A Carbon Price Forecasting Model Based on Variational Mode Decomposition and Spiking Neural Networks

Abstract

:1. Introduction

2. Methodologies

2.1. Variational Mode Decomposition (VMD)

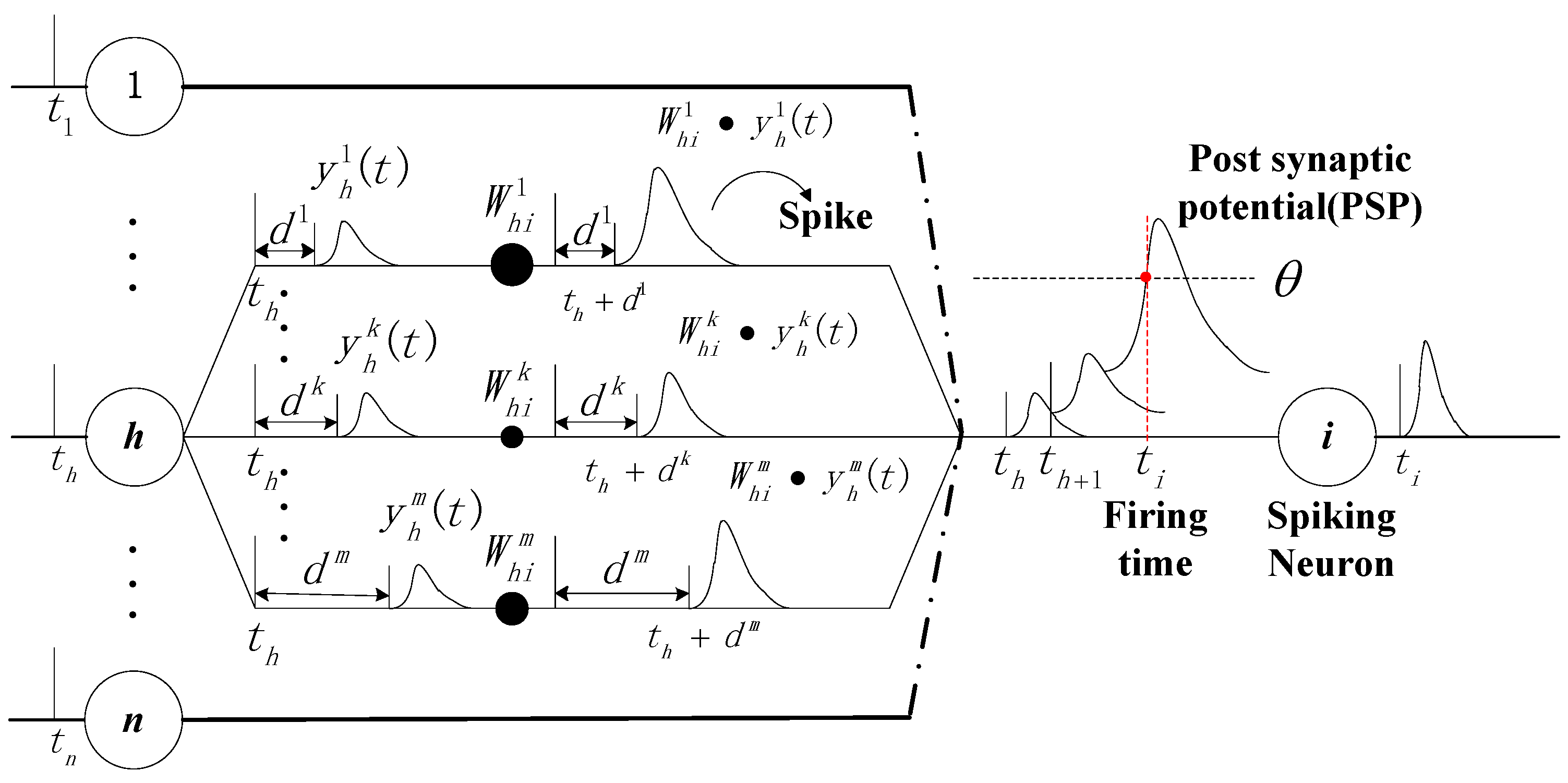

2.2. Spiking Neural Networks (SNNs)

- (1)

- Calculate E for the entire network according to the difference between the actual spike firing time and the desired spike firing time of all neurons j in output layer J, respectively:

- (2)

- Calculate for all neurons j in output layer J:where represents the set of all presynaptic neurons for neuron j.

- (3)

- Calculate for all neurons i in hidden layer I:where and are the set of all postsynaptic neurons and presynaptic neurons for neuron i, respectively.

- (4)

- Adjust the weights and for output layer J and hidden layer I, respectively, according to the network learning rate as follows.

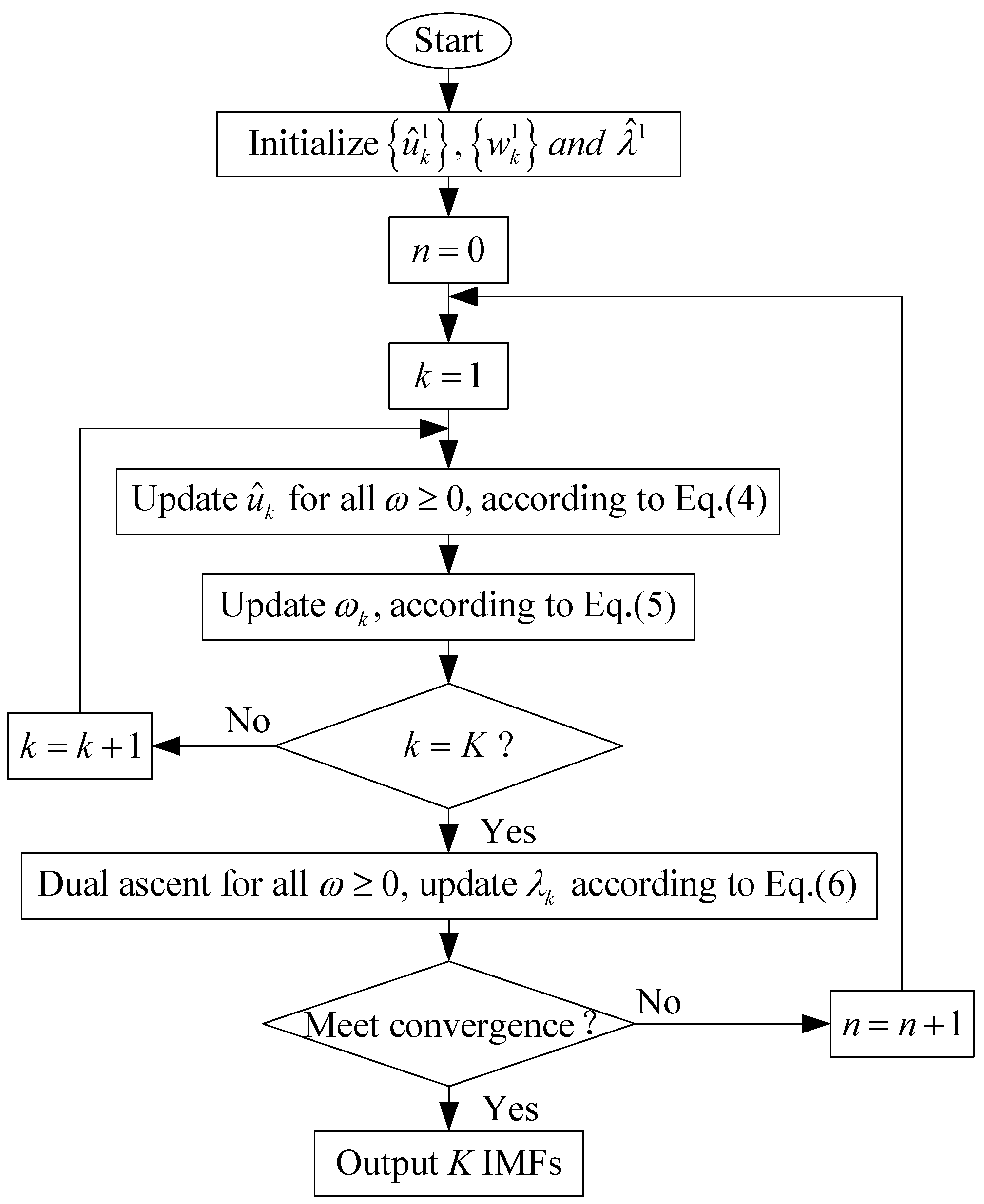

3. The Proposed VMD-SNN Forecasting Model

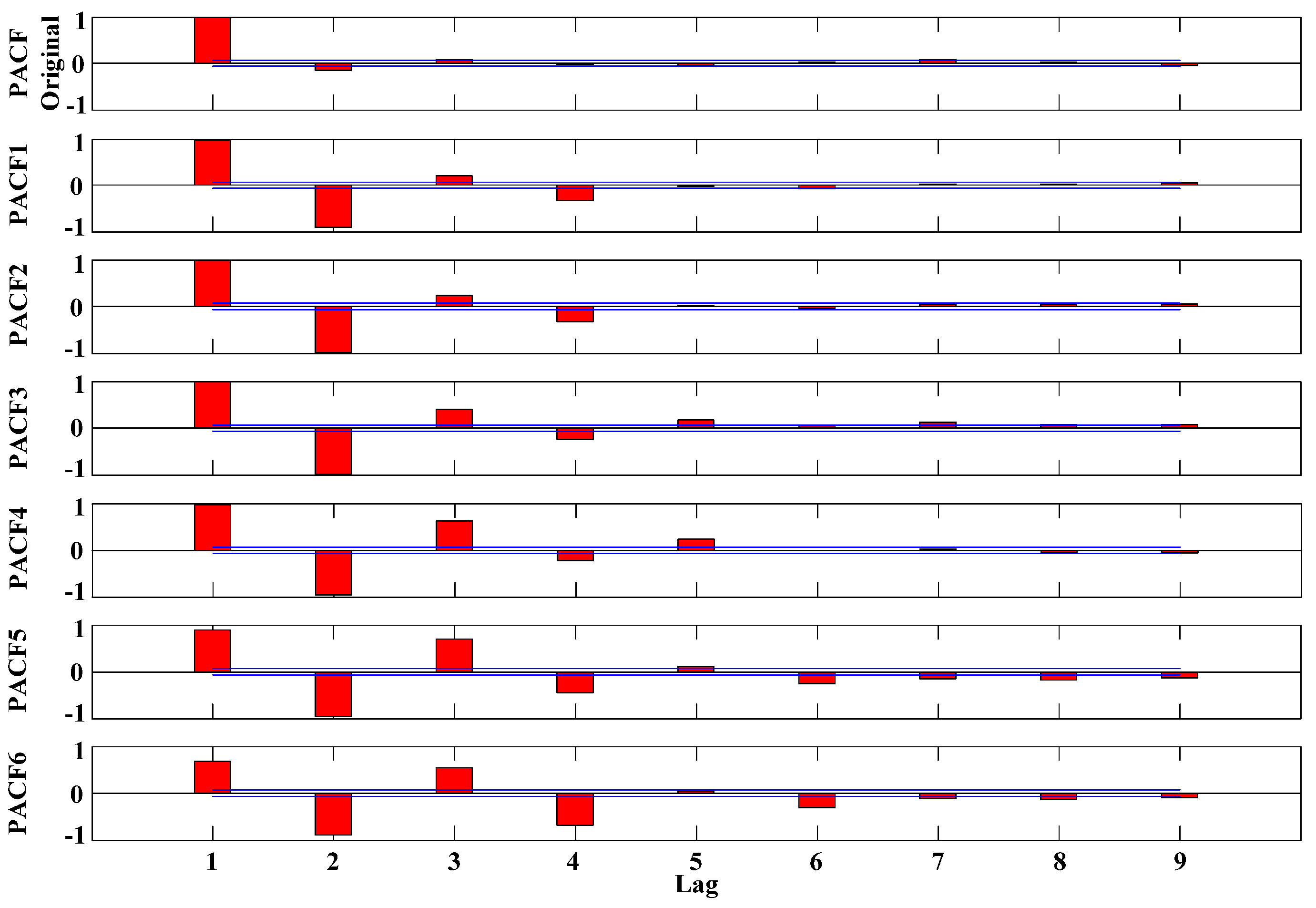

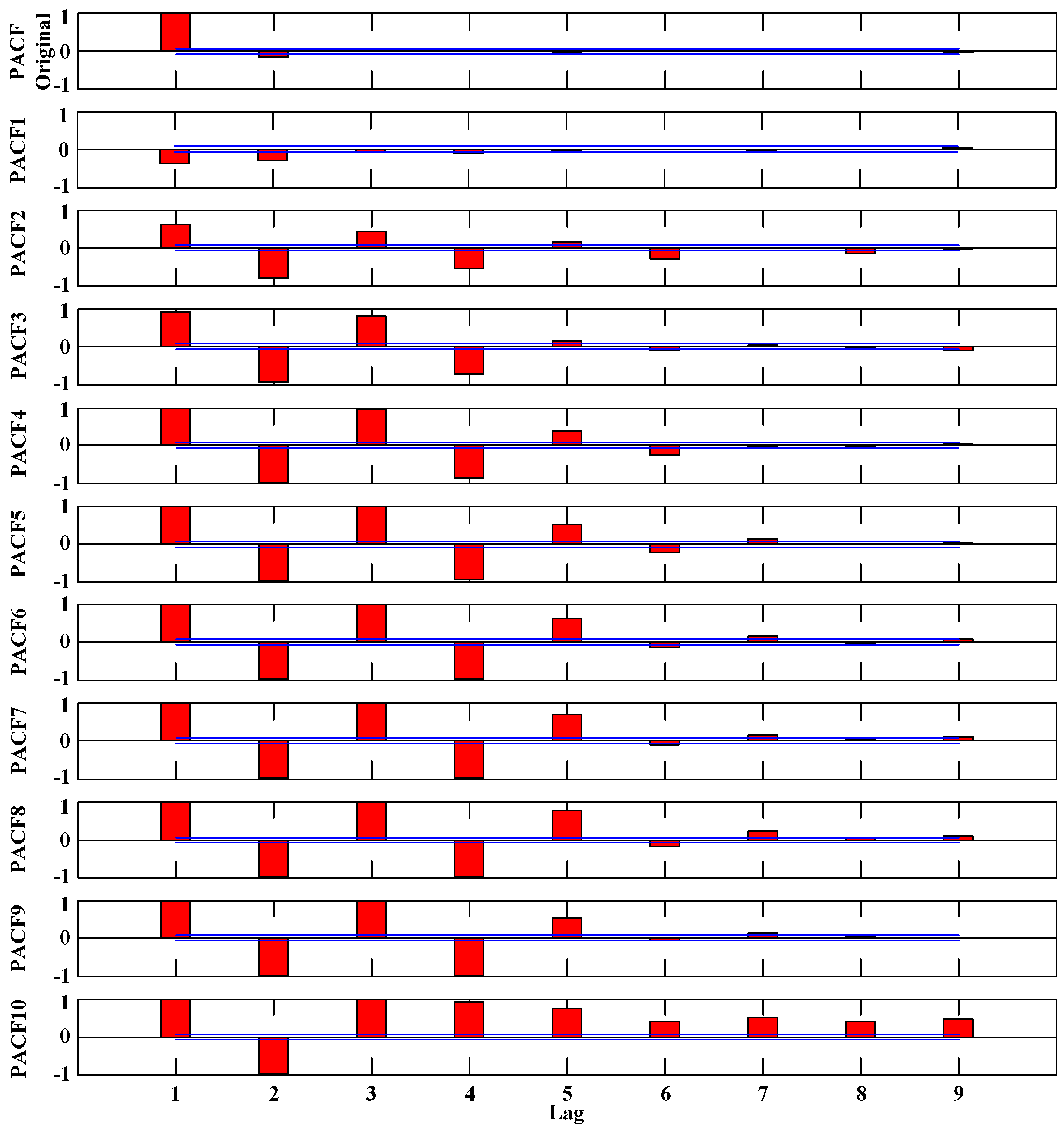

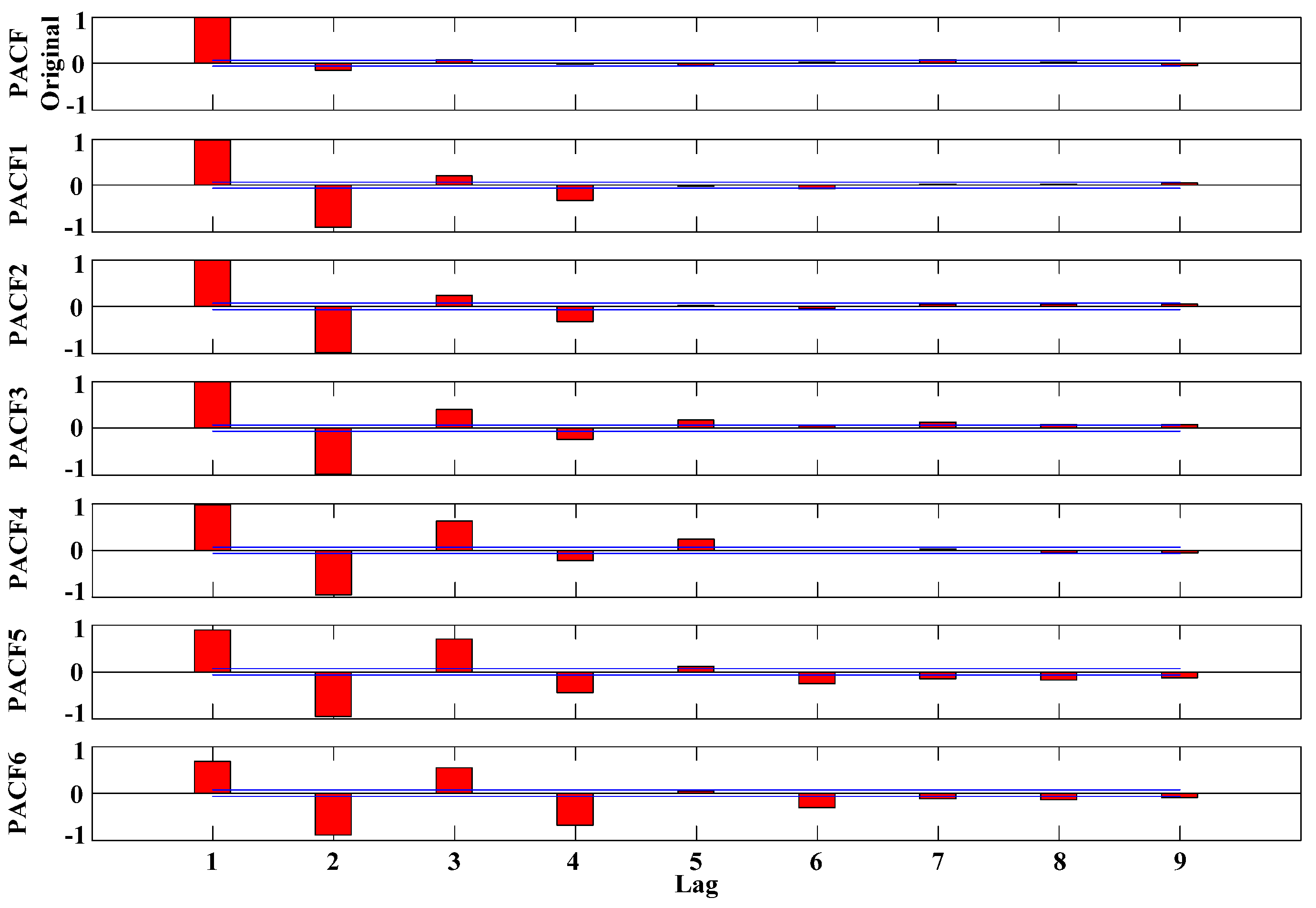

3.1. Determination of Input Variables by PACF

3.2. Overall Procedures of the VMD-SNN Forecasting Model

- Step 1.

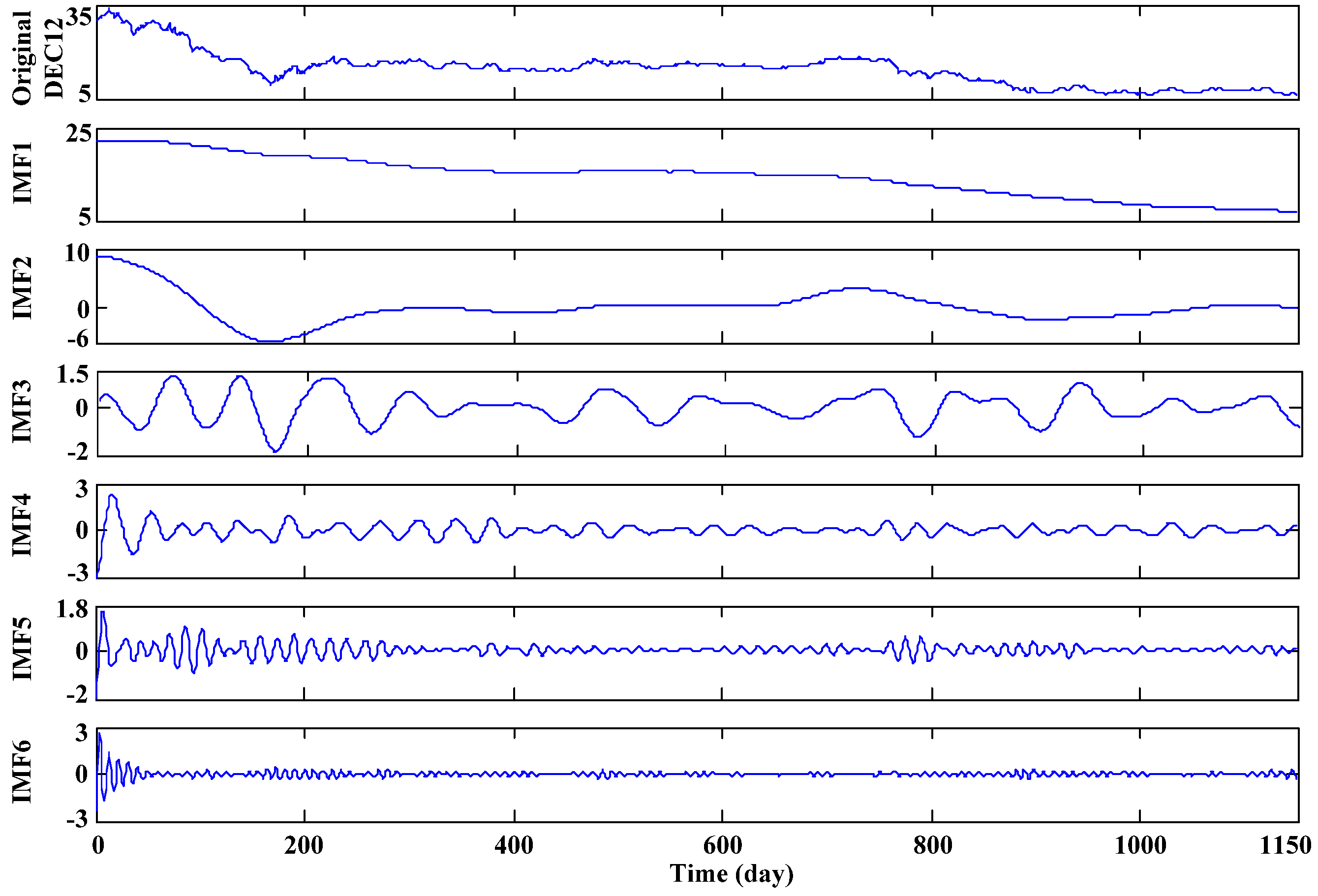

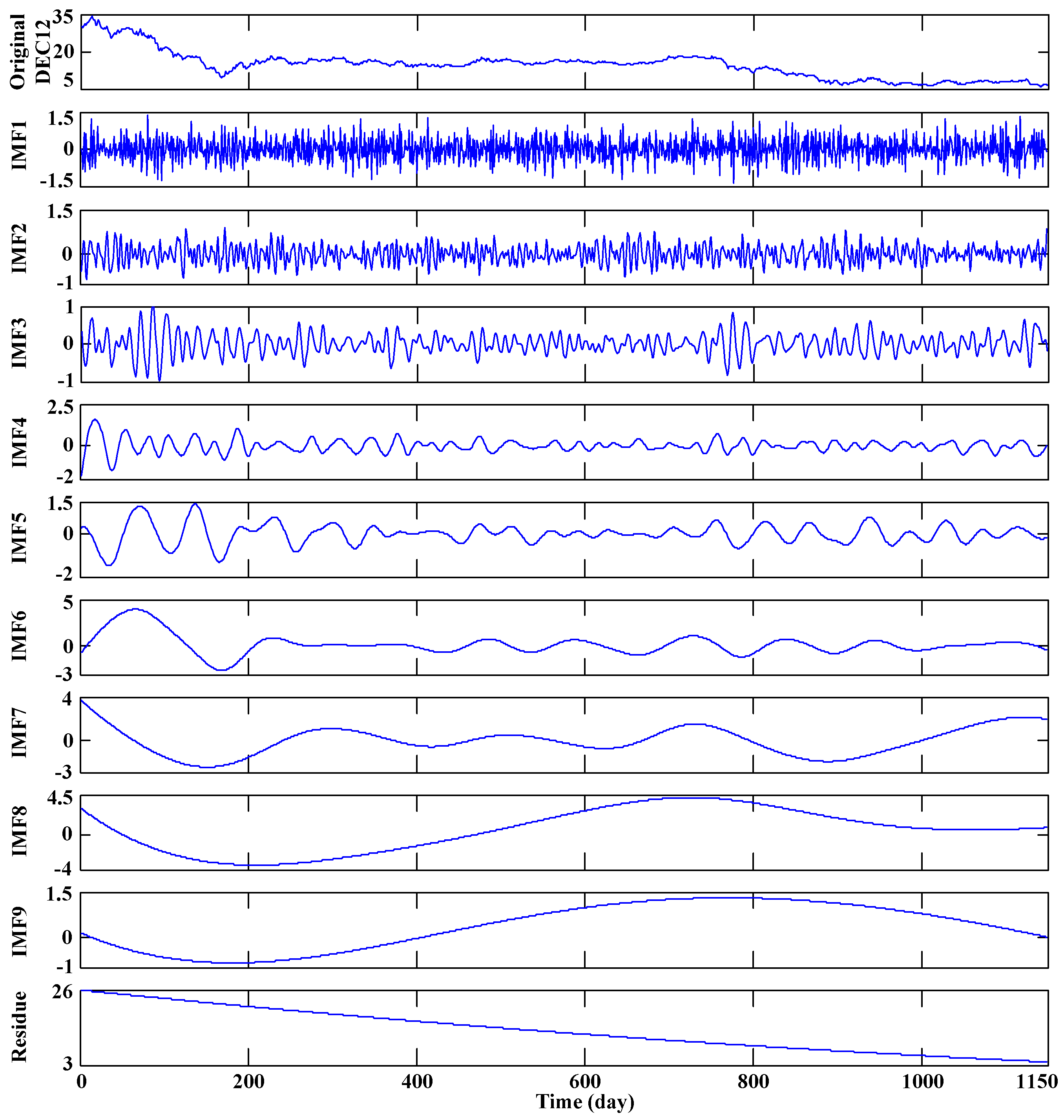

- Apply the VMD algorithm to decompose the original carbon price series into K IMF components (sub-series).

- Step 2.

- For each IMF component, with the output variable , the input variables are determined through observing the partial autocorrelogram via PACF.

- Step 3.

- A three-layer SNN forecasting model is built for each IMF component. Perform SNN training using the training sample prior to importing the test sample into the well-trained SNN model. The output is then the forecasting value of the current IMF component.

- Step 4.

- Aggregate the forecasting results of all the IMF components obtained by the previous steps to produce a combined forecasting result for the original carbon price series.

- Step 5.

- The comprehensive error evaluation criteria proposed in this paper are applied to evaluate and analyze the final forecasting result.

4. Simulation and Results Analysis

4.1. Data Description

4.2. Comprehensive Evaluation Criteria

4.2.1. Evaluation Indexes

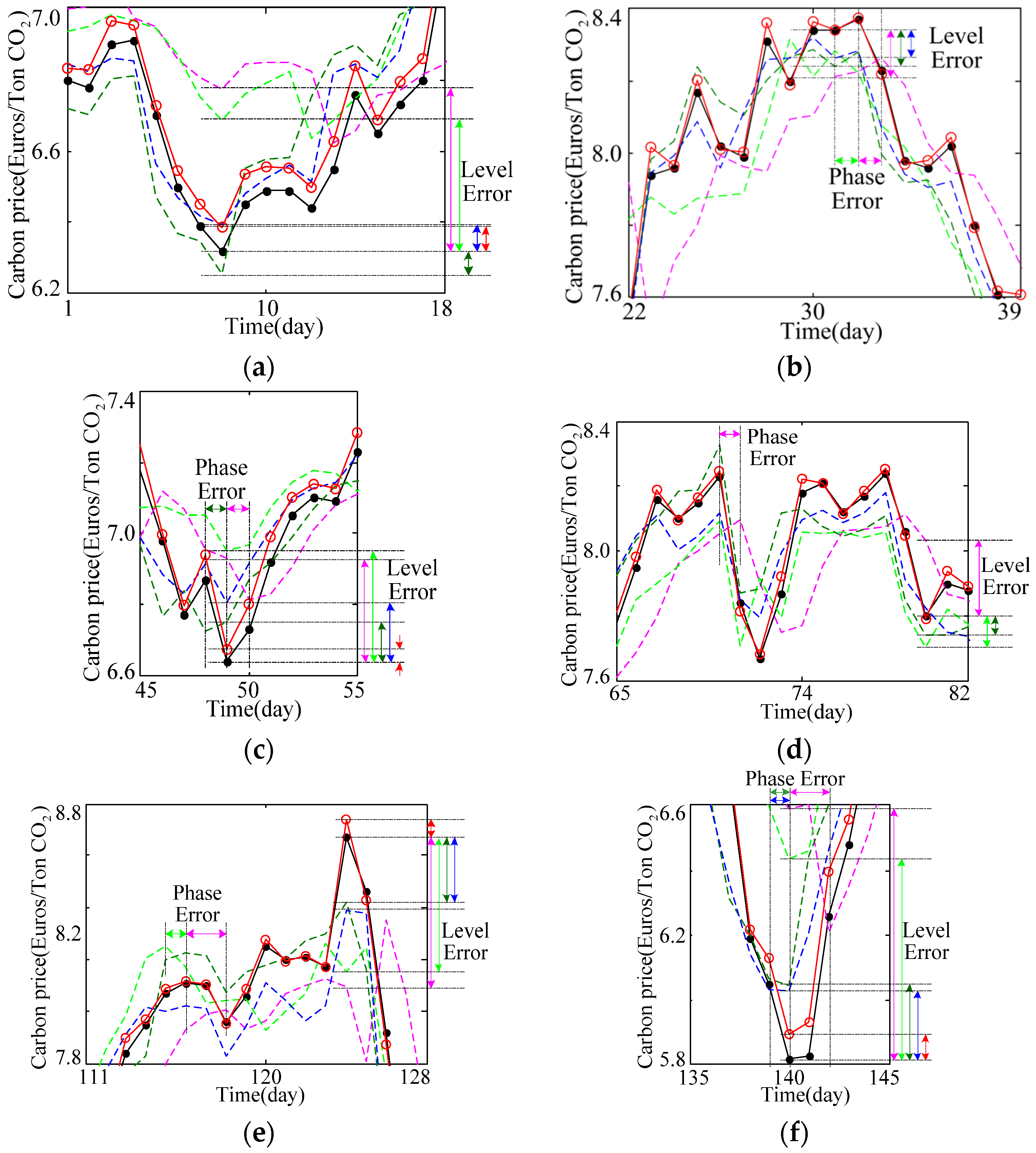

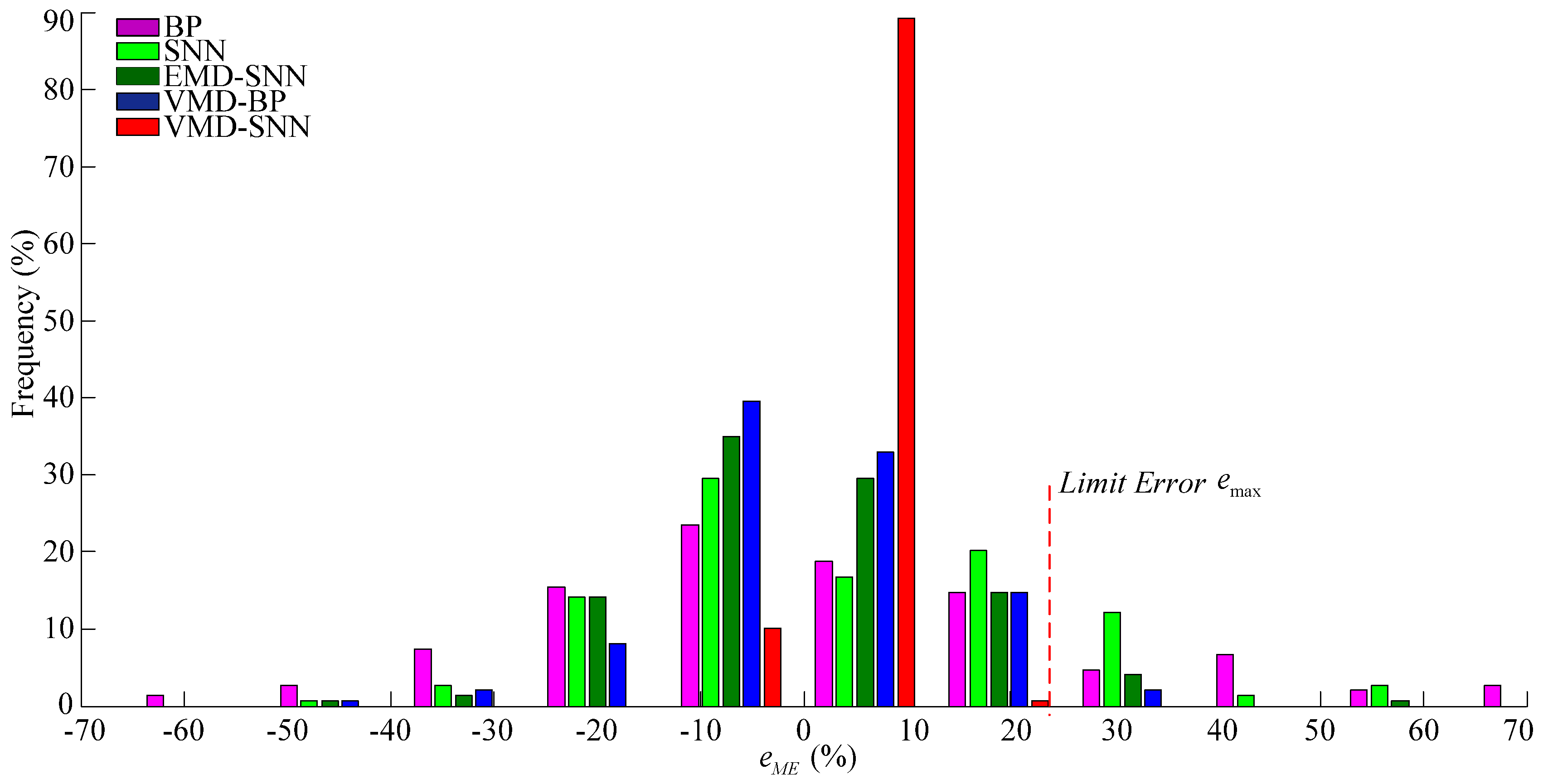

4.2.2. Histogram of the Error Frequency Distribution

4.3. Parameter Setting

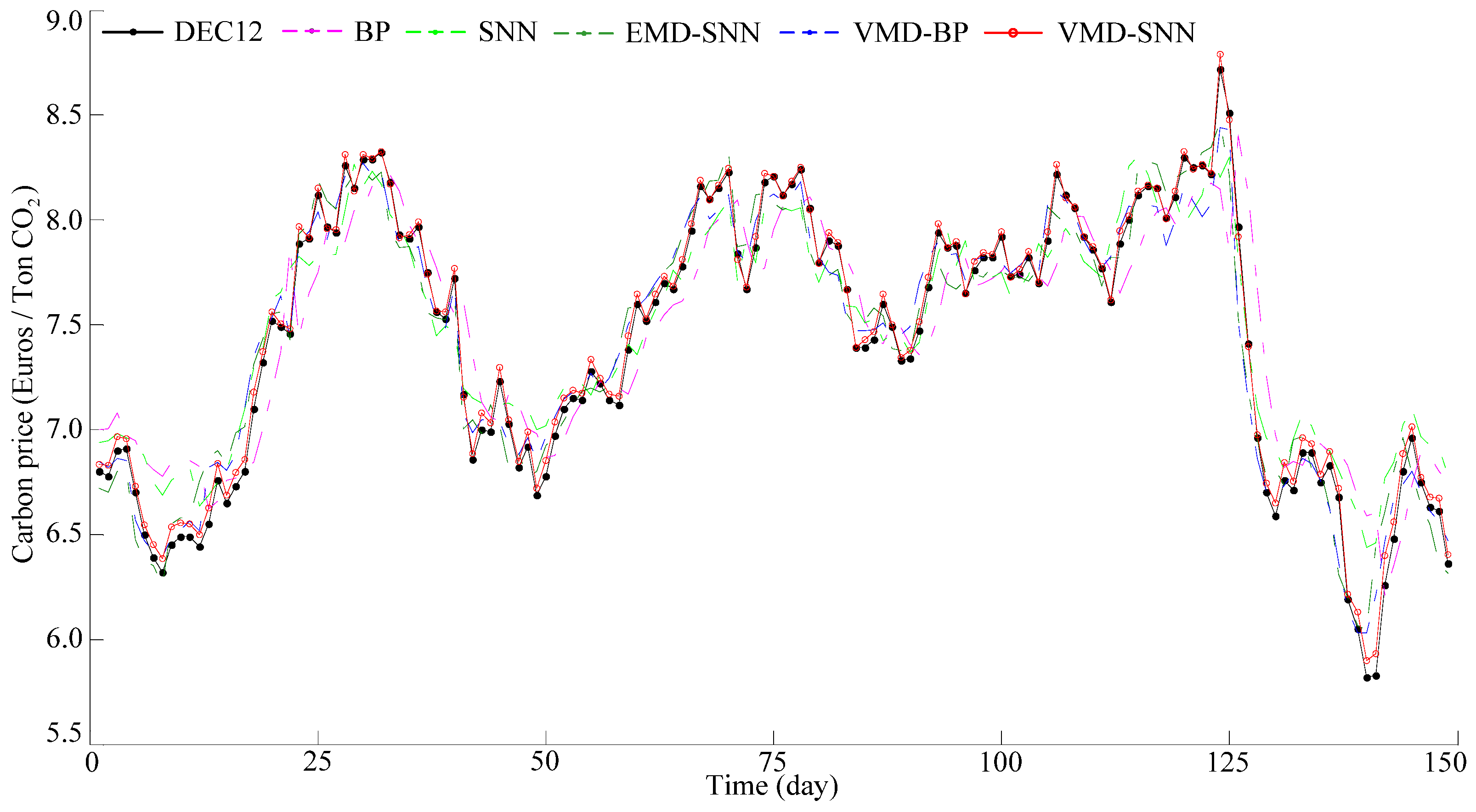

4.4. Results and Analysis

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Series | Mode Decomposition Algorithm | |

|---|---|---|

| VMD | EMD | |

| DEC12 | ||

| IMF1 | ||

| IMF2 | ||

| IMF3 | ||

| IMF4 | ||

| IMF5 | ||

| IMF6 | ||

| IMF7 | — | |

| IMF8 | — | |

| IMF9 | — | |

| Residue | — | |

| Evaluation Indexes | Forecasting Models | ||||

|---|---|---|---|---|---|

| BP | SNN | EMD-SNN | VMD-BP | VMD-SNN | |

| RMSE | 0.2655 | 0.2077 | 0.1528 | 0.1231 | 0.0437 |

| MAE | 0.2062 | 0.1690 | 0.1220 | 0.0955 | 0.0355 |

| MaxAPE (%) | 13.239 | 10.827 | 10.546 | 6.495 | 2.197 |

| 0.9180 | 0.9621 | 0.9709 | 0.9822 | 0.9993 | |

5. Conclusions

Acknowledgments

Author Contributions

Conflicts of Interest

References

- Alberola, E.; Chevallier, J.; Chèze, B. Price drivers and structural breaks in European carbon price 2005–2007. Energy Policy 2008, 36, 787–797. [Google Scholar] [CrossRef]

- Liu, Y.; Huang, G.; Cai, Y. An inexact mix-integer two-stage linear programming model for supporting the management of a low-carbon energy system in China. Energies 2011, 4, 1657–1686. [Google Scholar] [CrossRef]

- Yang, J.; Feng, X.; Tang, Y. A power system optimal dispatch strategy considering the flow of carbon emissions and large consumers. Energies 2015, 8, 9087–9106. [Google Scholar] [CrossRef]

- Zhu, Y.; Li, Y.P.; Huang, G.H. A dynamic model to optimize municipal electric power systems by considering carbon emission trading under uncertainty. Energy 2015, 88, 636–649. [Google Scholar] [CrossRef]

- Chevallier, J. Carbon futures and macroeconomic risk factors: A view from the EU ETS. Energy Econ. 2009, 31, 614–625. [Google Scholar] [CrossRef]

- Wang, Y.; Wu, C. Forecasting energy market volatility using GARCH models: Can multivariate models beat univariate models? Energy Econ. 2012, 34, 2167–2181. [Google Scholar] [CrossRef]

- Tsai, M.T.; Kuo, Y.T. A forecasting system of carbon price in the carbon trading markets using artificial neural network. Int. J. Environ. Sci. Dev. 2013, 4, 163–167. [Google Scholar] [CrossRef]

- Zhu, B.; Wang, P.; Chevallier, J. Carbon price analysis using empirical mode decomposition. Comput. Econ. 2014, 45, 195–206. [Google Scholar] [CrossRef]

- Zhu, B. A novel multiscale combined carbon price prediction model integrating empirical mode decomposition, genetic algorithm and artificial neural network. Energies 2012, 5, 355–370. [Google Scholar] [CrossRef]

- Li, W.; Lu, C. The research on setting a unified interval of carbon price benchmark in the national carbon trading market of China. Appl. Energy 2015, 155, 728–739. [Google Scholar] [CrossRef]

- Maass, W. Networks of spiking neurons: The third generation of neural network models. Neural Netw. 1997, 10, 1659–1671. [Google Scholar] [CrossRef]

- Gerstner, W.; Kistler, W.M. Spiking Neuron Models: Single Neurons, Populations, Plasticity; Cambridge University Press: Cambridge, UK, 2002. [Google Scholar]

- Ponulak, F.; Kasinski, A. Introduction to spiking neural networks: Information processing, learning and applications. Acta Neurobiol. Exp. 2010, 71, 409–433. [Google Scholar]

- Bohte, S.M.; Kok, J.N.; La-Poutre, H. Error-backpropagation in temporally encoded networks of spiking neurons. Neurocomputing 2002, 48, 17–37. [Google Scholar] [CrossRef]

- Rowcliffe, P.; Feng, J. Training spiking neuronal networks with applications in engineering tasks. IEEE Trans. Neural Netw. 2008, 19, 1626–1640. [Google Scholar] [CrossRef] [PubMed]

- Ghosh-Dastidar, S.; Adeli, H. Improved spiking neural networks for EEG classification and epilepsy and seizure detection. Integr. Comput. Aided Eng. 2007, 14, 187–212. [Google Scholar]

- Kulkarni, S.; Simon, S.P.; Sundareswaran, K. A spiking neural network (SNN) forecast engine for short-term electrical load forecasting. Appl. Soft Comput. 2013, 13, 3628–3635. [Google Scholar] [CrossRef]

- Sharma, V.; Srinivasan, D. A spiking neural network based on temporal encoding for electricity price time series forecasting in deregulated markets. In Proceedings of the 2010 IEEE International Joint Conference on Neural Networks (IJCNN), Barcelona, Spain, 18–23 July 2010.

- Lin, Y.; Teng, Z.J. Prediction of grain yield based on spiking neural networks model. In Proceedings of the 3rd IEEE International Conference on Communication Software and Networks (ICCSN), Xi’an, China, 27–29 May 2011.

- Seifert, J.; Uhrig-Homburg, M.; Wagner, M. Dynamic behavior of CO2 spot price. J. Environ. Econ. Manag. 2008, 56, 180–194. [Google Scholar] [CrossRef]

- Zhang, Y.J.; Wei, Y.M. An overview of current research on EU ETS: Evidence from its operating mechanism and economic effect. Appl. Energy 2010, 87, 1804–1814. [Google Scholar] [CrossRef]

- Huang, N.E.; Shen, Z.; Long, S.R.; Wu, M.C.; Shih, H.H.; Zheng, Q.; Yen, N.C.; Tung, C.C.; Liu, H.H. The empirical mode decomposition and the Hilbert spectrum for nonlinear and nonstationary time series analysis. Proc. R. Soc. Lond. A 1998, 454, 903–995. [Google Scholar] [CrossRef]

- Hong, Y.Y.; Yu, T.H.; Liu, C.Y. Hour-ahead wind speed and power forecasting using empirical mode decomposition. Energies 2013, 6, 6137–6152. [Google Scholar] [CrossRef]

- Fan, G.F.; Qing, S.; Wang, H. Support vector regression model based on empirical mode decomposition and auto regression for electric load forecasting. Energies 2013, 6, 1887–1901. [Google Scholar] [CrossRef]

- Dragomiretskiy, K.; Zosso, D. Variational mode decomposition. IEEE Trans. Signal Proc. 2014, 62, 531–544. [Google Scholar] [CrossRef]

- Upadhyay, A.; Pachori, R.B. Instantaneous voiced/non-voiced detection in speech signals based on variational mode decomposition. J. Frankl. Inst. 2015, 352, 2679–2707. [Google Scholar] [CrossRef]

- Lahmiri, S. Long memory in international financial markets trends and short movements during 2008 financial crisis based on variational mode decomposition and detrended fluctuation analysis. Phys. A Stat. Mech. Appl. 2015, 437, 130–138. [Google Scholar] [CrossRef]

- Aneesh, C.; Kumar, S.; Hisham, P.M. Performance comparison of variational mode decomposition over empirical wavelet transform for the classification of power quality disturbances using support vector machine. Procedia Comput. Sci. 2015, 46, 372–380. [Google Scholar] [CrossRef]

- Wang, Y.; Markert, R.; Xiang, J. Research on variational mode decomposition and its application in detecting rub-impact fault of the rotor system. Mech. Syst. Signal Proc. 2015, 60, 243–251. [Google Scholar] [CrossRef]

- Dégerine, S.; Lambert-Lacroix, S. Characterization of the partial autocorrelation function of nonstationary time series. J. Multivar. Anal. 2003, 87, 46–59. [Google Scholar] [CrossRef]

- Guo, Z.; Zhao, W.; Lu, H. Multi-step forecasting for wind speed using a modified EMD-based artificial neural network model. Renew. Energy 2012, 37, 241–249. [Google Scholar]

- Giebel, G.; Brownsword, R.; Kariniotakis, G. The State-of-the-Art in Short-Term Prediction of Wind Power: A Literature Overview, 2nd ed.; ANEMOS. Plus: Risoe DTU, Roskilde, Denmark, 2011. [Google Scholar]

- ICE EUA Futures Contract: Historic Data 2008-2012. Available online: http://www.theice.com (accessed on 24 December 2014).

© 2016 by the authors; licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons by Attribution (CC-BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Sun, G.; Chen, T.; Wei, Z.; Sun, Y.; Zang, H.; Chen, S. A Carbon Price Forecasting Model Based on Variational Mode Decomposition and Spiking Neural Networks. Energies 2016, 9, 54. https://doi.org/10.3390/en9010054

Sun G, Chen T, Wei Z, Sun Y, Zang H, Chen S. A Carbon Price Forecasting Model Based on Variational Mode Decomposition and Spiking Neural Networks. Energies. 2016; 9(1):54. https://doi.org/10.3390/en9010054

Chicago/Turabian StyleSun, Guoqiang, Tong Chen, Zhinong Wei, Yonghui Sun, Haixiang Zang, and Sheng Chen. 2016. "A Carbon Price Forecasting Model Based on Variational Mode Decomposition and Spiking Neural Networks" Energies 9, no. 1: 54. https://doi.org/10.3390/en9010054