Assessment of Construction Cost Saving by Concrete Mixing the Activator Material

Building and Urban Research Institute, Korea Institute of Civil Engineering and Building Technology, Daehwa-dong 283, Goyandae-Ro, ILsanseo-Gu, Goyang-Si, Gyeonggi-Do 10223, Korea

Sustainability 2016, 8(4), 403; https://doi.org/10.3390/su8040403

Submission received: 5 February 2016

/

Revised: 1 April 2016

/

Accepted: 8 April 2016

/

Published: 23 April 2016

(This article belongs to the Section Sustainable Engineering and Science)

Abstract

:Studies which reduce cement usage, develop an alternative by partial replacement of cement with blast-furnace slag, fly ash, or such industrial byproducts, and evaluate the environmental load and economic value of concrete mixed with such are in high demand. In this study, A-BFS (Activator Blast Furnace Slag), which is mixed with an activator in order to induce early-age strength manifestation of BFS mixed concrete was used to execute a physical property evaluation of concrete. This study first conducted physical property tests for compression strength of concrete that partially replaced OPC (ordinary Portland cement) with A-BFS and executed a comparison/analysis with 100% OPC. It was thought that if concrete early strength is manifested through this process when applied to RC (Reinforced Concrete) building, at most a three to four day construction cycle would be possible, according to which the economic value of the construction period reduction was evaluated. For this evaluation, general apartment houses (Case 1) were taken as the evaluation subject, and for comparison, Cases 2, 3, and 4 were set up by the mix ratio of A-BFS, and the economic value evaluation range was established. As a result, it was found that Case 2 had no change from Case 1, while Case 3 saved about 106,654,762 KRW (Korea Won) and Case 4 saved about 159,982,143 KRW.

1. Introduction

In the case of concrete mixed with the fine powder of blast furnace slag and a mixture of ordinary Portland cement, compressive strength at an early age shows a low strength expression rate compared to the compressive strength of concrete that only uses OPC, with particularly slow expression of strength under a low temperature environment. This causes difficulty in the active use of this concrete due to delays in the construction of reinforced concrete structures and freezing-thawing. Therefore, in this study, an evaluation on the physical properties of concrete was carried out using an A-BFS (Activator Blast Furnace Slag) mixed with an activator in order to induce the expression of strength in BFS (Blast Furnace Slag)-mixed concrete at an earlier age. In addition, after reviewing the characteristic of early strength expression by A-BFS, the removal time of forms was expected to be shortened by application of A-BFS concrete in RC building structure construction. Quantitative assessment on economic feasibility of the effects in shortening of construction time and reduction of construction expense was performed.

According to South Korea’s standard specification for construction, if the structural concrete compressive strength is 5 MPa or higher, then the side forms, such as foundation, beams, columns, and walls, can be removed. In addition, in case common concrete is used, are allowed to be eliminated without a compressive strength test after six days when the average daily temperature ranges from 10–20 °C and in four or more days if it exceeds 20 °C [1].

In this study, OPC was compared to common concrete through a physical test on the concrete partially replaced with A-BFS. If an early-strength concrete test is developed when the RC structure is applied, it could be constructed in 3–4 days. Therefore, construction costs according to the shortening of a construction period were assessed.

For the assessment of construction costs, in addition, an apartment has been chosen as the subject building (hereinafter referred to as the “Case 1”), and the comparisons (Cases 2–4) were selected according to the A-BFS mix ratio.

Then, the construction costs by case according to the A-BFS replacement ratio and considering overhead costs, home office overhead, and interest expenses were evaluated.

2. Literature Review

2.1. Concept of Economic Analysis

For the economic analysis, a cost-benefit analysis technique was used to perform validity analysis on an investment and was applied for a cost comparison of facility construction. While they are identical in that both consider the temporal value of cost, cost-benefit analysis explicitly handles both cost and benefit, while economic analysis only handles cost. Since this study analyzes the direct economic benefit of applying A-BFS concrete at early strength expression agent and considers the benefit of a shortened construction period, a cost-benefit analysis which evaluates the economic benefit of shortened construction time must be paralleled [2].

2.2. Global Trend of Economic Assessment Research

Most Korean construction companies compute economic assessments for apartment houses based on a standard estimation and unit cost. The standard estimation is data published for the purpose of providing a general standard for computation of an appropriate predetermined price of construction being carried out by public institutions, such as the government. Standard estimation is used as basic data by national and local governments, government-invested institutions, and institutions that require supervision and authorization by the above institutions. Standard estimation and unit costs are published on an annual basis by the Construction Association of Korea (CAK) [3].

Economic assessments on buildings in Korea can be summarized as standard estimation and actual construction cost system. Some studies are criticizing that standard estimation is inappropriate for computing construction costs because it cannot properly reflect constantly-changing market prices and has limitations in the accommodation of new technologies and construction methods. Such studies emphasize the importance of actual construction costs. However, the actual construction cost system is not yet being widely used by Korean construction companies, and most of the economic assessments in the practical construction field were analyzed using standard estimation and unit cost.

Overseas, the elemental cost method and the elemental unit quantity method are widely used methods of economic assessment. The elemental cost method is a method that computes construction costs per unit area based on the total floor area of a corresponding building and briefly calculates construction costs by multiplying the cost per unit area with total floor area. The elemental unit quantity method is a method that computes the required expenses by multiplying the quantity of each material in the building with the unit price of each material.

This method is similar to the standard estimation, unit cost, and actual construction cost integration methods of Korea. The California Department of Transportation in the United States performs estimation using a computer program for business costs and construction costs called BEES (Basic Engineering System). This system, in particular, is composed of road sector and structure estimations. Additionally, the system of business cost computation is classified into the preliminary engineer’s cost estimate and the final engineer’s cost estimate. The second method is a method of cost analysis that uses labor expenses and the material expense of production.

In the case of Japan, economic assessment methods can be largely divided into bugakari method, market price method, subscribed estimate integration method for major materials, and unit price method. First, the method uses bugakari (estimation, in the case of Korea), which refers to an indication of the amount of site laborers, materials, such as reinforcements and cements, and machinery, like cranes and bulldozers, needed to construct a unit amount of each construction type [4,5]. The bugakari method can be referred to as an index showing productivity of construction. Second, the market price method involves unit construction costs in a changing market environment that examines direct construction expenses using the transaction price between the general constructor and subcontracted constructors to reflect the actual market price in integration [6,7].

2.3. Research Trends in the Estimation of Apartment Construction Costs

For the efficient management of construction costs, Barrie et al. [8] suggested preliminary estimates, fair-cost estimates, and definite estimates. Kim et al. [9] classified estimates into preliminary and definite estimates depending on accuracy and pre-cost and post-cost according to quotation time.

Pre-cost is the cost estimated before construction is completed. It is classified into preliminary estimates, design estimates, construction estimates, and budget cost of work schedule (BCWS). In contrast, post-cost refers to actual consumption (so-called “actual cost”). It represents basic data used for the preparation of construction settlement statements of financial statements. Im et al. [10] classified estimates into preliminary, definite, process, and settlement estimates. The types and characteristics of estimates classified in previous studies are stated in Table 1. The ideal results which have been consistently asserted in previous studies are that pre-cost and post-cost are the same.

The results of the analysis on construction cost estimation techniques by researchers are summarized by investigating previous studies on the estimation of construction costs (Table 1). The results obtained through the construction cost estimation methods are expressed in total construction costs. In terms of the estimation method, regression analysis, artificial neural network (ANN), and case-based reasoning have been used. Among them, regression analysis has been most common. Considering its relatively high forecasting accuracy, it would be reasonable to develop an estimation model using regression analysis.

A total of 15 research variables were chosen through these methods as follows: gross floor area, site area, building area, building coverage ratio, floor area ratio, average height, number of underground floors, number of buildings, number of households, average area (m2), parking lot size, and finish work costs (Table 2).

2.4. Research Trend of Concrete Using Blast Furnace Slag

Recently in Korea, studies on cementless concrete or geopolymer concrete, which only uses fine powder of blast furnace slag without using any ordinary Portland cement to harden with an alkali activator, are being conducted by material development and application as secondary products [25].

However, it cannot be applied to concrete structures like apartment houses due to the difficulty in mass production for in-site concrete, and low durability [26].

In addition, while existing studies on improvement in early strength mainly use early strength admixture and early strength cement to apply a rich mix concrete with high strength, there are hardly any studies on improving early age (one day, three days) strength of concrete mixed with fine powder of blast furnace slag. Studies for shortening of the construction period are mainly conducted on reinforcement bar line assembly technology, system form application technology, and precast material application technology. Among studies on the improvement of early strength in concrete, studies on shortening of the construction period through improved early strength of high strength concrete, such as 10 MPa/10 h in sliding forms are receiving the spotlight. There was no study on early removal (age of 1–3 days) of forms in apartment structures [27].

Kritsada et al. researched the influence of fly ash and slag replacement on the carbonation rate of the concrete. An experimental investigation on the influences of pozzolanic replacement and curing period on carbonation resistance of concrete was carried out. A tentative model for estimating the carbonation depth of concrete under natural exposure was proposed based on the results from accelerated tests [28]. Sabbie et al. investigates the influence of design age, in addition to mix proportions and geometric aspects, on the GWP associated with making beams, columns, and a concrete building frame [29]. Tatiana et al. examined if the reduction in production emissions of blended cements compensates for the reduced durability and CO2 capture [30].

2.5. Research Trend of Early-Stength Concrete

The previous studies on the removal time of forms when early-strength concrete was used were analyzed.

The removal time of side forms was mentioned in “Estimation of Removal Time of Side Form of the Concrete Incorporating Fine Particle Cement” [31] and “Determination of Removal Time of Side Forms Based on the Strength Development of Concrete” [32], and “Practical Application of High Early Strength Type Concrete Using High Early Strength Type Binder” [33]. However, it is not easy to use them in actual construction sites. In addition, they failed to mention when slab forms should be removed.

Other early-strength concrete-related studies include “Study on the Practical Application of High Early Strength Type Concrete Using Fine Particle Cement” [34] and “Fundamental Properties of the Concrete depending on the Liquid Type High Early Strength Agent” [35], “Effect of Ingredients of Liquid Accelerating Agent on Cement Mortar” [36], “Study on the Characteristics of Concrete Using AE Water Reducing Agents of Early-strength Type” [37], “Research on Early-strength Development of Concrete by Accelerating Agents” [38], “An Experimental Study on the Development of Early Strength Concrete for Reduction of Working Period in Apartment” [39], “Properties of Strength Development of Concrete at Early Age Incorporating Fine Particle Cement and Mineral Powder” [40], and “An Example of Construction Work Period Reduction Using Poly Carboxylate Acid Type Early Strength Concrete” [41]. However, these studies failed to suggest specific data on the removal time of forms. Even though there have been a lot of studies on early strength-type concrete, no study has ever mentioned the specific removal time of side and slab forms.

3. Experiment of Concrete Mixing Admixture

3.1. The Definition of Activator Blast-Furnace Slag (A-BFS)

A-BFS refers to an admixture made by mixing BFS and an activator additive (A-additive) to improve the performance of existing BFS products. A-BFS has early-stage strength development as shown Figure 1. A-additive is produced by collecting and manufacturing industrial byproducts from the production processes of other products, allowing for the necessary resources and energy for A-additive development to be recycled. Comprehensive research is currently being conducted on the manufacturing methods for the A-additive [42].

3.2. A-BFS Composite Material Analysis

3.2.1. Blast Furnace Slag (BFS)

BFS contains 95% to 99% of four ingredients; SiO2, Al2O3, CaO, and MgO. It has similar chemical properties to those of cement. These ingredients exhibit a reaction similar to the hydration reaction of cement; however, while ordinary Portland cement (OPC) exhibits a hydraulic reaction, granulated blast-furnace slag exhibits a latent hydraulic reaction. In other words, while the cement ingredients of OPC are eluted and a hydrate is formed and hardened by a hydraulic reaction with water molecules, the ingredients of granulated blast-furnace slag require the addition of a base or a sulfate for elution and cannot react solely by contact with water molecules. Instead, a reaction finally occurs with an addition of an activator, such as alkaline or sulfate salt. Hence, BFS has been widely used in the manufacture of concrete [43].

3.2.2. Activator Additive (A)

As shown in Table 3, Activator (A) additive is a chemical byproduct containing a mixture of calcium sulfoaluminate (C4A3S), Ca(OH)2, sodium hydroxide, limestone, and other chemicals that are added during the BFS manufacturing process. A is substituted for BFS to improve the existing BFS as shown in Figure 2. During the production process, A-BFS can be manufactured by mixing A-additive and existing BFS without additional processes [44].

Titanium Gypsum

If the absorbent “powdered limestone (CaCO3)” is reacted to remove SO2 generated at the combustion of fossil fuels (coal, oil) at a thermal power plant, in the Republic of Korea, Flue Gas Desulfurization (FGD) gypsum created as a byproduct is used as an additive by a cement manufacturer and for a secondary product.

The titanium gypsum used in this study is an industrial waste produced during the chemical reaction which neutralizes the acidity of sulfur into lime at the manufacture of titanium dioxide, and its chemical formula is CaSO4 + 2H2O. Titanium gypsum contains large amounts of CaO (39.2%) and SO3 (54.3%). If its particles come into contact with water molecules after drying, setting along with heating occurs. In addition, titanium gypsum works as a cement activator as well as the alkaline activator of BFS as pH increases from 6 (before calcination) to 7.5 (after calcination) when being mixed with limestone [45].

Sludge

Sludge is a substance in which turbid matter and coagulant hydroxide are concentrated. Since an aluminum coagulant is mostly used to remove turbid matters during the coagulation process, it is also called “alum sludge”.

The purpose of analyzing the chemical components of the dehydrated sludge is to process and recycle the sludge. The chemical components include water, coagulant, silica powder, and alumina powder. Since sludge is comprised of SiO2 (46.6%), Al2O3 (39.7%), and Fe2O3 (5.4%), it is close to clay in terms of ingredients. Therefore, it is very useful as an additive. In terms of the chemical components of the sludge applied to this study, silica powder (SiO2) was the highest with 35%–50%. In addition, a small amount of oxides (K, Mg, Na, Ca, Ti, S, P, etc.) were detected.

Limestone

Limestone is the most widely used mineral among the materials with CaO. It is widely distributed across Gangwon-do with a huge amount in reserve. It is lime (CaCO3) which accounts for the greatest portion in manufacturing clinker, the essential ingredient of Portland cement. This lime consists of CaO, SiO2, Al2O3, and Fe2O3. After a calcination reaction, it produces four clinker minerals: alite, belite, aluminate, and ferrite. Each clinker mineral reveals different cement characteristics depending on its content so that it would be available as a clinker activator through the appropriate chemical mixture of materials.

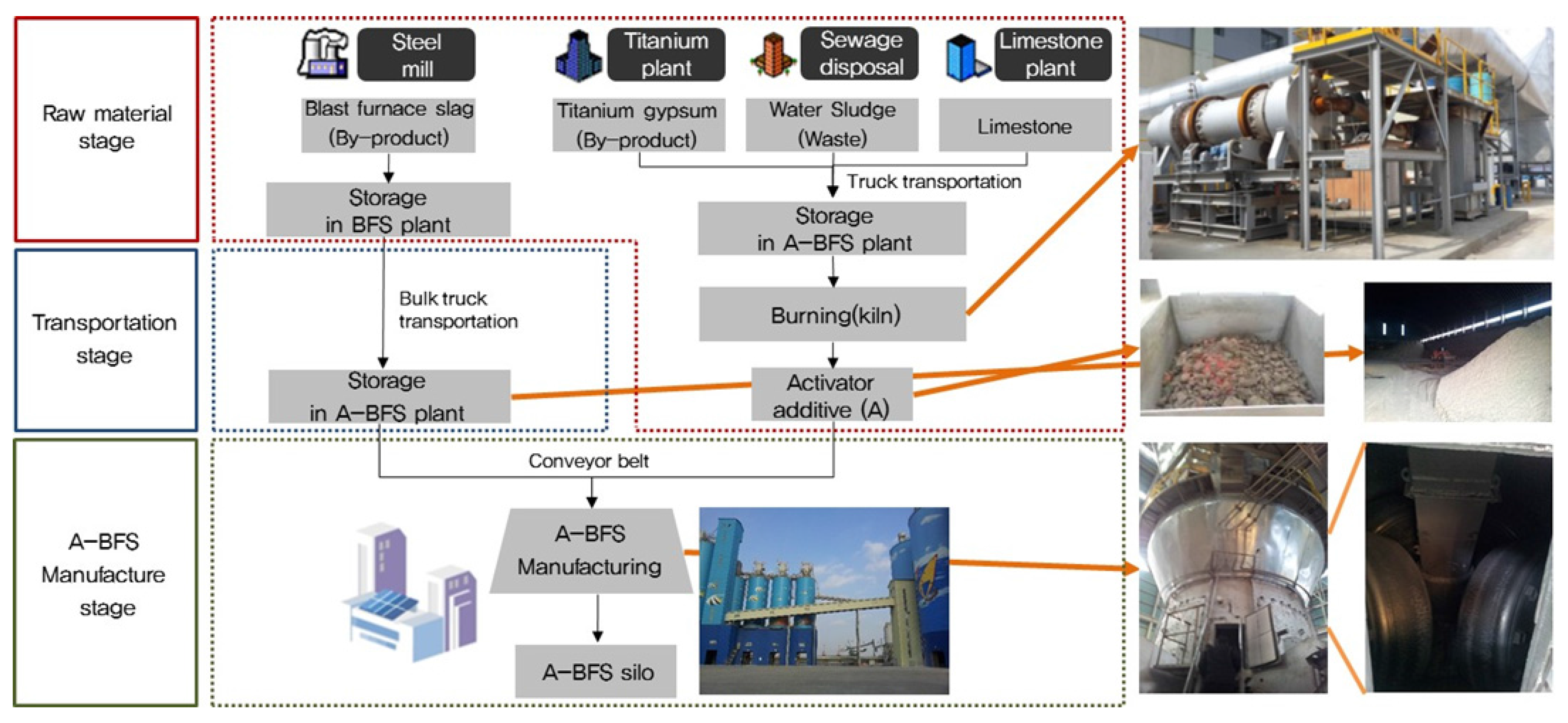

3.2.3. A-BFS Manufacturing Process

The detailed manufacturing process of A-BFS is divided into the raw material stage, transportation stage, and manufacture stage, as shown in Figure 3. The industrial byproduct “BFS” is collected in a steel mill and conveyed to a stockpile. To transport the BFS to the A-BFS factory, it is crushed into small particles (40 mm or smaller) in a crusher. Then, the crushed slag is conveyed and stored in the A-BFS factory. The components of “A” (titanium gypsum, sludge, limestone, etc.) are transported to manufacturers and a sewage treatment plant, and the transported materials are mixed and calcined. The waste additives produced through calcination are conveyed to the A-BFS factory using a conveyor belt. The conveyed BFS and waste additive are weighted and inserted into a large mixer. Then, they are manufactured into A-BFS products after ball-mill crushing and mixing processes.

In this study, a domestic commercial product was used for ordinary Portland cement (hereafter OPC), BFS was taken from what was generated from domestic steel manufacturer K. An industrial byproduct generated from the desulfurization process of a thermoelectric power plant was mixed and used as the activator to induce the hydration reaction of BFS. At this time, for quality management of the industrial byproduct used as the activator, limestone was partially added for ingredient adjustment. Physical/chemical properties of the materials used in this experiment are as shown in Table 4 [46].

As for aggregate used in the concrete physical property test, coarse aggregate was 20 mm rubble aggregate, and fine aggregate was wash aggregate.

The experiment factors and levels for durability evaluation and early-age compression strength of concrete are as shown in Table 5. As for test items and test methods, in order to evaluate flow characteristics, a slump test (KS F 2402) of unhardened concrete and an air content test (KS F 2421) were conducted, specimens were produced in accordance with KS F 2403, and compression strength was measured per age according to KS F 2405 [47,48,49,50].

3.3. Experiment Results

In general, BFS is rapidly cooled down and ground. Therefore, it is widely used in the manufacture of concrete as BFS cement or ground granulated blast-furnace slag (GGBS). Its replacement has been used in 30–50 percentages, considering various factors, such as required performances for concrete. If BFS is used in concrete, it is able to reduce the unit quantity to get the required slump. In addition, the following effects are expected: decrease in hydration heat, increase in water tightness, improvement of long-term strength, inhibition of alkali-aggregate reaction (AAR), and improvement of salt damage resistance and chemical resistance. Compared to Portland cement, in contrast, a decrease in the development of early strength and increase in early drying shrinkage were pointed out. Especially, even though there is a way to increase fineness from 4000 cm2/g to at least 6000 cm2/g to improve early strength through GGBS, this method is not often used in reality because it increases GGBS price up to almost the level of Portland cement.

Table 6 reveals the slump of admixture (early-strength development)-mixed concrete, air content test, compressive strength, and adiabatic temperature rise. Compared to the concrete in which 30% BFS was mixed with OPC, slump slightly increased while an air content level was remained close to the same. The reason why slump increased slightly is because of the smooth fractured surface of BFS and improved bearing effects among aggregates by matrix as lubrication among unhardened concrete particles increase due to boundary lubrication caused by the oxide layer on the surface.

In terms of the slump and air content, A-BFS-mixed concrete was similar to the BFS-mixed concrete. Therefore, it appears that there are almost no or little changes in unhardened concrete properties caused by an activator. According to compressive strength assessment, from 1-day to 28-day ages, it revealed excellent compressive strength compared to the conventional OPC+BFS mixture. In addition, the performances of early-strength development on A-BFS were confirmed.

The SO42 ion in the BFS stimulator is absorbed by the Al2O3 in the BFS and extracted in the vacancy along with the generation of ettringite because the early hydration reaction was accelerated by the eruption of various ions in the network structure. According to an adiabatic temperature rise test, the OPC+BFS combination revealed 35 °C of maximum temperature in the central part. It took 25 h to reach the highest level. It appears that the heat of hydration declined due to a decrease in cement content per unit volume of concrete because of the replacement of GGBFS.

In case of the A-BFS mixture, it took 22 hours to reach the highest temperature in the central region regardless of a replacement ratio, and the temperature ranged from 36.1 to 37.5 °C. In addition, the temperature rise gradient was gentle. In a concrete temperature crack, it would be possible to reduce a concrete temperature crack through A-BFS mixture with the factors influenced by maximum temperature rise and temperature rise gradient. For the removal of forms in general RC structure, at least 5 MPa and 14 MPa are required for wall forms and slab forms, respectively. In this case, they are constructed every six days. If the early-strength development of concrete is enabled, however, they might be constructed every 3–4 days at maximum. This test confirmed that the concrete obtained by mixing the A-BFS made with an addition of an activator with a binder (30%) is equal or greater than OPC in terms of compressive strength. In particular, the reduction of a construction period and effects of construction costs of the RC structure by the A-BFS mix ratio were assessed on the assumption that forms could be removed early with 18.9 MPa of three-day age compressive strength.

4. Economic Analysis of RC Building

4.1. Outline

In this study, subjects of assessment were limited to apartment houses and the economic feasibility of RC buildings applied with A-BFS concrete as a material for early strength expression was assessed after selecting flat type apartment as the most universal form of apartment houses. For assessment, general apartment houses were selected as subjects of assessment, and different cases were defined according to mix ratio of A-BFS for comparison. First, an economic assessment during the construction step was carried out on Case 1 according to the generally-used method of economic assessment. Additionally, as the construction period for each floor of RC building was shortened with improved compressive strength at the early age of Cases 2 and 3, compared to Case 1, the construction reduced cost of the building by the shortened period was computed and reflected on economic assessment of buildings in Cases 2 and 3. Economic assessment according to the construction period was limited to framework construction for the subject building. The elemental cost method and elemental unit quantity method were used for economic assessment during the construction step. Due to improvements of early age compressive strength according to the mix ratio of A-BFS concrete, economic feasibility of each case of RC building with the A-BFS mixture was assessed by analyzing the reduction in the construction period as a site management expense, headquarters management expense, and interest expense.

4.2. Method

4.2.1. Object

The wall column structure which is mostly adopted in the construction of apartments was chosen as the assessment subject. The outline of the subject buildings is described in Table 7. Specifically, they are 24-story buildings (supply dwelling area: 111.33 m2) situated in Seoul. In this assessment, cases were set according to the air-cooled blast furnace slag (A-BFS) concrete mix ratio. As described in Table 8, compared to Case 1, Cases 2 and 3 were 20% and 30%, respectively, in terms of A-BFS concrete mix ratio. Due to the mixture of A-BFS concrete, the number of early aging days increased. Therefore, it was assumed that the construction period for one floor decreased from six days to four and three days.

Even so, a decrease in construction period for each floor from six days to four and three days when the A-BFS mix ratio was 20% and 30%, respectively, is not the result obtained from the actual construction site. It was assumed that it could actually happen in the future. Furthermore, each case’s concrete price was estimated, using the unit prices of concrete raw materials on the KPI (Korea Price Information) [51]. The estimation of concrete cost is shown below:

Cost M is the Cost at the raw material for the production of 1 m3 of concrete (KRW/m3), Unit price M is the cost for each material (KRW/kg), M(i) is the amount of concrete used (kg/m3).

Cost M = ∑(M(i) × Unit price M) (i = 1: cement, 2: aggregate, 3: admixture, 4: water)

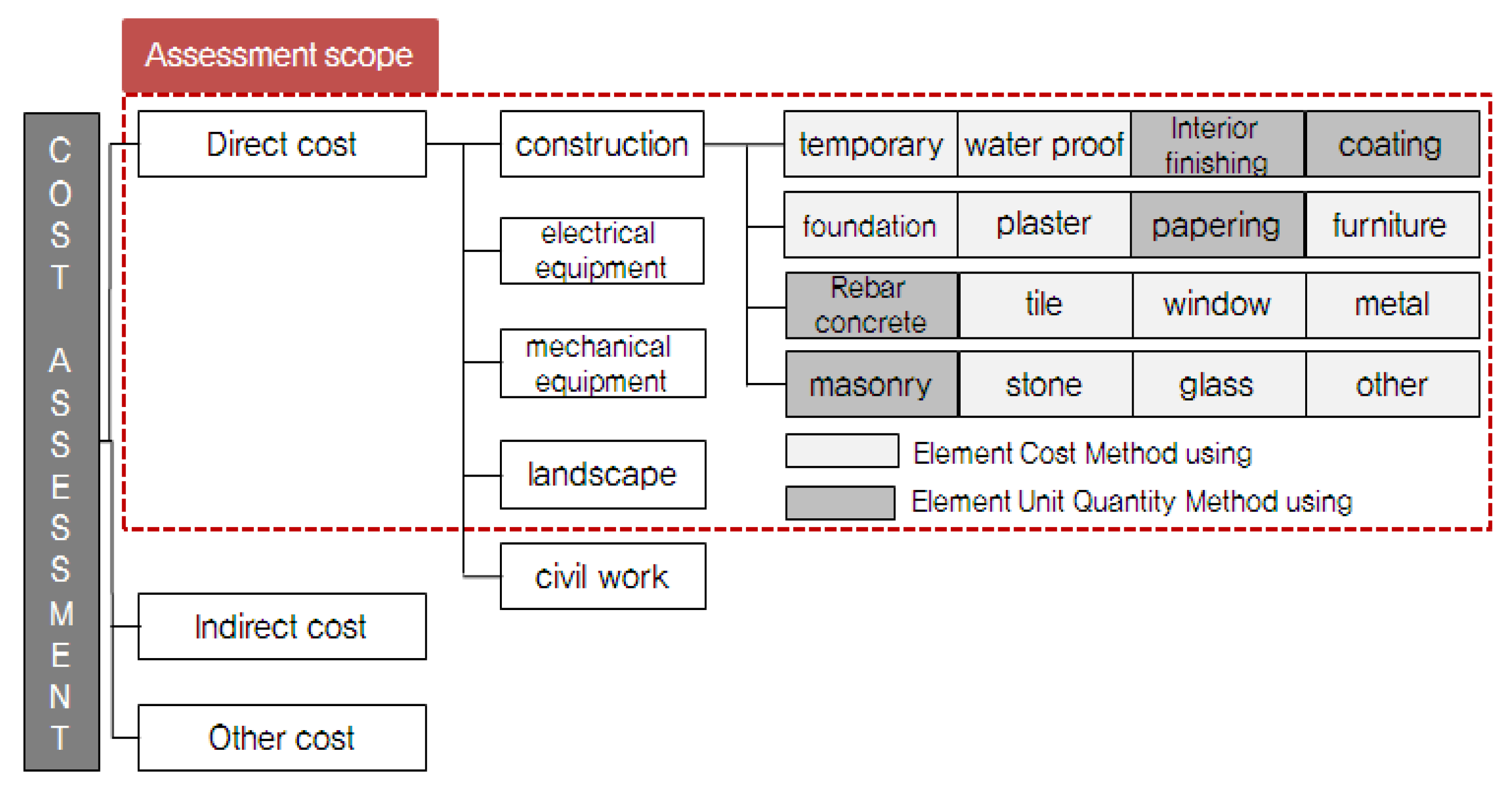

4.2.2. Scope

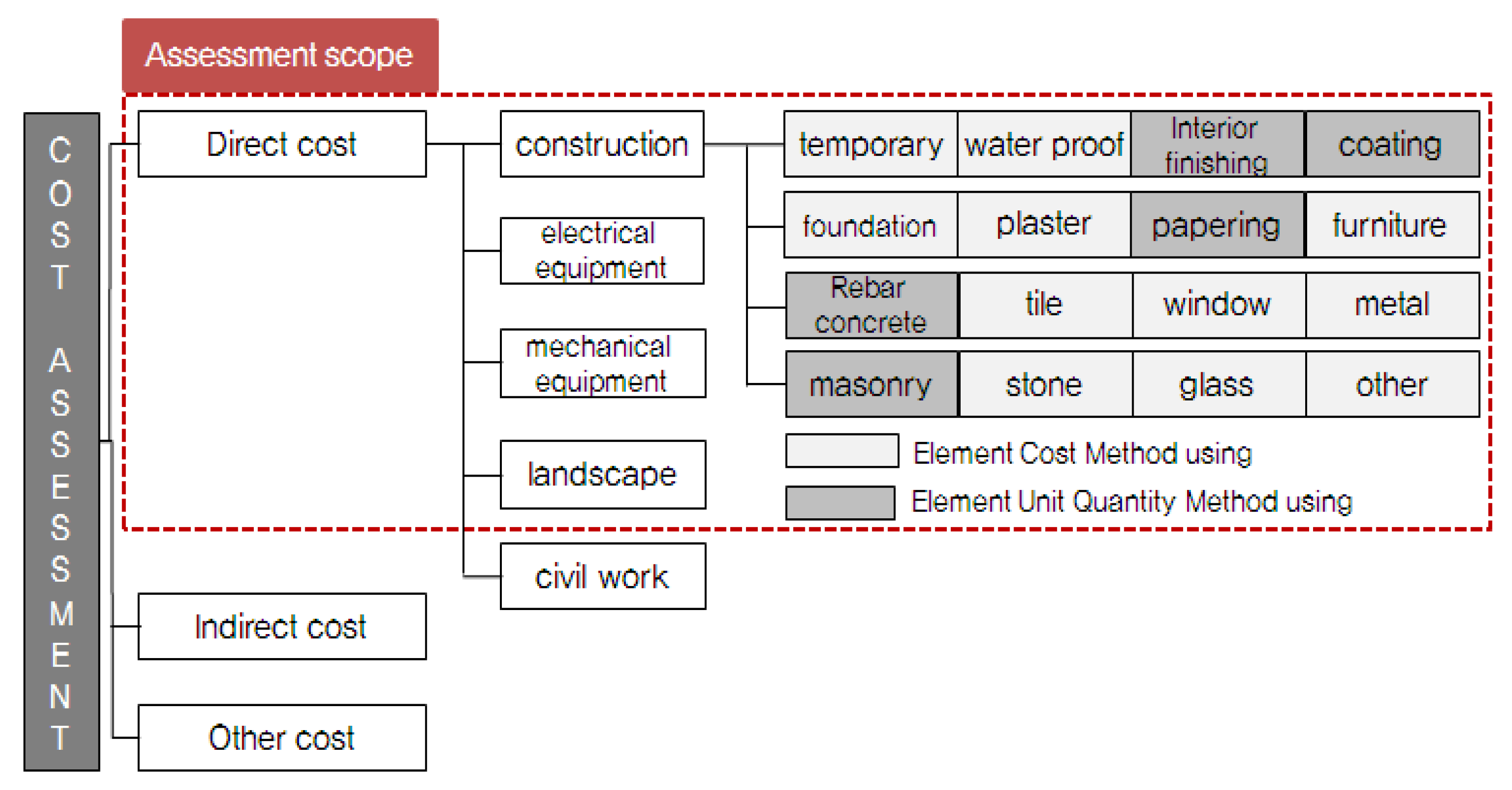

The economic assessment during the construction step on the subject building had a scope as shown in Figure 4. The assessment was only performed on construction work, electrical installation, mechanical work, and landscape construction that correspond to direct construction cost. On one hand, auxiliary engineering work of direct construction, indirect construction cost, and other expenses were excluded. Additionally, among direct construction costs, the economic assessment on construction work was performed separately using the elemental cost method and the elemental unit quantity method for each construction type.

Five construction types (reinforced concrete, masonry work, interior finishing work, papering work, and painting work) used the elemental unit quantity method on major construction types to compute the required cost by multiplying the quantity of each material with the unit cost. For 14 other constructions (temporary work, foundation/designated work, waterproofing work, plaster work, tile work, stone work, window work, glass work, furniture work, metal work, and miscellaneous work), the elemental cost method of assessing the economic feasibility using the construction cost per unit area based on total floor area was also used [52,53].

4.2.3. Direct Cost Evaluation of Construction

Economic feasibility during the construction step was assessed using the elemental cost method and elemental unit quantity method described earlier. Design documents were prepared for major construction types to compute cost by quantity, and historical cost data of similar construction types were utilized for remaining construction types to compute the construction cost per unit area [54,55]. This was multiplied by total floor area to calculate the required cost. The method of assessing economic feasibility using actual construction costs of similar constructions is a method widely used in developed nations, such as the United States and Japan [56,57]. Since this method is acknowledged for the reliability of the result, this method was paralleled in this assessment. On one hand, since the cost of construction work is affected by the construction period, the assessment result on the construction period must be reflected for an accurate economic assessment [58,59]. As the criteria for fluctuations in the construction cost according to change in the construction period should be established, analysis on the overall construction period was performed for a more rational economic assessment. After deducing processes that correspond to the critical path affecting the overall construction period, the result was simulated using a process table composed of the deduced processes and process management software called P3 (Primavera Project Planner, Oracle corporation, CA, USA). Construction work is characterized by slight differences in the construction cost shown by similar projects because each project has different construction methods, materials applied, and productivity of labor. Accordingly, it is necessary to precisely establish conditions of cost computation and assumptions prior to computation of construction costs [60].

(1) First, only direct construction cost of one apartment building with 25 floors and 4-unit combinations was computed as the subject building.

(2) Second, the elemental cost method and the elemental unit quantity method were paralleled as methods for computation of the construction cost. Reinforced concrete construction, masonry work, interior finishing work, papering work, and painting work were computed by unit cost after computation of quantity. Other construction types applied arithmetic means of prices from three similar constructions. However, if the time of computation of the construction cost was in the past, the price inflation rate was reflected using the “construction cost index” announced by the Korea Institute of Construction Technology.

(3) Third, the construction cost of the subject building was assessed using the result shown in Table 9 computed with a structural analysis programs in Korea called MIDAS [61] and BIM (Building Information Method) [62]. The quality of the structure was calculated using the structure analysis program MIDAS ADS [63]. In terms of structural analysis, the quantity of the subject buildings (apartments) was calculated, and the same quality was applied to all cases (Cases 1–4). After reviewing the structure of the subject building’s structure and deriving a member size, the quality of concrete, reinforcing rod, and forms was estimated through MIDAS. Based on the member size and architectural drawings derived through structural analysis, the subject buildings (apartments) were BIM-modeled, using ArchiCAD software. Then, the finished floor area and material quantity of the subject buildings (apartments) were derived based on the BIM modeling and the quantity of the structure. After applying the breakdown costs, then, the quality of a total of 81 different materials was calculated. After that, gypsum board walls were classified into the finished floor area estimate using the BIM model, partition walls, inner walls, and ceiling finishing. Then, the area of the walls (m2) made of the following materials was calculated: general gypsum board (12.5 T), finish material gypsum board (9.5 T), and ceiling gypsum board (9.5 T) [64,65].

To estimate the consumption of gypsum board, wall construction was applied for each part. Then, the quantity of the materials associated with the consumption of gypsum board was estimated, using breakdown costs.

After summarizing the quantity of the said structure, finish materials, and gypsum boards, the consumption of major construction materials used for the subject buildings (apartments) was estimated as stated in Table 9.

Direct construction costs during the construction step were computed using the computation result of the quantity of the subject building by applying the unit price from standard estimation, with the elemental unit quantity method applied for reinforced concrete work, masonry work, interior finishing work, papering work, and painting work. For other construction types, such as temporary work, foundation and designated works, waterproofing work, plaster work, tile work, stone work, window work, glass work, furniture work, metal work, and miscellaneous work, the elemental cost method was used to compute costs by converting actual cost data of similar constructions [66]. Table 10 shows an example that applied the quantity of the subject building using the elemental unit quantity method.

For example, detailed construction costs for reinforced work is computed as follows. First, unit construction cost was analyzed by classifying into material cost, labor cost, and other expenses. Material cost is the price of major materials, such as reinforcing bar and binding wire. Labor cost is the cost for working forces, such as reinforcing bar placers and general workers [67]. Other expenses include rent fees for tools and others. Using such a method, unit costs corresponding to the quantity of each construction was analyzed to compute the construction cost for reinforced concrete work, masonry work, interior finishing work, papering work, and painting work using the same method [68]. In this assessment, among direct construction costs during the construction step, quantity computation for each material was performed for reinforced concrete work, masonry work, interior finishing work, papering work, and painting work. The elemental unit quantity method which computes required costs by multiplying the quantity with unit costs was used to draw conclusions.

Based on such conclusions, using the quantity and the supplied area of the subject building composed of a concrete wall structures with 108 m2, four-unit combinations, and 25 floors, items of direct construction costs for each case were computed. For easier comparison on direct construction costs with the overall costs of each construction type, direct construction costs were computed as per unit area (KRW/m2). As the result of the assessment, overall costs and cost per unit area of reinforced concrete work were found to be 1,386,821,005 KRW (Case 1), 1,361,091,055 KRW (Case 2), and 1,348,285,055 KRW (Case 3), and 163,251 KRW/m2 (Case 1), 160,222 KRW/m2 (Case 2), and 158,715 KRW/m2 (Case 3), respectively.

The overall cost and cost per area were 47,068,598 and 5541 (KRW/m2) for masonry work, 332,193,765 and 39,105 (KRW/m2) for interior finishing work, 97,276,846 and 11,451 (KRW/m2) for papering work, and 43,749,846 and 5150 (KRW/m2) for painting work [69].

First, for computation of the unit price per area from actual data from similar constructions, the mean construction cost for each construction type of an apartment house with the similar size by four companies was applied. A cost assessment by construction type was deduced based on the supplied area of the subject building and actual data of similar constructions by four companies. As in the elemental unit quantity method, cost was computed as the overall construction cost and cost per unit area (KRW/m2) of each construction type [70]. Additionally, for electrical installation work, mechanical work, and landscape work that belong to the scope of this assessment, the elemental cost method was used as described above to perform the economic assessment on the building based on data from construction companies by applying the total floor area of the subject building. Using data from four companies, the construction cost per unit area of each construction type was multiplied by total floor area of the subject apartment to compute the cost for temporary work, foundation and designated works, waterproofing work, plaster work, tile work, stone work, window work, glass work, furniture work, metal work, miscellaneous work, electric work, and facility work. Costs for direct construction during the construction process was deduced [71]. The overall direct construction cost of the subject building was 5,375,441,169 KRW (Case 1), 5,349,711,219 KRW (Case 2), 5,336,905,219 KRW (Case 3), and the cost per unit area was 632,776 KRW/m2 (Case 1), 629,748 KRW/m2 (Case 2), and 628,240 KRW/m2 (Case 3), as shown in Table 11 [72].

4.2.4. Cost Saving Due to Reduced Construction Period

Since construction cost is influenced by the increase and decrease in construction period, accurate economic analysis requires a reflection of changes in the construction period [73]. In this assessment, the amount of change in the construction period for each case of the subject building was assessed according to a shortening by the use of A-BFS concrete.

Conditions of the construction period were configured as follows.

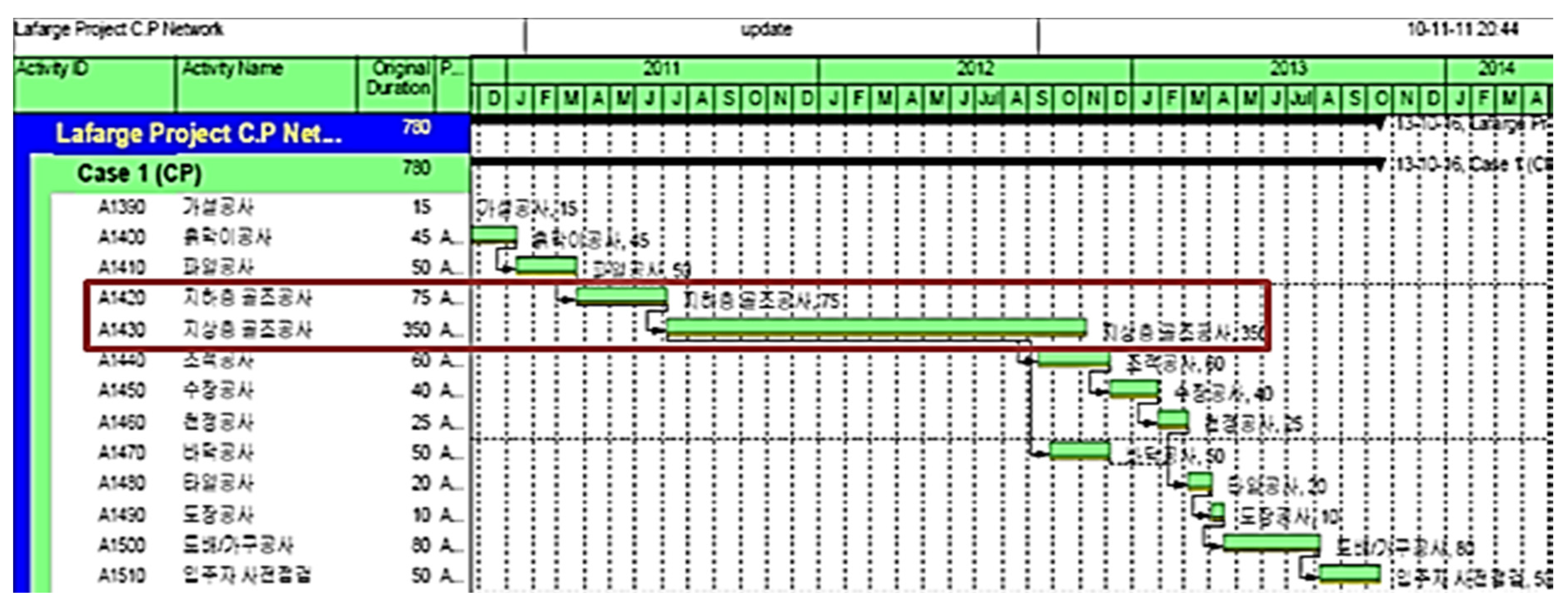

First, a single apartment building with 25 floors and four-unit combination was used, and only critical activity was taken into consideration. Critical activity refers to the longest path in the process table that determines the overall construction period. Additionally, for the number of days used in the process, working days, excluding holidays and non-working, days were used.

As early-age days of each case was shortened according to the ratio of A-BFS concrete, the construction period for one floor was assumed as six days for the standard building in Case 1, four days for Case 2 that applied 20% A-BFS concrete, and three days for Case 3 that applied 30% A-BFS concrete.

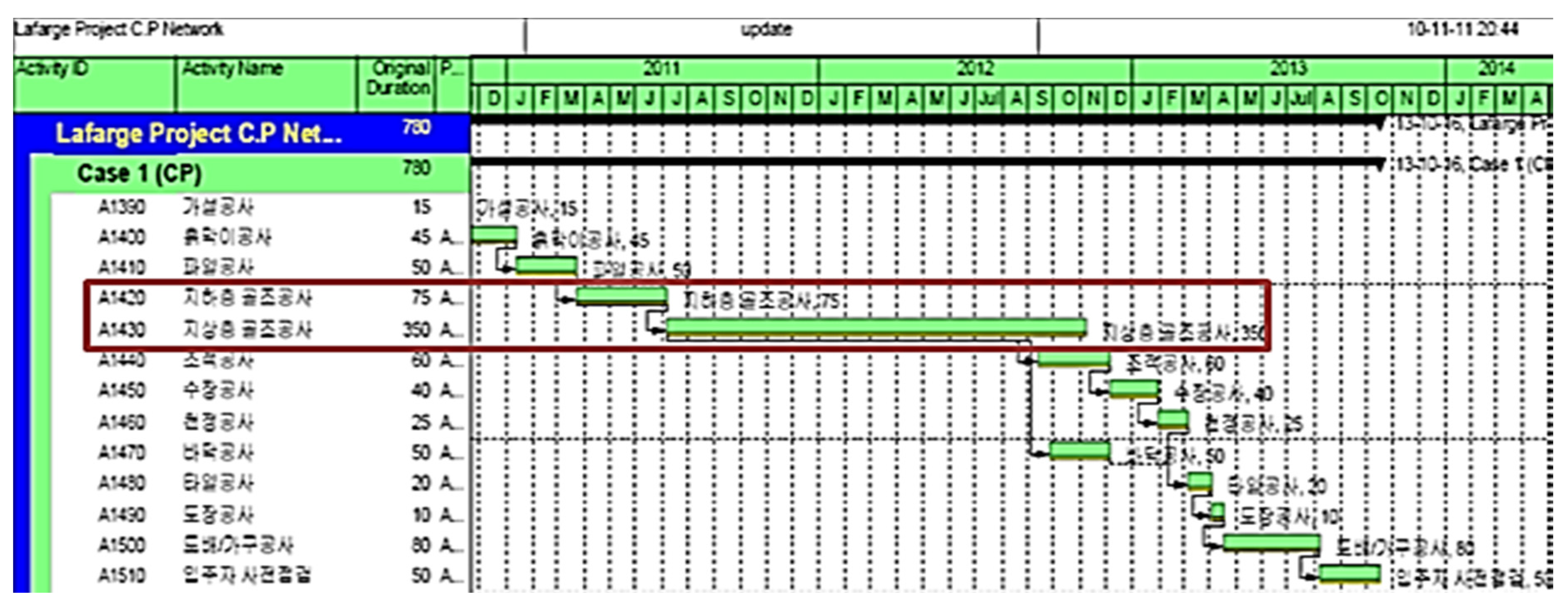

Processes that correspond to the critical path influencing the overall construction period were deduced. Based on this, the construction period of each construction type was assessed using process management software called P3 (Primavera Project Planner). In this assessment, the increase and decrease in the construction period of Case 1 were evaluated as shown in Figure 5.

Table 12 shows the shortening of construction period for each case [74]. Compared to Case 1, Cases 2 and 3, respectively, showed shortening of the construction period by 142 days (4.7 months) and 213 days (7.1 months). This is probably because the construction period for one floor was assumed from six days to four days and three days along with increased compressive strength at an early age.

The analysis results on the construction period were converted to costs and reflected in the economic assessment [75].

The parts of construction cost that showed quantitative reduction with a shortening of the construction period were general management expense, headquarters management expense, and interest expense. General management expense is an expense spent for the operation and management of the construction site, which includes labor costs for dispatched employees and on-site expenses, and this item increases proportionally to construction period.

Headquarters management expense can be described as the headquarters operation expense that encompasses expenses supported by the headquarters at the site. Usually, the general management expense is within 5%–6% of the overall construction cost. Headquarters management expense is determined according to the number of projects being carried out by the construction company [76].

In general, construction companies compute that the sum of the headquarters management expenses for all projects in progress as about 10%. Headquarters management expense is approximated by 1/n according to the number of projects. In the case of interest expense, almost no interest expense occurs with contracted constructions in general, but interest expense from borrowing of construction costs does occur in the case of self-construction by the company [77].

As a result of analyzing the cash flow of four apartments built as self-constructions and computing the interest expense with consideration on the loan and a recent interest rate of 15%, the interest expense, on average, was found to be about 3.06% of the overall construction cost. The amount of cost reduced by a shortened construction period was computed based on such results, and the result is shown in Table 9.

The construction cost for an apartment building with 25 floors and four-unit combinations was assumed as 6.2 billion won, and the construction period was assumed as 28 months. Economic effects from shortening by 4.7 months in Case 2 compared to Case 1 was about 106,654,762 KRW, and the effect from shortening by 7.1 months in Case 3 was about 159,982,143 KRW as shown in Table 13.

4.3. Result

The result of the cost assessment on the building that applied A-BFS, a mixture for early strength expression, is as shown in Table 14. Overall construction costs for each case of the subject apartment building during construction step was deduced as 5,375,411,169 KRW. This was identical for Cases 2 and 3 compared to Case 1, because there was no change in the price of concrete material despite the change in the mix ratio of A-BFS.

On one hand, the construction period of the building was changed by a change in the early age compressive strength of concrete due to the mixture of A-BFS.

This was reflected in the economic assessment of the building. As a result of reflecting fluctuations in the construction period, Case 2 showed a reduction effect of about 106,654,762 KRW, and Case 3 showed an effect of about 159,982,143 KRW compared to Case 1.

That is, the cost per unit area after deduction of the reduced amount was 632,777 (KRW/m2) for Cases 1, 617,193 (KRW/m2) for Case 2, and 609,408 (KRW/m2) for Case 3.

This was evaluated as a reduction of 2.5% for Case 2 and 3.7% for Case 3 compared to Case 1.

5. Conclusions

In this study, after reviewing the aspect of early strength expression by A-BFS, the effect of a shortened construction period and construction cost reduction according to early removal of forms by application of A-BFS concrete in RC building structure was assessed to obtain the following conclusion.

A-BFS mixed concrete had a tendency to slightly increase the slump value with a mixture of A-BFS. As a result of measuring compressive strength, higher expression of compressive strength was shown at an early age with a mixture of A-BFS, compared to a plain mix.

As a result of the cost saving assessment on a building that applied A-BFS concrete, overall construction costs for each case were found to be 5,375,411,169 KRW (Case 1), 5,268,786,407 KRW (Case 2), and 5,215,459,026 KRW (Case 3). This is because there was a change in concrete price and construction period for each case, according to the difference in the mix ratio of A-BFS for Cases 2 and 3, compared to Case 1.

As a result of the cost saving assessment on the shortening of the construction period, Cases 2 and 3 showed reductions of about 106,654,762 KRW and 159,982,143 KRW, respectively. Additionally, as a result of the cost saving assessment on the reduction of concrete price, Cases 2 and 3 showed reductions of about 25,729,950 KRW and 38,535,950 KRW, respectively.

The cost per unit area after the deduction of the reduced amount was evaluated as 632,777 (KRW/m2) for Case 1, 617,193 (KRW/m2) for Case 2, and 609,408 (KRW/m2) for Case 3. This was a reduction of 2.5% for Case 2 and 3.7% for Case 3, compared to Case 1.

Acknowledgments

This research was supported by a grant (Code 11-Technology Innovation-F04) from Construction Technology Research Program (CTIP) funded by Ministry of Land, Infrastructure and Transport.

Conflicts of Interest

The author declares no conflict of interest.

References

- Architectural Institute of Korea (Aik). Building Construction Standard; Kimoondang Publishing Company: Seoul, Korea, 2013. [Google Scholar]

- Kirk, S.J. Life Cycle Costing for Design Professionals; McGraw-Hill Inc.: New York, NY, USA, 1982. [Google Scholar]

- Korea Institute of Civil Engineering and Building Technology. Standard of Construction Estimate; Construction Association of Korea (CAK): Seoul, Korea, 2015. [Google Scholar]

- Yun, S.H.; Cho, H.H.; Tae, Y.H.; Ahn, B.R.; An, S.H.; Huh, Y.K. Productivity analysis of steel works for cost estimation of public projects in Korea. KSCE J. Civil Eng. 2012, 16, 1–7. [Google Scholar] [CrossRef]

- Kenji, K. Simulation and Evaluation for the Basic Work-floor in High-rise Building Construction; Architectural Institute of Japan (AIJ): Tokyo, Japan, 2001. [Google Scholar]

- Chien, Y.F. A Study of Simulation on Production Planning and Control–No.5, Work Process Planning Using Overtime Work; Architectural Institute of Japan: Tokyo, Japan, 2003. [Google Scholar]

- Park, W.Y. Expense Management of Owner and Condition Investment of Cost Performance Advantage; Construction Economy Research Institute of Korea: Seoul, Korea, 2006. [Google Scholar]

- Barrie, D.S.; Plaulson, B.C. Professional Construction Management, 3rd ed.; McGraw-Hill Inc.: New York, NY, USA, 2002. [Google Scholar]

- Kim, M.H. The Plan of Construction Cost; Kimoondang Publishing Company: Seoul, Korea, 2005. [Google Scholar]

- Im, J.I. IFC test between commercial 3D CAD application using IFC. Korea J. Constr. Eng. Manag. 2008, 9, 85–94. [Google Scholar]

- Kim, K.D. Study on the Rational Cost Model of Apartment House in the Incipient Planning Stage. Archit. Inst. Korea 1990, 29, 291–298. [Google Scholar]

- An, S.H.; Park, W.Y.; Kang, K.I. Study on the process about apartment payments with an actual cost ratio of a work performed. Archit. Inst. Korea 2002, 18, 125–132. [Google Scholar]

- Cho, H.H.; Lee, Y.S. Development and use of building construction cost index. Korea J. Constr. Eng. Manag. 2004, 5, 10–13. [Google Scholar]

- Kim, K.H.; Kang, K.I. Comparing Accuracy of Prediction Cost Estimation Using Case-Based Reasoning and Neural Networks. Archit. Inst. Korea 2004, 20, 93–105. [Google Scholar]

- Kim, D.S. Parametric Cost Estimation of Apartment Housing Based on Actual Cost Analysis. Master’s Thesis, Korea University, Seoul, Korea, 2009. [Google Scholar]

- Kwon, H.S. Cost prediction model of Public Multi-housing Projects in Schematic Design Phase. Korea J. Constr. Eng. Manag. 2008, 9, 1–10. [Google Scholar]

- Lim, S.Y. A Study on Improving the Estimation Accuracy of Apartment Project Cost. Master’s Thesis, Chon-nam University, Gwangju, Korea, 2010. [Google Scholar]

- Oberlender, G.; Trost, S. Predicting Accuracy of Early Cost Estimates Based on Estimate Quality. J. Constr. Eng. Manag. 2001, 127, 173–182. [Google Scholar] [CrossRef]

- Trost, S.; Oberlender, G. Predicting Accuracy of Early Cost Estimates Using Factor Analysis and Multivariate Regression. J. Constr. Eng. Manag. 2003, 123, 198–204. [Google Scholar] [CrossRef]

- Karshenas, S.; Tse, J. A case-based reasoning approach to construction cost estimating. In Proceedings of the Congress on Computing in Civil Engineering, Washington, DC, USA, 3–7 November 2002; p. 113.

- Attalla, M.; Hegazy, T. Predicting Cost Deviation in Reconstruction Projects: Artificial Neural Networks versus Regression. J. Constr. Eng. Manag. 2003, 129, 405–411. [Google Scholar] [CrossRef]

- Soutos, M.; Lowe, D.J. ProCost-Towards a Powerful Early Stage Cost Estimating Tool. J. Constr. Eng. Manag. 2005, 179, 1–12. [Google Scholar]

- Lowe, D.; Emsley, M.; Harding, A. Predicting Construction Cost Using Multiple Regression Techniques. J. Constr. Eng. Manag. 2006, 132, 750–758. [Google Scholar] [CrossRef]

- Dogan, S.; Arditi, D.; Gunaydin, H. Determining Attribute Weights in a CBR Model for Early Cost Prediction of Structural Systems. J. Constr. Eng. Manag. 2006, 132, 1092–1098. [Google Scholar] [CrossRef]

- Marmol, I.; Ballester, P.; Cerro, S.; Monros, G.; Morales, J.; Sanchez, L. Use of granite sludge wastes for the production of coloured cement-based mortars. Cem. Concr. Compos. 2010, 32, 617–622. [Google Scholar] [CrossRef]

- Skaropoulou, A.; Sotiriadis, K.; Kakali, G.; Tsivilis, S. Use of mineral admixtures to improve the resistance of limestone cement concrete against thaumasite form of sulfate attack. Cem. Concr. Compos. 2013, 37, 267–275. [Google Scholar] [CrossRef]

- Moon, H.Y.; Choi, H.W.; Kim, Y.J. Estimation of Strength of Ground Granulated Blast Furnace Slag Mix Concrete Using Hydrothermal Curing Method. Korea Concr. Inst. J. 2004, 16, 102–110. [Google Scholar]

- Kritsada, S.; Lutz, F. Carbonation rates of concretes containing high volume of pozzolanic materials. Cem. Concr. Res. 2007, 37, 1647–1653. [Google Scholar]

- Sabbie, A.M.; Monteiro, P.J.M. Greenhouse gas emissions from concrete can be reduced by using mix proportions, geometric aspects, and age as design factors. Environ. Res. Lett. 2015, 10. [Google Scholar] [CrossRef]

- Tatiana, G.S.; Víctor, Y.; Julián, A. Life cycle greenhouse gas emissions of blended cement concrete including carbonation and durability. Int. J. Life Cycle Assess. 2013, 19, 3–12. [Google Scholar]

- Han, M.C.; Park, S.J.; Kim, K.M.; Choi, S.Y. Estimation of Removal Time of Side Form of the Concrete Incorporating Fine Particle Cement. Archit. Inst. Korea 2009, 25, 121–128. [Google Scholar]

- Han, C.G.; Han, M.C. Determination of Removal Time of Side Forms Based on the Strength Development of Concrete. Archit. Inst. Korea 2001, 152, 87–943. [Google Scholar]

- Kim, K.M. Practical Application of High Early Strength Type Concrete Using High Early Strength Type Binder. Available online: http://www.dbpia.co.kr/Journal/ArticleDetail/NODE01312501?TotalCount=0&Seq=4&Collection=0&Page=0&PageSize=0&isFullText=0&isIdentifyAuthor=1 (accessed on 4 April 2016).

- So, K.H.; Kim, K.M. Study on the Practical Application of High Early Strength Type Concrete Using Fine Particle Cement. Available online: http://www.nl.go.kr/nl/search/bookdetail/online.jsp?contents_id=CNTS-00030490224 (accessed on 4 April 2016).

- Noh, S.K. A Fundermental Properties of the Concrete depending on the Liquid Type High Early Strength Agent. Available online: http://www.nl.go.kr/nl/search/bookdetail/online.jsp?contents_id=CNTS-00030616284 (accessed on 4 April 2016).

- Lee, M.H.; Song, Y.C. Effect of Ingredients of Liquid Accelerating Agent on Cement Mortar. Archit. Inst. Korea. Available online: http://www.nl.go.kr/nl/search/bookdetail/online.jsp?contents_id=CNTS-00030480657 (accessed on 4 April 2016).

- Jeon, H.K.; Ji, S.W.; Seo, C.H. Study on the Characteristics of Concrete Using AE Water Reducing Agents of Early-strength Type. Available online: http://www.nl.go.kr/nl/search/bookdetail/online.jsp?contents_id=CNTS-00030521298 (accessed on 4 April 2016).

- Song, Y.C.; Sa, S.H.; Ji, S.W.; Jeon, H.K.; Seo, C.H. Research on Early-strength Development of Concrete by Accelerating Agents. Available online: http://www.nl.go.kr/nl/search/bookdetail/online.jsp?contents_id=CNTS-00030597337 (accessed on 4 April 2016).

- Keum, K.H.; Lee, W.A.; Song, Y.C.; Jeong, Y.H.; Kim, Y.R.; Kim, S.M. An Experimental Study on the Development of Early Strength Concrete for Reduction of Working Period in Apartment. Available online: http://www.auric.or.kr/User/Rdoc/DocRdocCP.aspx?returnVal=RD_R&page=1&dn=302965 (accessed on 4 April 2016).

- Kim, K.H.; Hwang, I.S.; Kim, K.M.; Park, S.J.; Han, C.G. Properties of Strength Development of Concrete at Early Age Incorporating Fine Particle Cement and Mineral Powder. Available online: http://www.nl.go.kr/nl/search/bookdetail/online.jsp?contents_id=CNTS-00030616252 (accessed on 4 April 2016).

- Lee, S.H.; Hong, K.S. An Example of Construction Work Period Reduction Using Poly Carboxylate Acid Type Early Strength Concrete. Available online: http://www.auric.or.kr/User/Rdoc/DocRdocCP.aspx?returnVal=RD_R&page=1&dn=302023 (accessed on 22 March 2016).

- Kim, W.Y.; Kim, J.S.; Ha, G.J.; Kim, J.G. Development of Engineered Cementitious Composite (ECC) with Ground Granulated Blast-Furnace Slag. Available online: http://img.kisti.re.kr/originalView/originalView.jsp (accessed on 22 March 2016).

- Hirotaka, M.; Haruki, I.; Emile, H.I. Utilization of calcite and waste glass for preparing construction materials with a low environmental load. J. Environ. Manag. 2011, 92, 2881–2885. [Google Scholar]

- Othmane, B.; El-Hadj, K. Effects of granulated blast furnace slag and super plasticizer type on the fresh properties and compressive strength of self-compacting concrete. Cem. Concr. Compos. 2012, 34, 583–590. [Google Scholar]

- Gazquez, M.J.; Bolivar, J.P.; Vaca, F.; Garcia-Tenorio, R.; Caparros, A. Evaluation of the use of TiO2 industry red gypsum waste in cement production. Cem. Concr. Compos. 2013, 37, 76–81. [Google Scholar] [CrossRef]

- Baek, C.W.; Kim, H.S.; Park, J.B.; Jun, J.Y.; Suh, C.W. Durability of concrete using large amounts of ground granulated blast furnace slag. Korea Concr. Inst. Conf. 2011, 23, 219–220. [Google Scholar]

- Korean Agency for Technology and Standards (KATS). The Test Method of Slump for Concrete; Korea Industrial Standards, Ministry of Trade, Industry and Energy: Sejong-si, Korea, 2015. [Google Scholar]

- Korean Agency for Technology and Standards (KATS). The Test Method of Air Content for Unpacked Concrete; Korea Industrial Standards, Ministry of Trade, Industry and Energy: Sejong-si, Korea, 2015. [Google Scholar]

- Korean Agency for Technology and Standards (KATS). The Manufacturing Method of Specimen for Concrete Strength Test; Korea Industrial Standards, Ministry of Trade, Industry and Energy: Sejong-si, Korea, 2015. [Google Scholar]

- Korean Agency for Technology and Standards (KATS). The Test Method of Compressive Strength for Concrete; Korea Industrial Standards, Ministry of Trade, Industry and Energy: Sejong-si, Korea, 2015. [Google Scholar]

- Wang, H.L.; Li, Y. Analysis on Energy Conservation Materials’ Influence on Energy Saving Construction Cost. Adv. Mater. Res. 2014, 859, 274–279. [Google Scholar] [CrossRef]

- Construction Association of Korea. Comprehensive Construction Cost; Construction Association of Korea: Seoul, Korea, 2010. [Google Scholar]

- Mun, K.J.; So, S.Y.; Soh, Y.S. The effect of slaked lime, anhydrous gypsum and limestone powder on properties of blast furnace slag cement mortar and concrete. Constr. Build. Mater. 2007, 21, 1576–1582. [Google Scholar] [CrossRef]

- Seo, J.O.; Ryu, H.G.; Lee, D.R. Development of Public Office Cost Estimating Framework in Feasibility and Design Stage. Archit. Inst. Korea 2008, 24, 153–160. [Google Scholar]

- Christensen, P.; Sparks, G.; Kostuk, K. A method-based survey of life cycle costing literature pertinent to infrastructure design and renewal. Can. J. Civ. Eng. 2005, 10, 250–259. [Google Scholar] [CrossRef]

- Hastak, M.; Halpin, D. Assessment of Life-Cycle Benefit-Cost of Composites in Construction. J. Compos. Constr. 2000, 4, 103–111. [Google Scholar] [CrossRef]

- Kang, H.W. A Study on the Analysis of Maintenance Costs though the Estimation of Elemental Cost for Educational Buildings. Master’s Thesis, Chung-ang University, Seoul, Korea, 2009. [Google Scholar]

- Designing Buildings Ltd. (limited company). Available online: http://www.designingbuildings.co.uk/wiki/Elemental_cost_plan_for_design_and_construction (accessed on 22 March 2016).

- Jeon, J.Y. A Study on Construction Cost Estimating Method based on Actual Cost Data. Archit. Inst. Korea 2002, 18, 121–128. [Google Scholar]

- Jeon, J.Y. A Study on Computer Algorithm of Proper Construction Cost Estimating Method by Historical Data Analysis. Korea Inst. Constr. Eng. Manag. 2003, 4, 192–200. [Google Scholar]

- MIDAS Information Technology. Available online: http://midasarchi.com/ (accessed on 26 March 2016).

- Lee, S.H. A Basic Study on the Development of an Interface between Revit Architecture and Midas for the Augmented Collaboration of Architectural Design and Structural Analysis at the Early Design Stage. J. Archit. Inst. Korea 2011, 27, 51–59. [Google Scholar]

- Kim, K.J. The Process for Structural Design of Buildings Based 3D Building Information Modeling. Master’s Thesis, Sun-moon University, Asan, Korea, 2009. [Google Scholar]

- Oh, H.O.; Kim, J.H.; Kim, M.S.; Lee, J.H.; Jeong, J.H. Study on the Structure Design Process and Modeling Guidelines Based on BIM. J. Archit. Inst. Korea 2011, 27, 107–114. [Google Scholar]

- Kim, Y.R.; Cho, Y.S. The Study on Application of Korean BIM Process in the Structural Design Phase based on a Case Study. J. Archit. Inst. Korea 2009, 25, 19–26. [Google Scholar]

- Kim, M.K.; Shin, S.H.; Hyun, C.T. A Study on Cost Management at the Pre-construction Phase in the Korean Construction Market. Korean J. Constr. Eng. Manag. 2002, 1, 265–270. [Google Scholar]

- Kevorkijan, V.M. The quality of aluminum dross particles and cost-effective reinforcement for structural aluminum-based composites. Compos. Sci. Technol. 1999, 59, 1745–1751. [Google Scholar] [CrossRef]

- Qingtao, L.; Zhuguo, L.; Guanglin, Y. Effects of elevated temperatures on properties of concrete containing ground granulated blast furnace slag as cementitious material. Constr. Build. Mater. 2012, 35, 687–692. [Google Scholar]

- Narasimhan, H.; Chew, M.Y.L. Integration of durability with structural design: An optimal life cycle cost based design procedure for reinforced concrete structures. J. Archit. Inst. Korea 2009, 23, 918–929. [Google Scholar] [CrossRef]

- Ock, J.H.; Han, S.H. A Study on the Problem Analysis and Improvement Plan Development of the Construction Cost Saving Policy in the Public Educational Facilities Projects. J. Archit. Inst. Korea 2001, 2, 98–106. [Google Scholar]

- Park, C.H.; Abdelghani, S.; Joël, B.; Han, W.S.; Alain, V.; Lee, W.I. An integrated optimisation for the weight, the structural performance and the cost of composite structures. Compos. Sci. Technol. 2009, 69, 1101–1107. [Google Scholar] [CrossRef]

- Bonn, D. Cost-saving construction of quality old people’s facilities Supplement to the Official. J. Eur. Communities 1997, 40, 154–155. [Google Scholar]

- Gardner, R.G. Construction cost savings on a complex landfill closure: The beulah landfill project. Ann. Landfill Symp. 1998, 3, 109–120. [Google Scholar]

- Korea Housing Corporation. Change and Prospect of Apartment Housing Model and Structure System in Korea; Korea Housing Corporation: Seongnam-si, Gyeonggi-Do, Korea, 2005. [Google Scholar]

- Jin, S.Y. A Study on the Direction of Technological Development for Shortening of Framework Construction Time in Korea. Korea Inst. Constr. Eng. Manag. 2009, 9, 145–152. [Google Scholar]

- Claus, R. Service life of building envelope components: making it operational in economical assessment. Constr. Build. Mater. 2002, 16, 83–89. [Google Scholar]

- Chung, S.G.; Choi, Y.K.; Chung, S.G. Study on Construction Cost Saving of Pile Foundation Using Pile Load Test for Design. Korean Soc. Civil Eng. 1998, 18, 341–352. [Google Scholar]

Figure 1.

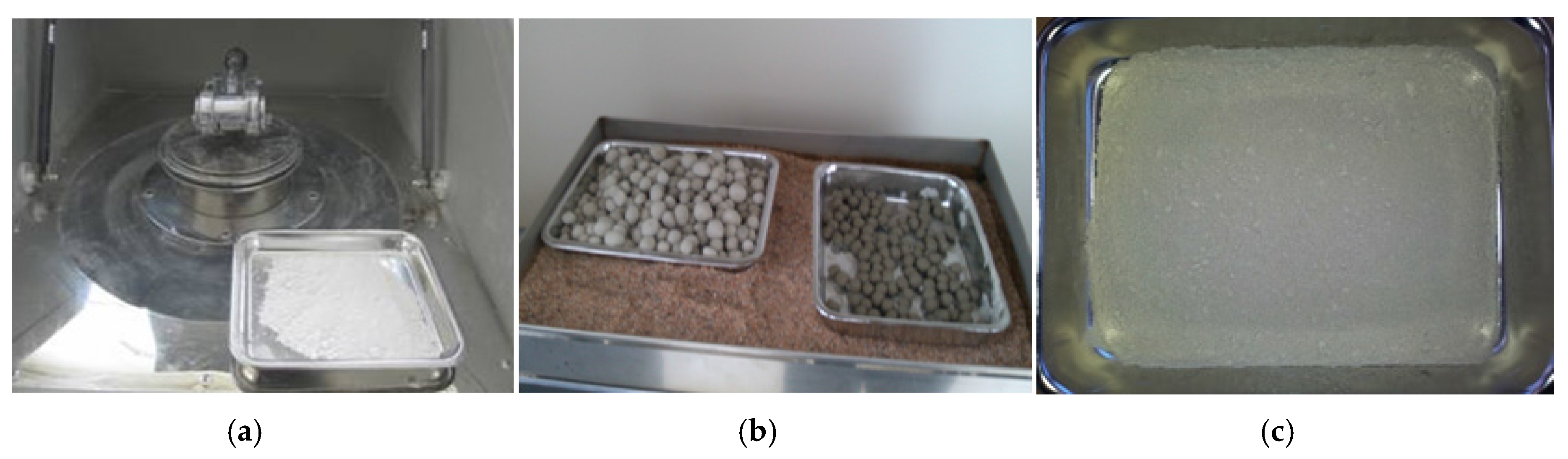

Composition material of A-BFS. (a) Blast Furnace Slag (BFS); (b) activator additive (A); and (c) A-BFS.

Figure 1.

Composition material of A-BFS. (a) Blast Furnace Slag (BFS); (b) activator additive (A); and (c) A-BFS.

Figure 2.

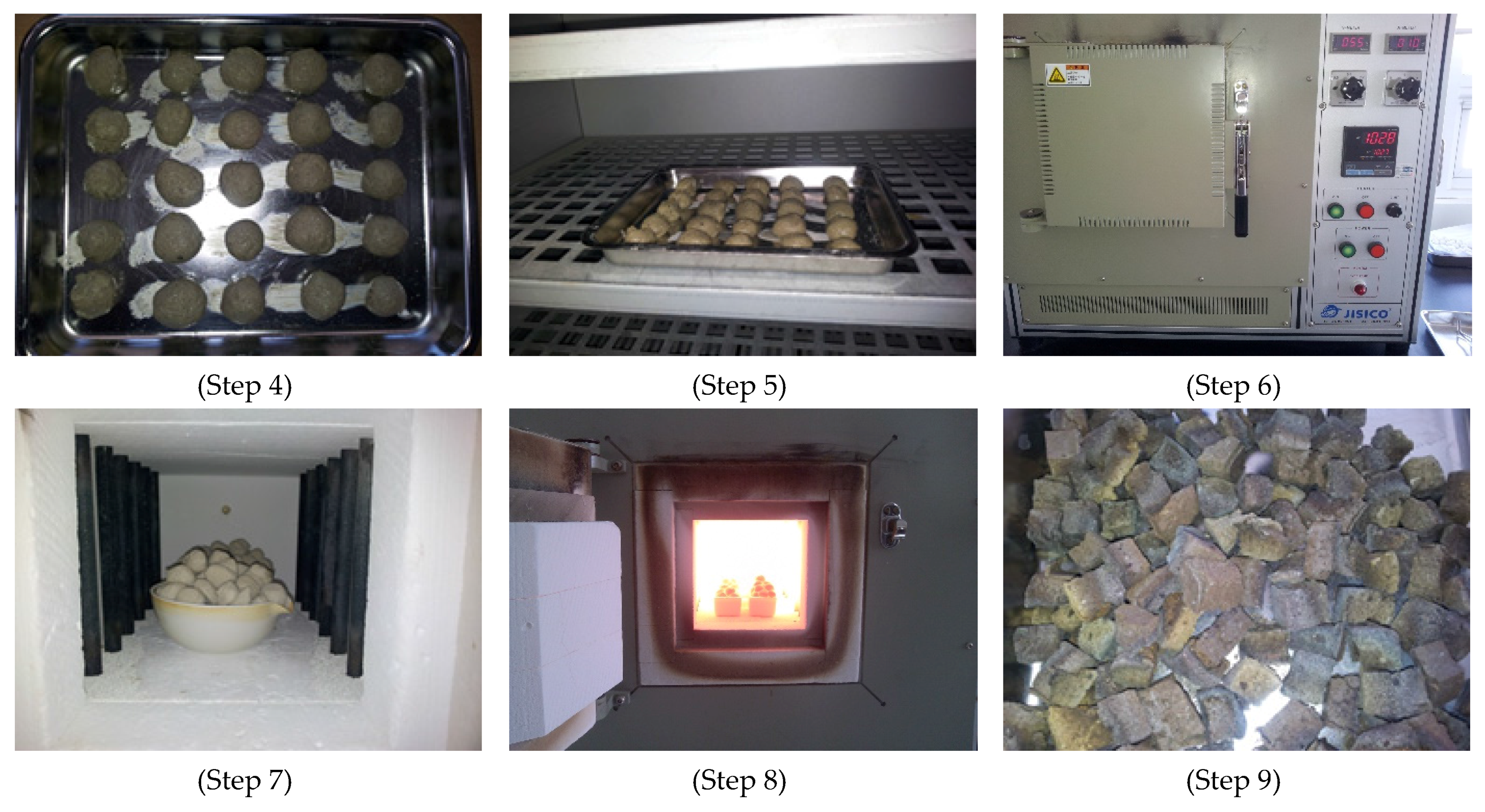

Titanium gypsum (a); sludge (b); limestone (c) of activator addictive composition material. Dry (composition material a + b + c) in dryer (100°C) (step 1); Crushed(mixed a, b, c) (step 2); Mixing with water (Step 3); Making a circle shape (Step 4); Dry in dryer(100°C) (step 5); Simple kilns (step 6); Input in the simple kilns (step 7); Fired (600 °C~1350 °C) (step 8); After firing and hardening (step 9) of activator addictive manufacturing process.

Figure 2.

Titanium gypsum (a); sludge (b); limestone (c) of activator addictive composition material. Dry (composition material a + b + c) in dryer (100°C) (step 1); Crushed(mixed a, b, c) (step 2); Mixing with water (Step 3); Making a circle shape (Step 4); Dry in dryer(100°C) (step 5); Simple kilns (step 6); Input in the simple kilns (step 7); Fired (600 °C~1350 °C) (step 8); After firing and hardening (step 9) of activator addictive manufacturing process.

Figure 3.

Production process of A-BFS.

Figure 4.

Scope of cost assessment in the construction process

Figure 5.

Evaluation example of the construction period.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| NO. | Researcher | Method |

|---|---|---|

| 1 | Kim et al. (1990) [11] | Regression Analysis |

| 2 | An et al. (2002) [12] | Regression Analysis, Artificial Neural Networks |

| 4 | Cho et al. (2003) [13] | Regression Analysis |

| 5 | Kim et al. (2004) [14] | Regression Analysis, Artificial Neural Networks, Genetic Algorithms, Inference of Case-based |

| 9 | Kim et al.(2009) [15] | Regression Analysis |

| 10 | Kwon et al. (2008) [16] | Regression Analysis |

| 11 | Lim et al.(2010) [17] | Inference of Case-based |

| 13 | Oberlender et al. (2001) [18] | Regression Analysis |

| 14 | Trost et al. (2003) [19] | Inference of Case-based |

| 15 | Karshenas et al. (2002) [20] | Element analysis and Regression Analysis |

| 16 | Attalla et al. (2003) [21] | Regression Analysis |

| 18 | Soutos et al. (2005) [22] | Bpn/T and E, NNS/GAs |

| 19 | Lowe et al. (2006) [23] | Linear regression models |

| 20 | Dogan et al. (2006) [24] | Artificial Neural Networks |

| NO. | Researcher | Estimating Variable |

|---|---|---|

| 1 | Kim et al. (1990) [11] | Period, gross area and structure type, etc. 10 categories |

| 2 | Kim et al. (2004) [14] | Area, stories and households, etc. 10 categories |

| 3 | Lim et al. (2010) [17] | Based type, roof type, gross area and land area, etc. 15 categories |

| Material | Chemical Composition (%) | Total (%) | Gravity | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| SiO2 | Al2O3 | Fe2O3 | CaO | MgO | SO3 | K2O | TiO2 | P2O5 | ||||

| Blast furnace slag | 34.76 | 14.50 | 0.48 | 41.71 | 6.87 | 0.13 | 0.44 | 0.62 | 0.03 | 99.54 | - | |

| Activator additive (Before burning) | Titanium gypsum | 1.49 | 0.54 | 0.80 | 35.83 | 0.44 | 51.23 | 0.09 | 1.55 | 0.02 | 91.9 | 2.62 |

| Sludge | 34.97 | 27.34 | 4.44 | 0.79 | 1.14 | 1.07 | 1.77 | 0.47 | 0.73 | 72.72 | 1.84 | |

| Limestone | 0.5 | 0.3 | 0.2 | 96.7 | 1.9 | 0.1 | 0.0 | 0.0 | 0.0 | 99.7 | 2.76 | |

| Item Type | Oxide Composition (%) | Blaine (g/cm2) | Specific Gravity | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| SiO2 | Al2O3 | CaO | Fe2O3 | MgO | Na2O | K2O | P2O5 | TiO2 | SO3 | |||

| OPC | 24.48 | 5.01 | 61.97 | 3.19 | 2.94 | 0.12 | 0.89 | 0.03 | 0.10 | 2.24 | 3470 | 3.15 |

| BFS | 34.76 | 14.50 | 41.71 | 0.48 | 6.87 | 0.14 | 0.44 | 0.03 | 0.62 | 0.13 | 4600 | 2.91 |

| Activator additive | 9.35 | 13.92 | 44.40 | 1.29 | 1.64 | 0.08 | 0.28 | 0.35 | 0.79 | 27.40 | - | - |

| Type | W/B (%) | S/a (%) | Unit Weight (kg/m3) | AE | ||||||

|---|---|---|---|---|---|---|---|---|---|---|

| W | C | BFS | A-BFS (BFS: Activator) | S | G | |||||

| 1 | OPC+BFS (30%) | 49.4 | 48.0 | 168 | 238 | 102 | - | 856 | 935 | 1% |

| 2 | OPC+A-BFS (10%) | 306 | - | 34 (24:8) | 858 | 937 | ||||

| 3 | OPC+A-BFS (20%) | 272 | - | 68 (48:20) | 858 | 936 | ||||

| 4 | OPC+A-BFS (30%) | 238 | - | 102 (71:31) | 857 | 936 | ||||

OPC: ordinary Portland cement; W/B: Water-binder ratio; S/a: Sand-aggregate ratio (fine aggregate modulus). BFS: Blast furnace slag; G: Coarse aggregate; S: Fine aggregate; W: Water; AE: Chemical admixture.

| Type | Slump (mm) | Air Content (%) | Compressive Strength (MPa) | Reaching Time (h) of Core Max Temperature | Core Max Temperature (°C) | ||||

|---|---|---|---|---|---|---|---|---|---|

| 1 day | 3 day | 7 day | 28 day | ||||||

| 1 | OPC+BFS (30%) | 170 | 2.2 | 6.8 | 15.6 | 23.2 | 33.2 | 25 | 35.0 |

| 2 | OPC+A-BFS (10%) | 185 | 1.8 | 7.6 | 17.9 | 27.1 | 37.9 | 22 | 36.1 |

| 3 | OPC+A-BFS (20%) | 190 | 2.2 | 8.1 | 18.0 | 27.5 | 38.2 | 22 | 37.1 |

| 4 | OPC+A-BFS (30%) | 200 | 2.3 | 8.9 | 18.9 | 27.4 | 38.6 | 22 | 37.3 |

| Summary | |

|---|---|

|

|

|

|

|

|

|

|

| Division | Details | Construction Period for One Floor (Days) | Price of Concrete (KRW/m3) |

|---|---|---|---|

| Case 1 | General Concrete | 6 | 63,024 |

| Case 2 | 20% mix of A-BFS concrete | 4 | 59,970 |

| Case 3 | 30% mix of A-BFS concrete | 3 | 58,450 |

| Used Materials Name | Unit | Case 1 | Case 2 | Case 3 |

|---|---|---|---|---|

| Volume (unit/m2) | ||||

| concrete | m3 | 0.84 | ||

| gang form | kg | 0.14 | ||

| cement brick (0.5 B) | piece | 14.35 | ||

| cement | kg | 24.44 | ||

| sand | m3 | 0.05 | ||

| paint | kg | 0.24 | ||

| gypsum board (9.5 T) | kg | 12.98 | ||

| Division | Name | Unit | Volume | Cost [KRW] | |

|---|---|---|---|---|---|

| Rebar construction (ton) | material cost | rebar | kg | 1.03 | 840,480 |

| bond line | Kg | 6.50 | 9100 | ||

| Total (1) | 849,580 | ||||

| labor cost | qualified | Person | 3.08 | 341,187 | |

| normal | Person | 1.20 | 79,946 | ||

| Total (2) | 421,133 | ||||

| expenses cost | tool | Equation | 0.02 | 8423 | |

| other | Equation | 0.05 | 21,057 | ||

| Total (3) | 29,479 | ||||

| Total cost (1) + (2) + (3) | 1,300,193 | ||||

| Concrete pump car (m3) | material cost | pump car | hour | 0.02 | 369 |

| concrete (Case 1~4) | m3 | 1 | 63,024 | ||

| 61,500 | |||||

| 59,970 | |||||

| 58,450 | |||||

| Total (1) | 63,393 | ||||

| labor cost | pump car | hour | 0.02 | 314 | |

| qualified | person | 0.05 | 4838 | ||

| normal | person | 0.02 | 1599 | ||

| Total (2) | 6751 | ||||

| expenses cost | pump car | hour | 0.02 | 557 | |

| Total (3) | 557 | ||||

| Total cost (1) + (2) + (3) | Case 1 | 70,701 | |||

| Case 2 | 69,177 | ||||

| Case 3 | 67,647 | ||||

| Case 4 | 66,127 | ||||

| Construction Type | Case 1, 2, 3, 4 | |||

|---|---|---|---|---|

| Cost (KRW) | Cost of Unit Area (KRW/m2) | |||

| I. Construction | 1. temporary | 51,100,501 | 6015 | |

| 2. foundation | 8,123,544 | 956 | ||

| 3. rebar concrete | Case 1 | 1,386,821,005 | 163,251 | |

| Case 2 | 1,361,091,055 | 160,222 | ||

| Case 3 | 1,348,285,055 | 158,715 | ||

| 4. masonry | 47,068,598 | 5541 | ||

| 5. waterproof | 99,047,626 | 11,660 | ||

| 6. plaster | 249,566,152 | 29,378 | ||

| 7. tile | 237,547,762 | 27,963 | ||

| 8. stone | 81,559,470 | 9601 | ||

| 9. interior finishing | 332,193,765 | 39,105 | ||

| 10. papering | 97,276,846 | 11,451 | ||

| 11. window | 370,824,513 | 43,652 | ||

| 12. glass | 69,771,267 | 8213 | ||

| 13. coating | 43,749,846 | 5150 | ||

| 14. furniture | 585,097,337 | 68,875 | ||

| 15. metal | 65,856,459 | 7752 | ||

| 16. other | 43,748,094 | 5150 | ||

| II. electrical equipment | 705,069,139 | 82,998 | ||

| III. mechanical equipment | 813,726,931 | 95,789 | ||

| IV. landscape | 87,292,314 | 10,276 | ||

| Total | Case 1 | 5,375,441,169 | 632,776 | |

| Case 2 | 5,349,711,219 | 629,748 | ||

| Case 3 | 5,336,905,219 | 628,240 | ||

| Div. | Construction Period (day) | Comparison (Compared to Case 1) | Reference |

|---|---|---|---|

| Case 1 | 780 | - | - |

| Case 2 | 638 | 142 day shortening (4.7 month) | Shortening of construction period by increased compressive strength at early age (One floor construction period reduced from six days >> four days) |

| Case 3 | 568 | 213 day shortening (7.1 month) | Shortening of construction period by increased compressive strength at early age (One floor construction period reduced from six days >> three days) |

Table 13.

Cost reduction by a shortened construction period (assuming construction cost of 6.2 billion (KRW) and construction period of 28 months for a building of 25 floors and four-unit combinations).

| Div. | Shortening Period | Saving Cost (KRW) | Total (KRW) | ||

|---|---|---|---|---|---|

| General Admin. Cost * | Head Office Admin. Cost ** | Interest Expense *** | |||

| Case 1 | - | - | - | - | - |

| Case 2 | 4.7 month | 58,555,556 | 10,456,349 | 37,642,857 | 106,654,762 |

| Case 3 | 7.1 month | 87,833,333 | 15,684,524 | 56,464,286 | 159,982,143 |

* General administrative cost- Four similar project cases are investigated.- The ratio of general management expense is 5%–6% of overall construction cost with a mean of 5.6%.** Head office administrative cost- Headquarters management expense differs according to the number of projects being performed by the construction company.- Generally, total HQ management expenses for all projects is about 10%.- In this analysis, assumption was made to perform 10 projects, which equals to 1% of construction cost.*** Interest expense- Amount of loans in three similar projects based on self-construction is investigated.- Interest expense is calculated by converting to the recent interest rate of 15%- The ratio of interest expense is 1.5%–4.7% of overall construction cost with a mean of 3.06%.

| Division | Case 1 | Case 2 | Case 3 | |

|---|---|---|---|---|

| Total cost (KRW) | 5,375,441,169 | - | - | |

| Cost saving (KRW) | C | - | 106,654,762 | 159,982,143 |

| M | - | 25,729,950 | 38,535,950 | |

| Total cost after cost saving(KRW) | 5,375,441,169 | 5,268,786,407 | 5,215,459,026 | |

| Unit Cost after cost saving (KRW/m2) | 632,777 | 617,193 | 609,408 | |

| Cost ratio (%) compare to Case 1 | 100.00% | 97.5% | 96.3% | |

C: Cost saving by shortening the construction period; M: Cost saving by reducing the material (concrete) cost.

© 2016 by the author; licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC-BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Kim, T.H. Assessment of Construction Cost Saving by Concrete Mixing the Activator Material. Sustainability 2016, 8, 403. https://doi.org/10.3390/su8040403

AMA Style

Kim TH. Assessment of Construction Cost Saving by Concrete Mixing the Activator Material. Sustainability. 2016; 8(4):403. https://doi.org/10.3390/su8040403

Chicago/Turabian StyleKim, Tae Hyoung. 2016. "Assessment of Construction Cost Saving by Concrete Mixing the Activator Material" Sustainability 8, no. 4: 403. https://doi.org/10.3390/su8040403

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.