Financing the Renovation of the Cypriot Building Stock: An Assessment of the Energy Saving Potential of Different Policy Scenarios Based on the Invert/EE-Lab Model

Abstract

:1. Introduction

2. Current Context in Cyprus

2.1. Policy Framework on Energy Efficiency

2.2. Building Stock

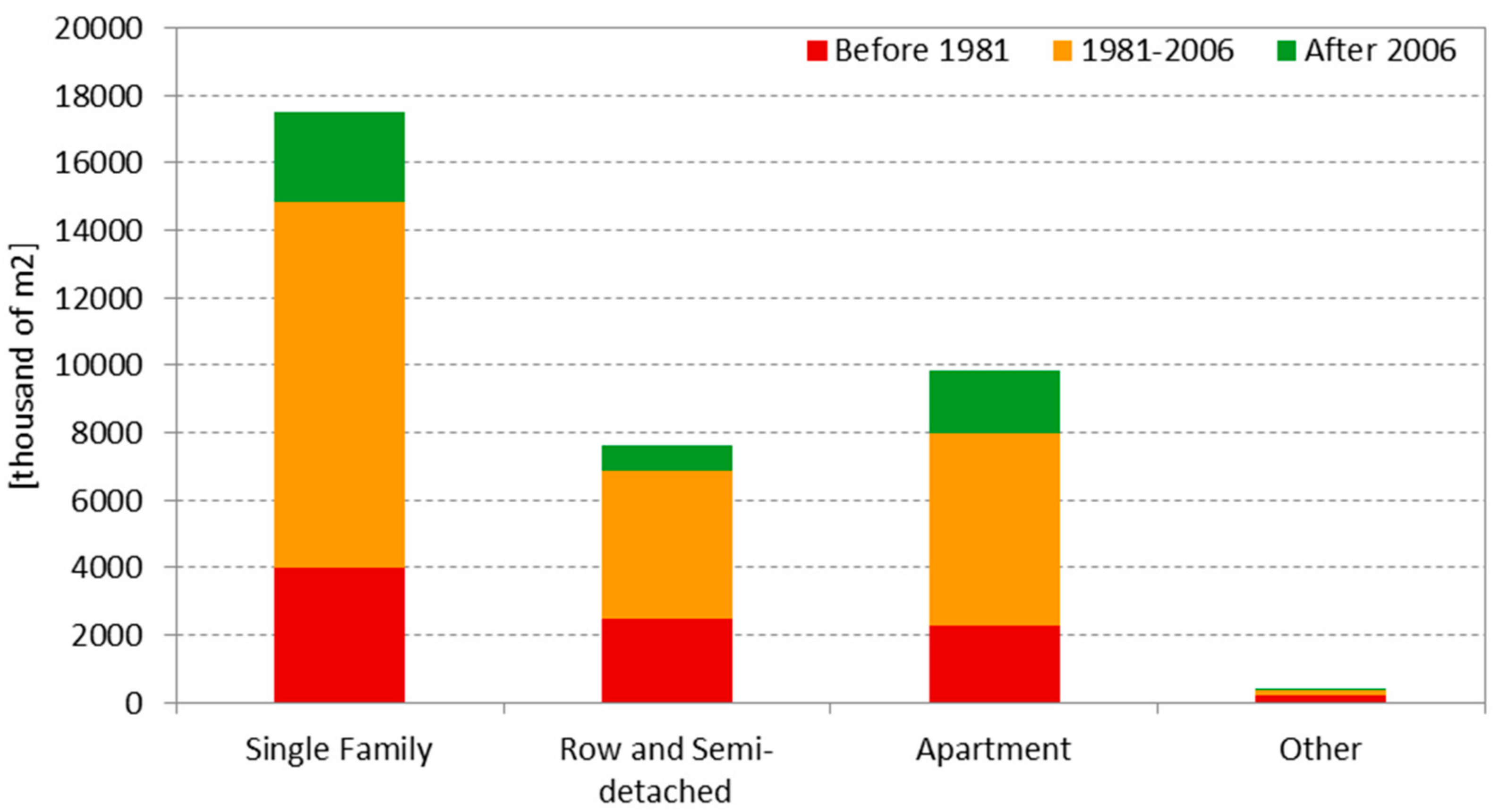

2.2.1. Residential Building Stock

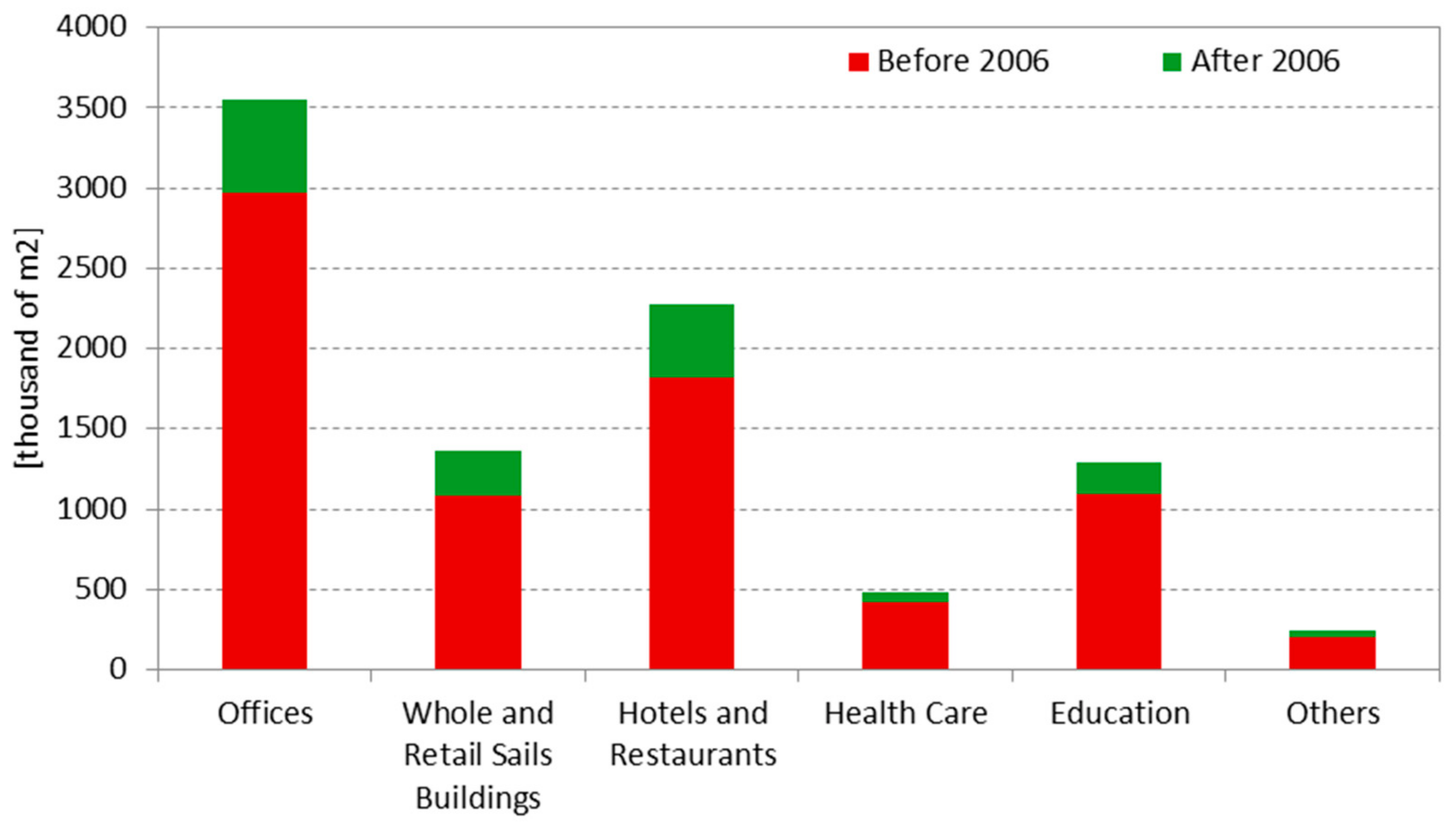

2.2.2. Non-Residential Building Stock

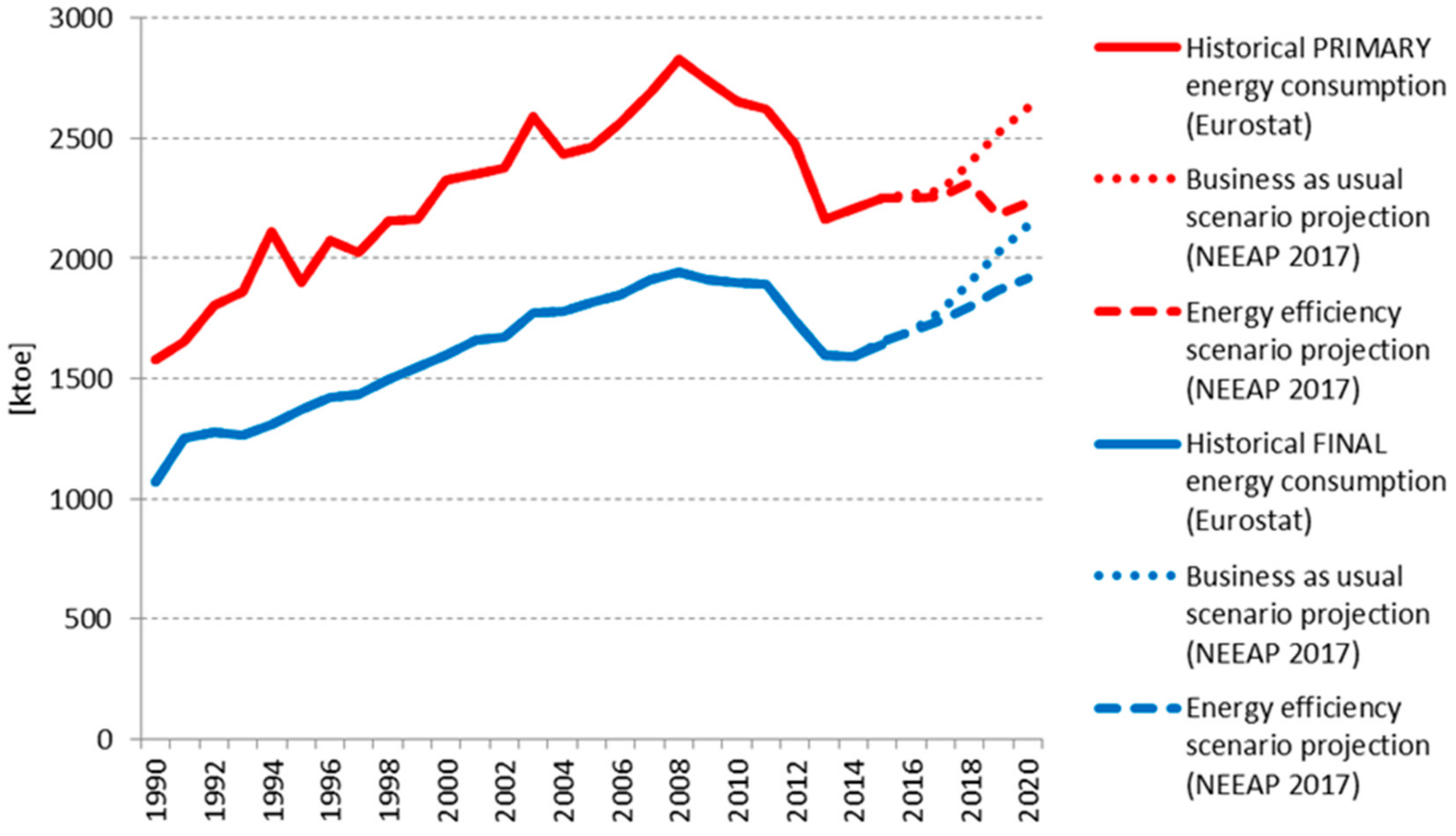

2.3. Discussion

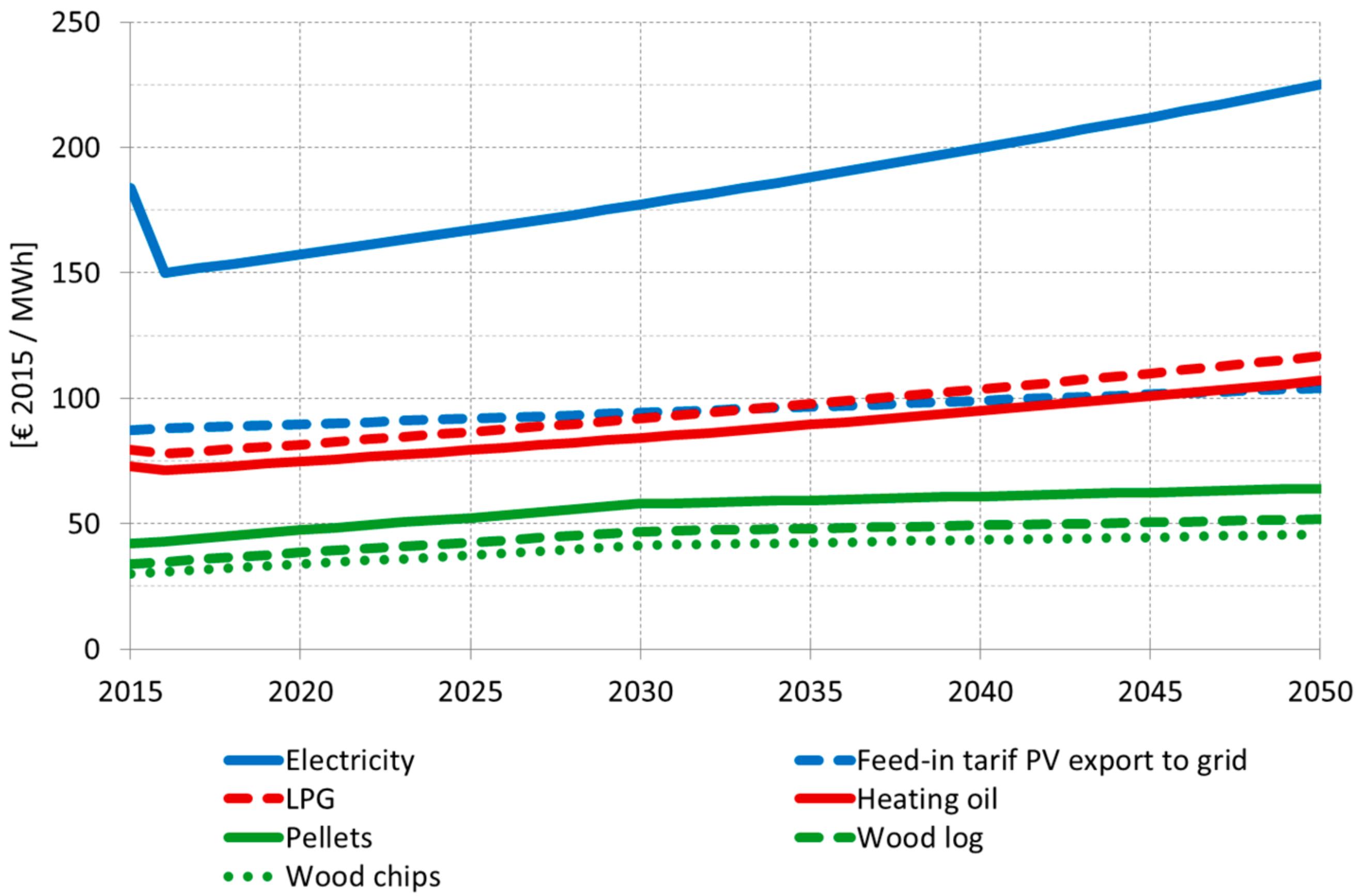

3. Methods

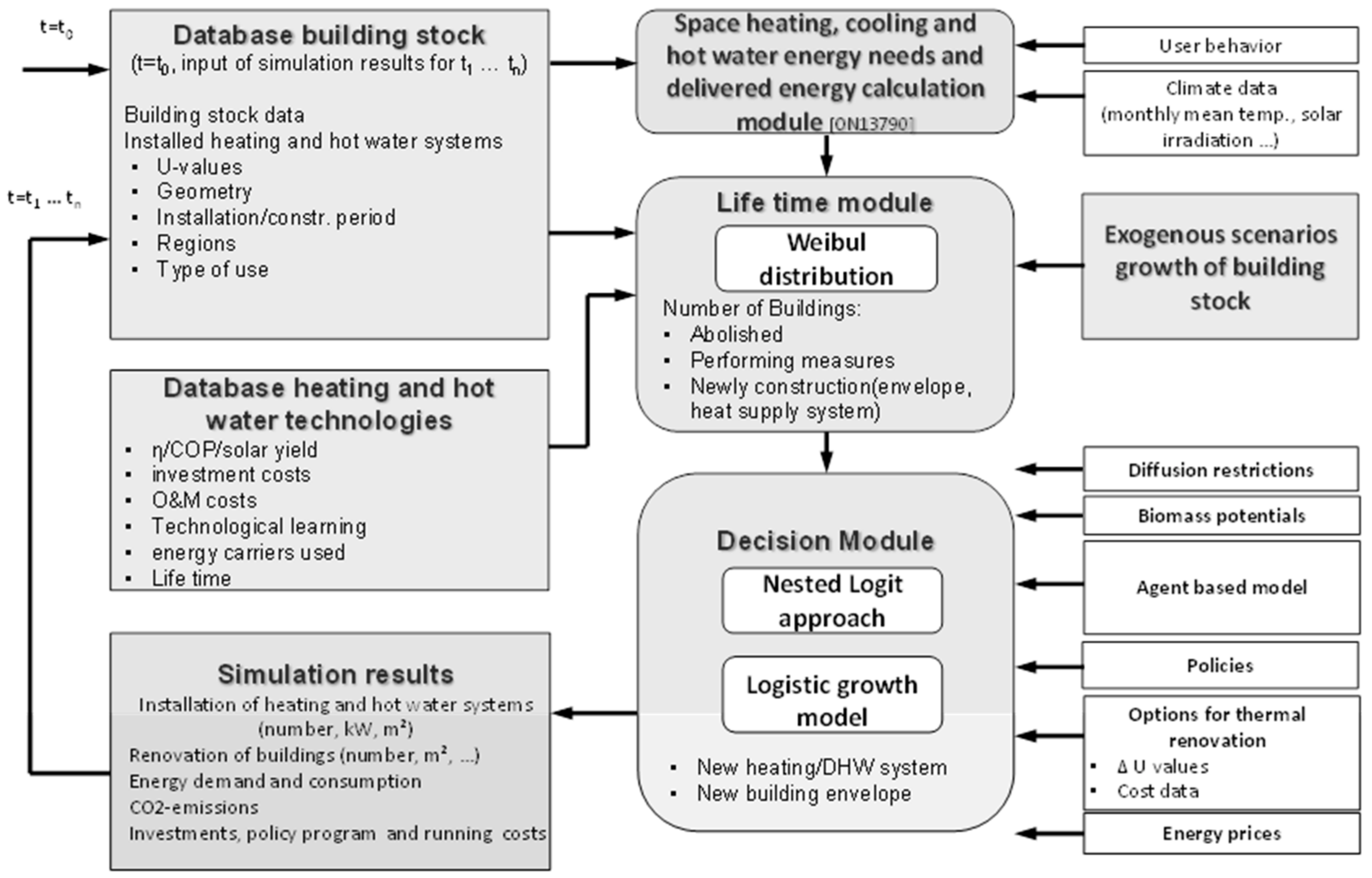

3.1. About Building Stock Modelling

3.2. Application of Invert/EE-Lab Model

- describe the building stock, heating, cooling, and domestic hot water systems on highly disaggregated level;

- calculate the related energy needs and delivered energy based on technical calculation procedures (Austrian implementation of the EN 13790 and 15603);

- determine reinvestment cycles for different building components and technologies using Weibull distribution-based survival curves;

- simulate the decisions of various agents (i.e., owner types) in case that an investment decision is due for a specific building segment.

3.3. Policy Scenarios

- Tax income credit with which landlords can deduct a share of the cost of acquiring/installing certain EE measures against their income tax (Policy 10).

- Gradually increasing minimum energy performance requirement (no worse than Class E by 2025 and no worse than Class D by 2030) when a property is rented out (Policy 11).

- Reduction of VAT rate from 19% to 5% for energy efficiency investments including technologies and labour costs (Policy 12).

- To demonstrate the feasibility of building designs which are of more ambitious levels than the current NZEB levels, a grant for new ZEB/PEB is introduced (Policy 13).

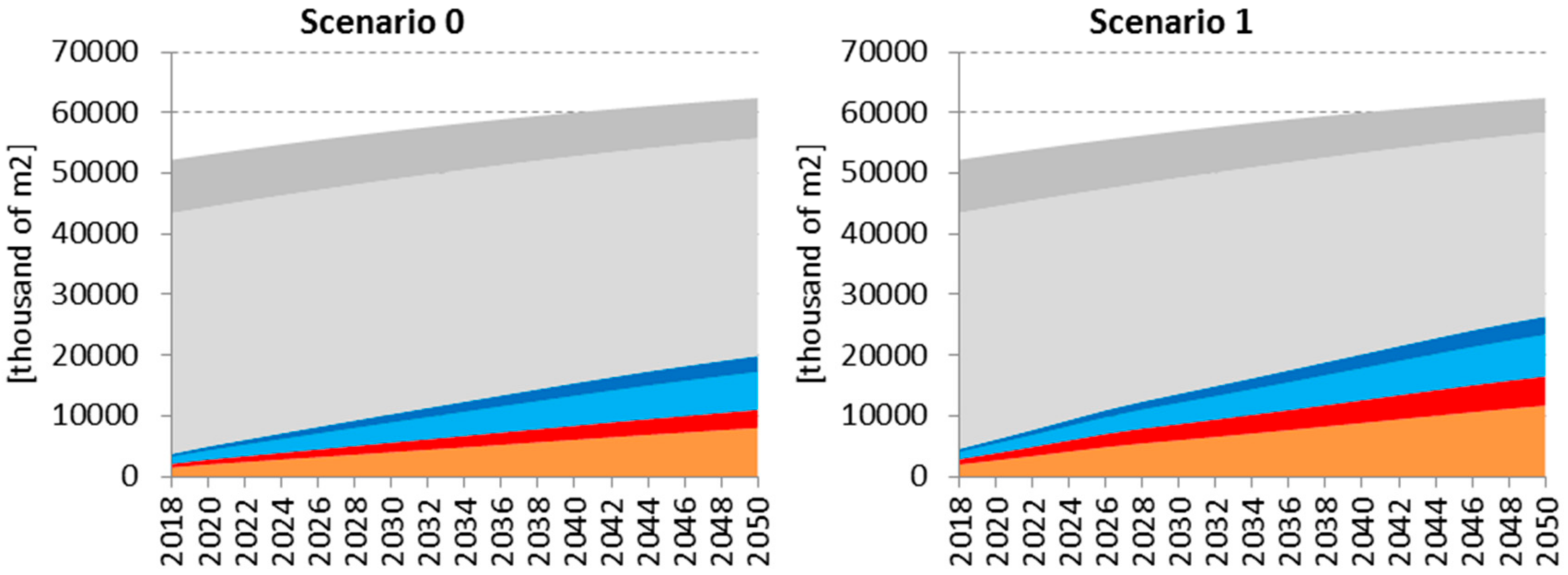

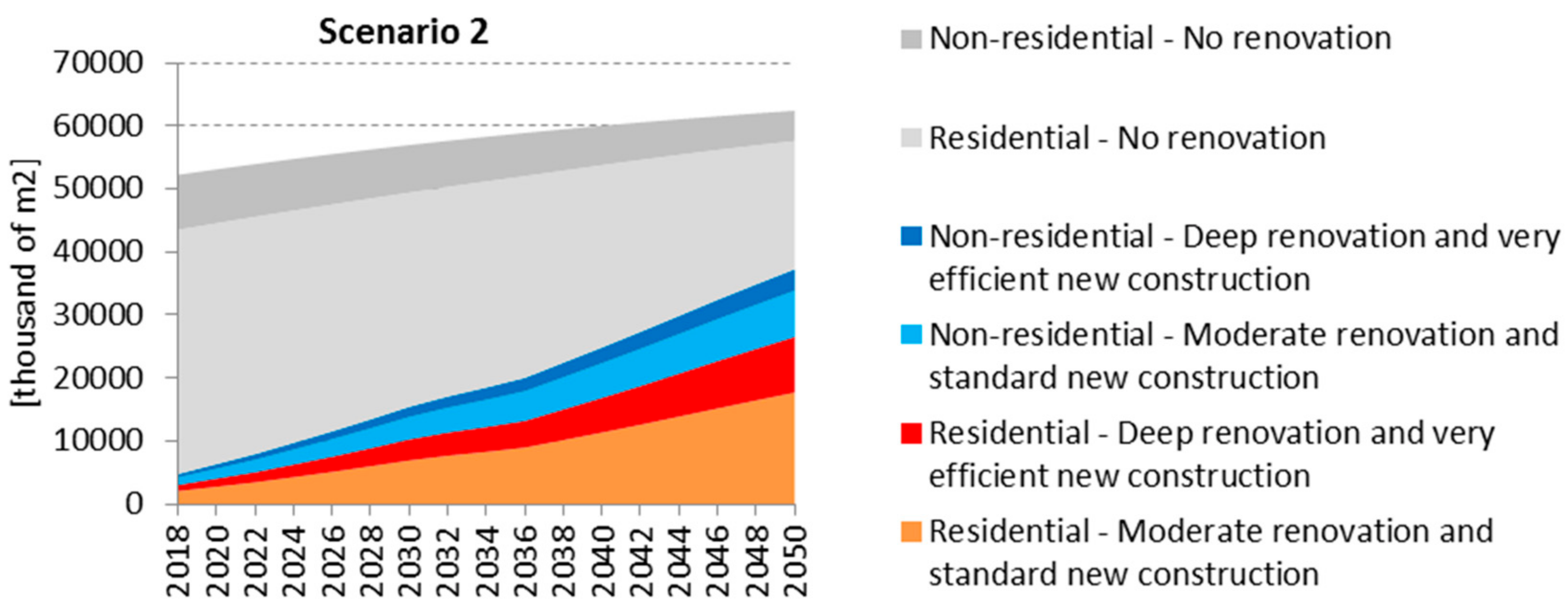

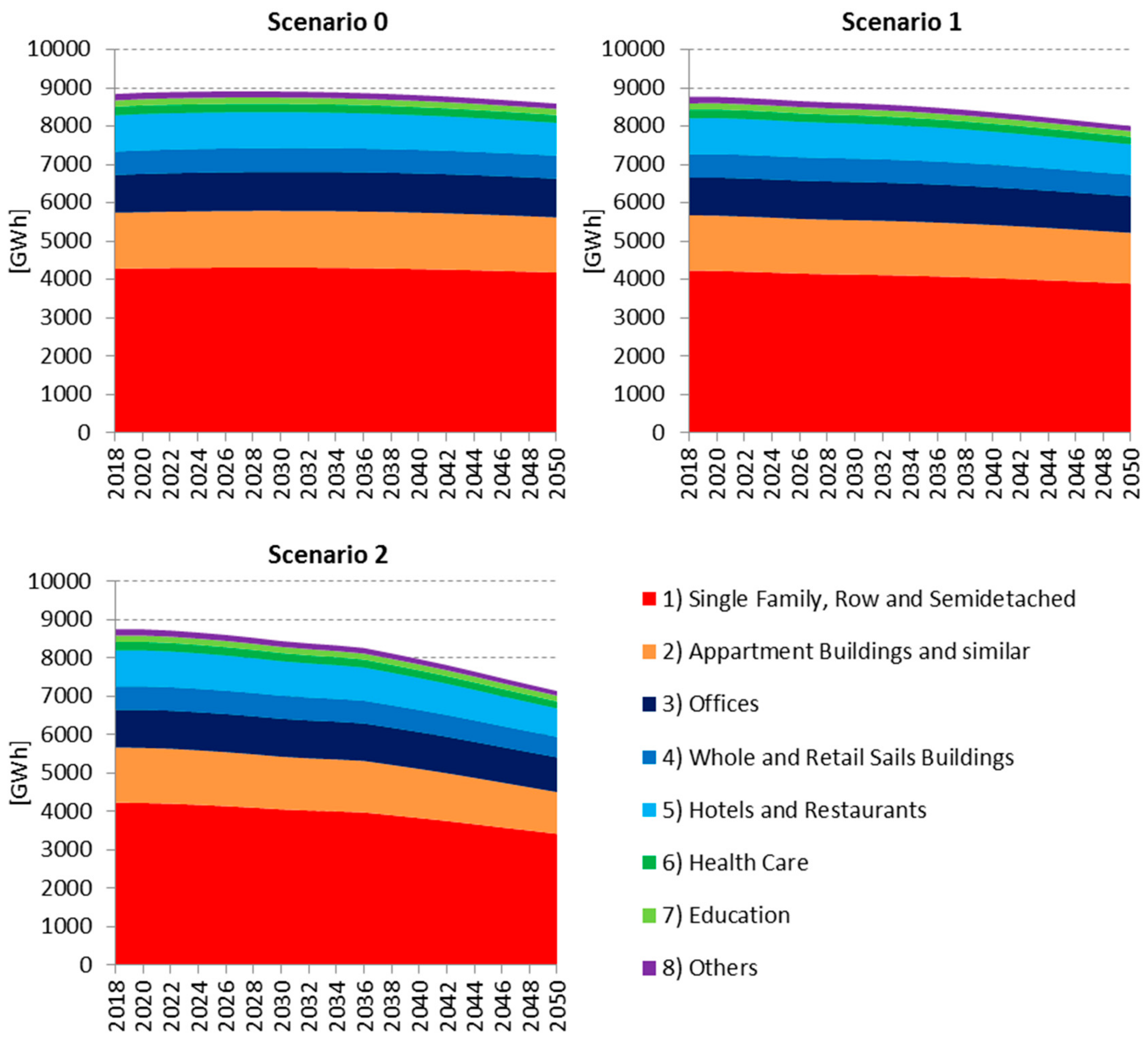

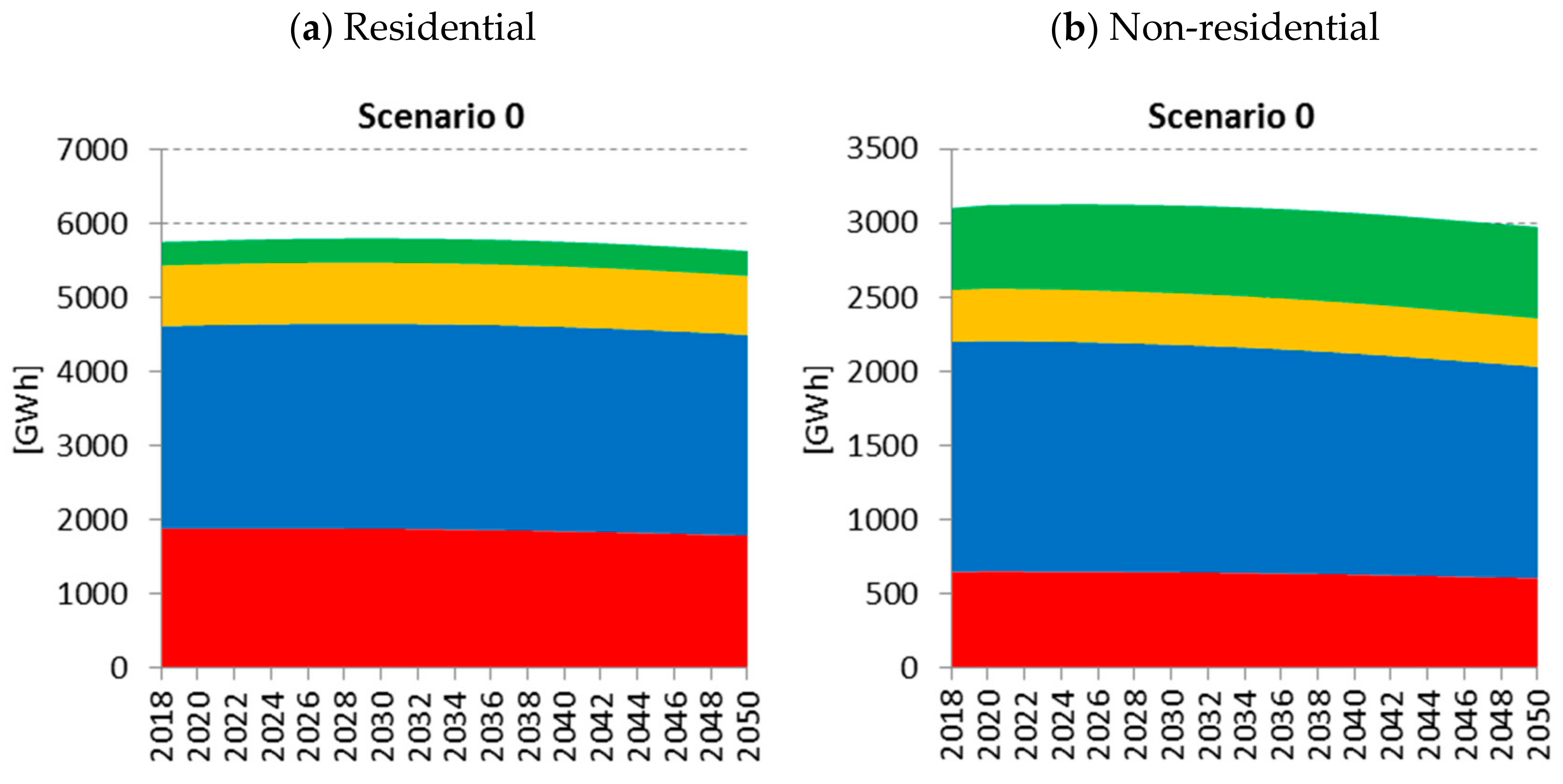

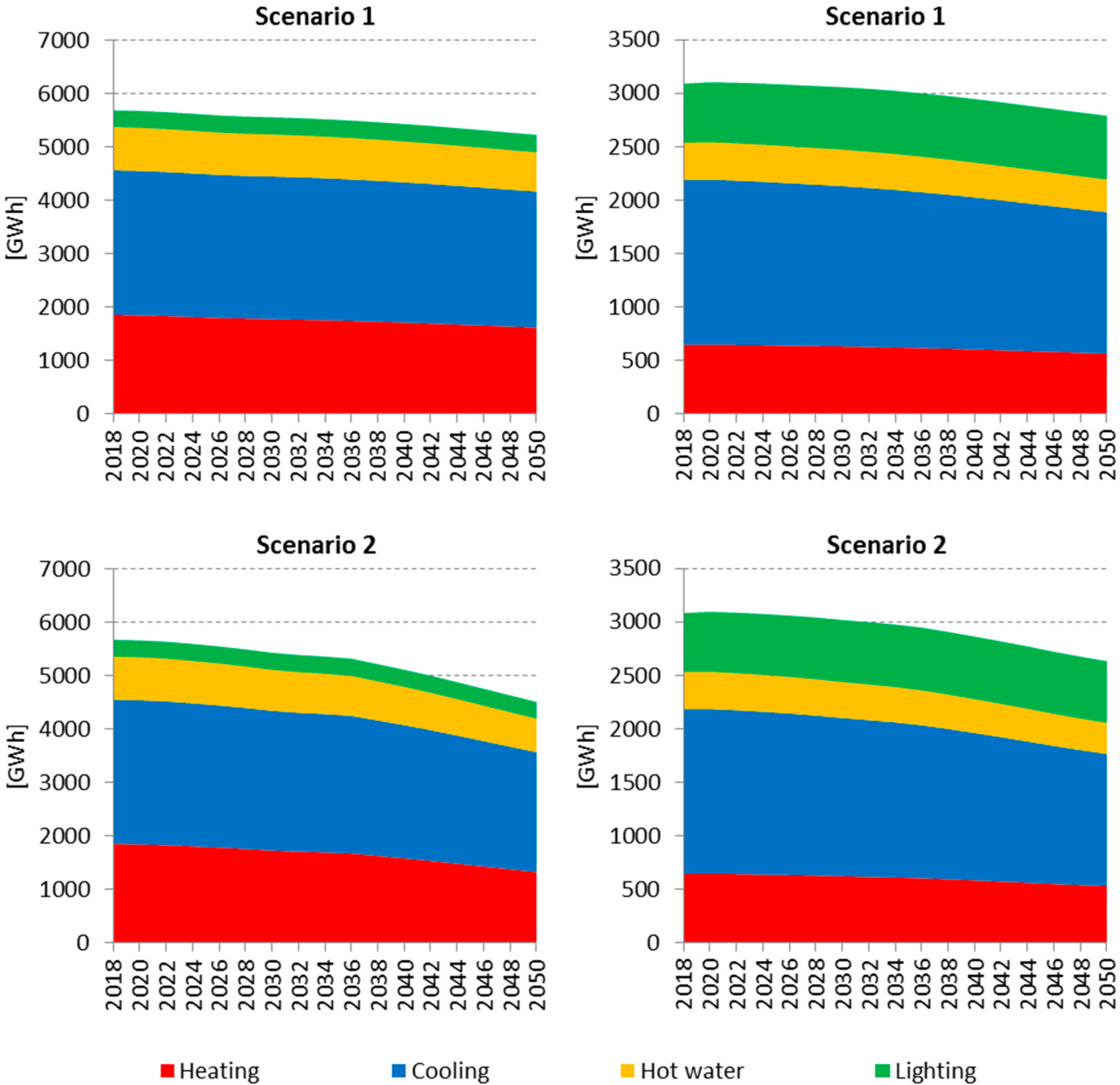

4. Modelling Results

- Scenario 1 would increase the share of moderately renovated buildings and standard new constructions from 12.7% to 16.5% in 2030 and from 22.6% to 29.4% in 2050;

- Scenario 1 would increase the share of deeply renovated buildings and very efficient new construction from 5.8% to 7.9% in 2030 and from 10% to 13.5% in 2050;

- Scenario 2 would increase the share of moderately renovated buildings and standard new constructions to 18.3% in 2030 and to 39.6% in 2050;

- Scenario 2 would increase the share of deeply renovated buildings and very efficient new constructions to 9.2% in 2030 and to 20.5% in 2050.

5. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Piripitsi, A.; Stougiannis, E.; Chatzinikolaou, N.; Thoma, G.; Ellinopoulos, C.; Kakouris, M.; Ioannou, S.; Kyrizis, K. Fourth National Energy Efficiency Action Plan of Cyprus; Cyprus Ministry of Energy, Commerce, Industry and Tourism: Nicosia, Cyprus, 2017.

- Zachariadis, T.; Michopoulos, A.; Vougiouklakis, Y.; Struss, B.; Piripitsi, K.; Ellinopoulos, C. In-Depth Assessment of the Energy Efficiency Potential in Cyprus. Cyprus Econ. Policy Rev. 2017, 11, 86–112. [Google Scholar]

- Serghides, D.K.; Dimitriou, S.; Katafygiotou, M.C.; Michaelidou, M. Energy efficient refurbishment towards nearly zero energy houses, for the Mediterranean region. In Proceedings of the 7th International Conference on Sustainability in Energy and Buildings, Lisbon, Portugal, 1–3 July 2015. [Google Scholar]

- Panayiotou, G.; Kalogirou, S.; Florides, G.; Maxoulis, C.N.; Papadopoulos, A.M.; Neophytou, M.F.; Georgakis, G. The characteristics and the energy behaviour of the residential building stock of Cyprus in view of Directive 2002/91/EC. Energy Build. 2010, 42, 2083–2089. [Google Scholar] [CrossRef]

- Mantzos, L.; Wiesenthal, T.; Matei, N.A.; Tchung-Ming, S.; Rozsai, M. JRC-IDEES: Integrated Database of the European Energy Sector. Methodological Note; EUR 28773 EN, JRC108244; Publications Office of the European Union: Luxembourg, 2017; ISBN 978-92-79-73465-6. [Google Scholar]

- Cyprus Ministry of Energy, Commerce, Industry and Tourism. Calculation for Setting the Minimum Energy Performance Requirements at Cost Optimal Levels According to Article 5 of the Directive 2010/31/EE for the Energy Performance of Buildings; Cyprus Ministry of Energy, Commerce, Industry and Tourism: Nicosia, Cyprus, 2013.

- Michael, A.; Phocas, M.C. Energy Performance Evaluation and Heat Insulation Measures for Typical Educational Buildings in Cyprus. In Proceedings of the 3rd International Conference on Renewable Energy Sources & Energy Efficiency, Nicosia, Cyprus, 19–20 May 2011; ISBN 978-9963-567-02-7. [Google Scholar]

- Cyprus Statistical Service. Health and Hospital Statistics 2012; Cyprus Statistical Service: Nicosia, Cyprus, 2014. [Google Scholar]

- Katafygioutou, M.C.; Serghides, D.K. Analysis of structural elements and energy consumption of school building stock in Cyprus: Energy simulations and upgrade scenarios of a typical school. Energy Build. 2014, 72, 8–16. [Google Scholar] [CrossRef]

- Cyprus Ministry of Education and Culture. Registry of Private Pre-school, Primary and Secondary Education Facilities; Cyprus Ministry of Energy, Commerce, Industry and Tourism: Nicosia, Cyprus, 2015.

- Cyprus Energy Agency. WE-Qualify. Training, Specialization, Certification. Acquiring Knowledge and Skills for the Energy Performance Improvement of Buildings in Cyprus; Final Report; Cyprus Energy Agency: Nicosia, Cyprus, 2016. [Google Scholar]

- Cost, M. Langfristige Energieverbrauchs- und CO2-Reduktionspotenziale im Wohngebäudesektor der Schweiz. Ph.D. Thesis, ETH Zürich, Zürich, Switzerland, 2006. [Google Scholar]

- Sartori, I.; Wachenfeldt, B.J.; Hestnes, A.G. Energy demand in the Norwegian building stock: Scenarios on potential reduction. Energy Policy 2009, 37, 1614–1627. [Google Scholar] [CrossRef]

- Hansen, P. Entwicklung Eines Energetischen Sanierungsmodells für den Europäischen Wohngebäudesektor unter dem Aspekt der Erstellung von Szenarien für Energie- und CO2-Einsparpotenziale bis 2030; Schriften des Forschungszentrums Jülich, Energie Umwelt; Forschungszentrum Jülich GmbH: Jülich, Germany, 2009; Volume 48, ISBN 978-3-89336-590-6. [Google Scholar]

- Olonscheck, M.; Holsten, A.; Kropp, J.P. Heating and cooling energy demand and related emissions of the German residential building stock under climate change. Energy Policy 2011, 39, 4795–4806. [Google Scholar] [CrossRef]

- Broin, E.Ó.; Mata, É.; Göransson, A.; Johnsson, F. The effect of improved efficiency on energy savings in EU-27 buildings. Energy 2013, 57, 134–148. [Google Scholar] [CrossRef]

- Heeren, N.; Jakob, M.; Martius, G.; Gross, N.; Wallbaum, H. A component based bottom-up building stock model for comprehensive environmental impact assessment and target control. Renew. Sustain. Energy Rev. 2013, 20, 45–56. [Google Scholar] [CrossRef]

- Mata, E.; Kalagasidis, A.S.; Johnsson, F. A modeling strategy for energy, carbon, and cost assessments of building stocks. Energy Build. 2013, 56, 100–108. [Google Scholar] [CrossRef]

- McKenna, R.; Merkel, E.; Fehrenbach, D.; Mehne, S.; Fichtner, W. Energy efficiency in the German residential sector: A bottom-up building-stock-model-based analysis in the context of energy-political targets. Build. Environ. 2013, 62, 77–88. [Google Scholar] [CrossRef]

- Mattinen, M.K.; Heljo, J.; Vihola, J.; Kurvinen, A.; Lehtoranta, S.; Nissinen, A. Modeling and visualization of residential sector energy consumption and greenhouse gas emissions. J. Clean. Prod. 2014, 81, 70–80. [Google Scholar] [CrossRef]

- Tuominen, P.; Holopainen, R.; Eskola, L.; Jokisalo, J.; Airaksinen, M. Calculation method and tool for assessing energy consumption in the building stock. Build. Environ. 2014, 75, 153–160. [Google Scholar] [CrossRef]

- Dascalaki, E.G.; Balaras, C.A.; Kontoyiannidis, S.; Droutsa, K.G. Modeling energy refurbishment scenarios for the Hellenic residential building stock towards the 2020 & 2030 targets. Energy Build. 2016, 132, 74–90. [Google Scholar]

- Sandberg, N.H.; Sartori, I.; Vestrum, M.I.; Brattebø, H. Using a segmented dynamic dwelling stock model for scenario analysis of future energy demand: The dwelling stock of Norway 2016–2050. Energy Build. 2017, 146, 220–232. [Google Scholar] [CrossRef]

- Wilkerson, J.T.; Cullenward, D.; Davidian, D.; Weyant, J.P. End use technology choice in the National Energy Modeling System (NEMS): An analysis of the residential and commercial building sectors. Energy Econ. 2013, 40, 773–784. [Google Scholar] [CrossRef]

- Fujimori, S.; Masui, T.; Yuzuru, M. AIM/CGE [basic] Manual; NIES Discussion Paper Series; Center for Social and Environmental Systems Research, NIES: Tsukuba, Japan, 2012. [Google Scholar]

- Li, F.G.N.; Strachan, N. Modelling energy transitions for climate targets under landscape and actor inertia. Environ. Innov. Soc. Trans. 2017, 24, 106–129. [Google Scholar] [CrossRef] [Green Version]

- Bataille, C.; Jaccard, M.; Nyboer, J.; Rivers, N. Towards General Equilibrium in a Technology-Rich Model with Empirically Estimated Behavioral Parameters. Energy J. 2006, 27, 93–112. [Google Scholar] [CrossRef]

- Elsland, R. Long-Term Energy Demand in the German Residential Sector; Development of an Integrated Modelling Concept to Capture Technological Myopia; Nomos Verlagsgesellschaft: Baden-Baden, Germany, 2016; ISBN 978-3-8487-2631-8. [Google Scholar]

- Henkel, J. Modeling the Diffusion of Innovative Heating Systems in Germany—Decision Criteria, Influence of Policy Instruments and Vintage Path Dependencies. Ph.D. Thesis, Technical University of Berlin, Berlin, Germany, 2012. [Google Scholar]

- Bauermann, K. German Energiewende and the Heating Market—Impact and Limits of Policy. University of Duisburg-Essen, EWL Working Paper No. [20/2013]. 2013. Available online: http://econpapers.repec.org/paper/duiwpaper/1320.htm (accessed on 20 April 2017).

- De Vita, A.; Tasios, N.; Evangelopoulou, S.; Forsell, N.; Fragiadakis, K.; Fragkos, P.; Evangelopoulou, S.; Zampara, M.; Papadopoulos, D.; Nakos, C.; et al. EU Reference Scenario 2016. Energy, Transport and GHG Emissions: Trends to 2050; Publications Office of the European Union: Luxembourg, 2016. [Google Scholar]

- Müller, A. Energy Demand Assessment for Space Conditioning and Domestic Hot Water: A Case Study for the Austrian Building Stock. Ph.D. Thesis, Technische Universität Wien, Vienna, Austria, 2015. [Google Scholar]

- Steinbach, J. Modellbasierte Untersuchung von Politikinstrumenten zur Förderung erneuerbarer Energien und Energieeffizienz im Gebäudebereich; Fraunhofer Verlag: München, Germany, 2016; ISBN 978-3-8396-0987-3. [Google Scholar]

- Nabera, E.; Volka, R.; Schultmann, F. From the building level energy performance assessment to the national level: How are uncertainties handled in building stock models. Procedia Eng. 2017, 180, 1443–1452. [Google Scholar] [CrossRef]

- Chappin, E.; Hesselink, L.; Blok, K.; Müller, A.; Fries, B.; Braungardt, S. Changing Energy Efficiency Technology Adoption in Households. Deliverable D3.2 of the CHEETAH Project. Horizon 2020 Project Number. 723716, TU Delft. 2017. Available online: https://www.briskee-cheetah.eu/static/media/uploads/site-3/library/d3.2.cheetah_working_paper_on_modelling_and_survey.pdf (accessed on 19 October 2017).

- Kranzl, L.; Hummel, M.; Müller, A.; Steinbach, J. Renewable heating. Perspectives and the impact of policy instruments. Energy Policy 2013, 59, 44–58. [Google Scholar] [CrossRef]

- Crawley, D.B.; Lawrie, L.K.; Winkelmann, F.C.; Buhl, W.; Huang, Y.J.; Pedersen, C.O.; Strand, R.K.; Liesen, R.J.; Fisher, D.E.; Witte, M.J.; et al. EnergyPlus: Creating a new-generation building energy simulation program. Energy Build. 2001, 33, 319–331. [Google Scholar] [CrossRef]

- Zangheri, P.; Armani, R.; Pietrbon, M.; Pagliano, L.; Boneta, M.F.; Müller, A. Heating and Cooling Energy Demand and Loads for Building Types in Different Countries of the EU. D2.3. of WP2 of the Entranze Project. Available online: http://www.entranze.eu/files/downloads/D2_3/Heating_and_cooling_energy_demand_and_loads_for_building_types_in_different_countries_of_the_EU.pdf (accessed on 23 March 2017).

- Williams, H.C.W.L. On the formulation of travel demand models and economic evaluation measures of user benefit. Environ. Plan. A 1977, 9, 285–344. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Details | Building Codes | Information Tools | Financial Measures | Education & Training |

|---|---|---|---|---|

| Main policy measures | a. Minimum energy performance requirements in new and existing buildings b. Nearly Zero Energy Buildings | a. Energy performance certification scheme b. Energy audits | a. Grants for EE & renewables b. Grants for PV instalment and NET metering c. Grants “I save—I upgrade” | a. Qualified energy experts b. Energy auditors c. Energy managers d. Energy service providers |

| Decree references | a. 568/2007, 446/2009, 432/2013, 119/2016 b. 366/2014 | a. 433/2013, 71/2016 b. 437/2015 | - | a. 164/2016, 419/2015, 309/2017 b. 184/2012 c. 344/2016 d. 210/2014 |

| Target group | a. New constructions and major renovations b. New constructions | a. Building owners, tenants, occupants b. Industry, SME actors | a. Households, companies, public entitiesb. Householdsc. Households, companies, public entities | a. Licenced engineers/architects with min 3-year work experience b. Licenced engineers with min 3-year work experience c. Professionals with relevant experience d. Energy service companies and other energy-related professionals |

| Impl. period | a. 2008– b. 2020– | a. 2013– b. 2015– | a. 2004–2013 b. 2013–2020 c. 2014–2020 | a. 2013– b. 2012– c. 2016– d. 2014– |

| Requirements | 2007 | 2009 | 2013 | 2017 | 2020 (NZEB) |

|---|---|---|---|---|---|

| Max U-value of walls [W/m2K] | 0.85 | 0.85 | 0.72 | 0.40 | 0.40 |

| Max U-value of roofs [W/m2K] | 0.75 | 0.75 | 0.63 | 0.40 | 0.40 |

| Max U-value of floors [W/m2K] | 2.00 | 2.00 | 2.00 | 0.40 | 0.40 |

| Max U-value of windows [W/m2K] | 3.8 | 3.8 | 3.23 | 2.9 | 2.25 |

| Maximum U-mean [W/m2K] | - | 1.3–1.8 | 1.3–1.8 * | - | - |

| Max window shading coefficient [−] | - | - | 0.63 | 0.63 | - |

| Installation provisions | - | RES | RES | - | - |

| Min share of PEC to be covered by RES | - | - | 3% (n-res) | 3–25% (res) * 7% (n-res) * | 25% * |

| Max mean installed lighting power (offices) [W/m2] | - | - | - | 10 * | 10 * |

| Minimum Energy Class | - | Class B | Class B | Class B * | Class A * |

| Max energy demand for heating (res) [kWh/m2] | - | - | - | - | 15 * |

| Max primary energy consumption [kWh/m2] | - | - | - | - | 100 (res) * 125 (n-res) * |

| Main Elements | Grant Scheme 2004–2013 | Grant Scheme 2014–2020 |

|---|---|---|

| Funding structure | Fund financed by a fee of EUR 0.50 c/kWh on electricity consumption for all final consumers | Cofinanced with EU Structural Funds |

| Total available funding | EUR 100 million (corresponding to around 10 million/year) | EUR 31.8 million (corresponding to around 4–5 million per year) |

| Targeted buildings | Owner-occupied residential buildings; Public sector buildings that exercise economic activity; Commercial buildings; Buildings of non-for-profit organisations | Residential buildings or building units part of an apartment building; Buildings owned or rented by SMEs |

| Energy upgrade target | - | Class B, 40% energy savings, nZEB renovation |

| Factors determining financial support | Technology type | Household income; Ambition of energy upgrade |

| Main Intervention measures | Residential: Building envelope insulation; Solar thermal systems; PV systems Non-residential: Recovery of waste energy; Reduction of non-productive energy consumption and energy losses; Energy management systems; Automation; cogeneration system, Solar thermal systems; PV systems | Residential/Non-residential: Building envelope insulation; Window replacement; Energy efficiency boilers for space heating/domestic hot water; Geothermal heat pumps; Solar thermal systems; Biomass boilers; Efficient light bulbs; waste energy recovery systems; cogeneration systems; Smart meters; External removable or fixed shading; Energy efficient air conditioning systems (split units) |

| Implementation body | Cyprus Institute of Energy | Ministry of Energy, Commerce, Industry and Transport |

| Building Type | Age | Space Heating | Space Cooling | Water Heating | Lighting | Appliances | Cooking |

|---|---|---|---|---|---|---|---|

| [kWh/m2] | [kWh/m2] | [kWh/m2] | [kWh/m2] | [kWh/m2] | [kWh/m2] | ||

| Single family | Before 1981 | 54 | 72 | 23 | 8 | 20 | 6 |

| 1981–2006 | 40 | 54 | 18 | 7 | 15 | 4 | |

| After 2006 | 36 | 50 | 15 | 6 | 14 | 4 | |

| Row and Semidetached | Before 1981 | 59 | 58 | 23 | 9 | 21 | 6 |

| 1981–2006 | 43 | 44 | 18 | 7 | 16 | 4 | |

| After 2006 | 39 | 40 | 15 | 6 | 15 | 4 | |

| Apartment | Before 1981 | 45 | 105 | 23 | 8 | 19 | 6 |

| 1981–2006 | 33 | 84 | 18 | 6 | 15 | 4 | |

| After 2006 | 30 | 76 | 15 | 6 | 13 | 4 | |

| Other | Before 1981 | 56 | 53 | 23 | 4 | 8 | 0 |

| 1981–2006 | 41 | 41 | 18 | 3 | 8 | 0 | |

| After 2006 | 37 | 38 | 15 | 3 | 7 | 0 |

| Thermal System | Fuel | Single Family | Row & Semidetached | Apartment | Other | |

|---|---|---|---|---|---|---|

| Heating | Central heating (kerosene): standard | oil | 33% | 32% | 15% | 2% |

| Central heating (kerosene): condensing | oil | - | - | - | - | |

| Room stoves (kerosene) | oil | 2% | 2% | 2% | 1% | |

| Central heating (gas): standard | gas | 3% | 1% | 1% | - | |

| Central heating (gas): condensing | gas | - | - | - | - | |

| Room stoves (gas) | gas | 14% | 13% | 1- | 27% | |

| Central heating (electric): standard HP | electricity | 3% | 4% | 5% | 1% | |

| Central heating (electric): geothermal HP | electricity | - | - | - | - | |

| Room fixed units (hot air): standard | electricity | 17% | 22% | 35% | 15% | |

| Room fixed units (hot air): efficient | electricity | 4% | 5% | 9% | 4% | |

| Room stoves (electric) | electricity | 9% | 1- | 12% | 22% | |

| Room storage heaters (EAC) | electricity | 2% | 3% | 5% | - | |

| Room Fireplace | biomass | 9% | 5% | 1% | 2% | |

| Room solar heating system | - | - | - | - | 1% | |

| No or other heating facilities | - | 2% | 2% | 5% | 7% | |

| All | 100% | 100% | 100% | 100% | ||

| Cooling | Central cooling (electric): standard HP | electricity | 3% | 4% | 5% | 1% |

| Central cooling (electric): geothermal HP | electricity | - | - | - | - | |

| Room fixed units (cold air): standard | electricity | 63% | 63% | 62% | 65% | |

| Room fixed units (cold air): efficient | electricity | 16% | 16% | 15% | 16% | |

| No or other cooling facilities | - | 18% | 18% | 18% | 18% | |

| All | 100% | 100% | 100% | 100% | ||

| Building Type | Age | Space Heating | Space Cooling | Water Heating | Lighting |

|---|---|---|---|---|---|

| Offices | Before 2006 | 80 | 171 | 5 | 44 |

| After 2006 | 54 | 117 | 4 | 40 | |

| Whole and Retail Sails Buildings | Before 2006 | 37 | 332 | 3 | 105 |

| After 2006 | 25 | 226 | 2.5 | 95 | |

| Hotels and Restaurants | Before 2006 | 104 | 170 | 110 | 55 |

| After 2006 | 71 | 116 | 75 | 50 | |

| Health Care | Before 2006 | 96 | 181 | 121 | 70 |

| After 2006 | 66 | 123 | 83 | 65 | |

| Education | Before 2006 | 35 | 55 | 7 | 35 |

| After 2006 | 24 | 37 | 5 | 30 | |

| Others | Before 2006 | 197 | 358 | 137 | 70 |

| After 2006 | 134 | 244 | 93 | 65 |

| Thermal System | Fuel | Off | SubRet | HotRest | Health | Edu | Other | |

|---|---|---|---|---|---|---|---|---|

| Heating | Central heating (kerosene): stand. | oil | 41% | 11% | 43% | 31% | 86% | 41% |

| Central heating (kerosene): conden. | oil | 1% | 1% | 1% | 1% | 2% | 1% | |

| Room stoves (kerosene) | oil | - | - | - | - | - | - | |

| Central heating (gas): standard | gas | 4% | 1% | 10% | 4% | 3% | 6% | |

| Central heating (gas): condensing | gas | - | - | 1% | - | - | - | |

| Room stoves (gas) | gas | - | - | - | - | - | - | |

| Central heating (electric): stand. HP | elect. | 44% | 78% | 40% | 61% | 5% | 44% | |

| Central heating (electric): geoth. HP | elect. | 1% | 1% | - | 1% | - | 1% | |

| Room fixed units (hot air): standard | elect. | 6% | 4% | 3% | - | 2% | 4% | |

| Room fixed units (hot air): efficient | elect. | 1% | - | 1% | - | - | 1% | |

| Room stoves (electric) | elect. | - | - | - | - | - | - | |

| Room storage heaters (EAC) | elect. | - | - | - | - | - | - | |

| Room Fireplace | biom. | - | - | - | - | - | - | |

| Room solar heating system | - | - | - | - | - | - | - | |

| No or other heating facilities | 2% | 3% | 1% | 2% | 2% | 2% | ||

| All | 100% | 100% | 100% | 100% | 100% | 100% | ||

| Cooling | Central cooling (electric): stand. HP | elect. | 56% | 82% | 61% | 68% | 34% | 59% |

| Central cooling (electric): geoth. HP | elect. | 1% | 1% | - | 1% | - | 1% | |

| Room fixed units (cold air): standard | elect. | 20% | 4% | 24% | 9% | 5% | 19% | |

| Room fixed units (cold air): efficient | elect. | 3% | - | 4% | 2% | 1% | 3% | |

| No or other cooling facilities | 20% | 13% | 10% | 20% | 60% | 19% | ||

| All | 100% | 100% | 100% | 100% | 100% | 100% | ||

| Policy | Main Achievements and Concerns | |

|---|---|---|

| Building codes | Main achievements | Mandatory energy performance requirements in building codes have been a significant achievement; gradual tightening of requirements and switch from prescriptive- to performance-based requirements are regarded as positive steps. |

| Concerns | NZEB levels for 2020 are not ambitious; compliance with requirements in major renovations is an issue | |

| Information tools | Main achievements | All legislation regarding energy performance certification and energy audits have been put in place. |

| Concerns | Current or potential users are often not informed about energy performance class of their buildings and are unaware of benefits of potential energy efficiency improvements. | |

| Education & training | Main achievements | A comprehensive framework for education, qualification, and training for energy auditors, specialised experts for energy performance certificates, energy service providers, and energy managers is available |

| Concerns | Need to improve the vocational education and training system for technical occupations; training needs in construction sector are expected to grow. | |

| Financial measures | Main achievements | Government-supported grants to households, businesses, and public sector have been a major generator of energy savings in the country. |

| Concerns | Transition from grant-based to a more diverse portfolio of economic policy measures has not yet been made. | |

| Timeframe | Residential | Non-Residential | |||||

|---|---|---|---|---|---|---|---|

| Owner Occupied | Apartment Blocks | Rented Buildings | Vulnerable Group | Rented | Owned | ||

| Existing buildings | <2013 | Grant | - | - | Grant | - | Grant |

| Now | Grant | - | Grant | Grant | |||

| Proposed | Credit line/Preferential loans | Tax income for landlords | Special grants | Credit line/Preferential loans | |||

| ZEB Grants | ZEB Grants | ESCO portfolio guarantees | |||||

| New buildings | Now | - | - | - | - | - | - |

| Proposed | Credit line/Preferential loans | - | Special grants | - | ZEB Grants | ||

| ZEB Grants | ZEB Grants | ||||||

| Endogenously Calculated | Exogenously Defined |

|---|---|

|

|

| End-Use | Residential | Non-Residential | ||||

|---|---|---|---|---|---|---|

| Building Stock | Renovation Option | Building Stock | Renovation Option | |||

| 2012 | Moderate | Deep | 2012 | Moderate | Deep | |

| [kWh/m2] | [kWh/m2] | [kWh/m2] | [kWh/m2] | [kWh/m2] | [kWh/m2] | |

| Space heating | 47 | 17 | 15 | 70 | 26 | 21 |

| Domestic hot water | 20 | 10 | 9 | 37 | 18 | 13 |

| Space cooling | 67 | 38 | 34 | 166 | 60 | 46 |

| Lighting | 8 | 6 | 6 | 56 | 37 | 28 |

| Total | 142 | 71 | 64 | 329 | 141 | 108 |

| Policy Elements | Policy 1 | Policy 2 | Policy 3 | Policy 4 | Policy 5 |

|---|---|---|---|---|---|

| Building vintage | Existing | Existing | New & existing | New & existing | - |

| Policy type | Investment grants for energy efficiency | Investment grants for energy efficiency | Minimum energy performance requirements | Minimum energy performance requirements | Energy performance certificates |

| Period | 2014–2020 | 2014–2020 | 2013–2020 | 2021–2050 | 2010–2050 |

| Building type | All | Residential | All | All | All |

| Energy or renovation level | Moderate & deep | Moderate | EPC class B | Nearly zero energy | - |

| Occupant profile | All | Low income | All | All | All |

| Public annual budget | 2.5 Million € | 0.5 Million € | - | - | - |

| Investment coverage | 25% | 25% | - | - | - |

| Policy Elements | Policy 1+ | Policy 2+ | Policy 6 | Policy 7 | Policy 8 | Policy 9 |

|---|---|---|---|---|---|---|

| Building vintage | Existing * | Existing * | Existing buildings | All | All | All |

| Policy type | Investment grants for energy efficiency * | Investment grants for energy efficiency * | Credit line for energy efficiency | Roll out of inform. campaigns | Inform. centres for energy renovation | Workforce education |

| Period | 2014–2020 * | 2014–2020 * | 2018–2028 | 2018–2050 | 2020–2050 | 2014–2050 |

| Building type | All * | Residential * | All | All | All | All |

| Energy or renov. level | Moderate & deep * | Moderate * | Moderate & deep | - | - | - |

| Occupant profile | All * | Low income * | Building owners | All | All | - |

| Public annual budget | 10 mill € | 2.5 mill € | 5 mill € | 0.1 mill € | 0.5 mill € | 0.25 mill € |

| Bank annual budget | - * | - * | 20 mill € | - | - | - |

| Invest. coverage | 25% * | 25% * | 50% | - | - | - |

| Repay. period | - * | - * | 15 years | - | - | - |

| Policy Elements | Policy 1+ | Policy 2+ | Policy 6+ | Policy 10 | Policy 11 | Policy 12 | Policy 13 |

|---|---|---|---|---|---|---|---|

| Building vintage | Existing * | Existing * | Existing * | Existing | Existing | Existing | New |

| Policy type | Invest. grants energy eff. * | Invest. grants energy eff. * | Credit line for energy efficiency * | Tax income credit for landlords | Min. energy perf. require-ments for rentals | VAT reduction for energy efficiency interventions | Grants for zero energy buildings |

| Period | 2014–2020 * | 2014–2020 * | 2018–2028 * | 2018–2025 | 2025–2050 | 2020–2050 | 2020–2022 |

| Building type | All * | Res. * | All * | All | All | Res. | All |

| Energy or renov. level | Moderate & deep * | Shall. * | Moderate & deep * | Moderate | Moderate & deep | Moderate & deep | Zero Energy |

| Occ. profile | All * | Low income * | Building owners * | Land-lords | Land-lords | All | All |

| Public annual budget | 12 mill € | 5 mill € | 7.5 mill € | 2.5 mill € | - | - | 2.5 mill € |

| Bank annual budget | - * | - * | 25 mill € | - | - | - | - |

| Invest. cov. | 25% * | 25% * | 75% | 50% | - | - | 25% |

| Repay. period | - * | - * | 15 years * | 10 years | - | - | - |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Economidou, M.; Zangheri, P.; Müller, A.; Kranzl, L. Financing the Renovation of the Cypriot Building Stock: An Assessment of the Energy Saving Potential of Different Policy Scenarios Based on the Invert/EE-Lab Model. Energies 2018, 11, 3071. https://doi.org/10.3390/en11113071

Economidou M, Zangheri P, Müller A, Kranzl L. Financing the Renovation of the Cypriot Building Stock: An Assessment of the Energy Saving Potential of Different Policy Scenarios Based on the Invert/EE-Lab Model. Energies. 2018; 11(11):3071. https://doi.org/10.3390/en11113071

Chicago/Turabian StyleEconomidou, Marina, Paolo Zangheri, Andreas Müller, and Lukas Kranzl. 2018. "Financing the Renovation of the Cypriot Building Stock: An Assessment of the Energy Saving Potential of Different Policy Scenarios Based on the Invert/EE-Lab Model" Energies 11, no. 11: 3071. https://doi.org/10.3390/en11113071