Inclusive Finance, Human Capital and Regional Economic Growth in China

1

School of Economics, Fudan University, Shanghai 200433, China

2

Chongqing Dajiang Sub-branch, Agricultural Bank of China, Chongqing 401320, China

3

School of Finance, Shanghai University of Finance and Economics, Shanghai 200433, China

4

School of Business Administration, Zhongnan University of Economics and Law, Wuhan 430073, China

*

Author to whom correspondence should be addressed.

†

These authors contributed equally to this work.

Sustainability 2018, 10(4), 1194; https://doi.org/10.3390/su10041194

Submission received: 1 February 2018

/

Revised: 8 April 2018

/

Accepted: 11 April 2018

/

Published: 16 April 2018

(This article belongs to the Section Economic and Business Aspects of Sustainability)

Abstract

:Inclusive finance is an important financial development strategy in the world. The promoting effect of the human capital on economic growth has also gained theoretical and empirical support. This paper attempts to deeply examine the interaction among inclusive finance, human capital and regional economic growth as well as their mutual influence mechanism. To the end, data of 31 provinces and cities from 2005 to 2015 were chosen to build a corresponding panel data template. Meanwhile, the fixed effect model was adopted for an empirical test. Results suggest the following. (1) Inclusive finance and human capital can exert a significantly positive promoting effect on regional economic growth. The influence of inclusive finance on regional economic growth is more obvious, while the nonlinear influence of human capital is more significant; (2) Inclusive finance is observed to have a significantly negative influence on economic growth of China’s central region (mainly referring to eight provinces, including Shanxi). The positive promoting effect of inclusive finance on economic growth of China’s west region (mainly referring to 12 provinces and cities, including Chongqing) is found to be the most significant. Differently, human capital exerts the most significantly promoting effect on China’s central region. The economic development level differs in different regions of China. As an increasing number of talent resources gather in the central and western region of China and the financial system is built in the two regions, resource optimization has become a necessity, which is the linchpin to China’s sustainable economic development.

1. Introduction

Along with continuous development of China’s economy, differentiation of regional economy has gradually become an important factor restricting a country’s overall economic development. This problem is mainly reflected as slow development of finance in rural areas, funding difficulties of small- and medium-sized enterprises, disproportional distribution of talent resources, etc. All this has resulted in a widening gap of regional economic development. To alleviate funding difficulty of micro-, small- and medium-sized enterprises and to promote rural financial development, inclusive finance was put forward for the first time in the International Year of Microcredit 2005. Its purpose is to improve service quality and clients of financial institutions by increasing depth and breadth of financial services and building corresponding inclusive finance institutions. To traditional economic theories, the functioning mechanism of financial institutions is, to some extent, independent. This results in a major difference in the influence of financial institutions of different types. It is apt to say that emergence of inclusive finance has largely alleviated the difficulty of how to more accurately analyze influence of financial institutions on different industries. Not only can service quality of financial institutions be more effectively measured, but also the service scope of financial institutions can be macroscopically measured. With construction of the inclusive finance system, economic activities have obtained more and more financial resources, thus creating more and more opportunities for economic development. This also demonstrates the promoting effect of inclusive finance on sustainable regional economic development [1].

Besides, talent resources are another essential factor influencing regional economic development. In traditional economic theories, labor is a major influencing factor. However, China’s current regional economic development is faced with a serious restriction of talent resources. Disproportional distribution of talent resources has in some way seriously impeded promotion of productivity. Although China’s economy has been ushered into a stably transitional period, the economic development status of China’s eastern coastal areas and west inland areas suggest that the gap in talent resource distribution has imposed a significant influence on regional economy, which deprives sustainable regional economic development of a solid foundation [2].

Seen from the point of view of the financial system and talent resources, differences of the financial environment and disproportionality of talent resource distribution can both influence regional industry development, and, as a result, sustainable regional economic development might either be promoted or impeded. How to find the influence mechanism of financial service factors and talent resource factors on regional economic development has become an issue of great concern to sustainable development of regional industries. This paper proceeds from financial service and talent resources to examine the influence among inclusive finance, human capital and China’s regional economic growth. It is observed that the influence mechanism of inclusive finance and human capital differs in the economic development process of different regions. Meanwhile, corresponding policy suggestions are proposed to alleviate the widening gap of China’s economic development to ensure sustainable development of China’s economy.

To better realize optimal allocation of financial resources and talent resources, this paper proceeds from the perspective of financial service and talent development to examine the relationship among inclusive finance, human capital and China’s regional economic growth. It is hoped that the mechanism through which inclusive finance and human capital influences China’s regional economic growth can be found. The influence mechanism can provide a theoretical basis for China’s financial system construction and talent resource deployment, through which the widening gap of China’s regional economic development can be mitigated, and sustainable development of China’s economy can be ensured.

The structural arrangement of this paper is as follows: Section 2 is the literature review; Section 3 is the measurement of inclusive finance and human capital; Section 4 includes data, variables and the model; Section 5 is the empirical test; and Section 6 is the conclusions and suggestions for future research.

2. Literature Review

The concept of inclusive finance was first introduced in the event of International Year of Microcredit 2005, known as the “inclusive financial system”, and the definition with a high degree of recognition is given as follows: the customer group of the financial industry should include individual users and business users, and financial services need to be more inclusive to promote financial services to help more vulnerable economic groups. The focus of research results of inclusive finance lies in the use of inclusive finance and that inclusive finance affects regional economy. Since there exist relatively large differences in the rural financial development among eastern, central and western China, which leads to the imbalance of economic development, to ease and improve the problem, it is obligatory to vigorously advance the concept of inclusive finance and perfect the financial system in the western region [3]. As there are serious internal defects in China’s microfinance industry, which has inhibited the financial market and hindered the development of the overall economy, the key to solving this problem is to give full play to the role of inclusive finance. Guo and Ding (2015) [4] analyzed the development status of inclusive finance in different countries from the perspective of the banking industry and found that economic development and financial awareness will produce a serious impact on the development of inclusive finance. He and Miao (2015) [5] believed that both exclusion and inclusion contained in the inclusive financial system have an impact on economic development, and the development of inclusive finance would contribute to build and perfect the financial system.

Furthermore, the study on the impact of inclusive finance on regional economy is gradually valued by researchers in recent years. Gabor and Brooks (2017) [6] and Park and Shin (2017) [7] analyzed the impact of diversity, hierarchy and functional comprehensiveness of inclusive finance on regional economy according to the inherent meaning of inclusive finance. Wang and Guan (2017) [1] measured the development level of inclusive finance around the world with the index of inclusive finance and drew the conclusion that personal income, education degree and information interaction rate are the important factors affecting financial development, and, to construct an inclusive financial system, it is supposed to consider the financial depth and banking stability level. Corrado and Corrado (2017) [8] analyzed the inclusion of inclusive finance as well as its development process, and pointed out that the inclusive financial system can provide better development opportunities for regional economic activities, and it is the key element of sustainable economic development. Dupas and Robinson (2013) [9] used the operating frequency of personal financial accounts to analyze the impact of financial services on regional economy and found that inclusive finance can produce a significant impact on employment, consumption and production. Ayyagari et al. (2011) [10] found that the inclusive nature of financial services can guarantee a fairly good social credit level, maintain long-term consumption and investment plans, and then promote the development of regional economy. Anzoategui et al. (2014) [11] analyzed the impact of inclusive finance on personal savings behaviors with family investigation data, and pointed out that inclusive finance would exert a marked impact on exchange, and developing inclusive finance can radically enhance the degree of trust between individual users and financial institutions. Beck et al. (2007) [12] believed that the establishment and improvement of the inclusive financial system can enhance the utilization efficiency of social resources from the macro level, and it has the trend of changing with economic development in an equidirectional way. Sarma and Pais (2011) [13] pointed out that inclusive finance is relatively closely linked with employment rate, urbanization and cultural development. As indicated in the results of the current research, inclusive finance can measure the development level of regional financial industry fairly well, but the development of the financial industry can only reflect the impact of capital on the overall economy, so it is necessary to comprehensively discuss the action mechanism of inclusive finance in the development process of regional economy from the perspective of internal elements of regional economy.

In China, Wang and Hu (2013) [14] pointed out that the construction of the inclusive financial system will also improve regional income disparities and enhance the implementation effect of macro-financial strategies. Du and Pan (2016) [15] discovered that there is an inverted U-shaped relationship between inclusive finance and regional economy on a national scale, but influencing mechanisms of all regions are different to a relatively larger extent. Li et al. (2016) [16] made use of cross-sectional data from different countries and found that investment funds from the bank’s corporate proportion index has a significant impact in impeding economic development, but, with the improvement of life quality, the positive role of inclusive finance would gradually increase. Lu et al. (2017) [17], by comparing the factors of influencing regional differences of inclusive finance, concluded that the overall level of inclusive finance in China is relatively low, but it is obviously better in the eastern region than that in other regions, and the relationship between inclusive finance and regional economic growth presents an inverted U-shaped relationship.

Since the 1960s, the focus of research on human capital has gradually shifted from the calculation method of human capital into the influencing mechanism of human capital on economic growth. Kalaitzidakis et al. (2001) [18] pointed out that the nonlinear influencing mechanism of human capital on economic growth gradually receives the attention of researchers. Such a nonlinear effect can well explain the incidence relation between the accumulation of human capital and the development of regional economy. Mamuneas et al. (2006) [19] discovered that, after the stock of human capital has reached a certain threshold value, human capital can significantly play a positive role in promoting the development of regional economy. By comparing the influence of educational background and technological innovation on economic growth, respectively, Lin (2013) [20] observed that educational background has a stronger promoting effect on economic growth. Besides, Lin (2004) [21] contrastively studied the influence of educational degree and labor force on economic growth, finding that the promoting effect of education of different subjects on economic activities shows significant difference. Wang et al. (2016) [22] pointed out the influencing mechanism generated by human capital needs to be accumulated in terms of time dimension, while human capital has a significant positive role in promoting regional economic growth. Kraekel (2016) [23] analyzed the impact of the input method of human capital on corporate performance and discovered that general education form can enhance employees’ output more effectively and have an obvious effect in promoting the enterprise’s long-term development. Murphy and Topel (2016) [24] discovered that the input of human capital has had difficulty keeping pace with the technical needs of economic development; the accumulated human capital as well as the growth speed can exert a significant impact on economic growth, while the inequality of human capital will play a corresponding inhibiting role. Cavalcanti and Giannitsarou (2017) [25] discovered that human capital relies on educational inputs as well as the intensity of interpersonal networks and that a highly aggregated network state can effectively enhance the impact of human capital on the output of economic activities.

In China, the research on human capital has long been the focus of attention in the fields of management science and economics, and, due to the particularity of China’s economic system, domestic research on the application of human capital in economic theories starts relatively late and has been gradually able to form the research system of human capital with structural features of the Chinese market as the core. In the neoclassical growth model of human capital accumulation, the impact of human capital on economic growth would expanded along with time dimension, while more investment level would affect the stock of human capital. Bai (2013) [26] explored the relationship between human capital and economic growth and concluded that employed persons with a higher education level can significantly promote the growth of regional economy. According to the spillover theory of knowledge, there are differences among the impacts of different education levels on regional economic growth. The impact of primary education is directly reflected in the productivity elements, while the impact of higher education is directly reflected in technological innovation. Du et al. (2014) [27] studied the incidence relation between human capital and regional economic growth in respect of promoting mechanism and discovered that the promoting role of human capital on economic growth is not significant but can directly affect the development level of regional technological innovation. Wang and Zhu (2016) [28], combined with externality theory of human capital threshold, found that a significant influence relationship between threshold effect of the accumulation of human capital and regional economy exists. Thus, it can be seen that, in the existing research achievements of human capital, measurement methods of human capital are mostly concentrated on the measuring the education degree of labor force, which reflects the significance of investment in professional skills at the level of technological innovation.

By sorting out the results of domestic and foreign research on inclusive finance and economic growth and human capital and economic growth, it can be perceived that few studies considered the impact of inclusive financial and human capital on regional economy simultaneously. In the existing literature, Li et al. (2016) [16] have explicitly pointed out that inclusive finance would be affected by the level of education, thus making it difficult for financial services to play the core role. In the related research of inclusive finance, researchers tend to pay more attention to the inclusiveness reflected by inclusive finance in economic activities but ignore the potential influencing factors brought by the compatibility of the financial system. In the related research of human capital, Su and Liu (2016) [2] regarded the input of labor force training as a measure of human capital, and this method would be partly influenced by macroeconomic factors such as price levels, resulting in that there exists a significant causal relationship between human capital and the development of regional economy. Many studies have begun to return the focus of research to the perspective of basic elements and the factors of capital and labor force have become the focus of attention of many researchers. As the basic elements of economic activities, all economic activities need to be built on capital and labor force factors, and exploring the influencing mechanisms of inclusive finance and human capital on economic activities can offer more perfect guiding suggestions for the development of real economy.

Unlike the existing research, this study made progress in the following two aspects. On the one hand, under the background that China’s regional economy develops in an unbalanced manner, implementing inclusive finance and upgrading technical innovation strategies boost the coordinated development of regional economy; by analyzing the interrelation among inclusive finance, human capital and regional economic growth, this study revealed the influencing mechanism of inclusive finance and human capital on regional economic growth, which, to some extent, overcomes the deficiency of previous research that only studied the impact on regional economic growth unilaterally from inclusive finance or human capital. On the other hand, the study found that both inclusive finance and human capital produce a significant positive effect in stimulating regional economy; the influencing effect of inclusive finance seems to be more obvious while human capital produces a more significant nonlinear effect. Meanwhile, inclusive finance exerts a significant negative impact in the central region, and its positive impact in the western region is the strongest while the positive promoting impact of human capital in the central region is the strongest.

3. Measure of Inclusive Finance and Human Capital

3.1. The Relationship among Inclusive Finance, Human Capital and Regional Economy

In the development of regional economy, the perfection and inclusiveness of the financial system embodied by inclusive finance can bring more abundant financial services for more consumers, which means the process of regional capital flow does not merely run through the capital operation of large enterprises, but can also solve the financial difficulties of small- and middle-sized enterprises. The proposal of inclusive finance advances the diversified development of regional industry to a large extent, brings more development opportunities for micro-, small- and medium-sized enterprises and effectively promotes the development of rural finance to enrich regional economic activities.

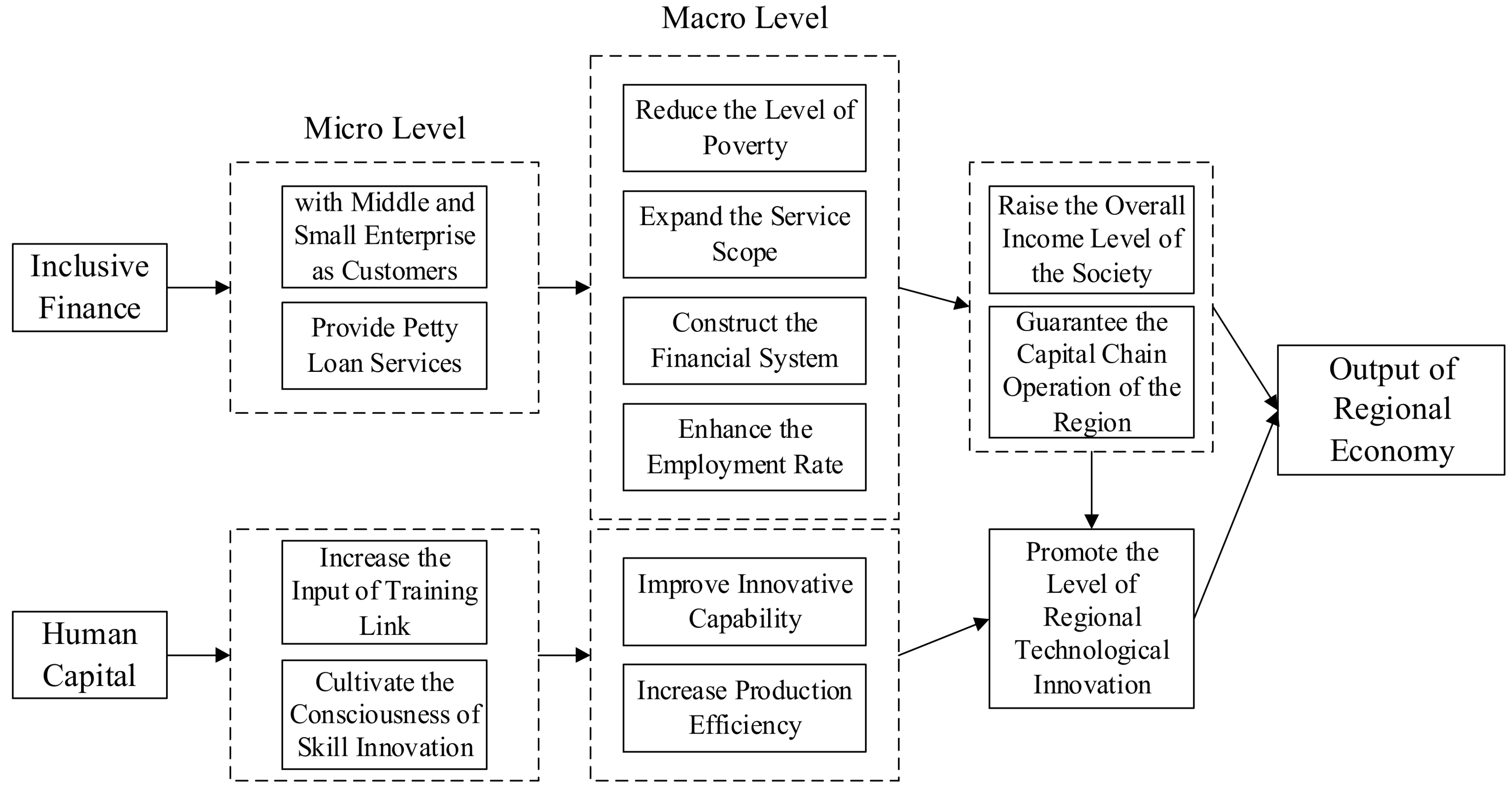

Furthermore, the comprehensive capacity of labor force embodied by human capital would be directly reflected in the link of the output of economic activities, and more training input quantity can greatly upgrade the innovative consciousness of labor force itself so that productivity can be significantly improved. From the perspective of regional economic output, both inclusive finance and human capital can positively drive the output of economic activities, and the logical relationship among the three is shown in Figure 1.

Inclusive finance and human capital play different roles in regional economic activities, but there also exists an influence relationship between the two. At the micro level, inclusive financial system will provide petty loans for more micro-, small- and medium-sized enterprises, which can improve the utilization efficiency of regional funds more effectively, and alleviate the financial difficulties of low-income groups. By contrast, human capital concentrates more on the training input of labor force so that participants of economic activities can have a stronger innovative consciousness. At the macro level, inclusive finance can effectively reduce the level of poverty, raise the overall social income, and solve the financial problems of specific enterprises. Besides, it accelerates the flow rate of regional capital chain, and exerts a positive effect on the innovation level of regional technologies embodied by human capital. It is worth noting that, although inclusive finance and human capital can affect regional economic output from financial services and technological innovation, the broader customer group of financial services may bring a vicious circle of capital chain, making many troubled assets appear in regional economic activities, and then have a certain negative impact. Therefore, the purpose of this paper is to test the relationships among inclusive finance, human capital and regional economic growth to verify the theoretical logic relationship among the three.

3.2. Measure of Inclusive Finance

Inclusive finance is an index to measure the quality of financial services provided by regional financial institutions and the scope of their audience, and the core value of the index lies in the impact of financial services on various social groups or enterprises. Considering the particularity of China’s economic structure, when preparing the index system of inclusive finance, it is supposed to exhibit the characteristics of the financial industry more comprehensively, and display the comprehensiveness of financial services, the balanced development of financial institutions and the sustainability of the financial environment. This requires that the index system of inclusive finance include a variety of different financial industries to enhance the intrinsic diversity characteristics of inclusive finance.

In the process of constructing the index system of inclusive finance, based on the definition of the concept of inclusive finance given by international organizations as well as the method of constructing the index system of inclusive finance in existing literature, financial services put forward by Beck et al. (2007) [12] in the research results should be accessible, usable and effective. Moreover, Lu et al. (2017) [17] pointed out that there should be a certain receptivity in the application of financial services. Therefore, this paper constructs the index system for measuring the index of inclusive finance from the following four dimensions (Table 1).

The index system of inclusive finance in China mainly includes availability dimension of financial services, usability dimension of financial services, utility dimension of financial services and receptivity dimension of financial services, of which the first three are all positive indexes while the last one is a negative index. The higher the value of a positive index is, the better the dimension is. The lower the value of a negative index is, the better the dimension is.

Among the accessibility dimensions of financial service, two indexes, namely the number of financial institution branches and the number of practitioners, can demonstrate the service scope of financial institutions from the perspective of customer groups and measure accessibility of financial service.

Among the use dimensions of financial service, the per capita resident savings can reflect residents’ use degree of service of financial institutions, while insurance penetration and density can indicate the use status of financial service provided by the insurance industry. The usability of financial service can well reflect the actual participation degree of financial system participants. Saving service and insurance service are at the core of most participants’ demands.

Among the utility dimensions of financial service, the percentage of outstanding deposit in GDP and the percentage of outstanding loan in GDP can suggest from the social perspective the role of financial service in economic activities.

Among the affordability dimensions of financial service, the percentage of non-financial institutions’ financing amount in GDP can show the financing difficulty of regular financial institutions and the degree of industrial competition of financial service.

Based on the evaluation indexes contained in four different dimensions of the index of inclusive finance, this paper puts forward the calculating methods of the index of inclusive finance in light of the calculating methods of human development indexes proposed by Based on Sarma and Pais (2011) [13], combined with the standardized processing of different indexes by Lu et al. (2017) [17], Zhou et al. (2017) [29] as well as the weight measurement methods:

- (1)

- The standardized processing of various dimension indexes. To more intuitively display the differences of various dimension indexes at the regional level and avoid the impact of indexes in the order of magnitudes, standardized processing was carried out for every dimension index, which includes processing of positive indexes and processing of negative indexes:where Formula (1) is the standardized processing of positive indexes while Formula (2) presents the standardized processing of negative indexes. represents the k index value of i province in year t, refers to the value after goes through standardized processing, is the maximum value of the k index in year t, and stands for the minimum value of the k index in year t.

- (2)

- Calculation of the weight of each dimension. To measure the importance of different dimensions of different indexes of inclusive finance, the coefficient of variation method was used to calculate the weight of each dimension, and the calculation formula is as follows:where represents the coefficient of variation of the k index in year t, represents the standard deviation of the k index in year t, represents the mean value of the k index in year t, and stands for the weight of the k index in year t.

- (3)

- Calculation of measure values of all dimensions. To show the characteristics of measure values of all dimensions more intuitively, the index value that underwent standardized processing in each region was multiplied by the weight of each dimension, thereby obtaining the measure value of each dimension:

- (4)

- Calculation of the index of inclusive finance. This study used the calculation method of human development indexes to calculate the index of inclusive finance correspondingly to exhibit the service quality and customer group scope of financial institutions at the macro level, and the calculation formula is as follows:where represents the index of inclusive finance of i province in year t, and . The higher the index of inclusive finance is, the better the development situation of inclusive finance in the region is.

3.3. Measure of Human Capital

Human capital plays a vital role in the development of economics theories, while, based on research achievements related to human capital and economic growth, it can be observed that the measure of human capital has always been an important factor influencing this index. Among the existing research results of human capital, enrollment rate and adult literacy rate were once the measuring standards adopted by many researchers, but the interpretation of economic output by these two measuring methods seems to be quite limited. In the process of constructing the evaluation index of human capital, this paper positions human capital on the capital input quantity for upgrading labor skills and comprehensive capacity at the social overall level. As a result, capital input of human capital should be used to measure the enhancement degree of labor force itself, and then reveal the inherent characteristics of human capital at the objective level. Thus, by taking the method used by Dong (2017) [30] and Zhu et al. (2011) [31] to measure human capital with educational input, training input as well as environmental input, this study employed per capita education level to measure human capital, and then constructed the measurement index of the variable. The calculation formula is as follows:

In Formula (7), represents the total number of years of receiving education in i province in year t, means the number of people with the cultural level of primary school in i province in year t, refers to the number of people with the cultural level of middle school in i province in year t, stands for the number of people with the cultural level of high school in i province in year t, and suggests the number of people with the cultural level of junior college and above in i province in year t. In Formula (8), represents the per capita education level in i province in year t, and means the total sampling population aged over six years old in i province in year t.

This paper employs the region’s average education years to measure the education level of labor force within the region, and this way can fully display the educational input quantity contained in human capital. From the objective point of view of measurement, per capita education level does not merely reflect the input of labor in education, but can also estimate the educational environment quality at the social level, which can fully demonstrate the inherent characteristics of human capital.

4. Data, Variables and Model

4.1. Data Source

In the process of building the empirical model that reflects the impact of inclusive finance and human capital on regional economic growth, this paper has built different variables, and selects the panel data of 31 provinces in China from 2005 to 2015 as the sample for empirical analysis. There are 341 samples, and all data come from National Bureau of Statistics of China [32], website of People’s Bank of China [33], Wind Database, “Regional Financial Operation Report” [34] of previous years and statistical yearbooks of various provinces and cities. The descriptive statistical results of sample variables in the whole country are listed in Table 2.

Table 2 presents descriptive statistical results of samples and variables throughout China. It can be seen that the minimum of the variable LNGGDP is negative, while the values of other variables are all positive. Among them, because LR and CPI are both higher than 1, their mean and standard deviation are both higher than those of other variables. The symbol of every variable is explained in detail in Appendix A.

4.2. Variable Selection

4.2.1. Explained Variables

Regional economic growth. To eliminate the impact of population factors in different regions on the total economic output, the author chose total output value per capital as the measure of regional economic growth, that is, was the index to measure the variable of regional economic growth, which represents the total output value per capital of i province in year t. To reduce the impact of prices, the study took 2004 as the base period of constant prices, and adjusted the regional GDP by using GDP deflator of various years, thus obtaining the actual regional GDP, and, in addition, used the gross regional population of various years to get the actual total output value per capital in all regions.

4.2.2. Explaining Variables

Inclusive finance. Based on the measurement method of the index of inclusive finance and combined with the actual observed values of different dimensions, this study calculated the index, and used to represent the index of inclusive finance in i province in year t. The calculation process of the index of inclusive finance was built on the calculating method of human development index, which can more effectively reveal the advantages and disadvantages of regional financial institutions in the dimension of financial service quality and service scope to indicate the development level of inclusive finance in the region more objectively.

Human capital. Based on the measurement approach of human capital, the researcher measured the input quantity of human capital with the education level of labor force. means the regional education level per capita in i province in year t. Per capita education level can embody the education level of the region as a whole objectively and thus it allowed calculating the educational input quantity of different regions.

4.2.3. Control Variables

This paper needs to conduct an in-depth analysis of the factors influencing regional economic growth, while, in the research of many economic theories, due to the existence of economic endogenous problems, it is required to introduce control variables to reduce the influence of endogenousness on the relationship between explained variables and explaining variables. Thus, this study regarded the degree of government intervention, degree of regional opening, investment level of fixed assets and degree of inflation as control variables of the empirical model.

Degree of government intervention. Due to the particularity of China’s economic system, the government plays a significant role in the process of regional economic development, while the government’s financial expenditure to a certain extent determined the development of regional industries. Thus, the proportion of the government’s financial expenditure to the regional GDP to measure the degree of government intervention was used.

Degree of regional opening. With the continuous development of China’s foreign trade, the value of import and export has gradually become an important economic pillar of many provinces. In view of this situation, the proportion of the total export–import volume to the regional GDP to measure the degree of regional opening was used.

Investment level of fixed assets. Combined with the development of China in recent decades, infrastructure construction has been the focus of attention of the government all the time. Therefore, the investment level of fixed assets can also reflect the development trend of regional economy.

Degree of inflation: Currently, China’s economy is at a rapidly-developing stage, which is accountable for the rising price level and consumption level. Considering difficulty to measure the overall degree of inflation in China, the consumer price index, , was used to measure the degree of inflation so as to ensure objectivity of data and obtain the CPI level in different regions.

4.3. Model Building

When analyzing the influence relationship between inclusive finance and human capital and regional economic growth, the variables and samples selected in this paper were all acquired from the provincial level in different years, which made the panel data model better reflect the impact of inclusive finance and human capital on regional economy. Therefore, this study built an empirical model that displays the impact of inclusive finance and human capital on regional economic growth, and the concrete model is as follows:

5. Empirical Test

5.1. Unit Root Test

Before the regression analysis of the empirical model, it was required to conduct a corresponding unit root test on the panel data to ensure the stability of the data, avoid the spurious regression of the panel data model, etc. To better carry out the unit root test on the empirical model of this paper that reflects the impact of inclusive finance and human capital on regional economic growth, the author selected LLC (Levin, Lin, Chu) test, IPS (Im, Pesaran, Shin) test, ADF (Augmented Dickey-Fuller)-Fisher test and PP (Philips-Perron)-Fisher test as the methods to test the unit root, and conducted the unit root test from two aspects, namely homogeneous unit root test and heterogeneous unit root test, to ensure the stability of the different data selected and avoid the spurious regression phenomenon of subsequent regression analysis results. First, the author conducted the unit root test on all sequence original values in the empirical analysis model of this paper, and the test results are displayed in Table 3.

In view of the unit test results of the sequence original value in Table 3, only two variables, namely IFI and CPI, passed the 1% significance level test using four test methods, while none of the other variables could pass the test. This indicated that these sequences have unit roots, and thus it was necessary to carry out first-order difference processing on sequences and further investigate the sequence stability.

Table 4 shows the results of the unit root test of sequence first-order difference, and it can be discovered that, except for INV sequence, which passed 5% of the significance level tests under the IPS test, the other sequences passed the LLC test, IPS test, ADF-Fisher test and PP-Fisher test at the significance level of 1%. This suggests that all the sequences do not have the unit root and maintain stable after receiving the processing of first-order difference. Although the original value of various variables could not pass the unit root test, the variables, after first-order difference processing, all passed the unit root test. Therefore, they can be regarded as the sequence of the first-order integration. Thus, it can be known that various variables constitute the sequence of integrated of order, which met the preconditions of the cointegration test, thus allowed conducting the co-integration analysis of the panel data model.

5.2. Cointegration Test

According to the results of the unit root test of sequences of the panel data model in this paper, it can be perceived that regional economic growth, inclusive finance and human capital, degree of government intervention, degree of regional opening, investment level of fixed assets and degree of inflation and other sequences were all sequences of integrated order, thus meeting the preconditions of the cointegration test. In the process of cointegration test, this study chose both Kao test and Pedroni test to conduct an in-depth analysis of the co-integration relationship between different sequences respectively.

Table 5 exhibits the cointegration test results, and it can be discovered that in the Kao test, p value was smaller than 0.05, which illustrated that the original hypothesis of “there exists no co-integration relationship” can be rejected. In the Pedroni test, only the p values of Panel PP statistic and Panel ADF statistic were smaller than 0.05, while, in the intergroup statistics, only the p values of Group PP statistic and Group ADF statistic were smaller than 0.05, which illustrated that only the results of four statistics passed the cointegration test while the results of the other three statistics temporarily could not indicate the existence of a cointegration relationship in the sequence.

It is worth noting that, in the co-integration analysis and research of panel data of different time spans, Pedroni (2010) [35] pointed out that, when T ≤ 20, among seven statistics, only the efficiency of Panel ADF-Statistic and Group ADF-Statistic were relatively high; hence, when T = 11, the cointegration test process just needs to observe the p value of two statistics. It can be perceived that the p values of both Panel ADF-Statistic and Group ADF-Statistic were smaller than 0.05, suggesting that the original hypothesis of “there exists no co-integration relationship” can be rejected. Therefore, the two test results prove that regional economic growth, inclusive finance and human capital, degree of government intervention, degree of regional opening, investment level of fixed assets and degree of inflation and other sequences have stable incidence relations in the long-term development and it is allowed to carry on the subsequent regression analysis of the empirical model.

5.3. Result Analysis

The author further employed F test and Hausman test to discriminate the type of panel data model, the null hypothesis of the F test is a true model and a mixed regression model. The alternative hypothesis is a true model and a fixed effects model. The null hypothesis of Hausman test is an individual random effects model, while the alternative hypothesis is a true model and an individual fixed effects model, and the results are as follows.

According to Table 6 and type of panel data model, the model to verify influence of inclusive finance and human capital on regional economic growth should be a fixed effects model.

According to the discrimination results of types of the panel data model, it is suggested to build a double-fixed effect model of individuals and time that reflects the impact of inclusive finance and human capital on regional economic growth. This study first conducted a regression analysis of the panel data model of the overall national sample, and comprehensively analyzed the linear relationship and the nonlinear relationship among inclusive finance, human capital and regional economic growth. The regression results are shown below.

Table 7 exhibits the regression results of the panel data model of total samples around the country. In this table, Model 1 is the most basic model, while Models 2–6, respectively, analyze the possible nonlinear influence relationship between inclusive finance and human capital and regional economic growth.

Based on Formula (10), Model 1 carried out a regression analysis on the linear relationship between inclusive finance and human capital and regional economic growth, and the regression results reveals that both inclusive finance and human capital are significant at the level of 1%, and, moreover, all control variables are significant at the levels of 5% and 1%, which illustrates that there exists a significant linear influence relationship between inclusive finance and human capital and regional economic growth. The coefficients of these two indexes are positive numbers, proving that both inclusive finance and human capital produce a positive impact in promoting regional economic growth.

Based on Model 1, Model 2 added the square term of inclusive finance to explore whether there is a nonlinear relationship between inclusive finance and regional economic growth. While considering the linear influence relationship of human capital, the regression results reveal that the square term of inclusive finance is not significant. Inclusive finance and human capital are significant at the level of 1%, which illustrates that there still only exists a linear influence relationship between inclusive finance and regional economic growth, while the nonlinear influence relationship is not significant when considering the linear influence relationship of human capital.

Based on Model 1, Model 3 added the square term of human capital, and studied where there is a nonlinear influence relationship between human capital and regional economic growth while considering the linear influence relationship of inclusive finance. The regression results reveal that the square term of human capital and inclusive finance is significant at the level of 1%, while human capital is not significant, which illustrates that there is a nonlinear influence relationship between human capital and regional economic growth but the linear influence relationship is not significant when considering that inclusive finance generates the linear effect. This suggests the influence of human capital on regional economic growth weakens when the human capital is set to be in a fixed range of value. However, when the human capital exceeds the fixed range of value, the influence continues strengthening.

Based on Model 1, Model 4 simultaneously added the square term of inclusive finance as well as the square term of human capital to examine whether there are both a linear influence relationship and a nonlinear influence relationship between inclusive finance and human capital and regional economic growth. The regression results indicate that the square terms of inclusive finance and human capital are both significant at the level of 1%, while the square term of inclusive finance and human capital is not significant, which explains that there is a significant linear influence relationship between inclusive finance and regional economic growth and a significant nonlinear influence relationship between human capital and regional economic growth when considering the linear effect and the nonlinear effect generated by inclusive finance and human capital at the same time. This means that the promoting effect of inclusive finance on regional economic growth is relatively stable, while the nonlinear influence between human capital and regional economic growth is significant. Based on that, one can predict that the influence of human capital on regional economy would not change along with changes of human capital.

Based on Model 2, Model 5 made improvements, and mainly examined whether inclusive finance and regional economic growth have a nonlinear influence relationship or a linear influence relationship. The regression results reveal that inclusive finance and the square term of inclusive finance are significant, respectively, at the levels of 1% and 5%. Furthermore, the coefficient of the square term of inclusive finance is a negative number, demonstrating that there exists a significant linear influence relationship as well as an inverted U-shaped nonlinear influence relationship between inclusive finance and regional economic growth. When inclusive finance develops to certain stage, the influence of inclusive finance on regional economic growth reaches a peak. If the influence exceeds the peak, wasted financial resources would be caused.

Based on Model 3, Model 6 made corresponding adjustments. It mainly examined whether there exists a nonlinear influence relationship or a linear influence relationship between human capital and regional economic growth. The regression results show that the square term of human capital is significant at the level of 1%. Furthermore, the coefficient is a positive number, while human capital is not significant, which illustrates that there is a significant U-shaped nonlinear influence relationship between human capital and regional economic growth. This result is similar to the result of Model 3. It also suggests that the influence of human capital on regional economic growth gradually weakens and then strengthens.

By arranging the regression analysis results of total samples of the country, the conclusion can be drawn that, in different conditions, the forms of impact of inclusive finance and human capital on regional economic growth differ to a relatively extent, while the regression results of Models 1–5 all verify the significant positive promotion role between inclusive finance and regional economic growth, while the regression results of Model 3, Model 4 and Model 6 all verify that there exists a significant nonlinear influence relationship between human capital and regional economic growth.

To further explore the impact of inclusive finance and human capital in different Chinese regions, here, according to the division way of Chinese eastern region, central region and western region, this paper divides the total samples of the country into the sample of the eastern region, the sample of the central region and the sample of the western region, due to a small gap in inclusive finance and human capital of different regions. Equation (10) is used to conduct a regression analysis of sample data in different regions, a fixed effects model is built, and the regression results are shown as follows.

Table 8 exhibits the regression results of samples of different Chinese regions. Among them, Model 7 is the regression result of the sample of the eastern region, Model 8 is the regression result of the sample of the central region, and Model 9 is the regression result of the sample of the western region. As indicated in the regression result of Model 7, inclusive finance and human capital are significant, respectively, at the levels of 5% and 1%. Furthermore, both coefficients are positive numbers, proving that inclusive finance and human capital play a significant positive promotion role on regional economic growth in the eastern region. In the regression result of Model 8, both inclusive finance and human capital are significant at the level of 1%, but the coefficient of inclusive finance is a negative number while the coefficient of human capital is a positive number, which indicates that inclusive finance generates a significant inhibiting effect on regional economic growth in the central region, while human capital produces a significant positive effect in stimulating regional economic growth. According to the regression result of Model 9, both inclusive finance and human capital are significant at the level of 1%. Furthermore, both coefficients are positive numbers, suggesting that inclusive finance and human capital play a significant positive promotion role on regional economic growth in the western region.

By sorting the regression results of the samples of the eastern, central and western regions, it can be perceived that there are significant influence relationships among inclusive finance and human capital and regional economic growth, but their influencing mechanisms are largely different in different regions. This phenomenon may exert a serious impact on regional industrial structure and economic sustainable development, so it is supposed to develop different policies according to the economic environment of different regions to cope with the differences in the impact of inclusive finance and human capital.

6. Conclusions and Suggestions

- (1)

- Financial development and labor characteristics have always been hot topics for economic growth theories. To show the influence of these two aspects on economic activities better, this paper, from a macro perspective, explored the influence relationship between inclusive finance and human capital and regional economic growth. The definition forms of the concepts of inclusive finance and human capital have certain differences under different research perspectives, so this study defined the two concepts according to the research content and research purpose to ensure the reliability and practicability of the analysis results.

- (2)

- This study selected the data of 31 provinces in China from 2005 to 2015 and built the corresponding panel data model. The results of the empirical test indicate that inclusive finance and human capital generate a positive promotion effect on regional economic growth, and, of the two, the influencing effect of inclusive finance is stronger. However, when testing the nonlinear influence relationship among inclusive finance, human capital and regional economic growth, the nonlinear influence relationship produced by human capital is relatively significant in all cases, which illustrates that human capital has an obvious nonlinear effect on regional economic growth, and the strength of this influence relationship continues to increase over time. Therefore, inclusive finance and human capital have a significantly linear influence on inclusive finance and human capital in China. Inclusive finance in the long course of its development can exert a stronger promoting effect on economic activities. Meanwhile, the promoting effect can maintain economic growth at a steady level. This also reflects the importance of China’s integrated financial system on output of economic activities. On the contrary, the influence of human capital on regional economic activities is significantly nonlinear. This means that, along with progress of time, accumulation of human capital can more vigorously accelerate economic development in different regions of China. The influence mechanism can reflect striking difference of human resource from the traditional labor force. China’s overall integrated economic development relies on increase of human capital.

- (3)

- Due to huge differences in the development of China’s regional economy, this study divided regional samples of the country into the sample of the eastern region, the sample of the central region and the sample of the western region. By comparing and analyzing the regression results of the panel data models of the three regions, it was discovered that inclusive finance in the eastern region and western region positively boost regional economic growth. Furthermore, inclusive finance in the western region has the strongest promotion effect, while inclusive finance in the central region hinders regional economic growth. Human capital in all three regions plays a positive role in stimulating regional economic growth, inclusive finance in the middle region has the strongest promotion effect, and the promotion effect of inclusive finance in the eastern region is similar to that in the western region. Development of the financial environment in China’s central region has a negative influence on economic activities. According to practical situations of China’s central region, there is a large rural population, which holds back the urbanization process in this region. As a result, the credit environment is not well guaranteed, meaning that there are potential credit risks existing in the region’s financial system construction. Due to that, economic activities have been seriously impeded in the region. Besides, the industrial structure in central China lacks diversification, where the secondary industry plays a dominant role. This makes it difficult for the industry to seek self-development through a complete financial system. All the above explains the negative influence of the financial environment on the core industry of central China. The western region needs more perfect financial system to advance the rapid development of regional economy, which also proves the importance of financial services on economic activities in underdeveloped areas. In contrast to the financial environment, human capital input can effectively fuel economic activities of central China. This cannot be separated from dense distribution of institutions of higher learning in China’s central region. Meanwhile, the industry has been gradually transformed from labor-intensive to technology-intensive. Hence, talent resource can exert a greater influence on the region’s productivity and can fundamentally boost economic development of the whole region.

- (4)

- China is still in the economic transition period. With improvement of comprehensive qualities of labor resources in China, China’s labor market has transformed from a labor-intensive one to a technology-intensive one. The transformation can increase not only the economic output efficiency, but also the regional per capita income. Based on research conclusions of this paper, the Chinese government should vigorously accelerate construction of the inclusive finance system to ensure completeness and security of the financial system. Particularly in western China, the inclusive finance system is needed to boost development of micro-, small- and medium-sized enterprises and rural finance. In China’s central region, construction of the inclusive finance system can reduce the negative influence of assets on economic activities, give full play to the promoting effect of financial service on different industries, and accelerate construction of a favorable credit environment in central region. On the other hand, that human capital exerts an influence on economic development of different regions coincides with traditional economic theories. It should be noted that the promoting effect of human capital on China’s central region is the strongest, which indirectly suggests that China’s central region need talent resources and that the talent demand of China’s central resources is far higher than that of the other regions. This indicates that increase of the input of human capital can continuously fuel economic activities of China’s central region. Therefore, more attention should be paid to talent development and introduction of China’s central region. Comparatively, China’s eastern region is widely regarded as regions most advanced in developing inclusive finance and equipped with the strongest human capital in China. The development status of China’s east region in this paper fully demonstrates that inclusive finance and human capital can both effectively propel regional economic growth. Therefore, to alleviate the huge gap in China’s regional economic development, it is imperative to optimize resource distribution of inclusive finance and human capital, because this can more vigorously guarantee continuous development of China’s economy.

Acknowledgments

The research for this paper was supported by the National Natural Science Foundation of China (No. 71573050 and No. 71573170), the Shanghai Social Science Fund (No. 2015BJB003 and No. 2014BJB003) and the National Social Science Fund of China (No. 14BGL001).

Author Contributions

Guangyou Zhou performed the theory analysis and contributed to drafting the manuscript. Kuangxiong Gong analyzed the data. Sumei Luo conceived and empirical analysis. Guohu Xu Measured the Inclusive Finance and Human Capital.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

{kind=link}

Table A1.

A Introduction of variables.

| Abbreviations | Variables | Definition |

|---|---|---|

| PGDP | Regional economic growth level | The regional economic growth level is measured using the per capita GDP of every province and city. |

| IFI | Inclusive finance index | The inclusive finance index of different provinces and cities in China is built from four dimensions based on the inclusive finance measurement method provided in Section 3.2. |

| LR | Human capital level | The human capital level is measured using the average educational years in every province and city. |

| GOV | Government intervention degree | The percentage of the government fiscal expenditure in every province and city is used to measure the degree of government intervention. |

| OPEN | Regional opening degree | The regional opening degree is measured using the export percentage of every province and city in regional GDP. |

| INV | Fixed asset investment level | The fixed asset investment level is measured using the percentage of the fixed asset investment of every province and city in regional GDP. |

| CPI | Degree of inflation | The degree of inflation is measured using residents’ consumer price index. |

References

- Wang, X.; Guan, J. Financial Inclusion: Measurement, Spatial Effects and Influencing Factors. Appl. Econ. 2017, 49, 1751–1762. [Google Scholar] [CrossRef]

- Su, Y.; Liu, Z. The Impact of Foreign Direct Investment and Human Capital on Economic Growth: Evidence From Chinese Cities. China Econ. Rev. 2016, 37, 97–109. [Google Scholar] [CrossRef]

- Yan, H. Study on the Development of Inclusive Finance in China; Party School of the Central Committee of CPC: Beijing, China, 2013. [Google Scholar]

- Guo, T.; Ding, X. International Comparative Study of Inclusive Finance—From the Perspective of Bank Services. J. Int. Financ. Res. 2015, 2, 55–64. [Google Scholar]

- He, D.; Miao, W. Financial Exclusion, Financial Inclusion and Inclusive Financial Institution in China. Financ. Trade Econ. 2015, 3, 5–16. [Google Scholar]

- Gabor, D.; Brooks, S. The Digital Revolution in Financial Inclusion: International Development in the Fintech Era. New Political Econ. 2017, 22, 423–436. [Google Scholar] [CrossRef]

- Park, D.; Shin, K. Economic Growth, Financial Development, and Income Inequality. Emerg. Mark. Financ. Trade 2017, 53, 2794–2825. [Google Scholar] [CrossRef]

- Corrado, G.; Corrado, L. Inclusive Finance for Inclusive Growth and Development. Curr. Opin. Environ. Sustain. 2017, 24, 19–23. [Google Scholar] [CrossRef]

- Dupas, P.; Robinson, J. Why Don’t the Poor Save More? Evidence from Health Savings Experiments. Am. Econ. Rev. 2013, 4, 1138–1171. [Google Scholar] [CrossRef]

- Ayyagari, M.; Demirguec-Kunt, A.; Maksimovic, V. Firm Innovation in Emerging Markets: The Role of Finance, Governance, and Competition. J. Financ. Quant. Anal. 2011, 6, 1545–1580. [Google Scholar] [CrossRef]

- Anzoategui, D.; Demirguec-Kunt, A.; Peria, M.S.M. Remittances and Financial Inclusion: Evidence from El Salvador. World Dev. 2014, 1, 338–349. [Google Scholar] [CrossRef]

- Beck, T.; Demirguc-Kunt, A.; Martinez Peria, M.S. Reaching Out: Access to and Use of Banking Services Across Countries. J. Financ. Econ. 2007, 1, 234–266. [Google Scholar] [CrossRef]

- Sarma, M.; Pais, J. Finacial Inclusion and Development. J. Int. Dev. 2011, 5, 613–628. [Google Scholar] [CrossRef]

- Wang, J.; Hu, G. The Evaluation of the Development of China’s Inclusive Finance and the Analysis of Factors. Financ. Forum 2013, 6, 31–36. [Google Scholar]

- Du, Q.; Pan, Y. Research on the Influence of Inclusive Finance on Regional Economic Development in China—An Empirical Analysis Based on Inter-Provincial Panel Data. Inq. Econ. Issues 2016, 3, 178–184. [Google Scholar]

- Li, T.; Xu, X.; Sun, S. Inclusive Finance and Economic Growth. J. Financ. Res. 2016, 4, 1–16. [Google Scholar]

- Lu, F.; Huang, Y.; Xu, P. Provincial Differences of China’s Inclusive Finance and Influencing Factors. J. Financ. Econ. 2017, 1, 111–120. [Google Scholar]

- Kalaitzidakis, P.; Mamuneas, T.P.; Savvides, A.; Stengos, T. Measures of Human Capital and Nonlinearities in Economic Growth. J. Econ. Growth 2001, 3, 229–254. [Google Scholar] [CrossRef]

- Mamuneas, T.P.; Savvides, A.; Stengos, T. Economic Development and the Return to Human Capital: A Smooth Coefficient Semiparametric Approach. J. Appl. Econ. 2006, 1, 111–132. [Google Scholar] [CrossRef]

- Lin, T.-C. Education, Technical Progress, and Economic Growth: The Case of Taiwan. Econ. Educ. Rev. 2003, 2, 213–220. [Google Scholar] [CrossRef]

- Lin, T.-C. The Role of Higher Education in Economic Development: An Empirical Study of Taiwan Case. J. Asian Econ. 2004, 2, 355–371. [Google Scholar] [CrossRef]

- Wang, W.; Li, Q.; Lien, D. Human Capital, Political Capital, and Off-Farm Occupational Choices in Rural China. Int. Rev. Econ. Financ. 2016, 42, 412–422. [Google Scholar] [CrossRef]

- Kraekel, M. Human Cpaital Investment and Work Incentives. J. Econ. Manag. Strategy 2016, 3, 627–651. [Google Scholar] [CrossRef]

- Murphy, K.M.; Topel, R.H. Human Capital Investment, Inequality, and Economic Growth. J. Labor Econ. 2016, 34, S99–S127. [Google Scholar] [CrossRef]

- Cavalcanti, T.V.V.; Giannitsarou, C. Growth and Human Capital: A Network Approach. Econ. J. 2017, 603, 1279–1317. [Google Scholar] [CrossRef]

- Bai, X. Statistical Analysis on the Relationship between Education Level of Employed Population and Economic Growth. Master’s Thesis, Southwestern University of Finance and Economics, Chengdu, China, 2013. [Google Scholar]

- Du, W.; Yang, Z.; Xia, G. Study on the Impact Mechanism of Human Capital on Economic Growth. China Soft Sci. 2014, 8, 173–183. [Google Scholar]

- Wang, Y.; Zhu, P. The Threshold Effect of Human Capital in China’s Economic Growth. Stat. Res. 2016, 1, 13–19. [Google Scholar]

- Zhou, B.; Mao, D.; Zhu, G. “Internet +”, Inclusive Finance and Economic Growth—Empirical Test of PVAR Model Based on Panel Data. Financ. Theory Pract. 2017, 38, 9–16. [Google Scholar]

- Dong, Z. Research on the Interactive Relationship between Human Capital and Economic Growth—An Empirical Analysis Based on China’s Human Capital Index. Macroeconomics 2017, 88–98. [Google Scholar]

- Zhu, C.; Shi, P.; Yue, H.; Han, X. The Study on Bind of Human Capital, Human Capital Structure and Regional Economic Growth Efficiency. China Soft Sci. 2011, 2, 110–119. [Google Scholar]

- National Bureau of Statistics of China. Available online: http://data.stats.gov.cn/easyquery.htm?cn=E0103 (accessed on 31 August 2017).

- People’s Bank of China. Available online: http://www.pbc.gov.cn/diaochatongjisi/116219/index.html (accessed on 31 August 2017).

- Monetary Policy Department of People’s Bank of China. Available online: http://www.pbc.gov.cn/zhengcehuobisi/125207/125227/125960/126049/index.html (accessed on 31 August 2017).

- Pedroni, P. Critical Values for Cointegration Tests in Heterogeneous Panels with Multiple Regressors. Oxf. Bull. Econ. Stat. 1999, 61, 653–670. [Google Scholar] [CrossRef]

Figure 1.

Logical relationship diagram among inclusive finance, human capital and regional economy.

Table 1.

The index system of inclusive finance in China.

| Dimension | Specific Index | Descriptive Index |

|---|---|---|

| Availability of financial services | Number of branches of financial institutions/100,000 persons | Customer group scope of services of financial institutions |

| Number of employees of financial institutions/100,000 persons | Customer group scope of services of financial personnel | |

| Usability of financial services | Savings of urban and rural residents/person | Residents’ use of financial services |

| Insurance income/population size | Insurance density | |

| Insurance income/GDP | Insurance penetration | |

| Utility of financial services | Deposit balance/GDP | Utility embodied in deposit and other financial services |

| Loan balance/GDP | Utility embodied in lending and other financial services | |

| Receptivity of financial services | Financing amount of non-financial institutions/GDP | Financing difficulty of formal financial institutions |

Table 2.

Descriptive statistical results of sample variables in the whole country.

| Variable | Average Value | Median | Maximum Value | Minimum Value | Standard Deviation | Sample Number |

|---|---|---|---|---|---|---|

| LNPGDP | 0.8258 | 0.8171 | 2.1960 | −0.6892 | 0.5739 | 341 |

| FIZ | 0.2296 | 0.1876 | 0.9081 | 0.0647 | 0.1666 | 341 |

| LR | 8.5018 | 8.5163 | 12.0807 | 3.7384 | 1.1995 | 341 |

| GOV | 0.2375 | 0.1953 | 1.3459 | 0.0798 | 0.1820 | 341 |

| OPEN | 0.3223 | 0.1396 | 1.7215 | 0.0357 | 0.3965 | 341 |

| INV | 0.6636 | 0.6590 | 1.3283 | 0.2529 | 0.2143 | 341 |

| CPI | 102.9035 | 102.5000 | 110.1000 | 97.7000 | 2.0113 | 341 |

Table 3.

Results of the unit root test of sequence original values.

| Test Method | Original Value | ||||||

|---|---|---|---|---|---|---|---|

| LNPGDP | FIZ | LR | GOV | OPEN | INV | CPI | |

| LLC | 3.4404 | −10.6695 | −9.8573 | −5.2581 | −7.0099 | −8.1045 | −23.4284 |

| (0.9997) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |

| IPS | 7.0663 | −1.6012 | −2.8079 | −0.3364 | −0.0648 | −0.4045 | −6.4432 |

| (1.0000) | (0.0547) | (0.0025) | (0.3683) | (0.4742) | (0.3429) | (0.0000) | |

| ADF-Fisher | 34.1367 | 93.6227 | 100.6200 | 68.1058 | 66.9164 | 72.5711 | 209.8930 |

| (0.9985) | (0.0058) | (0.0014) | (0.2774) | (0.3121) | (0.1687) | (0.0000) | |

| PP-Fisher | 29.1642 | 107.2360 | 129.0290 | 82.4187 | 76.6664 | 65.1162 | 207.6520 |

| (0.9999) | (0.0003) | (0.0000) | (0.0425) | (0.0995) | (0.3688) | (0.0000) | |

| Stable or not | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

Note: The results of the unit root test of various in the parentheses are the corresponding p values.

Table 4.

Results of the unit root test of sequence first-order difference.

| Test Method | First-Order Difference | ||||||

|---|---|---|---|---|---|---|---|

| LNPGDP | FIZ | LR | GOV | OPEN | INV | CPI | |

| LLC | −44.9868 | −15.3766 | −16.5391 | −9.5370 | −15.7319 | −15.7125 | −24.1379 |

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |

| IPS | −5.4612 | −2.6299 | −3.8525 | −1.9327 | −2.4466 | −2.0775 | −4.6935 |

| (0.0000) | (0.0043) | (0.0001) | (0.0266) | (0.0072) | (0.0189) | (0.0000) | |

| ADF-Fisher | 137.3100 | 122.3860 | 149.6030 | 106.3810 | 12(0.9490 | 115.2110 | 196.2040 |

| (0.0000) | (0.0000) | (0.0000) | (0.0004) | (0.0000) | (0.0000) | (0.0000) | |

| PP-Fisher | 114.4200 | 217.4930 | 274.6870 | 199.7940 | 205.7640 | 141.6370 | 345.8380 |

| (0.0001) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |

| Stable or not | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

Note: The results of the unit root test of various in the parentheses are the corresponding p values.

Table 5.

Cointegration test results of panel data.

| Test Method | Statistic | Statistical Value | P Value |

|---|---|---|---|

| Kao test | ADF | −5.7294 | 0.0000 |

| Pedroni test | Panel v-Statistic | −5.7525 | 1.0000 |

| Panel ρ-Statistic | 6.3624 | 1.0000 | |

| Panel PP-Statistic | −3.1481 | 0.0008 | |

| Panel ADF-Statistic | −4.1620 | 0.0000 | |

| Group ρ-Statistic | 8.8006 | 1.0000 | |

| Group PP-Statistic | −9.1910 | 0.0000 | |

| Group ADF-Statistic | −5.1473 | 0.0000 |

Table 6.

Results of discriminating the type of the panel data model.

| Test Method | Original Hypothesis | Statistical Value | P Value |

|---|---|---|---|

| F test | The real mode is a fixed model | 71.4883 | 0.0000 |

| Hausman test | The real mode is an individual random effect model | 46.5665 | 0.0000 |

Table 7.

Regression results of national total samples.

| Variable | Model 1 | Model 2 | Model 3 | Model 4 | Model 5 | Model 6 |

|---|---|---|---|---|---|---|

| constant term | −4.053746 *** | −4.04608 *** | −2.186537 *** | −2.225775 *** | −2.816176 *** | −2.449031 *** |

| (−11.9067) | (−11.9065) | (−3.9705) | (−4.0363) | (−6.1183) | (−4.4169) | |

| FIZ | 1.005972 *** | 1.956014 *** | 1.125238 *** | 1.844245 *** | 3.774767 *** | |

| (2.9518) | (2.7024) | (3.3809) | (2.6126) | (3.8026) | ||

| FIZ2 | −1.518931 | −1.154155 | −2.863333 ** | |||

| (−1.4869) | (−1.1548) | (−2.0270) | ||||

| LR | 0.355302 *** | 0.352853 *** | −0.114273 | −0.104801 | −0.070879 | |

| (16.9252) | (16.7902) | (−1.0158) | (−0.9297) | (−0.6236) | ||

| LR2 | 0.027925 *** | 0.027251 *** | 0.026047 *** | |||

| (4.2448) | (4.1284) | (3.9071) | ||||

| GOV | 0.313488 ** | 0.242538 | 0.528871 *** | 0.469762 *** | 0.481418 ** | 0.655049 *** |

| (2.0907) | (1.5441) | (3.4234) | (2.8879) | (2.2187) | (4.2965) | |

| OPEN | −0.310394 *** | −0.316696 *** | −0.194322 *** | −0.201912 *** | −0.666323 *** | −0.198912 *** |

| (−4.6789) | (−4.7736) | (−2.7717) | (−2.8690) | (−7.6262) | (−2.7903) | |

| INV | 0.865403 *** | 0.844629 *** | 0.834478 *** | 0.81944 *** | 1.395194 *** | 0.897878 *** |

| (12.6985) | (12.1644) | (12.5076) | (12.0611) | (16.4341) | (13.7886) | |

| CPI | 0.010488 *** | 0.01 *** | 0.010207 *** | 0.009843 *** | 0.021186 *** | 0.012343 *** |

| (3.1319) | (2.9779) | (3.1316) | (3.0076) | (4.6405) | (3.7954) | |

| fixed effect | Fixed | Fixed | Fixed | Fixed | Fixed | Fixed |

| Time fixed effect | Fixed | Fixed | Fixed | Fixed | Fixed | Fixed |

| F value | 246.1809 | 240.5413 | 253.4235 | 247.0612 | 124.4212 | 251.5160 |

| p value | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

| Goodness of fit | 0.9629 | 0.9631 | 0.9649 | 0.9649 | 0.9289 | 0.9637 |

| Total sample number | 341 | 341 | 341 | 341 | 341 | 341 |

Note: figures in parentheses are the t statistics of estimated coefficients; ***, ** represent the significance at the level of 1%, 5% respectively.

Table 8.

Sample regression results in the eastern, central and western regions.

| Variable | Model 7 | Model 8 | Model 9 |

|---|---|---|---|

| constant term | −3.783842 *** | −5.277084 *** | −3.205175 *** |

| (−8.0336) | (−7.9726) | (−5.6779) | |

| FIZ | 0.919155 ** | −2.693263 *** | 2.608737 *** |

| (2.5597) | (−2.9301) | (3.8259) | |

| LR | 0.29586 *** | 0.308267 *** | 0.295141 *** |

| (9.4754) | (7.0728) | (8.3723) | |

| GOV | 1.346055 *** | 3.315032 *** | 0.050806 |

| (2.9346) | (4.1331) | (0.2783) | |

| OPEN | −0.428877 *** | −1.763641 *** | 0.586287 ** |

| (−5.9765) | (-3.4706) | (2.4905) | |

| INV | 0.813691 *** | 0.818099 *** | 0.777463 *** |

| (7.5275) | (5.3421) | (6.7541) | |

| CPI | 0.014972 *** | 0.026351 *** | 0.002771 |

| (3.3034) | (3.9449) | (0.5003) | |

| F value | 376.4326 | 89.4651 | 112.9737 |

| p value | 0.0000 | 0.0000 | 0.0000 |

| Goodness of fit | 0.9804 | 0.9297 | 0.9356 |

| Total sample number | 121 | 88 | 132 |

Note: figures in the parentheses are the t statistics of estimated coefficients; ***, ** represent the significance at the level of 1%, 5% respectively.

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Zhou, G.; Gong, K.; Luo, S.; Xu, G. Inclusive Finance, Human Capital and Regional Economic Growth in China. Sustainability 2018, 10, 1194. https://doi.org/10.3390/su10041194

AMA Style

Zhou G, Gong K, Luo S, Xu G. Inclusive Finance, Human Capital and Regional Economic Growth in China. Sustainability. 2018; 10(4):1194. https://doi.org/10.3390/su10041194

Chicago/Turabian StyleZhou, Guangyou, Kuangxiong Gong, Sumei Luo, and Guohu Xu. 2018. "Inclusive Finance, Human Capital and Regional Economic Growth in China" Sustainability 10, no. 4: 1194. https://doi.org/10.3390/su10041194

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.