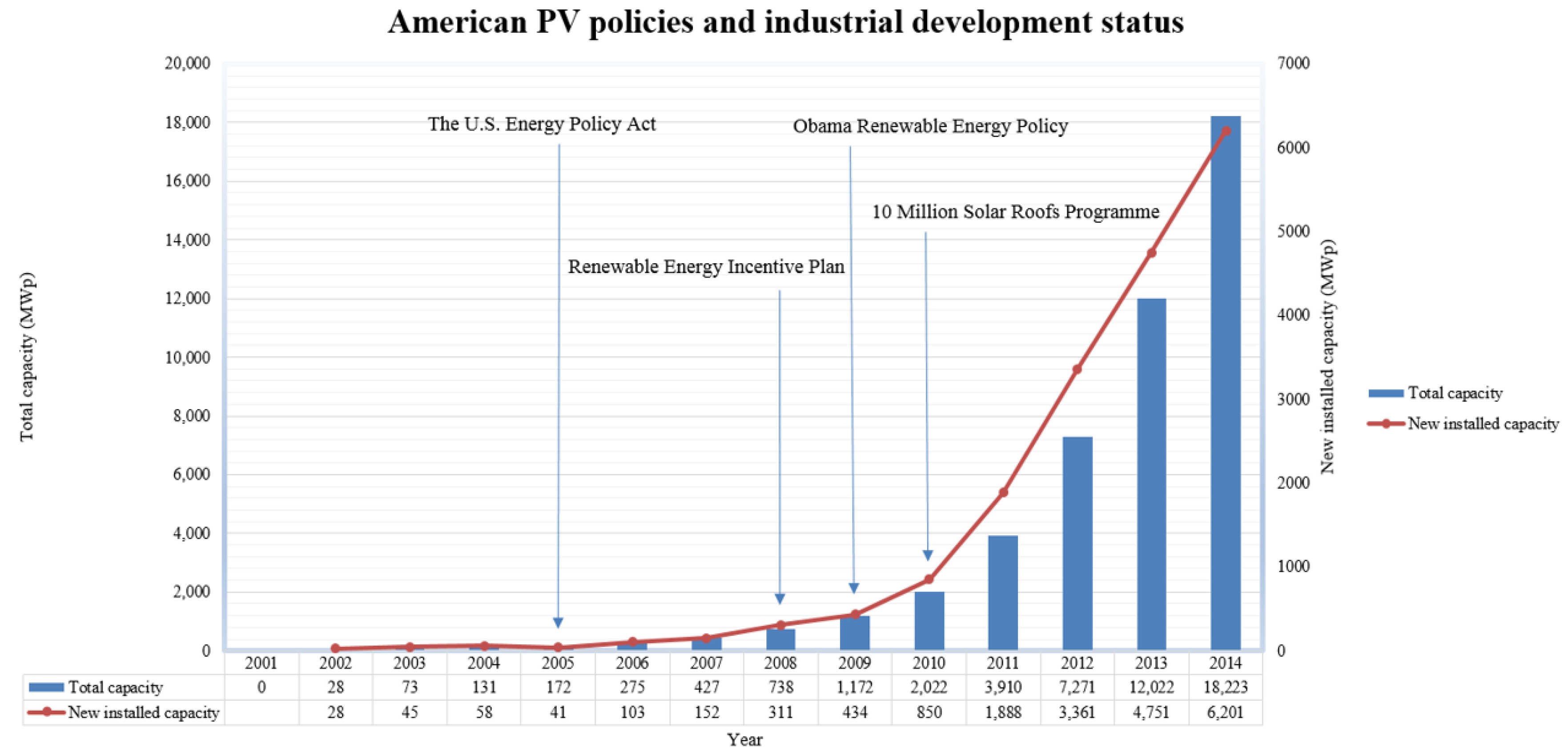

2.5. PV Incentive Policies in the USA

2.6. Lessons Learned from Leading Countries

3. Discussion of the Hong Kong Case

3.1. Technology Choice for HK

3.2. Installation Resources for BIPV in HK

3.3. Possible Initiatives for Hong Kong

3.3.1. Legal Measures

3.3.2. Installation Cost Support Measures

3.3.3. Financial Support Measures

3.3.4. Feed-in Tariff Measures

4. Discussion

5. Conclusions

- (1)

- The BIPV system, which requires little extra installation and land, is a promising way of relieving the increasing financial and environmental costs of fossil fuel energy generation.

- (2)

- Due to the relatively high initial investment and service costs, it is still difficult for PV technology to compete against fossil fuels in Hong Kong’s local energy market of. The government should release subsidy and sustain policies to help the PV industry grow.

- (3)

- The service and labor market should be opened up to providers abroad to reduce the price. Measures must be taken to further improve the efficiency of practitioners so that the soft costs could also be cut.

- (4)

- Subsidy of PV development with PV electricity grants should be implemented to support the PV business.

Acknowledgments

Author Contributions

Conflicts of Interest

References

- Electrical and Mechanical Services Department (EMSD). “Hong Kong Energy End-Use Data 2014”. Available online: http://www.emsd.gov.hk/filemanager/en/content_762/HKEEUD2014.pdf (accessed on 30 June 2016).

- CLP Power Hong Kong Limited. ‘Response to Hong Kong’s Climate Change Strategy and Action Agenda’. Available online: http://www.epd.gov.hk/epd/english/climate_change/consult.html (accessed on 30 June 2016).

- Ni, M.; Leung, M.K.H.; Sumathy, K.; Leung, D.Y.C. Potential of renewable hydrogen production for energy supply in Hong Kong. Int. J. Hydrog. Energy 2006, 31, 1401–1412. [Google Scholar] [CrossRef]

- Peng, J.Q.; Lu, L. Investigation on the development potential of rooftop PV system in Hong Kong and its environmental benefits. Renew. Sustain. Energy Rev. 2013, 27, 149–162. [Google Scholar] [CrossRef]

- Gao, X.X.; Yang, H.; Lu, L. Study on offshore wind power potential and wind farm optimization in Hong Kong. Appl. Energy 2014, 130, 519–531. [Google Scholar] [CrossRef]

- Parida, B.; Iniyan, S.; Goic, R. A review of solar photovoltaic technologies. Renew. Sustain. Energy Rev. 2011, 3, 1625–1636. [Google Scholar] [CrossRef]

- Yuan, J.; Sun, S.; Zhang, W.; Xiong, M. The economy of distributed PV in China. Energy 2014, 78, 939–949. [Google Scholar] [CrossRef]

- Ding, M.; Xu, Z.; Wang, W.; Wang, X.; Song, Y.; Chen, D. A review on China’s large-scale PV integration: Progress, challenges and recommendations. Renew. Sustain. Energy Rev. 2016, 53, 639–652. [Google Scholar] [CrossRef]

- Kaushika, N.D.; Gautam, N.K.; Kaushik, K. Simulation model for sizing of standalone solar PV system with interconnected array. Sol. Energy Mater. Sol. Cells 2005, 85, 499–519. [Google Scholar] [CrossRef]

- Fernández-Infantes, A.; Contreras, J.; Bernal-Agustín, J.L. Design of grid connected PV systems considering electrical, economical and environmental aspects: A practical case. Renew. Energy 2006, 31, 2042–2062. [Google Scholar] [CrossRef]

- Li, D.H.W.; Cheung, K.L.; Lam, T.N.T.; Chan, W.W.H. A study of grid-connected photovoltaic (PV) system in Hong Kong. Appl. Energy 2011, 90, 122–127. [Google Scholar] [CrossRef]

- Cerón, I.; Caamaño-Martín, E.; Neila, F.J. ‘State-of-the-art’ of building integrated photovoltaic products. Renew. Energy 2013, 58, 127–133. [Google Scholar] [CrossRef] [Green Version]

- Reisi, A.R.; Moradi, M.H.; Jamasb, S. Classification and comparison of maximum power point tracking techniques for photovoltaic system: A review. Renew. Sustain. Energy Rev. 2013, 19, 433–443. [Google Scholar] [CrossRef]

- Chaurey, A.; Deambi, S. Battery storage for PV power systems: An overview. Renew. Energy 1992, 2, 227–235. [Google Scholar] [CrossRef]

- Lambert, D.W.H.; Holland, R.; Crawley, K. Appropriate battery technology for a new, rechargeable, micro-solar lantern. J. Power Sources 2000, 88, 108–114. [Google Scholar] [CrossRef]

- Hua, S.; Zhou, Q.; Kong, D.; Ma, J. Application of valve-regulated lead-acid batteries for storage of solar electricity in stand-alone photovoltaic systems in the northwest areas of China. J. Power Sources 2006, 158, 1178–1185. [Google Scholar] [CrossRef]

- Schmid, L.A.; Hoffmann, C.A.A. Replacing diesel by solar in the Amazon: short-term economic feasibility of PV-diesel hybrid systems. Energy Policy 2004, 32, 881–898. [Google Scholar] [CrossRef]

- Nelson, D.B.; Nehrir, N.H.; Wang, C. Unit sizing and cost analysis of stand-alone hybrid wind/PV/fuel cell power generation systems. Renew. Energy 2006, 31, 1641–1656. [Google Scholar] [CrossRef]

- Deshmukh, M.K.; Deshmukh, S.S. Modeling of hybrid renewable energy systems. Renew. Sustain. Energy Rev. 2008, 12, 235–249. [Google Scholar] [CrossRef]

- Enslin, J.H.R.; Wolf, M.S.; Snyman, D.B.; Swiegers, W. Integrated photovoltaic maximum power point tracking converter. IEEE Trans. Ind. Electron. 1997, 44, 769–773. [Google Scholar] [CrossRef]

- Noguchi, T.; Togashi, S.; Nakamoto, R. Short-current pulse-based maximum-power-point tracking method for multiple photovoltaic-and-converter module system. IEEE Trans. Ind. Electron. 2002, 49, 217–223. [Google Scholar] [CrossRef]

- Sun, X.; Wu, W.; Li, X.; Zhao, Q. A research on photovoltaic energy controlling system with maximum power point tracking. In Proceedings of the Power Conversion Conference, Osaka, Japan, 2–5 April 2002.

- Algazar, M.M.; Al-Monier, H.; El-Halim, H.A.; El Kotb Salem, M.E. Maximum power point tracking using fuzzy logic control. Electr. Power Energy Syst. 2012, 39, 21–28. [Google Scholar] [CrossRef]

- Abdelsalam, A.K.; Massoud, A.M.; Ahmed, S.; Enjeti, P.N. High-performance adaptive perturb and observe MPPT technique for photovoltaic-based microgrids. IEEE Trans. Power Electron. 2011, 26, 1010–1021. [Google Scholar] [CrossRef]

- Moradi, M.H.; Reisi, A.R. A hybrid maximum power point tracking method for photovoltaic systems. Sol. Energy 2011, 85, 2965–2976. [Google Scholar] [CrossRef]

- IEA. Technology Roadmap: Solar Photovoltaic Energy—2014 Edition. Available online: http://www.iea.org/publications/freepublications/publication/technology-roadmap-solar-photovoltaic-energy---2014-edition.html (accessed on 20 July 2016).

- Ratnam, E.L.; Weller, S.R.; Kellett, C.M. Scheduling residential battery storage with solar PV: Assessing the benefits of net metering. Appl. Energy 2015, 155, 881–891. [Google Scholar] [CrossRef]

- Khoury, J.; Mbayed, R.; Salloum, G.; Monmasson, E. Optimal sizing of a residential PV-battery backup for an intermittent primary energy source under realistic constraints. Energy Build. 2015, 105, 206–216. [Google Scholar] [CrossRef]

- Khalilpour, R.; Vassallo, A. Planning and operation scheduling of PV-battery systems: A novel methodology. Renew. Sustain. Energy Rev. 2016, 53, 194–208. [Google Scholar] [CrossRef]

- Guinot, B.; Champel, B.; Montignac, F.; Lemaire, E.; Vannucci, D.; Sailler, S.; Bultel, Y. Techno-economic study of a PV-hydrogen-battery hybrid system for off-grid power supply: Impact of performances’ ageing on optimal system sizing and competitiveness. Int. J. Hydrog. Energy 2015, 40, 623–632. [Google Scholar] [CrossRef]

- Parra, D.; Walker, G.S.; Gillott, M. Modeling of PV generation, battery and hydrogen storage to investigate the benefits of energy storage for single dwelling. Sustain. Cities Soc. 2014, 10, 1–10. [Google Scholar] [CrossRef]

- Khalilpour, K.R.; Vassallo, A. Technoeconomic parametric analysis of PV-battery systems. Renew. Energy 2016, 97, 757–768. [Google Scholar] [CrossRef]

- Pearce, J.M. Expanding photovoltaic penetration with residential distributed generation from hybrid solar photovoltaic + combined heat and power systems. Energy 2009, 34, 1947–1954. [Google Scholar] [CrossRef]

- Mostofi, M.; Nosrat, A.H.; Pearce, J.M. Institutional-scale operational symbiosis of photovoltaic and cogeneration energy systems. Int. J. Environ. Sci. Technol. 2011, 8, 31–44. [Google Scholar] [CrossRef]

- Nosrat, A.H.; Swan, L.G.; Pearce, J.M. Improved performance of hybrid photovoltaic-trigeneration systems over photovoltaic–cogen systems including effects of battery storage. Energy 2013, 49, 366–374. [Google Scholar] [CrossRef]

- Ramli, M.A.M.; Hiendro, A.; Twaha, S. Economic analysis of PV/diesel hybrid system with flywheel energy storage. Renew. Energy 2015, 78, 398–405. [Google Scholar] [CrossRef]

- Tsuanyo, D.; Azoumah, Y.; Aussel, D.; Neveu, P. Modeling and optimization of batteryless hybrid PV (photovoltaic)/Diesel systems for off-grid applications. Energy 2015, 86, 152–163. [Google Scholar] [CrossRef]

- Li, C.; Ge, X.F.; Zheng, Y.; Xu, C.; Ren, Y.; Song, C.G.; Yang, C.X. Techno-economic feasibility study of autonomous hybrid wind/PV/battery power system for a household in Urumqi, China. Energy 2013, 55, 263–272. [Google Scholar] [CrossRef]

- Caballero, F.; Sauma, E.; Yanine, F. Business optimal design of a grid-connected hybrid PV (photovoltaic)-wind energy system without energy storage for an Easter Island’s block. Energy 2013, 61, 248–261. [Google Scholar] [CrossRef]

- Bhattacharjee, S.; Acharya, S. PV–wind hybrid power option for a low wind topography. Energy Convers. Manag. 2015, 89, 942–954. [Google Scholar] [CrossRef]

- Rehman, S.; Alam, M.M.; Meyer, J.P.; Al-Hadhrami, L.M. Feasibility study of a wind–PV–diesel hybrid power system for a village. Renew. Energy 2012, 38, 258–268. [Google Scholar] [CrossRef]

- Maheri, A. Multi-objective design optimisation of standalone hybrid wind-PV-diesel systems under uncertainties. Renew. Energy 2014, 66, 650–661. [Google Scholar] [CrossRef]

- Bianchini, A.; Magnelli, N.; Ferrara, G.; Carneval, E.A.; Ferrar, L. Optimization of a PV-wind-diesel hybrid system for a remote stand-alone application. Energy Procedia 2015, 81, 133–145. [Google Scholar] [CrossRef]

- Shezan, SK.A.; Julai, S.; Kibria, M.A.; Ullah, K.R.; Saidur, R.; Chong, W.T.; Akikur, R.K. Performance analysis of an off-grid wind-PV (photovoltaic)-diesel-battery hybrid energy system feasible for remote areas. J. Clean. Prod. 2016, 125, 121–132. [Google Scholar] [CrossRef]

- Fthenakis, V.M. End-of-life management and recycling of PV modules. Energy Policy 2000, 28, 1051–1058. [Google Scholar] [CrossRef]

- Goe, M.; Gaustad, G. Estimating direct climate impacts of end-of-life solar photovoltaic recovery. Sol. Energy Mater. Sol. Cells 2016, in press. [Google Scholar] [CrossRef]

- Tao, J.; Yu, S. Review on feasible recycling pathways and technologies of solar photovoltaic modules. Sol. Energy Mater. Sol. Cells 2015, 141, 108–124. [Google Scholar] [CrossRef]

- McDonald, N.C.; Pearce, J.M. Producer responsibility and recycling solar photovoltaic modules. Energy Policy 2010, 38, 7041–7047. [Google Scholar] [CrossRef]

- Peng, J.Q.; Lu, L.; Yang, H.X. Review on life cycle assessment of energy payback and greenhouse gas emission of solar photovoltaic systems. Renew. Sustain. Energy Rev. 2013, 19, 255–274. [Google Scholar] [CrossRef]

- Lu, L.; Peng, J.; Yang, H. Environmental Payback Time Analysis of Building-Integrated Photovoltaic (BIPV) Applications in Hong Kong. Appl. Energy 2010, 87, 3625–3631. [Google Scholar] [CrossRef]

- Masson, G.; Latour, M.; Rekinger, M.; Theologitis, I.T.; Papoutsi, M. Global Market Outlook for Photovoltaics 2013–2017. Available online: http://www.construction21.org/articles/h/report--global-market-outlook-for-photovoltaics-2013-2017.html (accessed on 15 July 2016).

- Martinot, Eric, REN21 Renewables Global Futures Report. Available online: http://www.ren21.net/future-of-renewables/global-futures-report/ (accessed on 15 July 2016).

- IEA-PVPS, 2015 Snapshot of Global Photovoltaic Markets. Available online: http://www.iea-pvps.org/index.php?id=241 (accessed on 15 July 2016).

- Karakaya, E.; Sriwannawit, P. Barriers to the adoption of photovoltaic systems: The state of the art. Renew. Sustain. Energy Rev. 2015, 49, 60–66. [Google Scholar] [CrossRef] [Green Version]

- BSW-Solar. Statistic Data on the German Solar Power (Photovoltaic) Industry; German Solar Industry Association (BSW-Solar): Berlin, Germany, 2014. [Google Scholar]

- CLP Power Hong Kong Limited. Energy Charge for Residential Customers. Available online: https://www.clp.com.hk/en/customer-service/tariff/residential-customers (accessed on 9 August 2015).

- Zhang, X.; Shen, L.; Chan, S.Y. The diffusion of solar energy use in HK: What are the barriers? Energy Policy 2012, 41, 241–249. [Google Scholar] [CrossRef]

- Menz, F.C.; Vachon, S. The effectiveness of different policy regimes for promoting wind power: Experiences from the states. Energy Policy 2016, 34, 1786–1796. [Google Scholar] [CrossRef]

- Yin, H.; Powers, N. Do state renewable portfolio standards promote in-state renewable generation. Energy Policy 2010, 38, 1140–1149. [Google Scholar] [CrossRef]

- Buckman, G. The effectiveness of Renewable Portfolio standard banding and carve-outs in supporting high-cost types of renewable electricity. Energy Policy 2011, 39, 4105–4114. [Google Scholar] [CrossRef]

- International Energy Agency (IEA). National Survey Report of PV Power Applications in Japan 2010; IEA: Tokyo, Japan, 2011. [Google Scholar]

- Chapman, A.J.; McLellan, B.; Tezuka, T. Residential solar PV policy: An analysis of impacts, successes and failures in the Australian case. Renew. Energy 2016, 86, 1265–1279. [Google Scholar] [CrossRef]

- Huang, P.; Negro, S.O.; Hekkert, M.P.; Bin, K.X. How China became a leader in solar PV: An innovation system analysis. Renew. Sustain. Energy Rev. 2016, 64, 777–789. [Google Scholar] [CrossRef]

- Barbose, G.; Wiser, R.; Heeter, J.; Mai, T.; Bird, L.; Bolinger, M.; Carpenter, A.; Heath, G.; Keyser, D.; Macknick, J.; et al. A retrospective analysis of benefits and impacts of U.S. renewable portfolio standards. Energy Policy 2016, 96, 645–660. [Google Scholar] [CrossRef]

- Dusonchet, L.; Telaretti, E. Comparative economic analysis of support policies for solar PV in the most representative EU countries. Renew. Sustain. Energy Rev. 2015, 42, 986–998. [Google Scholar] [CrossRef]

- Kaizuka, I. Net billing schemes, experience from Japan e evolution to net Export FiT. In Proceedings of the PVPS Workshop, Frankfurt, Germany, 24 September 2012; pp. 1–20.

- Myojo, S.; Ohashi, H. Effects of consumer subsidies for renewable energy on industry growth and welfare: Japanese solar energy. In Proceedings of the 39th Annual Conference of European Association for Research in Industrial Economics, Rome, Italy, 2–4 September 2012.

- Foster, R. Japan Photovoltaics Market Overview; Sandia National Laboratory, US Department of Energy: Livermore, CA, USA, 2005; pp. 1–36. [Google Scholar]

- Sweden, M. Residential PV system installation in Japan e example of PV community. In Proceedings of the Stakeholders Workshop IEA PVPS Task 10, Malmö, Sweden, 14 November 2006; pp. 1–28.

- Huenteler, J.; Schmidt, T.S.; Kanie, N. Japan’s post-Fukushima challenge-implications from the German experience on renewable energy policy. Energy Policy 2012, 45, 6–11. [Google Scholar] [CrossRef]

- Japan Renewable Energy Policy Platform. Renewables Japan Status Report 2010 Executive Summary; JREPP: Tokyo, Japan, 2010. [Google Scholar]

- Yamamoto, Y. Rooftops and Residential: Solar Power in Japan; Suntech Power: Tokyo, Japan, 2012; Available online: http://blog.suntechpower.com/2012/suntechexplains/rooftops-and-residential-solar-power-in-japan/ (accessed on 13 November 2014).

- Plasto, J. PV: Big in Japan. Inter PV.net. Available online: http://www.interpv.net/market/market_view.asp?idx=312&part_code=04&page=5;2010 (accessed on 13 November 2014).

- Yamada, H.; Ikki, O. National survey report of PV power application in Japan 2012. In IEA Cooperative Programme on PVPS Task 1 Exchanging and Dissemination of Information on PV Power Systems; IEA: Tokyo, Japan, 2013; pp. 1–45. [Google Scholar]

- Avril, S.; Mansilla, C.; Busson, M.; Lemaire, T. Photovoltaic energy policy: Financial estimation and performance comparison of the public support in five representative countries. Energy Policy 2012, 51, 244–258. [Google Scholar] [CrossRef]

- Reinmuller, D.; Praetorius, B.; Langniss, O. Sustainable Energy Policy Concepts; Final Report; International Solar Energy Society: Freiburg, Germany, 2002. [Google Scholar]

- Grau, T.; Huo, M.; Neuhoff, K. Survey of photovoltaic industry and policy in Germany and China. Energy Policy 2012, 51, 20–37. [Google Scholar] [CrossRef]

- Fulton, M.; Capalino, R. The German Feed-in Tariff: Recent Policy Changes; Deutsche Bank Group Investment Research Report; Deutsche Bank Group: Frankfurt, Germany, 2012. [Google Scholar]

- Terna Rapporto Mensile Sul Sistema Elettrico. Available online: http://www.terna.it/it-it/sistemaelettrico/dispacciamento/datiesercizio/rapportomensile.aspx (accessed on 13 June 2016).

- Ministero dell’Ambiente e della Tutela del Territorio e del Mare. Decreto Ministeriale 16 Marzo 2001—Programma Tetti Fotovoltaici; Ministero dell’Ambiente e della Tutela del Territorio e del Mare: Roma, Italy, 2001. [Google Scholar]

- Orioli, A.; Gangi, A.D. The recent change in the Italian policies for photovoltaics: Effects on the payback period and levelized cost of electricity of grid-connected photovoltaic systems installed in urban contexts. Energy 2015, 92, 1989–2005. [Google Scholar] [CrossRef]

- Italian Government. Decreto Ministeriale 28 Luglio 2005—Criteri per L’Incentivazione Della Produzione di Energia Elettrica Mediante Conversione Fotovoltaica Della Fonte Solare; Italian Government: Rome, Italy, 2005.

- Italian Government. Decreto Ministeriale 6 Febbraio 2006-Criteri per L’Incentivazione Della Produzione di Energia Elettrica Mediante Conversione Fotovoltaica Della Fonte Solare—Dlgs 387/2003-Modifica DM 28 Luglio 2005; Italian Government: Rome, Italy, 2005.

- Italian Government. Decreto Ministeriale 19 Febbraio 2007—Criteri e Modalità per Incentivare la Produzione di Energia Elettrica Mediante Conversione Fotovoltaica Della Fonte Solare, in Attuazione Dell’articolo 7 del Decreto Legislativo 29 Dicembre 2003, n. 387; Italian Government: Rome, Italy, 2007.

- AEEG—Autorità per l’Energia Elettrica, il Gas e il Sistema Idrico. Delibera ARG/elt 74/08. Testo Integrato Delle Modalità E Delle Condizioni Tecnico-Economiche per lo Scambio sul Posto (TISP). Available online: http://www.autorita.energia.it/it/docs/08/074-08arg.htm (accessed on 13 June 2016).

- Italian Government. Decreto Ministeriale 6 Agosto 2010—Incentivazione Della Produzione di Energia Elettrica Mediante Conversione Fotovoltaica Della Fonte Solare; Italian Government: Rome, Italy, 2010.

- Italian Government. Decreto Ministeriale 5 Maggio 2011—Incentivazione Della Produzione di Energia Elettrica da Impianti Solari Fotovoltaici; Italian Government: Rome, Italy, 2011.

- Cucchiella, F.; D’Adamo, I. Feasibility study of developing photovoltaic power projects in Italy: An integrated approach. Renew. Sustain. Energy Rev. 2012, 16, 1562–1576. [Google Scholar] [CrossRef]

- Italian Government. Decreto Ministeriale 5 Luglio 2012—Attuazione dell’art. 25 del Decreto Legislativo 3 Marzo 2011, n. 28, Recante Incentivazione Della Produzione di Energia Elettrica da Impianti Solari Fotovoltaici (c.d. Quinto Conto Energia); Italian Government: Rome, Italy, 2012.

- Zhang, S.; He, Y. Analysis on the development and policy of solar PV power in China. Renew. Sustain. Energy Rev. 2013, 21, 393–401. [Google Scholar] [CrossRef]

- National Development and Reform Commission. The Perfection of Photovoltaic Price Policy 2013. Available online: http://tgs.ndrc.gov.cn/ggkx/201309/t20130903_557009.html (accessed on 13 May 2015).

- Zahran, S.; Brody, D.; Vedlitz, A.; Lacy, M.; Schelly, C. Greening local energy explaining the geographic distribution of household solar energy use in the United States. J. Am. Plan. Assoc. 2008, 74, 419–434. [Google Scholar] [CrossRef]

- Denholm, P.; Margolis, R. Supply Curves for Rooftop Solar PV-Generated Electricity for the United States; Technical Report; National Renewable Energy Laboratory: Golden, CO, USA, 2008.

- Pelland, S.; Poissant, Y. An evaluation of the potential of building integrated photovoltaics in Canada. In Proceedings of the 31st Annual Conference of the Solar Energy Society of Canada (SESCI), Montréal, QC, Canada, 20–24 August 2006.

- Defaix, P.R.; van Sark, W.G.; Worrell, E.; de Visser, E. Technical potential for photovoltaics on buildings in the EU-27. Sol. Energy 2012, 86, 2644–2653. [Google Scholar] [CrossRef]

- Radhi, H. On the value of decentralized PV systems for the GCC residential sector. Energy Policy 2011, 39, 2020–2027. [Google Scholar] [CrossRef]

- Radhi, H. Trade-off between environmental and economic implications of PV systems integrated into the UAE residential sector. Renew. Sustain. Energy Rev. 2012, 16, 2468–2474. [Google Scholar] [CrossRef]

- National Renewable Energy Laboratory. System Advisor Model-Help; National Renewable Energy Laboratory: Golden, CO, USA, 2015.

- Electric Price of CLP. Available online: https://www.clp.com.hk/zh/customer-service-site/tariff-site/Documents/clp_tarifftable_chi.pdf (accessed on 13 May 2015).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Investment Support | |||

Law:

| Installation:

| Financing:

| |

| Return Support | |||

Feed-in tariff:

| PV electricity grant:

| ||

| Germany | Italy | Japan | Mainland China | USA | |

|---|---|---|---|---|---|

| 1991 |

| ||||

| 1992 |

| ||||

| 1993 |

| ||||

| 1994 |

| ||||

| 1999 |

| ||||

| 2001 |

| ||||

| 2003 |

| ||||

| 2004 |

| ||||

| 2005 |

|

|

| ||

| 2007 |

| ||||

| 2008 |

| ||||

| 2009 |

|

|

| ||

| 2010 |

|

| |||

| 2011 |

| ||||

| 2012 |

| ||||

| 2013 |

|

| 2016 | 2017 | 2018 | 2019 | 2020 | |

|---|---|---|---|---|---|

| Annual new installation capacity (MWp) | 400.0 | 400.0 | 400.0 | 400.0 | 400.0 |

| Accumulated installation capacity (MWp) | 400.0 | 800.0 | 1200.0 | 1600.0 | 2000.0 |

| Estimated annual PV power generation (GWh) | 345.2 | 690.4 | 1035.6 | 1380.8 | 1726.0 |

| Estimated total power generated during lifetime of annual installation (GWh) | 6285.85 | 6285.85 | 6285.85 | 6285.85 | 6285.85 |

| Unit Investment (HKD/Wp) | HKD 23.64 | HKD 22.46 | HKD 21.34 | HKD 20.27 | HKD 19.26 |

| LCOE without any subsidy (HKD/kWh) | HKD 1.50 | HKD 1.43 | HKD 1.36 | HKD 1.29 | HKD 1.23 |

| 2016 | 2017 | 2018 | 2019 | 2020 | |

|---|---|---|---|---|---|

| Government subsidy in 20% case (Billion HKD) | 1.89 | 1.79 | 1.70 | 1.62 | 1.54 |

| Real investment in 20% case (Billion HKD) | 7.56 | 7.18 | 6.82 | 6.48 | 6.16 |

| LCOE of 20% case (HKD/kWh) | 1.20 | 1.14 | 1.09 | 1.03 | 0.98 |

| Government subsidy in 60% case (Billion HKD) | 5.67 | 5.39 | 5.12 | 4.86 | 4.62 |

| Real investment in 60% case (Billion HKD) | 3.78 | 3.59 | 3.41 | 3.24 | 3.08 |

| LCOE of 60% case (HKD/kWh) | 0.60 | 0.57 | 0.54 | 0.52 | 0.49 |

| Government subsidy in fixed 4 HKD case (Billion HKD) | 1.60 | 1.60 | 1.60 | 1.60 | 1.60 |

| Real investment in fixed 4 HKD case (Billion HKD) | 7.86 | 7.38 | 6.94 | 6.51 | 6.10 |

| LCOE of fixed 4 HKD case (HKD/kWh) | 1.25 | 1.17 | 1.10 | 1.04 | 0.97 |

| 2016 | 2017 | 2018 | 2019 | 2020 | |

|---|---|---|---|---|---|

| Annual new installation capacity (MWp) | 400.0 | 400.0 | 400.0 | 400.0 | 400.0 |

| Accumulated installation capacity (MWp) | 400.0 | 800.0 | 1200.0 | 1600.0 | 2000.0 |

| Estimated annual PV power generation (MWh) | 345.2 | 690.4 | 1035.6 | 1380.8 | 1726.0 |

| Estimated electricity generated during lifetime (MWh) 20 year with 1% degradation per year | 6285.85 | 6285.85 | 6285.85 | 6285.85 | 6285.85 |

| Unit Investment (HKD/Wp) | HKD 23.64 | HKD 22.46 | HKD 21.34 | HKD 20.27 | HKD 19.26 |

| LCOE (HKD/kWh) | 1.50 | 1.42 | 1.35 | 1.29 | 1.22 |

| FiT (HKD/kWh) | 0.51 | 0.44 | 0.37 | 0.30 | 0.23 |

| Total FiT cost to government (Billion HKD) | 0.17 | 0.33 | 0.45 | 0.56 | 0.64 |

© 2016 by the authors; licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC-BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Song, A.; Lu, L.; Liu, Z.; Wong, M.S. A Study of Incentive Policies for Building-Integrated Photovoltaic Technology in Hong Kong. Sustainability 2016, 8, 769. https://doi.org/10.3390/su8080769

Song A, Lu L, Liu Z, Wong MS. A Study of Incentive Policies for Building-Integrated Photovoltaic Technology in Hong Kong. Sustainability. 2016; 8(8):769. https://doi.org/10.3390/su8080769

Chicago/Turabian StyleSong, Aotian, Lin Lu, Zhizhao Liu, and Man Sing Wong. 2016. "A Study of Incentive Policies for Building-Integrated Photovoltaic Technology in Hong Kong" Sustainability 8, no. 8: 769. https://doi.org/10.3390/su8080769