Mobile Money, Individuals’ Payments, Remittances, and Investments: Evidence from the Ashanti Region, Ghana

1

Graduate Program in Sustainability Science Global Leadership Initiative (GPSS-GLI), The University of Tokyo, Kashiwa 277-8563, Japan

2

Department of International Studies, The University of Tokyo, Kashiwa 277-0882, Japan

*

Author to whom correspondence should be addressed.

Sustainability 2018, 10(5), 1409; https://doi.org/10.3390/su10051409

Submission received: 30 March 2018

/

Revised: 23 April 2018

/

Accepted: 27 April 2018

/

Published: 3 May 2018

(This article belongs to the Section Economic and Business Aspects of Sustainability)

Abstract

:While many studies that are focused on mobile money concern the effects of mobile money on consumption and informal risk-sharing, little evidence is provided on how mobile money influences payments and microbusiness investment for low-income people. We estimate the effects of access to mobile money on individuals’ payments and income-generating activities by using data from the Ashanti Region of Ghana. Based on propensity-score matching and propensity-score weighted regression, we find that participation in mobile money is not dependent on individuals’ financial status. We also observe that mobile-money users are likely to send and receive larger volumes of payments and remittances. We further find that mobile-money users are more likely to save higher amounts, invest more in education, microbusinesses, land, and buildings, and also consume more relative to non-users.

1. Introduction

Financial inclusion could be defined as the full range of services (payments, savings, credit, and insurance), to specific quality features of delivery (for example, stability and affordability), inclusiveness (with special focus on the poor), and choice (offer of service by a range of institutions). Mobile money as a financial inclusion tool is suggested to have the potential to provide access to financial services to two billion unbanked adults [1], as well as about 200 million formal and informal micro, small, and medium-size enterprises in developing economies that lack access to affordable financial services [2,3]. Being unbanked (or financially excluded) is strongly linked to poverty [1,4].

Lack of access to financial services contributes to creating poverty traps and forces people to remain poor over generations [5,6]. The United Nations Sustainable Development Goals (SDGs) indicate the key role that greater access to financial services can play in achieving the ambitious 17 SDGs. The most prominent goals are goal number one—zero poverty, and goal number two—no hunger. Financially, including the poor through mobile money is likely to increase volumes of domestic payments and spur participation in a formal economy, with the benefits of smoothing incomes, protecting against vulnerabilities, facilitating day-to-day living, and pushing toward sustainable development goals [2,3]. However, evidence of its effect on individuals’ domestic payments and sustainable microbusiness investment is lacking.

Some studies provide evidence of the effect of financial inclusion tools such as credit, savings, insurance payments, and mobile money on poverty reduction. With respect to Mexico, a study on access to formal financial services including credit showed that access is not transformational in lifting people from poverty, though it does improve general well-being in terms of reduced depression, increased trust in others, and increased female decision-making power [7]. However, credit stimulated business start-ups or expansion and higher incomes in Bangladesh, Bosnia Indonesia [8,9], India, Mexico, and Mongolia [10,11]. Credit improved the ability of entrepreneurs to cope with risk in the Philippines and improved the consumption of low income salaried workers in South Africa [12].

However, evidence of the welfare effect of mobile money is slowly forthcoming. In Kenya, for instance, mobile money is largely used for payments [13]. Suri and Jack [14] found that in Kenya, access to mobile money agents within a 1-km radius of households increases household’s savings between 2–3%. In Uganda, a panel data analysis of households by [15] found that mobile-money usage had a positive impact on welfare. Households with access to mobile money recorded an increase per capita in expenditure on consumption (measured by food consumption), health, education, semi-durable items, and contributions to socio-cultural functions. This is attributed to mobile money user households receiving more frequent and higher amounts of remittances than non-user households.

Jack and Suri [16], in a non-experimental panel data analysis, found that the reduced transaction costs as a result of mobile money (M-PESA) usage enabled users to absorb large negative income shocks better without any reduction in household consumption, compared with non-M-PESA users. In contrast, households that did not have access to M-PESA had their consumption reduced as a result of the shocks by an average of 7%. A similar ill shock response by poor households owing to mobile-money usage is recorded by Suri, Jack, and Stoker [17]. In the same vein, Robert, Tilman, and Nina [4] recorded that M-PESA usage increased the amount and frequency of remittance received while facilitating increased risk-sharing among networks of friends and family.

Other studies [18,19] have found that financial inclusion through access to mobile money increases the willingness of individuals to remit cash. Aker and Wilson [20], through a randomized control trial experiment with a government cash transfer program, found that using mobile money reduced costs for both the organization that made the transfers and the recipients. The recipients used the costs saved to increase expenditures on food, reduce the depletion of assets, and invest in a variety of cash crop productions.

While many financial inclusion studies document the mixed effects of microcredit for low-income people, existing studies lack rigorous evidence with respect to the following useful aspects:

- (i)

- whether mobile money services really serve low-income people [13],

- (ii)

- how the use of mobile money relates to individuals’ volumes of domestic payments, and

- (iii)

- whether access to mobile money payment services increases individuals’ likelihood of participating in a formal economy in a sustainable way [21].

Apart from consumption expenditure, a basic need that drives financial activity for both the rich and poor is to seize investment opportunities as they arise [22]. Hence, examining these aspects is important for the economic empowerment of low-income people and their livelihood sustainability. Klapper et al. [3] elaborated on how access to financial services can help achieve sustainability in terms of no poverty and zero hunger. Digital financial payments, for example, can enable people receive remittances from family and friends to help reduce the likelihood of getting into poverty traps [16]. Government anti-poverty cash-outs could be delivered using mobile money. While mobile money presents greater prospects to expand access to financial services, the challenge that policymakers face is how to sustainably leverage the potential of mobile money to meet the needs of the underserved, as well as to ensure the sustainability of the financial services. Thus, there is a need to understand the clear linkage between how the provision of access to the financial inclusion tool relates to the financial inclusion of the unbanked in a country-specific context [23] in order to ensure sustainability. This study provides information that can guide policy on how to leverage the potential of mobile money to promote the sustainability of micro-enterprises, reduce poverty, and improve well-being.

The objective of this paper is to evaluate the impact of mobile money on individuals’ payments and investments while considering the case of the Ashanti Region in Ghana. Specifically, we focus on examining the type of people (i.e., the segment of society) using mobile money, the level of participation in mobile money, and the relationship between participation and individual payments, remittances, and investment in sustainable income-generating activities.

Using primary data obtained from 557 study participants (388 users and 169 non-users) largely from the informal sector across urban, peri-urban, and rural communities in Ghana, we examine whether the socio-economic characteristics, payments, remittances, savings, and micro-investment activities of mobile-money users significantly differ from those of non-mobile money users. To correct for potential selection bias from the use of mobile money in our model, propensity-score matching and propensity-score weighting regression methods are deployed.

First, we find that participation in mobile money is independent of the financial status of an individual. Second, among participants, those with higher financial assets are more likely to be better positioned to do higher volumes of transactions of mobile money. Third, we observe that mobile-money users are more likely to send and receive payments and remittances, save more, invest more in businesses, land, and buildings, and consume more. These findings are consistent with some existing studies [19,22,24,25]. This paper adds to existing literature by providing non-experimental evidence suggesting that providing access to finance through mobile money may be a useful tool to improve the lives of people.

The rest of the paper is structured as follows. Section 2 explains our hypotheses to be tested. Section 3 describes the trend of mobile money in Ghana. Section 4 explains the data collection methodology. Section 5 discusses the estimation strategies employed, and the estimation results are contained in Section 6. Conclusions follow in Section 7.

2. Hypotheses

To examine the impact of mobile money on individuals’ payments and investments, we propose the following hypotheses. First, we hypothesized a positive effect of financial assets on mobile money participation. Mobile money as a financial inclusion tool may enable people to increase their participation in the formal economy, and thereby help them improve their lives [3]. However, one needs to be able to afford a phone and a SIM card (subscriber identification module used in mobile phones), and one needs to register a SIM card as a mobile wallet to begin any transaction—such as for example, to receive payments. In a case in which one wants to save, purchase government investment bonds, or make a payment, one may require some financial resources. Further, in the case of Ghana, most of the mobile money transactions are charged a service charge of 1%.

Hypothesis 1 (H1).

Higher financial assets contribute to participation in mobile money.

Hypothesis 2 (H2).

Higher financial assets contribute to higher volumes of transaction via mobile money.

To estimate the impact of mobile money on individuals’ payments, we hypothesized that mobile use has a positive effect on individuals’ domestic payments and remittances. Batista and Vicente [19], Blumenstock, Eagle, and Fafchamps [18] showed that access to mobile money increased willingness to send remittances. Fast, easy, and convenient means of making and receiving payments through the use of mobile money means faster transactions within time constraints. Thus, it creates more opportunities for payments and remittance in an economy within a certain period. Hence, we propose a third hypothesis.

Hypothesis 3 (H3).

Mobile money participation contributes to greater volumes of domestic payments and remittance.

Finally, to estimate the impact of mobile money on investments, we hypothesized a positive effect of mobile money participation on investments. Here, investments mean any expenditure that goes into generating value that would yield benefits over time. This could be physical or non-material investments, such as in health and education. A growing body of rigorous evidence suggests that access to financial services have a positive impact on employment, business activities, household consumption, and well-being [21,26]. When people enroll into mobile money, access is enhanced to formal financial services, and hence, participation in the formal economy is improved. For example, aside from - consumption, remittances sent and received could be used in acquiring assets or paying for school fees. The transaction through the mobile money space could provide an avenue to build income. For example, with a GH¢5 (USD 1.30), a mobile money user could purchase a government security bond that could earn interest of 13–17% per year. At the time of this baseline data collection, the exchange rate between the Ghana cedi and the US dollar was approximately GH¢3.8–4.2:$1. Hence, an average of GH¢4.00:$1.00 is used throughout this paper.

Hypothesis 4 (H4).

Mobile money participation contributes to higher investments in business and capital assets.

3. Trends and Mechanisms of Mobile Money in Ghana

The payment systems in Ghana consist of an array of institutional arrangements and processes that facilitate the movement of monetary claims between two or more economic entities. The Bank of Ghana defines mobile money as electronic cash backed by an equivalent amount of Bank of Ghana notes and coins stored using SIM in a mobile phone as an identifier. The Bank of Ghana gives license to mobile network operators (MNOs) to issue mobile money. The MNOs keep the electronic account on the SIM in the mobile phone for users of mobile money [27].

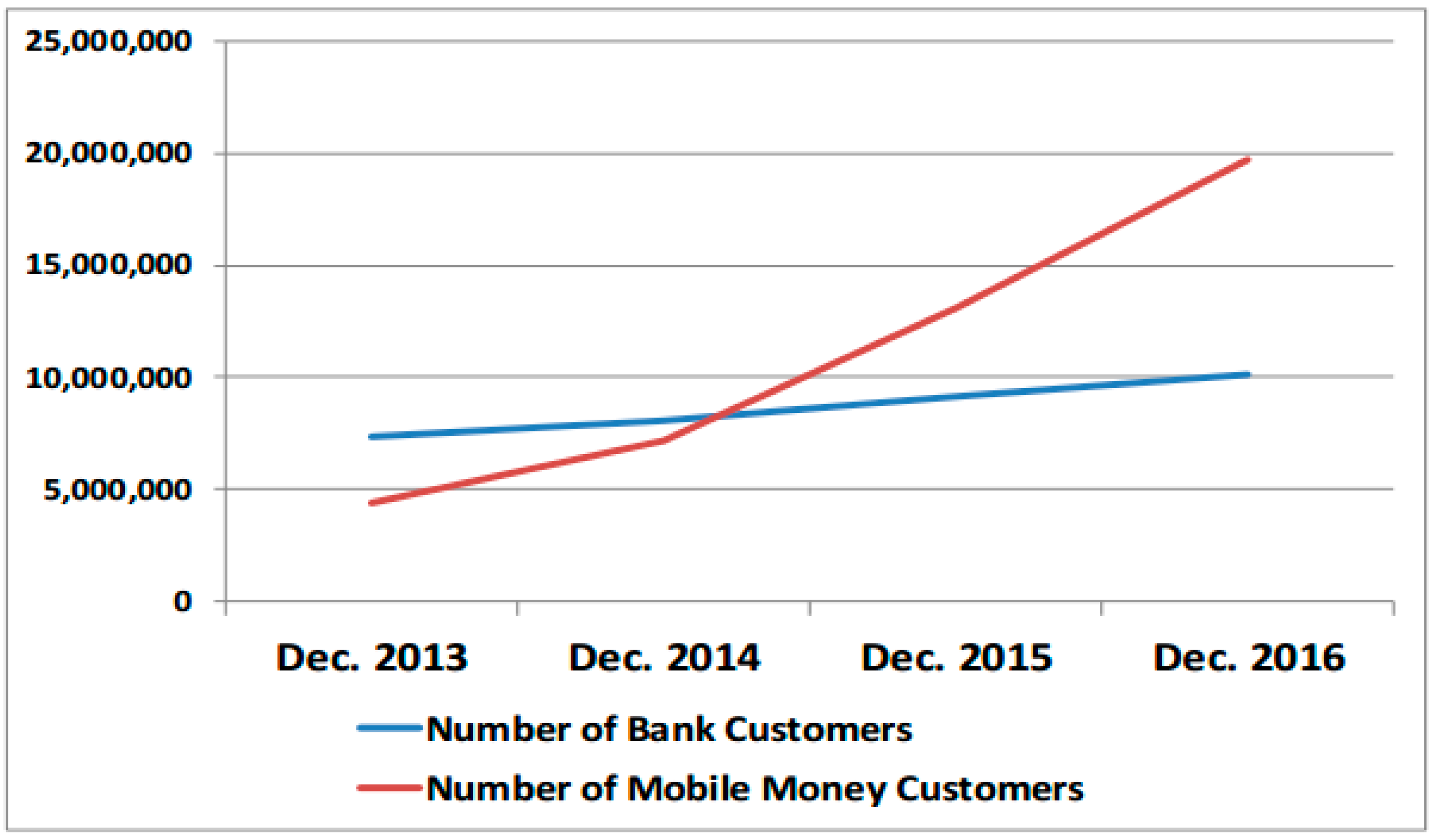

Mobile money is a major and growing part of the payment system, mostly for unbanked and underserved people [2,27]. Figure 1 indicates a sharp rise in mobile money account holders from 2012 to 2016 compared with the relatively slow increase in the number of bank account holders.

In 2012, the number of mobile money account holders was approximately three million fewer than the number of bank account holders. However, by December 2016, the number of mobile money account holders increased to 20 million, which was double the number of bank account holders in Ghana.

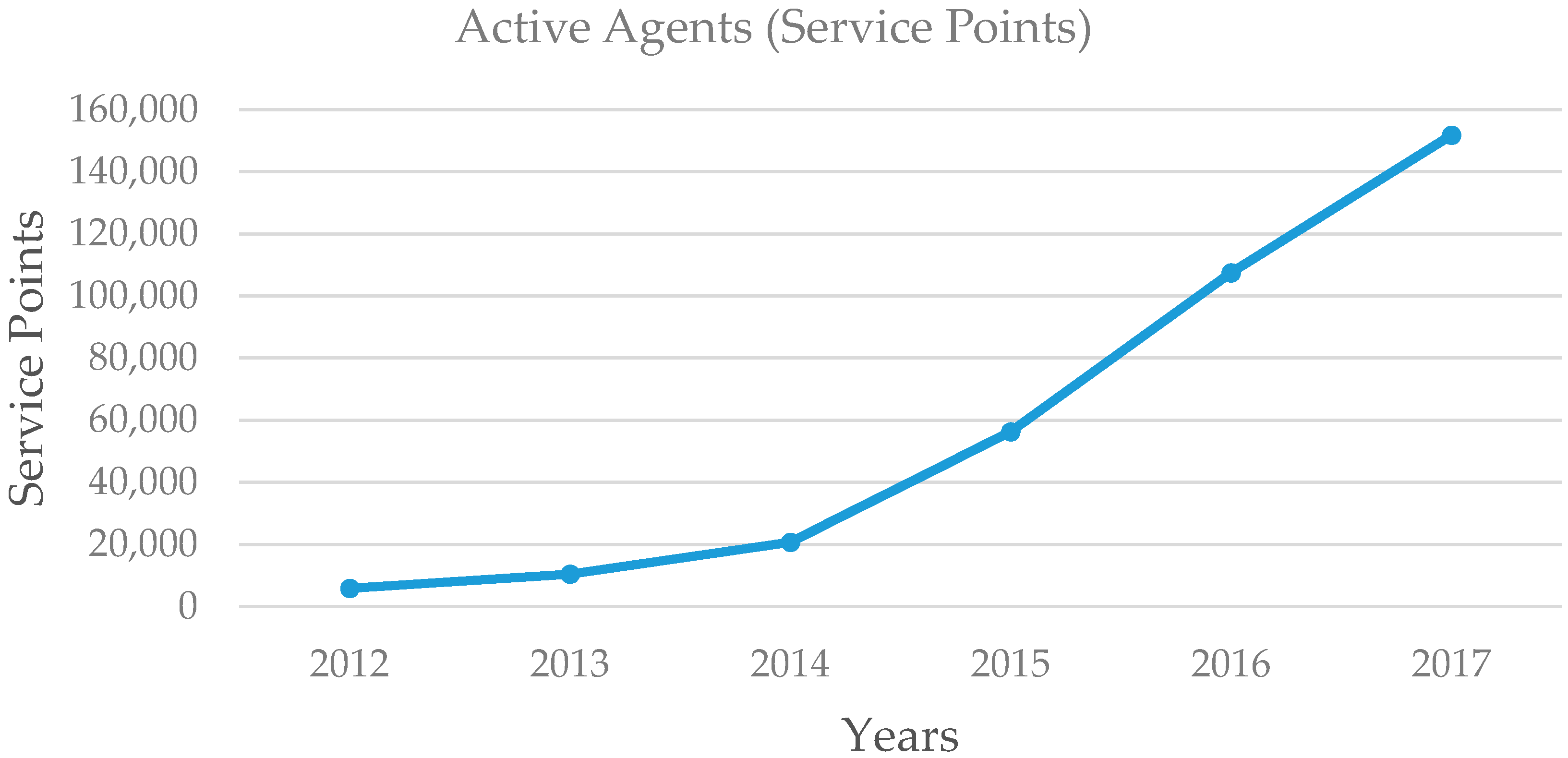

Figure 2 shows the number of active mobile money agents (or service points), which has also risen sharply from 2012 to the end of 2016.

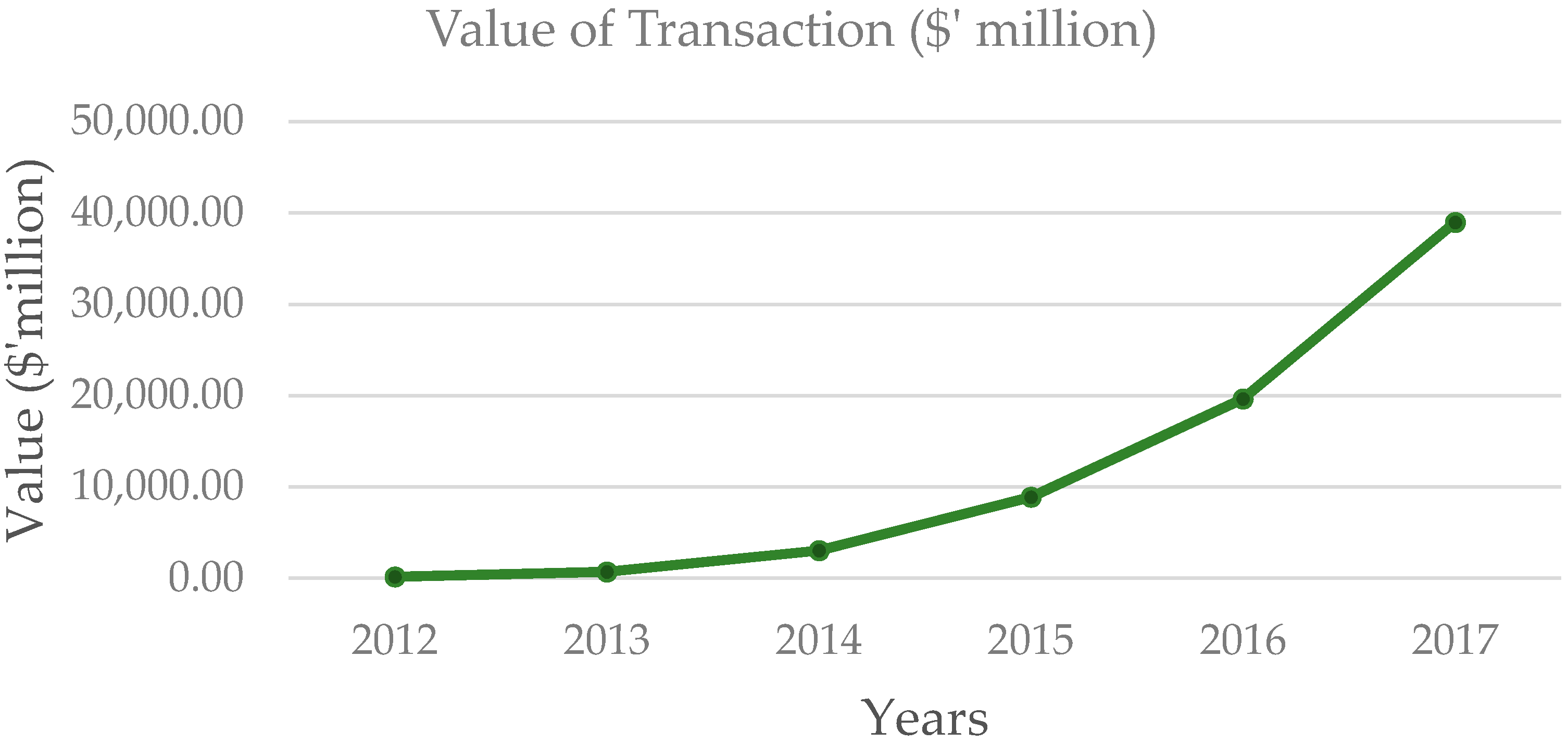

Similarly, Figure 3 shows a sharp increase in the yearly volume of transactions in the mobile money space to $20 billion.

Recent technological advancement has led to a proliferation of mobile phones and their penetration into both urban and rural areas in Ghana. These developments have created an environment for mobile network operators (MNOs) in collaboration with banks to develop the business of providing mobile money and delivering banking with speed, flexibility, convenience, and affordability to the doorsteps of users [26].

A person owning a mobile phone and SIM has to approach an MNO to subscribe to a mobile money service in order to own an account called a wallet. A wallet is mainly used to transfer value from one person to another person (P2P), for the payment of goods and services, such as buying airtime and data, paying utility bills, paying school fees, paying cable television bills, paying the salaries of some workers, paying cocoa farmers, making government cash transfers to poor households, paying taxi fares, paying off microcredit loans, ensuring savings, and contributing to microinsurance.

In 2016, Ecobank Capital Advisors, together with the Mobile Telecommunications Network (MTN), launched a government security bond called “TBILL4ALL”. This is an investment instrument that can be purchased with as low as GH¢5.00 (USD 1.3) at any time of the day, and it earned between 13–17% interest per year at the time of launch. For the convenience of the user, mobile money wallets may be linked to bank accounts to provide the user with a unique consumer experience in terms of providing access to a variety of financial services that are designed to meet the needs of the poor and the unbanked [27,28].

Once a subscriber loads money into his or her wallet, the amount in the wallet is backed by an equivalent unit of notes and coins at a partner bank. The store of value function of the mobile money leads to quarterly interest payments of on the balance of the mobile money float. The total interest paid to holders of electronic money wallets in 2016 amounted to GH¢24.79 (USD 6.2) million. Users pay a two-way transaction cost amounting to about 1% of the amount transacted. For instance, when a user transfers funds from his mobile wallet to a receiver, the sender pays 1% of the amount transferred. In addition, when a receiver goes to a vendor for the cash amount received, the receiver also pays 1% of the amount withdrawn. Part of the commission is used to pay the monthly commission to vendors, and the rest is taken by the partner bank and the mobile money network operator as business returns.

4. Methodology

We collected data in September 2016 and February 2017 to gather information from respondents, including mobile-money users and non-users, through a questionnaire. To select participants for the survey, we used a stratified sampling approach. First, we considered all 10 regions of Ghana, based on the 2010 Population and Housing Census. The Ashanti Region is the region with the largest population in Ghana, and it was selected because it presented a fair representation of rural, urban, and peri-urban communities. Regarding the population distribution within the districts of the Ashanti Region in terms of percentage of urban and rural areas, study participants were drawn from two communities each in Kumasi Metropolis: Obuasi Municipal Assembly, and Amansie West District.

In lieu of a population list of those districts, enumerators randomly approached prospective study participants in streets, homes, and workplaces. The prospective participants were then told about the study and requested to be voluntary participants. Our target was adults who were at least 18 years of age and owned a mobile phone. This approach was taken because having a mobile phone is a requirement to have access to mobile money, and we are interested in finding the difference between those who use mobile money and those who do not. Precaution was taken to ensure that gender was balanced among to participants to be surveyed.

4.1. Data Collection

In total, 557 study participants were enrolled in the study and surveyed. Of the 557, 388 were mobile-money users, and 169 were non-users. Of the 388 mobile-money users, eight were government salary workers, 20 were salary workers in private entities, 20 were students, and 307 were engaged in self-employment activities, such as retail or petty trading, farming, dressmaking, hairdressing, and other artisan work. The remaining 31 were unemployed. Of the 169 non-mobile money users, three were government salary workers, 10 salary workers with private entities, four were students, and 130 were engaged in self-employment activities such as retail or petty trading, farming, dressmaking, hairdressing, and other artisan work. The remaining 20 were unemployed, and two were on pension.

The data collected from respondents included socio-economic characteristics such as age, gender, education, occupation, income levels, expenditure, and assets ownership. Information about migrant status and knowledge of and use of mobile money was also collected. In addition we also conducted two hypothetical risk and time preference games based on a pairwise choice [29,30]. As can be seen from Appendix A, game one has 10 sets of questions with two answer options: A (receive today) or B (receive three months later). Throughout the 10 questions, the amount for answer option A remained the same, while the amount for answer option B kept increasing by units of (GH¢2.00). In this regard, where an individual switched from A to B indicated the impatience level that can be estimated by calculating the discount rate of the switching point. Game two is shown in Appendix B, and this was similar to game one; however, the answer options were A, preference for a fixed amount (GH¢10.00) in three months, and B, which indicated a higher amount (GH¢12.00) in six months. Answer option A was fixed for all of the questions, while option B was increased by units of GH¢2.00. We used the discount rate at the game one switching point and the discount rate at the game two switching point to calculate the present bias of the individual [31].

As perceived risk is considered to be an important factor in using mobile money [32,33], we collected information on risk preference, as shown in Appendix C. The game has two projects: project A, which receives a certain payoff, and project B, which yields a probabilistic payoff of a certain amount (GH¢12) or 0, each at 50% probability. The games are hypothetical, with no physical monetary incentive. We prepared eight games, and the certain payoff in project A increased as we went down the list of eight games (Appendix C). The expected payoff for project B remained the same in all eight games. The expected payoff of these projects was equalized in game 4, and from then onward, it was higher for project A. Thus, the earlier the respondent switched from project B to project A, the more risk averse the person was. We made an index between one and eight, with eight being the most risk averse. There were 10 multiple switches. The first switching points of these were considered in the analysis. Again, there were 47 respondents who did not switch at all. They chose project B for all eight games, meaning that such observers preferred to take risks.

4.2. Estimation Strategy

The objective of the paper is to determine the kind of people using mobile money and estimate how mobile-money usage has affected domestic payments and the investments of current users. Investment here means any expenditure that goes into day-to-day income-generating activities. To achieve the first objective, we examined the determinants of mobile-money users by discrete choice models of probit and logit estimations. Further, to examine the volume of mobile money transacted, we use an ordinary least squares (OLS) estimation.

For the second objective, we estimated:

where Yi is the outcome, which is the remittance sent, remittance received, investment in microbusiness, spending in education, and health by the individual, savings, and consumption. MMi is a mobile money participating dummy that equals 1 if an individual participates, and 0 otherwise. is a vector of control variables at the individual level. includes financial assets, age, gender, years of schooling, household size, numbers of non-household dependents, marital status, distance to the nearest vendor or service point, number of months a person has heard about mobile money, discount rate, and present bias. is the error term.

We examined whether beta 1 is statistically significantly different from zero. Here, since individuals may self-select themselves as using mobile money, the variable MM may be endogenous. For example, participants using mobile money may be people who naturally have an affinity toward accepting and using new products quickly, and thus, an unobserved trait may be correlated with a higher amount of payment or investment. Or, we may have a reverse causality, that is, a higher amount of investment or payment induces people to use mobile money. Thus, we employed propensity-score matching (PSM) and inverse propensity-score weighted regression to reduce the differences that were due to observable characteristics between users and non-users. In conducting PSM, we assume that the conditional independence assumption is met, that is, given a set of covariates, X, which are not affected by treatment, potential outcomes are independent of treatment assignment [34]. This conditional exogeneity implies that we removed bias through ensuring that the Xs are adequately balanced between treatment and control individuals [34,35]. Hence, the systematic difference between mobile-money users and non-users with the same values of covariates can be attributable to mobile money. Admittedly, the limitation of PSM is that it only controls for observed differences between treatment and control, as is often the case in non-experimental studies.

Various algorithm methods were used for the matching; however, the Caliper radius (0.1) and kernel common trim (0.1) methods are reported here, because they gave the lowest mean bias estimates. The Caliper method has the advantage of avoiding the risk of bad matches. This method chooses an individual from the comparison group as a matching partner for a treated individual who lies within the caliper (‘propensity range’) and that is closest in terms of propensity score [34]. In other words, the method compares individuals from two different groups by imposing a tolerance level of maximum propensity score. This is called the common support condition, and it is based on distance (caliper). It raises the matching quality. In kernel matching, information from the non-user group is used to generate theoretical observations, and these observations are used to match observations within the user group. In the kernel common trim method, one can specify the distance within which comparable user groups can be selected. This was done by simply specifying a distance of (0.1) in stata.

According to Heckman, Ichimura, and Todd [36], although the PSM is able to remove the systematic observable difference between users and non-users, it reduces the efficiency of the estimation. Therefore, we further conduct an inverse propensity score weighting regression to achieve consistency in estimates in a process known as “doubly-robust” estimation [37]. This method uses the inverse of the propensity score as weights to run a regression of the outcome variable, as proposed by Robins and Rotnitzky [38] and as later improved by Hirano, Imbens, and Ridder [39]. Here, the weight is equal to one for observations that are users, and px(x)/(1 − ps(x)) where ps is the propensity score for non-user observations [40,41].

Finally, as not every respondent had undertaken activities such as remittance and investments in the last 12 months (i.e., many have zero values) in generating variables with logs, we added 1 to all of the observations before creating the respective log.

5. Estimation Results

5.1. Who Uses Mobile Money?

A summary of socio-economic characteristics of the user and non-user groups is shown in Table 1. A mobile money user is an individual who has ever used mobile money at least once to either receive money from someone, send money to someone, save, pay any bills, or perform any transaction service offered by the mobile money platform. A non-user is an individual who has never undertaken any of the transaction services offered by the mobile money platform.

Variables such as age, education, marriage status, minutes of walking to the nearest vendor, years of work, whether the respondent had heard about mobile money—and if so, how long ago (months), and percentage of friends on mobile money are significantly different between mobile-money users and non-users. However, the groups did not differ in terms of gender, migrant status, household size, number of non-household dependents, employment status, risk-taking ability, and impatience, which was indicated by discount rate and present bias. The average age of users was 32 years, while the average age for non-users was 35 years. About 51% of respondents were males. Within the user group, 50% were males and within the non-user group, 56% were males.

The average years of formal education for users was 10, which was one year higher than the free compulsory universal basic education level. The average years of formal education among non-users was eight. About 43% of the respondents were married. Within the user group, 39% were married, while 52% of the non-users were married. Mobile-money users, on average, had heard about mobile money longer, at an average of 43 months before enrolling in the study, while non-users heard about mobile money about 33 months before the study period.

It took a mobile user an average of four minutes to walk to the nearest service point, while it took the non-user an average of five minutes to walk to the nearest service point. Users had worked an average of six years after school, while non-users had worked longer, about nine years after school. Users had 68% of their friends on mobile money, while non-users had 51% of their friends on mobile money. Although not significant, users had a larger average household size of four, while non-users had a household size of three. Again, users had a higher average number of non-household dependents. Whether a user was a migrant or the number of years that the person had lived in the community (if not a migrant) was not different between the two groups.

Table 2 shows that there were significant differences for most of the variables relating to economic power between users and non-users.

About 61% of mobile-money users owned a formal bank account, and 53% owned a mobile-money account. However, only 37% of non-users owned a formal bank account, and 0.2% owned a mobile-money account. Users had an average monthly income of GH¢786.05 (USD 196.50), while non-users had a average monthly income of GH¢367.68 (USD 91.92). In terms of daily income, dividing monthly income by 30 days for each group gives a daily income of USD 6.55 for users, and USD 3.06 for non-users. With USD 6.55 per day, mobile-money users can be categorized above the international poverty line of USD 3.1 or less. Considering an average income of USD 3.06 per day, non-users can be categorized within the upper limit of the moderately poor line.

Payments sent is defined as the total value of cash-outs made for goods and services received. The mean monthly amount of payment sent by mobile-money users, GH¢1945.26 (USD 486.32), was higher than the mean monthly amount sent by non-users, GH¢1062.51 (USD 265.63). Thus, users sent significantly higher average yearly payments, GH¢15,133.86 (USD 3783.47), compared with non-users, who sent an average yearly payment of GH¢7727.41 (USD 1931.85). Payment received is defined as cash-in received for rendering services and goods. Users received a higher monthly payment of GH¢786.05 (USD 196.51) and yearly payments of GH¢9249.31 (USD 2312.33) compared with non-users, who received a monthly payment of GH¢367.68 (USD 91.92) and GH¢5868.09 (USD 1467.02) yearly.

Remittance is defined as the total value of free cash and in-kind gifts received from people or sent out to people. Mobile-money users sent a higher amount of GH¢285.97 (USD 71.21) of remittance per year compared with non-users who remit, GH¢141.24 (USD 35.31). Users sent an average of GH¢453.60 (USD 113.4) per year through mobile money. Similarly, on the receipt side, mobile-money users received higher average remittances of GH¢322.99 (USD 80.74) per year compared with the GH¢144.09 (USD 36.02) received by non-users. Consumption is defined by the amount of annual expenditure that goes to food, rent, and utility bills. Mobile-money users had a higher average monthly and yearly consumption.

However, in terms of total annual savings, investment in micro-enterprises, land, and buildings, and spending on health and education, no statistically significant difference is shown here among the two groups. Here, investment is defined as any expenditure that goes into income-generating activity, capital formation, or asset building that would yield value or income over time. Investment in education here implies any expenditure incurred by the respondent in educating him or herself, his or her spouse, children, any household member, or non-household member(s) in the last 12 months. Investment in health involves health-related expenditure for the respondent, spouse, children, other household member(s), or non-household member(s).

To examine the characteristics of mobile-money users, the marginal effects of logit and probit estimates are shown in Table 3. Both the logistic and probit regressions were estimated, and they show similar results; however, we discuss here the probit (column 2) results, because they provide estimates with lower standard errors. The relatively lower standard errors are useful indicators of efficient estimates.

The results indicate that years of formal education, household size, non-household dependents, and number of months since an individual heard about mobile money are significant variables that positively influence the probability of using mobile money. The number of years of formal education is significant, at 1%. An additional year of education is likely to increase the probability of using mobile money by 6.2%. Household size is significant at 5%. An addition of one member in a household is likely to increase mobile-money usage by 8.2%. Non-household dependent is significant at 5%. An addition of one person to non-household dependents is likely to increase mobile-money usage by 20.1%. The number of months that had passed since an individual had heard about mobile money is significant at 1%. A monthly increase in how long a person has known about mobile money is likely to increase mobile-money usage by 1.4%.

On the other hand, age, male status, married status, and distance to the nearest vendor are significant and negatively related to mobile-money usage. Age is significant at 10%, and a year increase in age is likely to reduce mobile-money usage by 1.1%. Being a male is significant at 1%, and it shows a probability of reducing mobile-money usage by 33.0%. Being married is likely to reduce mobile-money usage by 28.7%, and this effect is significant at 5%. In other words, females are more likely to transmit higher volumes of mobile money than males. This result might be due to the suggestions that mobile money can offer women better control of their finances and thereby empower them economically. Similarly, distance (minutes of walk) is negatively significant at 10%. This means that a one-minute increase in walking distance to the nearest vendor is likely to reduce mobile-money usage by 2.0%. In other words, individuals who are far from vendors are less likely to use mobile money.

A key economic variable that would help establish Hypothesis 1 concerns total financial assets. This is the sum total of cash that an individual has at various places such as banks or non-bank financial institutions, money with his/her employer, money at home, and money in his/her wallet or on mobile money. However, total financial assets are not significant, even though they showed a positive coefficient. The analysis of the findings from the probit estimates does not provide sufficient information to validate Hypothesis 1. Hence, Hypothesis 1 is rejected. In other words, participation in mobile money is not dependent on the financial status of an individual.

To confirm Hypothesis 2, we estimate the amount of mobile money sent by ordinary least squares (OLS) (Table 4). A positive significance is observed between total financial assets, years of formal education, household size, non-household dependents, months since the respondent heard about mobile money, and amount of money transmitted through mobile money per year.

Total financial assets is significant at 5%, and a 1% increase in the total financial assets of a user is likely to increase the individuals’ volume of mobile money transaction by 0.19%. This result implies that among those who use mobile money, individuals who have more cash are more likely to transmit a higher amount of money through mobile money within a year. This finding may be because individuals who have more cash are in a better position to take advantage of the transaction opportunities that mobile money presents, and this result thus confirms Hypothesis 2.

Non-household dependents are significant at 1%; thus, an addition of a non-household dependent is likely to increase the volume of mobile money transacted by 98%. At a 1% significance level, an additional increase in the number of months since the individual heard about mobile money is likely to increase the transaction volume by 1.9%.

5.2. Impacts of Mobile Money

To examine the impact of mobile money on payments and investments, we conduct PSM and propensity-score weighting regression. We use domestic activities such as payments, remittances, investments in microbusinesses, education, and health, savings, and consumption as the outcome variables. We use the same model as in column (2) of Table 3 to estimate the propensity scores.

PSM Results

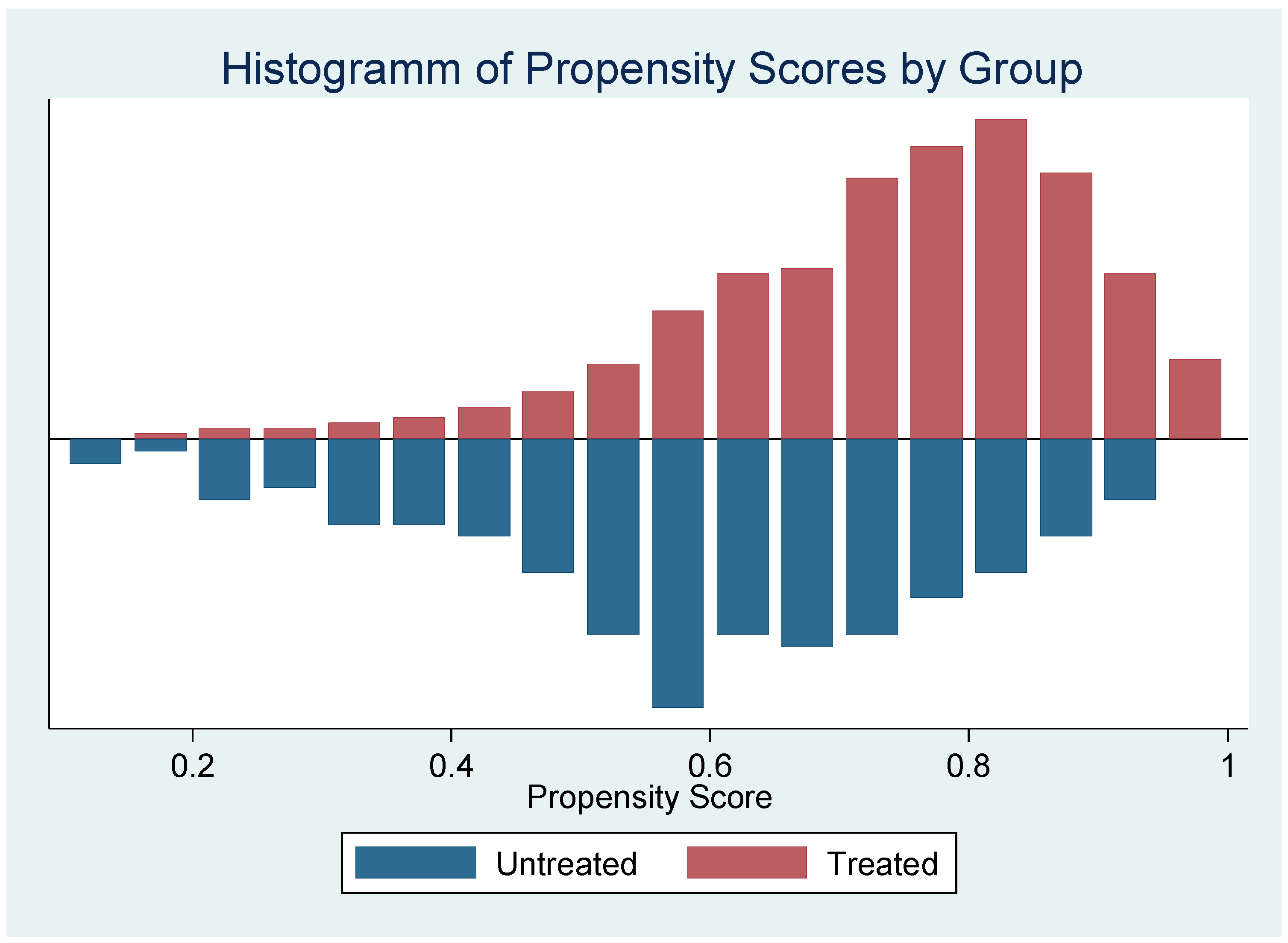

The propensity score (ps) score for non-users ranges between 0.1023816 and 0.9295550, while the ps for users ranges between 0.1982898 and 0.9813992. These results provide a feasible condition of common support or overlap for both users and non-users for successful matching. The feasible overlap range is between 0.1982898 and 0.929555. The histogram of the propensity score estimates is shown in Figure 4.

The balancing test for kernel matching and radius Caliper methods is shown in Table 5. The kernel common trim (0.1) method produced a more balanced matching than the radius Caliper (0.1) method. Kernel matching reduced the significant variables to zero (0), and the mean bias was reduced from 20.0 to 4.0 after matching. In the case of payments sent, kennel common trim (0.1) reduced the significant variables to one (1), and reduced the mean bias from 20.0 to 4.6.

The PSM results of the impact of mobile money on domestic payments and investments are shown in Table 6. Our results indicate that the logs of yearly domestic payments, remittances, investment in land, buildings, and microbusinesses, education, savings, and consumption are statistically significant for both the Kernel common trim (0.1) matching and radius Caliper (0.1) matching. The outcome variables—yearly payments sent and received, remittances sent and received, savings and investments in land, buildings, and microbusinesses—are significant at 1% for both matching methods. Yearly investments in education and consumption are each significant at 10% for both matching methods, while yearly investment in health is not significant. These results indicate that when considering only the observable differences when people within a population are randomly assigned to use mobile money, that group of people will send and receive higher volumes of payments and remittances, save higher amounts of money, invest in microbusinesses, land, and buildings, and consume more.

5.3. Inverse Propensity-Score Weighting Regression Results

To further enhance the robustness of our analysis, we conduct inverse propensity score-weighted regression on each of the outcome variables. The effects of mobile money on the logs of yearly payments sent, payments received, remittances sent, and remittances received are reported in Table 7.

5.3.1. Impact on Payments

We observe a positive effect of mobile-money usage on domestic payments. Mobile-money usage is positively related to yearly payments sent and payment received, and the effects are statistically significant at 1% and 5%, respectively. Using mobile money is likely to increase individuals’ domestic payments sent by 39.9%, and the payment received by 30.8%. These results confirm Hypothesis 3, which states that mobile money participation is positively related to the volume of domestic payments. Hence, we do not reject Hypothesis 3.

Within the other control variables, we observe that total financial assets, household size, non-household dependents, and total household physical assets are significant and positively related to both yearly domestic payments sent and payments received. Age and present bias are positively related to payments sent, but such variables are not significant with respect to payments received. Similarly, being a male and being formally employed are positively related to yearly payments received, but not significant in relation to payments sent. On the other hand, discount rate and migrant status are negatively related to payments sent, but are not significantly related to payment receipt.

5.3.2. Impact on Remittances

As presented in Table 7 (Columns 3 and 4), we observe positive effects of mobile-money usage on the volumes of yearly domestic remittance sent and on the volumes of yearly domestic remittances received, which are statistically significant at 1% and 5%, respectively. A mobile-money user is likely to send 131.2% more remittances and receive 73.3% more remittances than a non-user. These findings further confirm Hypothesis 3, which states that mobile-money usage contributes to greater volumes of remittances.

Among the other control variables, we find that additional time in knowing about mobile money positively relates to both yearly remittances sent and remittances received. Total financial assets, male status, minutes walked to the nearest vendor, and longer years of work are significant and positively related to the amount of remittance sent, but are not significantly related to remittances received. Being married is negatively related to remittances sent, but is not significantly related to remittances received. Moreover, age, risk-averseness, and formal employment are negatively related to remittances received, but are not significantly related to remittances sent. For location dummies such as rural (Amansie West District) and urban (Kumasi Metropolitan Assembly (KMA)), the base group is a peri-urban community (Obuasi Municipality). We found that relative to the peri-urban area, living in the urban community (KMA) is negatively related to both yearly remittances sent and yearly remittances received.

5.3.3. Impact on Investments

Table 8 (Column 1) indicates a significant positive effect of mobile-money usage on individuals’ yearly investment in microbusiness, land, and buildings. The investment variable in this study is generated using yearly microbusiness expenditure startup or expansion, as well as the expenditure that goes into land and building acquisition or maintenance. We find that at a 1% significance level, yearly investment in microbusiness is higher—102.9% more for mobile-money users than for non-users. This finding confirms Hypothesis 4, which indicates that individuals who use mobile money are likely to increase their investment in microbusiness and capital assets. We also observe that other control variables, such as total financial assets, age, household size, non-household dependents, household physical assets, self-employment, and living in a rural community are significantly positively related to investment in microbusiness, land, and building.

Column (2) of Table 8 indicates the estimated results for the impact of mobile money on investment in education. We observe that mobile-money usage is significant at 1%, and is positively related to investment in education. Individuals who use mobile money are more likely to invest 121.8% more in education than non-users. Variables such as total financial assets, age, household size, non-household dependents, present bias, and years of work are positively related to investment in education. On the other hand, discount rate is negatively related to investment in education, which means that individuals who are less patient are less likely to invest in education.

In Column (3) of Table 8, we show the results of the impact of mobile money usage on investment in health. We observe no significant relationship between mobile money usage and investment in health. Other factors such as age, household size, months since the respondent heard about mobile money, and living in both rural and urban communities are positively related to investment in health. Being a male, minutes of walk to the nearest vendor, and being in formal employment are negatively related to investment in health.

5.3.4. Impact on Savings

Column (4) of Table 8 indicates the results of our examination of the impact of mobile money on savings. We observe a significant and positive relationship between mobile-money usage and savings. The amount of yearly savings is higher among mobile-money users by 136.3%, and the result is significant at 1%. Since mobile money provides easy access to a savings device and easy savings in general, it is possible that mobile money has provided access to an easy savings mechanism for users, and hence they are saving more. We also observe a significant relationship between other control variables and savings. Total financial assets, non-household dependents, household physical assets, discount rate, and longer years of work are significantly positively related to yearly savings.

5.3.5. Impact on Consumption

In Column (5) of Table 8, we examine the effect of mobile money usage on consumption. We observe a positively significant effect of mobile -money usage on consumption. Mobile-money users are likely to consume 24.0% more, and this result is significant at the 5% level. We also observe that age, household size, present bias, and household physical assets are significantly positively related to consumption. On top of that, we observe that individuals with a higher discount rate and those living in a rural area are less likely to consume more.

6. Discussion

The findings from Section 5.1 addresses Hypothesis 1, which deals with access to mobile money; hence, it explains whether there is equal access to mobile money by all segments of society with respect to financial assets. It also addresses Hypothesis 2, which, on the other hand, deals with level/intensity of participation for users of mobile money, in terms of amount of money transmitted. Access may not necessarily mean usage.

Aside from financial assets, non-household dependents and the length of time since a person had heard about mobile money are significant at 1% in determining the level of participation. As a person has a greater number of non-household dependents, s/he is likely to have more occasions that require him/her to transfer some financial resources to these dependents. Further, having more non-household dependents is often associated with more financial resources, and this higher wealth may be another reason for the significance of this variable. Again, an active user with a higher financial asset is also more likely to take advantage of the income-generating activities on a mobile-money platform to do more transactions, such as for example, put more money on the mobile wallet to earn more quarterly interest, or invest in treasury bills. Further, the longer the length of time since a person heard about the mobile money, it is also more likely that s/he gets accustomed to using mobile money for financial transactions.

On the other hand, active participants with less financial resources may be looking for opportunities to receive remittance for subsistence. Therefore, while the less financially-resourced may be active on mobile money with expectations to receive resources from family and friends, the more financially-resourced may be active on mobile money with expectations to earn income. These activities may include doing transactions with family and friends, taking and receiving loans using mobile money, transacting with business with business partners, and so on. These may be driving the higher level of financial activities by those who are more financially resourced. These explanations bring to the fore the sustainability issue of how to empower low-income people to take advantage of the income-generating potential that mobile money presents.

The findings from Section 5.3.1 suggest that mobile-money users are more likely to send and receive higher amounts of payments and remittances. In Section 5.3.2, the findings suggest that mobile-money users are also more likely to save more, invest more in education, microbusinesses, land, and buildings, and consume more. There may be several reasons for these findings.

First, it could be that mobile money provides fast, easy, and convenient means of financial transactions, which people can use for their day-to-day activities as the need arises. For instance, mobile money is used to send and receive payments [15] and remittances from family, friends [17,18], and business partners. For example, our data show that 74% of users who have ever received mobile money received the most recent amount from family and friends, and the purposes for the receipt are 56% for daily personal expenses, 19% for business-related activities, 10% for health-related expenses, and 4% for educational purposes. Similarly, 85% of users who have ever sent mobile money sent the most recent amount to family and friends for the purpose of daily personal expenses (56%), business-related activities (15%), education purposes (16%), and health-related expense (3%). An explanation for these findings is that access to mobile money has increased the willingness of individuals to remit cash, as suggested by Batista and Vicente [19], Blumenstock, Eagle, and Fafchamps [18], and Munyegera and Matsumoto [15].

Second, using mobile money for payments means faster transactions, which may include income-generating transactions [8,9,19,20]. Facilitating transactions with convenience implies a higher volume of transactions within a unit of time, and hence, a positive impact on microbusinesses may arise, as suggested by Bauchet, Marshall, Starita, Thomas, and Yalouris [25], and Klapper, El-Zoghbi, and Hess [3]. We observe that our data also aligned with this finding, because apart from daily personal expenses, business-related activities are the next most important purpose for the most recent transactions by users. Nineteen percent (19%) of the mobile money received and 16% of the mobile money sent was for business-related activities. The implication is that, once mobile money transactions are used for business-related activities, it is likely that these activities may generate income for users, which can be a useful contribution towards sustainable development goal one: no poverty.

In relation to health, mobile money does not significantly affect investment in health, possibly because participants are not using mobile money to undertake health-related activities. For example, payment for health insurance, hospital bills, and over-the-counter prescriptions are paid for in cash.

In relation to savings, our data show that the mean amount saved in the mobile wallet by the most recent users of mobile-money savings devices is GH¢351.00, for an average of 40 days. The higher total savings by users could be explained by participating in mobile money providing access to a convenient saving mechanism [14]. Hence, mobile-money users can save on phones easily and have easy access to the liquidity of savings and more flexible control over their finances. Easy access to liquidity contributes to consumption-smoothing, reduces vulnerability, and sustains livelihood.

7. Conclusions

In this study, we analyzed the impact of mobile-money participation on individuals’ payments and investments. Using individual-level data from 388 mobile-money users and 169 non-users, mainly from the informal sector of the Ashanti Region in Ghana, we find that participation in mobile money has a positive effect on individuals’ payments, remittances, savings, micro-investments, and consumption. We find in Section 5.1 that mobile-money users have a relatively higher level of income than non-users; however, financial status is not a significant indicator in determining who participates in mobile money. Hence, currently, participants in mobile money are neither distinctly poor nor wealthy. People from any segment of society are equally participating in mobile money, and hence, mobile money is likely to benefit people from all segments of society, whether rich or poor, once participation is initiated.

However, we observe that among those who participate in mobile money, those who have greater financial assets are more likely to send and receive more payments and remittances. We find in Section 5.3.4 that access to mobile money is positively related to total savings. In conclusion, people have day-to-day financial transaction needs, and at each time, they decide on an available channel that grants them the best satisfaction transaction. The fast, easy, convenient, and cost-effective features provided by mobile money might have offered the potential for facilitating the process of meeting existing financial needs, which is a step towards reducing poverty, smoothing income, and achieving sustainability. The bottom line is that mobile money is contributing towards the sustainable development goals.

As for further work, this study could be used as the basis for further study to observe the short and long-term impacts of mobile money. This study used only one round of data in a non-experimental procedure to estimate impacts. While we employed PSM and inverse propensity-score weighting regressions to remove any biases that arise due to observable differences between users and non-users of mobile money, the underlying assumption for using these methods is that unobserved differences are not important for the outcomes. For future work, collecting multiple rounds of data over a period to create panel data or good instrumental variables is expected. Alternatively, a randomized control trial experiment could be conducted to estimate these impacts to determine whether the positive outcome is same. To perform a similar study in a different country, it is important to consider a higher sample size to ensure a stronger statistical power of the impact estimate.

Author Contributions

This paper is part of a more extensive research, a doctoral dissertation, prepared by E.K.A. and directed by A.S. The task of writing this paper was carried out by both authors.

Acknowledgments

The authors would like to express their sincere appreciation to KDDI Foundation for supporting this study with funds for fieldwork and for publishing.

Conflicts of Interest

The authors declare no conflict of interest. The founding sponsors had no role in the design of the study; in the collection, analyses, or interpretation of data; in the writing of the manuscript, and in the decision to publish the results.

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table A1.

Time Preference Game 1.

| Supposed That You Are to Choose between Two Amounts to Receive: a Smaller Amount Today and a Bigger Amount Later. Which Option Do You Prefer? | A or B | ||

|---|---|---|---|

| Option A, Today | Option B, in 3 Months’ Time | ||

| TP1 | GH¢10.00 | GH¢12 | |

| TP2 | GH¢10.00 | GH¢14 | |

| TP3 | GH¢10.00 | GH¢16 | |

| TP4 | GH¢10.00 | GH¢18 | |

| TP5 | GH¢10.00 | GH¢20 | |

| TP6 | GH¢10.00 | GH¢22 | |

| TP7 | GH¢10.00 | GH¢24 | |

| TP8 | GH¢10.00 | GH¢26 | |

| TP9 | GH¢10.00 | GH¢28 | |

| TP10 | GH¢10.00 | GH¢30 | |

Appendix B

Table A2.

Time Preference Game 2.

| Supposed That You Are to Choose between Two Amounts to Receive: a Smaller Amount Today and a Bigger Amount Later. Which Option Do You Prefer? | A or B | ||

|---|---|---|---|

| Option A, in 3 Months’ Time | Option B, in 6 Months’ Time | ||

| TP1 | GH¢10.00 | GH¢12 | |

| TP2 | GH¢10.00 | GH¢14 | |

| TP3 | GH¢10.00 | GH¢16 | |

| TP4 | GH¢10.00 | GH¢18 | |

| TP5 | GH¢10.00 | GH¢20 | |

| TP6 | GH¢10.00 | GH¢22 | |

| TP7 | GH¢10.00 | GH¢24 | |

| TP8 | GH¢10.00 | GH¢26 | |

| TP9 | GH¢10.00 | GH¢28 | |

| TP10 | GH¢10.00 | GH¢30 | |

Appendix C

Table A3.

Risk Game.

| Project A | Project B | A or B | ||

|---|---|---|---|---|

| You Obtain for Sure: | 50% Chance of Obtaining: | 50% Chance of Obtaining: | ||

| RG1 | GH¢5.00 | GH¢12.00 | GH¢0 | |

| RG2 | GH¢6.00 | GH¢12.00 | GH¢0 | |

| RG3 | GH¢7.00 | GH¢12.00 | GH¢0 | |

| RG4 | GH¢8.00 | GH¢12.00 | GH¢0 | |

| RG5 | GH¢9.00 | GH¢12.00 | GH¢0 | |

| RG6 | GH¢10.00 | GH¢12.00 | GH¢0 | |

| RG7 | GH¢11.00 | GH¢12.00 | GH¢0 | |

| RG8 | GH¢12.00 | GH¢12.00 | GH¢0 | |

Appendix D

Table A4.

Variables and their Definition.

| Variable | Definition | Unit of Measurement | Hypothesized Relationship |

|---|---|---|---|

| Outcome Variables | |||

| User | This is a categorical variable that indicates 1 if an individual has ever used mobile money to undertake any transaction, and 0 otherwise | Dummy | |

| Payment sent | The total value of money paid for goods and services received in the last 12 months | Continuous | |

| Payments received | The total value of money received for goods and services given out in the last 12 months | Continuous | |

| Remittances sent | The total value of cash and in-kind gift given out in the last 12 months, without expecting to be paid back | Continuous | |

| Remittances received | The total value of cash and in-kind gift received in the last 12 months, that would not be paid back | Continuous | |

| Investment in microbusiness | Total value of money spent to start, run a business, or acquire an asset for a business for income-generating activity | Continuous | |

| Investment in education | Total value of money spent by the respondent for educating him/herself, spouse, children, a household member, or any non-household member in the last 12 months | Continuous | |

| Investment in health | Total value of money spent by the respondent for him/herself, spouse, children, a household member, or non-household member | Continuous | |

| Savings | Total value of money saved in the last 12 months. | Continuous | |

| Consumption | Total value of money spent on food, water, electricity, gas, and rent, for him/herself and household members in the past 12 months | Continuous | |

| Independent variables | |||

| Age | This variable indicates how old an individual is. | Years | +/− |

| Male | This indicates the gender of an individual. 1 if the individual is a man, and 0 if the individual is a woman | dummy | +/− |

| Years of schooling | The number of years an individual spent formally in school | Years | + |

| Household size | The number of people living in a house together and sharing the same housekeeping arrangement | Discrete | + |

| Non-household dependents | Persons who do not belong to the household of the respondent; however, they depend on the respondent for a living. | Discrete | + |

| Married | Indicates the marital status of the respondent. 1 when the respondent is married, and 0 otherwise | Dummy | +/− |

| Minutes to the nearest vendor | Indicates the number of minutes of walk it takes the respondent to get to the nearest mobile-money service point | Minutes | − |

| Discount rate | This is the respondent’s individual discount rate, which is calculated based on his/or her rate of time preference. | Index | +/− |

| Present bias | The tendency of a respondent to give stronger weight to payoffs that are closer to now, than a future payoff. | Dummy | +/− |

| Risk-averse | Respondent preference to take risk | Index | − |

| Migrant | Indicates the migrant status of the respondent. 1 if a respondent is born in the Ashanti Region, and 0 otherwise | Dummy | + |

| Formal employment | Indicates whether the respondent is formally employed or not. 1 if a respondent is in formal employment, and 0 otherwise | Dummy | + |

| Self-employment | Indicates the self-employment status of a respondent. It is 1 if a respondent is self-employed and 0 otherwise. | Dummy | − |

| Years of work | Number of years a respondent has worked after school. | Years | + |

| First heard about mobile money (months ago) | Indicates the number of months since a respondent has heard about mobile money. | Months | + |

| Minutes to bank | The minutes of walk it takes a respondent to get to the nearest bank. | Minutes | + |

| Rural | Indicates a location dummy, 1, when the respondent lives in a rural area, and 0 otherwise. | Dummy | + |

| Urban | Indicates a location dummy, 1 if a respondent resides in an urban area, and 0 otherwise. | Dummy | − |

| Total financial | The value of total financial assets owned by the respondents | Continuous | + |

| Physical assets | The value of total physical assets owned by the household of the respondent | Continuous | + |

References

- Demirguc-Kunt, A.; Klapper, L.; Singer, D.; Van Oudheusden, P. The Global Findex Database 2014: Measuring Financial Inclusion around the World; World Bank Group: Washington, DC, USA, 2015. [Google Scholar]

- The World Bank Development Research Group, Better than Cash Alliance, & Bill & Melinda Gates Foundation. The Opportunities of Digitizing Payments How digitization of Payments, Transfers, and Remittances Contributes to the G20 Goals of Broad-Based Economic Growth, Financial Inclusion, and Women’s Economic Empowerment. 2014. Available online: http://siteresources.worldbank.org/EXTGLOBALFIN/Resources/85196381332259343991/G20_Report_Final_Digital_payments.pdf (accessed on 19 February 2018).

- Klapper, L.; El-Zoghbi, M.; Hess, J. Achieving the Sustainable Development Goals—The Role of Financial Inclusion; CGAP: Washington, DC, USA, 2016. [Google Scholar]

- Robert, C.; Tilman, E.; Nina, H. Financial inclusion and development: Recent impact evidence. Focus Note 2014, 92, 1–12. Available online: http://www.cgap.org/sites/default/files/FocusNote-Financial-Inclusion-and-Development-April-2014.pdf (accessed on 1 May 2018).

- Aghion, P.; Bolton, P. A Theory of Trickle-Down Growth and Development. Rev. Econ. Stud. 1997, 64, 151–172. [Google Scholar] [CrossRef]

- Beck, T.; Demirguc-Kunt, A.; Levine, R. Finance, Inequality, and the Poor. J. Econ. Growth 2007, 12, 27–49. [Google Scholar] [CrossRef]

- Angelucci, M.; Karlan, D.; Zinman, J. Microcredit impacts: Evidence from a Randomized Microcredit Program Placement Experiment by Compartamos Banco. Am. Econ. J. Appl. Econ. 2015, 7, 151–182. [Google Scholar] [CrossRef]

- Yunus, M. Creating a World without Poverty: Social Business and the Future of Capitalism. Glob. Urban Dev. 2008, 4, 1–19. [Google Scholar]

- Augsburg, B.; De Haas, R.; Harmgart, H.; Meghir, C. The impacts of microcredit: Evidence from Bosnia and Herzegovina. Am. Econ. J. Appl. Econ. 2015, 7, 183–203. [Google Scholar] [CrossRef]

- Banerjee, A.; Duflo, E.; Glennerster, R.; Kinnan, C. The miracle of microfinance? Evidence from a randomized evaluation. Am. Econ. J. Appl. Econ. 2015, 7, 22–53. [Google Scholar] [CrossRef]

- Crépon, B.; Devoto, F.; Duflo, E.; Parienté, W. Estimating the Impact of Microcredit on Those Who Take It up: Evidence from a Randomized Experiment in Morocco. Am. Econ. J. Appl. Econ. 2015, 7, 123–150. [Google Scholar] [CrossRef]

- Karlan, D.; Zinman, J. Microcredit in Theory and Practice: Using Randomized Credit Scoring for Impact Evaluation. Science 2011, 332, 1278–1284. [Google Scholar] [CrossRef] [PubMed]

- Evaluation, A.; Bank, W.; Support, G.; Inclusion, F.; Households, L. Financial Inclusion: A Foothold on the Ladder toward Prosperity? An Evaluation of World Bank Group Support for Financial Inclusion for Low-Income Households and Microenterprises. 2015. Available online: http://ieg.worldbankgroup.org/sites/default/files/Data/Evaluation/files/financialinclusion.pdf (accessed on 19 February 2018).

- Suri, T.; Jack, W. The long-run poverty and gender impacts of mobile money. Science 2016, 354, 1288–1292. [Google Scholar] [CrossRef] [PubMed]

- Munyegera, G.K.; Matsumoto, T. Mobile Money, Remittances, and Household Welfare: Panel Evidence from Rural Uganda. World Dev. 2016, 79, 127–137. [Google Scholar] [CrossRef]

- Jack, W.; Suri, T. Risk sharing and transactions costs: Evidence from Kenya’s mobile money revolution. Am. Econ. Rev. 2014, 104, 183–223. [Google Scholar] [CrossRef]

- Suri, T.; Jack, W.; Stoker, T.M. Documenting the birth of a financial economy. Proc. Natl. Acad. Sci. USA 2012, 109, 10257–10262. [Google Scholar] [CrossRef] [PubMed]

- Blumenstock, J.; Eagle, N.; Fafchamps, M. Risk Sharing over the Mobile Phone Network: Evidence from Rwanda. Available online: https://aae.wisc.edu/mwiedc/papers/2011/blumenstock_joshua.pdf (accessed on 23 February 2018).

- Batista, C.; Vicente, P.C. Introducing Mobile Money in Rural Mozambique: Evidence from a Field Experiment. Nova Africa. 2012. Available online: https://doi.org/10.2139/ssrn.2384561 (accessed on 1 May 2018).

- Aker, J.C.; Wilson, K. Can Mobile Money be used to Promote Savings? Evidence from Preliminary Research Northern Ghana. FEBS J. 2013, 281, 1–11. [Google Scholar]

- Dupas, P.; Robinson, J. Savings Constraints and Microenterprise Development: Evidence from a Field Experiment in Kenya. Am. Econ. J. Appl. Econ. 2013, 5, 163–192. [Google Scholar] [CrossRef]

- Collins, D.; Morduch, J.; Rutherford, S.; Ruthven, O. Portfolios of the Poor: How the World’s Poor Live on $2 a Day; Princeton University Press: Princeton, NJ, USA, 2009. [Google Scholar]

- Kelly, S.E.; Rhyne, E. By the Numbers. High-Performance Composites. Available online: https://doi.org/10.1038/scientificamerican0514-20a (accessed on 24 February 2018).

- Blumenstock, J.E.; Eagle, N.; Fafchamps, M. Airtime transfers and mobile communications: Evidence in the aftermath of natural disasters. J. Dev. Econ. 2016, 120, 157–181. [Google Scholar] [CrossRef]

- Dupas, P.; Robinson, J. Why don’ the poor save more? Evidence from health savings experiments. Am. Econ. J. Appl. Econ. 2013, 103, 1138–1191. [Google Scholar]

- Bauchet, J.; Marshall, C.; Starita, L.; Thomas, J.; Yalouris, A. Latest Findings from Randomized Evaluations of Microfinance. December 2011, pp. 1–27. Available online: https://www.cgap.org/sites/default/files/CGAP-Forum-Latest-Findings-from-Randomized Evaluations-of-Microfinance-Dec-2011.pdf (accessed on 24 February 2014).

- Bank of Ghana. Impact of Mobile Money on the Payment System in Ghana: An Econometric Analysis 2017. Available online: https://www.bog.gov.gh/privatecontent/Public_Notices/Impact of Mobile Money on the Payment Systems in Ghana.pdf (accessed on 13 October 2017).

- Page, M.; Molina, M.; Jones, G.; Makarov, D. The Mobile Economy. 2013. Available online: https://www.gsma.com/newsroom/wp-content/uploads/2013/12/GSMA-Mobile-Economy-2013.pdf (accessed on 24 February 2018).

- Holt, C.A.; Laury, S.K. Risk Aversion and Incentive Effects. Am. Econ. Rev. 2002, 92, 1644–1655. [Google Scholar] [CrossRef]

- Tanaka, T.; Camerer, C.F.; Nguyen, Q. Risk and Time Preferences: Linking Experimental and Household Survey Data from Vietnam. Am. Econ. Rev. 2010, 100, 557–571. [Google Scholar] [CrossRef]

- Tanaka, Y.; Munro, A. Regional variation in risk and time preferences: Evidence from a large-scale field experiment in rural Uganda. J. Afr. Econ. 2014, 23, 151–187. [Google Scholar] [CrossRef]

- Tobbin, P.; Kuwornu, J.K. Adoption of Mobile Money Transfer Technology: Structural Equation Modeling Approach. Eur. J. Bus. Manag. 2011, 3, 59–78. [Google Scholar]

- Bauer, H.H.; Reichardt, T.; Barnes, S.J.; Neumann, M.M. Driving consumer acceptance of mobile marketing: A theoretical framework and empirical study. J. Electron. Commer. Res. 2005, 6, 181–192. [Google Scholar]

- Caliendo, M.; Kopeinig, S. Some Practical Guidance for the Implementation of Propensity Score Matching. J. Econ. Surv. 2008, 22, 31–72. [Google Scholar] [CrossRef]

- Ravallion, M. Chapter 59 Evaluating anti-poverty programs. In Handbook of Development Economics; Development Research Group, The World Bank: Washington, DC, USA, 2007; Volume 4, pp. 3787–3846. ISBN 978-0-44-453100-1. [Google Scholar]

- Heckman, J.J.; Ichimura, H.; Todd, P. Matching as an Econometric Evaluation Estimator. Rev. Econ. Stud. 1998, 65, 261–294. [Google Scholar] [CrossRef]

- Wooldridge, J.M. Inverse probability weighted estimation for general missing data problems. J. Econ. 2007, 141, 1281–1301. [Google Scholar] [CrossRef]

- Robins, J.M.; Rotnitzky, A. Semiparametric Efficiency in Multivariate Regression Models with Missing Data. J. Am. Stat. Assoc. 1995, 90, 122–129. [Google Scholar] [CrossRef]

- Hirano, K.; Imbens, G.W.; Ridder, G. Efficient Estimation of Average Treatment Effects Using the Estimated Propensity Score. Econometrica 2003, 71, 1161–1189. [Google Scholar] [CrossRef]

- Hirano, K.; Imbens, G. Estimation of causal effects using propensity score weighting: An application to data on right heart catheterization. Health Serv. Outcomes Res. Methodol. 2001, 2, 259–278. [Google Scholar] [CrossRef]

- Suzuki, A.; Mano, Y.; Abebe, G. Earnings, Savings, and Happiness from Working in a Labor-intensive Export Sector: Unskilled Workers in the Cut Flower Industry in Ethiopia. 2016. Available online: https://editorialexpress.com/cgibin/conference/download.cgi?db_name=CSAE2016&paper_id=701 (accessed on 1 February 2018).

Figure 1.

Graph of mobile money accounts vs. formal bank accounts in Ghana. Source: Bank of Ghana 2017 [27].

Figure 1.

Graph of mobile money accounts vs. formal bank accounts in Ghana. Source: Bank of Ghana 2017 [27].

Figure 2.

Graph of number of active mobile money agents or vendors or service points in Ghana. Source: Authors’ drawing from Bank of Ghana’s raw data in 2017.

Figure 2.

Graph of number of active mobile money agents or vendors or service points in Ghana. Source: Authors’ drawing from Bank of Ghana’s raw data in 2017.

Figure 3.

Graph of value of transactions per year in the mobile money space. Source: Authors computation from Bank of Ghana’s raw data in 2017.

Figure 3.

Graph of value of transactions per year in the mobile money space. Source: Authors computation from Bank of Ghana’s raw data in 2017.

Figure 4.

Graph of balancing test: propensity scores by group. Source: Authors computation from field data collected in 2016.

Figure 4.

Graph of balancing test: propensity scores by group. Source: Authors computation from field data collected in 2016.

Table 1.

Socio-economic Variables of Respondents.

| Variable | 1 Mobile-Money Users (N = 388) | 2 Non-Users (N = 169) | 3 p-Value of Difference |

|---|---|---|---|

| Age (years) | 31.5 | 35.2 | 0.00 *** |

| (11.18) | (14.29) | ||

| Education (years) | 9.62 | 7.54 | 0.00 *** |

| (3.86) | (4.41) | ||

| Gender (1 = male) | 0.5 | 0.56 | 0.19 |

| (0.50) | (0.50) | ||

| Married (1 = yes) | 0.39 | 0.52 | 0.01 ** |

| (0.49) | (0.50) | ||

| Migrant (1 = yes) | 0.32 | 0.34 | 0.67 |

| (0.47) | (0.48) | ||

| Risk-averse (1–8: 8, most risk-averse) | 7.24 | 7.18 | 0.81 |

| (2.25) | (2.29) | ||

| Discount rate | 0.33 | (0.34) | 0.24 |

| (0.16) | (0.16) | ||

| Present bias | −0.02 | −0.003 | 0.15 |

| (0.12) | (0.14) | ||

| Minutes of walk to the nearest vendor | 4.17 | 4.94 | 0.08 * |

| (4.29) | (5.42) | ||

| Household size | 3.53 | 3.22 | 0.12 |

| (2.22) | (2.12) | ||

| Non-household dependents | 0.48 | 0.39 | 0.15 |

| (0.67) | (0.60) | ||

| Employment status | 0.86 | 0.85 | 0.59 |

| (0.02) | (0.36) | ||

| Work experience (years) | 6.13 | 8.53 | 0.01 ** |

| (9.09) | (10.44) | ||

| First heard about mobile money (months ago) | 43.1 | 32.96 | 0.00 ** |

| (20.68) | (20.33) | ||

| Percentage of friends on mobile money | 67.6 | 50.8 | 0.00 *** |

| (4.89) | (2.85) |

Standard deviations in parentheses. *** p < 0.01, ** p < 0.05, * p < 0.1.

Table 2.

Other Variables of Respondents.

| Variable | 1 Mobile-Money Users (N = 388) | 2 Non-Users (N = 169) | 3 p-Value of Difference |

|---|---|---|---|

| Ownership of Bank Account | 0.61 | 0.37 | 0.00 *** |

| (0.49) | (0.49) | ||

| Ownership of Mobile-Money Account | 0.54 | 0.02 | 0.00 *** |

| (0.50) | (0.13) | ||

| Payments Sent (last 30 days (GH¢)) | 1945.26 | 1062.51 | 0.00 *** |

| (2888.24) | (1201.32) | ||

| Payments Sent (last 12 months (GH¢)) | 15,133.86 | 7727.41 | 0.04 * |

| (45,538.13) | (7895.03) | ||

| Mobile Money Sent (all transactions, last 12 months (GH¢)) | 453.6 | 0 | 0.07 * |

| (3347.28) | |||

| Mobile Money Received (all transactions last 12 months (GH¢)) | 375.63 | 0 | 0.08 * |

| (2785.29) | |||

| Respondents’ Income (last 30 days (GH¢)) | 786.05 | 367.68 | 0.02 * |

| (2238.83) | (592.59) | ||

| Respondents’ Income (last 12 months (GH¢)) | 9249.30 | 5868.09 | 0.01 ** |

| (15,236.96) | (8065.06) | ||

| Remittance and Gifts Sent (last 12 months (GH¢)) | 285.97 | 141.24 | 0.00 *** |

| (527.40) | (317.60) | ||

| Remittance and Gifts Received (last 12 months (GH¢)) | 322.99 | 144.09 | 0.00 *** |

| (589.67) | (327.15) | ||

| Investment in Micro-Enterprise, Land, and Buildings | 4510.73 | 702.81 | 0.23 |

| (41,434.89) | (2190.07) | ||

| Investment in Education (last 12 months (GH¢)) | 1533.92 | 972.96 | 0.23 |

| (5799.43) | (2550.15) | ||

| Investment in Health (GH¢) | 390.17 | 347.36 | 0.60 |

| (856.85) | (969.08) | ||

| Total Savings (GH¢) | 1500.36 | 447.73 | 0.11 |

| (8643.36) | (1606.36) | ||

| Total Financial Assets (GH¢) | 1572.63 | 1051.41 | 0.13 |

| (4345.09) | (1591.46) | ||

| Household Total Physical Assets (GH¢) | 603,210 | 1,398,726 | 0.39 |

| (4,714,307) | (16,900,000) | ||

| Consumption (last 30 days in (GH¢)) | 571.84 | 453.84 | 0.01 * |

| (555.99) | (374.34) | ||

| Consumption (last 12 months in (GH¢)) | 5409.31 | 4126.36 | 0.03 * |

| (7347.99) | (4605.49) |

Standard deviations in parentheses. *** p < 0.01, ** p < 0.05, * p < 0.1.

Table 3.

Probit Estimate of Factors Influencing Mobile Money Participation (Marginal Effect).

| Variables | 1 (Logit) | 2 (Probit) |

|---|---|---|

| User | User | |

| ln (Financial assets) | 0.028 | 0.016 |

| (0.067) | (0.039) | |

| Age | −0.017 * | −0.011 * |

| (0.010) | (0.006) | |

| Male | −0.572 *** | −0.330 *** |

| (0.211) | (0.123) | |

| Years of schooling | 0.103 *** | 0.062 *** |

| (0.027) | (0.016) | |

| Household size | 0.147 ** | 0.082 ** |

| (0.059) | (0.033) | |

| Non-household dependents | 0.335 ** | 0.201 ** |

| (0.165) | (0.095) | |

| Married | −0.497 ** | −0.287 ** |

| (0.246) | (0.145) | |

| Minutes to the nearest vendor | −0.034 * | −0.020 * |

| (0.020) | (0.012) | |

| First heard about mobile money (months ago) | 0.025 *** | 0.014 *** |

| (0.006) | (0.003) | |

| Discount rate | −0.485 | −0.325 |

| (0.690) | (0.412) | |

| Present bias | −1.040 | −0.607 |

| (0.872) | (0.516) | |

| Risk-averse | 0.004 | 0.002 |

| (0.043) | (0.026) | |

| Constant | −0.429 | −0.200 |

| (0.710) | (0.412) | |

| Pseudo R2 | 0.121 | 0.120 |

| Observations | 557 | 557 |

Robust standard errors in parentheses. *** p < 0.01, ** p < 0.05, * p < 0.1.

Table 4.

Ordinary Least Squares (OLS) of Factors Influencing Level of Participation in Mobile Money.

Table 4.

Ordinary Least Squares (OLS) of Factors Influencing Level of Participation in Mobile Money.

| Variable | (1) |

|---|---|

| ln (Amount through Mobile Money) | |

| ln (Financial assets) | 0.198 ** |

| (0.0955) | |

| Age | 0.0148 |

| (0.0184) | |

| Male | −0.517 |

| (0.327) | |

| Years of schooling | 0.0333 |

| (0.0415) | |

| Household size | 0.117 |

| (0.0792) | |

| Non-household dependents | 0.980 *** |

| (0.267) | |

| Married | −0.378 |

| (0.418) | |

| Minutes to the nearest vendor | −0.0262 |

| (0.0397) | |

| First heard about mobile money (months ago) | 0.0194 *** |

| (0.00746) | |

| Discount rate | 0.892 |

| (1.067) | |

| Present bias | −0.752 |

| (1.361) | |

| Risk-averse | 0.0578 |

| (0.0640) | |

| Constant | −1.652 |

| (1.120) | |

| Observations | 388 |

| R-squared | 0.089 |

Robust standard errors in parentheses. *** p < 0.01, ** p < 0.05, * p < 0.1.

Table 5.

Matching Methods and Balancing Test.

| No. of Significant Variable | Pseudo R2 | p-Value LR * Test | Mean Bias | |

|---|---|---|---|---|

| Impact of Mobile Money on | ||||

| Payments Sent | ||||

| Before matching | 5 | 0.120 | 0.000 | 20.0 |

| Kernel common trim (0.1) | 1 | 0.007 | 0.854 | 4.6 |

| Radius caliper (0.1) | 1 | 0.006 | 0.902 | 4.3 |

| Payments Received | ||||

| Before matching | 5 | 0.120 | 0.000 | 20.0 |

| Kernel common trim (0.1) | 0 | 0.004 | 0.972 | 4.0 |

| Radius caliper (0.1) | 1 | 0.006 | 0.902 | 4.3 |

| Remittance Sent | ||||

| Before matching | 5 | 0.120 | 0.000 | 20.0 |

| Kernel common trim (0.1) | 0 | 0.004 | 0.972 | 4.0 |

| Radius caliper (0.1) | 1 | 0.006 | 0.902 | 4.3 |

| Remittance Received | ||||

| Before matching | 5 | 0.120 | 0.000 | 20.0 |

| Kernel common trim (0.1) | 0 | 0.004 | 0.972 | 4.0 |

| Radius caliper (0.1) | 1 | 0.006 | 0.902 | 4.3 |

| Investment in Microbusiness | ||||

| Before matching | 5 | 0.120 | 0.000 | 20.0 |

| Kernel common trim (0.1) | 0 | 0.004 | 0.972 | 4.0 |

| Radius caliper (0.1) | 1 | 0.006 | 0.902 | 4.3 |

| Investment in Education | ||||

| Before matching | 5 | 0.120 | 0.000 | 20.0 |

| Kernel common trim (0.1) | 0 | 0.004 | 0.972 | 4.0 |

| Radius caliper (0.1) | 1 | 0.006 | 0.902 | 4.3 |

| Investment in Health | ||||

| Before matching | 5 | 0.120 | 0.000 | 20.9 |

| Kernel common trim (0.1) | 0 | 0.004 | 0.972 | 4.0 |

| Radius caliper (0.1) | 1 | 0.006 | 0.902 | 4.3 |

| Savings | ||||

| Before matching | 5 | 0.120 | 0.000 | 20.0 |

| Kernel common trim (0.1) | 0 | 0.004 | 0.972 | 4.0 |

| Radius caliper (0.1) | 1 | 0.006 | 0.902 | 4.3 |

| Consumption | ||||

| Before matching | 5 | 0.120 | 0.000 | 20.2 |

| Kernel common trim (0.1) | 0 | 0.004 | 0.968 | 4.2 |

| Radius caliper (0.1) | 1 | 0.006 | 0.914 | 4.3 |

* LR is log likelihood ratio.

Table 6.

Propensity-Score Matching (PSM) Results of Mobile Money on Domestic Payments and Investments.

Table 6.

Propensity-Score Matching (PSM) Results of Mobile Money on Domestic Payments and Investments.