Comparing the Effects of Vehicle Automation, Policy-Making and Changed User Preferences on the Uptake of Electric Cars and Emissions from Transport

Abstract

:1. Introduction

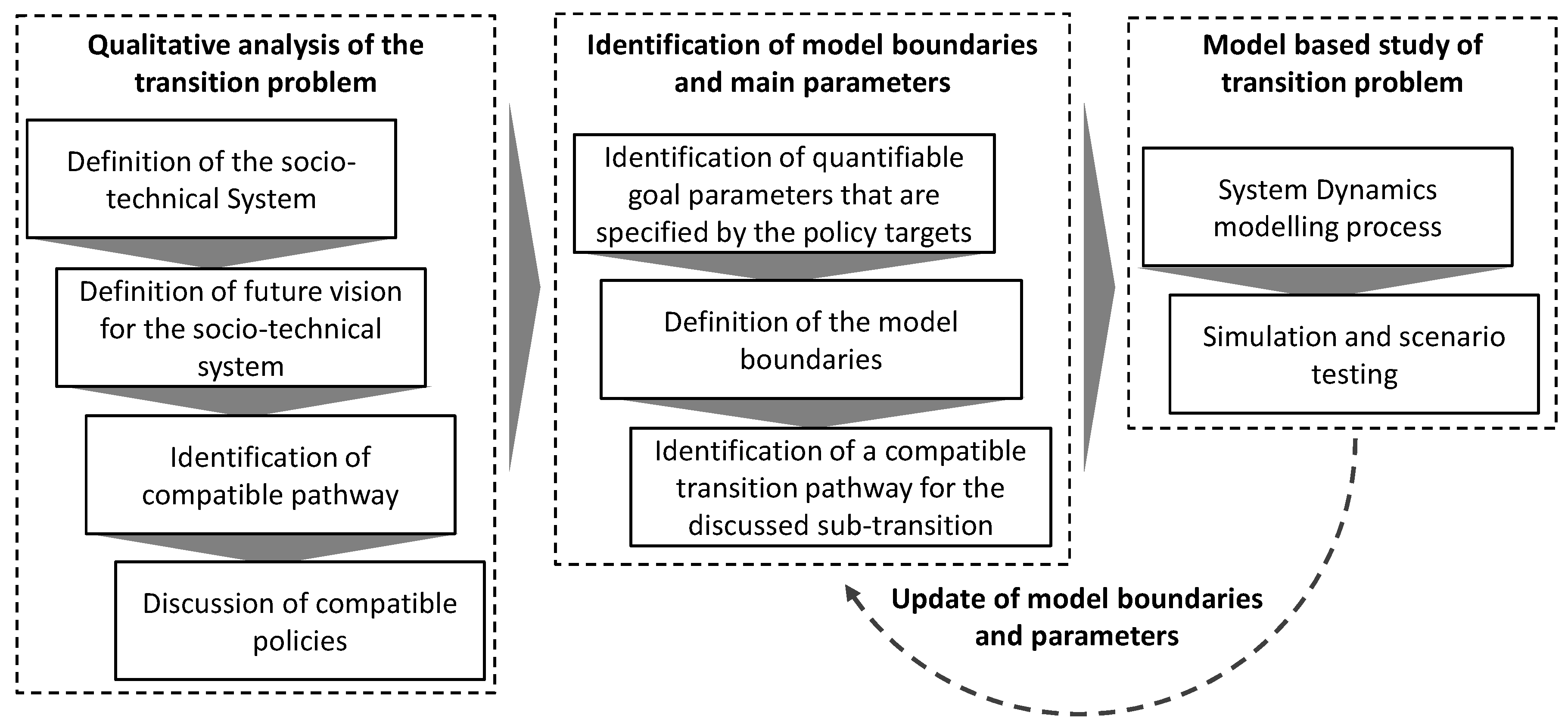

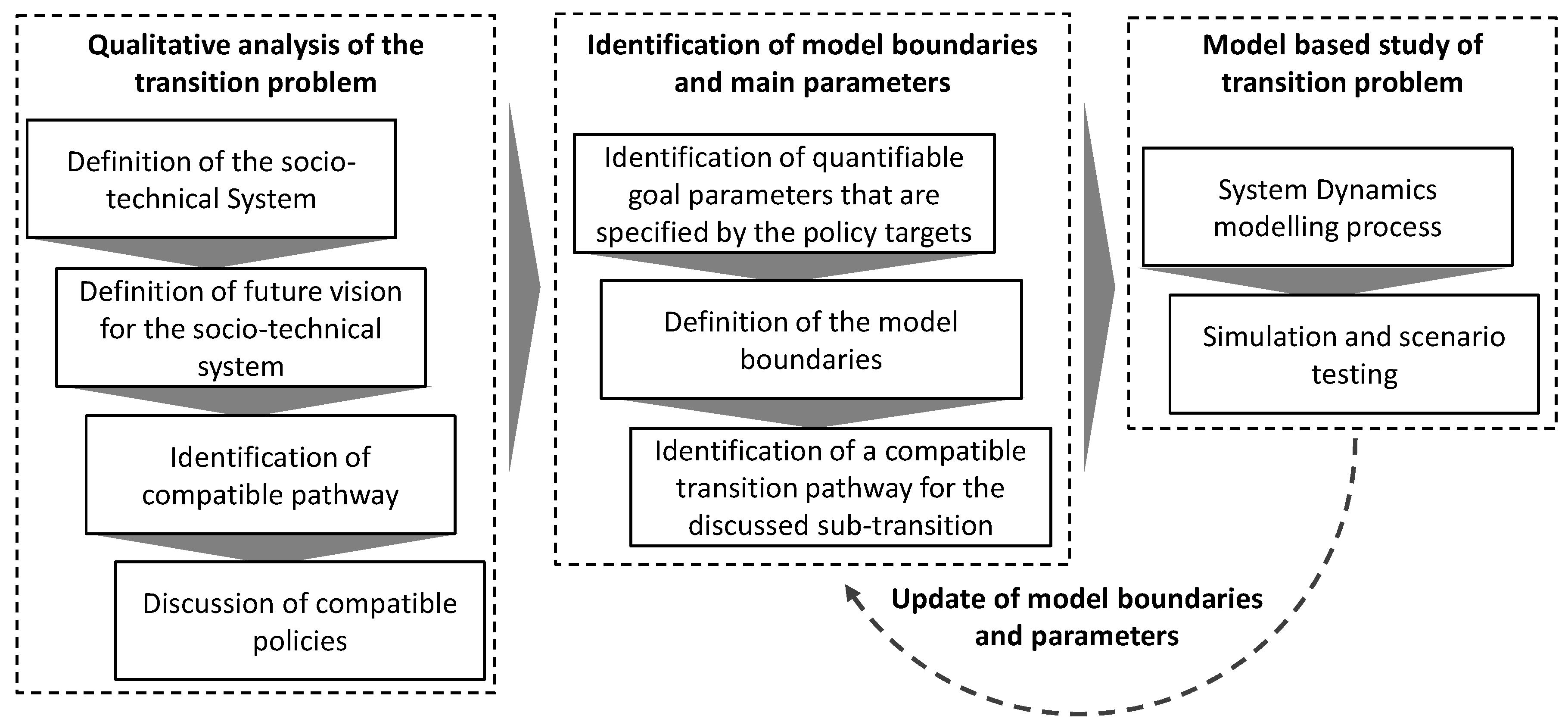

2. Materials and Methods

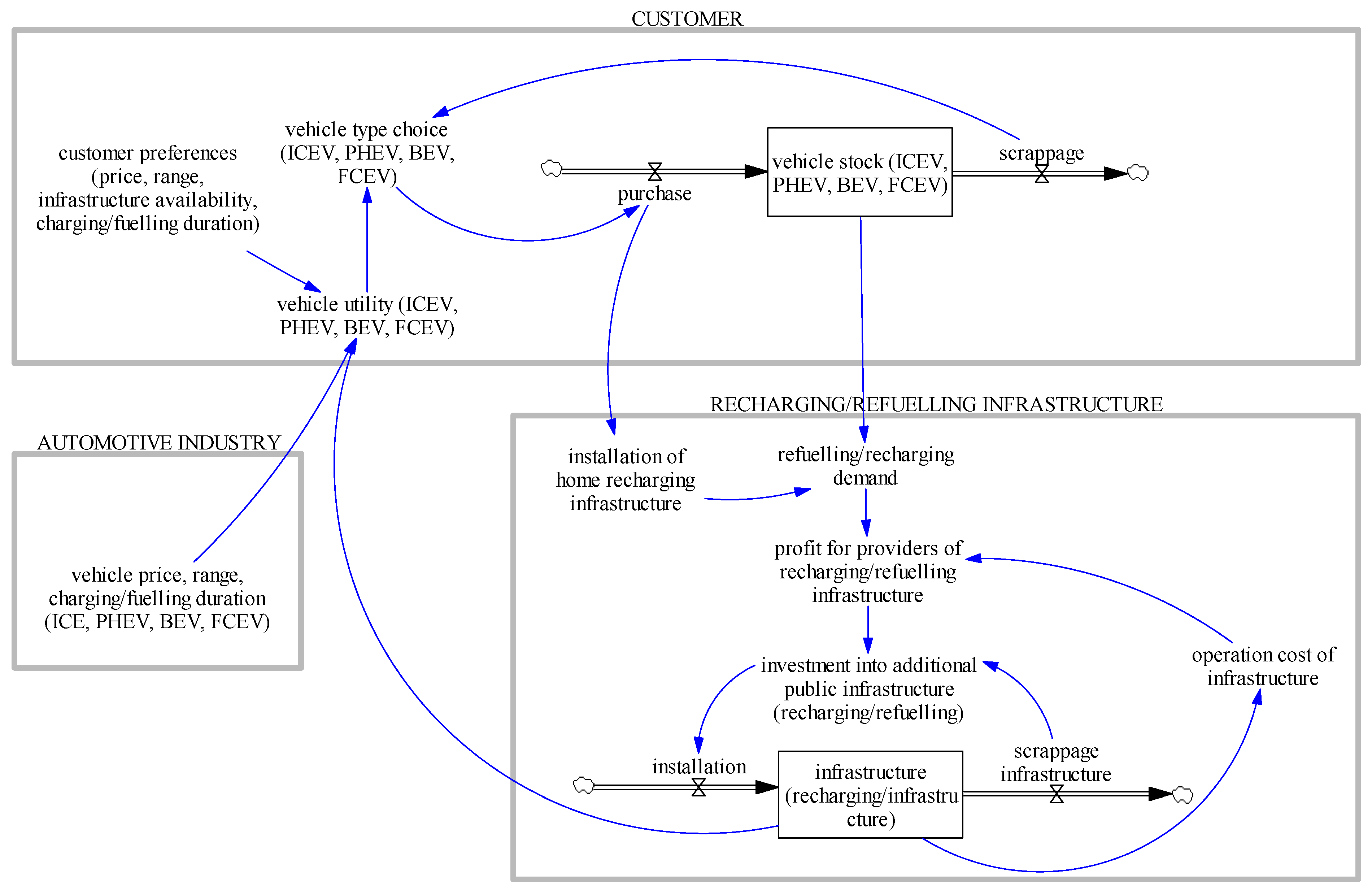

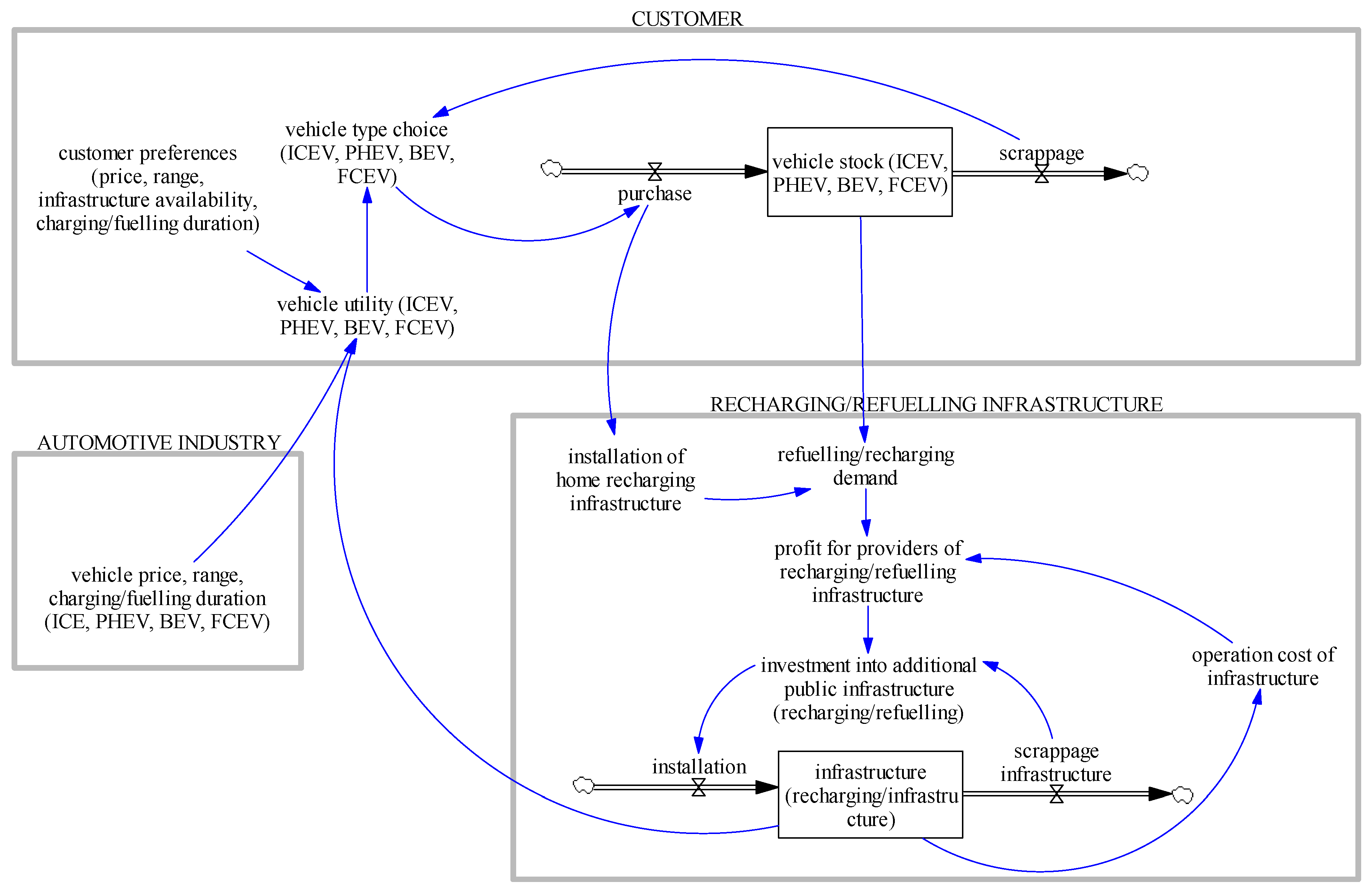

2.1. Model Overview

- Customer choice (choice of the vehicle type)

- Automotive industry (provision of the different vehicle types)

- Recharging/refuelling infrastructure providers (provision of recharging infrastructure)

2.2. Model Equations

2.3. Data

2.4. Assumptions

3. Results

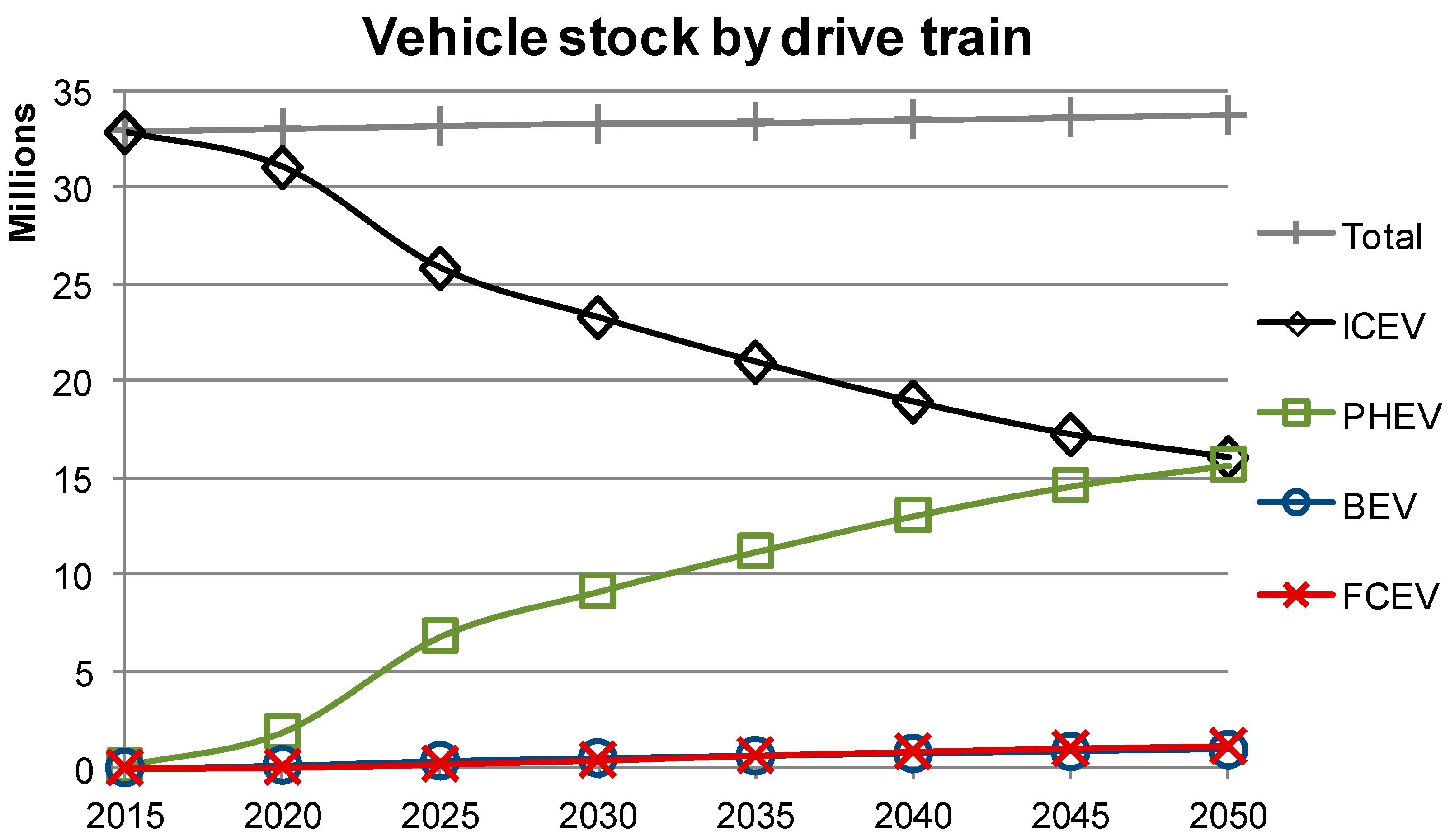

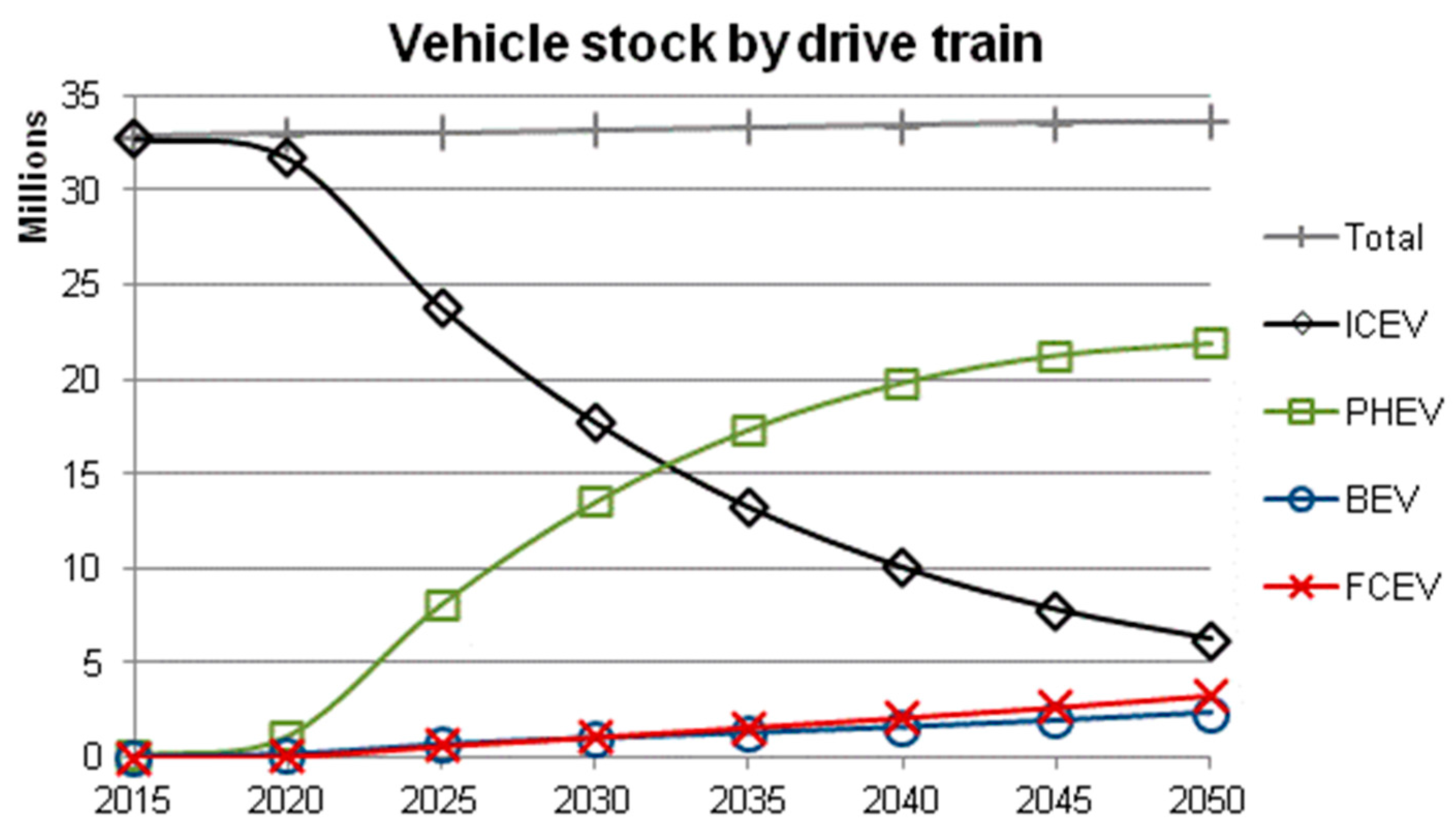

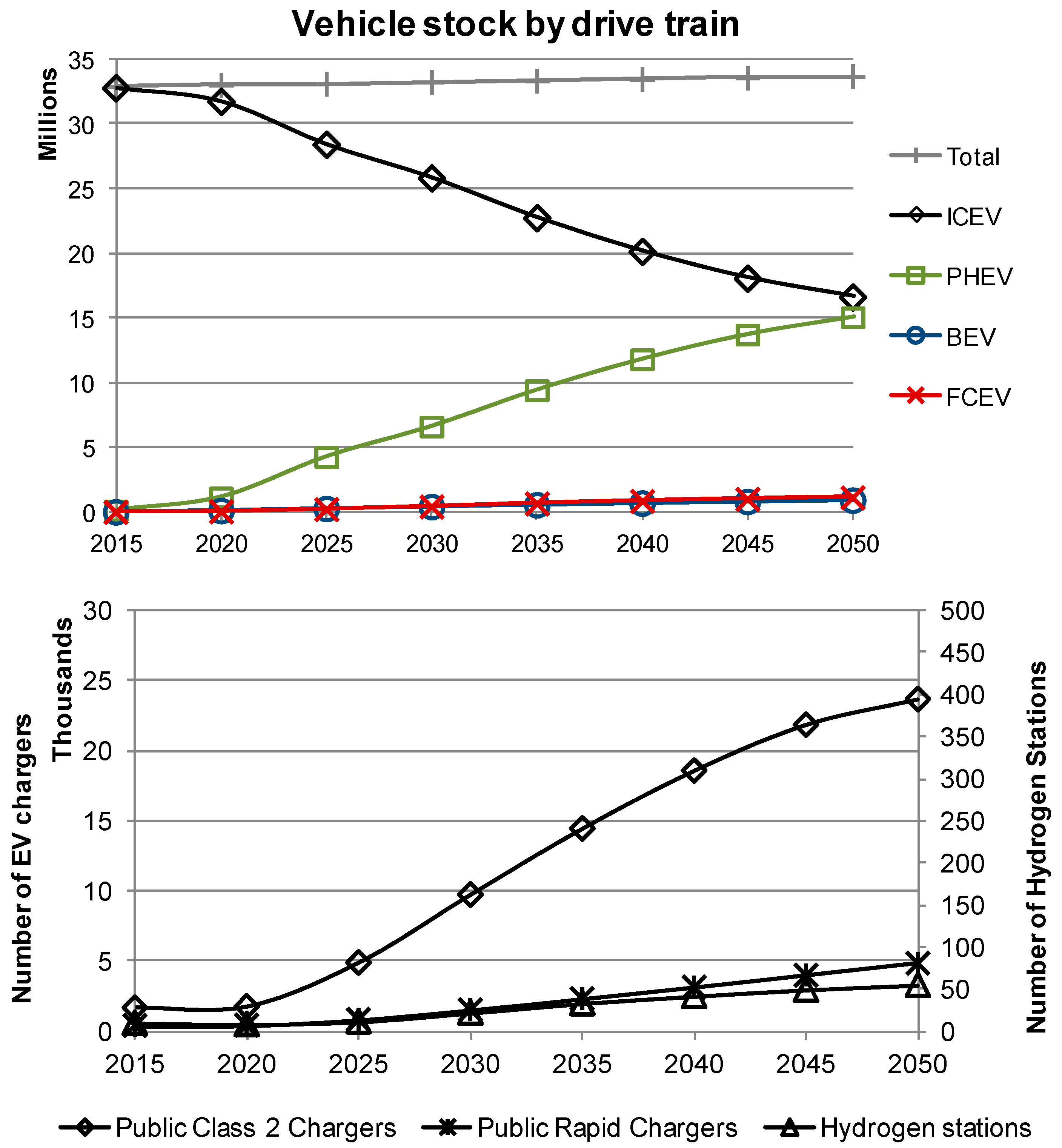

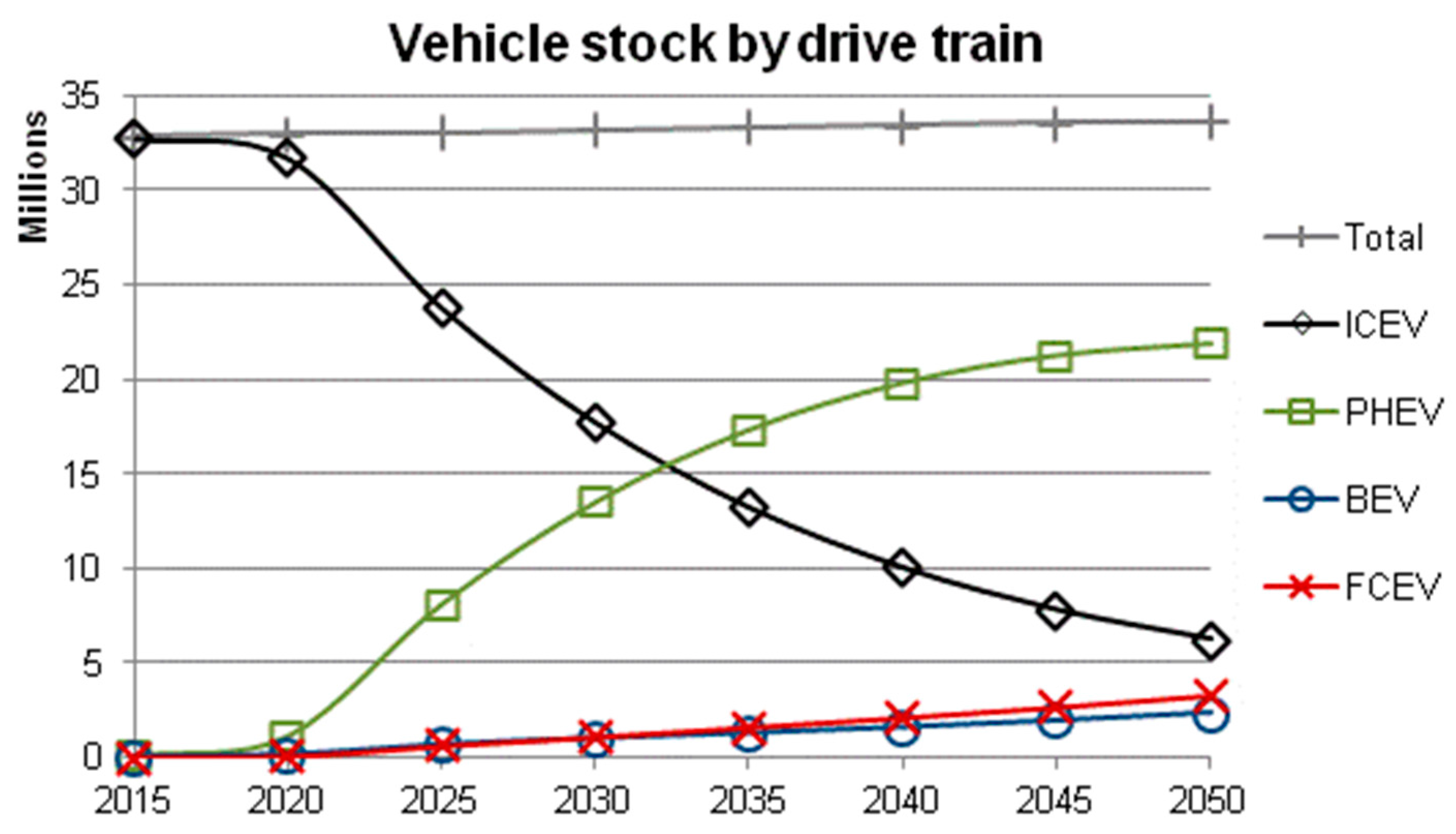

3.1. Business-as-Usual Scenario

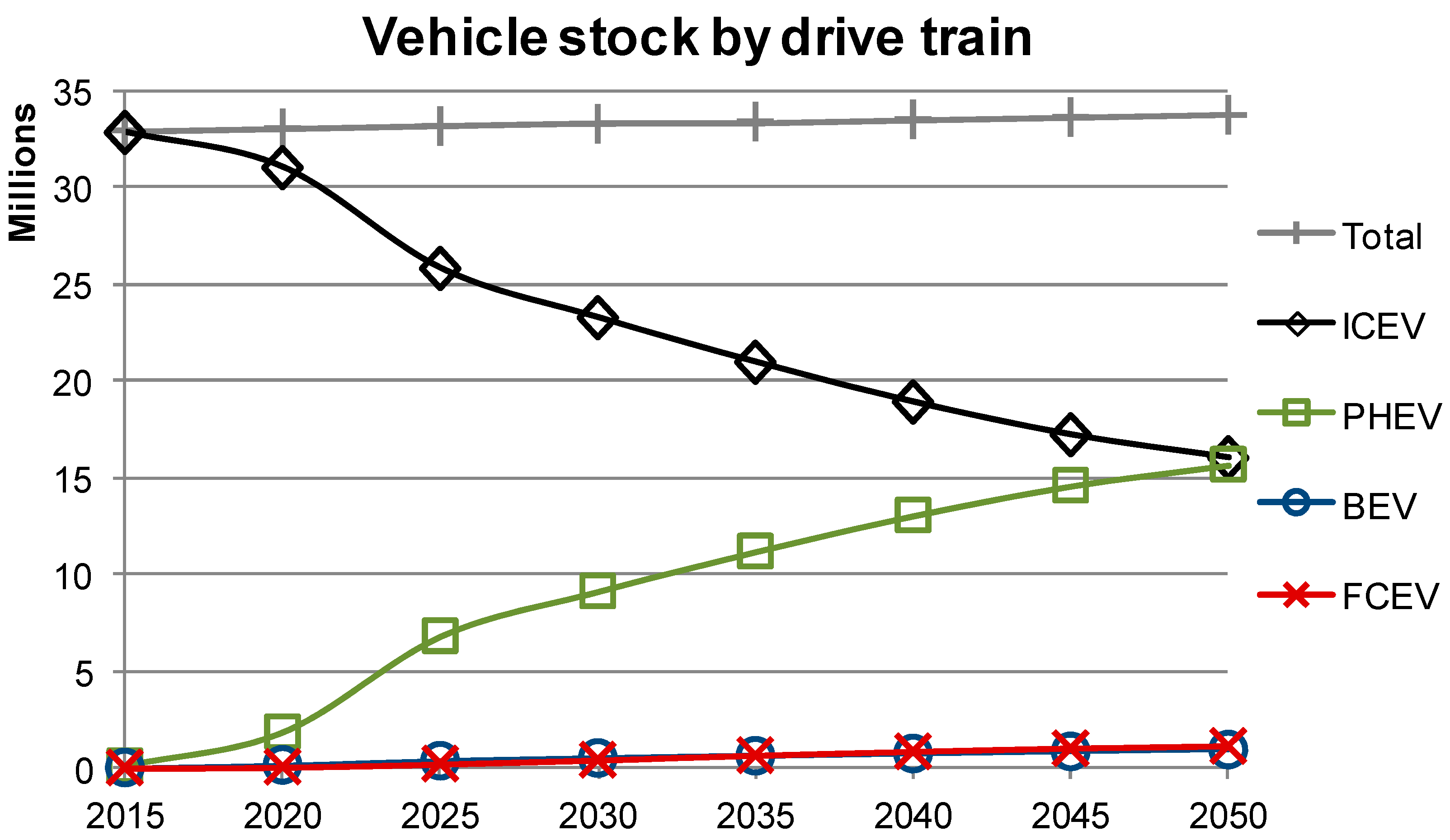

3.2. Technology Optimistic Scenario

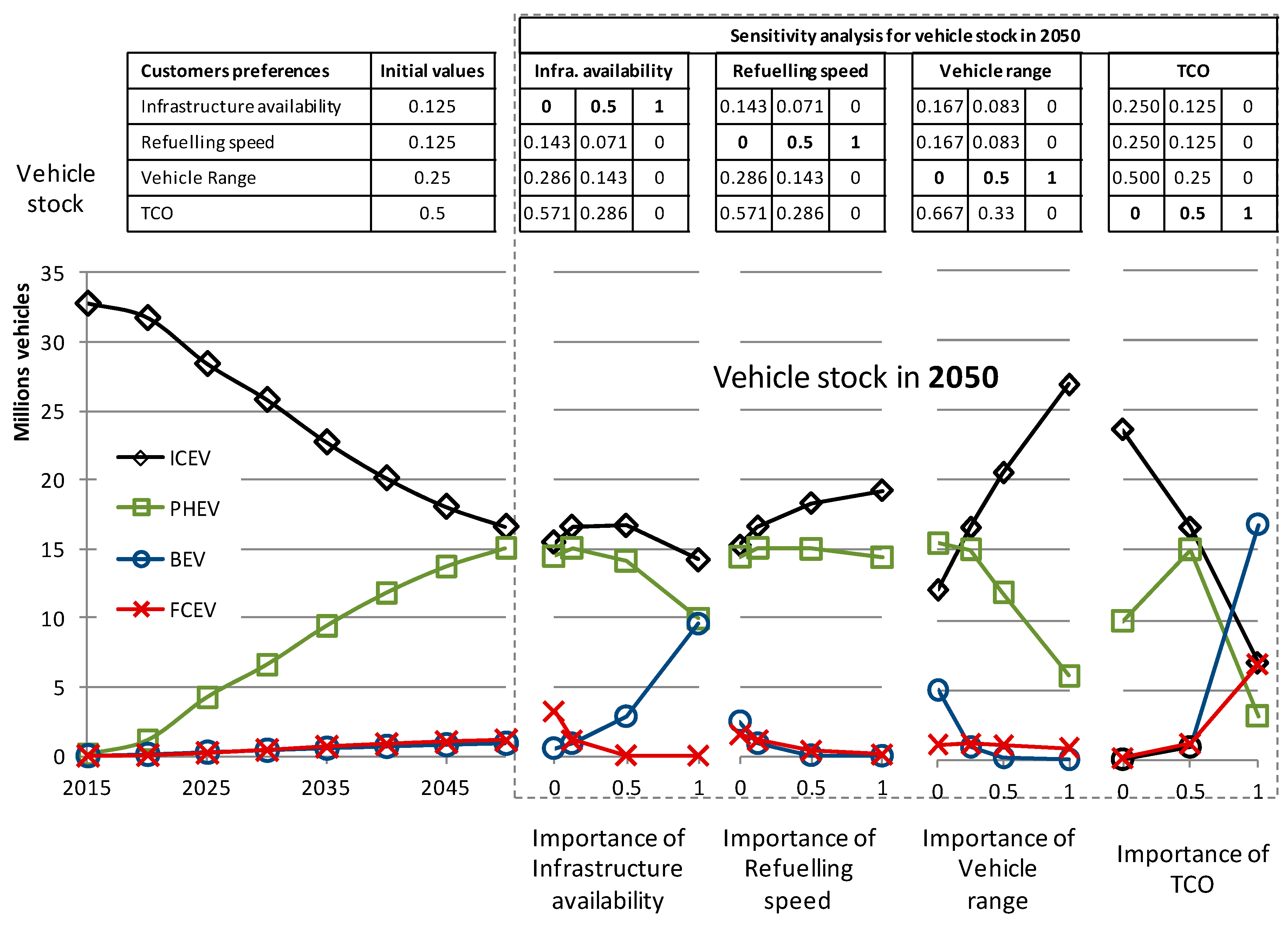

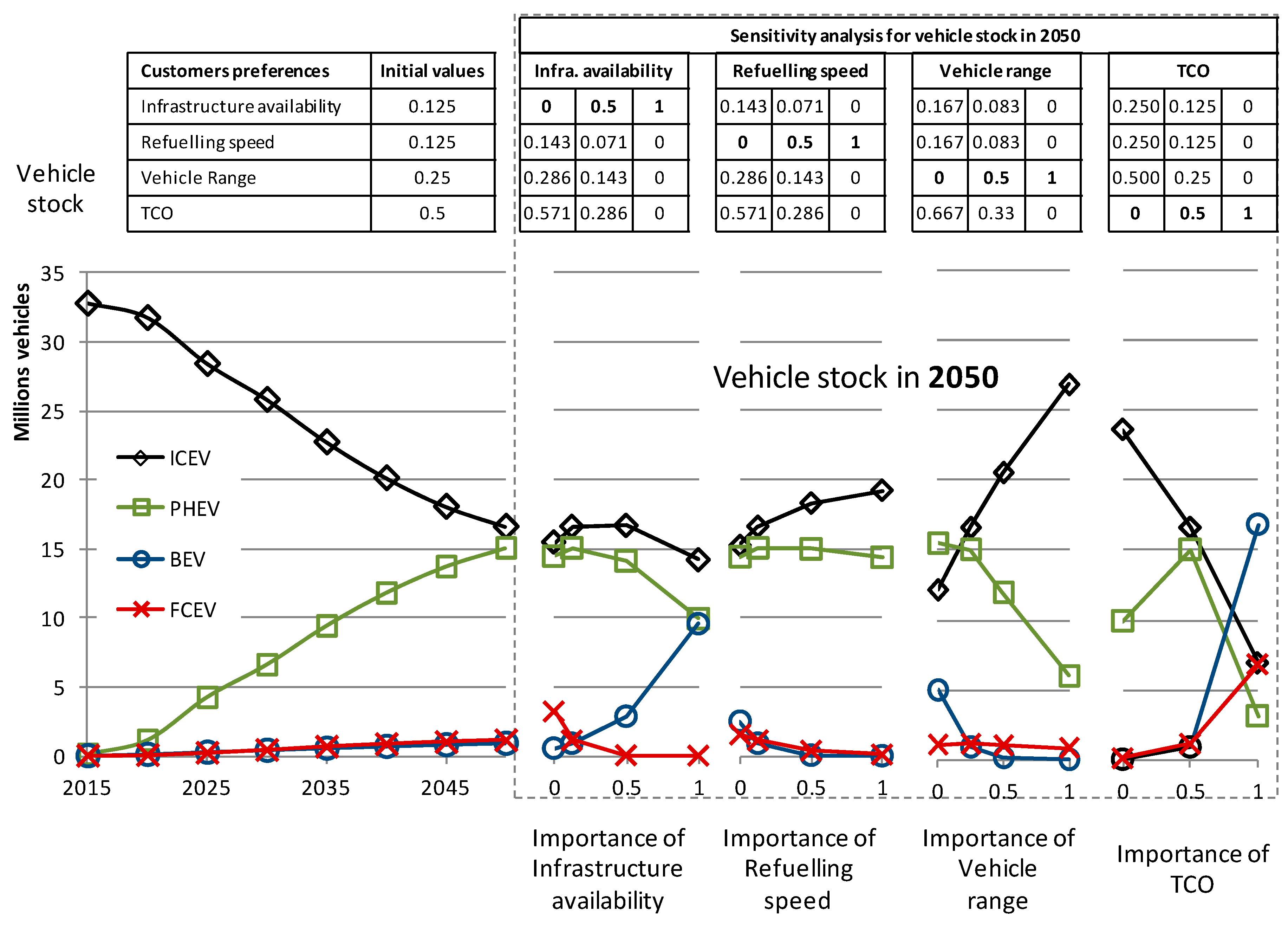

3.3. Changing Customers’ Preferences and Expectations

3.4. More Radical Policy-Making Scenario

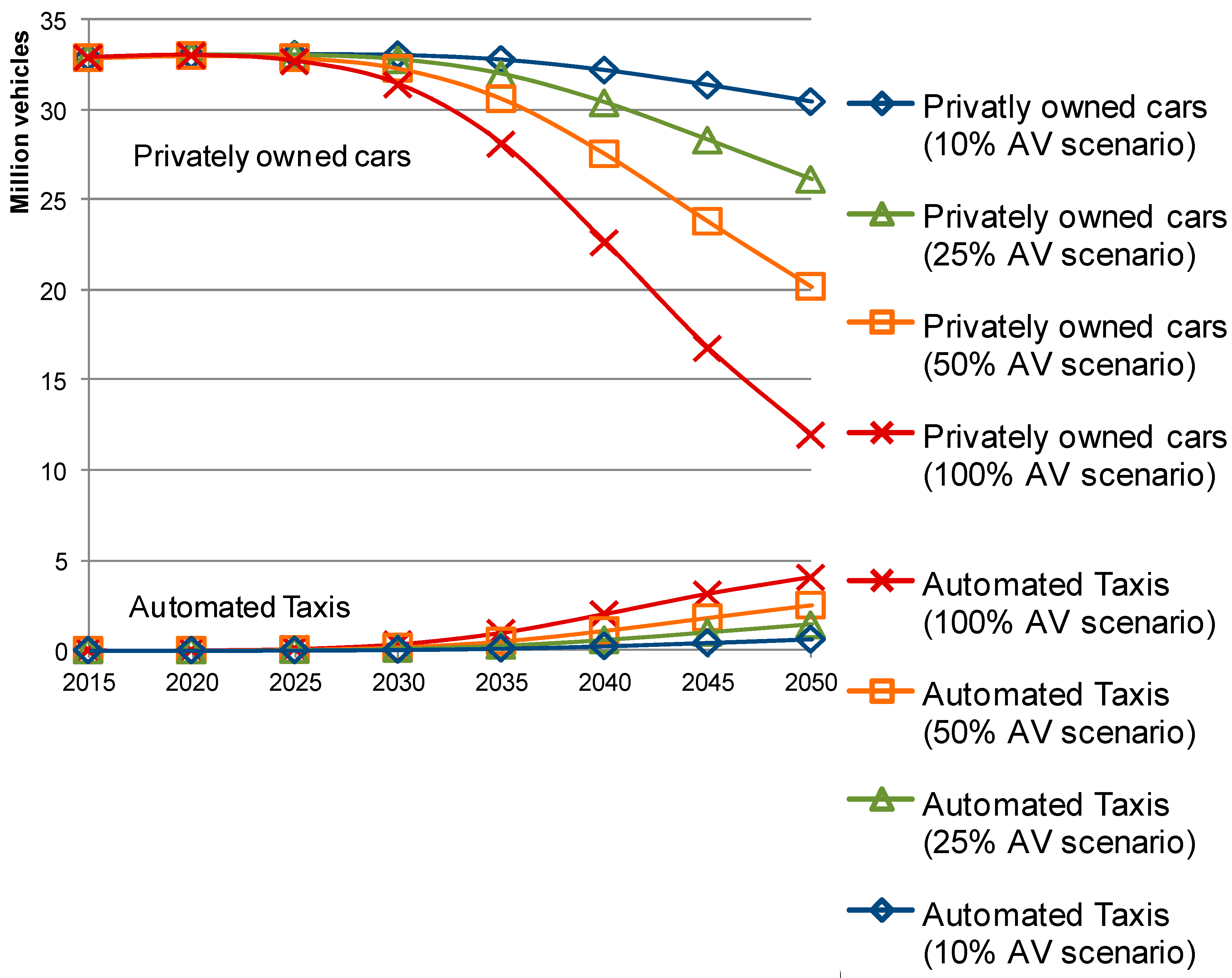

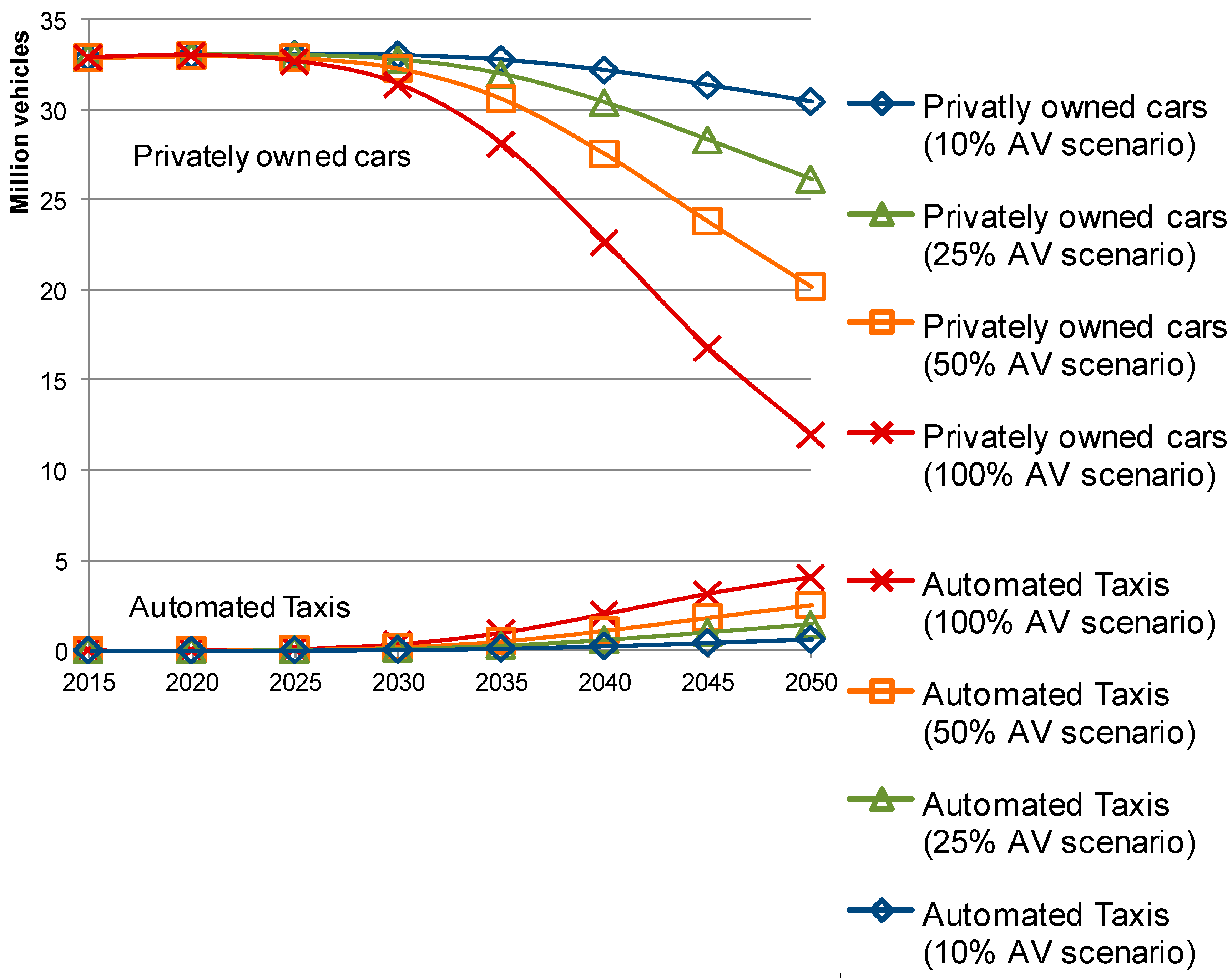

3.5. The Role of Automated Vehicles and Novel Business Models

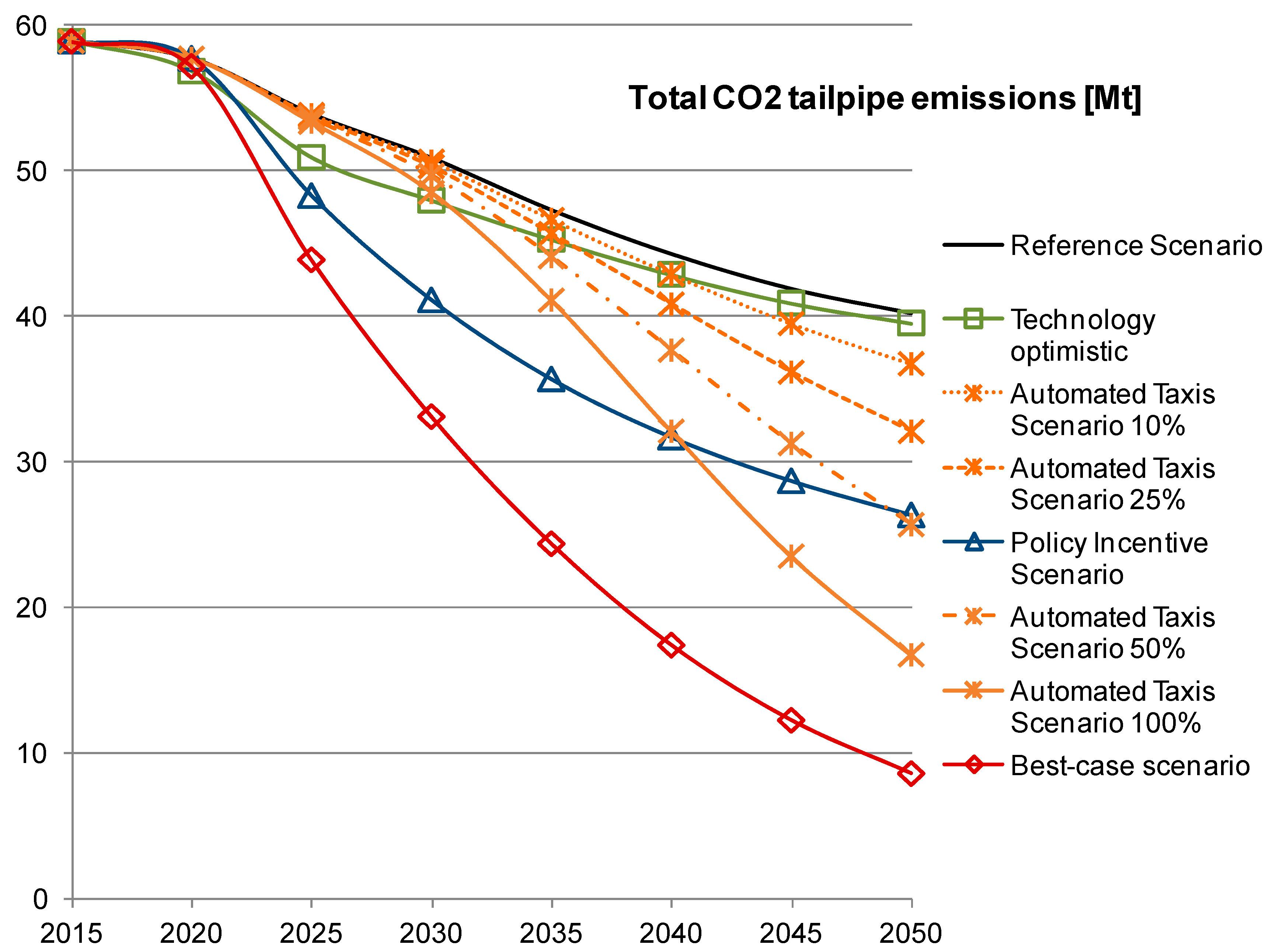

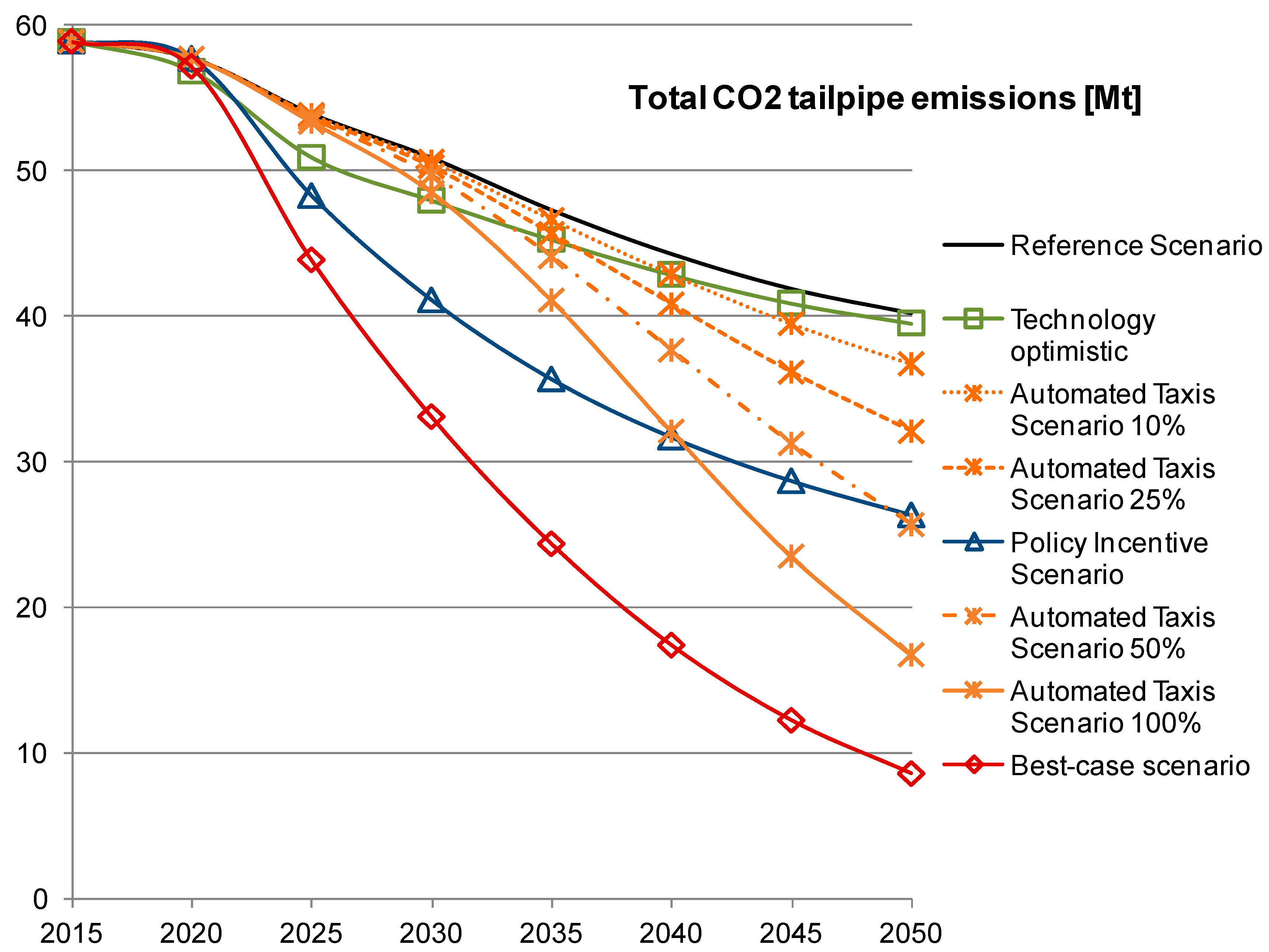

3.6. Bringing Everything Together—The Best-Case Scenario

4. Discussion

Acknowledgments

Author Contributions

Conflicts of Interest

References

- IEA. Energy Technology Perspectives 2010: Scenarios and Strategies to 2050; IEA: Paris, France, 2010. [Google Scholar]

- DECC. The Carbon Plan: Delivering Our Low Carbon Future; DECC: London, UK, 2011. [Google Scholar]

- Howey, D.D.; North, D.R.; Martinez-Botas, D.R. Road Transport Technology and Climate Change Mitigation; No. Briefing Paper No. 2; Grantham Institute for Climate Change: London, UK, December 2010. [Google Scholar]

- IEA. Hybrid and Electric Vehicles—The Electric Drive Gains Tractions; IEA: Paris, France, 2013. [Google Scholar]

- IPPC. CLIMATE CHANGE 2014 Synthesis Report; IPPC: Rome, Italy, 2014. [Google Scholar]

- McKinsey & Company. A Portfolio of Power-Trains for Europe: A Fact-Based Analysis—The Role of Battery Electric Vehicles, Plug-In Hybrids and Fuel Cell Electric Vehicles; McKinsey & Company: New York, NY, USA, 2010. [Google Scholar]

- Mazur, C.; Contestabile, M.; Offer, G.J.; Brandon, P.N. Assessing and comparing German and UK transition policies for electric mobility. Environ. Innov. Soc. Transit. 2015, 14, 84–100. [Google Scholar]

- ICCT. Driving Electrification a Global Comparison of Fiscal Incentive Policy for Electric Vehicles; ICCT: Washington, DC, USA, May 2014. [Google Scholar]

- IEA. Energy Technology Perspective; IEA: Paris, France, 2014. [Google Scholar]

- Geels, F.W. Processes and patterns in transitions and system innovations: Refining the co-evolutionary multi-level perspective. Technol. Forecast. Soc. Chang. 2005, 72, 681–696. [Google Scholar]

- Jacobsson, S.; Bergek, A. Transforming the energy sector: The evolution of technological systems in renewable energy technology. Ind. Corp. Chang. 2004, 13, 815–849. [Google Scholar]

- Shove, E.; Walker, G. CAUTION! Transitions ahead: Politics, practice, and sustainable transition management. Environ. Plan. A 2007, 39, 763–770. [Google Scholar]

- Teubal, M. What is the systems perspective to Innovation and Technology Policy (ITP) and how can we apply it to developing and newly industrialized economies? J. Evol. Econ. 2002, 12, 233–257. [Google Scholar]

- Unruh, G.C. Understanding carbon lock-in. Energy Policy 2000, 28, 817–830. [Google Scholar]

- Jacobsson, S.; Bergek, A. Innovation system analyses and sustainability transitions: Contributions and suggestions for research. Environ. Innov. Soc. Transit. 2011, 1, 41–57. [Google Scholar]

- Markard, J.; Raven, R.; Truffer, B. Sustainability transitions: An emerging field of research and its prospects. Res. Policy 2012, 41, 955–967. [Google Scholar]

- Van Den Bergh, J.C.J.M.; Truffer, B.; Kallis, G. Environmental innovation and societal transitions: Introduction and overview. Environ. Innov. Soc. Transit. 2011, 1, 1–23. [Google Scholar]

- Collantes, G.; Sperling, D. The origin of California’s zero emission vehicle mandate. Transp. Res. Part A Policy Pract. 2008, 42, 1302–1313. [Google Scholar]

- Kieckhafer, K.; Walther, G.; Axmann, J.; Spengler, T. Integrating agent-based simulation and system dynamics to support product strategy decisions in the automotive industry. In Proceedings of the 2009 Winter Simulation Conference (WSC), Austin, TX, USA, 13–16 December 2009; pp. 1433–1443. [Google Scholar]

- Schwanen, T.; Banister, D.; Anable, J. Scientific research about climate change mitigation in transport: A critical review. Transp. Res. Part A Policy Pract. 2011, 45, 993–1006. [Google Scholar] [Green Version]

- Tran, M.; Banister, D.; Bishop, J.D.K.; McCulloch, M.D. Realizing the electric-vehicle revolution. Nat. Clim. Chang. 2012, 2, 328–333. [Google Scholar]

- Auvinen, H.; Ruutu, S.; Tuominen, A.; Ahlqvist, T.; Oksanen, J. Process supporting strategic decision-making in systemic transitions. Technol. Forecast. Soc. Chang. 2015, 94, 97–114. [Google Scholar]

- Bakker, S.; Trip, J.J. Policy options to support the adoption of electric vehicles in the urban environment. Transp. Res. Part D Transp. Environ. 2013, 25, 18–23. [Google Scholar]

- Offer, G.J. Automated Vehicles and Electrification of Transport. Energy Environ. Sci. 2015, 8, 26–30. [Google Scholar]

- Struben, J.; Sterman, J. Transition challenges for alternative fuel vehicle and transportation systems. Environ. Plan. B Plan. Des. 2008, 35, 1070–1097. [Google Scholar]

- Struben, J.J.R. Essays on Transition Challenges for Alternative Propulsion Vehicles and Transportation Systems; Massachusetts Institute of Technology, Sloan School of Management: Cambridge, MA, USA, 2006. [Google Scholar]

- Greenblatt, J.B.; Saxena, S. Autonomous taxis could greatly reduce greenhouse-gas emissions of US light-duty vehicles. Nat. Clim. Chang. 2015, 5, 860–863. [Google Scholar]

- Keles, D.; Wietschel, M.; Most, D.; Rentz, O. Market penetration of fuel cell vehicles-Analysis based on agent behaviour. Int. J. Hydrogen Energy 2008, 33, 4444–4455. [Google Scholar]

- Meyer, P.E.; Winebrake, J.J. Modeling technology diffusion of complementary goods: The case of hydrogen vehicles and refueling infrastructure. Technovation 2009, 29, 77–91. [Google Scholar]

- Shepherd, S.; Bonsall, P.; Harrison, G. Factors affecting future demand for electric vehicles: A model based study. Transp. Policy 2012, 20, 62–74. [Google Scholar]

- Charalabidis, Y.; Loukis, E.; Androutsopoulou, A. Enhancing Participative Policy Making through Modelling and Simulation: A State of the Art Review. In Proceedings of the European, Mediterranean & Middle Eastern Conference on Information Systems, Athens, Greece, 30–31 May 2011. [Google Scholar]

- Sterman, J. Business Dynamics; Irwin: Martinsville, OH, USA, 2000. [Google Scholar]

- Mazur, C.; Contestabile, M.; Offer, G.J.; Brandon, N.P. Understanding the drivers of fleet emission reduction activities of the German car manufacturers. Environ. Innov. Soc. Transit. 2015, 16, 3–21. [Google Scholar]

- Budde, B.; Alkemade, F.; Weber, K.M. Expectations as a key to understanding actor strategies in the field of fuel cell and hydrogen vehicles. Technol. Forecast. Soc. Chang. 2012, 79, 1072–1083. [Google Scholar]

- Jänicke, M.; Jacob, K. Lead markets for environmental innovations: A new role for the nation state. Glob. Environ. Polit. 2004, 4, 29–46. [Google Scholar]

- UK Department for Transport. Public Attitudes to Electric Vehicles; UK Department for Transport: London, UK, June 2014.

- Augustin, N.H.; Cummins, R.P.; French, D.D. Exploring spatial vegetation dynamics using logistic regression and a multinomial logit model. J. Appl. Ecol. 2001, 38, 991–1006. [Google Scholar]

- Contestabile, M. A Model-Based Analysis of European Policies to Support Hydrogen Fuel Cells in Road Transport. Ph.D. Thesis, Imperial College London, London, UK, 2012. [Google Scholar]

- Supple, D.R. Managing the Transition toward Self-Sustaining Alternative Fuel Vehicle Markets: Policy Analysis Using a Dynamic Behavioral Spatial Model. Ph.D. Thesis, Massachusetts Institute of Technology, Cambridge, MA, USA, 2007. [Google Scholar]

- UNECE Transport Division. ForFITS—User Manual (Chapter 18—Vehicles, Powertrain Choice (Logit)). Available online: http://www.unece.org/trans/theme_forfits.html (accessed on 14 November 2013).

- Hensher, D.A.; Rose, J.M.; Greene, W.H. Applied Choice Analysis: A Primer; Cambridge University Press: Cambridge, UK, 2005. [Google Scholar]

- Koppelman, F.S.; Bhat, C. A Self Instructing Course in Mode Choice Modeling: Multinomial and Nested Logit Models; U.S. Department of Transportation Federal Transit Administration: Washington, DC, USA, 2006.

- Offer, G.J.; Contestabile, M.; Howey, D.A.; Clague, R.; Brandon, N.P. Techno-economic and behavioural analysis of battery electric, hydrogen fuel cell and hybrid vehicles in a future sustainable road transport system in the UK. Energy Policy 2011, 39, 1939–1950. [Google Scholar]

- Kurani, K.S.; Axsen, J.; Caperello, N.; Davies-Shawhyde, J.; Dempster, P.; Kempster, M.; Nesbitt, K.A.; Stillwater, T. Plug-In Hybrid Electric Vehicle (PHEV) Demonstration and Consumer Education, Outreach, and Market Research Program: Volumes I and II; University of California at Davis: Davis, CA, USA, 2010. [Google Scholar]

- Chang, D.; Erstad, D.; Lin, E.; Rice, A.F.; Goh, C.T.; Tsao, A.A.; Snyder, J. Financial Viability of Non-Residential Electric Vehicle Charging Stations; Luskin Center for Innovation: Los Angeles, CA, USA, 2012. [Google Scholar]

- RACFoundation. UK Fuel Market Review; RACFoundation: London, UK, 2013. [Google Scholar]

- E. Institute. Retail Marketing Survey 2013; E. Institute: Glendale, AZ, USA, 2013. [Google Scholar]

- UK H2 Mobility. UK H2 Mobility Project—Refuelling Infrastructure; UK H2 Mobility: London, UK, 2014. [Google Scholar]

- Wiederer, A.; Philip, R. Policy Options for Electric Vehicle Charging Infrastructure in C40 Cities; The National Academies of Sciences, Engineering, and Medicine: Washington, DC, USA, 2010. [Google Scholar]

- Element Energy. Strategies for the Uptake of Electric Vehicles and Associated Infrastructure Implications; Element Energy: Cambridge, UK, 2009. [Google Scholar]

- Bushman, R.M.; Piotroski, J.D.; Smith, A.J. Capital allocation and timely accounting recognition of economic losses. J. Bus. Financ. Account. 2011, 38, 1–33. [Google Scholar]

- US Environmental Protection Agency. Fuel Economy Guide; US Environmental Protection Agency: Washington, DC, USA, 2014.

- AEA. A Review of the Efficiency and Cost Assumptions for Road Transport Vehicles to 2050—Report for the Committee on Climate Change; AEA: Nashville, TN, USA, 2012. [Google Scholar]

- SMMT. SMMTs Electric and ALTERNATIVELY-Fuelled Vehicle Registration Figures for MONTH and the Year-to-Date; SMMT: London, UK, 2014. [Google Scholar]

- Nykvist, B.; Nilsson, M. Rapidly falling costs of battery packs for electric vehicles. Nat. Clim. Chang. 2015, 5, 329–332. [Google Scholar]

- Contestabile, M.; Offer, G.J.; Slade, R.; Jaeger, F.; Thoennes, M. Battery electric vehicles, hydrogen fuel cells and biofuels. Which will be the winner?. Energy Environ. Sci. 2011, 4, 3754–3772. [Google Scholar]

- Davidson, P.; Spinoulas, A. Driving alone versus riding together—How shared autonomous vehicles can change the way we drive. Road Transp. Res. 2016, 25, 51–66. [Google Scholar]

- Fagnant, D.J.; Kockelman, K.M. The travel and environmental implications of shared autonomous vehicles, using agent-based model scenarios. Transp. Res. Part C Emerg. Technol. 2014, 40, 1–13. [Google Scholar]

- Clark, B.; Parkhurst, G.; Ricci, M. Understanding the Socioeconomic Adoption Scenarios for Autonomous Vehicles: A Literature Review; University of the West of England, Bristol: Bristol, UK, 2016. [Google Scholar]

- Cohen, T.; Jones, P.; Cavoli, C. Social and Behavioural Questions Associated with Automated Vehicles; UCL Transport Institute: London, UK, 2017. [Google Scholar]

- Hörl, S.; Ciari, F.; Axhausen, K.W. Recent perspectives on the impact of autonomous vehicles. In Arbeitsberichte Verkehrs-und Raumplan; Institute for Transport Planning and System: Zürich, Switzerland, 2016. [Google Scholar]

- Schreurs, M.A.; Steuwer, S.D. Autonomous driving-political, legal, social, and sustainability dimensions. In Autonomous Driving: Technical, Legal and Social Aspects; Springer: Berlin, Germany, 2016; pp. 149–171. [Google Scholar]

- Langdon, P.; Politis, I.; Bradley, M.; Skrypchuk, L.; Mouzakitis, A.; Clarkson, J. Obtaining design requirements from the public understanding of driverless technology. In Proceedings of the International Conference on Applied Human Factors and Ergonomics, Los Angeles, CA, USA, 17–21 July 2017; pp. 749–759. [Google Scholar]

- Politis, I.; Langdon, P.; Bradley, M.; Skrypchuk, L.; Mouzakitis, A.; Clarkson, P.J. Designing autonomy in cars: A survey and two focus groups on driving habits of an inclusive user group, and group attitudes towards autonomous cars. In Proceedings of the International Conference on Applied Human Factors and Ergonomics, Los Angeles, CA, USA, 17–21 July 2017; pp. 161–173. [Google Scholar]

- MIT Technology Review. How Do You Design an Autonomous Car from Scratch? MIT Technology Review: Cambridge, MA, USA, 2017. [Google Scholar]

- Goodbody. Economic Review of the Small Public Service Vehicle Industry; Goodbody Economic Consultants in Association with Faber Maunsell and IMS Millward Brown (Commission for Taxi Regulation); Goodbody: London, UK, 2014. [Google Scholar]

- IEEE. News Release on Intelligent Transportation System. 2012. Available online: http://www.ieee.org/about/news/2012/5september_2_2012.html (accessed on 30 October 2017).

- Sprei, F. Disrupting mobility. Energy Res. Soc. Sci. 2017, 37, 238–242. [Google Scholar]

- Van der Vooren, A.; Brouillat, E. Evaluating CO2 reduction policy mixes in the automotive sector. Environ. Innov. Soc. Transit. 2015, 14, 60–83. [Google Scholar]

- Kohler, J.; Whitmarsh, L.; Nykvist, B.; Schilperoord, M.; Bergman, N.; Haxeltine, A. A transitions model for sustainable mobility. Ecol. Econ. 2009, 68, 2985–2995. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Vehicle stock | |

| Vehicle scrapping | |

| Total vehicle demand | |

| Annual purchase of each vehicle type | |

| Probability to choose a certain vehicle type | with U being identical for deterministic component V |

| Actual market share of each vehicle type | |

| Utility for each vehicle type | |

| Total cost of Ownership | |

| Recharging station availability | |

| Station availability (compared to other stations) | |

| Hydrogen station availability compared to theoretically needed number of stations | |

| Hydrogen station availability in comparison to hydrogen vehicles | |

| Total recharging capacity at public stations | |

| Total change in Rapid and Standard chargers | . |

| Annual revenues for each charger | |

| Annual recharging infrastructure cost (similar for hydrogen infrastructure) | |

| Average recharging time |

| Customer | |||

|---|---|---|---|

| Name of Variable | Value | Unit | Comment |

| vehicle stock ICEV (t = 2011) | 33,000,000 | vehicles | initial vehicle stock derived from SMMT reports |

| vehicle stock HEVs/PHEV (t = 2011) | 100,000 | vehicles | |

| vehicle stock BEV (t = 2011) | 2000 | vehicles | |

| vehicle stock FCEV (t = 2011) | 0 | vehicles | |

| change in vehicle demand | 1 | percent | Annual increase in sales |

| scale factor ICEV µ | 1 | - | Determined through calibration based upon historical data. The scale factor for ICEV has been left at 1. Then the PHEV and BEV factors have been adapted iteratively until the modelled sales numbers matched the real ones for the period of 2011–2013. The factor for FCEVs is the same as the ICEV factor as both vehicle drive trains are similar for the user. |

| scale factor PHEV µ | 1.69 | - | |

| scale factor BEV µ | 0.985 | - | |

| scale factor FCEV µ | 1 | - | |

| weight of TCO | 50 | % | from UK government study on customer preferences concerning alternative vehicles [36] |

| weight of vehicle range | 25 | % | |

| weight of infrastructure availability | 12.5 | % | |

| weight of refuelling time | 12.5 | % | |

| annual km driven | 10,500 | km | [36] |

| PHEV kilometres driven in EV mode | 41 | % | Calculation based upon an EV range of an Honda Accord Hybrid of 15 miles and the distribution of miles driven in the UK according to [43] |

| BEVs energy recharged at home | 80 | % | Calculation based upon an EV range of an Mercedes Benz B Class of 85 miles and the distribution of miles driven in the UK according to [43] |

| PHEVs energy charged at public stations | 5 | % | Based on a PHEV usage patterns study [44] where it had been observed that 2 of 34 (ca. 6%) drivers had been charging their vehicles also not at home. |

| Infrastructure | |||

|---|---|---|---|

| Name of Variable | Value | Unit | Comment |

| petrol price (t = 2010) | 0.7 | €/litre | Pre-tax predictions based on [6] |

| electricity price (t = 2010) | 100 | €/MWh | Pre-tax predictions based on [6] |

| hydrogen price (t = 2010) | 16.6 | €/kg | Pre-tax predictions based on [6] |

| mark-up electricity cost | 80 | percent | Based upon proposed scenarios by [45] |

| mark-up H2 cost | 6 | percent | Typical margins of petrol stations [46] |

| ratio of petrol stations per vehicle | 1/3660 | Stations per vehicle | Based upon historical data [46,47]. The parameter has been determined with the help of current number petrol stations and the total number of vehicles on UK’s roads |

| total number of hydrogen stations needed | 1150 | stations | Based upon estimate of [48] |

| initial stock of Class 2 chargers | 1670 | Public chargers | According to http://chargemap.com/stats/united-kingdom there are in total 1758 charging points. 95% correspond to Class 2 chargers. |

| initial stock of Rapid chargers | 400 | Public chargers | According to http://chargemap.com/stats/united-kingdom there are in total 1758 charging points. 5% correspond to Rapid chargers. |

| initial stock of hydrogen stations | 10 | stations | Estimate based upon h2stations.org |

| average power of domestic charger | 3 | kW | [49] |

| average power of Class 2 charger | 3 | kW | [49] |

| average power of Rapid charger | 50 | kW | [49] |

| lifespan of EV chargers | 10 | Years | [49] |

| lifespan of hydrogen stations | 30 | Years | [49] |

| ratio of BEV owners with domestic charging capability | 80 | percent | Based upon demographics of BEV and PHEV users [50] |

| installation cost of Class 2 charger | 4000 | € | [49] |

| installation cost of Rapid charger | 50,000 | € | [49] |

| operation & maintenance cost of EV charger | 10 | percent | in percent of initial purchase cost [49] |

| expected ROCI (Return on Capital Invested) for infrastructure | 5.5 | percent | Based upon study undertaken on average return rates [51] |

| Automotive Parameters | |||

|---|---|---|---|

| Name of Variable | Value | Unit | Comment |

| vehicle lifetime | 14.5 | years | Calibrated. With 14.5 years for the scrapping the total demand for vehicles corresponds to real data provided by SMMT |

| ICEV petrol consumption | 0.078 | L/km | Based upon the fuel economy of a Honda Accord [52] |

| PHEV petrol consumption | 0.051 | L/km | Based upon the fuel economy of a Honda Accord in HEV mode [52] |

| PHEV electricity consumption | 0.23 | kWh/km | Based upon a Honda Accord in EV mode [52] |

| BEV electricity consumption | 0.18 | kWh/km | Based upon a Nissan Leaf [52] |

| FCEV hydrogen consumption | 0.0104 | kg/km | Based upon a Honda FCX Clarity [52] |

| ICEV range (t = 2010) | 900 | km | For first year derived from [6] |

| PHEV range (t = 2010) | 800 | km | For first year derived from [6] |

| BEV range (t = 2010) | 130 | km | For first year derived from [6] |

| FCEV range (t = 2010) | 700 | km | For first year derived from [6] |

| refuelling time ICEV | 2 | min | Own experience |

| refuelling time PHEV | 2 | min | Own experience |

| refuelling time FCEV | 4 | min | http://www.ukh2mobility.co.uk/fcevs/ |

| ICEV price (t = 2010) | 20,000 | € | For first year derived from [6], updated with 2014 prices based on http://www.greencarsite.co.uk |

| PHEV price (t = 2010) | 47,000 | € | For first year derived from [6], updated with 2014 prices based on http://www.greencarsite.co.uk |

| BEV price (t = 2010) | 85,000 | € | For first year derived from [6], updated with 2014 prices based on http://www.greencarsite.co.uk |

| FCEV price (t = 2010) | 160,000 | € | For first year derived from [6], updated with 2014 prices based on http://www.greencarsite.co.uk |

| Year when sale of FCEV starts | 2016 | Expected sales start of FCEVs in the UK | |

| in km | 2010 | 2050 |

|---|---|---|

| ICEV | 900 | 1300 |

| PHEV | 800 | 1200 |

| BEV | 130 | 220 1 |

| FCEV | 700 | 850 |

| 2010 | 2015 | 2020 | 2030 | 2035 | 2040 | 2050 | |

|---|---|---|---|---|---|---|---|

| Petrol [€/L] | 0.7 | 0.75 | 0.73 | 0.85 | 0.88 | 0.92 | 0.98 |

| Electricity [€/MWh] | 100 | 120 | 140 | 140 | 140 | 135 | 125 |

| Hydrogen [€/kg] | 16.6 | 9.9 | 6.6 | 5 | 4.7 | 4.5 | 4.4 |

| in € | 2015 | 2020 | 2030 | 2040 | 2050 |

|---|---|---|---|---|---|

| ICEV | 20,500 | 22,000 | 22,000 | 22,000 | 21,000 |

| PHEV | 41,800 | 34,000 | 25,000 | 24,000 | 23,500 |

| BEV | 43,000 | 36,000 | 26,000 | 24,500 | 23,500 |

| FCEV | 60,000 | 38,000 | 26,000 | 24,700 | 23,700 |

| PHEV HEV (Historic Data) | PHEV HEV (Modelled) | EV (Historic Data) | EV (Modelled) | |

|---|---|---|---|---|

| 2011 | 23,000 | 21,918 | 1100 | 1082 |

| 2012 | 27,000 | 26,178 | 1300 | 1564 |

| 2013 | 30,000 | 31,443 | 2500 | 2449 |

| in € | 2015 | 2020 | 2030 | 2040 | 2050 | |

|---|---|---|---|---|---|---|

| ICEV | 20,500 | 22,000 | 22,000 | 22,000 | 21,000 | |

| EV optimistic scenario | PHEV | 41,800 | 29,000 (34,000) | 25,000 | 24,000 | 23,500 |

| BEV | 43,000 | 30,500 (36,000) | 26,000 | 24,500 | 23,500 | |

| FCEV | 60,000 | 34,500 (38,000) | 26,000 | 24,700 | 23,700 |

| Infrastructure Availability | Recharging Duration | Range | TCO | |

|---|---|---|---|---|

| Initial weights (2015) | 12.5% | 12.5% | 25% | 50% |

| Adapted weights (2025) | 5% | 5% | 10% | 80% |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Mazur, C.; Offer, G.J.; Contestabile, M.; Brandon, N.B. Comparing the Effects of Vehicle Automation, Policy-Making and Changed User Preferences on the Uptake of Electric Cars and Emissions from Transport. Sustainability 2018, 10, 676. https://doi.org/10.3390/su10030676

Mazur C, Offer GJ, Contestabile M, Brandon NB. Comparing the Effects of Vehicle Automation, Policy-Making and Changed User Preferences on the Uptake of Electric Cars and Emissions from Transport. Sustainability. 2018; 10(3):676. https://doi.org/10.3390/su10030676

Chicago/Turabian StyleMazur, Christoph, Gregory J. Offer, Marcello Contestabile, and Nigel Brandon Brandon. 2018. "Comparing the Effects of Vehicle Automation, Policy-Making and Changed User Preferences on the Uptake of Electric Cars and Emissions from Transport" Sustainability 10, no. 3: 676. https://doi.org/10.3390/su10030676